Analysis of Time-Driven Activity-Based Costing for Volkswagen

VerifiedAdded on 2020/05/28

|12

|2658

|223

Report

AI Summary

This report delves into the concept of Time-Driven Activity-Based Costing (TDABC), exploring its features and contrasting it with traditional and activity-based costing methods. It begins with an overview of the Volkswagen Group, its mission, marketing strategies, and technology. The report then defines TDABC, explaining its core principles, including the use of time equations and capacity cost rates. It highlights the advantages of TDABC, such as its ability to capture activity complexities and its cost-effectiveness. The report also outlines the differences between TDABC, traditional costing, and activity-based costing, emphasizing how TDABC assigns costs based on time drivers. Finally, the report assesses the suitability of TDABC for Volkswagen, considering the company's diverse departments and processes. The conclusion reinforces the effectiveness and appropriateness of TDABC for the company's operational needs.

RRU

Managerial Accounting

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 1

Table of Contents

Introduction...........................................................................................................................................2

Background of Volkswagen Company................................................................................................2

Mission of Volkswagen Group.......................................................................................................3

Marketing Strategy of Volkswagen Group.....................................................................................3

Technology of Volkswagen Group.................................................................................................3

Overview of Time-Driven Activity-Based Costing...............................................................................4

Features of Time-Driven Activity-Based Costing............................................................................6

Differences between Time-Driven Activity-Based Costing, Traditional Costing, and Activity-Based

Costing...............................................................................................................................................7

Suitability of Time-Driven Activity-Based Costing for Volkswagen Company....................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Table of Contents

Introduction...........................................................................................................................................2

Background of Volkswagen Company................................................................................................2

Mission of Volkswagen Group.......................................................................................................3

Marketing Strategy of Volkswagen Group.....................................................................................3

Technology of Volkswagen Group.................................................................................................3

Overview of Time-Driven Activity-Based Costing...............................................................................4

Features of Time-Driven Activity-Based Costing............................................................................6

Differences between Time-Driven Activity-Based Costing, Traditional Costing, and Activity-Based

Costing...............................................................................................................................................7

Suitability of Time-Driven Activity-Based Costing for Volkswagen Company....................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

MANAGERIAL ACCOUNTING 2

Introduction

The report is being prepared to identify the concept of Time-Driven Activity-Based Costing

and its features. Along with this, it will explain the difference between Time-Driven Activity-

Based Costing, Traditional Costing, and Activity-Based Costing. Further, the report will

assist Volkswagen Company a client of management consultancy firm in identifying whether

the Time-Driven Activity-based Costing is appropriate for their company's environment and

processes or not.

Background of Volkswagen Company

The Volkswagen AG is internationally known as Volkswagen Group. It is a German

company deal in the manufacturing of automotive automobiles and has it's headquartered in

Wolfsburg, Germany. Commercial and turbomachinery are designed and manufactured by

this company and along with this they also offer related services such as fleet management,

leasing, and financing. In 2016, the company overtake the Toyota Company and became the

largest automaker in the world by sales. For over two decades it has been successful in

maintaining Europe’s largest market share. In 2016, the company was declared as world's

second-biggest manufacturer vehicles in the automobile industry by the report of

Organization Internationale des Cosntructeurs d’Automobiles. According to the production

volume, the second biggest automobile manufacturer is Volkswagen Group, behind Toyota.

The passenger cars sold by Volkswagen Group under the Lamborgini, SEAT, Bentley,

Skoda, Audi, Volkswagen marques, Porsche, and Bugatti; marques MAN, Scania brand

under commercial vehicles and Ducati brand under motorcycles.

Introduction

The report is being prepared to identify the concept of Time-Driven Activity-Based Costing

and its features. Along with this, it will explain the difference between Time-Driven Activity-

Based Costing, Traditional Costing, and Activity-Based Costing. Further, the report will

assist Volkswagen Company a client of management consultancy firm in identifying whether

the Time-Driven Activity-based Costing is appropriate for their company's environment and

processes or not.

Background of Volkswagen Company

The Volkswagen AG is internationally known as Volkswagen Group. It is a German

company deal in the manufacturing of automotive automobiles and has it's headquartered in

Wolfsburg, Germany. Commercial and turbomachinery are designed and manufactured by

this company and along with this they also offer related services such as fleet management,

leasing, and financing. In 2016, the company overtake the Toyota Company and became the

largest automaker in the world by sales. For over two decades it has been successful in

maintaining Europe’s largest market share. In 2016, the company was declared as world's

second-biggest manufacturer vehicles in the automobile industry by the report of

Organization Internationale des Cosntructeurs d’Automobiles. According to the production

volume, the second biggest automobile manufacturer is Volkswagen Group, behind Toyota.

The passenger cars sold by Volkswagen Group under the Lamborgini, SEAT, Bentley,

Skoda, Audi, Volkswagen marques, Porsche, and Bugatti; marques MAN, Scania brand

under commercial vehicles and Ducati brand under motorcycles.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 3

Mission of Volkswagen Group

The mission of the group is to offer vehicles with safe, attractive and environmentally sound

features, which can survive in a competitive and tough market and set standards in the world.

Marketing Strategy of Volkswagen Group

The major focus of the company is towards increasing their core business by enhancing

productivity and decreasing production cost. In order to achieve following goals, the

company is concentrating on various strategies such as divestment of non-core segments, new

models introduction, and restructuring. The aim of the Volkswagen Group is to provide

products with good quality, safe environment, and enhanced productivity. The company has

adopted Double marketing strategy for the brand positioning. The meaning of Double

marketing is not spreading numerous messages in a single campaign, but various messages in

multiple campaigns are promoted parallel. The company who followed this strategy is Coke

due to the presence of high budget of marketing. In that campaign, various ads were

promoted at the same time but the outcomes of those campaigns were not positive.

The concentration of Volkswagen Group is on the easy obtainability of the vehicles for this

they have established 44 manufacturing sites in various countries of the world. Products

branding in different sections of manufacturing lines is the Volkswagen Group’s marketing

strategies.

Technology of Volkswagen Group

Blueprinting technology is used by Volkswagen Group which means the science of engine

reconstructing. In the blueprinting process balancing, carefully fitting, and measuring is being

performed which create an engine for performance enhancement. The Blueprinting process

involves setting all receiving the engine to its best value. The technologies which are used by

Mission of Volkswagen Group

The mission of the group is to offer vehicles with safe, attractive and environmentally sound

features, which can survive in a competitive and tough market and set standards in the world.

Marketing Strategy of Volkswagen Group

The major focus of the company is towards increasing their core business by enhancing

productivity and decreasing production cost. In order to achieve following goals, the

company is concentrating on various strategies such as divestment of non-core segments, new

models introduction, and restructuring. The aim of the Volkswagen Group is to provide

products with good quality, safe environment, and enhanced productivity. The company has

adopted Double marketing strategy for the brand positioning. The meaning of Double

marketing is not spreading numerous messages in a single campaign, but various messages in

multiple campaigns are promoted parallel. The company who followed this strategy is Coke

due to the presence of high budget of marketing. In that campaign, various ads were

promoted at the same time but the outcomes of those campaigns were not positive.

The concentration of Volkswagen Group is on the easy obtainability of the vehicles for this

they have established 44 manufacturing sites in various countries of the world. Products

branding in different sections of manufacturing lines is the Volkswagen Group’s marketing

strategies.

Technology of Volkswagen Group

Blueprinting technology is used by Volkswagen Group which means the science of engine

reconstructing. In the blueprinting process balancing, carefully fitting, and measuring is being

performed which create an engine for performance enhancement. The Blueprinting process

involves setting all receiving the engine to its best value. The technologies which are used by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 4

the Volkswagen Group are environment-friendly and for this, they utilize recycled and

recyclable ingredients whenever possible. These strategies of the company help them in

increasing their market share, trust, and loyalty of the customers.

Overview of Time-Driven Activity-Based Costing

The time-Driven Activity-Based Costing method is implemented in order to overcome the

difficulties faced by the traditional ABC in changing the environment and to grab the full

activities complexity. Anderson and Kaplan are the developers of the new method or

approach for ABC and named it as Time-Driven Activity-based Costing. Under this

approach, time plays important role in distributing resources to the cost objects. Though

conservative ABC constantly had the dimension to make use of cost driver i.e. time, which

perform a different role in ABC’s new version. Traditional ABC method apply duration

drivers in the second stage of a cost allocation process, whereas the new approach uses the

time to drive costs directly from resources to cost objects, passing over the stage of first

assigning a department's resource costs to the multiple activities the department performs

(Janes and Succi, 2014). Therefore, with Time-Driven Activity-based costing, resources are

not allocated to particular activities; they are shared at a greater level. For every section or

procedure, costs of the resource are assigned directly to the cost objects with the help of two

estimates set and they are - the process time and cost per time unit. In place of cost per time

unit capacity cost rate can be used and process time can be calculated by time equation.

In this method, capacity cost rate is calculated first as overhead is divided by applied

capacity. The resources cost delivered to the operating department comprises of numerous

elements: employees, equipment, indirect labor, supervision, technology and equipment,

possession and other various indirect and support resources (Kaplan and Anderson, 2017).

The applied capacity which has been provided is the available time for creative work and can

the Volkswagen Group are environment-friendly and for this, they utilize recycled and

recyclable ingredients whenever possible. These strategies of the company help them in

increasing their market share, trust, and loyalty of the customers.

Overview of Time-Driven Activity-Based Costing

The time-Driven Activity-Based Costing method is implemented in order to overcome the

difficulties faced by the traditional ABC in changing the environment and to grab the full

activities complexity. Anderson and Kaplan are the developers of the new method or

approach for ABC and named it as Time-Driven Activity-based Costing. Under this

approach, time plays important role in distributing resources to the cost objects. Though

conservative ABC constantly had the dimension to make use of cost driver i.e. time, which

perform a different role in ABC’s new version. Traditional ABC method apply duration

drivers in the second stage of a cost allocation process, whereas the new approach uses the

time to drive costs directly from resources to cost objects, passing over the stage of first

assigning a department's resource costs to the multiple activities the department performs

(Janes and Succi, 2014). Therefore, with Time-Driven Activity-based costing, resources are

not allocated to particular activities; they are shared at a greater level. For every section or

procedure, costs of the resource are assigned directly to the cost objects with the help of two

estimates set and they are - the process time and cost per time unit. In place of cost per time

unit capacity cost rate can be used and process time can be calculated by time equation.

In this method, capacity cost rate is calculated first as overhead is divided by applied

capacity. The resources cost delivered to the operating department comprises of numerous

elements: employees, equipment, indirect labor, supervision, technology and equipment,

possession and other various indirect and support resources (Kaplan and Anderson, 2017).

The applied capacity which has been provided is the available time for creative work and can

MANAGERIAL ACCOUNTING 5

be acquired by eliminating inevitable ineptitudes from the hypothetical capacity; according to

the rule of thumb rule, it is normally expected to be 80 to 85 % of hypothetical capacity.

Though capacity is frequently measured in hours or minutes delivered, along with this it can

also be evaluated in other elements, such as gigabytes, weight or space. It must be noted that

the cost rate of the department is usable only if the resources mix delivered is almost same for

every action and deal executed within the section of the business.

If a department executes numerous procedures, each demanding various resources, then the

organization’s section must decompose operations of the department into more than two

processes and evaluate cost rate of separate capacity for every process (Kaplan and Anderson,

2007). As a final point, superior treatment is needed for the handling of resources seasonal or

peak capacity. More precisely, the slack period’s capacity cost should be the capacity that

will be essential if only the demand of the slack-period were to be achieved; the cost rate of

capacity in the peak months must be more costly and contain both the cost of delivering

capacity throughout the peak months along with the cost of capacity resources delivered, but

not needed, for the period of slack-demand.

Second, time equation is used in the Time-Driven Activity-based Costing in order to estimate

the usage of resources and cost of assigned resources to the activities which are performed

and processed transactions. A mathematical equation which states the required time in order

to perform a definite activity as a task of numerous time drivers, which can be distinct, dual

or continuous variables is known as Time equation (Namazi, 2016). For every transaction,

this type of time equation is utilized to define the required time to accomplish the activity.

Officially, the expected deal time based on k noticeable time drivers is stated as:

Tk = B0 + B1 X1 + …+ Bk Xk

with

be acquired by eliminating inevitable ineptitudes from the hypothetical capacity; according to

the rule of thumb rule, it is normally expected to be 80 to 85 % of hypothetical capacity.

Though capacity is frequently measured in hours or minutes delivered, along with this it can

also be evaluated in other elements, such as gigabytes, weight or space. It must be noted that

the cost rate of the department is usable only if the resources mix delivered is almost same for

every action and deal executed within the section of the business.

If a department executes numerous procedures, each demanding various resources, then the

organization’s section must decompose operations of the department into more than two

processes and evaluate cost rate of separate capacity for every process (Kaplan and Anderson,

2007). As a final point, superior treatment is needed for the handling of resources seasonal or

peak capacity. More precisely, the slack period’s capacity cost should be the capacity that

will be essential if only the demand of the slack-period were to be achieved; the cost rate of

capacity in the peak months must be more costly and contain both the cost of delivering

capacity throughout the peak months along with the cost of capacity resources delivered, but

not needed, for the period of slack-demand.

Second, time equation is used in the Time-Driven Activity-based Costing in order to estimate

the usage of resources and cost of assigned resources to the activities which are performed

and processed transactions. A mathematical equation which states the required time in order

to perform a definite activity as a task of numerous time drivers, which can be distinct, dual

or continuous variables is known as Time equation (Namazi, 2016). For every transaction,

this type of time equation is utilized to define the required time to accomplish the activity.

Officially, the expected deal time based on k noticeable time drivers is stated as:

Tk = B0 + B1 X1 + …+ Bk Xk

with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 6

Tk = expected time for a specific transaction;

B0 = expected basic time, provided by the employees;

Bi = estimation of time of driver i, provided by the employees, with i= 1,….,k;

Xi = volume estimation of time driver i, as stated by the computer built information system of

the company, with i= 1,…,k. (Mitchell and Nørreklit, Jakobsen, 2013)

Features of Time-Driven Activity-Based Costing

The Time-Driven Activity-based Costing method is very precise and gainful model

which is fast, low-cost, and easy to construct.

Another feature of this method is a combination of the comprehensive transactional

data is obtainable from ERP and system of customer relationship management.

It is a model which helps in recognizing opportunities for the procedure competencies

and capacity supervision.

A model of costing is depending on the transactions precise of orders of individual,

procedures, customers and suppliers.

Another feature of this method is predictions of the demands of resource, permitting

companies to budget for the needed capacity in order to handle the production and

sales assessments in their tactical plans (Weirich, 2017).

Time-Driven Activity-based Costing is simply accessible across extremely varied and

multifaceted enterprises by accessible software presentations and database

technologies.

It is a model which is easy and reasonable to update as variations arise in course

competencies and cost of the course.

Tk = expected time for a specific transaction;

B0 = expected basic time, provided by the employees;

Bi = estimation of time of driver i, provided by the employees, with i= 1,….,k;

Xi = volume estimation of time driver i, as stated by the computer built information system of

the company, with i= 1,…,k. (Mitchell and Nørreklit, Jakobsen, 2013)

Features of Time-Driven Activity-Based Costing

The Time-Driven Activity-based Costing method is very precise and gainful model

which is fast, low-cost, and easy to construct.

Another feature of this method is a combination of the comprehensive transactional

data is obtainable from ERP and system of customer relationship management.

It is a model which helps in recognizing opportunities for the procedure competencies

and capacity supervision.

A model of costing is depending on the transactions precise of orders of individual,

procedures, customers and suppliers.

Another feature of this method is predictions of the demands of resource, permitting

companies to budget for the needed capacity in order to handle the production and

sales assessments in their tactical plans (Weirich, 2017).

Time-Driven Activity-based Costing is simply accessible across extremely varied and

multifaceted enterprises by accessible software presentations and database

technologies.

It is a model which is easy and reasonable to update as variations arise in course

competencies and cost of the course.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 7

It is considered as a common method for profitability and cost management which can

be utilized in all type of industries with difficulty in channels, processes, customers,

segments, and products, and huge expenditures for capital and people.

Differences between Time-Driven Activity-Based Costing, Traditional Costing, and

Activity-Based Costing

Time-Driven Activity-Based

Costing

Traditional Costing Activity-Based Costing

Time-Driven Activity-based

costing helps in recognizing

every department's capacity

and assigns the capacity cost

of the combined resources

over the cost object

established on the required

time to implement an

activity.

Traditional costing is the

factory overhead allocation

to products depending on the

production resources which

are consumed. In this

method, overhead is

frequently applied depending

on the number of hours

consumed of direct labor or

machine hours used

(Wilkinson, 2013).

Activity-based Costing

method which recognizes

actions in an organization

and allocates the cost of

every activity with all

services and products

resources according to the

definite consumption by each

(Coulter, McGrath and

Anthony, 2011).

Time-Driven Activity-based

Costing gives importance to

the time drivers for allocating

costs to services and

products.

Traditional Costing makes

use of distinct pool overhead

and is not capable to compute

the accurate cost (Hayden,

2017).

Activity-based costing gives

importance to cost drivers for

allocating costs to services

and products (Kaplan and

Anderson, 2006).

This method is less

expensive as compared to

This method invalids the

other important cost drivers

This method is very costly as

well as time-consuming to

It is considered as a common method for profitability and cost management which can

be utilized in all type of industries with difficulty in channels, processes, customers,

segments, and products, and huge expenditures for capital and people.

Differences between Time-Driven Activity-Based Costing, Traditional Costing, and

Activity-Based Costing

Time-Driven Activity-Based

Costing

Traditional Costing Activity-Based Costing

Time-Driven Activity-based

costing helps in recognizing

every department's capacity

and assigns the capacity cost

of the combined resources

over the cost object

established on the required

time to implement an

activity.

Traditional costing is the

factory overhead allocation

to products depending on the

production resources which

are consumed. In this

method, overhead is

frequently applied depending

on the number of hours

consumed of direct labor or

machine hours used

(Wilkinson, 2013).

Activity-based Costing

method which recognizes

actions in an organization

and allocates the cost of

every activity with all

services and products

resources according to the

definite consumption by each

(Coulter, McGrath and

Anthony, 2011).

Time-Driven Activity-based

Costing gives importance to

the time drivers for allocating

costs to services and

products.

Traditional Costing makes

use of distinct pool overhead

and is not capable to compute

the accurate cost (Hayden,

2017).

Activity-based costing gives

importance to cost drivers for

allocating costs to services

and products (Kaplan and

Anderson, 2006).

This method is less

expensive as compared to

This method invalids the

other important cost drivers

This method is very costly as

well as time-consuming to

MANAGERIAL ACCOUNTING 8

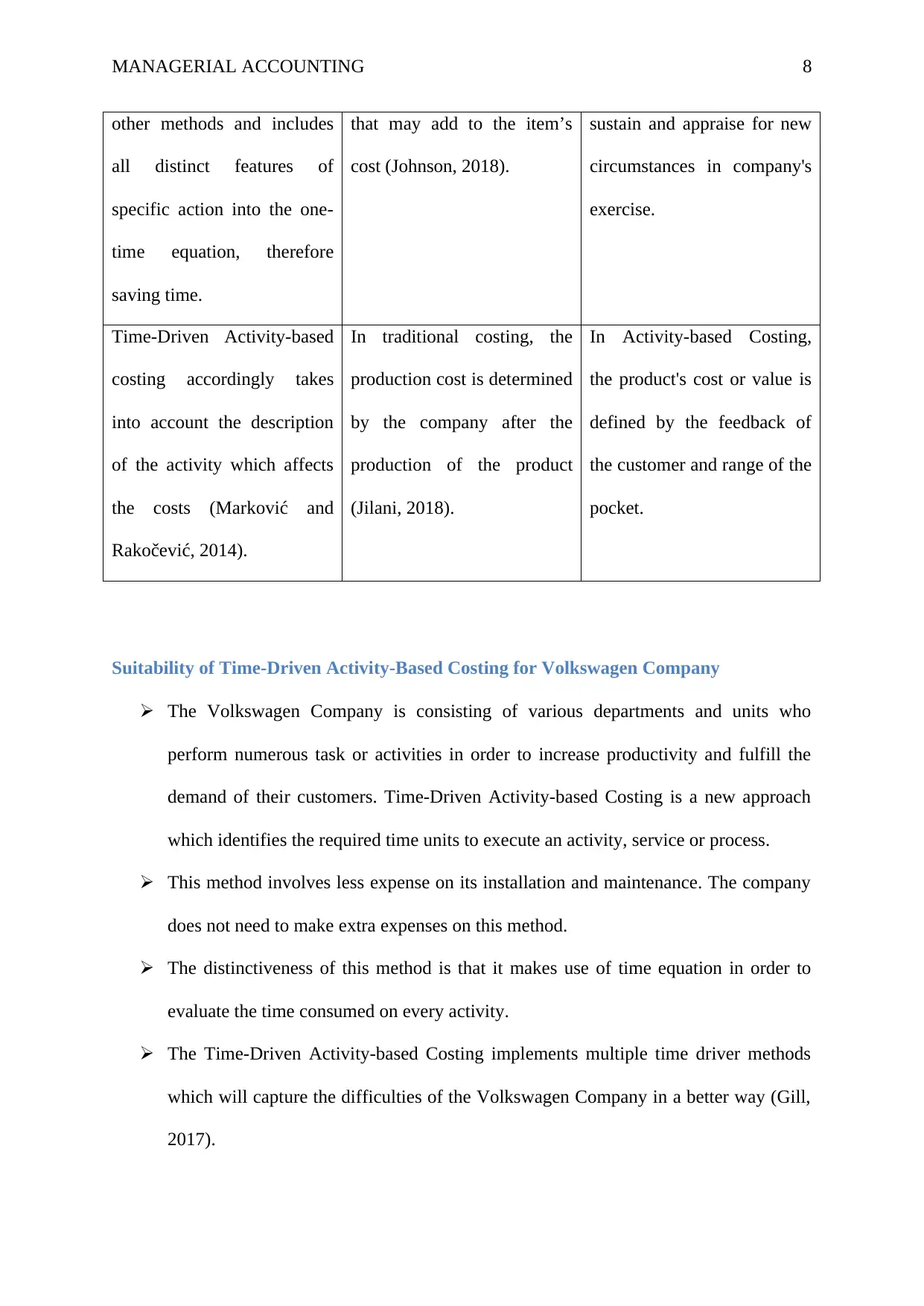

other methods and includes

all distinct features of

specific action into the one-

time equation, therefore

saving time.

that may add to the item’s

cost (Johnson, 2018).

sustain and appraise for new

circumstances in company's

exercise.

Time-Driven Activity-based

costing accordingly takes

into account the description

of the activity which affects

the costs (Marković and

Rakočević, 2014).

In traditional costing, the

production cost is determined

by the company after the

production of the product

(Jilani, 2018).

In Activity-based Costing,

the product's cost or value is

defined by the feedback of

the customer and range of the

pocket.

Suitability of Time-Driven Activity-Based Costing for Volkswagen Company

The Volkswagen Company is consisting of various departments and units who

perform numerous task or activities in order to increase productivity and fulfill the

demand of their customers. Time-Driven Activity-based Costing is a new approach

which identifies the required time units to execute an activity, service or process.

This method involves less expense on its installation and maintenance. The company

does not need to make extra expenses on this method.

The distinctiveness of this method is that it makes use of time equation in order to

evaluate the time consumed on every activity.

The Time-Driven Activity-based Costing implements multiple time driver methods

which will capture the difficulties of the Volkswagen Company in a better way (Gill,

2017).

other methods and includes

all distinct features of

specific action into the one-

time equation, therefore

saving time.

that may add to the item’s

cost (Johnson, 2018).

sustain and appraise for new

circumstances in company's

exercise.

Time-Driven Activity-based

costing accordingly takes

into account the description

of the activity which affects

the costs (Marković and

Rakočević, 2014).

In traditional costing, the

production cost is determined

by the company after the

production of the product

(Jilani, 2018).

In Activity-based Costing,

the product's cost or value is

defined by the feedback of

the customer and range of the

pocket.

Suitability of Time-Driven Activity-Based Costing for Volkswagen Company

The Volkswagen Company is consisting of various departments and units who

perform numerous task or activities in order to increase productivity and fulfill the

demand of their customers. Time-Driven Activity-based Costing is a new approach

which identifies the required time units to execute an activity, service or process.

This method involves less expense on its installation and maintenance. The company

does not need to make extra expenses on this method.

The distinctiveness of this method is that it makes use of time equation in order to

evaluate the time consumed on every activity.

The Time-Driven Activity-based Costing implements multiple time driver methods

which will capture the difficulties of the Volkswagen Company in a better way (Gill,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 9

Conclusion

Time-Driven Activity-Based Costing is very effective and inexpensive as compared to other

methods of costing. The important aspect of this method is that it takes into account the most

important cost driver i.e. time. The above report has provided the detail description of the

Volkswagen Group along with the concept of Time-Driven Activity-based Costing and its

features. It has also explained the difference between Time-Driven Activity-based Costing,

Traditional Costing, and Activity-based Costing. Further, the report has also reflected the

reasons why Time-Driven Activity-based Costing method is suitable for Volkswagen Group.

Volkswagen is well-known and one of the leading automobile companies in the world, which

involve various process and activities in its business operations. Therefore, Time-Driven

Activity-based Costing is very beneficiary for this company.

Conclusion

Time-Driven Activity-Based Costing is very effective and inexpensive as compared to other

methods of costing. The important aspect of this method is that it takes into account the most

important cost driver i.e. time. The above report has provided the detail description of the

Volkswagen Group along with the concept of Time-Driven Activity-based Costing and its

features. It has also explained the difference between Time-Driven Activity-based Costing,

Traditional Costing, and Activity-based Costing. Further, the report has also reflected the

reasons why Time-Driven Activity-based Costing method is suitable for Volkswagen Group.

Volkswagen is well-known and one of the leading automobile companies in the world, which

involve various process and activities in its business operations. Therefore, Time-Driven

Activity-based Costing is very beneficiary for this company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 10

References

Mitchell, F., and Nørreklit, H., Jakobsen, M., 2013, The Routledge Companion to Cost

Management, Routledge.

Kaplan, R.S., and Anderson, S.R., 2017, Time-Driven Activity-Based Costing, Accessed on:

11 January 2018, Accessed from: https://hbr.org/2004/11/time-driven-activity-based-costing

Kaplan, R.S., and Anderson, S.R., 2006, Time-Driven Activity-Based Costing, Accessed on:

11 January 2018, Accessed from: https://hbswk.hbs.edu/item/time-driven-activity-based-

costing

Gill, S., 2017, Cost and Management Accounting: Fundamentals and its Applications, Vikas

Publishing House.

Janes, A., and Succi, G., 2014, Lean Software Development in Action, Springer.

Marković, A., and Rakočević, S.B., 2014, Proceedings of the xiv international symposium

symorg 2014: new business models and sustainable competitiveness, FON.

Kaplan, R.S. and Anderson, S.R., 2007, Time-Driven Activity-Based Costing: A Simpler and

More Powerful Path to Higher Profits, Harvard Business Press.

Hayden, A., 2017, Activity-Based vs. Traditional Costing, Accessed on: 11 January 2018,

Accessed from: https://quickbooks.intuit.com/r/pricing-strategy/activity-based-vs-traditional-

costing/

Jilani, 2018, Difference Between ABC and Traditional Costing, Accessed on: 11 January

2018, Accessed from:

http://www.differencebetween.net/business/finance-business-2/difference-between-abc-and-

traditional-costing/

References

Mitchell, F., and Nørreklit, H., Jakobsen, M., 2013, The Routledge Companion to Cost

Management, Routledge.

Kaplan, R.S., and Anderson, S.R., 2017, Time-Driven Activity-Based Costing, Accessed on:

11 January 2018, Accessed from: https://hbr.org/2004/11/time-driven-activity-based-costing

Kaplan, R.S., and Anderson, S.R., 2006, Time-Driven Activity-Based Costing, Accessed on:

11 January 2018, Accessed from: https://hbswk.hbs.edu/item/time-driven-activity-based-

costing

Gill, S., 2017, Cost and Management Accounting: Fundamentals and its Applications, Vikas

Publishing House.

Janes, A., and Succi, G., 2014, Lean Software Development in Action, Springer.

Marković, A., and Rakočević, S.B., 2014, Proceedings of the xiv international symposium

symorg 2014: new business models and sustainable competitiveness, FON.

Kaplan, R.S. and Anderson, S.R., 2007, Time-Driven Activity-Based Costing: A Simpler and

More Powerful Path to Higher Profits, Harvard Business Press.

Hayden, A., 2017, Activity-Based vs. Traditional Costing, Accessed on: 11 January 2018,

Accessed from: https://quickbooks.intuit.com/r/pricing-strategy/activity-based-vs-traditional-

costing/

Jilani, 2018, Difference Between ABC and Traditional Costing, Accessed on: 11 January

2018, Accessed from:

http://www.differencebetween.net/business/finance-business-2/difference-between-abc-and-

traditional-costing/

MANAGERIAL ACCOUNTING 11

Johnson, R., 2018, Traditional Costing Vs. Activity-Based Costing, Accessed on: 11 January

2018, Accessed from: http://smallbusiness.chron.com/traditional-costing-vs-activitybased-

costing-33724.html

Wilkinson, J., 2013, Activity-based Costing (ABC) vs Traditional Costing, Accessed on: 11

January 2018, Accessed from: https://strategiccfo.com/activity-based-costing-abc-vs-

traditional-costing/

Namazi, M., 2016, Time-driven activity-based costing: Theory, applications and limitations,

Iranian Journal of Management Studies, 9(3), pp. 457-482.

Weirich, T., 2017, Why is Time-Driven Activity-Based Costing such a game changer?

Accessed on: 11 January 2018, Accessed from:

https://finance.toolbox.com/blogs/torstenweirich/why-is-time-driven-activity-based-costing-

such-a-game-changer-100110

Coulter, D., McGrath, G., and Anthony., 2011, Time-driven activity-based costing, Accessed

on: 11 January 2018, Accessed from: http://www.gaaaccounting.com/time-driven-activity-

based-costing/

Szychta, A., 2010, Time-Driven Activity-Based Costing in Service Industries, Accessed on:

11 January 2018, Accessed from:

https://www.researchgate.net/publication/267373766_Time-Driven_Activity-

Based_Costing_in_Service_Industries

Johnson, R., 2018, Traditional Costing Vs. Activity-Based Costing, Accessed on: 11 January

2018, Accessed from: http://smallbusiness.chron.com/traditional-costing-vs-activitybased-

costing-33724.html

Wilkinson, J., 2013, Activity-based Costing (ABC) vs Traditional Costing, Accessed on: 11

January 2018, Accessed from: https://strategiccfo.com/activity-based-costing-abc-vs-

traditional-costing/

Namazi, M., 2016, Time-driven activity-based costing: Theory, applications and limitations,

Iranian Journal of Management Studies, 9(3), pp. 457-482.

Weirich, T., 2017, Why is Time-Driven Activity-Based Costing such a game changer?

Accessed on: 11 January 2018, Accessed from:

https://finance.toolbox.com/blogs/torstenweirich/why-is-time-driven-activity-based-costing-

such-a-game-changer-100110

Coulter, D., McGrath, G., and Anthony., 2011, Time-driven activity-based costing, Accessed

on: 11 January 2018, Accessed from: http://www.gaaaccounting.com/time-driven-activity-

based-costing/

Szychta, A., 2010, Time-Driven Activity-Based Costing in Service Industries, Accessed on:

11 January 2018, Accessed from:

https://www.researchgate.net/publication/267373766_Time-Driven_Activity-

Based_Costing_in_Service_Industries

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.