Time Value of Money and Its Applications in Finance

VerifiedAdded on 2021/05/31

|6

|1293

|23

Report

AI Summary

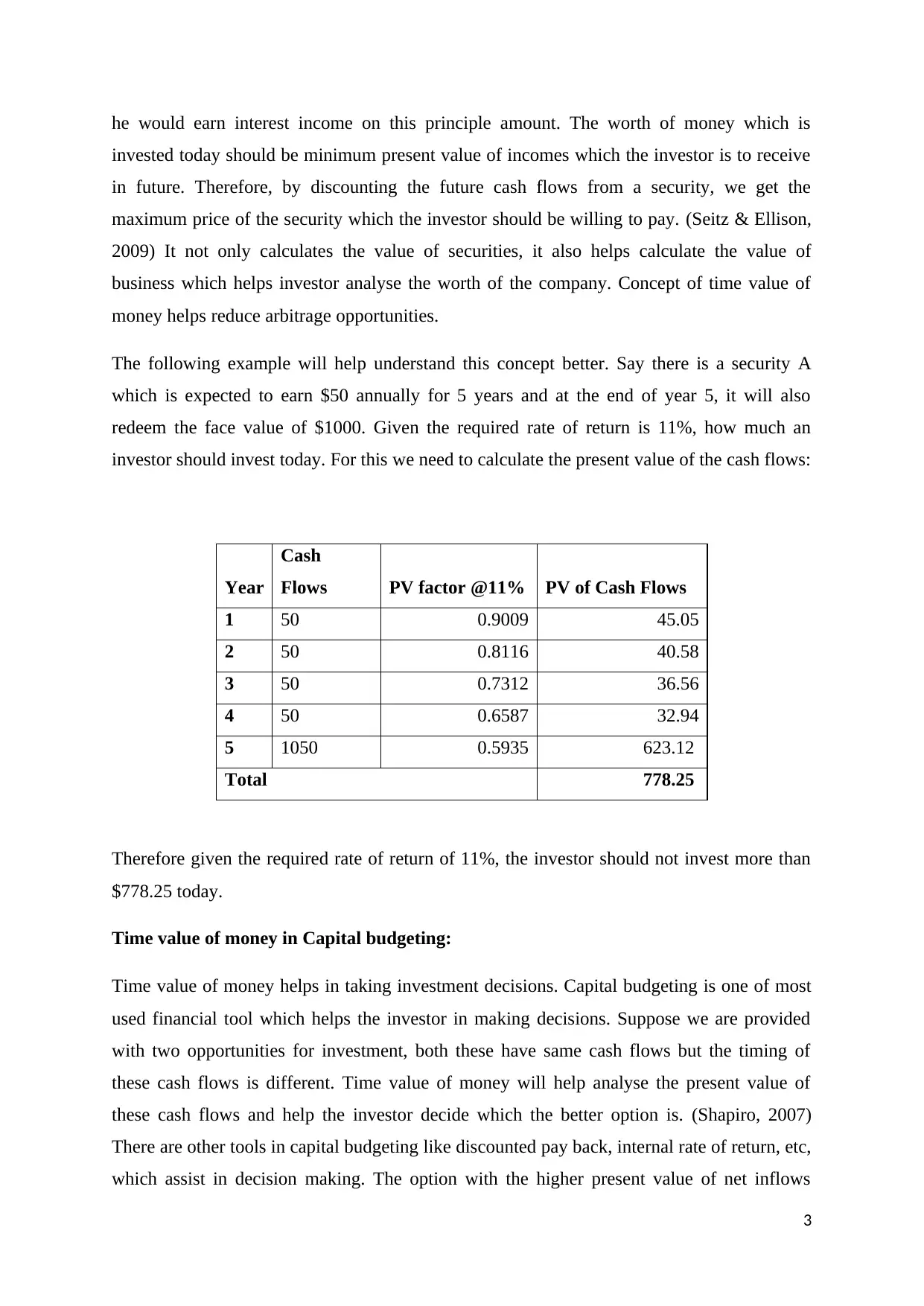

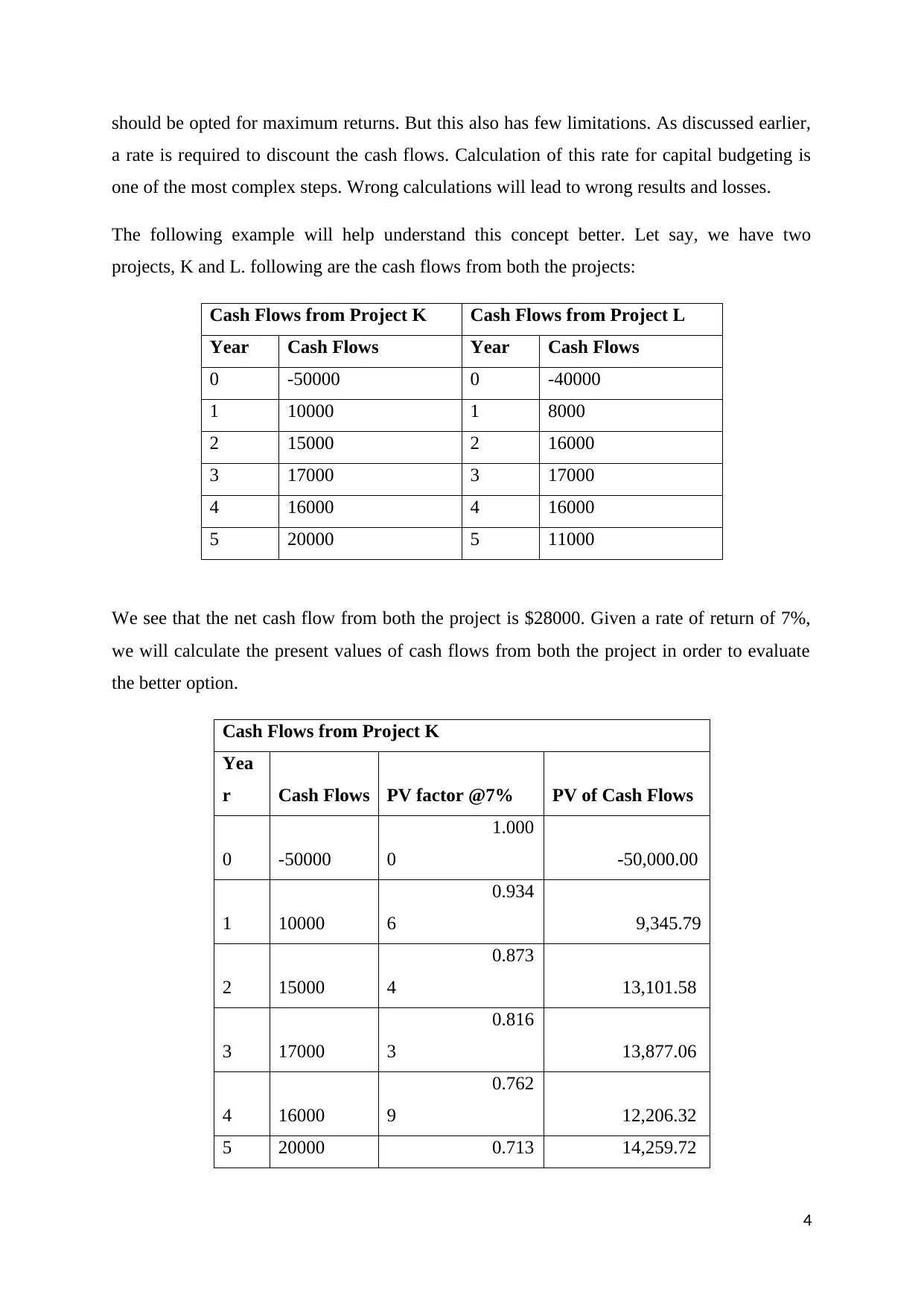

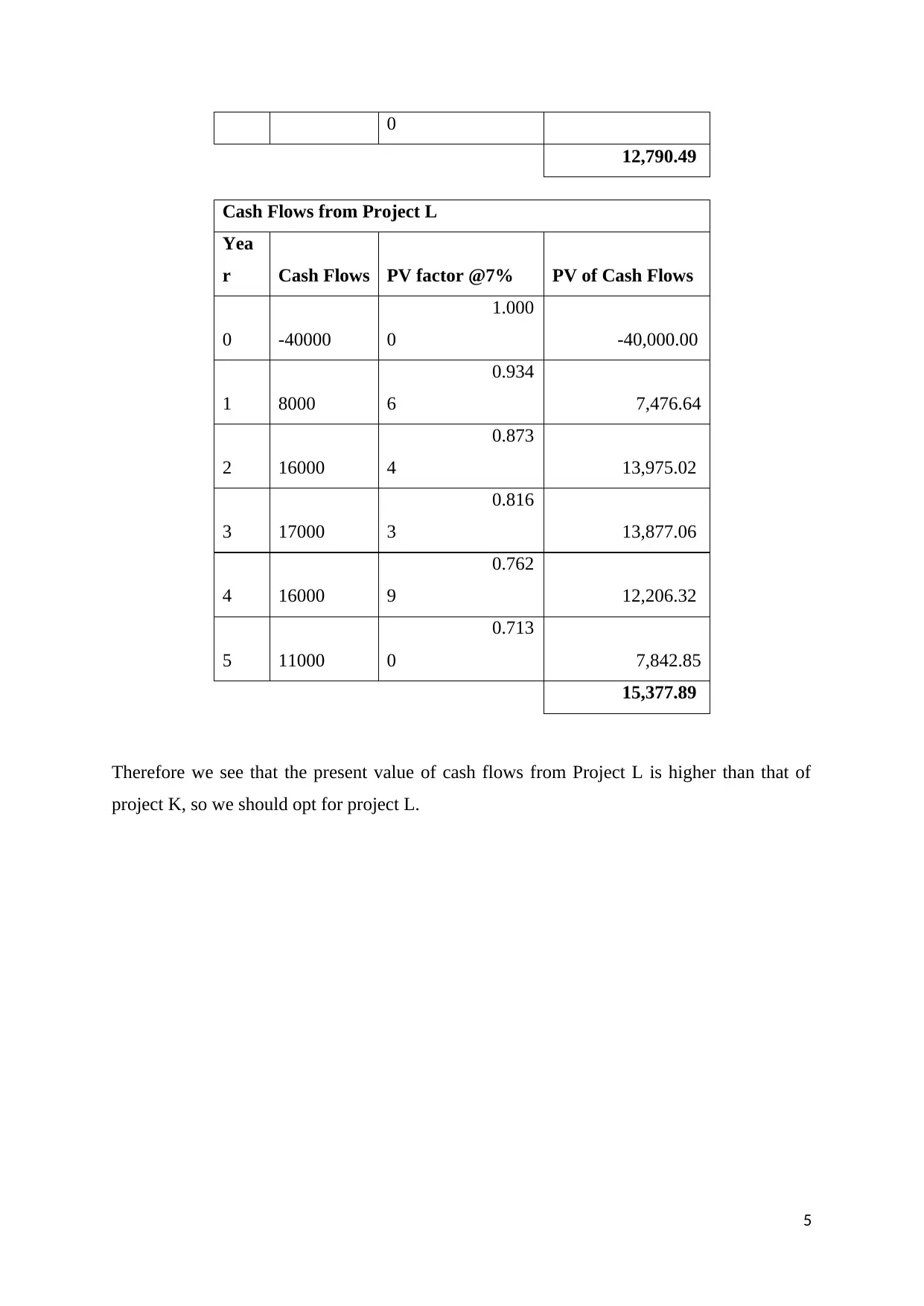

This report provides a comprehensive overview of the time value of money, a fundamental concept in finance. It explains the core principles, including the idea that money available at the present time is worth more than the same amount in the future due to its potential earning capacity. The report delves into the reasons behind this, such as risk, inflation, and opportunity cost, and explains how these factors influence financial decisions. It illustrates the concept with practical examples, including calculations of present value and its application in security valuation and capital budgeting. The report also discusses the limitations of the time value of money and its application in the valuation of securities and capital budgeting, highlighting the importance of the interest rate in these calculations. The report concludes by demonstrating how the time value of money is a crucial tool for making informed investment decisions and reducing arbitrage opportunities, providing examples for better understanding.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.