Evaluating Time-Driven Activity-Based Costing for Nestle's Operations

VerifiedAdded on 2020/05/28

|13

|2868

|604

Report

AI Summary

This report provides a comprehensive analysis of Time-Driven Activity-Based Costing (TDABC) and its suitability for the Nestle Company. It begins with an introduction to the concept of TDABC, highlighting its advantages over traditional costing and Activity-Based Costing (ABC). The report offers a detailed overview of Nestle, including its company profile, purpose, values, and strategic roadmap. It then delves into the specifics of TDABC, explaining the time equation, key features, and the process of assessing per-unit cost, and time consumption. Furthermore, the report differentiates between TDABC, ABC, and traditional costing methods, explaining why TDABC is appropriate for Nestle's operations. The report concludes by summarizing the benefits of implementing TDABC within Nestle's complex business structure, emphasizing its potential to enhance cost management and improve overall productivity. Relevant references are also included.

R

Nestle

Managerial Accounting

Time-Driven Activity-Based Costing

Nestle

Managerial Accounting

Time-Driven Activity-Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TIME-DRIVEN ACTIVITY BASED COSTING

1

Table of Contents

Introduction...........................................................................................................................................2

Company Profile................................................................................................................................2

Purpose of Nestle..........................................................................................................................3

Values of Nestle.............................................................................................................................3

Strategy of Nestle..........................................................................................................................3

Strategic Roadmap Of Nestle.........................................................................................................4

Time-Driven Activity-Based Costing (TDABC).....................................................................................4

Time Equation to Capture Complication........................................................................................6

Features of Time-Driven Activity-Based Costing (TDABC)..............................................................7

Difference between Time-Driven Activity-Based Costing (TDABC) and Activity-Based Costing (ABC)

...........................................................................................................................................................8

Difference between Time-Driven Activity-Based Costing (TDABC) and Traditional Costing..............8

Reason for why Time-Driven Activity-Based Costing is suitable for Nestle Company........................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

1

Table of Contents

Introduction...........................................................................................................................................2

Company Profile................................................................................................................................2

Purpose of Nestle..........................................................................................................................3

Values of Nestle.............................................................................................................................3

Strategy of Nestle..........................................................................................................................3

Strategic Roadmap Of Nestle.........................................................................................................4

Time-Driven Activity-Based Costing (TDABC).....................................................................................4

Time Equation to Capture Complication........................................................................................6

Features of Time-Driven Activity-Based Costing (TDABC)..............................................................7

Difference between Time-Driven Activity-Based Costing (TDABC) and Activity-Based Costing (ABC)

...........................................................................................................................................................8

Difference between Time-Driven Activity-Based Costing (TDABC) and Traditional Costing..............8

Reason for why Time-Driven Activity-Based Costing is suitable for Nestle Company........................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

TIME-DRIVEN ACTIVITY BASED COSTING

2

Introduction

Every organization wants to increase its productivity and manage the time and resources

taken by each activity. Nestle Company is one of them who always want to improve its

productivity and profit. Nestle is known as the largest company of food and beverages and a

well-known brand recognized across the world. This report is going to be prepared in order to

identify whether the Time-Driven Activity-Based Costing (TDABC) will be suitable for the

process and function of the business. The report will provide the brief description of the

Nestle Company along with the model of Time-Driven Activity-Based Costing (TDABC)

and its features. Further, the report will differentiate between the Activity-based Costing

(ABC), Traditional Costing, and Time-Driven Activity-based Costing (TDABC).

Company Profile

Nestle is an international company dealing in the sector of food and beverages. Headquarter

of the company is in Vevey, Switzerland. It is known as the world’s biggest company of

food, evaluated by metrics and revenues, since 2014. In 2014, the company was ranked on

No. 72 by the Fortune Global 500 and in 2016; it was ranked on No. 33 in the Forbes Global

2000 which involve the list of biggest companies. The product line of Nestle includes

breakfast cereals, Maggie, baby food, tea and coffee, medical food, ice cream, confectionery,

bottled water, snacks, pet foods, dairy products and frozen food (Nestle, 2018). Twenty-nine

brands of Nestle have yearly sales over CHF1 billion, comprising Nesquik, Maggie,

Nespresso, Vittel, Nescafe, Stouffer’s, and Kit Kat. Company operates in 194 countries with

447 factories, and 330,000 employees. Nestle company is the major shareholder of world’s

biggest company of cosmetics i.e. L’Oreal.

2

Introduction

Every organization wants to increase its productivity and manage the time and resources

taken by each activity. Nestle Company is one of them who always want to improve its

productivity and profit. Nestle is known as the largest company of food and beverages and a

well-known brand recognized across the world. This report is going to be prepared in order to

identify whether the Time-Driven Activity-Based Costing (TDABC) will be suitable for the

process and function of the business. The report will provide the brief description of the

Nestle Company along with the model of Time-Driven Activity-Based Costing (TDABC)

and its features. Further, the report will differentiate between the Activity-based Costing

(ABC), Traditional Costing, and Time-Driven Activity-based Costing (TDABC).

Company Profile

Nestle is an international company dealing in the sector of food and beverages. Headquarter

of the company is in Vevey, Switzerland. It is known as the world’s biggest company of

food, evaluated by metrics and revenues, since 2014. In 2014, the company was ranked on

No. 72 by the Fortune Global 500 and in 2016; it was ranked on No. 33 in the Forbes Global

2000 which involve the list of biggest companies. The product line of Nestle includes

breakfast cereals, Maggie, baby food, tea and coffee, medical food, ice cream, confectionery,

bottled water, snacks, pet foods, dairy products and frozen food (Nestle, 2018). Twenty-nine

brands of Nestle have yearly sales over CHF1 billion, comprising Nesquik, Maggie,

Nespresso, Vittel, Nescafe, Stouffer’s, and Kit Kat. Company operates in 194 countries with

447 factories, and 330,000 employees. Nestle company is the major shareholder of world’s

biggest company of cosmetics i.e. L’Oreal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TIME-DRIVEN ACTIVITY BASED COSTING

3

Purpose of Nestle

The purpose of Nestle is improving the life's quality and contributing to a better and

improved future. They want to contribute in shaping a healthier and better world by

encouraging society to have better and healthier lives. This is their way to contribute to

society and fulfill their corporate social responsibilities and confirming the success of the

company for long-term (Nestle, 2018).

Values of Nestle

The values of Nestle are imitated by their way of pursuing business; they always follow and

respect the rules and regulation implemented by the government. They always give equal

respect to the people with whom they work.

Strategy of Nestle

In today's scenario nutrition act as an important aspect of everyone's life. The strategy of the

Nestle Company is focused towards delivering various benefits to every individual through

the products and services they offer. The company is working hard from last 150 years and

now they have succeeded in attaining the top position by anticipating and understanding the

society needs, and constantly familiarizing themselves to grab the presented opportunities

(Nestle, 2018).

The fast-changing expectations and needs of the society reconfirm the strength of our

wellness, health and nutrition strategy. The world is at the point of change. The rapidity,

strength and the range of change are extraordinary. The digital disturbance is redesigning the

whole industry, relations with the company’s retailers and suppliers, and customers.

Technology and science developments are providing opportunities to the Nestle Company in

order to play a major role in considering the challenges faced by the society. In the world

3

Purpose of Nestle

The purpose of Nestle is improving the life's quality and contributing to a better and

improved future. They want to contribute in shaping a healthier and better world by

encouraging society to have better and healthier lives. This is their way to contribute to

society and fulfill their corporate social responsibilities and confirming the success of the

company for long-term (Nestle, 2018).

Values of Nestle

The values of Nestle are imitated by their way of pursuing business; they always follow and

respect the rules and regulation implemented by the government. They always give equal

respect to the people with whom they work.

Strategy of Nestle

In today's scenario nutrition act as an important aspect of everyone's life. The strategy of the

Nestle Company is focused towards delivering various benefits to every individual through

the products and services they offer. The company is working hard from last 150 years and

now they have succeeded in attaining the top position by anticipating and understanding the

society needs, and constantly familiarizing themselves to grab the presented opportunities

(Nestle, 2018).

The fast-changing expectations and needs of the society reconfirm the strength of our

wellness, health and nutrition strategy. The world is at the point of change. The rapidity,

strength and the range of change are extraordinary. The digital disturbance is redesigning the

whole industry, relations with the company’s retailers and suppliers, and customers.

Technology and science developments are providing opportunities to the Nestle Company in

order to play a major role in considering the challenges faced by the society. In the world

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TIME-DRIVEN ACTIVITY BASED COSTING

4

there are millions of people who do not receive proper nutrition, it the duty of Nestle

Company to help them and provide proper solutions (Nestle, 2012).

Strategic Roadmap Of Nestle

Source [https://www.nestle.com/aboutus/strategy]

Time-Driven Activity-Based Costing (TDABC)

The Time-Driven Activity-based Costing (TDABC) method is a new technique which is

introduced for overcoming the problem with Activity-based Costing. Activity-based Costing

4

there are millions of people who do not receive proper nutrition, it the duty of Nestle

Company to help them and provide proper solutions (Nestle, 2012).

Strategic Roadmap Of Nestle

Source [https://www.nestle.com/aboutus/strategy]

Time-Driven Activity-Based Costing (TDABC)

The Time-Driven Activity-based Costing (TDABC) method is a new technique which is

introduced for overcoming the problem with Activity-based Costing. Activity-based Costing

TIME-DRIVEN ACTIVITY BASED COSTING

5

(ABC) has supported many organizations in recognizing necessary opportunities of profit and

cost enhancements by re-presenting the loss-making customer relationships, procedure

developments on the shop floor, less cost of the design of the product, and modernized

product diversity (Ayvaz and Pehlivanli, 2011). The method provides probable large scale

opportunities for the companies. Luckily, the explanation is now conceivable by a method

which is named as time-driven activity-based costing (TDABC). This method has helped

many companies who have implemented this method in their system.

In this new method, management of the company can directly evaluate the demand of the

resources obligatory by every activity, deal, service, product or transaction rather than first

allocating the cost of the resource to the activities and then to customers or products (Basuki,

2014). For every resources group, estimation is required only for two parameters: per unit

cost of delivering capacity of resources and the unit time consumption of capacity of

resources by customers, products, and services. At the same time, the Time-Driven Activity-

based costing or (Time-Driven ABC) offers precise rates of cost-driver by permitting unit

times to be projected even for multifaceted, particular dealings (Kaplan and Amderson,

2007).

Assessing the per time unit cost of capacity- As an alternative to measure the time spent by

the employees, for this the managers will firstly identify the practical capacity of the supplied

resources as a percentage of hypothetical capacity. There are numerous ways to identify this.

According to the thumb rule, it can be easily assumed that applied capacity is 80 to 85% of

hypothetical full capacity. Therefore, if a machine or employee is ready to do the job of 40

hours for per week, then its applied capacity for per week is 32 to 35 hours.

Accessing the unit time of events- After calculating the per time unit cost of delivering

assets to the activities of the business; managers then determine the time consumed by a unit

5

(ABC) has supported many organizations in recognizing necessary opportunities of profit and

cost enhancements by re-presenting the loss-making customer relationships, procedure

developments on the shop floor, less cost of the design of the product, and modernized

product diversity (Ayvaz and Pehlivanli, 2011). The method provides probable large scale

opportunities for the companies. Luckily, the explanation is now conceivable by a method

which is named as time-driven activity-based costing (TDABC). This method has helped

many companies who have implemented this method in their system.

In this new method, management of the company can directly evaluate the demand of the

resources obligatory by every activity, deal, service, product or transaction rather than first

allocating the cost of the resource to the activities and then to customers or products (Basuki,

2014). For every resources group, estimation is required only for two parameters: per unit

cost of delivering capacity of resources and the unit time consumption of capacity of

resources by customers, products, and services. At the same time, the Time-Driven Activity-

based costing or (Time-Driven ABC) offers precise rates of cost-driver by permitting unit

times to be projected even for multifaceted, particular dealings (Kaplan and Amderson,

2007).

Assessing the per time unit cost of capacity- As an alternative to measure the time spent by

the employees, for this the managers will firstly identify the practical capacity of the supplied

resources as a percentage of hypothetical capacity. There are numerous ways to identify this.

According to the thumb rule, it can be easily assumed that applied capacity is 80 to 85% of

hypothetical full capacity. Therefore, if a machine or employee is ready to do the job of 40

hours for per week, then its applied capacity for per week is 32 to 35 hours.

Accessing the unit time of events- After calculating the per time unit cost of delivering

assets to the activities of the business; managers then determine the time consumed by a unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TIME-DRIVEN ACTIVITY BASED COSTING

6

of each activity. These figures can be attained by direct observation or by employee’s

interviews. There is no requirement of the surveys, even though employee’s survey might

help in big organizations. It is necessary to strain, however, the matter is not the time spend

by employee completing an activity but the time taken to finish one unit of particular activity.

Once, again accuracy is not dangerous; bumpy accuracy is enough (Kaplan and Anderson,

2007).

Driving the rates of the cost drivers- The rates of the cost-driver can be computed by

multiplying the variables i.e. two input variables, it is just has been projected.

Examining and reporting costs- The managers of the company are permitted by the time-

driven activity-based costing that their cost can be reported on a continuing base in a mode

that discloses the activity’s cost and time spent on those activities.

Updating the model- The Time-driven activity-based costing (TDABC) method can be

updated by the managers of the company to show variations in operating circumstances. In

order to add more activities in a department, there is no need for personnel interview, they

can just guess the required unit time for every activity. The rates of the cost-drivers can also

be updated by the managers.

Time Equation to Capture Complication

It has been assumed simply that every order or transaction of a specific type are similar and

need the same time duration to process. But Time-Driven Activity-Based Costing doesn’t ask

for this explanation. It can accommodate the difficulty of real-world processes by integrating

time equations, a different and attracting characteristics that allows the method to imitate how

order and action characteristic which affects the time of processing (Kaplan and Anderson,

2006). Time equation highly simplifies the assessing procedure and creates a far more precise

6

of each activity. These figures can be attained by direct observation or by employee’s

interviews. There is no requirement of the surveys, even though employee’s survey might

help in big organizations. It is necessary to strain, however, the matter is not the time spend

by employee completing an activity but the time taken to finish one unit of particular activity.

Once, again accuracy is not dangerous; bumpy accuracy is enough (Kaplan and Anderson,

2007).

Driving the rates of the cost drivers- The rates of the cost-driver can be computed by

multiplying the variables i.e. two input variables, it is just has been projected.

Examining and reporting costs- The managers of the company are permitted by the time-

driven activity-based costing that their cost can be reported on a continuing base in a mode

that discloses the activity’s cost and time spent on those activities.

Updating the model- The Time-driven activity-based costing (TDABC) method can be

updated by the managers of the company to show variations in operating circumstances. In

order to add more activities in a department, there is no need for personnel interview, they

can just guess the required unit time for every activity. The rates of the cost-drivers can also

be updated by the managers.

Time Equation to Capture Complication

It has been assumed simply that every order or transaction of a specific type are similar and

need the same time duration to process. But Time-Driven Activity-Based Costing doesn’t ask

for this explanation. It can accommodate the difficulty of real-world processes by integrating

time equations, a different and attracting characteristics that allows the method to imitate how

order and action characteristic which affects the time of processing (Kaplan and Anderson,

2006). Time equation highly simplifies the assessing procedure and creates a far more precise

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TIME-DRIVEN ACTIVITY BASED COSTING

7

cost model which will make the possibility of consuming traditional ABC techniques. The

key point is that the transaction can simply become complex, management of the company

can normally recognize how they are becoming complicated. The variable elements that

influence most of the activities can frequently state and classically record in the information

system of a company.

Features of Time-Driven Activity-Based Costing (TDABC)

Time-Driven Activity-based Costing (TDABC) is less expensive and can be easily

installed in the functioning of the business and can also be maintained properly. There

is no need to make additional expenses in this method.

Multiple time driver methods are implemented in this new method which will hold the

complexity of the Nestle Company in an improved way.

With the support of Time-Driven Activity-based costing the costing process becomes

simple because it supports the organization’s management in eliminating events like

interviews and survey and use applicable and significant information.

Organizations can enhance their system of cost management by explaining their

process capacity and application of cost and effectiveness of the orders, customers or

products.

Time-Driven Activity-based Costing method is different because it uses time equation

in which the consumption of time is evaluated on each activity.

This new approach identifies the opportunities for the competencies of the process

and supervision of capacity.

Time-Driven Activity-based Costing (TDABC) method is an exact and profit making

method because it is fast and simple to construct.

7

cost model which will make the possibility of consuming traditional ABC techniques. The

key point is that the transaction can simply become complex, management of the company

can normally recognize how they are becoming complicated. The variable elements that

influence most of the activities can frequently state and classically record in the information

system of a company.

Features of Time-Driven Activity-Based Costing (TDABC)

Time-Driven Activity-based Costing (TDABC) is less expensive and can be easily

installed in the functioning of the business and can also be maintained properly. There

is no need to make additional expenses in this method.

Multiple time driver methods are implemented in this new method which will hold the

complexity of the Nestle Company in an improved way.

With the support of Time-Driven Activity-based costing the costing process becomes

simple because it supports the organization’s management in eliminating events like

interviews and survey and use applicable and significant information.

Organizations can enhance their system of cost management by explaining their

process capacity and application of cost and effectiveness of the orders, customers or

products.

Time-Driven Activity-based Costing method is different because it uses time equation

in which the consumption of time is evaluated on each activity.

This new approach identifies the opportunities for the competencies of the process

and supervision of capacity.

Time-Driven Activity-based Costing (TDABC) method is an exact and profit making

method because it is fast and simple to construct.

TIME-DRIVEN ACTIVITY BASED COSTING

8

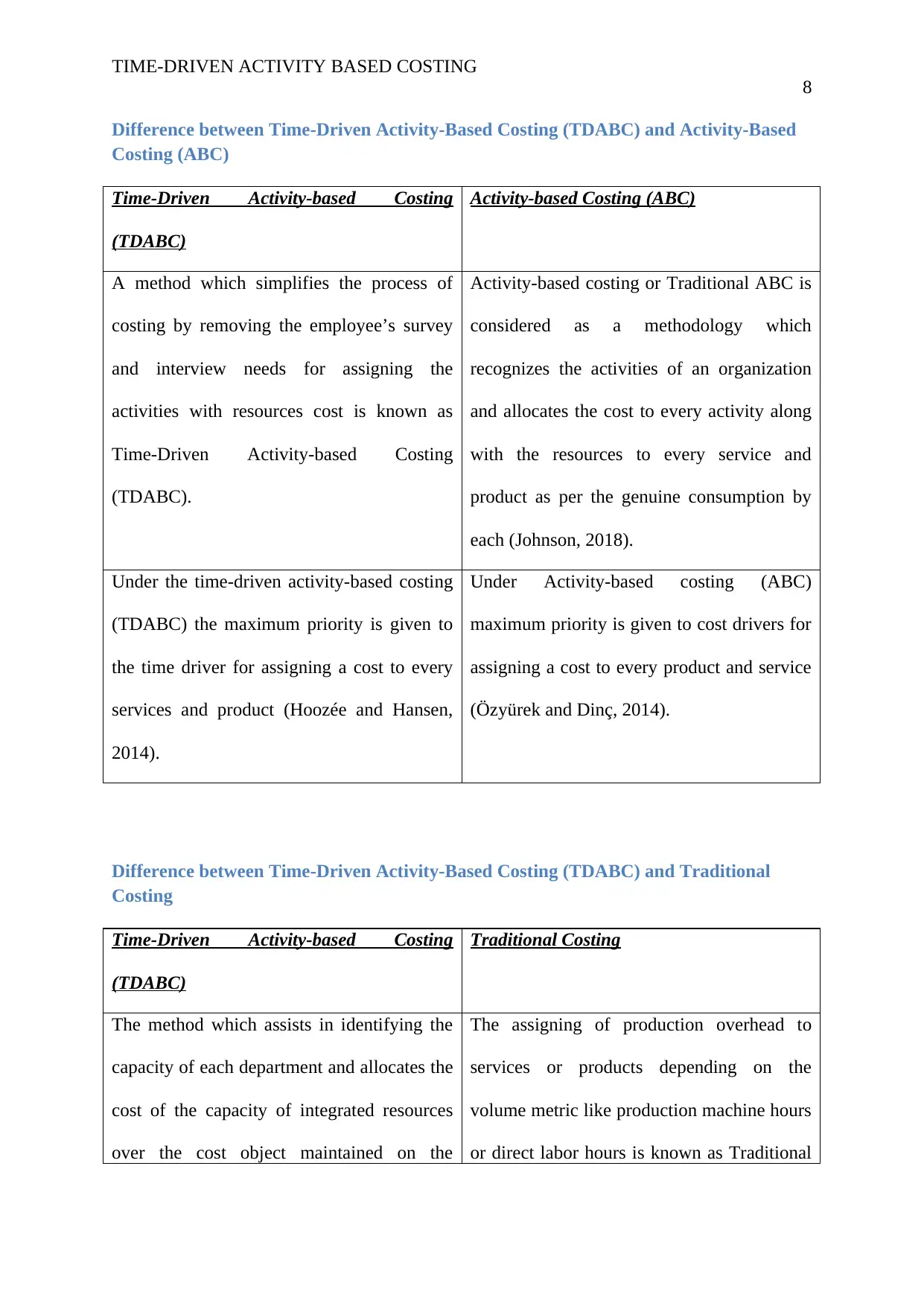

Difference between Time-Driven Activity-Based Costing (TDABC) and Activity-Based

Costing (ABC)

Time-Driven Activity-based Costing

(TDABC)

Activity-based Costing (ABC)

A method which simplifies the process of

costing by removing the employee’s survey

and interview needs for assigning the

activities with resources cost is known as

Time-Driven Activity-based Costing

(TDABC).

Activity-based costing or Traditional ABC is

considered as a methodology which

recognizes the activities of an organization

and allocates the cost to every activity along

with the resources to every service and

product as per the genuine consumption by

each (Johnson, 2018).

Under the time-driven activity-based costing

(TDABC) the maximum priority is given to

the time driver for assigning a cost to every

services and product (Hoozée and Hansen,

2014).

Under Activity-based costing (ABC)

maximum priority is given to cost drivers for

assigning a cost to every product and service

(Özyürek and Dinç, 2014).

Difference between Time-Driven Activity-Based Costing (TDABC) and Traditional

Costing

Time-Driven Activity-based Costing

(TDABC)

Traditional Costing

The method which assists in identifying the

capacity of each department and allocates the

cost of the capacity of integrated resources

over the cost object maintained on the

The assigning of production overhead to

services or products depending on the

volume metric like production machine hours

or direct labor hours is known as Traditional

8

Difference between Time-Driven Activity-Based Costing (TDABC) and Activity-Based

Costing (ABC)

Time-Driven Activity-based Costing

(TDABC)

Activity-based Costing (ABC)

A method which simplifies the process of

costing by removing the employee’s survey

and interview needs for assigning the

activities with resources cost is known as

Time-Driven Activity-based Costing

(TDABC).

Activity-based costing or Traditional ABC is

considered as a methodology which

recognizes the activities of an organization

and allocates the cost to every activity along

with the resources to every service and

product as per the genuine consumption by

each (Johnson, 2018).

Under the time-driven activity-based costing

(TDABC) the maximum priority is given to

the time driver for assigning a cost to every

services and product (Hoozée and Hansen,

2014).

Under Activity-based costing (ABC)

maximum priority is given to cost drivers for

assigning a cost to every product and service

(Özyürek and Dinç, 2014).

Difference between Time-Driven Activity-Based Costing (TDABC) and Traditional

Costing

Time-Driven Activity-based Costing

(TDABC)

Traditional Costing

The method which assists in identifying the

capacity of each department and allocates the

cost of the capacity of integrated resources

over the cost object maintained on the

The assigning of production overhead to

services or products depending on the

volume metric like production machine hours

or direct labor hours is known as Traditional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TIME-DRIVEN ACTIVITY BASED COSTING

9

required time element in order to start an

activity is known as Time-Driven Activity-

based Costing (TDABC).

Costing (Accounting Coach, 2018).

The Time-Driven Activity-based Costing

(TDABC) method is very capacity sensitive

and evaluates the activity’s standard cost

with the support of standard rates.

The traditional costing method allocates

indirect cost provisional to the volume. It

results in product’s cost overvaluation with

high volume; on the other side services or

products become underrated which are of less

volume (Houghton Mifflin Harcourt, 2016).

The new approach is cost saving as it does

not involve more cost in its installation and

implementation, along with this it includes

all different features of a particular activity.

Traditional costing method takes other cost

drivers into account that might be able to

increase the cost of the item (Wilkinson,

2013).

Reason for why Time-Driven Activity-Based Costing is suitable for Nestle Company

The Nestle Company involves various departments in its function of the business who

implement various procedures and activities for appreciating the productivity and

growth of the business. This new approach is created for this type of organization so

that the management can handle every activity and function.

Time-Driven Activity-based Costing (TDABC) is cost saving and easy to implement.

Therefore, this method will not disturb the budget of Nestle Company.

This method is an improved version of Traditional Activity-based Costing and it

supports company in guessing the basis demand of every single customer, product and

9

required time element in order to start an

activity is known as Time-Driven Activity-

based Costing (TDABC).

Costing (Accounting Coach, 2018).

The Time-Driven Activity-based Costing

(TDABC) method is very capacity sensitive

and evaluates the activity’s standard cost

with the support of standard rates.

The traditional costing method allocates

indirect cost provisional to the volume. It

results in product’s cost overvaluation with

high volume; on the other side services or

products become underrated which are of less

volume (Houghton Mifflin Harcourt, 2016).

The new approach is cost saving as it does

not involve more cost in its installation and

implementation, along with this it includes

all different features of a particular activity.

Traditional costing method takes other cost

drivers into account that might be able to

increase the cost of the item (Wilkinson,

2013).

Reason for why Time-Driven Activity-Based Costing is suitable for Nestle Company

The Nestle Company involves various departments in its function of the business who

implement various procedures and activities for appreciating the productivity and

growth of the business. This new approach is created for this type of organization so

that the management can handle every activity and function.

Time-Driven Activity-based Costing (TDABC) is cost saving and easy to implement.

Therefore, this method will not disturb the budget of Nestle Company.

This method is an improved version of Traditional Activity-based Costing and it

supports company in guessing the basis demand of every single customer, product and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TIME-DRIVEN ACTIVITY BASED COSTING

10

procedure with the support of necessary time to attain the events and the cost unit

time capacity.

Conclusion

In the conclusion, it can be suggested that Time-driven Activity-based Costing (TDABC) is

an effective technique or method which estimates the time and cost of the activities

implemented in an organization. This new approach is suitable and appropriate for Nestle

Company because it will help them in increasing their business’s productivity. Along with

this it is an inexpensive method and can be easily installed. As Nestle is the leading company

in the sector of food and beverages, therefore, it is important for the company to have an

improved and enhanced costing system. The above report has explained in detail about the

model of Time-Driven Activity-based Costing and its features along with the brief

description of the Nestle Company. The report has also identified some dissimilarity between

the Time-Driven Activity-based Costing (TDABC) and Activity-based Costing (ABC) and

the differences between Time-Driven Activity-based Costing (TDABC) and Traditional

Costing.

10

procedure with the support of necessary time to attain the events and the cost unit

time capacity.

Conclusion

In the conclusion, it can be suggested that Time-driven Activity-based Costing (TDABC) is

an effective technique or method which estimates the time and cost of the activities

implemented in an organization. This new approach is suitable and appropriate for Nestle

Company because it will help them in increasing their business’s productivity. Along with

this it is an inexpensive method and can be easily installed. As Nestle is the leading company

in the sector of food and beverages, therefore, it is important for the company to have an

improved and enhanced costing system. The above report has explained in detail about the

model of Time-Driven Activity-based Costing and its features along with the brief

description of the Nestle Company. The report has also identified some dissimilarity between

the Time-Driven Activity-based Costing (TDABC) and Activity-based Costing (ABC) and

the differences between Time-Driven Activity-based Costing (TDABC) and Traditional

Costing.

TIME-DRIVEN ACTIVITY BASED COSTING

11

References

Accounting Coach, 2018, Traditional costing definition, Accessed on: 12 January 2018,

Accessed from: https://www.accountingcoach.com/terms/T/traditional-costing

Ayvaz, E., and Pehlivanli, D., 2011, The Use of Time Driven Activity Based Costing and

Analytic Hierarchy Process Method in the Balanced Scorecard Implementation, International

Journal of Business and Management, 6(3), pp. 146-158.

Basuki, B., 2014, The Application of Time-Driven Activity-Based Costing In the Hospitality

Industry: An Exploratory Case Study, JAMAR, 12(1), 27-42.

Hoozée, S., and Hansen, S.C., 2014, A Comparison of Activity-based Costing and Time-

driven Activity-based Costing, Accessed on: 12 January 2018, Accessed from:

https://calhoun.nps.edu/bitstream/handle/10945/47751/Hansen-A-Comparison_2014-08.pdf?

sequence=1

Houghton Mifflin Harcourt, 2016, Activity-Based vs Traditional Costing, Accessed on: 12

January 2018, Accessed from:

https://www.cliffsnotes.com/study-guides/accounting/accounting-principles-ii/activity-based-

costing/activity-based-vs-traditional-costing

Johnson, R., 2018, Traditional Costing Vs. Activity-Based Costing, Accessed on: 12 January

2018, Accessed from: http://smallbusiness.chron.com/traditional-costing-vs-activitybased-

costing-33724.html

Kaplan, R.S., and Amderson, S.R., 2007, Time-driven activity-based costing, Accessed on:

12 January 2018, Accessed from:

https://fenix.tecnico.ulisboa.pt/downloadFile/3779580640677/HBR-Time-Driven

%20Activity-Based%20Costing.pdf

11

References

Accounting Coach, 2018, Traditional costing definition, Accessed on: 12 January 2018,

Accessed from: https://www.accountingcoach.com/terms/T/traditional-costing

Ayvaz, E., and Pehlivanli, D., 2011, The Use of Time Driven Activity Based Costing and

Analytic Hierarchy Process Method in the Balanced Scorecard Implementation, International

Journal of Business and Management, 6(3), pp. 146-158.

Basuki, B., 2014, The Application of Time-Driven Activity-Based Costing In the Hospitality

Industry: An Exploratory Case Study, JAMAR, 12(1), 27-42.

Hoozée, S., and Hansen, S.C., 2014, A Comparison of Activity-based Costing and Time-

driven Activity-based Costing, Accessed on: 12 January 2018, Accessed from:

https://calhoun.nps.edu/bitstream/handle/10945/47751/Hansen-A-Comparison_2014-08.pdf?

sequence=1

Houghton Mifflin Harcourt, 2016, Activity-Based vs Traditional Costing, Accessed on: 12

January 2018, Accessed from:

https://www.cliffsnotes.com/study-guides/accounting/accounting-principles-ii/activity-based-

costing/activity-based-vs-traditional-costing

Johnson, R., 2018, Traditional Costing Vs. Activity-Based Costing, Accessed on: 12 January

2018, Accessed from: http://smallbusiness.chron.com/traditional-costing-vs-activitybased-

costing-33724.html

Kaplan, R.S., and Amderson, S.R., 2007, Time-driven activity-based costing, Accessed on:

12 January 2018, Accessed from:

https://fenix.tecnico.ulisboa.pt/downloadFile/3779580640677/HBR-Time-Driven

%20Activity-Based%20Costing.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.