Winter 2020: Thomson Reuters Annual Report Analysis, ACCT 3410

VerifiedAdded on 2022/08/21

|16

|3377

|11

Report

AI Summary

This report provides a detailed analysis of Thomson Reuters' financial performance for the year ending December 31, 2018. It begins with an executive summary, covering the company's history, market position, competitors, and key personnel. The report then identifies and discusses the major components of the annual report, emphasizing their significance to investors. A comprehensive ratio analysis is performed, evaluating profitability, liquidity, and efficiency trends over multiple years and comparing them to industry averages. The analysis includes discussion of the company's risk management strategies, accounting policies, and the impact of Canadian accounting standards. Furthermore, it addresses the application of IAS 10 (Events After the Reporting Period) and their influence on the company's financial outlook. The report concludes with an assessment of the organization's future financial performance, incorporating all the analytical findings and considering the impacts of any relevant current events.

Running head: Intermediate Accounting

Intermediate Accounting

Name of the Student

Name of the University

Author Note

Intermediate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Intermediate Accounting

Executive summary

Thomson Reuters was founded in Toronto, Ontario, Canada by Roy Thomson in 1934. It is

one of the world’s largest provider related to news and other information based tools to

experts and professionals. Headquarter of Thomson Reuters is situated in Toronto, Canada.

Creating a particular focus on regulations and tax changes they aim to hold customers along

with speed on developments at a global basis by having worldwide network of journalists and

specialist editors. The shares of “Thomson Reuters” are listed on the “Toronto and New York

Stock Exchanges.” There are some of the competitors of Thomson Reuters which hold a

strong position such as S&P Global Market Intelligence, Bloomberg, Market Watch, Fact Set,

Dun & Bradstreet. Steve Hasker is the current President and Chief Executive Officer and a

director of Thomson Reuters.

Intermediate Accounting

Executive summary

Thomson Reuters was founded in Toronto, Ontario, Canada by Roy Thomson in 1934. It is

one of the world’s largest provider related to news and other information based tools to

experts and professionals. Headquarter of Thomson Reuters is situated in Toronto, Canada.

Creating a particular focus on regulations and tax changes they aim to hold customers along

with speed on developments at a global basis by having worldwide network of journalists and

specialist editors. The shares of “Thomson Reuters” are listed on the “Toronto and New York

Stock Exchanges.” There are some of the competitors of Thomson Reuters which hold a

strong position such as S&P Global Market Intelligence, Bloomberg, Market Watch, Fact Set,

Dun & Bradstreet. Steve Hasker is the current President and Chief Executive Officer and a

director of Thomson Reuters.

2

Intermediate Accounting

Table of Contents

Major Components of Annual Report........................................................................................3

Ratio analysis.............................................................................................................................4

Risk management strategy of Thomson Reuters........................................................................7

Accounting policy and its impact...............................................................................................8

Impact of the application of the Canadian accounting standards.............................................10

‘Events after the Reporting Period’ (IAS 10)..........................................................................10

Impact of the Organization and future financial performance.................................................12

References................................................................................................................................13

Intermediate Accounting

Table of Contents

Major Components of Annual Report........................................................................................3

Ratio analysis.............................................................................................................................4

Risk management strategy of Thomson Reuters........................................................................7

Accounting policy and its impact...............................................................................................8

Impact of the application of the Canadian accounting standards.............................................10

‘Events after the Reporting Period’ (IAS 10)..........................................................................10

Impact of the Organization and future financial performance.................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Intermediate Accounting

Major Components of Annual Report

An annual report is a complete report of a company which establishes its financial

health on presenting information on every financial year. It also focuses on presenting history

of the company along with its achievements and recognitions made in the past. It helps the

shareholders, investors, stakeholders, government, and media by giving accurate information

and all those details from the annual report helps the potential users in their decisions making

(Symes, Sharma & Davey, 2017). The major components of the annual report are as

following:

1. Letter from the Chairman- The performance of the company during a particular year

is mentioned here.

2. Director’s report- Crucial events happened during a particular year in a company are

included in this (Shaw et al., 2017).

3. Auditor’s report- An auditor conducts the audit on the accounts and presents the

report to the shareholders of the company.

4. Balance Sheet- Financial position is presented stating what the company is having and

what the obligations are.

5. Profit and loss Account- Net profit of a company that is earned during the current

financial year.

6. Cash flow Statement- How much cash is earned by the company and are used during

a particular period is stated here.

7. Schedules- Operational performance of a company during the reporting period are

included in this.

Intermediate Accounting

Major Components of Annual Report

An annual report is a complete report of a company which establishes its financial

health on presenting information on every financial year. It also focuses on presenting history

of the company along with its achievements and recognitions made in the past. It helps the

shareholders, investors, stakeholders, government, and media by giving accurate information

and all those details from the annual report helps the potential users in their decisions making

(Symes, Sharma & Davey, 2017). The major components of the annual report are as

following:

1. Letter from the Chairman- The performance of the company during a particular year

is mentioned here.

2. Director’s report- Crucial events happened during a particular year in a company are

included in this (Shaw et al., 2017).

3. Auditor’s report- An auditor conducts the audit on the accounts and presents the

report to the shareholders of the company.

4. Balance Sheet- Financial position is presented stating what the company is having and

what the obligations are.

5. Profit and loss Account- Net profit of a company that is earned during the current

financial year.

6. Cash flow Statement- How much cash is earned by the company and are used during

a particular period is stated here.

7. Schedules- Operational performance of a company during the reporting period are

included in this.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Intermediate Accounting

8. Accounts of subsidiary- The information related to the geographical location of the

company and contact is given.

9. Corporate governance- Directors and management information of the company,

including their remuneration, is discussed here.

10. Accounting policies- Regulations and policies being followed by the company while

preparing their financial statement are included in this.

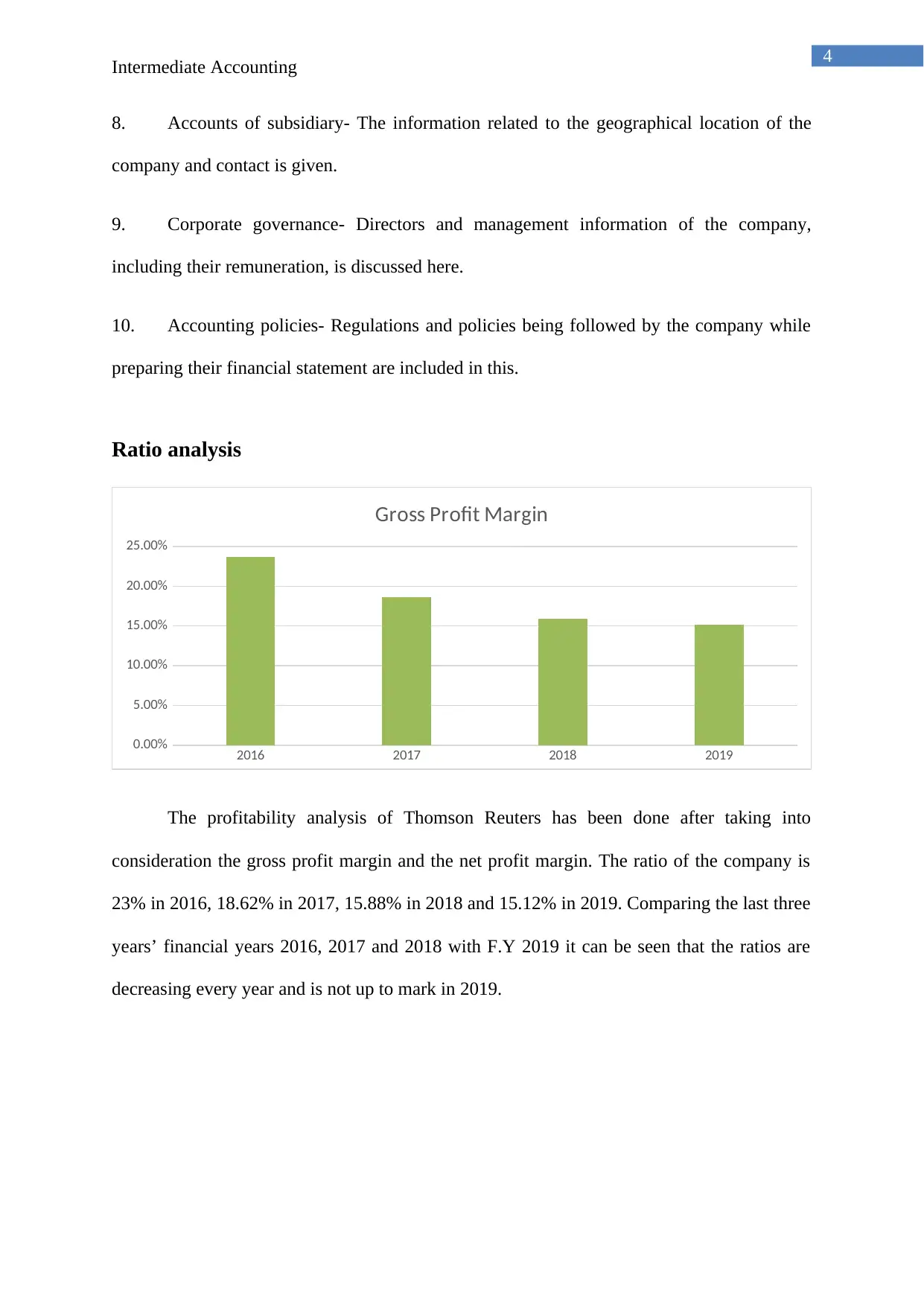

Ratio analysis

2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Gross Profit Margin

The profitability analysis of Thomson Reuters has been done after taking into

consideration the gross profit margin and the net profit margin. The ratio of the company is

23% in 2016, 18.62% in 2017, 15.88% in 2018 and 15.12% in 2019. Comparing the last three

years’ financial years 2016, 2017 and 2018 with F.Y 2019 it can be seen that the ratios are

decreasing every year and is not up to mark in 2019.

Intermediate Accounting

8. Accounts of subsidiary- The information related to the geographical location of the

company and contact is given.

9. Corporate governance- Directors and management information of the company,

including their remuneration, is discussed here.

10. Accounting policies- Regulations and policies being followed by the company while

preparing their financial statement are included in this.

Ratio analysis

2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Gross Profit Margin

The profitability analysis of Thomson Reuters has been done after taking into

consideration the gross profit margin and the net profit margin. The ratio of the company is

23% in 2016, 18.62% in 2017, 15.88% in 2018 and 15.12% in 2019. Comparing the last three

years’ financial years 2016, 2017 and 2018 with F.Y 2019 it can be seen that the ratios are

decreasing every year and is not up to mark in 2019.

5

Intermediate Accounting

2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

NetProfit Margin

At the same time, the net profit margin for 2019 is great with an immense growth as

compared to the previous year 2018. The net profit margin ratio of the company is 17% in

2016, 12.03% in 2017, 2.99% in 2018 and 26.58% in 2019. The ratios are decreasing

constantly from 2016 to 2918 but in 2019, the ratio growth is good. The industry average of

net profit is 10% which shows that in all the years the company is going well except the 2018

in which the net profit margin was too low.

2016 2017 2018 2019

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current ratio

On the other hand, the current ratio has been calculated as 1.02 in 2016, 0.62 in 2017,

1.64 in 2018 and 0.92 in 2019. The current ratio examines measure the liquidity of a

company after evaluating the ability of the business to pay off its current liabilities with

Intermediate Accounting

2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

NetProfit Margin

At the same time, the net profit margin for 2019 is great with an immense growth as

compared to the previous year 2018. The net profit margin ratio of the company is 17% in

2016, 12.03% in 2017, 2.99% in 2018 and 26.58% in 2019. The ratios are decreasing

constantly from 2016 to 2918 but in 2019, the ratio growth is good. The industry average of

net profit is 10% which shows that in all the years the company is going well except the 2018

in which the net profit margin was too low.

2016 2017 2018 2019

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current ratio

On the other hand, the current ratio has been calculated as 1.02 in 2016, 0.62 in 2017,

1.64 in 2018 and 0.92 in 2019. The current ratio examines measure the liquidity of a

company after evaluating the ability of the business to pay off its current liabilities with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Intermediate Accounting

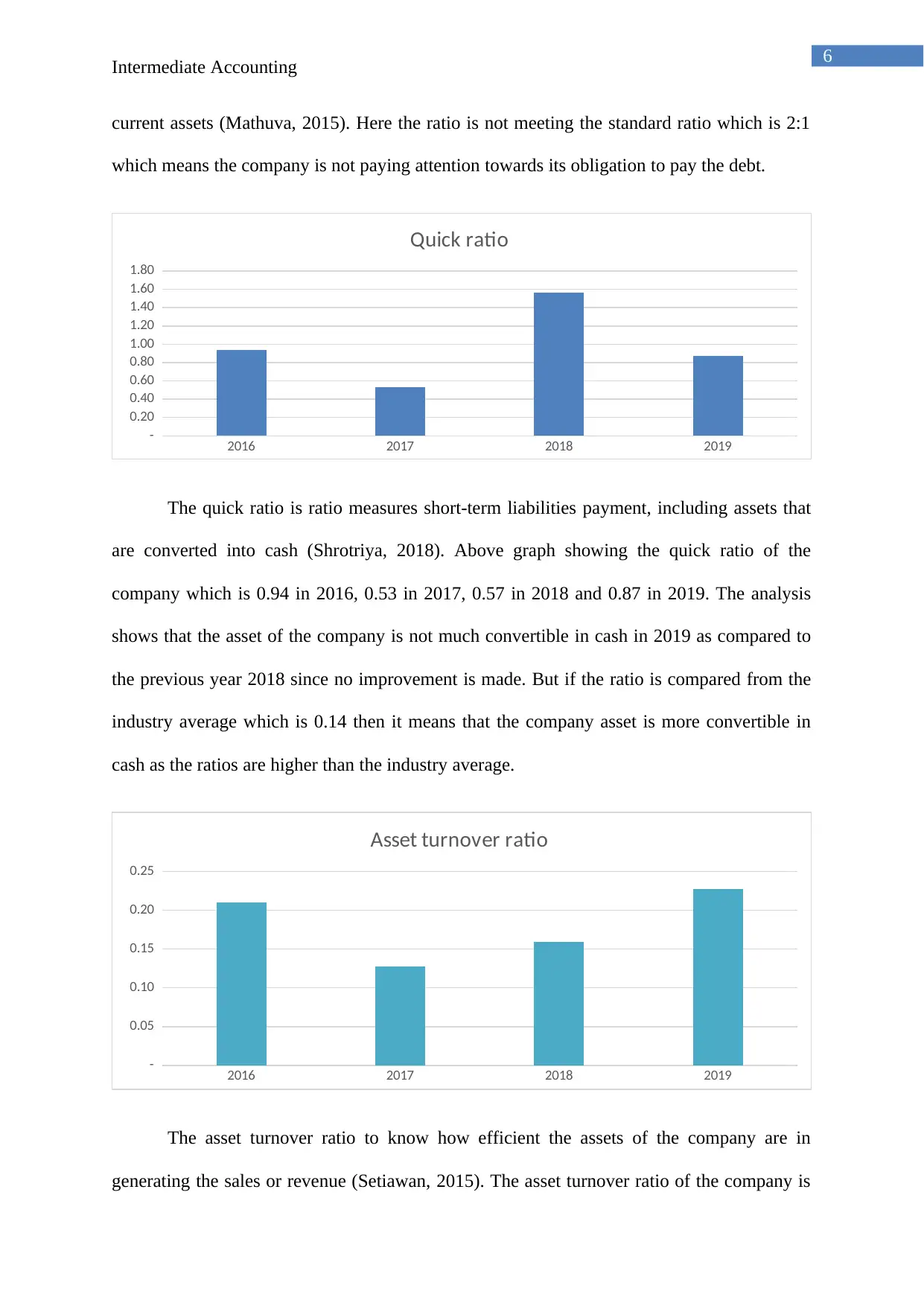

current assets (Mathuva, 2015). Here the ratio is not meeting the standard ratio which is 2:1

which means the company is not paying attention towards its obligation to pay the debt.

2016 2017 2018 2019

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Quick ratio

The quick ratio is ratio measures short-term liabilities payment, including assets that

are converted into cash (Shrotriya, 2018). Above graph showing the quick ratio of the

company which is 0.94 in 2016, 0.53 in 2017, 0.57 in 2018 and 0.87 in 2019. The analysis

shows that the asset of the company is not much convertible in cash in 2019 as compared to

the previous year 2018 since no improvement is made. But if the ratio is compared from the

industry average which is 0.14 then it means that the company asset is more convertible in

cash as the ratios are higher than the industry average.

2016 2017 2018 2019

-

0.05

0.10

0.15

0.20

0.25

Asset turnover ratio

The asset turnover ratio to know how efficient the assets of the company are in

generating the sales or revenue (Setiawan, 2015). The asset turnover ratio of the company is

Intermediate Accounting

current assets (Mathuva, 2015). Here the ratio is not meeting the standard ratio which is 2:1

which means the company is not paying attention towards its obligation to pay the debt.

2016 2017 2018 2019

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Quick ratio

The quick ratio is ratio measures short-term liabilities payment, including assets that

are converted into cash (Shrotriya, 2018). Above graph showing the quick ratio of the

company which is 0.94 in 2016, 0.53 in 2017, 0.57 in 2018 and 0.87 in 2019. The analysis

shows that the asset of the company is not much convertible in cash in 2019 as compared to

the previous year 2018 since no improvement is made. But if the ratio is compared from the

industry average which is 0.14 then it means that the company asset is more convertible in

cash as the ratios are higher than the industry average.

2016 2017 2018 2019

-

0.05

0.10

0.15

0.20

0.25

Asset turnover ratio

The asset turnover ratio to know how efficient the assets of the company are in

generating the sales or revenue (Setiawan, 2015). The asset turnover ratio of the company is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Intermediate Accounting

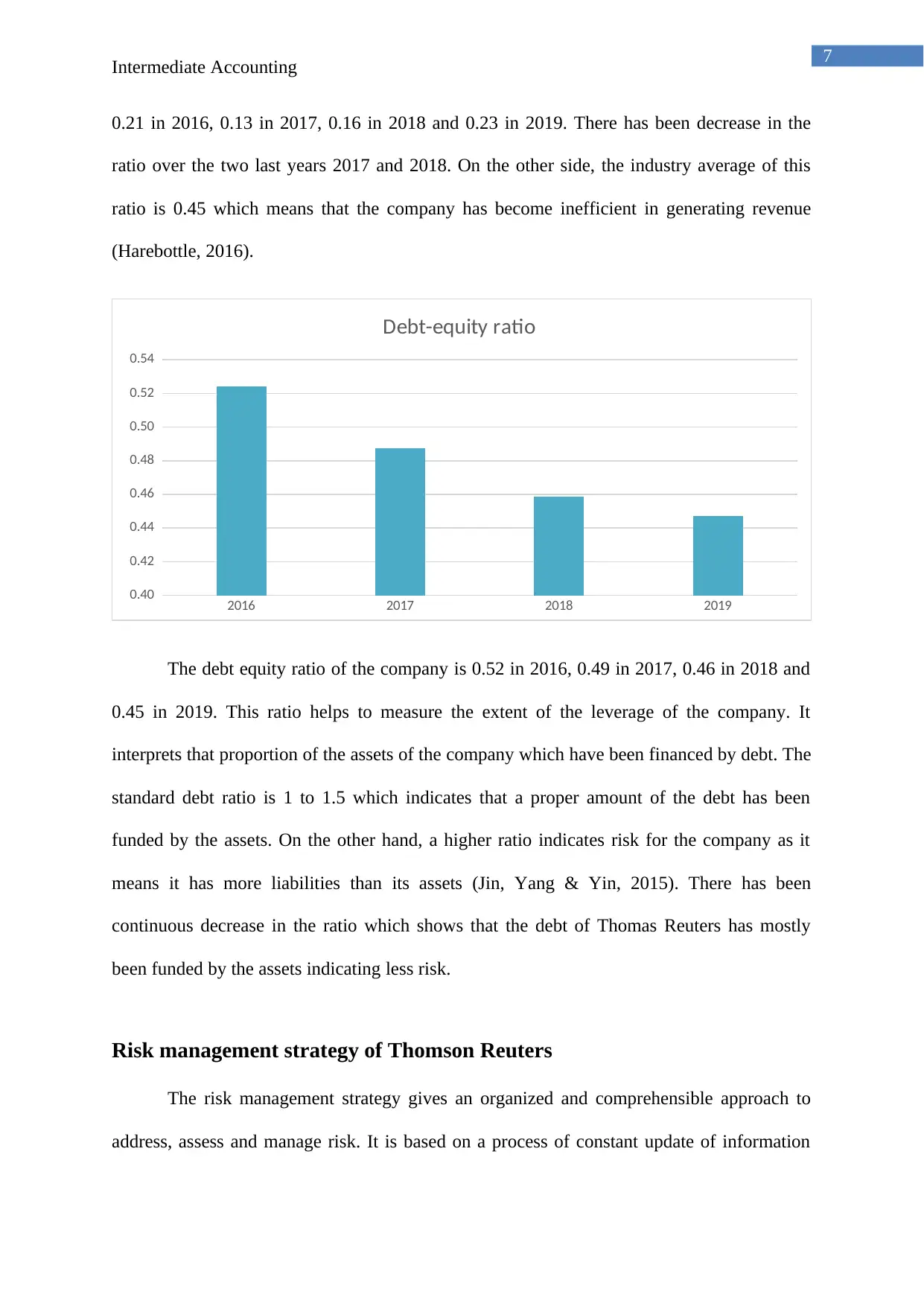

0.21 in 2016, 0.13 in 2017, 0.16 in 2018 and 0.23 in 2019. There has been decrease in the

ratio over the two last years 2017 and 2018. On the other side, the industry average of this

ratio is 0.45 which means that the company has become inefficient in generating revenue

(Harebottle, 2016).

2016 2017 2018 2019

0.40

0.42

0.44

0.46

0.48

0.50

0.52

0.54

Debt-equity ratio

The debt equity ratio of the company is 0.52 in 2016, 0.49 in 2017, 0.46 in 2018 and

0.45 in 2019. This ratio helps to measure the extent of the leverage of the company. It

interprets that proportion of the assets of the company which have been financed by debt. The

standard debt ratio is 1 to 1.5 which indicates that a proper amount of the debt has been

funded by the assets. On the other hand, a higher ratio indicates risk for the company as it

means it has more liabilities than its assets (Jin, Yang & Yin, 2015). There has been

continuous decrease in the ratio which shows that the debt of Thomas Reuters has mostly

been funded by the assets indicating less risk.

Risk management strategy of Thomson Reuters

The risk management strategy gives an organized and comprehensible approach to

address, assess and manage risk. It is based on a process of constant update of information

Intermediate Accounting

0.21 in 2016, 0.13 in 2017, 0.16 in 2018 and 0.23 in 2019. There has been decrease in the

ratio over the two last years 2017 and 2018. On the other side, the industry average of this

ratio is 0.45 which means that the company has become inefficient in generating revenue

(Harebottle, 2016).

2016 2017 2018 2019

0.40

0.42

0.44

0.46

0.48

0.50

0.52

0.54

Debt-equity ratio

The debt equity ratio of the company is 0.52 in 2016, 0.49 in 2017, 0.46 in 2018 and

0.45 in 2019. This ratio helps to measure the extent of the leverage of the company. It

interprets that proportion of the assets of the company which have been financed by debt. The

standard debt ratio is 1 to 1.5 which indicates that a proper amount of the debt has been

funded by the assets. On the other hand, a higher ratio indicates risk for the company as it

means it has more liabilities than its assets (Jin, Yang & Yin, 2015). There has been

continuous decrease in the ratio which shows that the debt of Thomas Reuters has mostly

been funded by the assets indicating less risk.

Risk management strategy of Thomson Reuters

The risk management strategy gives an organized and comprehensible approach to

address, assess and manage risk. It is based on a process of constant update of information

8

Intermediate Accounting

and checking of the assessment process on the basis of innovative actions taken by the

organization.

The risk management strategy of Thomson Reuters is supported by its strong

corporate governance strategy, which address the risk and make sure the compliances

required for the organization (Wressell, Rasmussen & Driscoll, 2018). The risk management

strategy consists of authentic information, effective management tools and software, and

skillful human resources which can help the company to manage risk effectively and to

enhance the growth rate effectively.

With the combination of these strategies the management of the company can

confidently predict the risk factors and take necessary actions effectively, which includes

effective management of customers, suppliers, compliance related issues and financial risks

while promoting the corporate governance and imposing better control system in the

organization (Okafor, Anderson & Warsame, 2016).

The risk management strategy of Thomas Reuters consists a supervisory intelligence

portal that provides a complete information to the investors so that they can get all the

relevant information which can help them to take investment decisions (Korableva, Gorelov

& Shulha, 2017). The risk management strategy also includes a shared categorization of all

the risk and compliance related matters that will directly influence the investors.

In addition to that the enterprise risk management feature is used to assess and

evaluate the risk, it tracks the events that may cause the occurrence of risk and help in

tracking and mitigating the potential risk that may occur due to the occurrence of any future

events.

Intermediate Accounting

and checking of the assessment process on the basis of innovative actions taken by the

organization.

The risk management strategy of Thomson Reuters is supported by its strong

corporate governance strategy, which address the risk and make sure the compliances

required for the organization (Wressell, Rasmussen & Driscoll, 2018). The risk management

strategy consists of authentic information, effective management tools and software, and

skillful human resources which can help the company to manage risk effectively and to

enhance the growth rate effectively.

With the combination of these strategies the management of the company can

confidently predict the risk factors and take necessary actions effectively, which includes

effective management of customers, suppliers, compliance related issues and financial risks

while promoting the corporate governance and imposing better control system in the

organization (Okafor, Anderson & Warsame, 2016).

The risk management strategy of Thomas Reuters consists a supervisory intelligence

portal that provides a complete information to the investors so that they can get all the

relevant information which can help them to take investment decisions (Korableva, Gorelov

& Shulha, 2017). The risk management strategy also includes a shared categorization of all

the risk and compliance related matters that will directly influence the investors.

In addition to that the enterprise risk management feature is used to assess and

evaluate the risk, it tracks the events that may cause the occurrence of risk and help in

tracking and mitigating the potential risk that may occur due to the occurrence of any future

events.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Intermediate Accounting

Accounting policy and its impact

The different accounting policy option that is available to the companies are stated below

Subsidiaries (section 1590)

• Consolidation method

• Equity method

• Cost method

Significantly influenced investees (section 3051)

• Equity method

• Cost method

• Joint ventures

Proportionate consolidation method

• Equity method

• Cost method

Internally generated intangible assets (section 3064)

• Capitalization of development costs

• Expenses incurred during the phase of development

Income taxes (section 3465)

• Taxes payable method

• Future income tax methods

Intermediate Accounting

Accounting policy and its impact

The different accounting policy option that is available to the companies are stated below

Subsidiaries (section 1590)

• Consolidation method

• Equity method

• Cost method

Significantly influenced investees (section 3051)

• Equity method

• Cost method

• Joint ventures

Proportionate consolidation method

• Equity method

• Cost method

Internally generated intangible assets (section 3064)

• Capitalization of development costs

• Expenses incurred during the phase of development

Income taxes (section 3465)

• Taxes payable method

• Future income tax methods

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Intermediate Accounting

Financial instruments

• Measurement of financial assets at fair value

• Measurements of financial assets and liabilities at amortized value (other than equity

and derivative instruments)

The organizations have the choices to select among these methods but they have to

select the best method among all these alternatives so that their financial statements can

reflect the true and fair view of the financial position of the organization (Lestari & Riyadi,

2018).

Impact of the application of the Canadian accounting standards

If Thomas Reuters get the opportunity to make a choice in the accounting policy, then

it will affect the financial statements and the retained earnings of the company (Jackson et al.,

2018). If the accounting policy is made as per the Canadian accounting policy, it will increase

the depreciation expenses which will make direct impact on the profit but at the same time it

will give tax benefit to the organization. Beside that Thomas Reuters also have to make more

changes in the valuation of the various financial instruments like equity and derivatives (Saqib

et al., 2016). The company will choose the specific policy over the other alternatives as it will

enhance the earning maximization capacity of the organization. This will bring a

comprehensive impact on the analysis process as from the accounting policies it will be

possible to get a transparent view of the financial statements of the company and from that

the actual financial position of Thomas Reuters can be easily assessed.

Intermediate Accounting

Financial instruments

• Measurement of financial assets at fair value

• Measurements of financial assets and liabilities at amortized value (other than equity

and derivative instruments)

The organizations have the choices to select among these methods but they have to

select the best method among all these alternatives so that their financial statements can

reflect the true and fair view of the financial position of the organization (Lestari & Riyadi,

2018).

Impact of the application of the Canadian accounting standards

If Thomas Reuters get the opportunity to make a choice in the accounting policy, then

it will affect the financial statements and the retained earnings of the company (Jackson et al.,

2018). If the accounting policy is made as per the Canadian accounting policy, it will increase

the depreciation expenses which will make direct impact on the profit but at the same time it

will give tax benefit to the organization. Beside that Thomas Reuters also have to make more

changes in the valuation of the various financial instruments like equity and derivatives (Saqib

et al., 2016). The company will choose the specific policy over the other alternatives as it will

enhance the earning maximization capacity of the organization. This will bring a

comprehensive impact on the analysis process as from the accounting policies it will be

possible to get a transparent view of the financial statements of the company and from that

the actual financial position of Thomas Reuters can be easily assessed.

11

Intermediate Accounting

‘Events after the Reporting Period’ (IAS 10)

The IAS 10 “Events After the Reporting Period” does contain the requirements which

are for the events occurring post the reporting period, and which can be adjusted in the

financial statements of the organization. The events that are adjusted, does provide evidence

that is upon the conditions which are existing on the last day of accounting period (Tebbens

& Thompson, 2017). The non-adjusting events are indicative of the circumstances, which

arise after the reporting period (Vasilenko & Titova, 2019). The IAS 10 was issued again in

the year 2003, December and does it gradually applied by every organization to their annual

periods and in the beginning on or after the 1st January, 2005.

The objective of the IAS 10, does discloses that an entity should be given related to

the date, and when the financial report are authorized for the issue and there are several

events after the reporting entity (Hisrich & Ramadani, 2017). As per this standard, the

organization should adjust the financial statements and for the events taking place afterwards.

The standard also implies that it does require the organization which does not make the

financial statements upon the ongoing basis and if the events after the reporting period does

indicate that the going concern is not inappropriate (van et al., 2016). The Scope in IAS 10, is

applied for the disclosure of transactions which is occurring after the reporting period. The

events that may occur after the reporting period can be favorable and unfavorable, which will

occur between the statement of financial position date and the date when the financial

statements are being authorized for the issue (Len & Glivenko, 2019).

The process that are involved in approving the financial statements is for the issue

which will be varying upon the financial decision, management decision, statutory

requirements, and several procedures that will be followed for preparation of accounts and

finalization of the same (Tan, 2018). For adjusting the events after the reporting period, the

Intermediate Accounting

‘Events after the Reporting Period’ (IAS 10)

The IAS 10 “Events After the Reporting Period” does contain the requirements which

are for the events occurring post the reporting period, and which can be adjusted in the

financial statements of the organization. The events that are adjusted, does provide evidence

that is upon the conditions which are existing on the last day of accounting period (Tebbens

& Thompson, 2017). The non-adjusting events are indicative of the circumstances, which

arise after the reporting period (Vasilenko & Titova, 2019). The IAS 10 was issued again in

the year 2003, December and does it gradually applied by every organization to their annual

periods and in the beginning on or after the 1st January, 2005.

The objective of the IAS 10, does discloses that an entity should be given related to

the date, and when the financial report are authorized for the issue and there are several

events after the reporting entity (Hisrich & Ramadani, 2017). As per this standard, the

organization should adjust the financial statements and for the events taking place afterwards.

The standard also implies that it does require the organization which does not make the

financial statements upon the ongoing basis and if the events after the reporting period does

indicate that the going concern is not inappropriate (van et al., 2016). The Scope in IAS 10, is

applied for the disclosure of transactions which is occurring after the reporting period. The

events that may occur after the reporting period can be favorable and unfavorable, which will

occur between the statement of financial position date and the date when the financial

statements are being authorized for the issue (Len & Glivenko, 2019).

The process that are involved in approving the financial statements is for the issue

which will be varying upon the financial decision, management decision, statutory

requirements, and several procedures that will be followed for preparation of accounts and

finalization of the same (Tan, 2018). For adjusting the events after the reporting period, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.