University Financial Analysis and Audit Risk Report for TFW (3102AFE)

VerifiedAdded on 2023/04/21

|11

|2381

|105

Report

AI Summary

This report presents a financial analysis of Top Fashion Warehouse Ltd (TFW), conducted through ratio analysis, examining liquidity, activity, profitability, and solvency. The analysis identifies inherent risks like changes in cash and inventory, as well as macroeconomic and business factor risks. Four key accounts are scrutinized: liquidity position, debt and asset position, inventory turnover, and inventory level, highlighting associated risks. The report also assesses key assertions related to cash, plant and machinery, interest-bearing liabilities, and inventory, emphasizing potential misstatements and the need for auditor verification. The conclusion summarizes the findings, emphasizing the identified risks and the importance of careful financial scrutiny. The assignment was based on the 3102AFE Client Analysis Case Study Trimester 3, 2018 assignment brief, and the student has provided a comprehensive analysis of the company's financial health.

Running head: AUDITING

Auditing

Name of the Student:

Name of the university:

Author’s Note:

Auditing

Name of the Student:

Name of the university:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Executive Summary

The aim of the assignment is to conduct a financial analysis on the Top Fashion Warehouse Ltd

Company and the same was done with the help of ratio analysis for the company. There were

several factors and important points considered for examining and evaluating the inherent risks

of the company. There were several accounts recognized for the company, which was having a

material impact on the balance sheet of the company, and the same was analysed for the

company.

Executive Summary

The aim of the assignment is to conduct a financial analysis on the Top Fashion Warehouse Ltd

Company and the same was done with the help of ratio analysis for the company. There were

several factors and important points considered for examining and evaluating the inherent risks

of the company. There were several accounts recognized for the company, which was having a

material impact on the balance sheet of the company, and the same was analysed for the

company.

2AUDITING

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Ratio Analysis..............................................................................................................................3

Inherent Risk................................................................................................................................3

Four Key Accounts......................................................................................................................4

Key Assertions.............................................................................................................................5

Conclusion.......................................................................................................................................7

Reference.........................................................................................................................................8

Appendix........................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Ratio Analysis..............................................................................................................................3

Inherent Risk................................................................................................................................3

Four Key Accounts......................................................................................................................4

Key Assertions.............................................................................................................................5

Conclusion.......................................................................................................................................7

Reference.........................................................................................................................................8

Appendix........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Introduction

The analysis of the Top Fashion Warehouse was conducted by analysing the company

and taking various accounts and factors into consideration for the company. The ratio analysis

for the company was evaluated by incorporating the various liquidity ratio, activity ratio,

profitability ratio and solvency ratio of the company. The inherent risk of the company are the

several factor that affects the company were analysed for the company and taken into

consideration. There were several account evaluated and identified for the company which were

having a material impact on the financials of the company.

Discussion

Ratio Analysis

The financial analysis of the Top Fashion Warehouse Ltd was evaluated with the help of

the ratio analysis for the company. The ratio analysis for the company was evaluated based on

the several ratio, which helped us examine and analyse the performance of the company. The

liquidity ratio, activity ratio, profitability ratio and the solvency ratio were some of the key ratio

evaluated for the company (Bhattacharjee, Maletta & Moreno 2015).

Inherent Risk

The inherent risk factor that arise from the nature of material misstatement of financial

statement of a company, or due to error, and omissions of the various factors and accounts. The

Top Fashion Warehouse Ltd and the business operations of the company were evaluated in order

to identify any inherent risk factor in the same

(BOTEZ, 2015). The two key inherent risk factor analysed for the company were the changes

observed in the cash and cash equivalents and the inventory of the company. The cash and cash

Introduction

The analysis of the Top Fashion Warehouse was conducted by analysing the company

and taking various accounts and factors into consideration for the company. The ratio analysis

for the company was evaluated by incorporating the various liquidity ratio, activity ratio,

profitability ratio and solvency ratio of the company. The inherent risk of the company are the

several factor that affects the company were analysed for the company and taken into

consideration. There were several account evaluated and identified for the company which were

having a material impact on the financials of the company.

Discussion

Ratio Analysis

The financial analysis of the Top Fashion Warehouse Ltd was evaluated with the help of

the ratio analysis for the company. The ratio analysis for the company was evaluated based on

the several ratio, which helped us examine and analyse the performance of the company. The

liquidity ratio, activity ratio, profitability ratio and the solvency ratio were some of the key ratio

evaluated for the company (Bhattacharjee, Maletta & Moreno 2015).

Inherent Risk

The inherent risk factor that arise from the nature of material misstatement of financial

statement of a company, or due to error, and omissions of the various factors and accounts. The

Top Fashion Warehouse Ltd and the business operations of the company were evaluated in order

to identify any inherent risk factor in the same

(BOTEZ, 2015). The two key inherent risk factor analysed for the company were the changes

observed in the cash and cash equivalents and the inventory of the company. The cash and cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

equivalent is the major and crucial current assets for the company helping the company in

maintaining the operations of the company run smooth. The time taken by the company for

producing the goods and completing the process of sales is quite longer, which takes around 46

weeks of time for completing the order and the same should be undertaken for the analysis of the

Top Fashion Warehouse Ltd (Hines et al. 2015). The risks are specific with the Top Fashion

Warehouse as the same will hamper the business operations of the company and the company

might not able to meet the short term goals and objectives of the company. The increase in the

inventory of the company might also signal that the company is not able to sell the products of

the company and the risk of obsolesce inventory for the company may rise. The key inherent risk

associated with the business operations of the company are the macroeconomic risk like the rise

in the inflation rate and interest rate scenario for the company and the business factor risk such as

counterparty default risk and the rising inventory of the company were some of the key factors

addressed (Beck, Glendening & Hogan 2016).

Four Key Accounts

The four key accounts that are at risk and the same explains significant risk and the same

has been identified when material changes has been observed in these accounts and the

difference between these accounts have been examined.

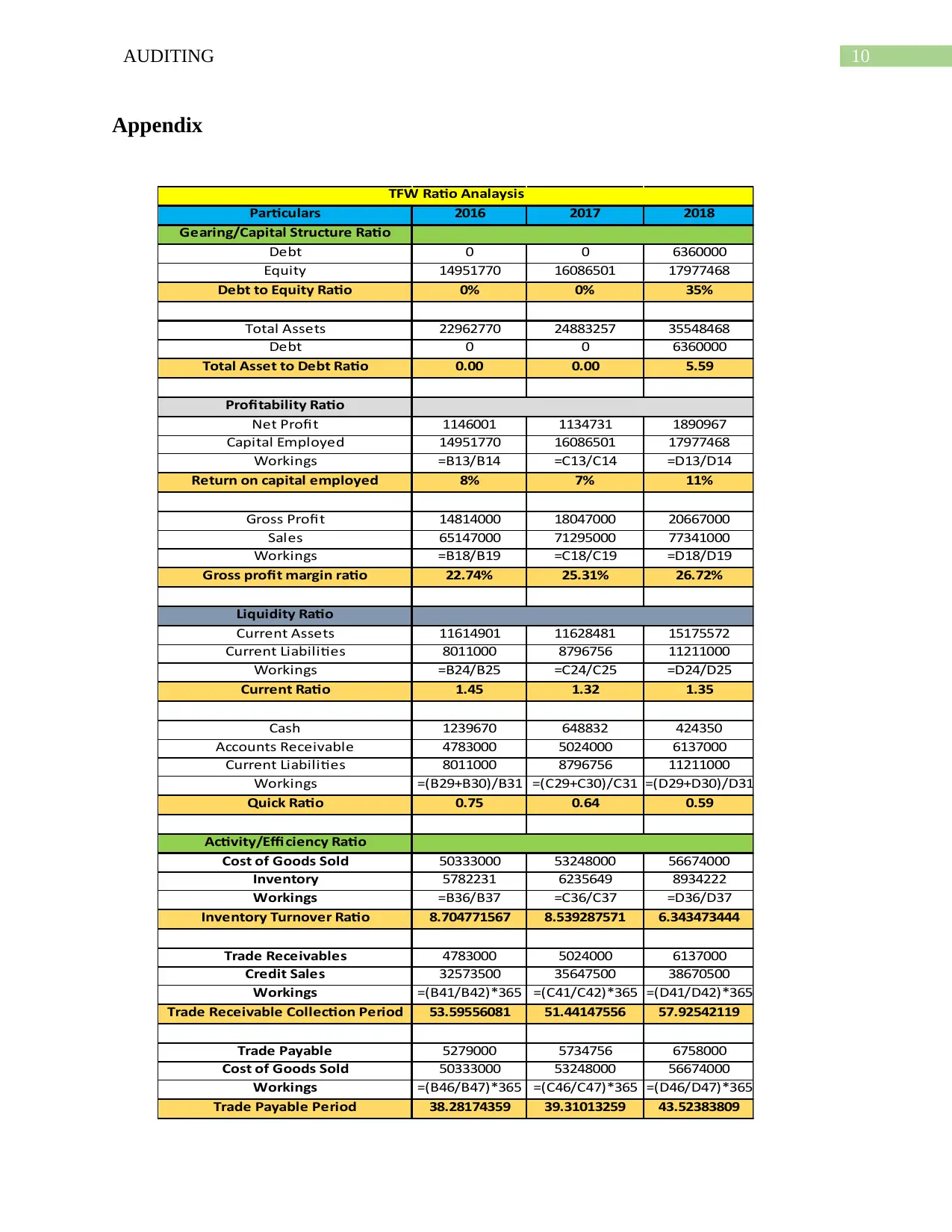

Liquidity Position: The liquidity ratio for the Top Fashion Warehouse Ltd has decreased from

the trend period 2016 to 2018 where the cash balance for the company has consistently decreased

and the inventory of the company rose in the trend period analyzed for the company

(Fredriksson, Kiran & Niemi 2018). The liquidity position of the company has worsened in the

trend period and the level of the cash and cash equivalents, which is a key part of the current

assets of the company, has decreased consistently which may influence the operations of the

equivalent is the major and crucial current assets for the company helping the company in

maintaining the operations of the company run smooth. The time taken by the company for

producing the goods and completing the process of sales is quite longer, which takes around 46

weeks of time for completing the order and the same should be undertaken for the analysis of the

Top Fashion Warehouse Ltd (Hines et al. 2015). The risks are specific with the Top Fashion

Warehouse as the same will hamper the business operations of the company and the company

might not able to meet the short term goals and objectives of the company. The increase in the

inventory of the company might also signal that the company is not able to sell the products of

the company and the risk of obsolesce inventory for the company may rise. The key inherent risk

associated with the business operations of the company are the macroeconomic risk like the rise

in the inflation rate and interest rate scenario for the company and the business factor risk such as

counterparty default risk and the rising inventory of the company were some of the key factors

addressed (Beck, Glendening & Hogan 2016).

Four Key Accounts

The four key accounts that are at risk and the same explains significant risk and the same

has been identified when material changes has been observed in these accounts and the

difference between these accounts have been examined.

Liquidity Position: The liquidity ratio for the Top Fashion Warehouse Ltd has decreased from

the trend period 2016 to 2018 where the cash balance for the company has consistently decreased

and the inventory of the company rose in the trend period analyzed for the company

(Fredriksson, Kiran & Niemi 2018). The liquidity position of the company has worsened in the

trend period and the level of the cash and cash equivalents, which is a key part of the current

assets of the company, has decreased consistently which may influence the operations of the

5AUDITING

company. The increase in inventory and account receivable, which are not readily in the liquid

form of an asset is a key risk identified in this area for the operations of the company.

Debt and Asset Position: The debt to total assets ratio for the company rose in the year 2018

when the company took significant amount of debt in the company for the operations of the

company. The debt of the company has significantly increased for the company reflecting the

financial risk of the company has increased and the same would increase significant influence on

the profitability of the company. The company should maintain an optimal balance between the

debt and equity level so that the business operations of the company runs smooth for the

company.

Inventory Turnover: The inventory turnover for the company in correspondence to the sales of

the company has consistently increased for the company reflecting that the company might not

be able to do the sales of the company. The inventory turnover has consistently fallen for the

company in the trend period analyzed for the company reflecting that the company might suffers

risk of obsolesce with high value of inventory into accounts for the company.

Inventory Level: The inventory level for the company has consistently increased for the

company reflecting that the company might not able to sell the produced goods of the company

and the risk of obsolesce may increase for the company. The rising inventory level for the

company needs to be dealt with the company with specific strategies and ideas so that the

management of the company can reduce the risk associated with the same.

Key Assertions

The key accounts, which faces the most risks as identified in the above paragraph, are

cash, plant and machinery, interest bearing liabilities and inventory. The cash balance of the

company. The increase in inventory and account receivable, which are not readily in the liquid

form of an asset is a key risk identified in this area for the operations of the company.

Debt and Asset Position: The debt to total assets ratio for the company rose in the year 2018

when the company took significant amount of debt in the company for the operations of the

company. The debt of the company has significantly increased for the company reflecting the

financial risk of the company has increased and the same would increase significant influence on

the profitability of the company. The company should maintain an optimal balance between the

debt and equity level so that the business operations of the company runs smooth for the

company.

Inventory Turnover: The inventory turnover for the company in correspondence to the sales of

the company has consistently increased for the company reflecting that the company might not

be able to do the sales of the company. The inventory turnover has consistently fallen for the

company in the trend period analyzed for the company reflecting that the company might suffers

risk of obsolesce with high value of inventory into accounts for the company.

Inventory Level: The inventory level for the company has consistently increased for the

company reflecting that the company might not able to sell the produced goods of the company

and the risk of obsolesce may increase for the company. The rising inventory level for the

company needs to be dealt with the company with specific strategies and ideas so that the

management of the company can reduce the risk associated with the same.

Key Assertions

The key accounts, which faces the most risks as identified in the above paragraph, are

cash, plant and machinery, interest bearing liabilities and inventory. The cash balance of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

business is shown to be on continuous fall which has a significant risk on the liquidity aspect of

the business (Shin, Lee & Park, 2013). The fall in the cash balance is enormous and the liquidity

of the business is at stake as with the falling cash balance, concern would be arise, how the

management of the company would be financing new projects and meeting the day to day

expenses of the business (Louwers et al., 2015). The auditor of the business needs to apply

vouching practices on the cash balances of the business in order to ensure that the balances are

showing true and fair view or whether some cash has been misappropriated by the management.

The property, plant and equipment account balances are shown to have increased during

2017 and again there is a significant increase in the balance of property, plant and equipment in

2018. There is a significant risk that the value of the net fixed asset has been misappropriated in

order to make the balance sheet of the business look good and improve the financial position of

the business (Abdullatif & Kawuq, 2015). The auditor of the business needs to verify the

balances of property, plant and equipment in order to ensure that the same are showing true and

fair view and in addition to this, the auditor also needs to physically verify the assets as there is a

significant risk that the asset may not exist in real.

The interest-bearing liabilities show slight decrease which suggest that the management

of the company has repaid a portion of the accumulated debts of the business but there can also

be a situation where debts are shown lower in order to show low amount for liabilities and

thereby show favorable financial position of the business (Stojanović & Andrić, 2016). The debt

balance itself represent risks and therefore, the management of the company might be lowering

the debts in order to show the investors that the debts are being lowered to reduce the overall

risks which is associated with the debt balance of the business.

business is shown to be on continuous fall which has a significant risk on the liquidity aspect of

the business (Shin, Lee & Park, 2013). The fall in the cash balance is enormous and the liquidity

of the business is at stake as with the falling cash balance, concern would be arise, how the

management of the company would be financing new projects and meeting the day to day

expenses of the business (Louwers et al., 2015). The auditor of the business needs to apply

vouching practices on the cash balances of the business in order to ensure that the balances are

showing true and fair view or whether some cash has been misappropriated by the management.

The property, plant and equipment account balances are shown to have increased during

2017 and again there is a significant increase in the balance of property, plant and equipment in

2018. There is a significant risk that the value of the net fixed asset has been misappropriated in

order to make the balance sheet of the business look good and improve the financial position of

the business (Abdullatif & Kawuq, 2015). The auditor of the business needs to verify the

balances of property, plant and equipment in order to ensure that the same are showing true and

fair view and in addition to this, the auditor also needs to physically verify the assets as there is a

significant risk that the asset may not exist in real.

The interest-bearing liabilities show slight decrease which suggest that the management

of the company has repaid a portion of the accumulated debts of the business but there can also

be a situation where debts are shown lower in order to show low amount for liabilities and

thereby show favorable financial position of the business (Stojanović & Andrić, 2016). The debt

balance itself represent risks and therefore, the management of the company might be lowering

the debts in order to show the investors that the debts are being lowered to reduce the overall

risks which is associated with the debt balance of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

The inventory balance is also considered to be at risk as in most of the businesses

misstatements and omissions are detected in the inventory balances (Mohammadi, Kalali &

Najafzadeh, 2014). As per the estimates which is available for 2018, the balance of inventory has

increased significantly in comparison to previous years which needs to be considered by the

auditor (Abdallah, Mssadeh & Othman, 2015). The auditor needs to evaluate the internal control

and thereby analyze the inventory management and recording process in order to ensure that no

manipulation is done in this respect. The auditor can even conduct a physical check for the

stocks in order to establish that the value which is shown in the financial statement are showing

true and fair view or not.

Conclusion

The financial analysis of the company was evaluated with the help of ratio analysis and various

other elements, which are evaluated for identifying the risk, associated with several accounts of

Top Fashion Warehouse Limited. There were several account evaluated and identified for the

company which were having a material affect the financials of the company. The key accounts,

which faces the most risks as identified in the above paragraph, are cash, plant and machinery,

interest bearing liabilities and inventory.

The inventory balance is also considered to be at risk as in most of the businesses

misstatements and omissions are detected in the inventory balances (Mohammadi, Kalali &

Najafzadeh, 2014). As per the estimates which is available for 2018, the balance of inventory has

increased significantly in comparison to previous years which needs to be considered by the

auditor (Abdallah, Mssadeh & Othman, 2015). The auditor needs to evaluate the internal control

and thereby analyze the inventory management and recording process in order to ensure that no

manipulation is done in this respect. The auditor can even conduct a physical check for the

stocks in order to establish that the value which is shown in the financial statement are showing

true and fair view or not.

Conclusion

The financial analysis of the company was evaluated with the help of ratio analysis and various

other elements, which are evaluated for identifying the risk, associated with several accounts of

Top Fashion Warehouse Limited. There were several account evaluated and identified for the

company which were having a material affect the financials of the company. The key accounts,

which faces the most risks as identified in the above paragraph, are cash, plant and machinery,

interest bearing liabilities and inventory.

8AUDITING

Reference

Abdallah, A. A. J., Mssadeh, A. A. D., & Othman, O. H. (2015). Measuring the Impact of

Business Risks on the Quality of the Auditing Process. Review of Integrative Business

and Economics Research, 4(2), 171.

Abdullatif, M., & Kawuq, S. (2015). The role of internal auditing in risk management: evidence

from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1), 30-50.

Beck, M. J., Glendening, M., & Hogan, C. E. (2016). Financial Statement Disaggregation,

Auditor Effort and Financial Reporting Quality. working paper, Michigan State

University.

Bhattacharjee, S., Maletta, M. J., & Moreno, K. K. (2015). The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), 225-238.

BOTEZ, D. (2015). Study Regarding the Need to Develop an Audit Risk Model. Audit financiar,

13(125).

Fredriksson, A., Kiran, A., & Niemi, L. (2018). Reputation Capital of Directorships and Audit

Quality.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Reference

Abdallah, A. A. J., Mssadeh, A. A. D., & Othman, O. H. (2015). Measuring the Impact of

Business Risks on the Quality of the Auditing Process. Review of Integrative Business

and Economics Research, 4(2), 171.

Abdullatif, M., & Kawuq, S. (2015). The role of internal auditing in risk management: evidence

from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1), 30-50.

Beck, M. J., Glendening, M., & Hogan, C. E. (2016). Financial Statement Disaggregation,

Auditor Effort and Financial Reporting Quality. working paper, Michigan State

University.

Bhattacharjee, S., Maletta, M. J., & Moreno, K. K. (2015). The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), 225-238.

BOTEZ, D. (2015). Study Regarding the Need to Develop an Audit Risk Model. Audit financiar,

13(125).

Fredriksson, A., Kiran, A., & Niemi, L. (2018). Reputation Capital of Directorships and Audit

Quality.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

Mohammadi, J., Kalali, A., & Najafzadeh, A. (2014). Risk-Based Auditing. Asian Journal of

Research in Business Economics and Management, 4(11), 366-372.

Shin, I. H., Lee, M. G., & Park, W. (2013). Implementation of the continuous auditing system in

the ERP-based environment. Managerial Auditing Journal, 28(7), 592-627.

Stojanović, T., & Andrić, M. (2016). Internal Auditing and Risk Management in

Corporations. Thematic Fields, 31.

Mohammadi, J., Kalali, A., & Najafzadeh, A. (2014). Risk-Based Auditing. Asian Journal of

Research in Business Economics and Management, 4(11), 366-372.

Shin, I. H., Lee, M. G., & Park, W. (2013). Implementation of the continuous auditing system in

the ERP-based environment. Managerial Auditing Journal, 28(7), 592-627.

Stojanović, T., & Andrić, M. (2016). Internal Auditing and Risk Management in

Corporations. Thematic Fields, 31.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

Appendix

Particulars 2016 2017 2018

Gearing/Capital Structure Ratio

Debt 0 0 6360000

Equity 14951770 16086501 17977468

Debt to Equity Ratio 0% 0% 35%

Total Assets 22962770 24883257 35548468

Debt 0 0 6360000

Total Asset to Debt Ratio 0.00 0.00 5.59

Profitability Ratio

Net Profit 1146001 1134731 1890967

Capital Employed 14951770 16086501 17977468

Workings =B13/B14 =C13/C14 =D13/D14

Return on capital employed 8% 7% 11%

Gross Profit 14814000 18047000 20667000

Sales 65147000 71295000 77341000

Workings =B18/B19 =C18/C19 =D18/D19

Gross profit margin ratio 22.74% 25.31% 26.72%

Liquidity Ratio

Current Assets 11614901 11628481 15175572

Current Liabilities 8011000 8796756 11211000

Workings =B24/B25 =C24/C25 =D24/D25

Current Ratio 1.45 1.32 1.35

Cash 1239670 648832 424350

Accounts Receivable 4783000 5024000 6137000

Current Liabilities 8011000 8796756 11211000

Workings =(B29+B30)/B31 =(C29+C30)/C31 =(D29+D30)/D31

Quick Ratio 0.75 0.64 0.59

Activity/Efficiency Ratio

Cost of Goods Sold 50333000 53248000 56674000

Inventory 5782231 6235649 8934222

Workings =B36/B37 =C36/C37 =D36/D37

Inventory Turnover Ratio 8.704771567 8.539287571 6.343473444

Trade Receivables 4783000 5024000 6137000

Credit Sales 32573500 35647500 38670500

Workings =(B41/B42)*365 =(C41/C42)*365 =(D41/D42)*365

Trade Receivable Collection Period 53.59556081 51.44147556 57.92542119

Trade Payable 5279000 5734756 6758000

Cost of Goods Sold 50333000 53248000 56674000

Workings =(B46/B47)*365 =(C46/C47)*365 =(D46/D47)*365

Trade Payable Period 38.28174359 39.31013259 43.52383809

TFW Ratio Analaysis

Appendix

Particulars 2016 2017 2018

Gearing/Capital Structure Ratio

Debt 0 0 6360000

Equity 14951770 16086501 17977468

Debt to Equity Ratio 0% 0% 35%

Total Assets 22962770 24883257 35548468

Debt 0 0 6360000

Total Asset to Debt Ratio 0.00 0.00 5.59

Profitability Ratio

Net Profit 1146001 1134731 1890967

Capital Employed 14951770 16086501 17977468

Workings =B13/B14 =C13/C14 =D13/D14

Return on capital employed 8% 7% 11%

Gross Profit 14814000 18047000 20667000

Sales 65147000 71295000 77341000

Workings =B18/B19 =C18/C19 =D18/D19

Gross profit margin ratio 22.74% 25.31% 26.72%

Liquidity Ratio

Current Assets 11614901 11628481 15175572

Current Liabilities 8011000 8796756 11211000

Workings =B24/B25 =C24/C25 =D24/D25

Current Ratio 1.45 1.32 1.35

Cash 1239670 648832 424350

Accounts Receivable 4783000 5024000 6137000

Current Liabilities 8011000 8796756 11211000

Workings =(B29+B30)/B31 =(C29+C30)/C31 =(D29+D30)/D31

Quick Ratio 0.75 0.64 0.59

Activity/Efficiency Ratio

Cost of Goods Sold 50333000 53248000 56674000

Inventory 5782231 6235649 8934222

Workings =B36/B37 =C36/C37 =D36/D37

Inventory Turnover Ratio 8.704771567 8.539287571 6.343473444

Trade Receivables 4783000 5024000 6137000

Credit Sales 32573500 35647500 38670500

Workings =(B41/B42)*365 =(C41/C42)*365 =(D41/D42)*365

Trade Receivable Collection Period 53.59556081 51.44147556 57.92542119

Trade Payable 5279000 5734756 6758000

Cost of Goods Sold 50333000 53248000 56674000

Workings =(B46/B47)*365 =(C46/C47)*365 =(D46/D47)*365

Trade Payable Period 38.28174359 39.31013259 43.52383809

TFW Ratio Analaysis

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.