SIT717 Assignment 1: Survey on ARIMA Models in Time Series Analysis

VerifiedAdded on 2022/09/18

|12

|3242

|27

Report

AI Summary

This report presents a survey on the application of Autoregressive Integrated Moving Average (ARIMA) models in time series data prediction. The survey explores the ARIMA model's components, including the AR, I, and MA terms, and their role in transforming non-stationary data into a stationary form, essential for reliable forecasting. It discusses the importance of stationarity, normality, and linearity tests in model validation. The report highlights ARIMA's prominence in business intelligence, emphasizing its ability to enhance the prediction of historical, current, and future trends, particularly in areas like economics, capacity planning, and weather forecasting. The survey also compares ARIMA with other machine learning techniques like LSTM and Prophet, underscoring ARIMA's effectiveness in time series analysis, and its ability to provide insights into the relationships between variables, supporting informed decision-making. The report also examines the tools used for modelling time series data using the ARIMA models and various tests that are essential for ensuring correct and reliable predictions about the projected values.

STATISTICS 1

A Brief Survey on Time Series Data Prediction Using ARIMA Models

Student’s name

Tutors name

Course

Institutional affiliation

City and state

Date

A Brief Survey on Time Series Data Prediction Using ARIMA Models

Student’s name

Tutors name

Course

Institutional affiliation

City and state

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS 2

Abstract

The survey explores the effect of ‘Auto-Regressive Integrated Moving

Averages’ (ARIMA), models in prediction of data based on time. ARIMA model

involves modelling of time series data in order to prediction. ARIMA models involves

many tests such as stationarity, normality and linearity. For the time series modelled

data, it is essential for the data to be stationary in order to provide reliable and

consistent results. The survey evaluated various other machine learning methods in

prediction. These techniques include; LSTM and PROPHET. The survey looked at

their differences and the behavior towards time series data. It was observed that

ARIMA is mostly used in prediction especially in business intelligence since it

enhances estimation of the historical, current and future forecasts.

Abstract

The survey explores the effect of ‘Auto-Regressive Integrated Moving

Averages’ (ARIMA), models in prediction of data based on time. ARIMA model

involves modelling of time series data in order to prediction. ARIMA models involves

many tests such as stationarity, normality and linearity. For the time series modelled

data, it is essential for the data to be stationary in order to provide reliable and

consistent results. The survey evaluated various other machine learning methods in

prediction. These techniques include; LSTM and PROPHET. The survey looked at

their differences and the behavior towards time series data. It was observed that

ARIMA is mostly used in prediction especially in business intelligence since it

enhances estimation of the historical, current and future forecasts.

STATISTICS 3

ARIMA models in prediction of time series data

1. Introduction

In the past years, time series data resolved by statisticians minus considering the

effects on their analysis that may be brought about by ‘non-stationeries’. Until

George. P and Jenkins. G came up with a monograph known as “Time series Analysis

forecast and control”. This tool helped in predicting so that the non-stationary data

could be transformed into stationary data. This would be done by ‘differencing’ series.

Time series data plays an essential role in future value forecast. Basing on past results,

time series is applied in forecasting changes in economics, capacity planning, weather

among others (Alsharif et al, 2019). However, features time-series data need specific

statistical methods to be applied. There are concepts that time series data uses and

these are autocorrelation, seasonality and stationary. In this paper, we are to discuss

the prominent time series method in forecasting and this method is known as ARIMA.

The ARIMA component is applied to transform time series data so as to ease the and

forecast future values in time series cheaply. ARIMA models give the best approach to

forecasting time series (Alsharif et al, 2019). The commonly used approaches in

forecasting time series data are ARIMA and exponential smoothing. These two

methods work hand in hand to solve problems. As exponential smoothing model relies

on describing data trends and seasonality, ARIMA models do describe the

autocorrelations within data. ARIMA is described as a group of models that

describes a specific time series relying on the previous values that is to say, its ‘own-

errors that are lagged on prediction errors. In this case, the ARIMA model is applied

ARIMA models in prediction of time series data

1. Introduction

In the past years, time series data resolved by statisticians minus considering the

effects on their analysis that may be brought about by ‘non-stationeries’. Until

George. P and Jenkins. G came up with a monograph known as “Time series Analysis

forecast and control”. This tool helped in predicting so that the non-stationary data

could be transformed into stationary data. This would be done by ‘differencing’ series.

Time series data plays an essential role in future value forecast. Basing on past results,

time series is applied in forecasting changes in economics, capacity planning, weather

among others (Alsharif et al, 2019). However, features time-series data need specific

statistical methods to be applied. There are concepts that time series data uses and

these are autocorrelation, seasonality and stationary. In this paper, we are to discuss

the prominent time series method in forecasting and this method is known as ARIMA.

The ARIMA component is applied to transform time series data so as to ease the and

forecast future values in time series cheaply. ARIMA models give the best approach to

forecasting time series (Alsharif et al, 2019). The commonly used approaches in

forecasting time series data are ARIMA and exponential smoothing. These two

methods work hand in hand to solve problems. As exponential smoothing model relies

on describing data trends and seasonality, ARIMA models do describe the

autocorrelations within data. ARIMA is described as a group of models that

describes a specific time series relying on the previous values that is to say, its ‘own-

errors that are lagged on prediction errors. In this case, the ARIMA model is applied

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS 4

in prediction of values in future. The series that are not seasonal denies originality

and not a probability as the ‘white noise’ is transformed using ARIMA models. There

are three models that make an up model of ARIMA and these are presented by p, d

and q as discussed below;

P means the order of the ‘AR’ term

d means the number of ‘differencing’ needed to transform the time series data from

being non stationary to being stationary

q represents the order of the ‘MA’ term

If ‘seasonal pattern’ are observed in a time series, then there is a requirement of

summing up all seasonal terms so that the series become ‘Seasonal ARIMA ‘known as

“SARIMA”. For one to start forming an ARIMA model, the time series is made

stationary. The reason behind this is that the concept ‘Auto Regressive’ in ARIMA

shows it is a ‘linear regression model’ which applies its “lags” as forecasts. It is well

known that linear regression models perform well only if predictors are not correlated

and work separately. A time series is made stationary through finding the difference

between the past values and the current values (past values minus current values). In

cases when series are ‘large’, differencing can be made several times. Therefore, d

shows the highest times for differencing required to turn the series stationary.

However, in cases where time series are stationary, the d is zero (d = 0).

P represents the ‘Auto Regressive’ (AR) order of the term. This is the number of

“lags” of Y that are applied as predictors. On the other hand, q means ‘moving

Average’ order of the term. It is the “lagged” predicated errors that are meant to be

in prediction of values in future. The series that are not seasonal denies originality

and not a probability as the ‘white noise’ is transformed using ARIMA models. There

are three models that make an up model of ARIMA and these are presented by p, d

and q as discussed below;

P means the order of the ‘AR’ term

d means the number of ‘differencing’ needed to transform the time series data from

being non stationary to being stationary

q represents the order of the ‘MA’ term

If ‘seasonal pattern’ are observed in a time series, then there is a requirement of

summing up all seasonal terms so that the series become ‘Seasonal ARIMA ‘known as

“SARIMA”. For one to start forming an ARIMA model, the time series is made

stationary. The reason behind this is that the concept ‘Auto Regressive’ in ARIMA

shows it is a ‘linear regression model’ which applies its “lags” as forecasts. It is well

known that linear regression models perform well only if predictors are not correlated

and work separately. A time series is made stationary through finding the difference

between the past values and the current values (past values minus current values). In

cases when series are ‘large’, differencing can be made several times. Therefore, d

shows the highest times for differencing required to turn the series stationary.

However, in cases where time series are stationary, the d is zero (d = 0).

P represents the ‘Auto Regressive’ (AR) order of the term. This is the number of

“lags” of Y that are applied as predictors. On the other hand, q means ‘moving

Average’ order of the term. It is the “lagged” predicated errors that are meant to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS 5

fixed in the ARIMA model.

2. Objectives of the Survey

This paper intends to carry out a survey on the ARIMA models’ usage in

predicting the time series data. In time series data, prediction finds several

applications in different sectors of industries or businesses. The reason as to why

ARIMA models are use is that most of the machine languages do not give the clear

image of predictions especially in the businesses involving in sales and others dealing

in financial matters. ARIMA is considered as the best model to interpret and evaluate

the time series data to achieve the stipulated goals or objectives. It enhances the

prediction of demand of products through optimization of production and warehouse

storage to anticipate the level of funds (money) from sales and even for future stock

values of price.

3. Tools used to model time series data

There are many choices of software that are used in modelling of time series

prediction. Through prediction using such tools, the ARIMA models are produced to

explain the data about variables needed to be studied. ARIMA is the statistical

technique that helps in projecting the future figures about the series basing on its own

inertia. To use ARIMA models, the data in the question should be at least 30 and

above historical data points for reliability issues and consistence. The ARIMA models

using time series data can be modeled in tools such as Python, R-language, Matlab,

STATA, MINITAB and many other languages. Most significant is that, before

reaching to the ‘sophisticated time series data’ some other models that form the

fountain of further predictions (ICDM, 2018a). It is believed that if the complicated

methods do not provide and yield reliable results, therefore there is no need of using

such methods. However, several procedures while using the ARIMA models in order

to present the clear results about time series data (Lucey et al, 2018). Mean; this is

among the procedures followed when modelling data since it shows the forecasts that

are equivalent to the value of mean about time series data. Naïve; this procedure

shows the equivalence of the forecasts and the previous values about time series and

fixed in the ARIMA model.

2. Objectives of the Survey

This paper intends to carry out a survey on the ARIMA models’ usage in

predicting the time series data. In time series data, prediction finds several

applications in different sectors of industries or businesses. The reason as to why

ARIMA models are use is that most of the machine languages do not give the clear

image of predictions especially in the businesses involving in sales and others dealing

in financial matters. ARIMA is considered as the best model to interpret and evaluate

the time series data to achieve the stipulated goals or objectives. It enhances the

prediction of demand of products through optimization of production and warehouse

storage to anticipate the level of funds (money) from sales and even for future stock

values of price.

3. Tools used to model time series data

There are many choices of software that are used in modelling of time series

prediction. Through prediction using such tools, the ARIMA models are produced to

explain the data about variables needed to be studied. ARIMA is the statistical

technique that helps in projecting the future figures about the series basing on its own

inertia. To use ARIMA models, the data in the question should be at least 30 and

above historical data points for reliability issues and consistence. The ARIMA models

using time series data can be modeled in tools such as Python, R-language, Matlab,

STATA, MINITAB and many other languages. Most significant is that, before

reaching to the ‘sophisticated time series data’ some other models that form the

fountain of further predictions (ICDM, 2018a). It is believed that if the complicated

methods do not provide and yield reliable results, therefore there is no need of using

such methods. However, several procedures while using the ARIMA models in order

to present the clear results about time series data (Lucey et al, 2018). Mean; this is

among the procedures followed when modelling data since it shows the forecasts that

are equivalent to the value of mean about time series data. Naïve; this procedure

shows the equivalence of the forecasts and the previous values about time series and

STATISTICS 6

lastly is the seasonal naïve. Seasonal naïve involves the forecasts for a specified

season that are equivalent to the values of seasonal period that is full. For instance,

when the predicted values of January 2019 are equivalent to those of time series

values in January of 2018.

The ARIMA models can forecast the Time Series Model (TSLM) as the

linear regression equations that forecasts the value needed about given variables. The

linear regression can be either linear trend or seasonality trends.

Yt = ao + a1X1t + a2X2t + ……. + anXnt + et

Where Xit are the explanatory variables, ai and b are the coefficients of

regression to be estimated. The most used trends in prediction time series data using

ARIMA models are linear trends and the seasonality effects. Also, the Seasonality

predictors are mostly in form of dummy variables which indicate the period of time

(monthly, quarterly, weekly and yearly) under which the predictions are made.

Furthermore, in ARIMA modelling other than linear trend and seasonality, there are

other several methods in prediction such as exponential smoothing and others. Most

significant in this paper is to assess the idea of prediction for future values about time

series as the ‘weighted average’ for last values whereby the weights that reduce the

time exponentially (Lucey et al, 2018). Besides, the method can as well be extended

to involved (method of Holt known as double exponential smoothing) or trend using

Holt Winter’s method. More so, the trends and seasonality coefficients in these

models can be determined by use of weighted averages of given expressions. In

addition, exponential smoothing is vital in predicting time series, the fundamental

point of view here is to forecast future outcomes whereby the attached weights

decrease exponentially as time changes. The equation of smoothing can be stated as

below;

Yt = a yt-1 + a(1-a) yt-2 + a(1-a)2 yt-3 + ……….

Where a (0,1) is smoothing parameter that are estimated. The displayed

method above can as well be extended to involve the doubled ‘exponential

smoothing’.

lastly is the seasonal naïve. Seasonal naïve involves the forecasts for a specified

season that are equivalent to the values of seasonal period that is full. For instance,

when the predicted values of January 2019 are equivalent to those of time series

values in January of 2018.

The ARIMA models can forecast the Time Series Model (TSLM) as the

linear regression equations that forecasts the value needed about given variables. The

linear regression can be either linear trend or seasonality trends.

Yt = ao + a1X1t + a2X2t + ……. + anXnt + et

Where Xit are the explanatory variables, ai and b are the coefficients of

regression to be estimated. The most used trends in prediction time series data using

ARIMA models are linear trends and the seasonality effects. Also, the Seasonality

predictors are mostly in form of dummy variables which indicate the period of time

(monthly, quarterly, weekly and yearly) under which the predictions are made.

Furthermore, in ARIMA modelling other than linear trend and seasonality, there are

other several methods in prediction such as exponential smoothing and others. Most

significant in this paper is to assess the idea of prediction for future values about time

series as the ‘weighted average’ for last values whereby the weights that reduce the

time exponentially (Lucey et al, 2018). Besides, the method can as well be extended

to involved (method of Holt known as double exponential smoothing) or trend using

Holt Winter’s method. More so, the trends and seasonality coefficients in these

models can be determined by use of weighted averages of given expressions. In

addition, exponential smoothing is vital in predicting time series, the fundamental

point of view here is to forecast future outcomes whereby the attached weights

decrease exponentially as time changes. The equation of smoothing can be stated as

below;

Yt = a yt-1 + a(1-a) yt-2 + a(1-a)2 yt-3 + ……….

Where a (0,1) is smoothing parameter that are estimated. The displayed

method above can as well be extended to involve the doubled ‘exponential

smoothing’.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS 7

The ‘Autoregressive Integrated Moving Average’ techniques completely use

various approaches. Autoregressive (AR) approach takes into account for the impact

of previous values about the predicted values.

Yt=a1yt-1+ a2yt-2+et; whereas the model of Moving Average (MA) that impacts

the noise of the estimated values of time series.

Yt=et+b1et-1+b2et-2.

Whereby et is the ‘random noise’ terms and each term about the random noise

have influence on three (3) yt values consecutively. In the current situation random

noise terms bring about the image of unexpected events such as statements made by

politicians that affect the stock markets (Sapankevych & Sankar, 2009) . The

combination of AR and MA models is read as ARMA and it can be shown in simple

way as:

Yt=et+b1et-1+b2et-2+a1yt-1+a2yt-2. As per the combination of AR and MA

(ARMA), the integrated portion for ARIMA is likely to correspond to technical

matters especially on how the ARMA models can be plotted and fitted out.

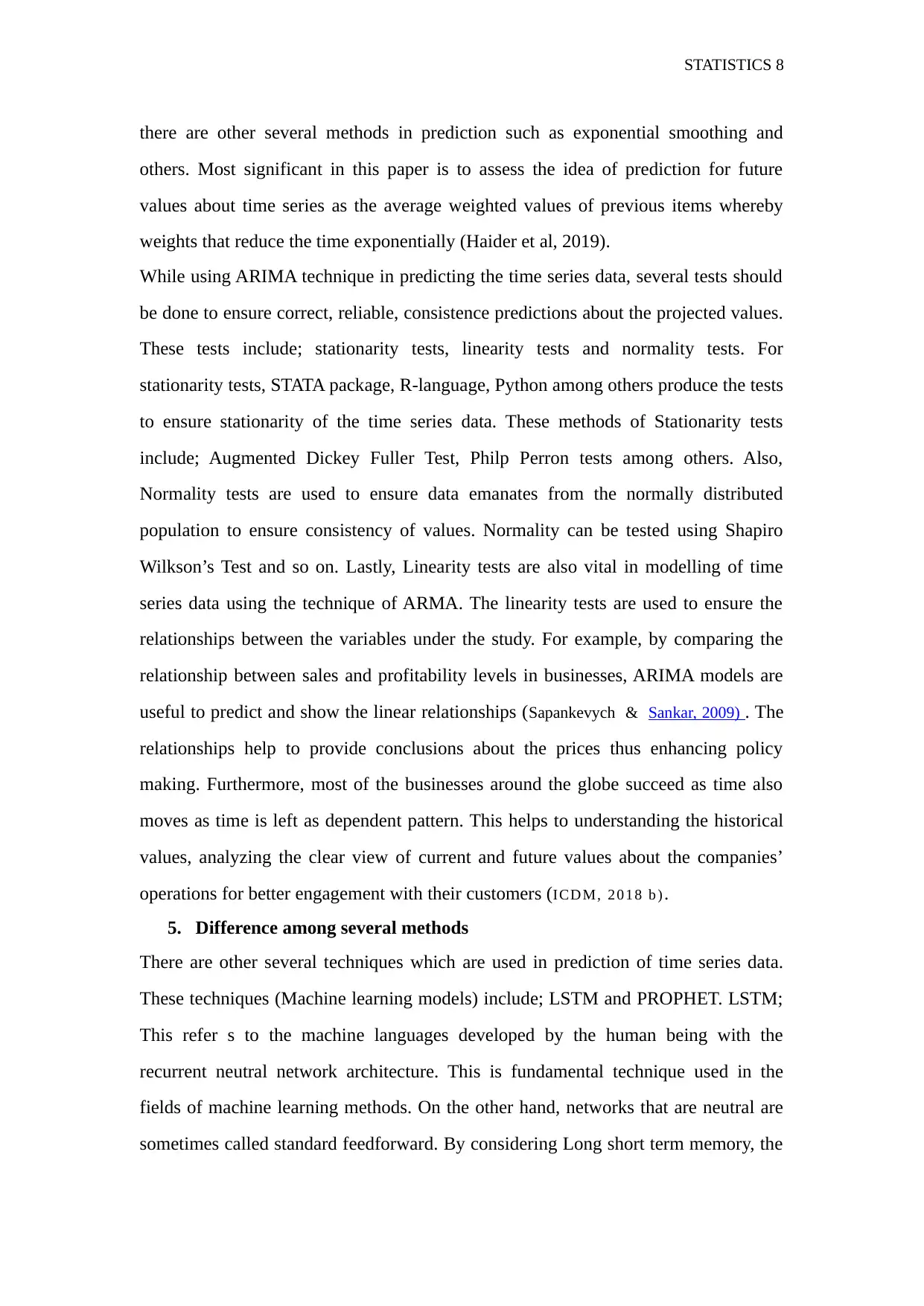

This therefore displays the basic overview of business prediction technique as

categorized in the diagram below.

4. How ARIMA works and its Usage in Business Intelligence

ARIMA models are linear trends and the seasonality effects. Also, the Seasonality

predictors are mostly in form of dummy variables which indicate the period of time

(monthly, quarterly, weekly and yearly) under which the predictions are made (Vigne

et al, 2017) Furthermore, in ARIMA modelling other than linear trend and seasonality,

The ‘Autoregressive Integrated Moving Average’ techniques completely use

various approaches. Autoregressive (AR) approach takes into account for the impact

of previous values about the predicted values.

Yt=a1yt-1+ a2yt-2+et; whereas the model of Moving Average (MA) that impacts

the noise of the estimated values of time series.

Yt=et+b1et-1+b2et-2.

Whereby et is the ‘random noise’ terms and each term about the random noise

have influence on three (3) yt values consecutively. In the current situation random

noise terms bring about the image of unexpected events such as statements made by

politicians that affect the stock markets (Sapankevych & Sankar, 2009) . The

combination of AR and MA models is read as ARMA and it can be shown in simple

way as:

Yt=et+b1et-1+b2et-2+a1yt-1+a2yt-2. As per the combination of AR and MA

(ARMA), the integrated portion for ARIMA is likely to correspond to technical

matters especially on how the ARMA models can be plotted and fitted out.

This therefore displays the basic overview of business prediction technique as

categorized in the diagram below.

4. How ARIMA works and its Usage in Business Intelligence

ARIMA models are linear trends and the seasonality effects. Also, the Seasonality

predictors are mostly in form of dummy variables which indicate the period of time

(monthly, quarterly, weekly and yearly) under which the predictions are made (Vigne

et al, 2017) Furthermore, in ARIMA modelling other than linear trend and seasonality,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS 8

there are other several methods in prediction such as exponential smoothing and

others. Most significant in this paper is to assess the idea of prediction for future

values about time series as the average weighted values of previous items whereby

weights that reduce the time exponentially (Haider et al, 2019).

While using ARIMA technique in predicting the time series data, several tests should

be done to ensure correct, reliable, consistence predictions about the projected values.

These tests include; stationarity tests, linearity tests and normality tests. For

stationarity tests, STATA package, R-language, Python among others produce the tests

to ensure stationarity of the time series data. These methods of Stationarity tests

include; Augmented Dickey Fuller Test, Philp Perron tests among others. Also,

Normality tests are used to ensure data emanates from the normally distributed

population to ensure consistency of values. Normality can be tested using Shapiro

Wilkson’s Test and so on. Lastly, Linearity tests are also vital in modelling of time

series data using the technique of ARMA. The linearity tests are used to ensure the

relationships between the variables under the study. For example, by comparing the

relationship between sales and profitability levels in businesses, ARIMA models are

useful to predict and show the linear relationships (Sapankevych & Sankar, 2009) . The

relationships help to provide conclusions about the prices thus enhancing policy

making. Furthermore, most of the businesses around the globe succeed as time also

moves as time is left as dependent pattern. This helps to understanding the historical

values, analyzing the clear view of current and future values about the companies’

operations for better engagement with their customers (I CD M, 2 01 8 b ) .

5. Difference among several methods

There are other several techniques which are used in prediction of time series data.

These techniques (Machine learning models) include; LSTM and PROPHET. LSTM;

This refer s to the machine languages developed by the human being with the

recurrent neutral network architecture. This is fundamental technique used in the

fields of machine learning methods. On the other hand, networks that are neutral are

sometimes called standard feedforward. By considering Long short term memory, the

there are other several methods in prediction such as exponential smoothing and

others. Most significant in this paper is to assess the idea of prediction for future

values about time series as the average weighted values of previous items whereby

weights that reduce the time exponentially (Haider et al, 2019).

While using ARIMA technique in predicting the time series data, several tests should

be done to ensure correct, reliable, consistence predictions about the projected values.

These tests include; stationarity tests, linearity tests and normality tests. For

stationarity tests, STATA package, R-language, Python among others produce the tests

to ensure stationarity of the time series data. These methods of Stationarity tests

include; Augmented Dickey Fuller Test, Philp Perron tests among others. Also,

Normality tests are used to ensure data emanates from the normally distributed

population to ensure consistency of values. Normality can be tested using Shapiro

Wilkson’s Test and so on. Lastly, Linearity tests are also vital in modelling of time

series data using the technique of ARMA. The linearity tests are used to ensure the

relationships between the variables under the study. For example, by comparing the

relationship between sales and profitability levels in businesses, ARIMA models are

useful to predict and show the linear relationships (Sapankevych & Sankar, 2009) . The

relationships help to provide conclusions about the prices thus enhancing policy

making. Furthermore, most of the businesses around the globe succeed as time also

moves as time is left as dependent pattern. This helps to understanding the historical

values, analyzing the clear view of current and future values about the companies’

operations for better engagement with their customers (I CD M, 2 01 8 b ) .

5. Difference among several methods

There are other several techniques which are used in prediction of time series data.

These techniques (Machine learning models) include; LSTM and PROPHET. LSTM;

This refer s to the machine languages developed by the human being with the

recurrent neutral network architecture. This is fundamental technique used in the

fields of machine learning methods. On the other hand, networks that are neutral are

sometimes called standard feedforward. By considering Long short term memory, the

STATISTICS 9

connections of feedback which change the values into computers of general purpose

computes anything that machines perform (Haider et al, 2019). They are used in

predicting sequence problems especially in complex ones like machine translation and

recognition of the speech.

The other technique in time series is called PROPHET, this involves the

prediction of data based on time. It is further based on the additive model whereby it

involves the trends that are non-linear and plotted out. The data about Facebook

Prophet can be categorized in terms of monthly, monthly and so on (Taylor

&Letham,2017). It is hard for many machine learning methods to give high quality

predictions since it requires substantial requirement of experience and ‘specific

skills’. This method allows both the non-experts and the experts in the field of

forecast the quality.

Generally, ARIMA technique provides specific and well understandable

results that prevail in the day today businesses and other organizations compared to

others techniques of prediction about time series data. It provides simple and clear

models such as the linear trends which are used to compare prices, sales and

profitability of levels of the businesses. This is because ARIMA models behave to be

the best statistical models since they provide technical considerations for the

businessmen to predict their prices, sales and other variables in question. This

therefore shows that ARIMA models are vital as per data that depend on time is

concerned.

Related Studies

The study conducted by McNally in 2018 on the techniques of modelling time

series data using LSTM other than ARIMA methods. McNally focused on the opening

connections of feedback which change the values into computers of general purpose

computes anything that machines perform (Haider et al, 2019). They are used in

predicting sequence problems especially in complex ones like machine translation and

recognition of the speech.

The other technique in time series is called PROPHET, this involves the

prediction of data based on time. It is further based on the additive model whereby it

involves the trends that are non-linear and plotted out. The data about Facebook

Prophet can be categorized in terms of monthly, monthly and so on (Taylor

&Letham,2017). It is hard for many machine learning methods to give high quality

predictions since it requires substantial requirement of experience and ‘specific

skills’. This method allows both the non-experts and the experts in the field of

forecast the quality.

Generally, ARIMA technique provides specific and well understandable

results that prevail in the day today businesses and other organizations compared to

others techniques of prediction about time series data. It provides simple and clear

models such as the linear trends which are used to compare prices, sales and

profitability of levels of the businesses. This is because ARIMA models behave to be

the best statistical models since they provide technical considerations for the

businessmen to predict their prices, sales and other variables in question. This

therefore shows that ARIMA models are vital as per data that depend on time is

concerned.

Related Studies

The study conducted by McNally in 2018 on the techniques of modelling time

series data using LSTM other than ARIMA methods. McNally focused on the opening

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS 10

and closing values of the cryptocurrencies using LSTM methods of prediction. He

found out that the accuracy level of the currency using open values was 52.8% with

its corresponding RSME of 5.5% (McNally, 2018).

Andrew (2018) conducted a study on the exploration on interconnections of

cryptocurrencies by the use of neutral networks such as ARIMA and PROPHET

models. The research investigated on the values that are zeroed on the time factor

about evaluation of prices. The models such as ARIMA and PROPHET identified

important features about the data sets of the prices forecasted.

6. Conclusions

In conclusion, selecting the model is regarded as a problem or a difficulty

while using machine learning methods for predictions. One of the ways how such a

problem can be evaluated is to separate several data into train and sets of tests for

computations of errors after understanding technique used to forecast time series data.

The basics of ARIMA models and time series prediction has been explained above.

While selecting machine learning model for forecasting, it is not easy to choose the

clear idea of which approach to use since all of them as discussed in this paper

provides forecasting of the time series data. Most significant is that, before reaching

to the ‘sophisticated time series data’ some other models that form the fountain of

further predictions. It is believed that if the complicated methods do not provide and

yield reliable results, therefore there is no need of using such methods. However,

several procedures while using the ARIMA models in order to present the clear results

about time series data. However, the degree defers in terms of preciseness, clarity,

consistency, unbiasedness and others. It is evident that, without metrics in business or

any other organization, management may become nebulous. Estimation and

Prediction of the data about the variables helps organizations to tell whether they are

incurring profits or losses and even forecasting future outcomes basing on the

historical phenomenon. With ARIMA models, each business can be in position to

measure the success and set targets from the policies made after estimations of the

and closing values of the cryptocurrencies using LSTM methods of prediction. He

found out that the accuracy level of the currency using open values was 52.8% with

its corresponding RSME of 5.5% (McNally, 2018).

Andrew (2018) conducted a study on the exploration on interconnections of

cryptocurrencies by the use of neutral networks such as ARIMA and PROPHET

models. The research investigated on the values that are zeroed on the time factor

about evaluation of prices. The models such as ARIMA and PROPHET identified

important features about the data sets of the prices forecasted.

6. Conclusions

In conclusion, selecting the model is regarded as a problem or a difficulty

while using machine learning methods for predictions. One of the ways how such a

problem can be evaluated is to separate several data into train and sets of tests for

computations of errors after understanding technique used to forecast time series data.

The basics of ARIMA models and time series prediction has been explained above.

While selecting machine learning model for forecasting, it is not easy to choose the

clear idea of which approach to use since all of them as discussed in this paper

provides forecasting of the time series data. Most significant is that, before reaching

to the ‘sophisticated time series data’ some other models that form the fountain of

further predictions. It is believed that if the complicated methods do not provide and

yield reliable results, therefore there is no need of using such methods. However,

several procedures while using the ARIMA models in order to present the clear results

about time series data. However, the degree defers in terms of preciseness, clarity,

consistency, unbiasedness and others. It is evident that, without metrics in business or

any other organization, management may become nebulous. Estimation and

Prediction of the data about the variables helps organizations to tell whether they are

incurring profits or losses and even forecasting future outcomes basing on the

historical phenomenon. With ARIMA models, each business can be in position to

measure the success and set targets from the policies made after estimations of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS 11

data.

List of References

Alsharif, A.M., Younes, K.M. & Kim, J. 2019. Time Series ARIMA Model for

Prediction of Daily and Monthly Average Global Solar Radiation: The Case Study of

Seoul, South Korea. Retrieved from: https://www.mdpi.com/2073-8994/11/2/240

Haider , S. A., Naqvi S.R , Akram, T. Umar, A.G. , Shahzad, A. , Sial, M.R.,

ICDM. 2018a. 20th International Conference on Data Mining. Retrieved from:

http://www.wikicfp.com/cfp/servlet/event.showcfp?eventid=66339

ICDM. 2018 b. The 2018 IEEE International Conference on Data

Mining. Retrieved from:

http://www2.kansai-u.ac.jp/dslab/workshop/2018/DMS2018/

Khaliq, S. & Kamran, M. 2019. LSTM Neural Network Based Forecasting Model for

Wheat Production in Pakistan. Retrieved from: https://www.mdpi.com/2073-

4395/9/2/72

Lucey, B. M., Vigne, S. A., Ballester, L., Barbopoulos, L., Brzeszczynski, J.,

Carchano, O., Zaghini, A. 2018. Future directions in international financial

integration research - A crowdsourced perspective. International Review of Financial

Analysis, 55, 35–49.

MacNally, S. 2018. Predicting the Price of Bitcoin Using Machine Learning.

Retrieved from:

https://www.researchgate.net/publication/325633087_Predicting_the_Price_of_Bitcoi

n_Using _Machine_Learning

Sapankevych, I.N. & Sankar, R. 2009. Time Series Prediction Using Support Vector

Machines: A Survey. Publisher: IEEE. Retrieved from:

https://ieeexplore.ieee.org/document/4840324/references#references

Taylor S. &, Letham, B. 2017. Forecasting at scale. Retrieved from:

https://peerj.com/preprints/3190/

Vigne, S. A., Lucey, B. M., O’Connor, F. A., &Yarovaya, L. 2017. The financial

data.

List of References

Alsharif, A.M., Younes, K.M. & Kim, J. 2019. Time Series ARIMA Model for

Prediction of Daily and Monthly Average Global Solar Radiation: The Case Study of

Seoul, South Korea. Retrieved from: https://www.mdpi.com/2073-8994/11/2/240

Haider , S. A., Naqvi S.R , Akram, T. Umar, A.G. , Shahzad, A. , Sial, M.R.,

ICDM. 2018a. 20th International Conference on Data Mining. Retrieved from:

http://www.wikicfp.com/cfp/servlet/event.showcfp?eventid=66339

ICDM. 2018 b. The 2018 IEEE International Conference on Data

Mining. Retrieved from:

http://www2.kansai-u.ac.jp/dslab/workshop/2018/DMS2018/

Khaliq, S. & Kamran, M. 2019. LSTM Neural Network Based Forecasting Model for

Wheat Production in Pakistan. Retrieved from: https://www.mdpi.com/2073-

4395/9/2/72

Lucey, B. M., Vigne, S. A., Ballester, L., Barbopoulos, L., Brzeszczynski, J.,

Carchano, O., Zaghini, A. 2018. Future directions in international financial

integration research - A crowdsourced perspective. International Review of Financial

Analysis, 55, 35–49.

MacNally, S. 2018. Predicting the Price of Bitcoin Using Machine Learning.

Retrieved from:

https://www.researchgate.net/publication/325633087_Predicting_the_Price_of_Bitcoi

n_Using _Machine_Learning

Sapankevych, I.N. & Sankar, R. 2009. Time Series Prediction Using Support Vector

Machines: A Survey. Publisher: IEEE. Retrieved from:

https://ieeexplore.ieee.org/document/4840324/references#references

Taylor S. &, Letham, B. 2017. Forecasting at scale. Retrieved from:

https://peerj.com/preprints/3190/

Vigne, S. A., Lucey, B. M., O’Connor, F. A., &Yarovaya, L. 2017. The financial

STATISTICS 12

economics of white precious metals-A survey. International Review of Financial

Analysis, 52, 292—30 8.

economics of white precious metals-A survey. International Review of Financial

Analysis, 52, 292—30 8.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.