Time Series Analysis and Forecasting of GD Stock Returns (Finance)

VerifiedAdded on 2023/01/16

|19

|3936

|100

Project

AI Summary

This project report analyzes the relationship between General Dynamics (GD) stock returns and the S&P 500 market returns using time series analysis. The analysis covers a four-year period from April 2015 to March 2019, utilizing descriptive statistics, graphical representations like time series plots and histograms for both GD stock and S&P 500 returns, including squared and absolute returns. The study employs multiple linear regression to model the dependence of GD's returns on its past returns and market returns, determining the appropriate number of lags through misspecification tests. The report constructs and evaluates autoregressive (AR) models to forecast GD stock returns, assessing the significance of lags and performing the Breusch-Godfrey test for autocorrelation to ensure model adequacy. The findings reveal insights into the volatility and skewness of GD stock returns compared to the market, and the study concludes with a statistically significant AR model and forecasting.

Time Series Modelling with Auto Regression Model and Forecasting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present report scrutinizes the relationship between the market return (S&P 500) and a

company’s return. General Dynamics (GD) has been selected as the company in the research.

Monthly market returns of GD and S&P 500 have been collected from Yahoo finance for a

period of four years. The time period of returns is 01-04-2015 to 01-03-2019. Market return

of S&P 500 has been described using descriptive any graphical methods. In second part of the

report the dependence of GD’s return on previous returns and previous market returns has

been assessed choosing significant number of lags. At last, an auto-regressive model has been

constructed with monthly returns of GD stock.

2

The present report scrutinizes the relationship between the market return (S&P 500) and a

company’s return. General Dynamics (GD) has been selected as the company in the research.

Monthly market returns of GD and S&P 500 have been collected from Yahoo finance for a

period of four years. The time period of returns is 01-04-2015 to 01-03-2019. Market return

of S&P 500 has been described using descriptive any graphical methods. In second part of the

report the dependence of GD’s return on previous returns and previous market returns has

been assessed choosing significant number of lags. At last, an auto-regressive model has been

constructed with monthly returns of GD stock.

2

Part A

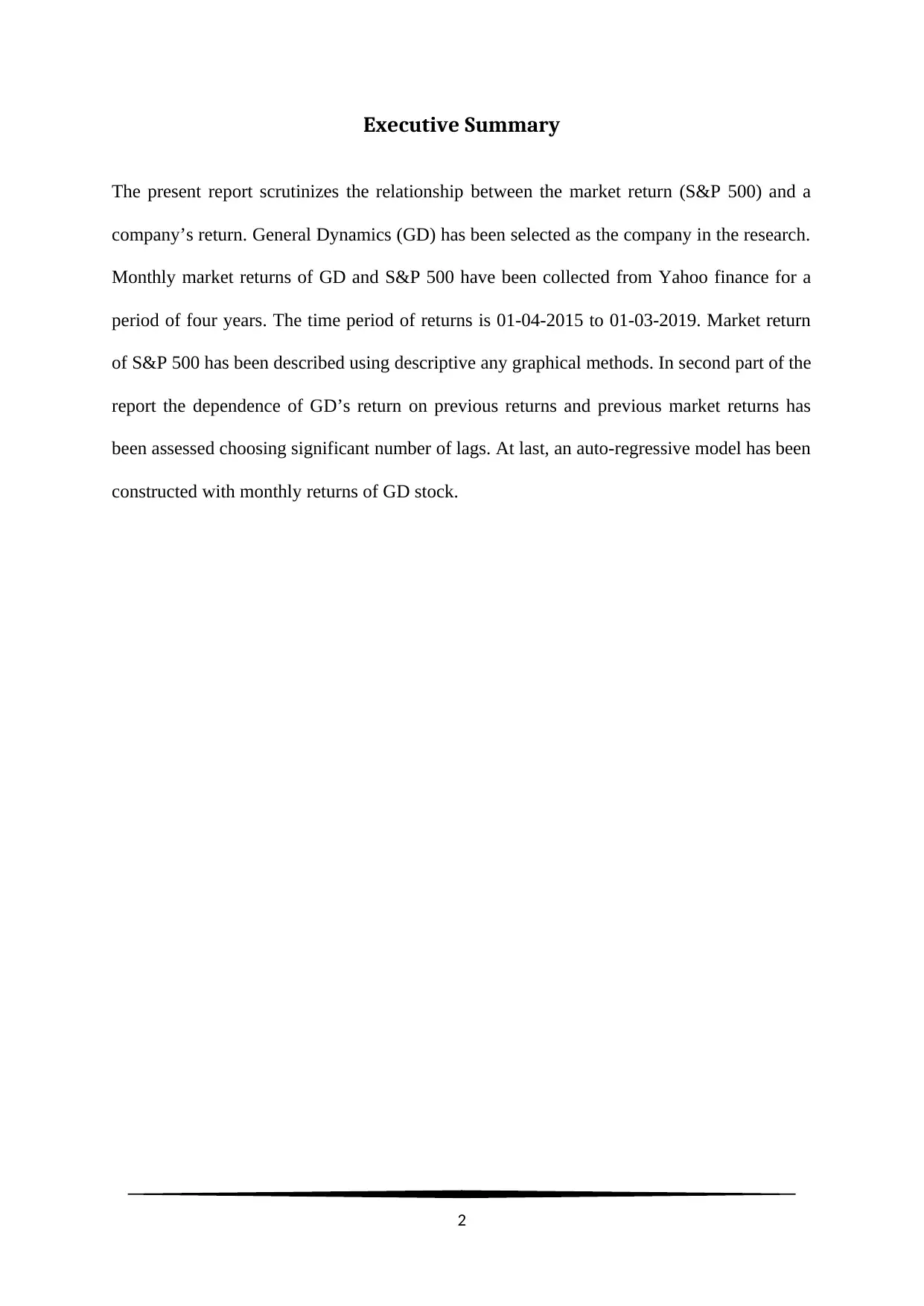

a) Time series plots and histograms have been constructed for monthly returns of GD stock.

Square of monthly returns, and absolute market returns have also been presented in time

series and histogram plots (Montgomery, Jennings, and Kulahci, 2016).

Figure 1: Time Series plot of monthly return on GD stock from 01-05-2015 to 01-03-2019

Figure 2: Histogram for monthly return on GD stock from 01-05-2015 to 01-03-2019

3

a) Time series plots and histograms have been constructed for monthly returns of GD stock.

Square of monthly returns, and absolute market returns have also been presented in time

series and histogram plots (Montgomery, Jennings, and Kulahci, 2016).

Figure 1: Time Series plot of monthly return on GD stock from 01-05-2015 to 01-03-2019

Figure 2: Histogram for monthly return on GD stock from 01-05-2015 to 01-03-2019

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

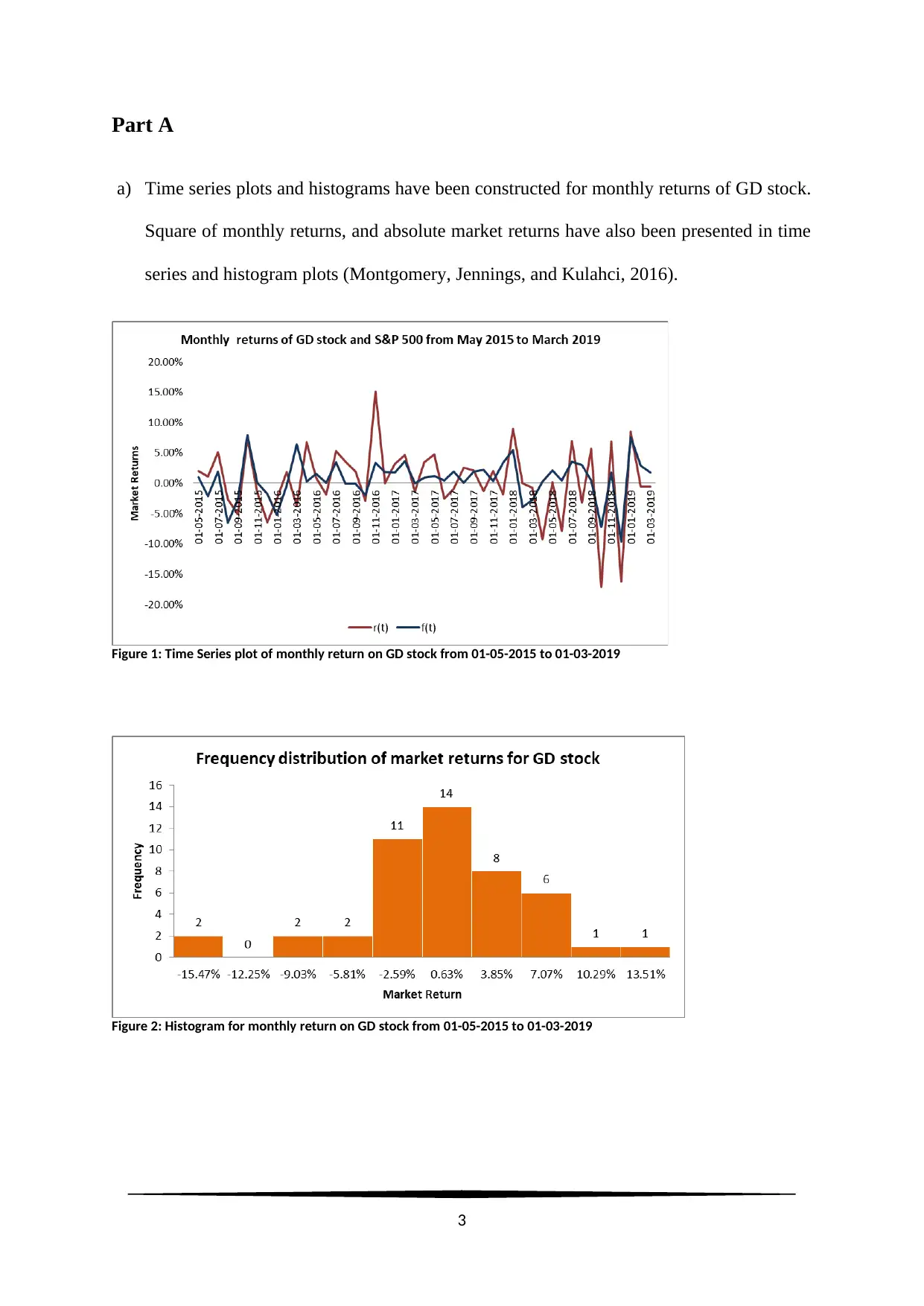

Figure 3: Time Series plot of square of monthly return on GD stock from 01-05-2015 to 01-03-2019

Figure 4: Histogram for square of monthly return on GD stock from 01-05-2015 to 01-03-2019

4

Figure 4: Histogram for square of monthly return on GD stock from 01-05-2015 to 01-03-2019

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

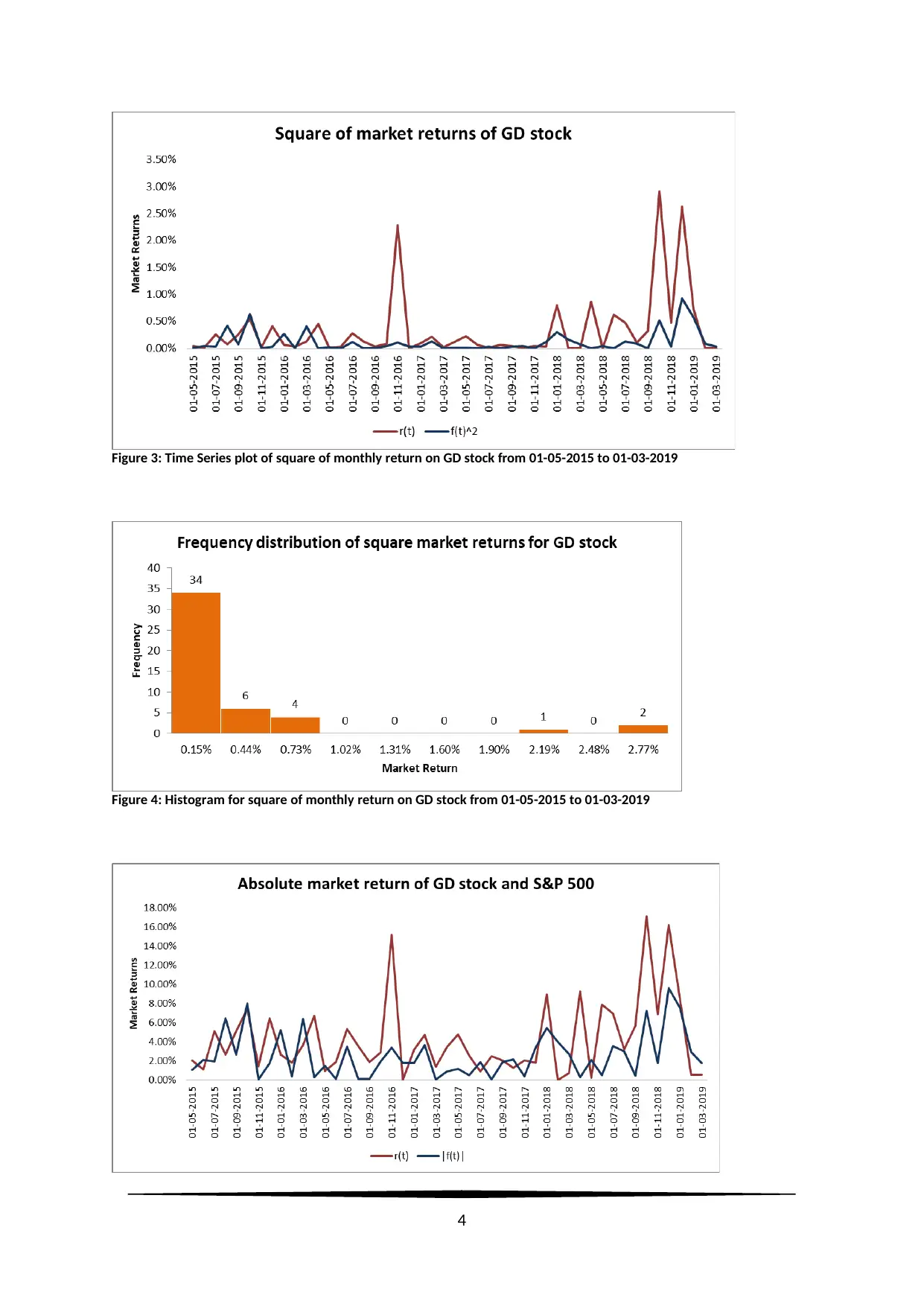

Figure 5: Time Series plot of absolute monthly return on GD stock from 01-05-2015 to 01-03-2019

Figure 6: Histogram for absolute monthly return on GD stock from 01-05-2015 to 01-03-2019

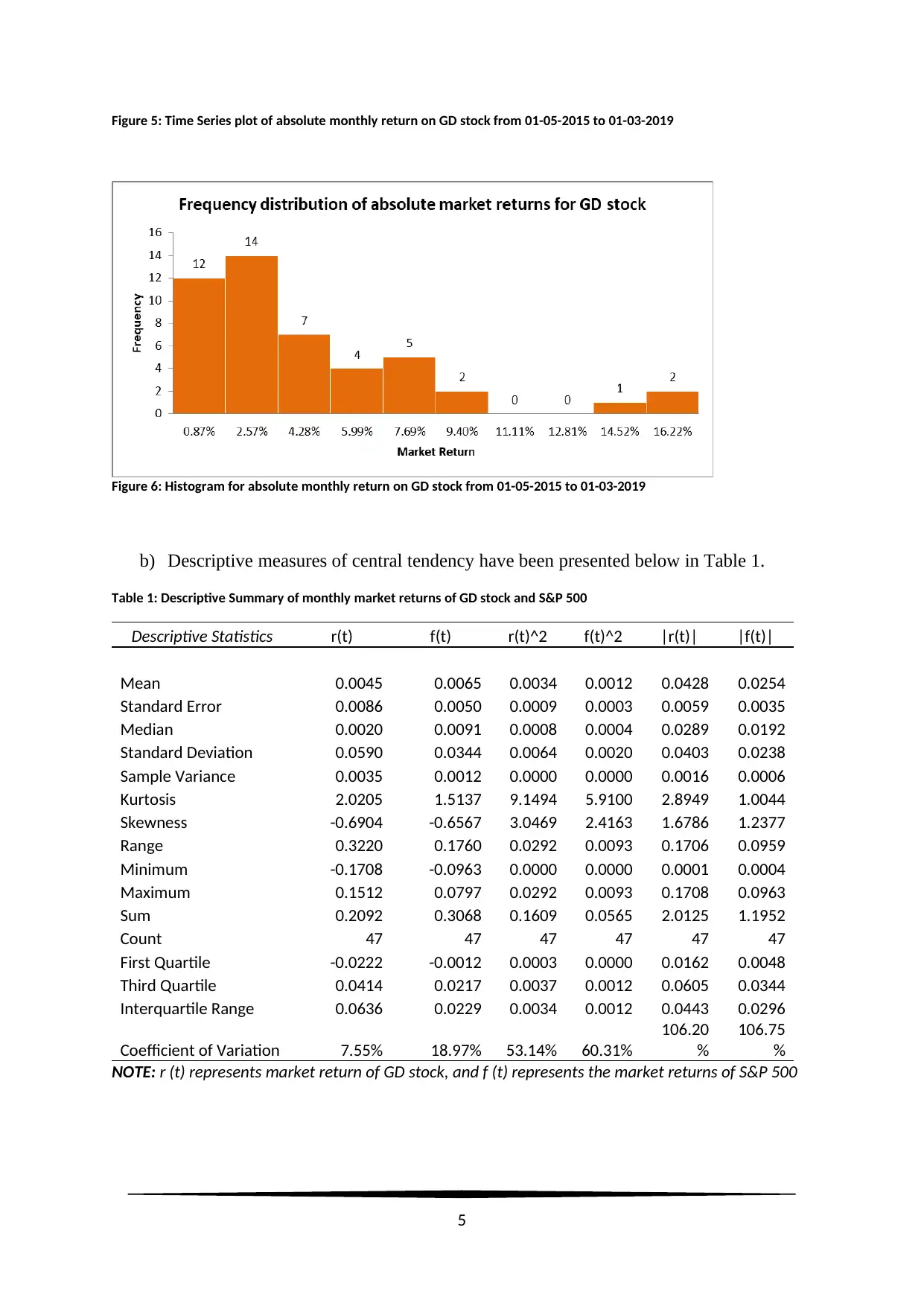

b) Descriptive measures of central tendency have been presented below in Table 1.

Table 1: Descriptive Summary of monthly market returns of GD stock and S&P 500

Descriptive Statistics r(t) f(t) r(t)^2 f(t)^2 |r(t)| |f(t)|

Mean 0.0045 0.0065 0.0034 0.0012 0.0428 0.0254

Standard Error 0.0086 0.0050 0.0009 0.0003 0.0059 0.0035

Median 0.0020 0.0091 0.0008 0.0004 0.0289 0.0192

Standard Deviation 0.0590 0.0344 0.0064 0.0020 0.0403 0.0238

Sample Variance 0.0035 0.0012 0.0000 0.0000 0.0016 0.0006

Kurtosis 2.0205 1.5137 9.1494 5.9100 2.8949 1.0044

Skewness -0.6904 -0.6567 3.0469 2.4163 1.6786 1.2377

Range 0.3220 0.1760 0.0292 0.0093 0.1706 0.0959

Minimum -0.1708 -0.0963 0.0000 0.0000 0.0001 0.0004

Maximum 0.1512 0.0797 0.0292 0.0093 0.1708 0.0963

Sum 0.2092 0.3068 0.1609 0.0565 2.0125 1.1952

Count 47 47 47 47 47 47

First Quartile -0.0222 -0.0012 0.0003 0.0000 0.0162 0.0048

Third Quartile 0.0414 0.0217 0.0037 0.0012 0.0605 0.0344

Interquartile Range 0.0636 0.0229 0.0034 0.0012 0.0443 0.0296

Coefficient of Variation 7.55% 18.97% 53.14% 60.31%

106.20

%

106.75

%

NOTE: r (t) represents market return of GD stock, and f (t) represents the market returns of S&P 500

5

Figure 6: Histogram for absolute monthly return on GD stock from 01-05-2015 to 01-03-2019

b) Descriptive measures of central tendency have been presented below in Table 1.

Table 1: Descriptive Summary of monthly market returns of GD stock and S&P 500

Descriptive Statistics r(t) f(t) r(t)^2 f(t)^2 |r(t)| |f(t)|

Mean 0.0045 0.0065 0.0034 0.0012 0.0428 0.0254

Standard Error 0.0086 0.0050 0.0009 0.0003 0.0059 0.0035

Median 0.0020 0.0091 0.0008 0.0004 0.0289 0.0192

Standard Deviation 0.0590 0.0344 0.0064 0.0020 0.0403 0.0238

Sample Variance 0.0035 0.0012 0.0000 0.0000 0.0016 0.0006

Kurtosis 2.0205 1.5137 9.1494 5.9100 2.8949 1.0044

Skewness -0.6904 -0.6567 3.0469 2.4163 1.6786 1.2377

Range 0.3220 0.1760 0.0292 0.0093 0.1706 0.0959

Minimum -0.1708 -0.0963 0.0000 0.0000 0.0001 0.0004

Maximum 0.1512 0.0797 0.0292 0.0093 0.1708 0.0963

Sum 0.2092 0.3068 0.1609 0.0565 2.0125 1.1952

Count 47 47 47 47 47 47

First Quartile -0.0222 -0.0012 0.0003 0.0000 0.0162 0.0048

Third Quartile 0.0414 0.0217 0.0037 0.0012 0.0605 0.0344

Interquartile Range 0.0636 0.0229 0.0034 0.0012 0.0443 0.0296

Coefficient of Variation 7.55% 18.97% 53.14% 60.31%

106.20

%

106.75

%

NOTE: r (t) represents market return of GD stock, and f (t) represents the market returns of S&P 500

5

Findings: Monthly market returns of GD stock (SD = 0.059) are more dispersed compared to

S&P 500 (SD = 0.034), for obvious reasons, as S&P 500 is the aggregate of all the stocks

traded in the stock exchange. Compared to the market, GD stock can be noted more volatile,

though, from Figure 1 it can be noted that volatility up to 01-01-2018 was more or less in line

with S&P 500. But, a sharp dip and downward trend can be clearly identified within the time

frame of 1-01-2018 to 01-03-2019. This particular observation can clearly be identified from

Figure 2 and Figure 3 presenting the square and absolute returns. Both GD and S&P500 are

found to be positively skewed. Due to recent fluctuations in returns of GD, skewness for GD

stock is noted to be slightly greater than S&P500. An average monthly return of GD is well

below the average S&P500 return, indicating that the stock performs below par the entire

market. Considering the median of returns, it is noted that median return for GD is way below

S&P500 (Addo, and Sunzuoye, 2013, pp.15-21). This particular statistical observation

indicated that average of GD stock is affected by few outlier or unusual higher returns.

Part B

Using multiple linear regression analysis, the mathematical model yt =c +∑

i=1

k

yt −i +∑

i=0

j

f t −i+ut

has been estimated with appropriate number of lags by misspecification tests.

Market returns from 01-05-2015 to 01-03-2019 have been considered for this regression

analysis.

First, the autocorrelations for market return for GD (r (t)) and S&P500 (f (t)) stocks have

been evaluated for 11 lags (number of observations = 47). No significant autocorrelation

(|ρ|≥3 ) was found for f (t). Significant autocorrelations were noted for lag 1, 2, and 6 for r (t).

The scholar included 6 lags for r (t) and zero lag for f (t) variables in the first ARDL

regression model (Belloumi, 2014, pp.269-287).

6

S&P 500 (SD = 0.034), for obvious reasons, as S&P 500 is the aggregate of all the stocks

traded in the stock exchange. Compared to the market, GD stock can be noted more volatile,

though, from Figure 1 it can be noted that volatility up to 01-01-2018 was more or less in line

with S&P 500. But, a sharp dip and downward trend can be clearly identified within the time

frame of 1-01-2018 to 01-03-2019. This particular observation can clearly be identified from

Figure 2 and Figure 3 presenting the square and absolute returns. Both GD and S&P500 are

found to be positively skewed. Due to recent fluctuations in returns of GD, skewness for GD

stock is noted to be slightly greater than S&P500. An average monthly return of GD is well

below the average S&P500 return, indicating that the stock performs below par the entire

market. Considering the median of returns, it is noted that median return for GD is way below

S&P500 (Addo, and Sunzuoye, 2013, pp.15-21). This particular statistical observation

indicated that average of GD stock is affected by few outlier or unusual higher returns.

Part B

Using multiple linear regression analysis, the mathematical model yt =c +∑

i=1

k

yt −i +∑

i=0

j

f t −i+ut

has been estimated with appropriate number of lags by misspecification tests.

Market returns from 01-05-2015 to 01-03-2019 have been considered for this regression

analysis.

First, the autocorrelations for market return for GD (r (t)) and S&P500 (f (t)) stocks have

been evaluated for 11 lags (number of observations = 47). No significant autocorrelation

(|ρ|≥3 ) was found for f (t). Significant autocorrelations were noted for lag 1, 2, and 6 for r (t).

The scholar included 6 lags for r (t) and zero lag for f (t) variables in the first ARDL

regression model (Belloumi, 2014, pp.269-287).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

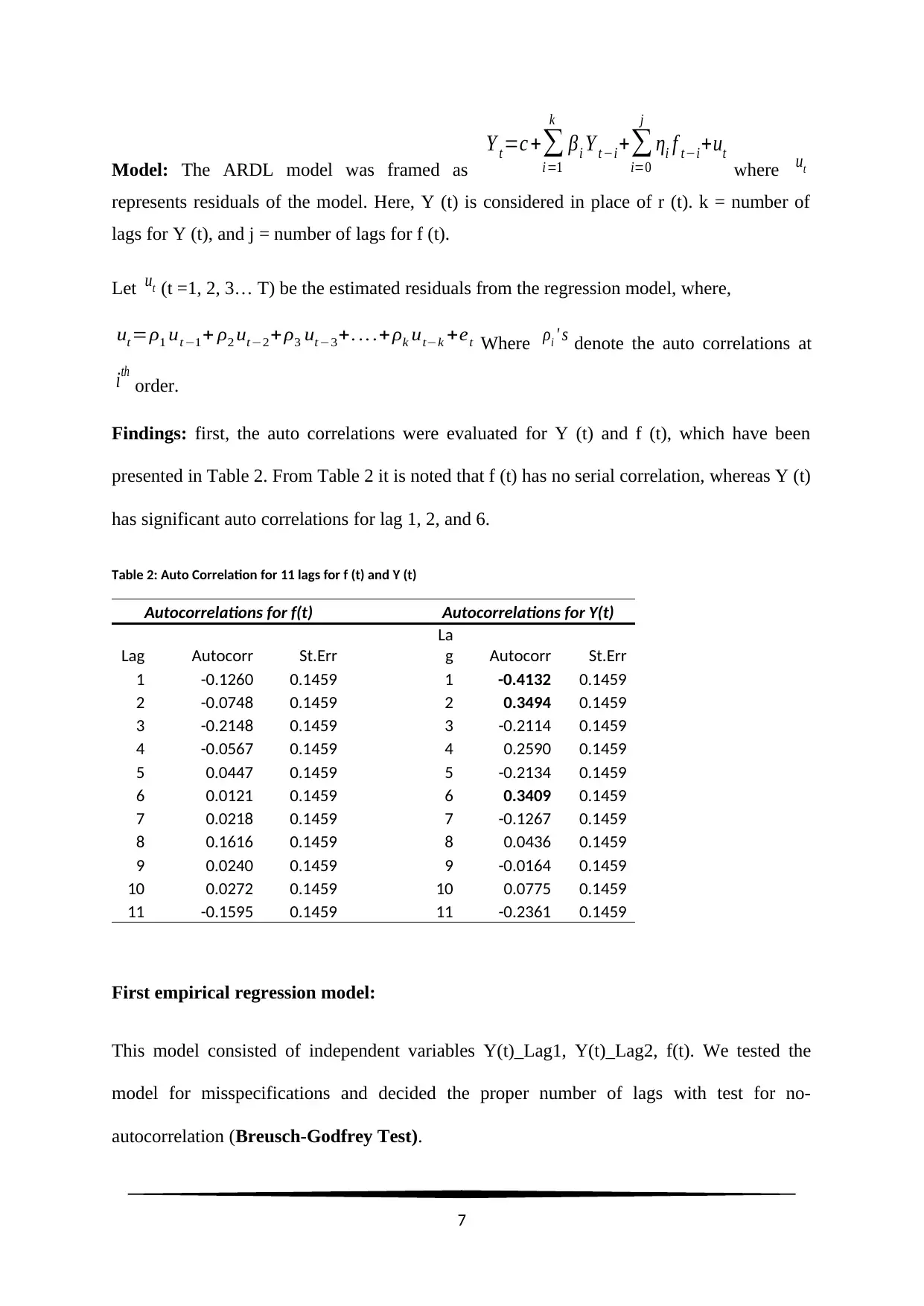

Model: The ARDL model was framed as

Y t =c +∑

i =1

k

βi Y t −i+∑

i=0

j

ηi f t−i+ut

where ut

represents residuals of the model. Here, Y (t) is considered in place of r (t). k = number of

lags for Y (t), and j = number of lags for f (t).

Let ut (t =1, 2, 3… T) be the estimated residuals from the regression model, where,

ut=ρ1 ut−1+ ρ2 ut−2+ ρ3 ut −3+. .. .+ ρk ut−k +et Where ρi ' s denote the auto correlations at

ith

order.

Findings: first, the auto correlations were evaluated for Y (t) and f (t), which have been

presented in Table 2. From Table 2 it is noted that f (t) has no serial correlation, whereas Y (t)

has significant auto correlations for lag 1, 2, and 6.

Table 2: Auto Correlation for 11 lags for f (t) and Y (t)

Autocorrelations for f(t) Autocorrelations for Y(t)

Lag Autocorr St.Err

La

g Autocorr St.Err

1 -0.1260 0.1459 1 -0.4132 0.1459

2 -0.0748 0.1459 2 0.3494 0.1459

3 -0.2148 0.1459 3 -0.2114 0.1459

4 -0.0567 0.1459 4 0.2590 0.1459

5 0.0447 0.1459 5 -0.2134 0.1459

6 0.0121 0.1459 6 0.3409 0.1459

7 0.0218 0.1459 7 -0.1267 0.1459

8 0.1616 0.1459 8 0.0436 0.1459

9 0.0240 0.1459 9 -0.0164 0.1459

10 0.0272 0.1459 10 0.0775 0.1459

11 -0.1595 0.1459 11 -0.2361 0.1459

First empirical regression model:

This model consisted of independent variables Y(t)_Lag1, Y(t)_Lag2, f(t). We tested the

model for misspecifications and decided the proper number of lags with test for no-

autocorrelation (Breusch-Godfrey Test).

7

Y t =c +∑

i =1

k

βi Y t −i+∑

i=0

j

ηi f t−i+ut

where ut

represents residuals of the model. Here, Y (t) is considered in place of r (t). k = number of

lags for Y (t), and j = number of lags for f (t).

Let ut (t =1, 2, 3… T) be the estimated residuals from the regression model, where,

ut=ρ1 ut−1+ ρ2 ut−2+ ρ3 ut −3+. .. .+ ρk ut−k +et Where ρi ' s denote the auto correlations at

ith

order.

Findings: first, the auto correlations were evaluated for Y (t) and f (t), which have been

presented in Table 2. From Table 2 it is noted that f (t) has no serial correlation, whereas Y (t)

has significant auto correlations for lag 1, 2, and 6.

Table 2: Auto Correlation for 11 lags for f (t) and Y (t)

Autocorrelations for f(t) Autocorrelations for Y(t)

Lag Autocorr St.Err

La

g Autocorr St.Err

1 -0.1260 0.1459 1 -0.4132 0.1459

2 -0.0748 0.1459 2 0.3494 0.1459

3 -0.2148 0.1459 3 -0.2114 0.1459

4 -0.0567 0.1459 4 0.2590 0.1459

5 0.0447 0.1459 5 -0.2134 0.1459

6 0.0121 0.1459 6 0.3409 0.1459

7 0.0218 0.1459 7 -0.1267 0.1459

8 0.1616 0.1459 8 0.0436 0.1459

9 0.0240 0.1459 9 -0.0164 0.1459

10 0.0272 0.1459 10 0.0775 0.1459

11 -0.1595 0.1459 11 -0.2361 0.1459

First empirical regression model:

This model consisted of independent variables Y(t)_Lag1, Y(t)_Lag2, f(t). We tested the

model for misspecifications and decided the proper number of lags with test for no-

autocorrelation (Breusch-Godfrey Test).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 3: Multiple Regression Model with p = 2, q = 0 lags for Y (t) and f (t)

Summary measures

Multiple R 0.7125

R-Square 0.5076

Adj R-Square 0.4716

StErr of Est 0.0438

ANOVA Table

Source df SS MS F p-value

Explained 3 0.0811 0.0270 14.0911 0.0000

Unexplained 41 0.0786 0.0019

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0034 0.0068 -0.5000 0.6198 -0.0171 0.0103

Y(t)_Lag1 -0.1482 0.1256 -1.1800 0.2448 -0.4019 0.1054

Y(t)_Lag2 0.1984 0.1204 1.6477 0.1071 -0.0448 0.4416

f(t) 0.9930 0.1996 4.9759 0.0000 0.5900 1.3960

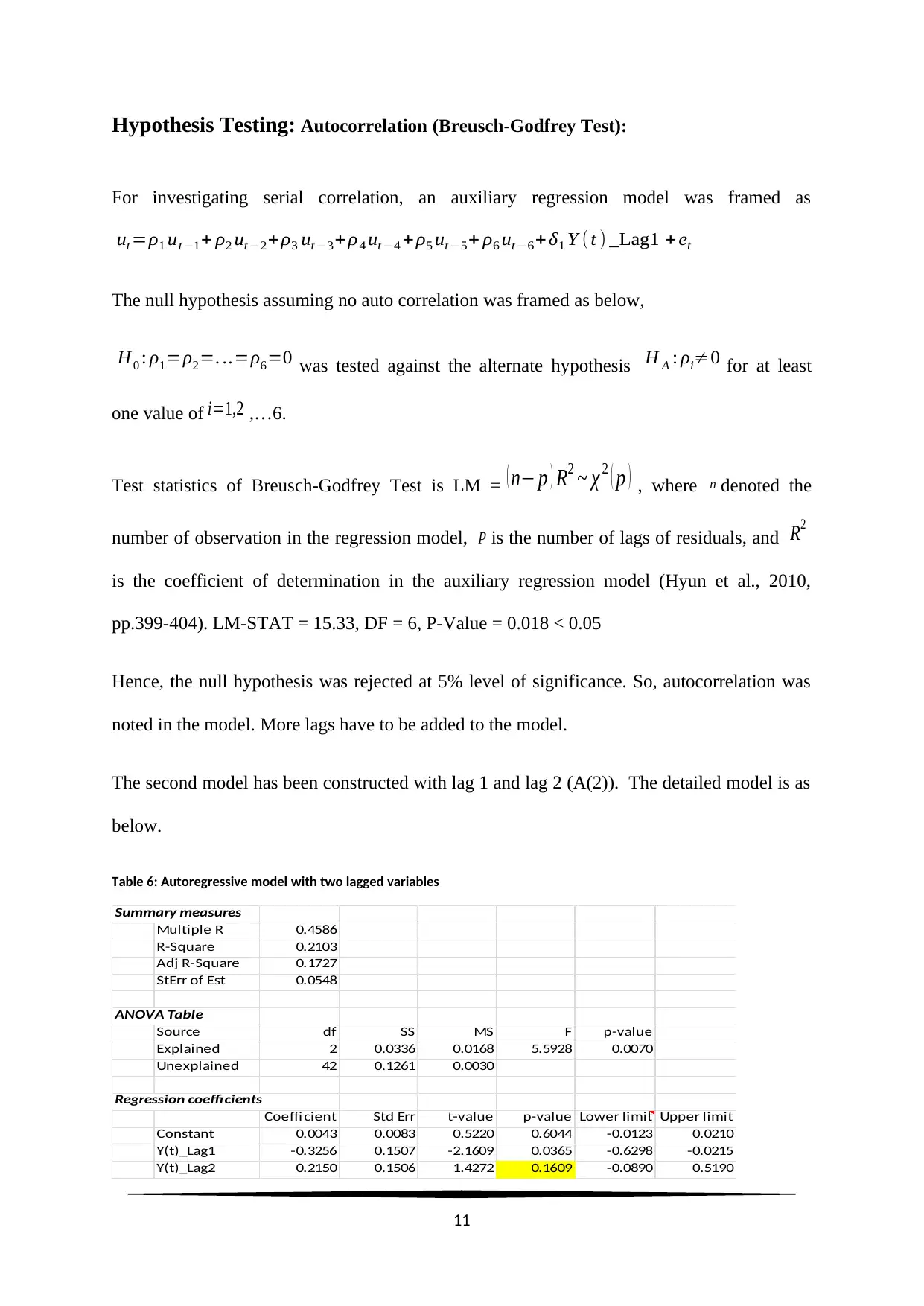

Hypothesis Testing: Autocorrelation (Breusch-Godfrey Test):

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut −1+ ρ2 ut −2+ ρ3 ut −3+ ρ4 ut −4 + ρ5 ut −5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + δ2 Y (t )_Lag2+ η1 f (t )+ et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

Test statistics of Breusch-Godfrey Test is LM = ( n− p ) R2 ~ χ 2 ( p ) , where n denoted the

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model.

LM-STAT = 7.28, DF = 6, P-Value = 0.295 > 0.05

8

Summary measures

Multiple R 0.7125

R-Square 0.5076

Adj R-Square 0.4716

StErr of Est 0.0438

ANOVA Table

Source df SS MS F p-value

Explained 3 0.0811 0.0270 14.0911 0.0000

Unexplained 41 0.0786 0.0019

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0034 0.0068 -0.5000 0.6198 -0.0171 0.0103

Y(t)_Lag1 -0.1482 0.1256 -1.1800 0.2448 -0.4019 0.1054

Y(t)_Lag2 0.1984 0.1204 1.6477 0.1071 -0.0448 0.4416

f(t) 0.9930 0.1996 4.9759 0.0000 0.5900 1.3960

Hypothesis Testing: Autocorrelation (Breusch-Godfrey Test):

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut −1+ ρ2 ut −2+ ρ3 ut −3+ ρ4 ut −4 + ρ5 ut −5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + δ2 Y (t )_Lag2+ η1 f (t )+ et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

Test statistics of Breusch-Godfrey Test is LM = ( n− p ) R2 ~ χ 2 ( p ) , where n denoted the

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model.

LM-STAT = 7.28, DF = 6, P-Value = 0.295 > 0.05

8

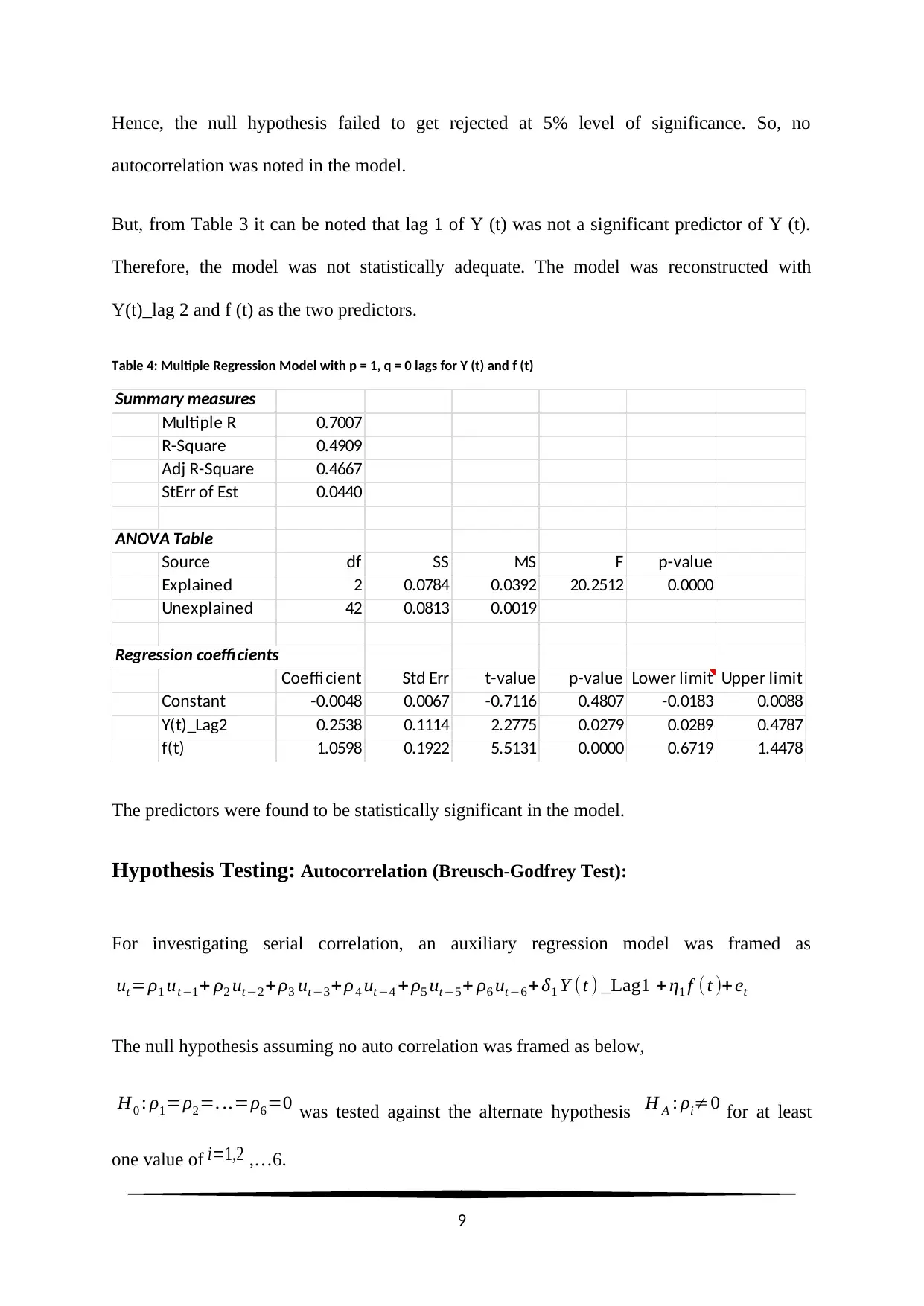

Hence, the null hypothesis failed to get rejected at 5% level of significance. So, no

autocorrelation was noted in the model.

But, from Table 3 it can be noted that lag 1 of Y (t) was not a significant predictor of Y (t).

Therefore, the model was not statistically adequate. The model was reconstructed with

Y(t)_lag 2 and f (t) as the two predictors.

Table 4: Multiple Regression Model with p = 1, q = 0 lags for Y (t) and f (t)

Summary measures

Multiple R 0.7007

R-Square 0.4909

Adj R-Square 0.4667

StErr of Est 0.0440

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0784 0.0392 20.2512 0.0000

Unexplained 42 0.0813 0.0019

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0048 0.0067 -0.7116 0.4807 -0.0183 0.0088

Y(t)_Lag2 0.2538 0.1114 2.2775 0.0279 0.0289 0.4787

f(t) 1.0598 0.1922 5.5131 0.0000 0.6719 1.4478

The predictors were found to be statistically significant in the model.

Hypothesis Testing: Autocorrelation (Breusch-Godfrey Test):

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut−1+ ρ2 ut−2+ρ3 ut−3+ ρ4 ut −4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + η1 f (t )+ et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

9

autocorrelation was noted in the model.

But, from Table 3 it can be noted that lag 1 of Y (t) was not a significant predictor of Y (t).

Therefore, the model was not statistically adequate. The model was reconstructed with

Y(t)_lag 2 and f (t) as the two predictors.

Table 4: Multiple Regression Model with p = 1, q = 0 lags for Y (t) and f (t)

Summary measures

Multiple R 0.7007

R-Square 0.4909

Adj R-Square 0.4667

StErr of Est 0.0440

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0784 0.0392 20.2512 0.0000

Unexplained 42 0.0813 0.0019

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0048 0.0067 -0.7116 0.4807 -0.0183 0.0088

Y(t)_Lag2 0.2538 0.1114 2.2775 0.0279 0.0289 0.4787

f(t) 1.0598 0.1922 5.5131 0.0000 0.6719 1.4478

The predictors were found to be statistically significant in the model.

Hypothesis Testing: Autocorrelation (Breusch-Godfrey Test):

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut−1+ ρ2 ut−2+ρ3 ut−3+ ρ4 ut −4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + η1 f (t )+ et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Test statistics of Breusch-Godfrey Test is LM = ( n− p ) R2 ~ χ 2 ( p ) , where n denoted the

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model.

LM-STAT = 8.75, DF = 6, P-Value = 0.188 > 0.05

Hence, the null hypothesis failed to get rejected at 5% level of significance. So, no

autocorrelation was noted in the model. The final model is

Y ( t )=0 . 2538∗Y ( t )Lag 2+1. 0598∗f (t )−0 . 0048 .

Part C

Using Linear Regression Analysis an AR (p) Model was estimated choosing the appropriate

number of lags. Misspecification testing was done on the model to choose number of

appropriate lags. Also, a statistically significant regression model has been constructed.

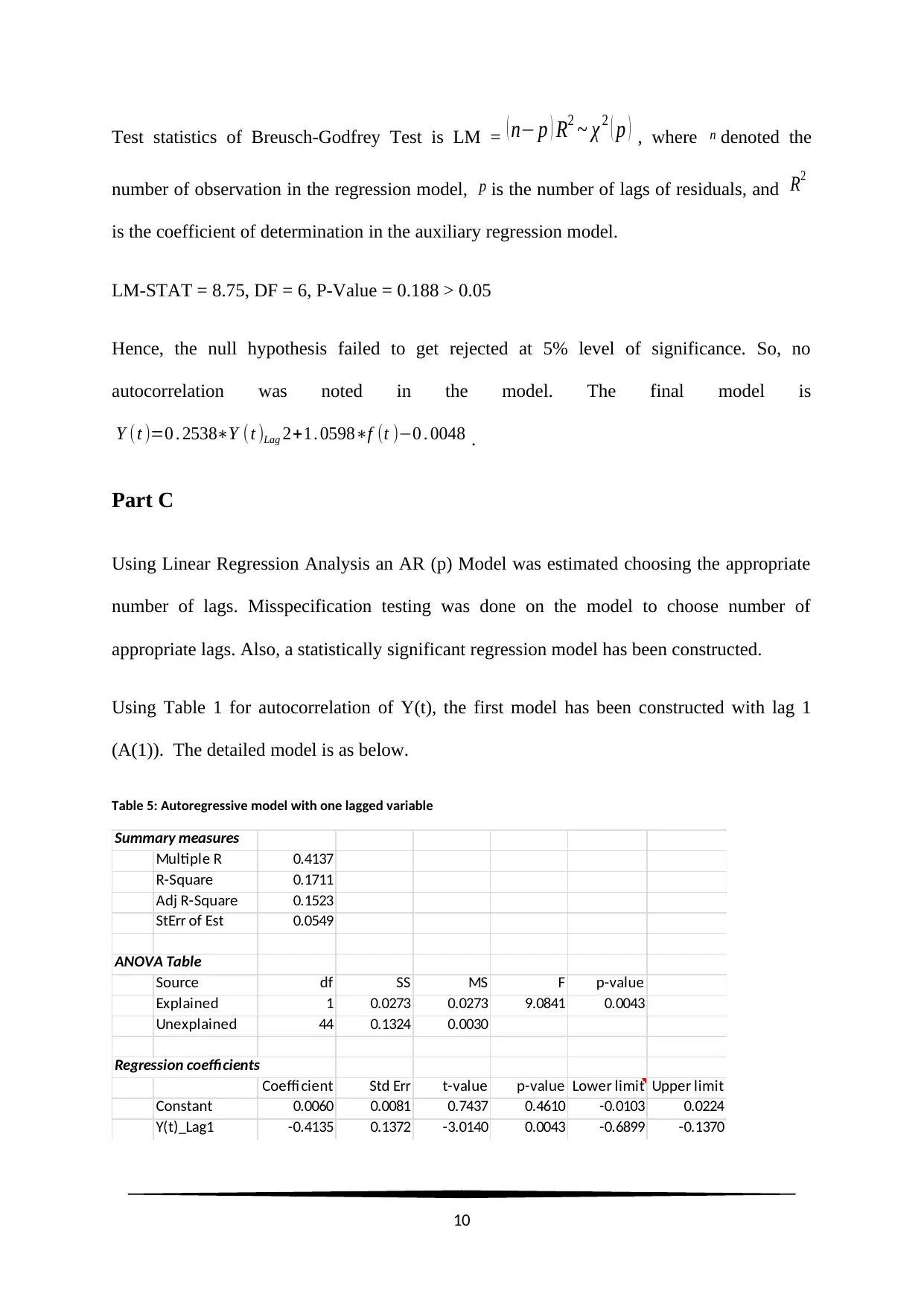

Using Table 1 for autocorrelation of Y(t), the first model has been constructed with lag 1

(A(1)). The detailed model is as below.

Table 5: Autoregressive model with one lagged variable

Summary measures

Multiple R 0.4137

R-Square 0.1711

Adj R-Square 0.1523

StErr of Est 0.0549

ANOVA Table

Source df SS MS F p-value

Explained 1 0.0273 0.0273 9.0841 0.0043

Unexplained 44 0.1324 0.0030

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant 0.0060 0.0081 0.7437 0.4610 -0.0103 0.0224

Y(t)_Lag1 -0.4135 0.1372 -3.0140 0.0043 -0.6899 -0.1370

10

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model.

LM-STAT = 8.75, DF = 6, P-Value = 0.188 > 0.05

Hence, the null hypothesis failed to get rejected at 5% level of significance. So, no

autocorrelation was noted in the model. The final model is

Y ( t )=0 . 2538∗Y ( t )Lag 2+1. 0598∗f (t )−0 . 0048 .

Part C

Using Linear Regression Analysis an AR (p) Model was estimated choosing the appropriate

number of lags. Misspecification testing was done on the model to choose number of

appropriate lags. Also, a statistically significant regression model has been constructed.

Using Table 1 for autocorrelation of Y(t), the first model has been constructed with lag 1

(A(1)). The detailed model is as below.

Table 5: Autoregressive model with one lagged variable

Summary measures

Multiple R 0.4137

R-Square 0.1711

Adj R-Square 0.1523

StErr of Est 0.0549

ANOVA Table

Source df SS MS F p-value

Explained 1 0.0273 0.0273 9.0841 0.0043

Unexplained 44 0.1324 0.0030

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant 0.0060 0.0081 0.7437 0.4610 -0.0103 0.0224

Y(t)_Lag1 -0.4135 0.1372 -3.0140 0.0043 -0.6899 -0.1370

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hypothesis Testing: Autocorrelation (Breusch-Godfrey Test):

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut−1+ ρ2 ut−2+ρ3 ut −3+ρ4 ut −4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

Test statistics of Breusch-Godfrey Test is LM = ( n− p ) R2 ~ χ 2 ( p ) , where n denoted the

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model (Hyun et al., 2010,

pp.399-404). LM-STAT = 15.33, DF = 6, P-Value = 0.018 < 0.05

Hence, the null hypothesis was rejected at 5% level of significance. So, autocorrelation was

noted in the model. More lags have to be added to the model.

The second model has been constructed with lag 1 and lag 2 (A(2)). The detailed model is as

below.

Table 6: Autoregressive model with two lagged variables

Summary measures

Multiple R 0.4586

R-Square 0.2103

Adj R-Square 0.1727

StErr of Est 0.0548

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0336 0.0168 5.5928 0.0070

Unexplained 42 0.1261 0.0030

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant 0.0043 0.0083 0.5220 0.6044 -0.0123 0.0210

Y(t)_Lag1 -0.3256 0.1507 -2.1609 0.0365 -0.6298 -0.0215

Y(t)_Lag2 0.2150 0.1506 1.4272 0.1609 -0.0890 0.5190

11

For investigating serial correlation, an auxiliary regression model was framed as

ut=ρ1 ut−1+ ρ2 ut−2+ρ3 ut −3+ρ4 ut −4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + et

The null hypothesis assuming no auto correlation was framed as below,

H0 : ρ1=ρ2=. ..=ρ6=0 was tested against the alternate hypothesis H A : ρi≠0 for at least

one value of i=1,2 ,…6.

Test statistics of Breusch-Godfrey Test is LM = ( n− p ) R2 ~ χ 2 ( p ) , where n denoted the

number of observation in the regression model, p is the number of lags of residuals, and R2

is the coefficient of determination in the auxiliary regression model (Hyun et al., 2010,

pp.399-404). LM-STAT = 15.33, DF = 6, P-Value = 0.018 < 0.05

Hence, the null hypothesis was rejected at 5% level of significance. So, autocorrelation was

noted in the model. More lags have to be added to the model.

The second model has been constructed with lag 1 and lag 2 (A(2)). The detailed model is as

below.

Table 6: Autoregressive model with two lagged variables

Summary measures

Multiple R 0.4586

R-Square 0.2103

Adj R-Square 0.1727

StErr of Est 0.0548

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0336 0.0168 5.5928 0.0070

Unexplained 42 0.1261 0.0030

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant 0.0043 0.0083 0.5220 0.6044 -0.0123 0.0210

Y(t)_Lag1 -0.3256 0.1507 -2.1609 0.0365 -0.6298 -0.0215

Y(t)_Lag2 0.2150 0.1506 1.4272 0.1609 -0.0890 0.5190

11

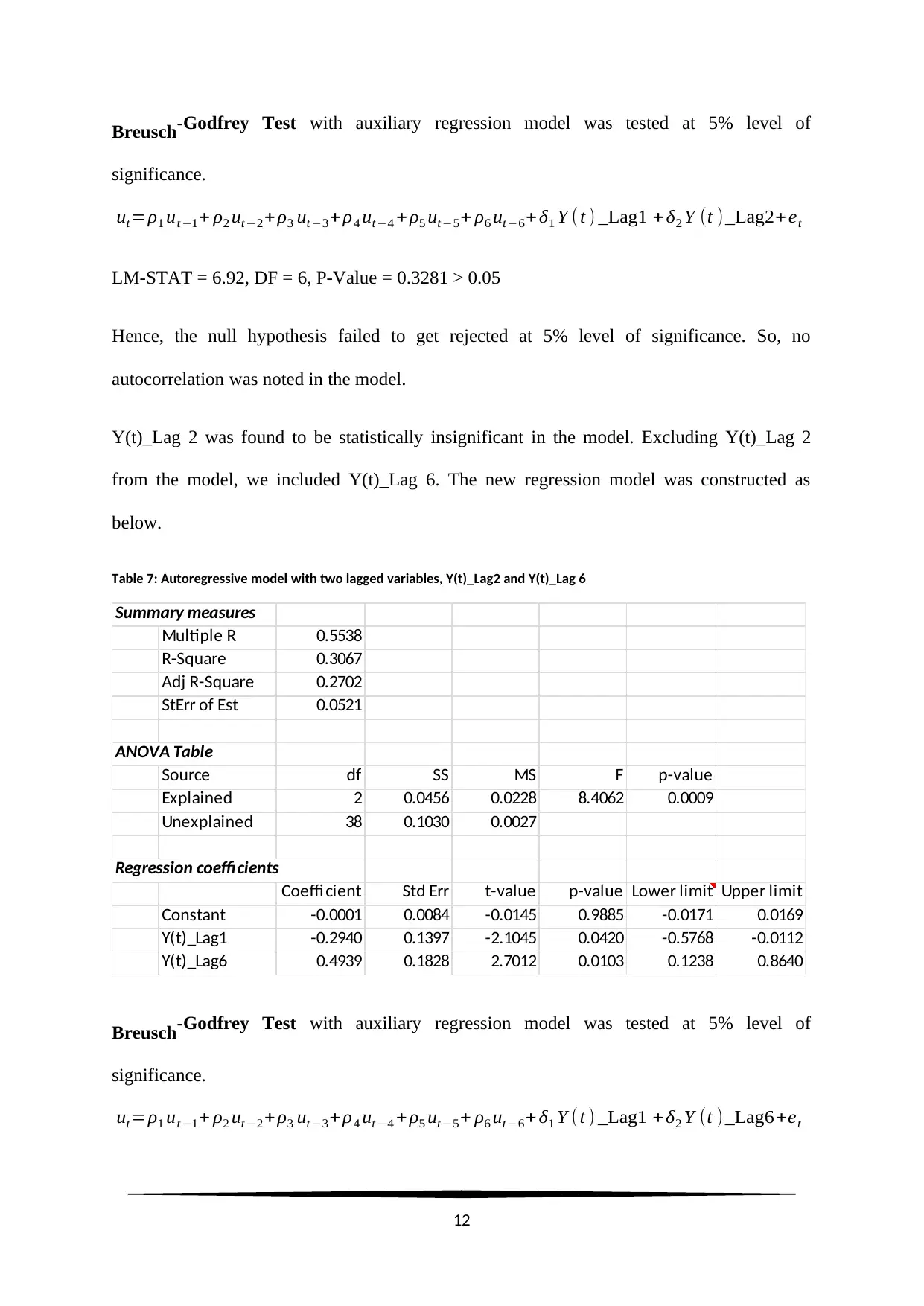

Breusch-Godfrey Test with auxiliary regression model was tested at 5% level of

significance.

ut=ρ1 ut −1+ ρ2 ut−2+ ρ3 ut −3+ ρ4 ut−4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + δ2 Y (t )_Lag2+et

LM-STAT = 6.92, DF = 6, P-Value = 0.3281 > 0.05

Hence, the null hypothesis failed to get rejected at 5% level of significance. So, no

autocorrelation was noted in the model.

Y(t)_Lag 2 was found to be statistically insignificant in the model. Excluding Y(t)_Lag 2

from the model, we included Y(t)_Lag 6. The new regression model was constructed as

below.

Table 7: Autoregressive model with two lagged variables, Y(t)_Lag2 and Y(t)_Lag 6

Summary measures

Multiple R 0.5538

R-Square 0.3067

Adj R-Square 0.2702

StErr of Est 0.0521

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0456 0.0228 8.4062 0.0009

Unexplained 38 0.1030 0.0027

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0001 0.0084 -0.0145 0.9885 -0.0171 0.0169

Y(t)_Lag1 -0.2940 0.1397 -2.1045 0.0420 -0.5768 -0.0112

Y(t)_Lag6 0.4939 0.1828 2.7012 0.0103 0.1238 0.8640

Breusch-Godfrey Test with auxiliary regression model was tested at 5% level of

significance.

ut=ρ1 ut −1+ ρ2 ut−2+ ρ3 ut−3+ ρ4 ut−4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y ( t ) _Lag1 + δ2 Y (t ) _Lag6+et

12

significance.

ut=ρ1 ut −1+ ρ2 ut−2+ ρ3 ut −3+ ρ4 ut−4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y (t ) _Lag1 + δ2 Y (t )_Lag2+et

LM-STAT = 6.92, DF = 6, P-Value = 0.3281 > 0.05

Hence, the null hypothesis failed to get rejected at 5% level of significance. So, no

autocorrelation was noted in the model.

Y(t)_Lag 2 was found to be statistically insignificant in the model. Excluding Y(t)_Lag 2

from the model, we included Y(t)_Lag 6. The new regression model was constructed as

below.

Table 7: Autoregressive model with two lagged variables, Y(t)_Lag2 and Y(t)_Lag 6

Summary measures

Multiple R 0.5538

R-Square 0.3067

Adj R-Square 0.2702

StErr of Est 0.0521

ANOVA Table

Source df SS MS F p-value

Explained 2 0.0456 0.0228 8.4062 0.0009

Unexplained 38 0.1030 0.0027

Regression coefficients

Coeffi cient Std Err t-value p-value Lower limit Upper limit

Constant -0.0001 0.0084 -0.0145 0.9885 -0.0171 0.0169

Y(t)_Lag1 -0.2940 0.1397 -2.1045 0.0420 -0.5768 -0.0112

Y(t)_Lag6 0.4939 0.1828 2.7012 0.0103 0.1238 0.8640

Breusch-Godfrey Test with auxiliary regression model was tested at 5% level of

significance.

ut=ρ1 ut −1+ ρ2 ut−2+ ρ3 ut−3+ ρ4 ut−4 + ρ5 ut−5+ ρ6 ut−6+ δ1 Y ( t ) _Lag1 + δ2 Y (t ) _Lag6+et

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.