Timber Floors Pty Ltd: Taxable Income and Tax Liability, Year 2018

VerifiedAdded on 2023/06/11

|5

|1340

|204

Homework Assignment

AI Summary

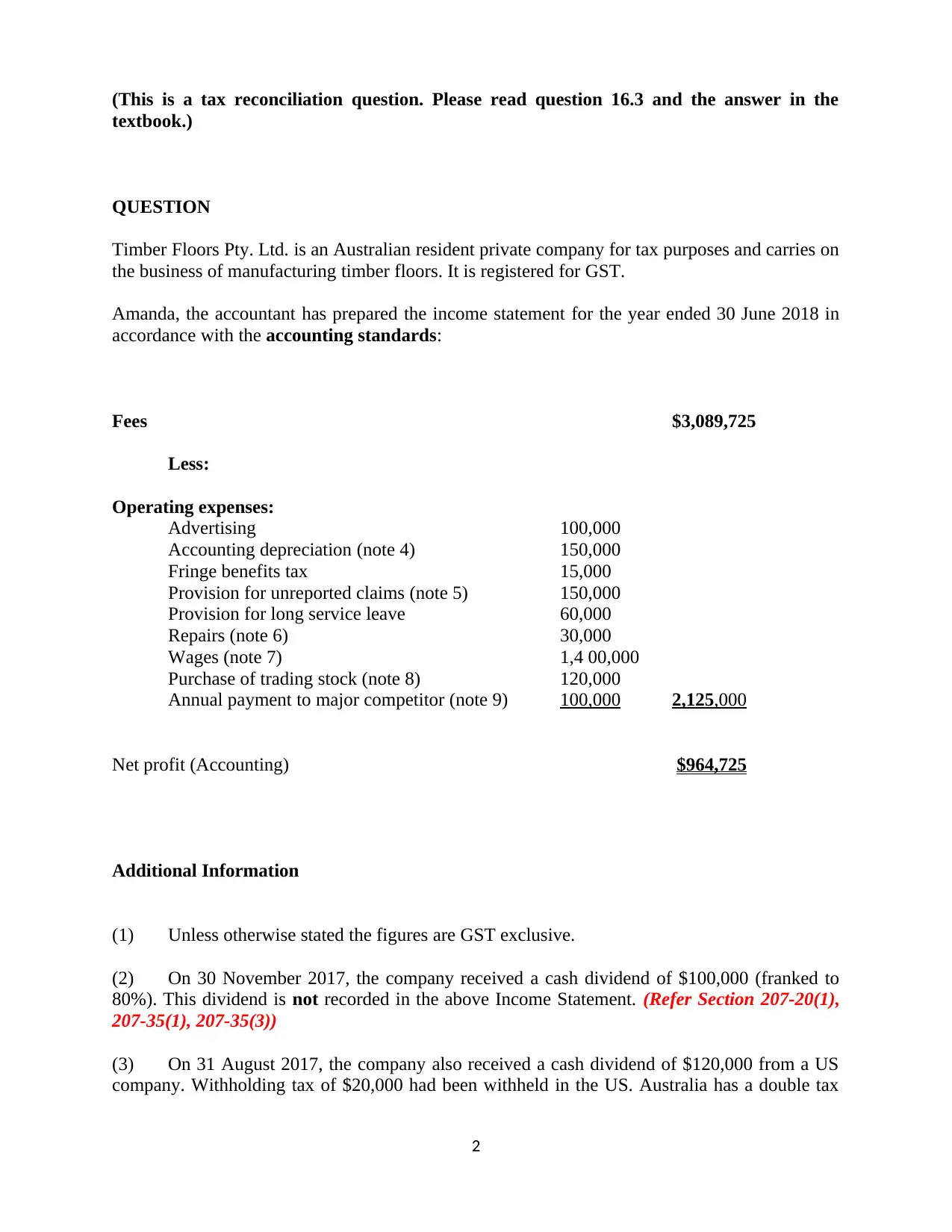

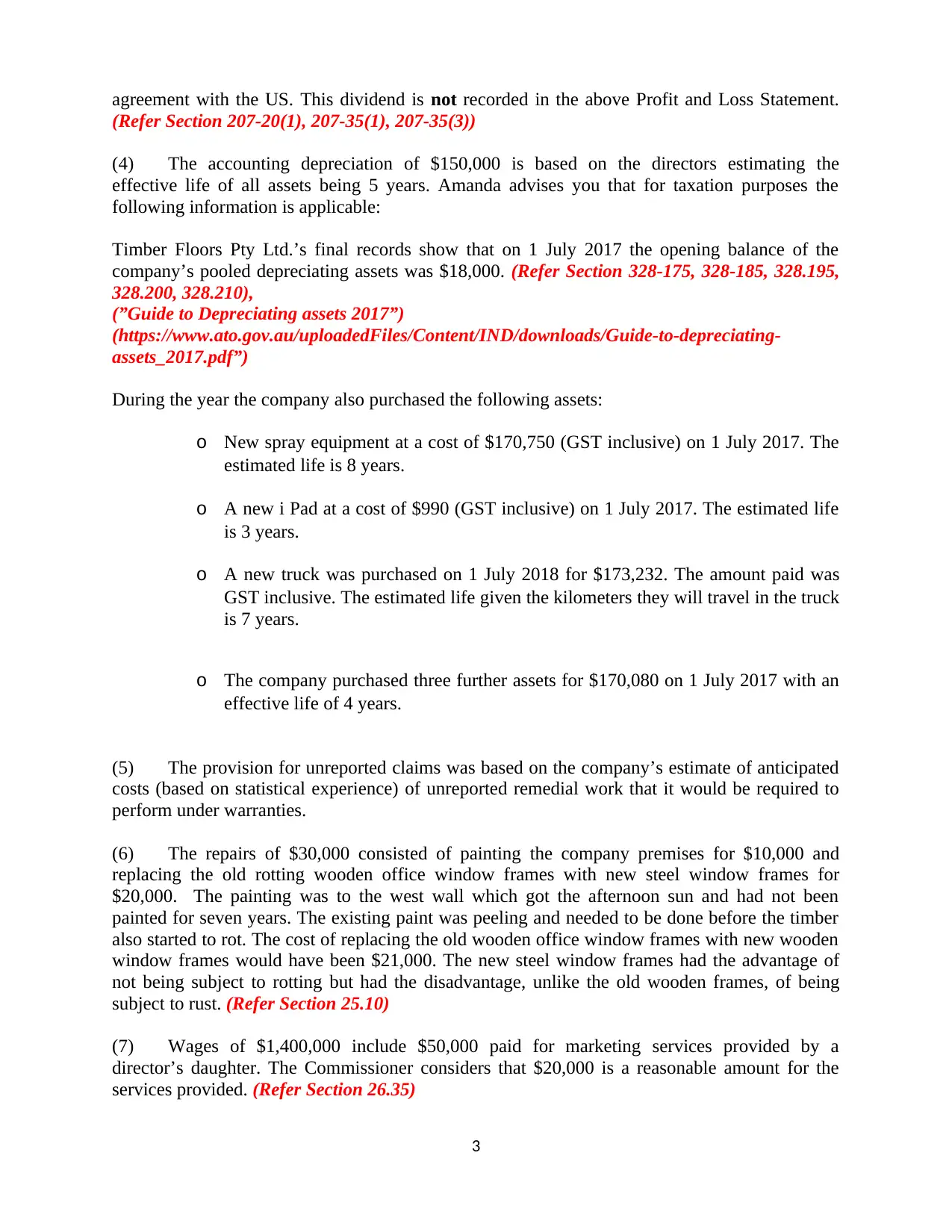

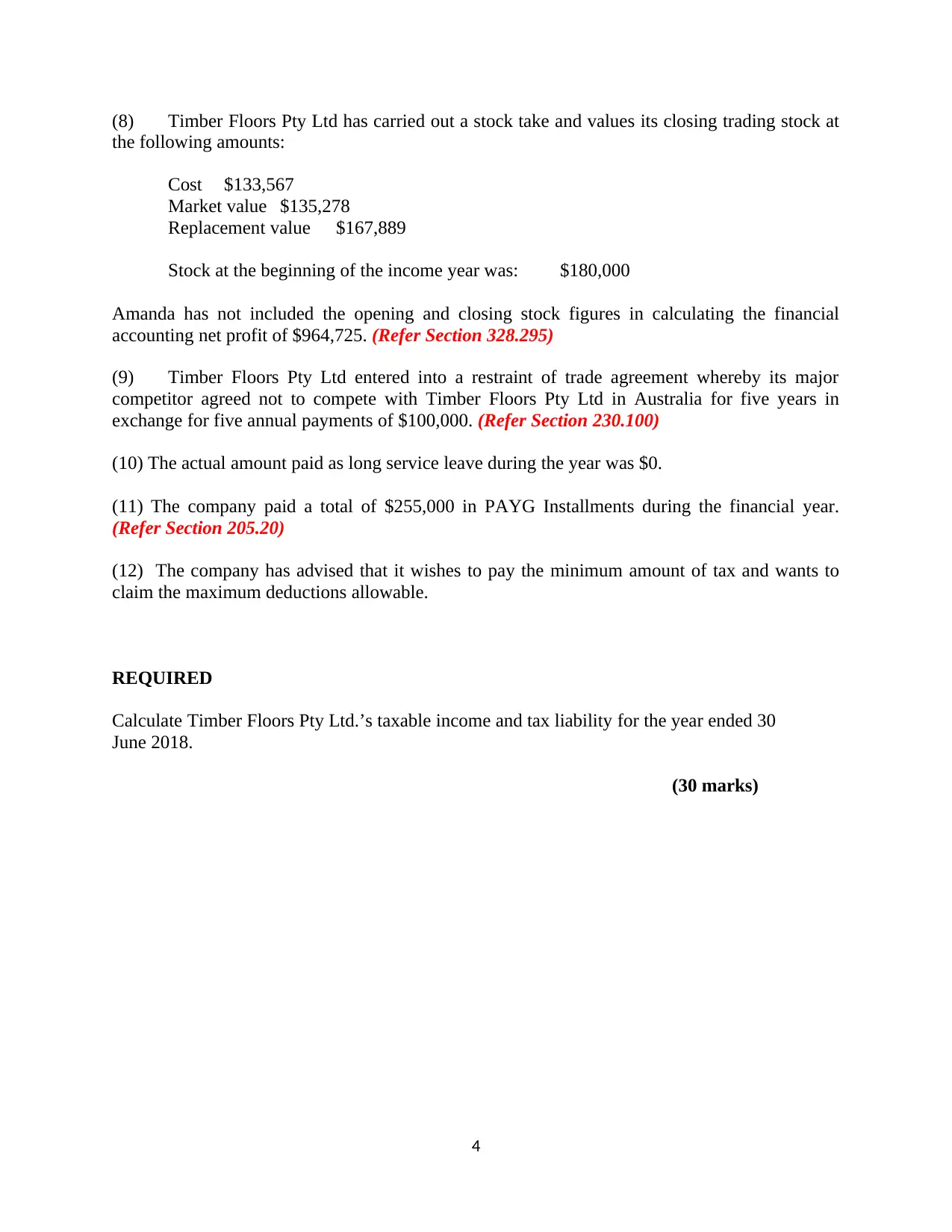

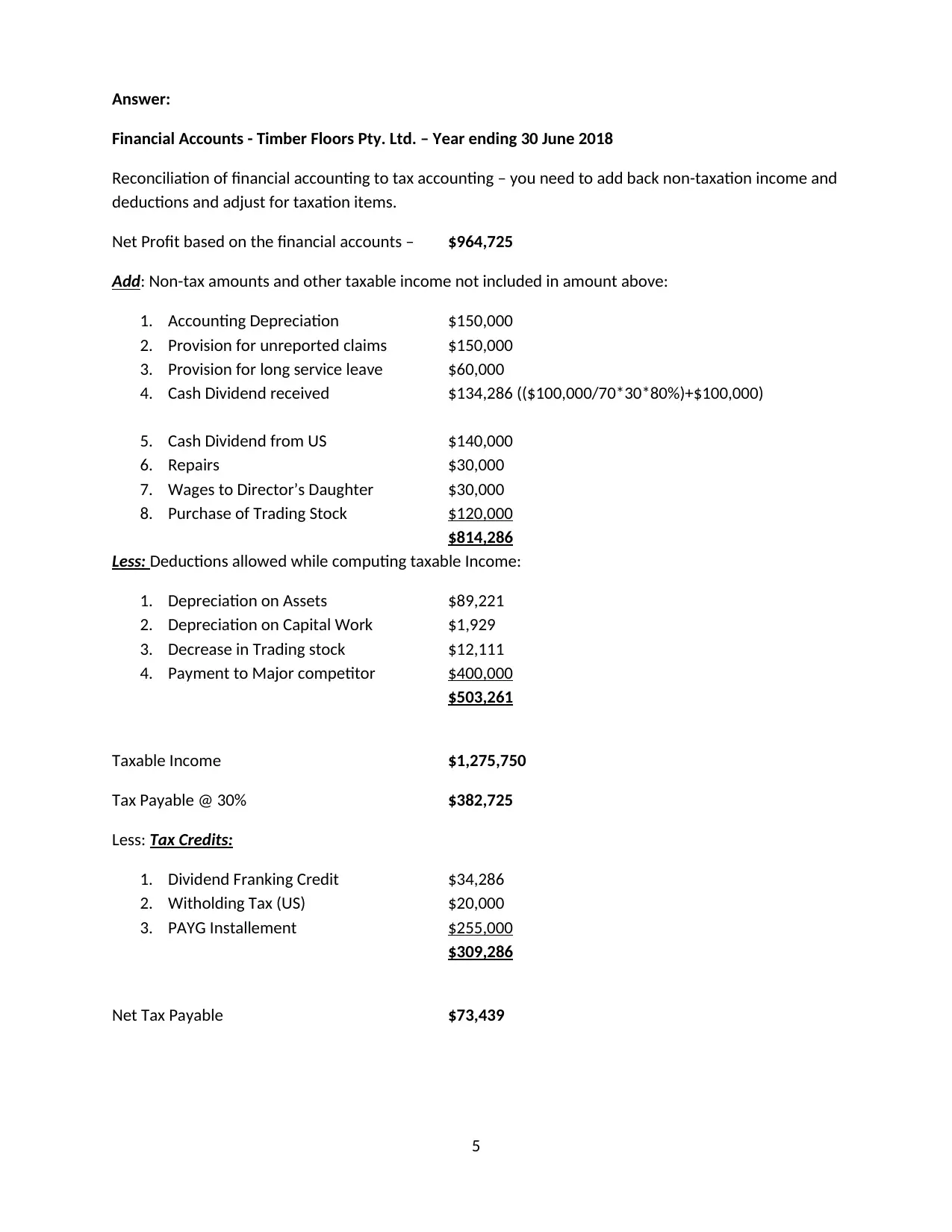

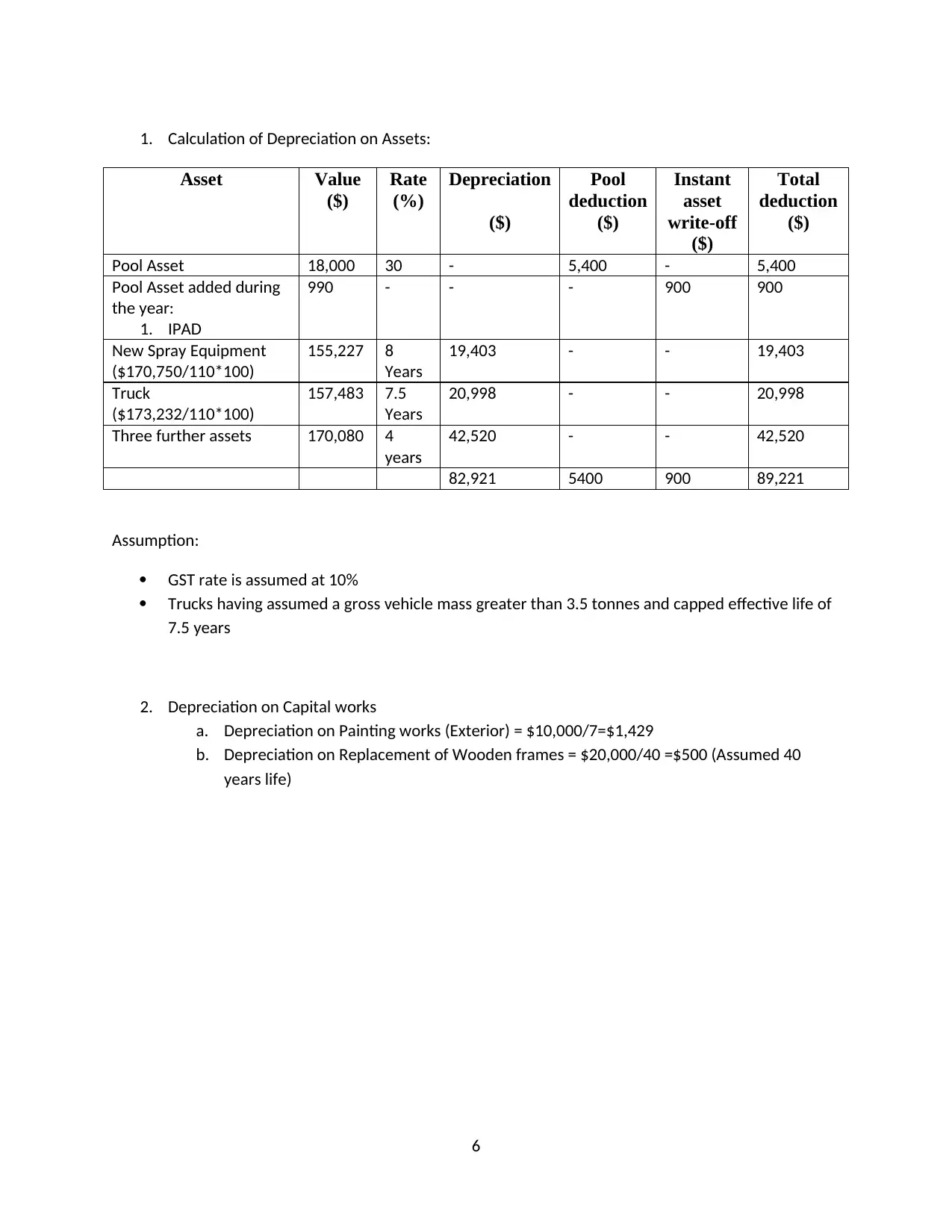

This assignment provides a detailed calculation of Timber Floors Pty Ltd.'s taxable income and tax liability for the year ended 30 June 2018. It begins with the net profit based on financial accounts and reconciles it to taxable income by adding back non-taxable amounts and other taxable income not included in the initial amount, such as accounting depreciation, provisions for unreported claims and long service leave, cash dividends received, repairs, and wages to a director's daughter. It then deducts allowable expenses like depreciation on assets and capital works, and adjustments in trading stock. The taxable income is determined, and the tax payable is calculated, followed by deductions for tax credits, including dividend franking credits, withholding tax, and PAYG installments, resulting in the net tax payable. The assignment includes calculations for depreciation on assets and capital works, with specific assumptions regarding GST rates and truck classifications.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.