Financial Analysis and Valuation of Texas Roadhouse Inc. Shares

VerifiedAdded on 2023/04/23

|6

|1248

|457

Case Study

AI Summary

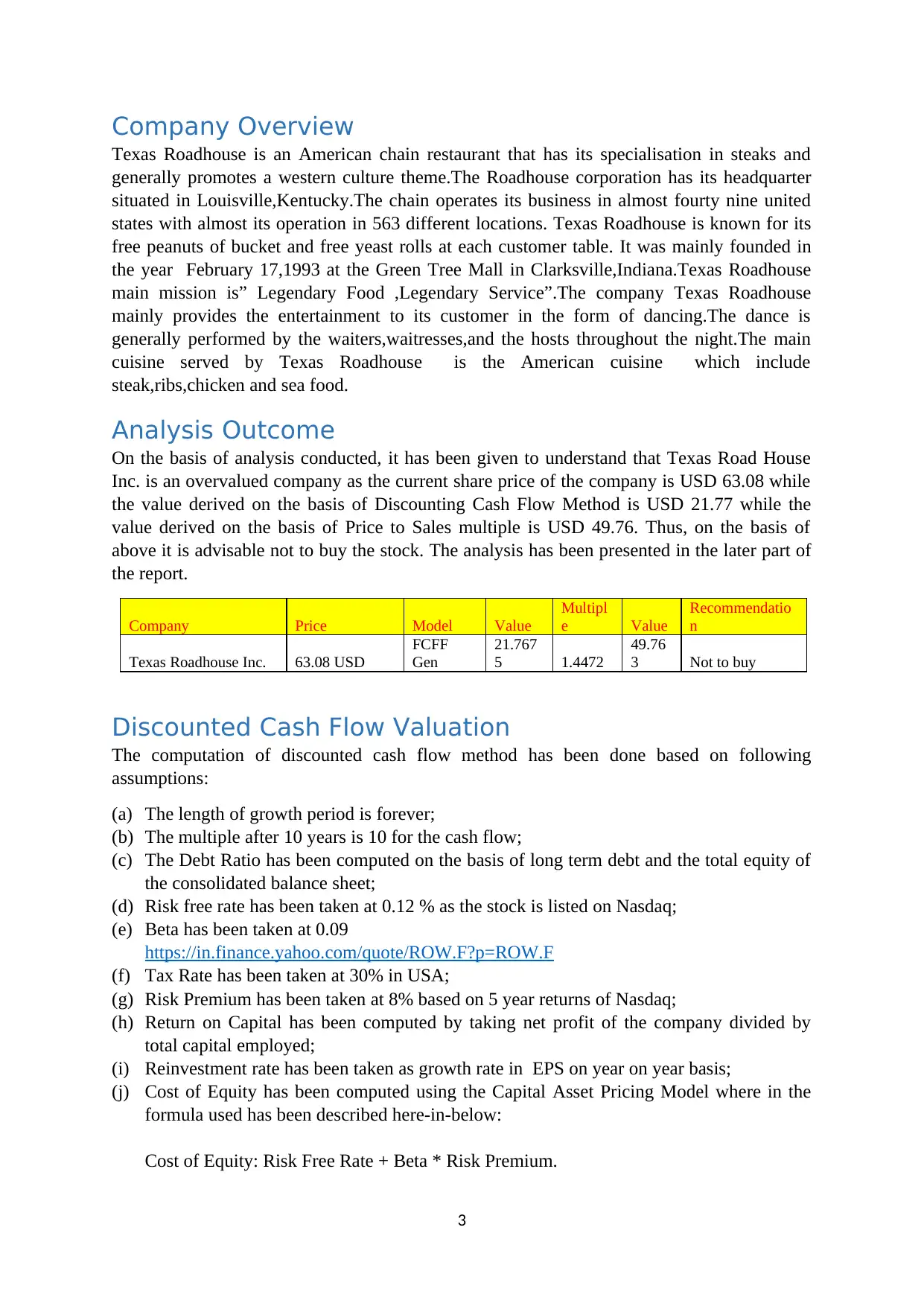

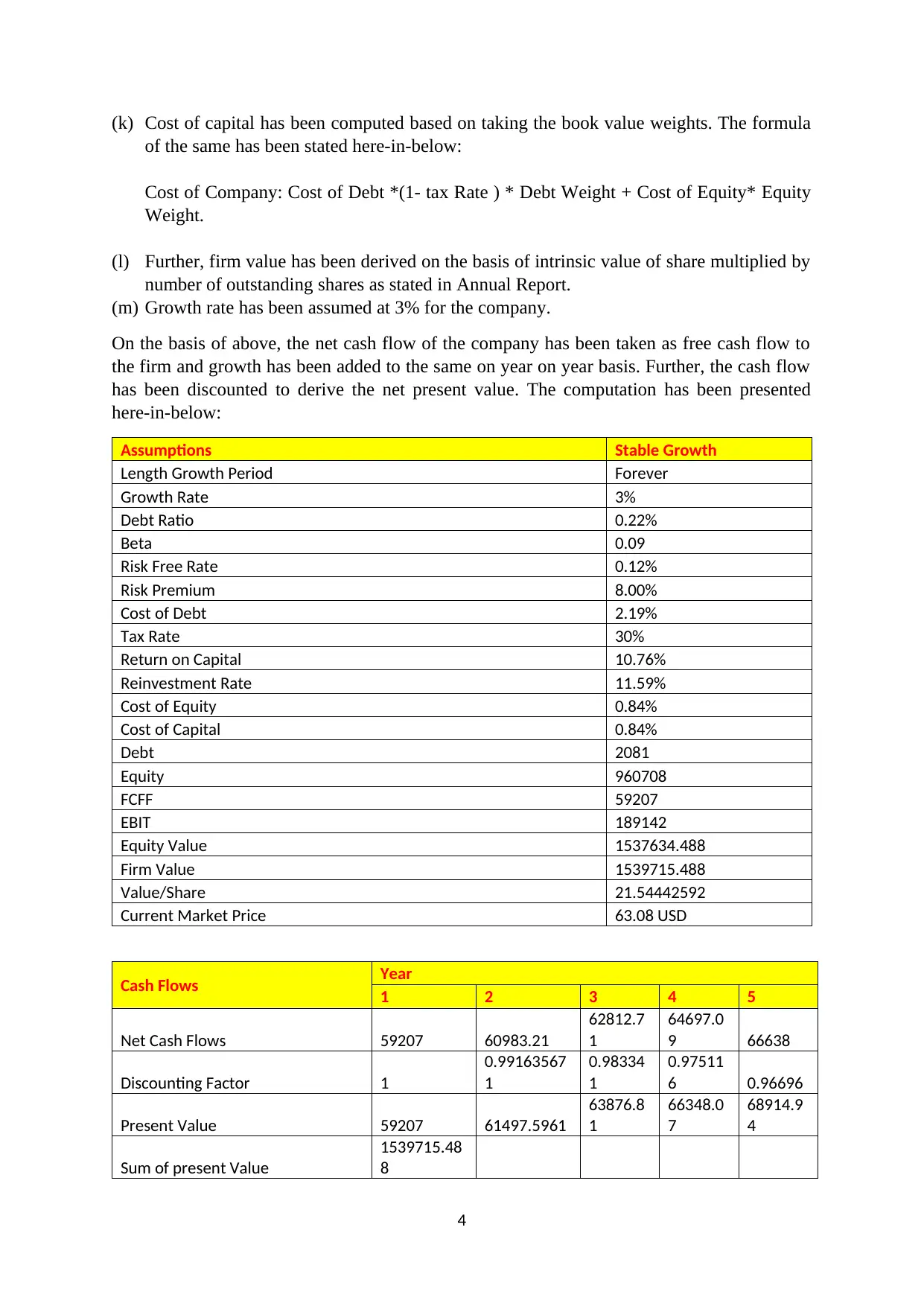

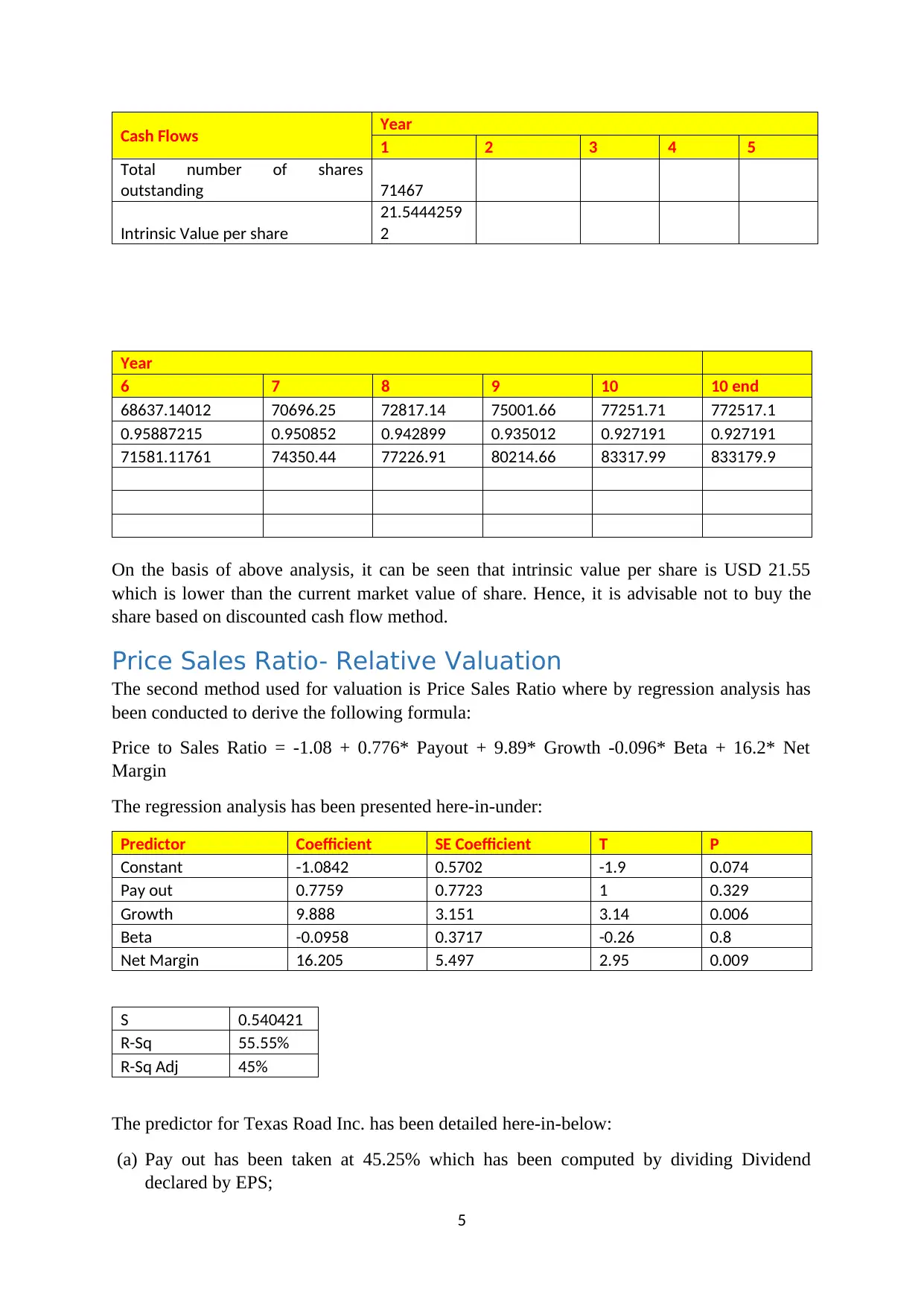

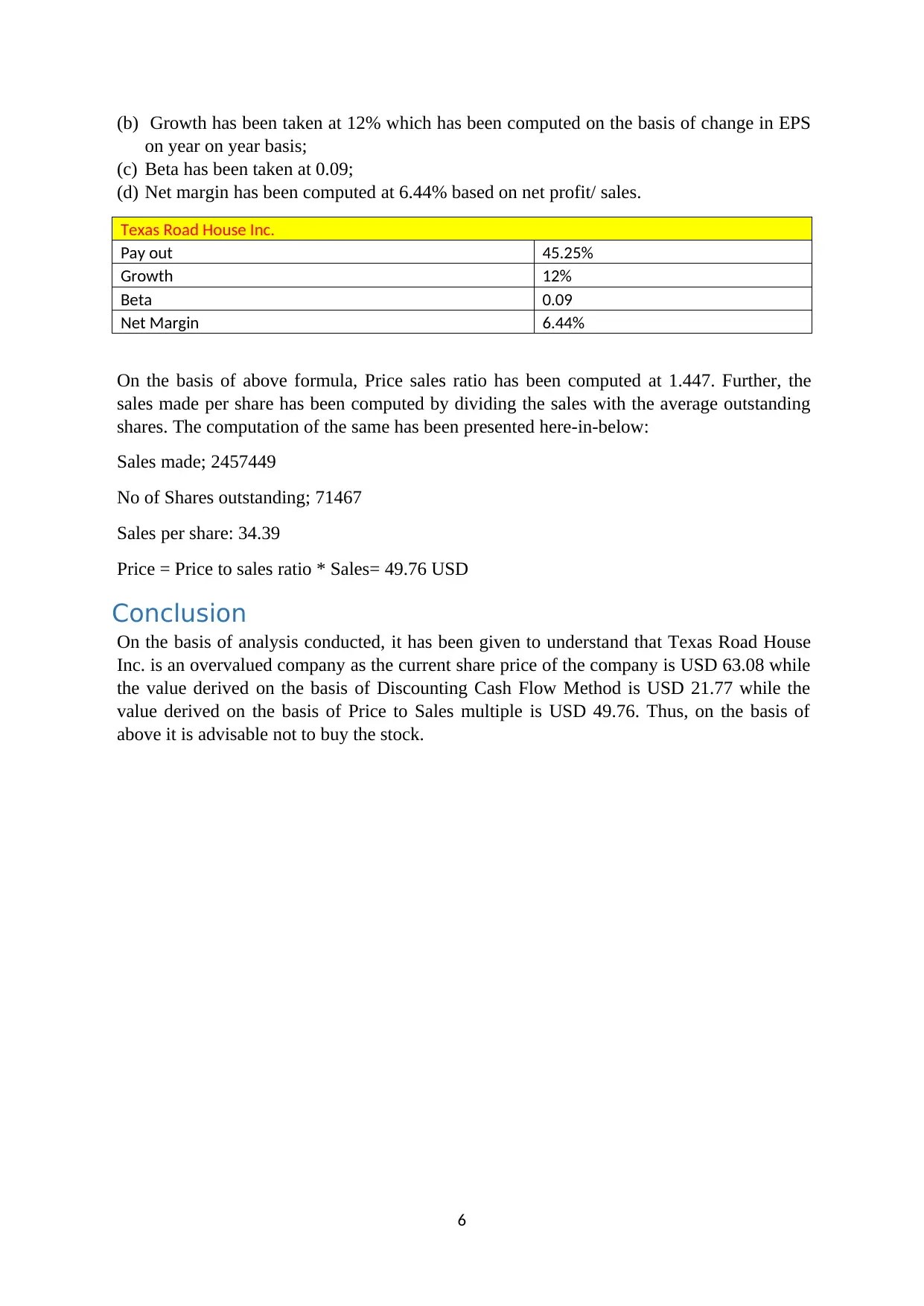

This case study provides a comprehensive business valuation and financial analysis of Texas Roadhouse Inc., utilizing both Discounted Cash Flow (DCF) and Price to Sales Ratio (PSR) methods. The analysis reveals that the company's stock may be overvalued, with the DCF method suggesting a value of USD 21.77 per share compared to the current market price of USD 63.08, and the PSR method indicating a value of USD 49.76. The DCF valuation incorporates assumptions such as a stable growth period, a terminal multiple of 10, and a 3% growth rate. The PSR valuation employs a regression analysis formula incorporating payout, growth, beta, and net margin. Based on these valuations, the recommendation is not to buy Texas Roadhouse Inc. stock. Desklib provides access to similar solved assignments and resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.