Finance Assignment: Time Value, Investment Analysis, Capital Budgeting

VerifiedAdded on 2021/06/17

|15

|3500

|34

Homework Assignment

AI Summary

This finance assignment solution covers a range of topics, including time value of money, investment analysis, and capital budgeting. The first question involves a two-period certainty model, calculating consumption and understanding dividend payouts. The second question deals with annual equivalent costs and valuation of interest-bearing securities. The third question focuses on time value of money, deferred annuities, and loan repayments, including effective annual interest rate, monthly repayments, and loan terms. The final question delves into capital budgeting, analyzing cash flows for mutually exclusive projects, calculating payback periods, net present values, profitability indexes, internal rates of return, and crossover points. The assignment provides detailed calculations and explanations for each problem, offering a comprehensive understanding of financial concepts and decision-making processes.

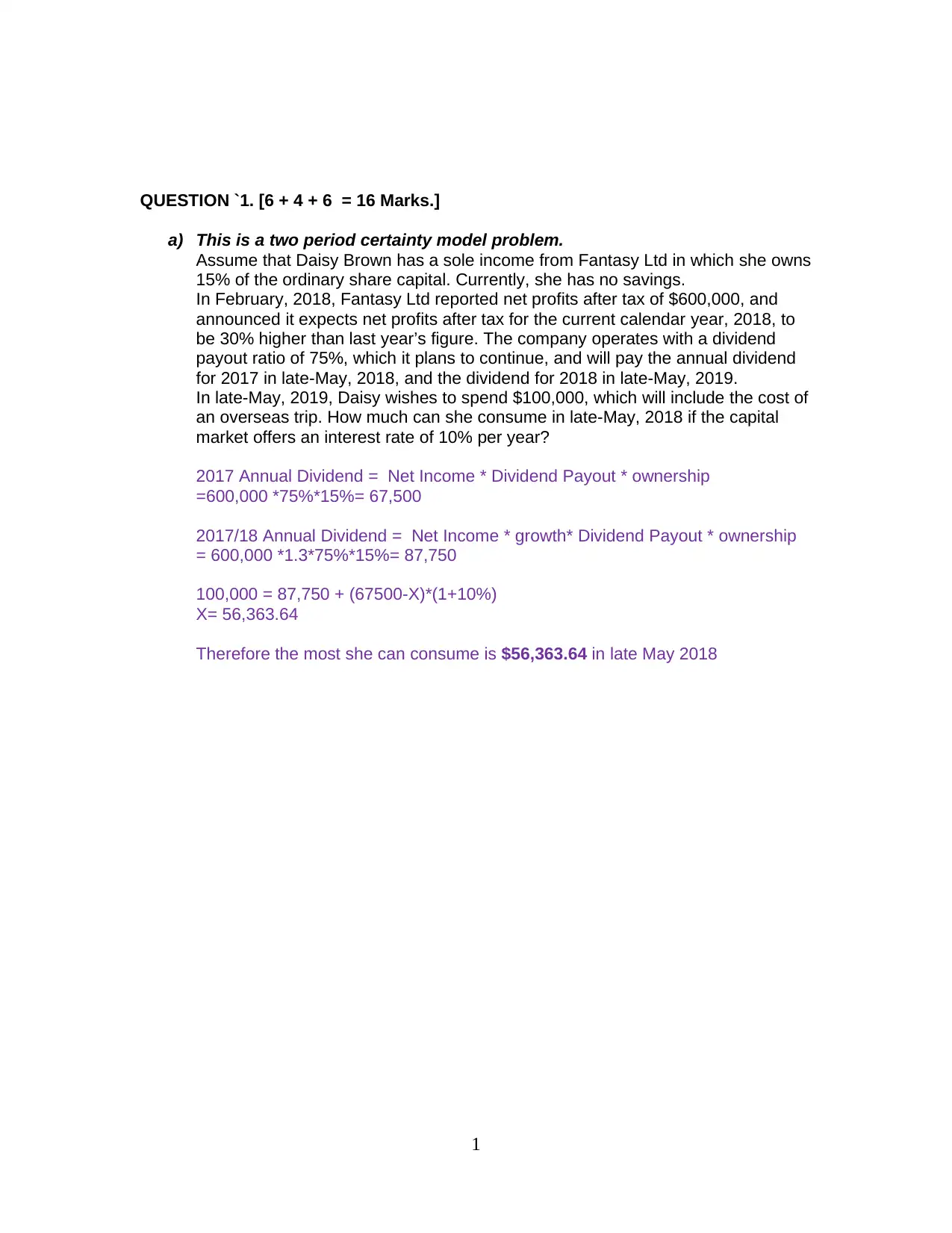

QUESTION `1. [6 + 4 + 6 = 16 Marks.]

a) This is a two period certainty model problem.

Assume that Daisy Brown has a sole income from Fantasy Ltd in which she owns

15% of the ordinary share capital. Currently, she has no savings.

In February, 2018, Fantasy Ltd reported net profits after tax of $600,000, and

announced it expects net profits after tax for the current calendar year, 2018, to

be 30% higher than last year’s figure. The company operates with a dividend

payout ratio of 75%, which it plans to continue, and will pay the annual dividend

for 2017 in late-May, 2018, and the dividend for 2018 in late-May, 2019.

In late-May, 2019, Daisy wishes to spend $100,000, which will include the cost of

an overseas trip. How much can she consume in late-May, 2018 if the capital

market offers an interest rate of 10% per year?

2017 Annual Dividend = Net Income * Dividend Payout * ownership

=600,000 *75%*15%= 67,500

2017/18 Annual Dividend = Net Income * growth* Dividend Payout * ownership

= 600,000 *1.3*75%*15%= 87,750

100,000 = 87,750 + (67500-X)*(1+10%)

X= 56,363.64

Therefore the most she can consume is $56,363.64 in late May 2018

1

a) This is a two period certainty model problem.

Assume that Daisy Brown has a sole income from Fantasy Ltd in which she owns

15% of the ordinary share capital. Currently, she has no savings.

In February, 2018, Fantasy Ltd reported net profits after tax of $600,000, and

announced it expects net profits after tax for the current calendar year, 2018, to

be 30% higher than last year’s figure. The company operates with a dividend

payout ratio of 75%, which it plans to continue, and will pay the annual dividend

for 2017 in late-May, 2018, and the dividend for 2018 in late-May, 2019.

In late-May, 2019, Daisy wishes to spend $100,000, which will include the cost of

an overseas trip. How much can she consume in late-May, 2018 if the capital

market offers an interest rate of 10% per year?

2017 Annual Dividend = Net Income * Dividend Payout * ownership

=600,000 *75%*15%= 67,500

2017/18 Annual Dividend = Net Income * growth* Dividend Payout * ownership

= 600,000 *1.3*75%*15%= 87,750

100,000 = 87,750 + (67500-X)*(1+10%)

X= 56,363.64

Therefore the most she can consume is $56,363.64 in late May 2018

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

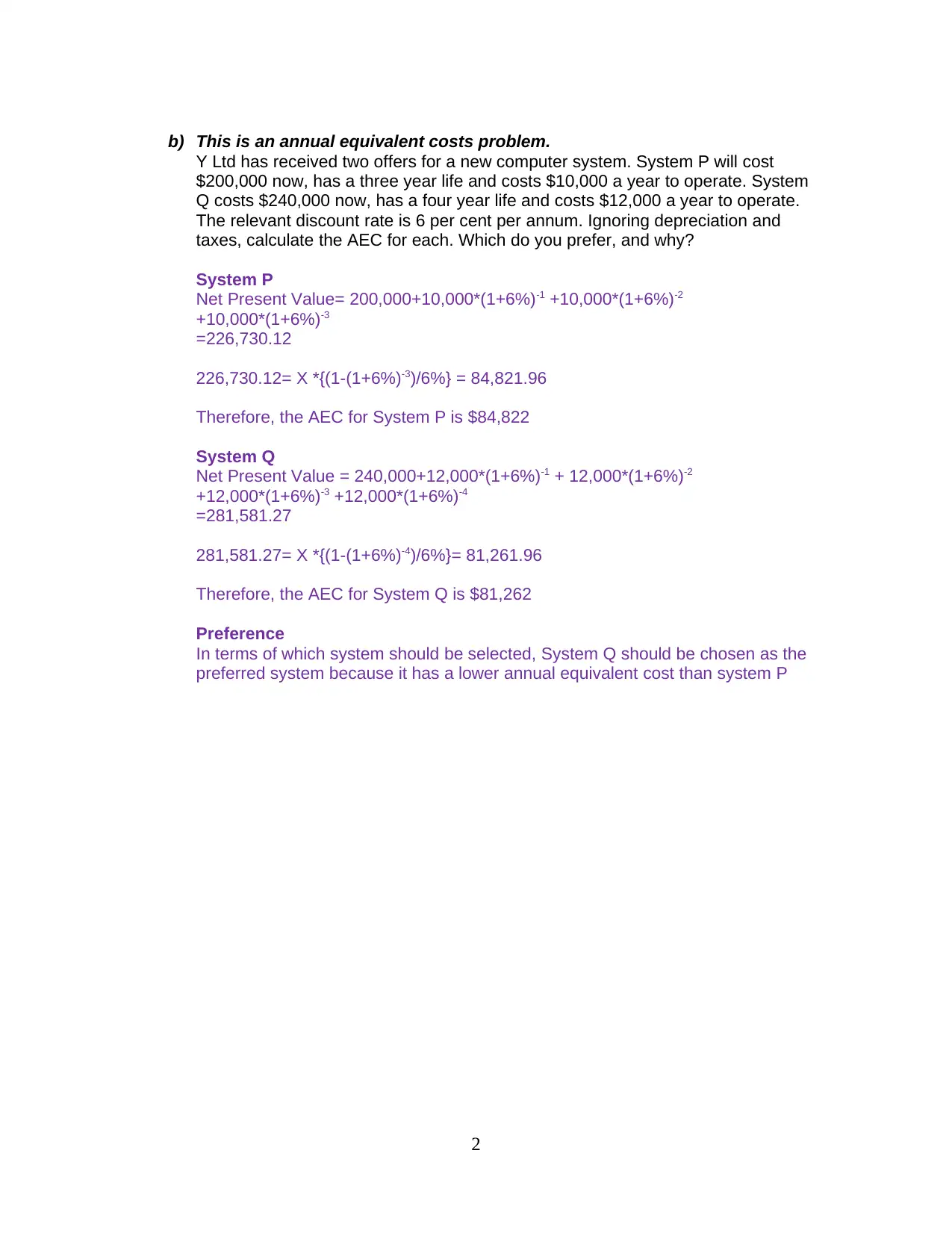

b) This is an annual equivalent costs problem.

Y Ltd has received two offers for a new computer system. System P will cost

$200,000 now, has a three year life and costs $10,000 a year to operate. System

Q costs $240,000 now, has a four year life and costs $12,000 a year to operate.

The relevant discount rate is 6 per cent per annum. Ignoring depreciation and

taxes, calculate the AEC for each. Which do you prefer, and why?

System P

Net Present Value= 200,000+10,000*(1+6%)-1 +10,000*(1+6%)-2

+10,000*(1+6%)-3

=226,730.12

226,730.12= X *{(1-(1+6%)-3)/6%} = 84,821.96

Therefore, the AEC for System P is $84,822

System Q

Net Present Value = 240,000+12,000*(1+6%)-1 + 12,000*(1+6%)-2

+12,000*(1+6%)-3 +12,000*(1+6%)-4

=281,581.27

281,581.27= X *{(1-(1+6%)-4)/6%}= 81,261.96

Therefore, the AEC for System Q is $81,262

Preference

In terms of which system should be selected, System Q should be chosen as the

preferred system because it has a lower annual equivalent cost than system P

2

Y Ltd has received two offers for a new computer system. System P will cost

$200,000 now, has a three year life and costs $10,000 a year to operate. System

Q costs $240,000 now, has a four year life and costs $12,000 a year to operate.

The relevant discount rate is 6 per cent per annum. Ignoring depreciation and

taxes, calculate the AEC for each. Which do you prefer, and why?

System P

Net Present Value= 200,000+10,000*(1+6%)-1 +10,000*(1+6%)-2

+10,000*(1+6%)-3

=226,730.12

226,730.12= X *{(1-(1+6%)-3)/6%} = 84,821.96

Therefore, the AEC for System P is $84,822

System Q

Net Present Value = 240,000+12,000*(1+6%)-1 + 12,000*(1+6%)-2

+12,000*(1+6%)-3 +12,000*(1+6%)-4

=281,581.27

281,581.27= X *{(1-(1+6%)-4)/6%}= 81,261.96

Therefore, the AEC for System Q is $81,262

Preference

In terms of which system should be selected, System Q should be chosen as the

preferred system because it has a lower annual equivalent cost than system P

2

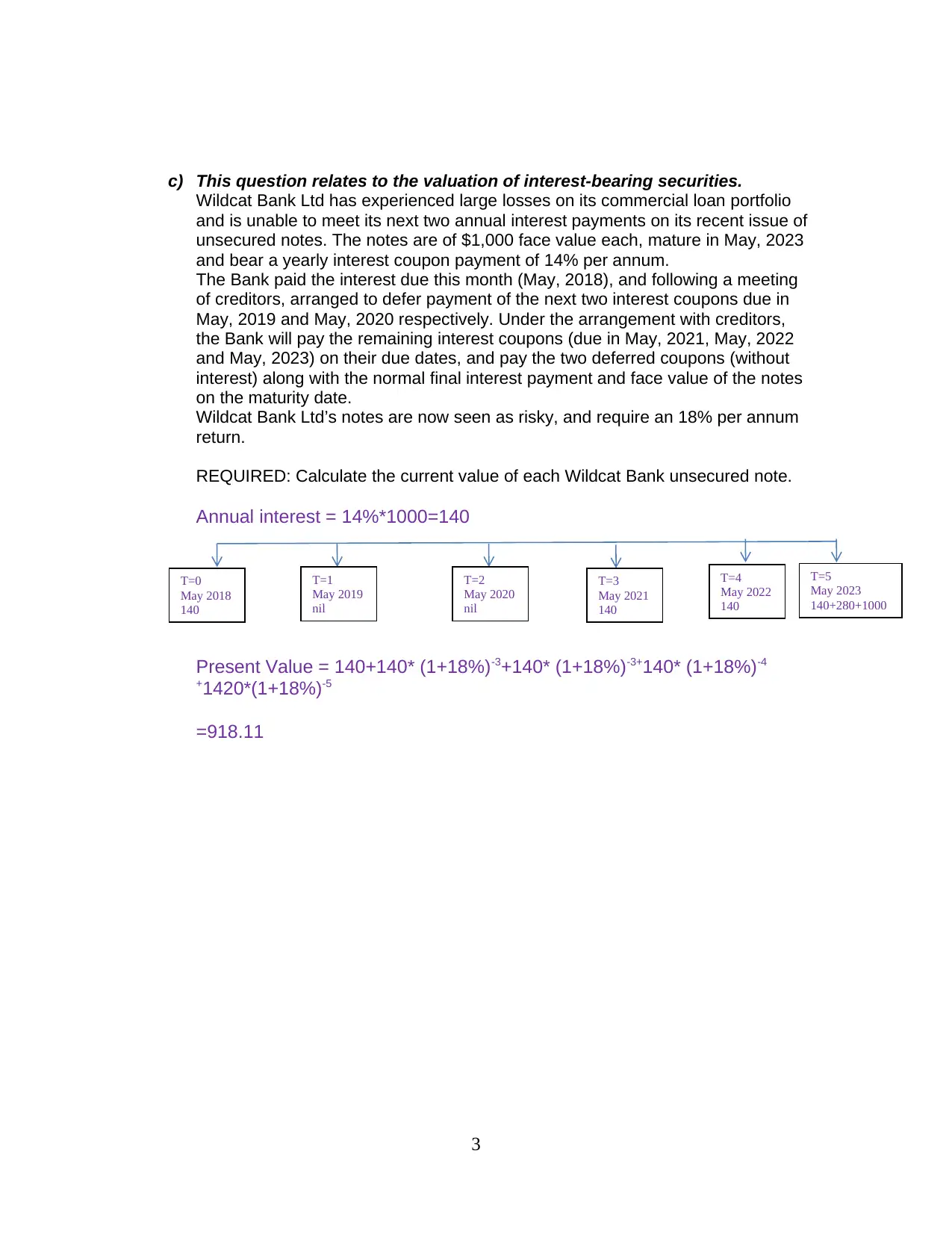

c) This question relates to the valuation of interest-bearing securities.

Wildcat Bank Ltd has experienced large losses on its commercial loan portfolio

and is unable to meet its next two annual interest payments on its recent issue of

unsecured notes. The notes are of $1,000 face value each, mature in May, 2023

and bear a yearly interest coupon payment of 14% per annum.

The Bank paid the interest due this month (May, 2018), and following a meeting

of creditors, arranged to defer payment of the next two interest coupons due in

May, 2019 and May, 2020 respectively. Under the arrangement with creditors,

the Bank will pay the remaining interest coupons (due in May, 2021, May, 2022

and May, 2023) on their due dates, and pay the two deferred coupons (without

interest) along with the normal final interest payment and face value of the notes

on the maturity date.

Wildcat Bank Ltd’s notes are now seen as risky, and require an 18% per annum

return.

REQUIRED: Calculate the current value of each Wildcat Bank unsecured note.

Annual interest = 14%*1000=140

Present Value = 140+140* (1+18%)-3+140* (1+18%)-3+140* (1+18%)-4

+1420*(1+18%)-5

=918.11

3

T=0

May 2018

140

T=5

May 2023

140+280+1000

T=4

May 2022

140

T=3

May 2021

140

T=2

May 2020

nil

T=1

May 2019

nil

Wildcat Bank Ltd has experienced large losses on its commercial loan portfolio

and is unable to meet its next two annual interest payments on its recent issue of

unsecured notes. The notes are of $1,000 face value each, mature in May, 2023

and bear a yearly interest coupon payment of 14% per annum.

The Bank paid the interest due this month (May, 2018), and following a meeting

of creditors, arranged to defer payment of the next two interest coupons due in

May, 2019 and May, 2020 respectively. Under the arrangement with creditors,

the Bank will pay the remaining interest coupons (due in May, 2021, May, 2022

and May, 2023) on their due dates, and pay the two deferred coupons (without

interest) along with the normal final interest payment and face value of the notes

on the maturity date.

Wildcat Bank Ltd’s notes are now seen as risky, and require an 18% per annum

return.

REQUIRED: Calculate the current value of each Wildcat Bank unsecured note.

Annual interest = 14%*1000=140

Present Value = 140+140* (1+18%)-3+140* (1+18%)-3+140* (1+18%)-4

+1420*(1+18%)-5

=918.11

3

T=0

May 2018

140

T=5

May 2023

140+280+1000

T=4

May 2022

140

T=3

May 2021

140

T=2

May 2020

nil

T=1

May 2019

nil

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

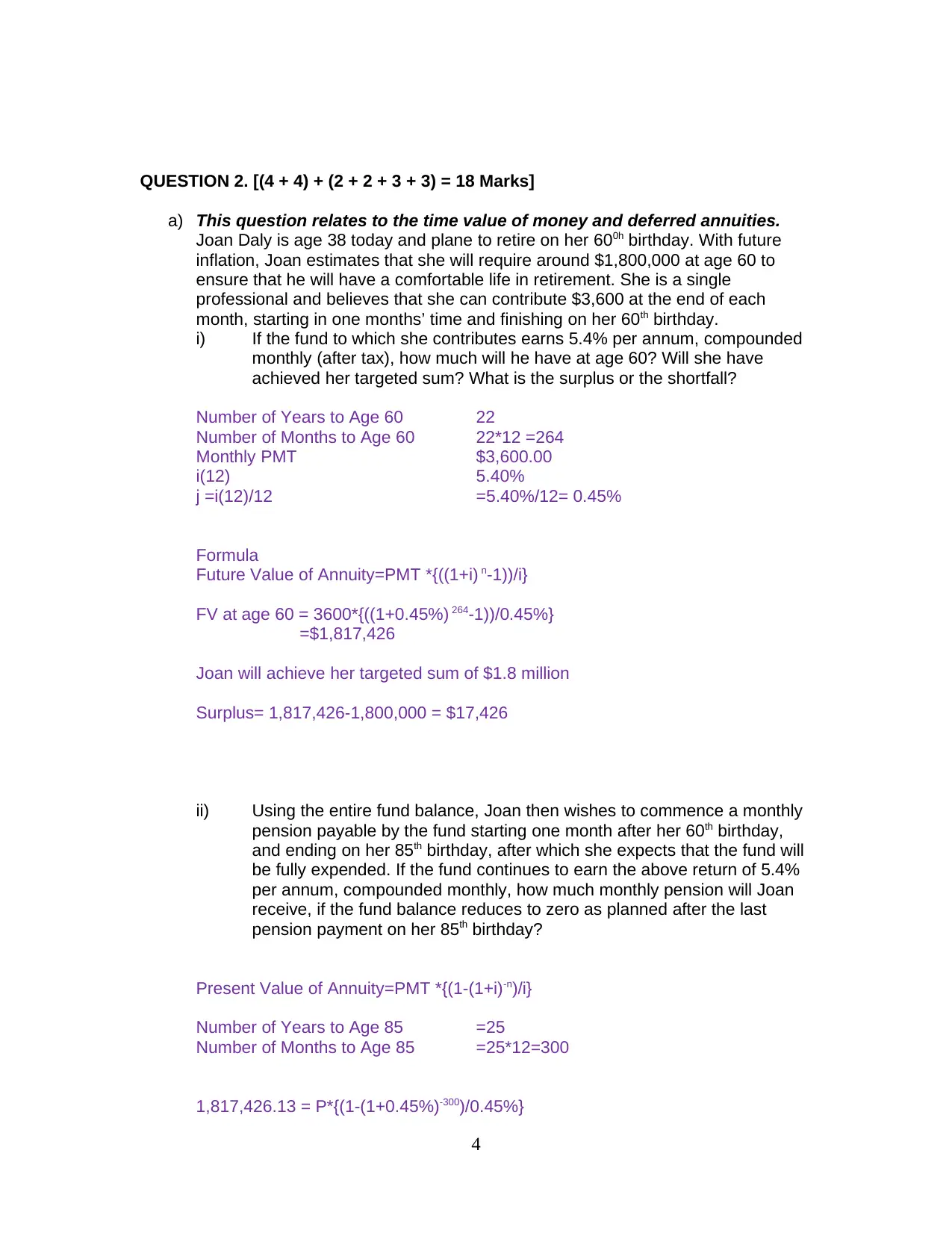

QUESTION 2. [(4 + 4) + (2 + 2 + 3 + 3) = 18 Marks]

a) This question relates to the time value of money and deferred annuities.

Joan Daly is age 38 today and plane to retire on her 600h birthday. With future

inflation, Joan estimates that she will require around $1,800,000 at age 60 to

ensure that he will have a comfortable life in retirement. She is a single

professional and believes that she can contribute $3,600 at the end of each

month, starting in one months’ time and finishing on her 60th birthday.

i) If the fund to which she contributes earns 5.4% per annum, compounded

monthly (after tax), how much will he have at age 60? Will she have

achieved her targeted sum? What is the surplus or the shortfall?

Number of Years to Age 60 22

Number of Months to Age 60 22*12 =264

Monthly PMT $3,600.00

i(12) 5.40%

j =i(12)/12 =5.40%/12= 0.45%

Formula

Future Value of Annuity=PMT *{((1+i) n-1))/i}

FV at age 60 = 3600*{((1+0.45%) 264-1))/0.45%}

=$1,817,426

Joan will achieve her targeted sum of $1.8 million

Surplus= 1,817,426-1,800,000 = $17,426

ii) Using the entire fund balance, Joan then wishes to commence a monthly

pension payable by the fund starting one month after her 60th birthday,

and ending on her 85th birthday, after which she expects that the fund will

be fully expended. If the fund continues to earn the above return of 5.4%

per annum, compounded monthly, how much monthly pension will Joan

receive, if the fund balance reduces to zero as planned after the last

pension payment on her 85th birthday?

Present Value of Annuity=PMT *{(1-(1+i)-n)/i}

Number of Years to Age 85 =25

Number of Months to Age 85 =25*12=300

1,817,426.13 = P*{(1-(1+0.45%)-300)/0.45%}

4

a) This question relates to the time value of money and deferred annuities.

Joan Daly is age 38 today and plane to retire on her 600h birthday. With future

inflation, Joan estimates that she will require around $1,800,000 at age 60 to

ensure that he will have a comfortable life in retirement. She is a single

professional and believes that she can contribute $3,600 at the end of each

month, starting in one months’ time and finishing on her 60th birthday.

i) If the fund to which she contributes earns 5.4% per annum, compounded

monthly (after tax), how much will he have at age 60? Will she have

achieved her targeted sum? What is the surplus or the shortfall?

Number of Years to Age 60 22

Number of Months to Age 60 22*12 =264

Monthly PMT $3,600.00

i(12) 5.40%

j =i(12)/12 =5.40%/12= 0.45%

Formula

Future Value of Annuity=PMT *{((1+i) n-1))/i}

FV at age 60 = 3600*{((1+0.45%) 264-1))/0.45%}

=$1,817,426

Joan will achieve her targeted sum of $1.8 million

Surplus= 1,817,426-1,800,000 = $17,426

ii) Using the entire fund balance, Joan then wishes to commence a monthly

pension payable by the fund starting one month after her 60th birthday,

and ending on her 85th birthday, after which she expects that the fund will

be fully expended. If the fund continues to earn the above return of 5.4%

per annum, compounded monthly, how much monthly pension will Joan

receive, if the fund balance reduces to zero as planned after the last

pension payment on her 85th birthday?

Present Value of Annuity=PMT *{(1-(1+i)-n)/i}

Number of Years to Age 85 =25

Number of Months to Age 85 =25*12=300

1,817,426.13 = P*{(1-(1+0.45%)-300)/0.45%}

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P=1,817,426.13/{(1-(1+0.45%)-300)/0.45%}

P=11,052.31

Joan will receive a monthly pension of $11,052.31

b) This question relates to loan repayments and loan terms.

Jack and Jill Jacobs wish to borrow $700,000 to buy a home. The loan from the

Highway Bank requires equal monthly repayments over 20 years, and carries.an

interest rate of 4.2% per annum, compounded monthly. The first repayment is

due at the end of one month after the loan proceeds are received.

You are required to calculate:

i) the effective annual interest rate on the above loan (show as a

percentage, correct to 3 decimal places).

Solve i using Formula

i = (1 + i(n)

n )n -1

Where

i(n)=4.2%

n=12

Therefore

i =( 1+i(12)/12)12-1

i=( 1+4.2%/12)12-1

=4.282%

Therefore, the effective annual interest rate is 4.282%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be paid every month

over the 20 year period of the loan.

Loan Amount 700,000

Number of Months 20 *12=240

i(12) 4.2%

j =4.2%/12= 0.35%

Solve PMT using Formula

Present Value =PMT *{(1-(1+i)-n)/i}

700,000 = PMT*{(1-(1+0.35%)-240)/0.35%}

PMT=700,000/{(1-(1+0.35%)-240)/0.35%}

5

P=11,052.31

Joan will receive a monthly pension of $11,052.31

b) This question relates to loan repayments and loan terms.

Jack and Jill Jacobs wish to borrow $700,000 to buy a home. The loan from the

Highway Bank requires equal monthly repayments over 20 years, and carries.an

interest rate of 4.2% per annum, compounded monthly. The first repayment is

due at the end of one month after the loan proceeds are received.

You are required to calculate:

i) the effective annual interest rate on the above loan (show as a

percentage, correct to 3 decimal places).

Solve i using Formula

i = (1 + i(n)

n )n -1

Where

i(n)=4.2%

n=12

Therefore

i =( 1+i(12)/12)12-1

i=( 1+4.2%/12)12-1

=4.282%

Therefore, the effective annual interest rate is 4.282%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be paid every month

over the 20 year period of the loan.

Loan Amount 700,000

Number of Months 20 *12=240

i(12) 4.2%

j =4.2%/12= 0.35%

Solve PMT using Formula

Present Value =PMT *{(1-(1+i)-n)/i}

700,000 = PMT*{(1-(1+0.35%)-240)/0.35%}

PMT=700,000/{(1-(1+0.35%)-240)/0.35%}

5

PMT=4,316

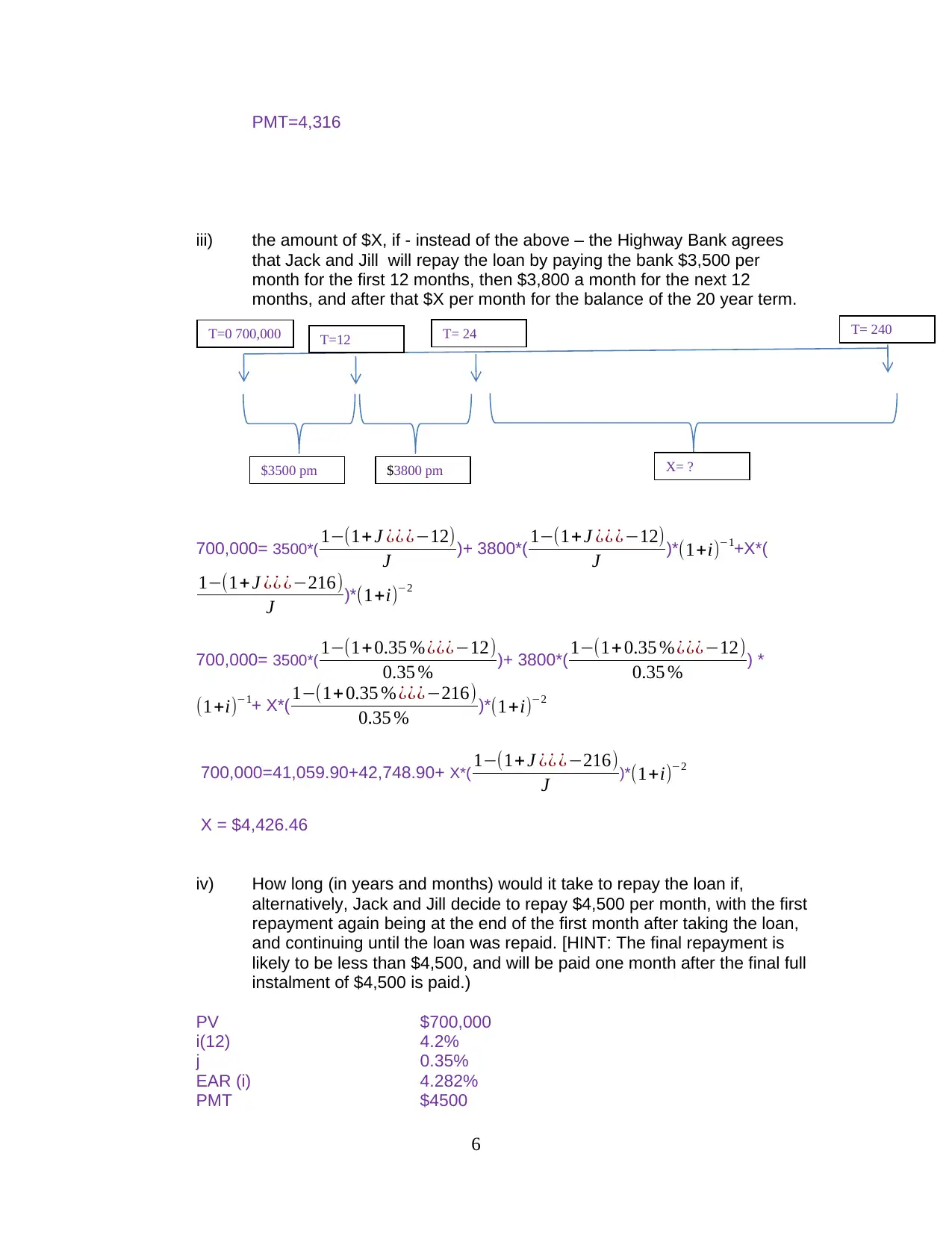

iii) the amount of $X, if - instead of the above – the Highway Bank agrees

that Jack and Jill will repay the loan by paying the bank $3,500 per

month for the first 12 months, then $3,800 a month for the next 12

months, and after that $X per month for the balance of the 20 year term.

700,000= 3500*( 1−(1+ J ¿¿ ¿−12)

J )+ 3800*( 1−(1+ J ¿¿ ¿−12)

J )*(1+i)−1+X*(

1−(1+J ¿¿ ¿−216)

J )*(1+i)−2

700,000= 3500*( 1−(1+0.35 %¿¿¿−12)

0.35 % )+ 3800*( 1−(1+0.35 %¿¿¿−12)

0.35 % ) *

(1+i)−1+ X*( 1−(1+ 0.35 % ¿¿¿−216)

0.35 % )*(1+i)−2

700,000=41,059.90+42,748.90+ X*( 1−(1+ J ¿¿ ¿−216)

J )*(1+i)−2

X = $4,426.46

iv) How long (in years and months) would it take to repay the loan if,

alternatively, Jack and Jill decide to repay $4,500 per month, with the first

repayment again being at the end of the first month after taking the loan,

and continuing until the loan was repaid. [HINT: The final repayment is

likely to be less than $4,500, and will be paid one month after the final full

instalment of $4,500 is paid.)

PV $700,000

i(12) 4.2%

j 0.35%

EAR (i) 4.282%

PMT $4500

6

$3500 pm $3800 pm X= ?

T= 24T=12T=0 700,000 T= 240

iii) the amount of $X, if - instead of the above – the Highway Bank agrees

that Jack and Jill will repay the loan by paying the bank $3,500 per

month for the first 12 months, then $3,800 a month for the next 12

months, and after that $X per month for the balance of the 20 year term.

700,000= 3500*( 1−(1+ J ¿¿ ¿−12)

J )+ 3800*( 1−(1+ J ¿¿ ¿−12)

J )*(1+i)−1+X*(

1−(1+J ¿¿ ¿−216)

J )*(1+i)−2

700,000= 3500*( 1−(1+0.35 %¿¿¿−12)

0.35 % )+ 3800*( 1−(1+0.35 %¿¿¿−12)

0.35 % ) *

(1+i)−1+ X*( 1−(1+ 0.35 % ¿¿¿−216)

0.35 % )*(1+i)−2

700,000=41,059.90+42,748.90+ X*( 1−(1+ J ¿¿ ¿−216)

J )*(1+i)−2

X = $4,426.46

iv) How long (in years and months) would it take to repay the loan if,

alternatively, Jack and Jill decide to repay $4,500 per month, with the first

repayment again being at the end of the first month after taking the loan,

and continuing until the loan was repaid. [HINT: The final repayment is

likely to be less than $4,500, and will be paid one month after the final full

instalment of $4,500 is paid.)

PV $700,000

i(12) 4.2%

j 0.35%

EAR (i) 4.282%

PMT $4500

6

$3500 pm $3800 pm X= ?

T= 24T=12T=0 700,000 T= 240

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Find n?

Solve n using formula

Present Value =PMT *{(1-(1+i)-n)/i}

700,000 =4,500*{(1-(1+0.35%)-n*12)/0.35%}

n = 18.753 years

=18 years 10 months

QUESTION 3. [(2 + 2 + 4 + 3 + 3 + 2 = 16 marks]

This question relates to alternative investment choice techniques

Andrew Hardcastle is considering the following cash flows for two mutually

exclusive projects.

Year Cash Flows, Investment M ($) Cash Flows, Investment N ($)

0 -48,000 -48,000

1 15,000 24,000

2 24,000 24,000

3 36,000 24,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the

payback period for each project, and on this basis, which project would

you prefer?

Assume Payments occur evenly over each year then Pay Back period=

initial investment/periodic cash inflow

Project M:

Periodic cash flow=(15,000+24,000+36,000)/3 = 25,000

Payback period = 48,000/25000= 1.92

Project N:

Periodic cash flow=(24,000+24,000+24,000)/3 = 24,000

Payback period = 48000/24000= 2

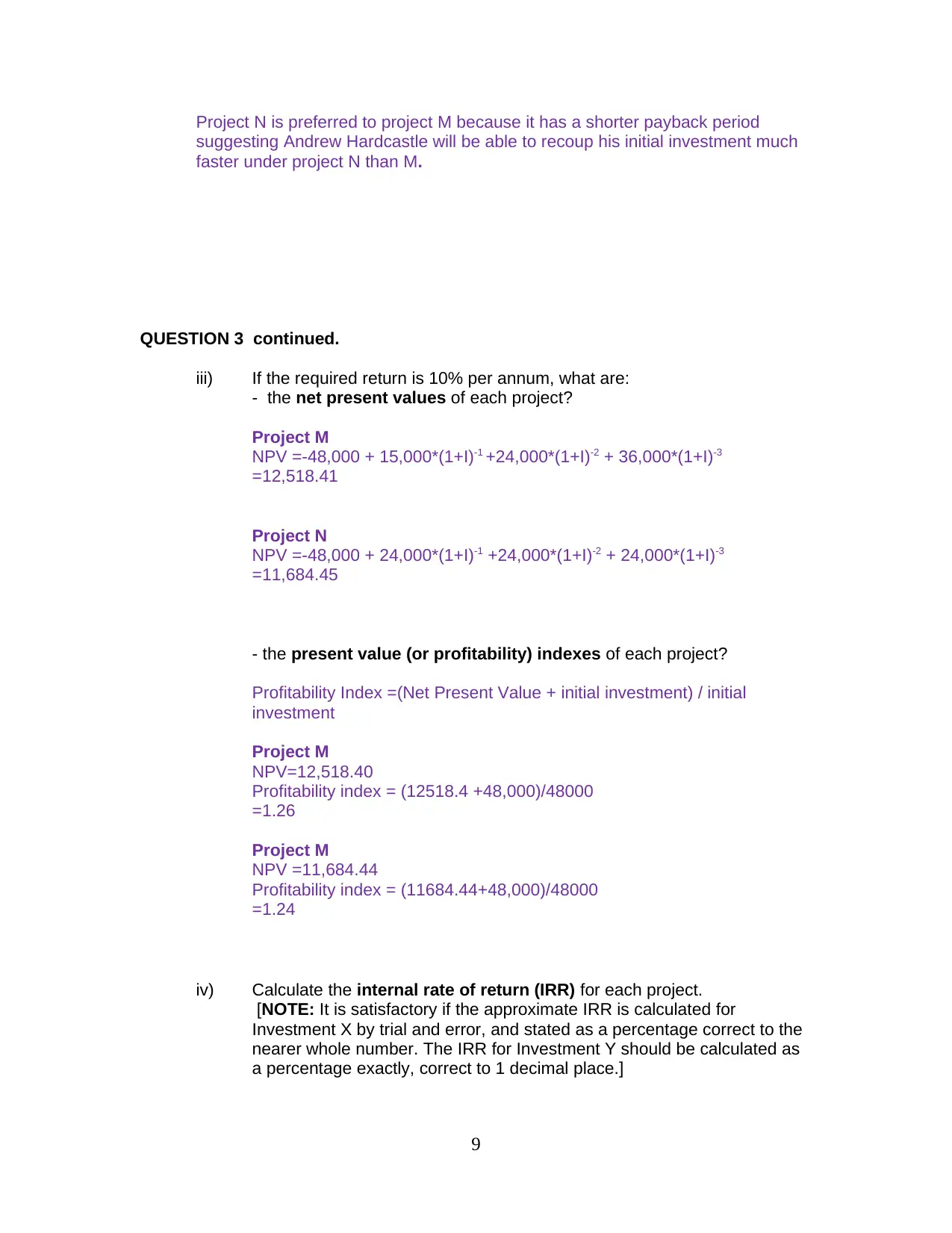

Preferred project- Project M

Reason

Project M is preferred to project N because it has a shorter payback

period suggesting Andrew Hardcastle will be able to recoup his initial

investment much faster under project M than N.

7

Solve n using formula

Present Value =PMT *{(1-(1+i)-n)/i}

700,000 =4,500*{(1-(1+0.35%)-n*12)/0.35%}

n = 18.753 years

=18 years 10 months

QUESTION 3. [(2 + 2 + 4 + 3 + 3 + 2 = 16 marks]

This question relates to alternative investment choice techniques

Andrew Hardcastle is considering the following cash flows for two mutually

exclusive projects.

Year Cash Flows, Investment M ($) Cash Flows, Investment N ($)

0 -48,000 -48,000

1 15,000 24,000

2 24,000 24,000

3 36,000 24,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the

payback period for each project, and on this basis, which project would

you prefer?

Assume Payments occur evenly over each year then Pay Back period=

initial investment/periodic cash inflow

Project M:

Periodic cash flow=(15,000+24,000+36,000)/3 = 25,000

Payback period = 48,000/25000= 1.92

Project N:

Periodic cash flow=(24,000+24,000+24,000)/3 = 24,000

Payback period = 48000/24000= 2

Preferred project- Project M

Reason

Project M is preferred to project N because it has a shorter payback

period suggesting Andrew Hardcastle will be able to recoup his initial

investment much faster under project M than N.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IN THE REMAINING PARTS, ASSUME THAT ALL CASH FLOWS

OCCUR AT THE END OF EACH YEAR.

ii) Would the payback periods then be any different to your answer in i)? If

so, what would the payback periods be?

a) Yes, the payback period will be different as the cash flows will occur at the end

of the period rather than uniformly

b)

Assume Payments occur at the end of each year then

Payback period = Years before recovery + unrecovered cost at start year/cash

flow during the year

Project M:

Year Cumulative cash flow

0 (48,000)

1 15,000 15,000

2 24,000 39,000

3 36,000 75,000

Payback Period = 2 + (48,000-39,000)/36000= 2.25

Project N:

Year Cumulative cash flow

0 (48,000)

1 24,000 24,000

2 24,000 48,000

3 24,000 72,000

Payback Period = 2 + (48,000-48,000)/24000= 2

In this situation, Assume payments occur at the end of each year then

Preferred project- Project N

Reason

8

OCCUR AT THE END OF EACH YEAR.

ii) Would the payback periods then be any different to your answer in i)? If

so, what would the payback periods be?

a) Yes, the payback period will be different as the cash flows will occur at the end

of the period rather than uniformly

b)

Assume Payments occur at the end of each year then

Payback period = Years before recovery + unrecovered cost at start year/cash

flow during the year

Project M:

Year Cumulative cash flow

0 (48,000)

1 15,000 15,000

2 24,000 39,000

3 36,000 75,000

Payback Period = 2 + (48,000-39,000)/36000= 2.25

Project N:

Year Cumulative cash flow

0 (48,000)

1 24,000 24,000

2 24,000 48,000

3 24,000 72,000

Payback Period = 2 + (48,000-48,000)/24000= 2

In this situation, Assume payments occur at the end of each year then

Preferred project- Project N

Reason

8

Project N is preferred to project M because it has a shorter payback period

suggesting Andrew Hardcastle will be able to recoup his initial investment much

faster under project N than M.

QUESTION 3 continued.

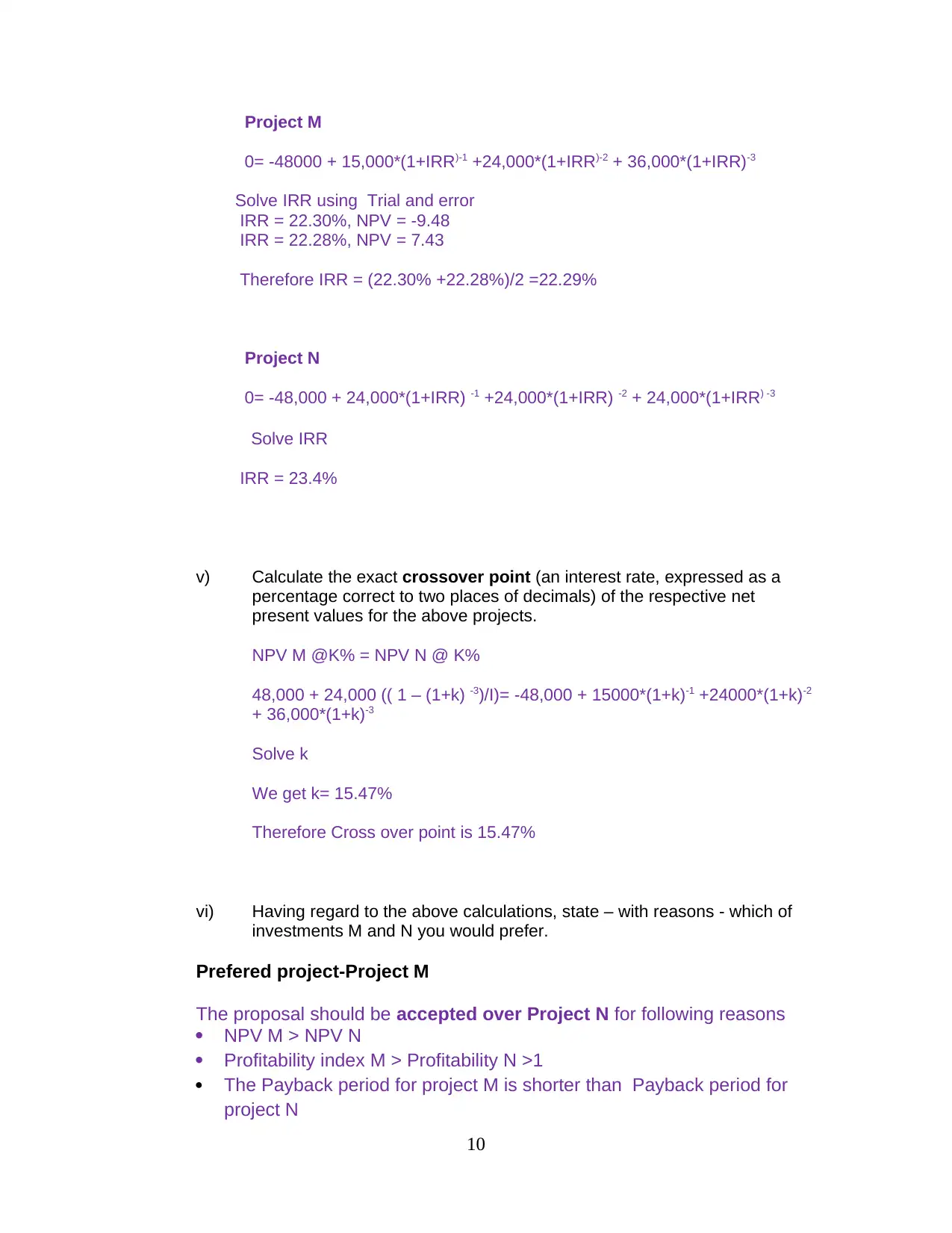

iii) If the required return is 10% per annum, what are:

- the net present values of each project?

Project M

NPV =-48,000 + 15,000*(1+I)-1 +24,000*(1+I)-2 + 36,000*(1+I)-3

=12,518.41

Project N

NPV =-48,000 + 24,000*(1+I)-1 +24,000*(1+I)-2 + 24,000*(1+I)-3

=11,684.45

- the present value (or profitability) indexes of each project?

Profitability Index =(Net Present Value + initial investment) / initial

investment

Project M

NPV=12,518.40

Profitability index = (12518.4 +48,000)/48000

=1.26

Project M

NPV =11,684.44

Profitability index = (11684.44+48,000)/48000

=1.24

iv) Calculate the internal rate of return (IRR) for each project.

[NOTE: It is satisfactory if the approximate IRR is calculated for

Investment X by trial and error, and stated as a percentage correct to the

nearer whole number. The IRR for Investment Y should be calculated as

a percentage exactly, correct to 1 decimal place.]

9

suggesting Andrew Hardcastle will be able to recoup his initial investment much

faster under project N than M.

QUESTION 3 continued.

iii) If the required return is 10% per annum, what are:

- the net present values of each project?

Project M

NPV =-48,000 + 15,000*(1+I)-1 +24,000*(1+I)-2 + 36,000*(1+I)-3

=12,518.41

Project N

NPV =-48,000 + 24,000*(1+I)-1 +24,000*(1+I)-2 + 24,000*(1+I)-3

=11,684.45

- the present value (or profitability) indexes of each project?

Profitability Index =(Net Present Value + initial investment) / initial

investment

Project M

NPV=12,518.40

Profitability index = (12518.4 +48,000)/48000

=1.26

Project M

NPV =11,684.44

Profitability index = (11684.44+48,000)/48000

=1.24

iv) Calculate the internal rate of return (IRR) for each project.

[NOTE: It is satisfactory if the approximate IRR is calculated for

Investment X by trial and error, and stated as a percentage correct to the

nearer whole number. The IRR for Investment Y should be calculated as

a percentage exactly, correct to 1 decimal place.]

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

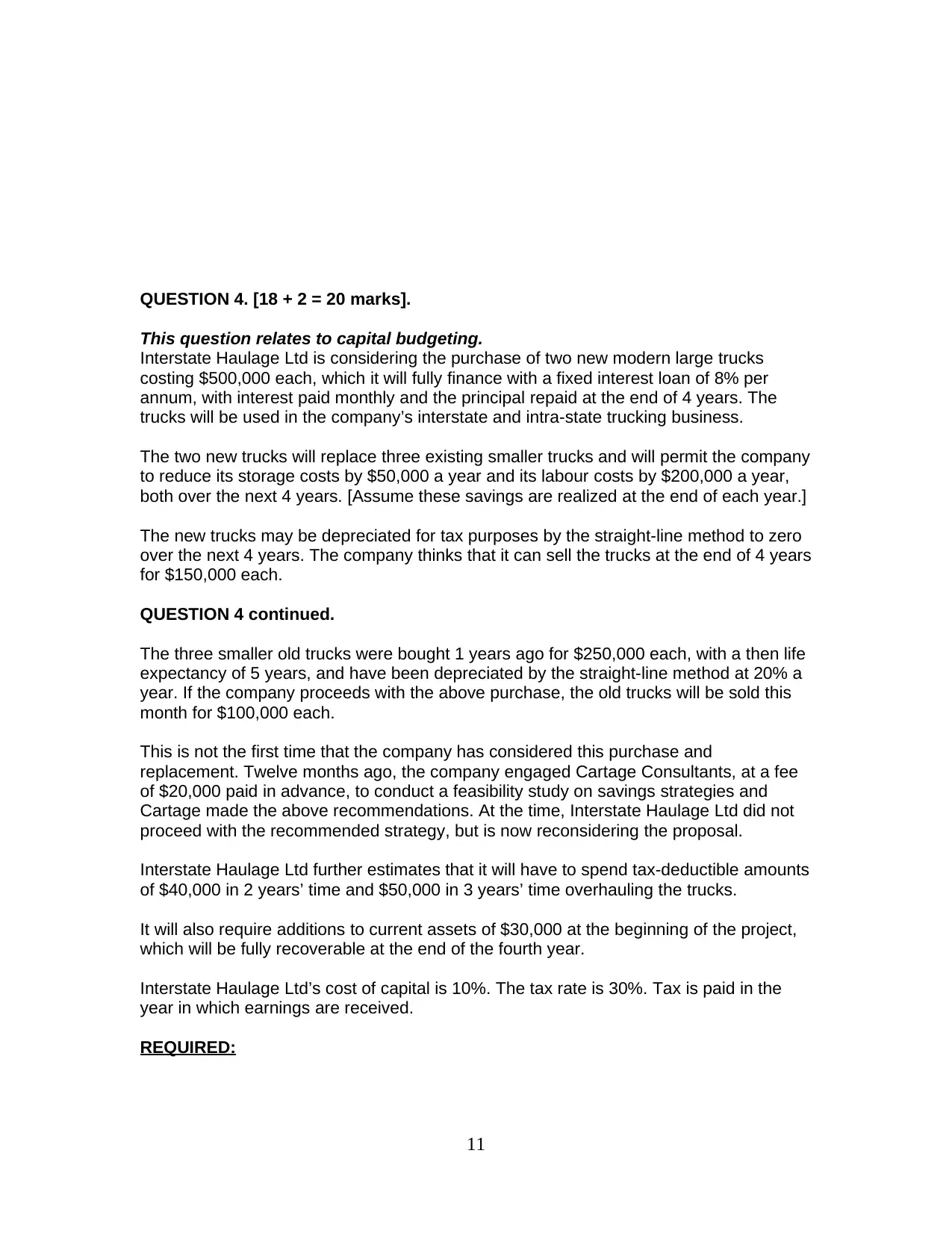

Project M

0= -48000 + 15,000*(1+IRR)-1 +24,000*(1+IRR)-2 + 36,000*(1+IRR)-3

Solve IRR using Trial and error

IRR = 22.30%, NPV = -9.48

IRR = 22.28%, NPV = 7.43

Therefore IRR = (22.30% +22.28%)/2 =22.29%

Project N

0= -48,000 + 24,000*(1+IRR) -1 +24,000*(1+IRR) -2 + 24,000*(1+IRR) -3

Solve IRR

IRR = 23.4%

v) Calculate the exact crossover point (an interest rate, expressed as a

percentage correct to two places of decimals) of the respective net

present values for the above projects.

NPV M @K% = NPV N @ K%

48,000 + 24,000 (( 1 – (1+k) -3)/I)= -48,000 + 15000*(1+k)-1 +24000*(1+k)-2

+ 36,000*(1+k)-3

Solve k

We get k= 15.47%

Therefore Cross over point is 15.47%

vi) Having regard to the above calculations, state – with reasons - which of

investments M and N you would prefer.

Prefered project-Project M

The proposal should be accepted over Project N for following reasons

NPV M > NPV N

Profitability index M > Profitability N >1

The Payback period for project M is shorter than Payback period for

project N

10

0= -48000 + 15,000*(1+IRR)-1 +24,000*(1+IRR)-2 + 36,000*(1+IRR)-3

Solve IRR using Trial and error

IRR = 22.30%, NPV = -9.48

IRR = 22.28%, NPV = 7.43

Therefore IRR = (22.30% +22.28%)/2 =22.29%

Project N

0= -48,000 + 24,000*(1+IRR) -1 +24,000*(1+IRR) -2 + 24,000*(1+IRR) -3

Solve IRR

IRR = 23.4%

v) Calculate the exact crossover point (an interest rate, expressed as a

percentage correct to two places of decimals) of the respective net

present values for the above projects.

NPV M @K% = NPV N @ K%

48,000 + 24,000 (( 1 – (1+k) -3)/I)= -48,000 + 15000*(1+k)-1 +24000*(1+k)-2

+ 36,000*(1+k)-3

Solve k

We get k= 15.47%

Therefore Cross over point is 15.47%

vi) Having regard to the above calculations, state – with reasons - which of

investments M and N you would prefer.

Prefered project-Project M

The proposal should be accepted over Project N for following reasons

NPV M > NPV N

Profitability index M > Profitability N >1

The Payback period for project M is shorter than Payback period for

project N

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4. [18 + 2 = 20 marks].

This question relates to capital budgeting.

Interstate Haulage Ltd is considering the purchase of two new modern large trucks

costing $500,000 each, which it will fully finance with a fixed interest loan of 8% per

annum, with interest paid monthly and the principal repaid at the end of 4 years. The

trucks will be used in the company’s interstate and intra-state trucking business.

The two new trucks will replace three existing smaller trucks and will permit the company

to reduce its storage costs by $50,000 a year and its labour costs by $200,000 a year,

both over the next 4 years. [Assume these savings are realized at the end of each year.]

The new trucks may be depreciated for tax purposes by the straight-line method to zero

over the next 4 years. The company thinks that it can sell the trucks at the end of 4 years

for $150,000 each.

QUESTION 4 continued.

The three smaller old trucks were bought 1 years ago for $250,000 each, with a then life

expectancy of 5 years, and have been depreciated by the straight-line method at 20% a

year. If the company proceeds with the above purchase, the old trucks will be sold this

month for $100,000 each.

This is not the first time that the company has considered this purchase and

replacement. Twelve months ago, the company engaged Cartage Consultants, at a fee

of $20,000 paid in advance, to conduct a feasibility study on savings strategies and

Cartage made the above recommendations. At the time, Interstate Haulage Ltd did not

proceed with the recommended strategy, but is now reconsidering the proposal.

Interstate Haulage Ltd further estimates that it will have to spend tax-deductible amounts

of $40,000 in 2 years’ time and $50,000 in 3 years’ time overhauling the trucks.

It will also require additions to current assets of $30,000 at the beginning of the project,

which will be fully recoverable at the end of the fourth year.

Interstate Haulage Ltd’s cost of capital is 10%. The tax rate is 30%. Tax is paid in the

year in which earnings are received.

REQUIRED:

11

This question relates to capital budgeting.

Interstate Haulage Ltd is considering the purchase of two new modern large trucks

costing $500,000 each, which it will fully finance with a fixed interest loan of 8% per

annum, with interest paid monthly and the principal repaid at the end of 4 years. The

trucks will be used in the company’s interstate and intra-state trucking business.

The two new trucks will replace three existing smaller trucks and will permit the company

to reduce its storage costs by $50,000 a year and its labour costs by $200,000 a year,

both over the next 4 years. [Assume these savings are realized at the end of each year.]

The new trucks may be depreciated for tax purposes by the straight-line method to zero

over the next 4 years. The company thinks that it can sell the trucks at the end of 4 years

for $150,000 each.

QUESTION 4 continued.

The three smaller old trucks were bought 1 years ago for $250,000 each, with a then life

expectancy of 5 years, and have been depreciated by the straight-line method at 20% a

year. If the company proceeds with the above purchase, the old trucks will be sold this

month for $100,000 each.

This is not the first time that the company has considered this purchase and

replacement. Twelve months ago, the company engaged Cartage Consultants, at a fee

of $20,000 paid in advance, to conduct a feasibility study on savings strategies and

Cartage made the above recommendations. At the time, Interstate Haulage Ltd did not

proceed with the recommended strategy, but is now reconsidering the proposal.

Interstate Haulage Ltd further estimates that it will have to spend tax-deductible amounts

of $40,000 in 2 years’ time and $50,000 in 3 years’ time overhauling the trucks.

It will also require additions to current assets of $30,000 at the beginning of the project,

which will be fully recoverable at the end of the fourth year.

Interstate Haulage Ltd’s cost of capital is 10%. The tax rate is 30%. Tax is paid in the

year in which earnings are received.

REQUIRED:

11

(a) Calculate the net present value (NPV), that is, the net benefit or net loss in

present value terms of the proposed purchase costs and the resultant

incremental cash flows.

[HINT: As shown in the text-book, it is recommended that for each year you

calculate the tax effect first, then identify the cash flows, then calculate the

overall net present value. Finally, make your recommendation.]

(See notes after table for formula and explanation of each cash flow)

Year 0 Year 1 Year 2 Year 3 Year 4

1.Cost Savings Storage 50,000 50,000 50,000 50,000

2.Cost Savings_Labour 200,000 200,000 200,000 200,000

3. Less overhaul Costs 0 40,000 50,000 0

4.Operating profit 250,000 210,000 200,000 250,000

5.Less Depreciation Exp 250,000 250,000 250,000 250,000

6.Less loss on sale of Old

Trucks

300,000 0 0 0

7.Net Income before tax (300,000) (40,000) (50,000) 0

8.Less Income Tax 90,000 12,000 15,000 0

9.Net Income after Tax (210,000) (28,000) (35,000) -

Add Depreciation 250,000 250,000 250,000 250,000

10.After Tax Cash Flow

operations

40,000 222,000 215,000 250,000

11.Initial Investment (1,000,000)

12.After Tax Terminal

Flow

210,000 210,000

13.Change in Assets (30,000) 30,000

14.After Tax Cash flows (1,000,000) 220,000 222,000 215,000 490,000

15. NPV (120,320)

Notes

1. Cost savings_Storage is 50,00 per annum

2. Cost savings_Labour is 200,00 per annum

3. Overhaul costs are $40,000 in 2 years’ time and $50,000 in 3 years’ time

4. Operating profit = cost savings (storage plus labour) - overhaul costs

5. Depreciation expense = (2* 500,000)/4 = 250,000 ( using straight-line method)

12

present value terms of the proposed purchase costs and the resultant

incremental cash flows.

[HINT: As shown in the text-book, it is recommended that for each year you

calculate the tax effect first, then identify the cash flows, then calculate the

overall net present value. Finally, make your recommendation.]

(See notes after table for formula and explanation of each cash flow)

Year 0 Year 1 Year 2 Year 3 Year 4

1.Cost Savings Storage 50,000 50,000 50,000 50,000

2.Cost Savings_Labour 200,000 200,000 200,000 200,000

3. Less overhaul Costs 0 40,000 50,000 0

4.Operating profit 250,000 210,000 200,000 250,000

5.Less Depreciation Exp 250,000 250,000 250,000 250,000

6.Less loss on sale of Old

Trucks

300,000 0 0 0

7.Net Income before tax (300,000) (40,000) (50,000) 0

8.Less Income Tax 90,000 12,000 15,000 0

9.Net Income after Tax (210,000) (28,000) (35,000) -

Add Depreciation 250,000 250,000 250,000 250,000

10.After Tax Cash Flow

operations

40,000 222,000 215,000 250,000

11.Initial Investment (1,000,000)

12.After Tax Terminal

Flow

210,000 210,000

13.Change in Assets (30,000) 30,000

14.After Tax Cash flows (1,000,000) 220,000 222,000 215,000 490,000

15. NPV (120,320)

Notes

1. Cost savings_Storage is 50,00 per annum

2. Cost savings_Labour is 200,00 per annum

3. Overhaul costs are $40,000 in 2 years’ time and $50,000 in 3 years’ time

4. Operating profit = cost savings (storage plus labour) - overhaul costs

5. Depreciation expense = (2* 500,000)/4 = 250,000 ( using straight-line method)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.