Time Series Analysis and Cointegration Assignment, ECN2005

VerifiedAdded on 2022/08/27

|14

|1646

|34

Homework Assignment

AI Summary

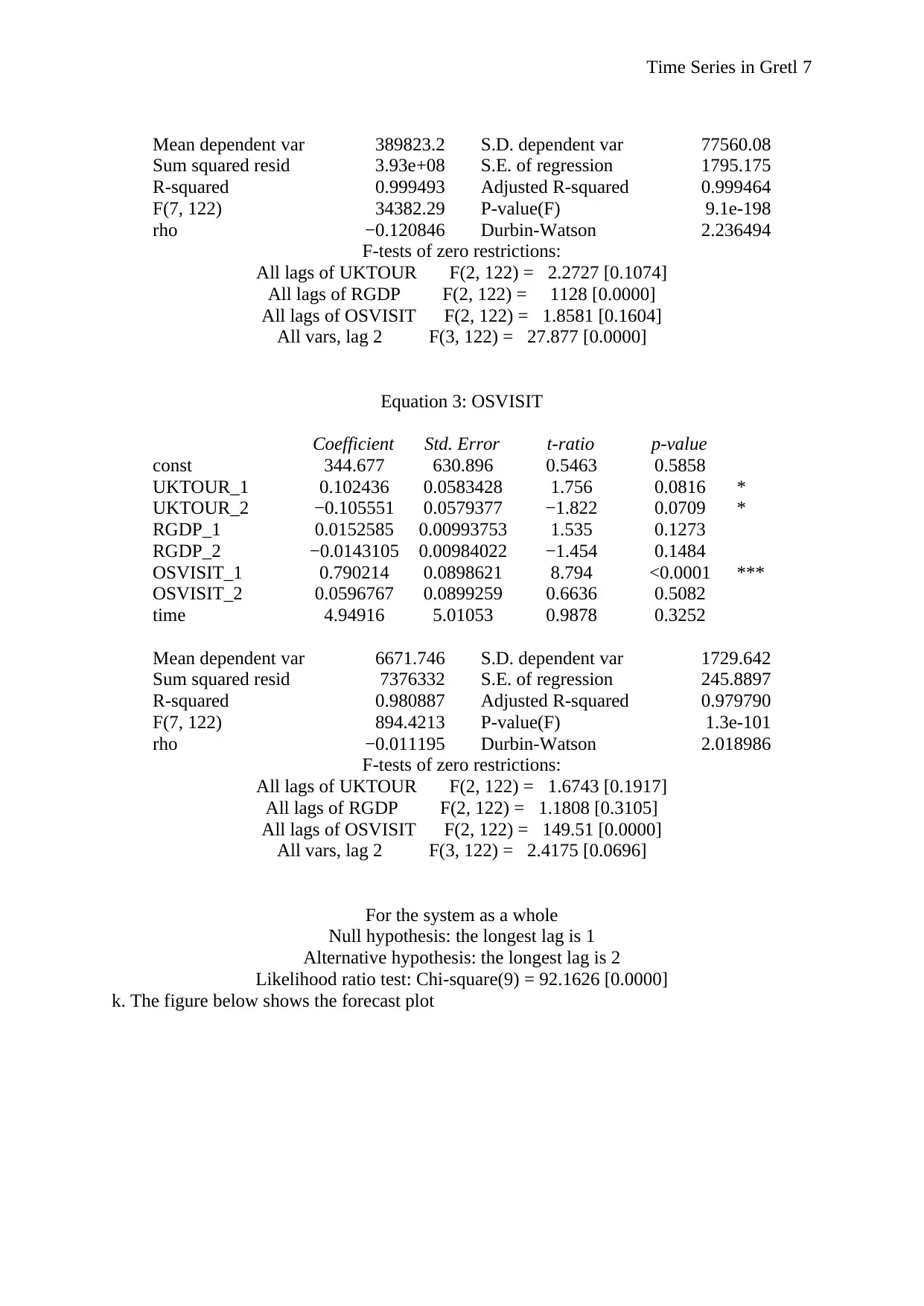

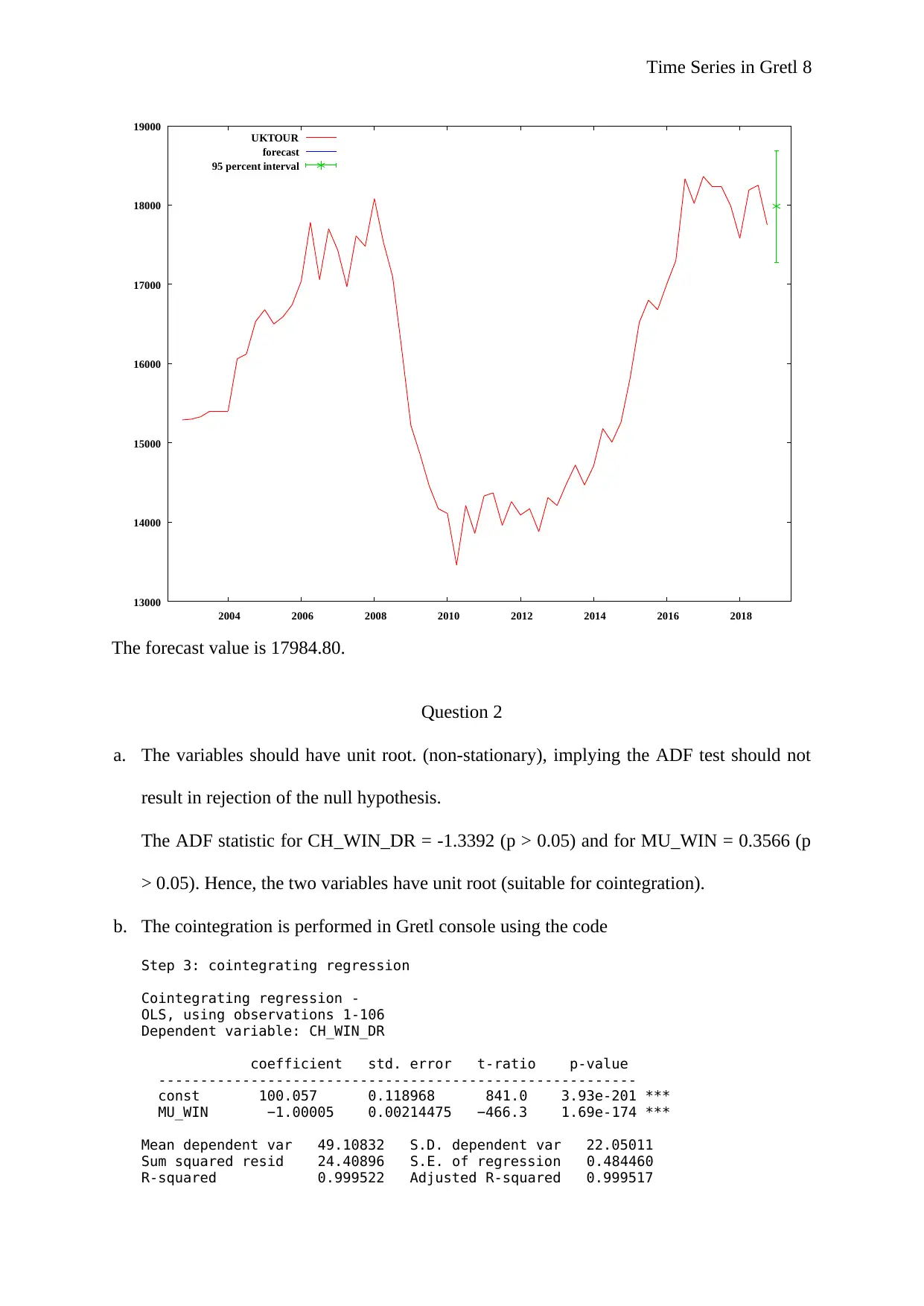

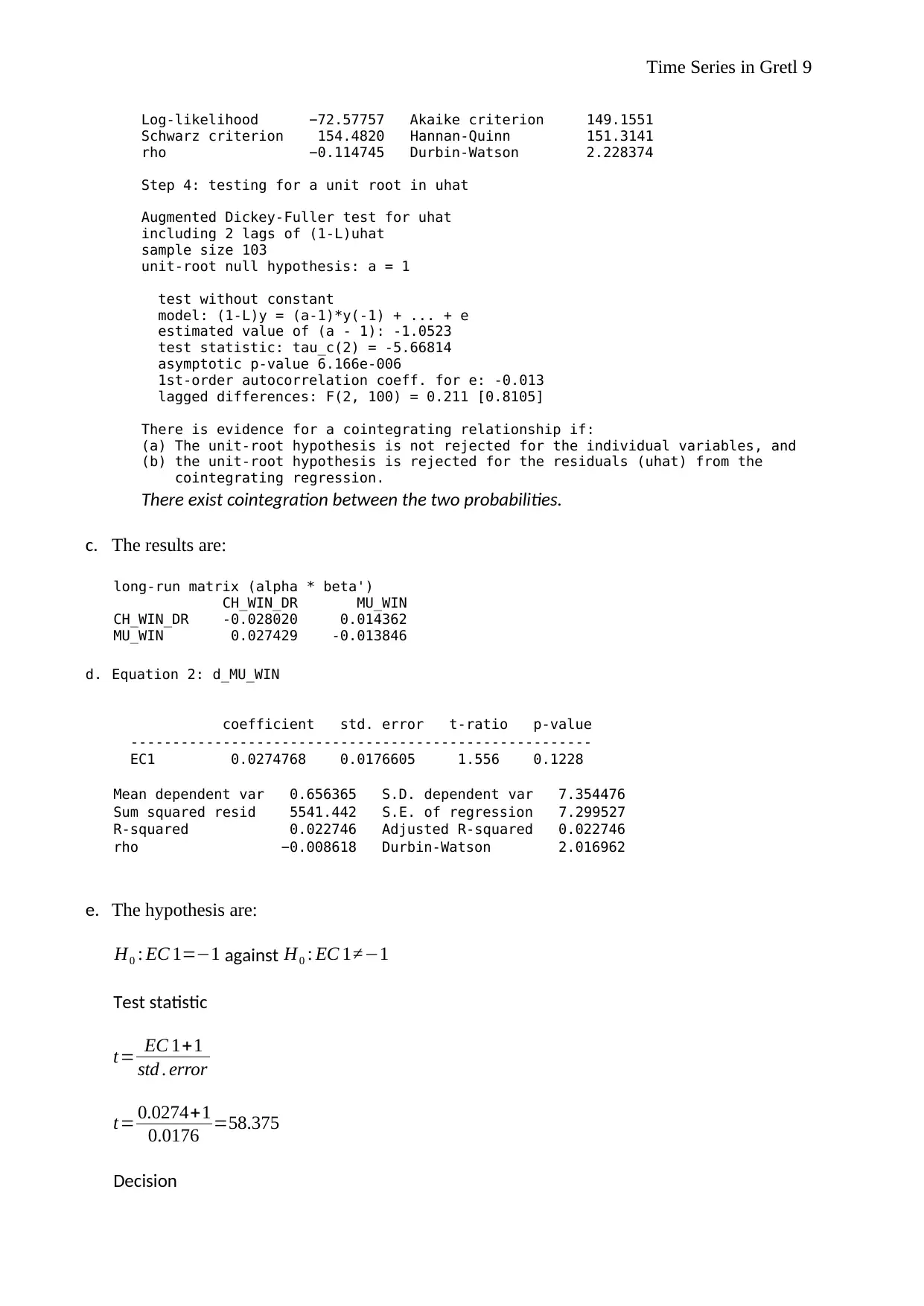

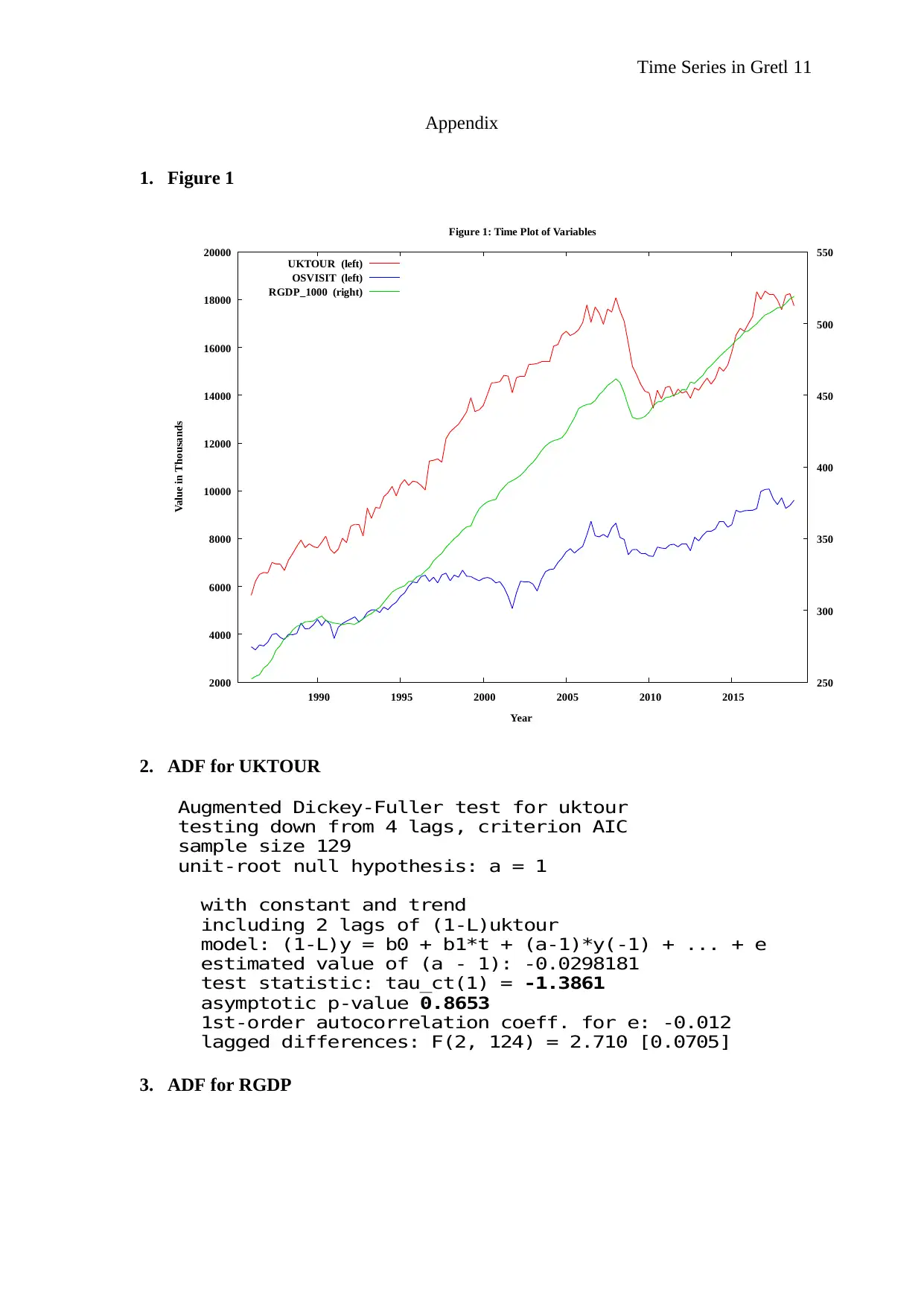

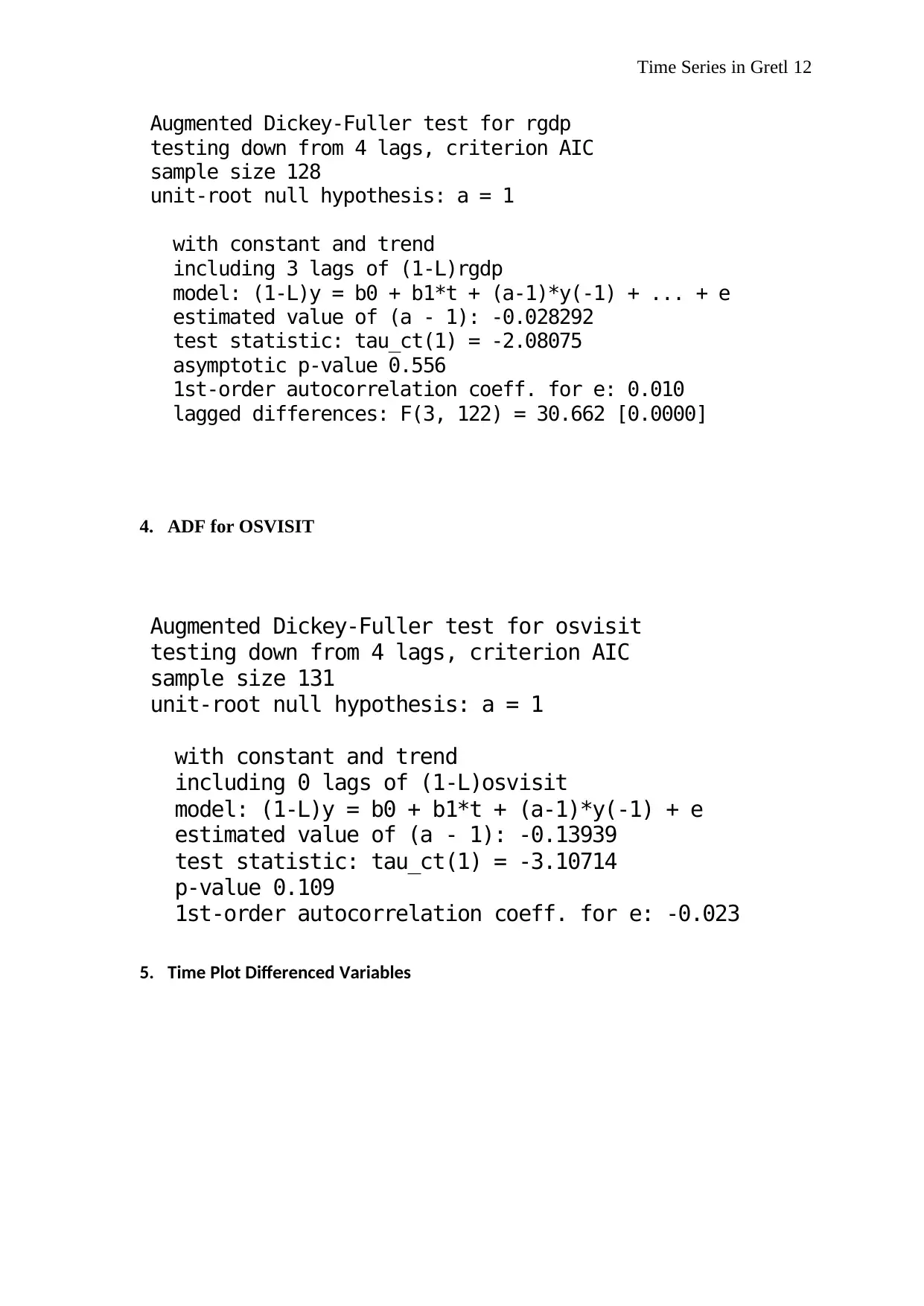

This document presents a comprehensive solution to a time series econometrics assignment for the ECN2005 course. The assignment utilizes the Gretl software to analyze quarterly data on UK real GDP, outbound tourist visits, and inbound tourist visits. The solution includes the application of Augmented Dickey-Fuller (ADF) tests to assess unit roots, transformations to achieve stationarity, and the development of Vector Autoregression (VAR) and Autoregressive Distributed Lag (ARDL) models. The analysis covers model specification, estimation, interpretation of coefficients, and the calculation of long-run elasticities. Furthermore, the solution investigates cointegration between variables and employs error correction models (ECM). The document provides detailed Gretl output, interpretations, and statistical tests, including the Quandt likelihood ratio test and portmanteau tests, to evaluate model validity and significance. The assignment covers topics like time series analysis, unit root testing, cointegration, VAR modeling, ARDL modeling, and error correction models.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.