BAO 5534: Analyzing Time Value of Money in Business Finance Decisions

VerifiedAdded on 2023/06/11

|19

|4592

|237

Homework Assignment

AI Summary

This assignment solution delves into the concept of the time value of money (TVM) and its significance in financial management decision-making, particularly within the context of BAO 5534 Business Finance. It covers the core principles of TVM, differentiating between discounting and compounding processes, and emphasizing the importance of using appropriate discount rates for various investment decisions. The solution also addresses the application of TVM in valuing financial instruments such as bonds and shares, and its crucial role in capital budgeting decisions, including the calculation of net present value (NPV). Furthermore, it identifies potential issues and challenges in applying TVM in real-world financial scenarios. The assignment also touches upon investment strategies like diversification and buy-and-hold, illustrating their practical implications. The document includes calculations related to life insurance policies and mortgage repayments, providing a comprehensive overview of TVM's practical applications in finance. Desklib is a valuable resource, offering access to similar solved assignments and study tools for students.

TASK 1

Importance of Time value of money in financial management decision making

a) Concept of time value of money (TVM)

The concept of time value is an economics concept also widely used in the discipline of

Financial Management for the purpose of decision making. The theory behind the TVM

is used to find out the future value of the money in present time period. In other words,

TVM is about finding the worth of a sum of money in present date as its equivalent in

future dates considering the effects of interest, inflation and other factors on the money if

it is kept until that future date. The assumption behind this concept is that, due to the

potential earning capacity a sum of money is worth more in the present than in the future.

TVM is also called as the discounted value of the money or the Net Present Value

(NPV). As a matter of fact a rational investor would want to receive a sum of money in

the present date as compared to a future date because the sooner the money is received

the more value it gives. It gives quantitative value to an assumption or plan which makes

it easy to make decisions.The five variables that are used for the TVM are;

Present value(PV) or the amount in hand

Future value or the equivalent of the PV in future

Time period or number of periods money is to be held

Interest rate or the discounting rate

Payment or installments (Woodruff 2018)

The formula for calculating the TVM based in the above variables is;

FV = PV x [ 1 + (i / n) ] (n x t)

b) Discounting VS Compounding process

Discounting:

Discounting is the indirect assessment of the present value of a sum of money to be

received in future. It can also be used to assess the amount to be invested in present so as

to receive certain amount at a later date. The concept is futuristic and helps to make

Importance of Time value of money in financial management decision making

a) Concept of time value of money (TVM)

The concept of time value is an economics concept also widely used in the discipline of

Financial Management for the purpose of decision making. The theory behind the TVM

is used to find out the future value of the money in present time period. In other words,

TVM is about finding the worth of a sum of money in present date as its equivalent in

future dates considering the effects of interest, inflation and other factors on the money if

it is kept until that future date. The assumption behind this concept is that, due to the

potential earning capacity a sum of money is worth more in the present than in the future.

TVM is also called as the discounted value of the money or the Net Present Value

(NPV). As a matter of fact a rational investor would want to receive a sum of money in

the present date as compared to a future date because the sooner the money is received

the more value it gives. It gives quantitative value to an assumption or plan which makes

it easy to make decisions.The five variables that are used for the TVM are;

Present value(PV) or the amount in hand

Future value or the equivalent of the PV in future

Time period or number of periods money is to be held

Interest rate or the discounting rate

Payment or installments (Woodruff 2018)

The formula for calculating the TVM based in the above variables is;

FV = PV x [ 1 + (i / n) ] (n x t)

b) Discounting VS Compounding process

Discounting:

Discounting is the indirect assessment of the present value of a sum of money to be

received in future. It can also be used to assess the amount to be invested in present so as

to receive certain amount at a later date. The concept is futuristic and helps to make

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions for future by determining the value of sum receivable or current value of sum to

be invested (Keythman 2015)

A denomination of money is worth more as of today than at a specified future

date or even tomorrow. Discounting helps in ascertaining the worth of future cash flows

in the present date and gives a clear idea whether or not the target is going to be achieved.

Another use of the process of discounting is that it helps in the valuation of financial

assets. For example, the current value of a bond is the present value and the value of the

same bond in some future date is the future value. The net present value is determined by

finding out the difference between the two values using a discounting rate.

Compounding:

Process of compounding presents a stark contrast to the process of discounting. This is a

direct concept of the time value of money. It helps in determining the future value of the

current investment i.e. to say the potential amount that will be received in a future date if

we invest today. Also it can be used for the purpose of calculating the payments to be

made at a future date for an existing loan or a loan to be taken.

Unlike discounting here we know the present value of money and the future value

is to be ascertained. Compounding occurs when the earnings to an asset in the form of

interest or capital gains are invested again. The result will be additional earnings in the

form of compound interest on the reinvested amount and the original amount.

Discounting over compounding:

Discounting is the most favored process in the concept of TVM for the purpose of

financial decision making because it gives an overview on the current value of money

considering all the factors that can come to play in future. It is a comprehensive method

of calculating the worth of an asset which considers the inflation, interest rates,

depreciation for depreciable assets and taxes. It provides better insights into the present

so as to make informed decisions for the future (Sanders 2017)It is wise to use

discounting in place of compounding since decisions are made as per the targets to be

achieved and the target in the form of future value is known in the discounting process

and the current course of action can be decided in the form of a present value (Surbhi

2015)

be invested (Keythman 2015)

A denomination of money is worth more as of today than at a specified future

date or even tomorrow. Discounting helps in ascertaining the worth of future cash flows

in the present date and gives a clear idea whether or not the target is going to be achieved.

Another use of the process of discounting is that it helps in the valuation of financial

assets. For example, the current value of a bond is the present value and the value of the

same bond in some future date is the future value. The net present value is determined by

finding out the difference between the two values using a discounting rate.

Compounding:

Process of compounding presents a stark contrast to the process of discounting. This is a

direct concept of the time value of money. It helps in determining the future value of the

current investment i.e. to say the potential amount that will be received in a future date if

we invest today. Also it can be used for the purpose of calculating the payments to be

made at a future date for an existing loan or a loan to be taken.

Unlike discounting here we know the present value of money and the future value

is to be ascertained. Compounding occurs when the earnings to an asset in the form of

interest or capital gains are invested again. The result will be additional earnings in the

form of compound interest on the reinvested amount and the original amount.

Discounting over compounding:

Discounting is the most favored process in the concept of TVM for the purpose of

financial decision making because it gives an overview on the current value of money

considering all the factors that can come to play in future. It is a comprehensive method

of calculating the worth of an asset which considers the inflation, interest rates,

depreciation for depreciable assets and taxes. It provides better insights into the present

so as to make informed decisions for the future (Sanders 2017)It is wise to use

discounting in place of compounding since decisions are made as per the targets to be

achieved and the target in the form of future value is known in the discounting process

and the current course of action can be decided in the form of a present value (Surbhi

2015)

c) Discount rate and its components

The discount rate is the rate of return used to calculate the present value of the future cash

flows in the discounted cash flow analysis. The rate of discounting considers two

elements for calculation of an appropriate discount rate; one is the risk free rate and the

other being the risk premium. Risk free rate means the receipt that has no chance of

default like the rate of return in the government securities. So to construct a suitable rate

for discounting, risk free rate is often extracted from the rate of return of the government

securities (Dalfard 2016) The risk premium, however, is the risk that the business is

exposed to during its operation. The risk factor could differ as per the instrument of

investment as it is mentioned earlier that each investment has a unique risk element

attached to it. While calculating the premium inflation is often considered as a part of

risk. The risk premium is calculated upon consideration of the following factors

Size of the company

Industry specific risk element

Inflation attribute

Company specific risk element.

The formula for calculating the discount rate is:

d) Use of different rates for different investment decisions:

It is important to use different rates for different investments because every investment is

exposed to unique risk factor(s) and they will have different returns. For a specific

investment the risk and return associated with that particular investment must be

considered to make the correct decisions otherwise if an incorrect rate is used the

decisions will automatically be incorrect. For example, an equity investment must

consider the risk premium of the company and industry from which the equity is to be

bought and the rate meant for any other company cannot be used to make an informed

decision. One decision affects the series of operations and other decisions as well, so for

everything to fall in a line it is important to use the relevant discount rate.

The discount rate is the rate of return used to calculate the present value of the future cash

flows in the discounted cash flow analysis. The rate of discounting considers two

elements for calculation of an appropriate discount rate; one is the risk free rate and the

other being the risk premium. Risk free rate means the receipt that has no chance of

default like the rate of return in the government securities. So to construct a suitable rate

for discounting, risk free rate is often extracted from the rate of return of the government

securities (Dalfard 2016) The risk premium, however, is the risk that the business is

exposed to during its operation. The risk factor could differ as per the instrument of

investment as it is mentioned earlier that each investment has a unique risk element

attached to it. While calculating the premium inflation is often considered as a part of

risk. The risk premium is calculated upon consideration of the following factors

Size of the company

Industry specific risk element

Inflation attribute

Company specific risk element.

The formula for calculating the discount rate is:

d) Use of different rates for different investment decisions:

It is important to use different rates for different investments because every investment is

exposed to unique risk factor(s) and they will have different returns. For a specific

investment the risk and return associated with that particular investment must be

considered to make the correct decisions otherwise if an incorrect rate is used the

decisions will automatically be incorrect. For example, an equity investment must

consider the risk premium of the company and industry from which the equity is to be

bought and the rate meant for any other company cannot be used to make an informed

decision. One decision affects the series of operations and other decisions as well, so for

everything to fall in a line it is important to use the relevant discount rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

e) TVM in valuation of financial instruments

Financial instruments such as bonds, equity and preference shares are the most common

forms of investment. To find the worth of each financial instrument and deciding the

most beneficial course of action before investing into any of them the concept of TVM is

very helpful. This is in reference to a household investor (Larson 2015)

The valuation of an instrument is a very crucial decision for any company. TVM

can help find the valuation or pricing to be fixed for the instrument in question. The

pricing is decided based on the factors like taxes, interest, scrap value, repairs and other

cash flows. Financial instruments are carried at fair value and the fair value is nothing

else but the time value of the investment on the financial instrument. The yield of an

instrument is calculated based on the market scenario and assumptions for the future and

that yield is then used to calculate the present value.

f) Capital budgeting decisions and TVM

TVM can help in finding out whether an investment will yield positive or negative result.

The concept is technical but worth the complication and it can be done in the spreadsheet.

The business unit wishes to forecast the viability of an investment in a project, expansion

or buying an asset. An investment made now will fetch returns after a few years. Time

value concept will accurately tell the worth of the investment in terms of the present

value for helping the business unit decide on whether or not to invest in the project. For

making capital budgeting decisions the company calculates the cash flows in the form of

inflows and the outflows. Then the net cash flow is discounted to estimate the current

worth of a future project in the form of the net present value thus found. It can be

represented in a formula as under (Merittt 2015)

NPV = C x {(1 - (1 + R)-T) / R} − Initial Investment (Freedman 2018)

g) Other issues in TVM

The following are the issues when it comes to the use of TVM in financial management

decision making:

The method of finding the present value involves technicality and expertise. It is

in itself a process to be learned to be applied.

Financial instruments such as bonds, equity and preference shares are the most common

forms of investment. To find the worth of each financial instrument and deciding the

most beneficial course of action before investing into any of them the concept of TVM is

very helpful. This is in reference to a household investor (Larson 2015)

The valuation of an instrument is a very crucial decision for any company. TVM

can help find the valuation or pricing to be fixed for the instrument in question. The

pricing is decided based on the factors like taxes, interest, scrap value, repairs and other

cash flows. Financial instruments are carried at fair value and the fair value is nothing

else but the time value of the investment on the financial instrument. The yield of an

instrument is calculated based on the market scenario and assumptions for the future and

that yield is then used to calculate the present value.

f) Capital budgeting decisions and TVM

TVM can help in finding out whether an investment will yield positive or negative result.

The concept is technical but worth the complication and it can be done in the spreadsheet.

The business unit wishes to forecast the viability of an investment in a project, expansion

or buying an asset. An investment made now will fetch returns after a few years. Time

value concept will accurately tell the worth of the investment in terms of the present

value for helping the business unit decide on whether or not to invest in the project. For

making capital budgeting decisions the company calculates the cash flows in the form of

inflows and the outflows. Then the net cash flow is discounted to estimate the current

worth of a future project in the form of the net present value thus found. It can be

represented in a formula as under (Merittt 2015)

NPV = C x {(1 - (1 + R)-T) / R} − Initial Investment (Freedman 2018)

g) Other issues in TVM

The following are the issues when it comes to the use of TVM in financial management

decision making:

The method of finding the present value involves technicality and expertise. It is

in itself a process to be learned to be applied.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Identifying the correct future cash flows of a project and the timing factor

involved to earn the return is complicated (Dalfard 2016)

There are always a minimum of four variables to be ascertained and the variables

keep changing as per the current and the future market scenario.

The normal human mind works as per the growth model but the TVM is based on

the regressive model of discounting which is just the opposite of human

psychology.

TASK 2

1. Answer:-

Studebaker seems to be looking on following financial goals:-

1. Diversification

2. Buy and hold

Diversification is a technique of investment in such a way your investment do not directly

associate with market ups and down, that simply means to not to put all eggs in one basket, so

that if you invest in only one company or one kind of investment and if such company falls then

in such case value of entire investment will also fall down, diversification allows to keep

portfolio in a less risky position. Diversification is a evolution strategy that exploits on market

chances by dealing outlay risk over dissimilar asset modules. Diversification tells for spreading

the selection among unlike assets which also includes stocks, bonds, real land, international

hoards, and cash equals. Through modification the investment will be able to comprimise on

the losses on the profits.

Buy and hold policy is opted to get good returns in long run instead of involving in day to day

speculation, in buy and hold policy one need to properly check about ways to investment before

investing and less attention is required in buy and hold policy.

involved to earn the return is complicated (Dalfard 2016)

There are always a minimum of four variables to be ascertained and the variables

keep changing as per the current and the future market scenario.

The normal human mind works as per the growth model but the TVM is based on

the regressive model of discounting which is just the opposite of human

psychology.

TASK 2

1. Answer:-

Studebaker seems to be looking on following financial goals:-

1. Diversification

2. Buy and hold

Diversification is a technique of investment in such a way your investment do not directly

associate with market ups and down, that simply means to not to put all eggs in one basket, so

that if you invest in only one company or one kind of investment and if such company falls then

in such case value of entire investment will also fall down, diversification allows to keep

portfolio in a less risky position. Diversification is a evolution strategy that exploits on market

chances by dealing outlay risk over dissimilar asset modules. Diversification tells for spreading

the selection among unlike assets which also includes stocks, bonds, real land, international

hoards, and cash equals. Through modification the investment will be able to comprimise on

the losses on the profits.

Buy and hold policy is opted to get good returns in long run instead of involving in day to day

speculation, in buy and hold policy one need to properly check about ways to investment before

investing and less attention is required in buy and hold policy.

In our opinion policy opted by Studebaker are beneficial for him and both are correct goal.It will

help in future

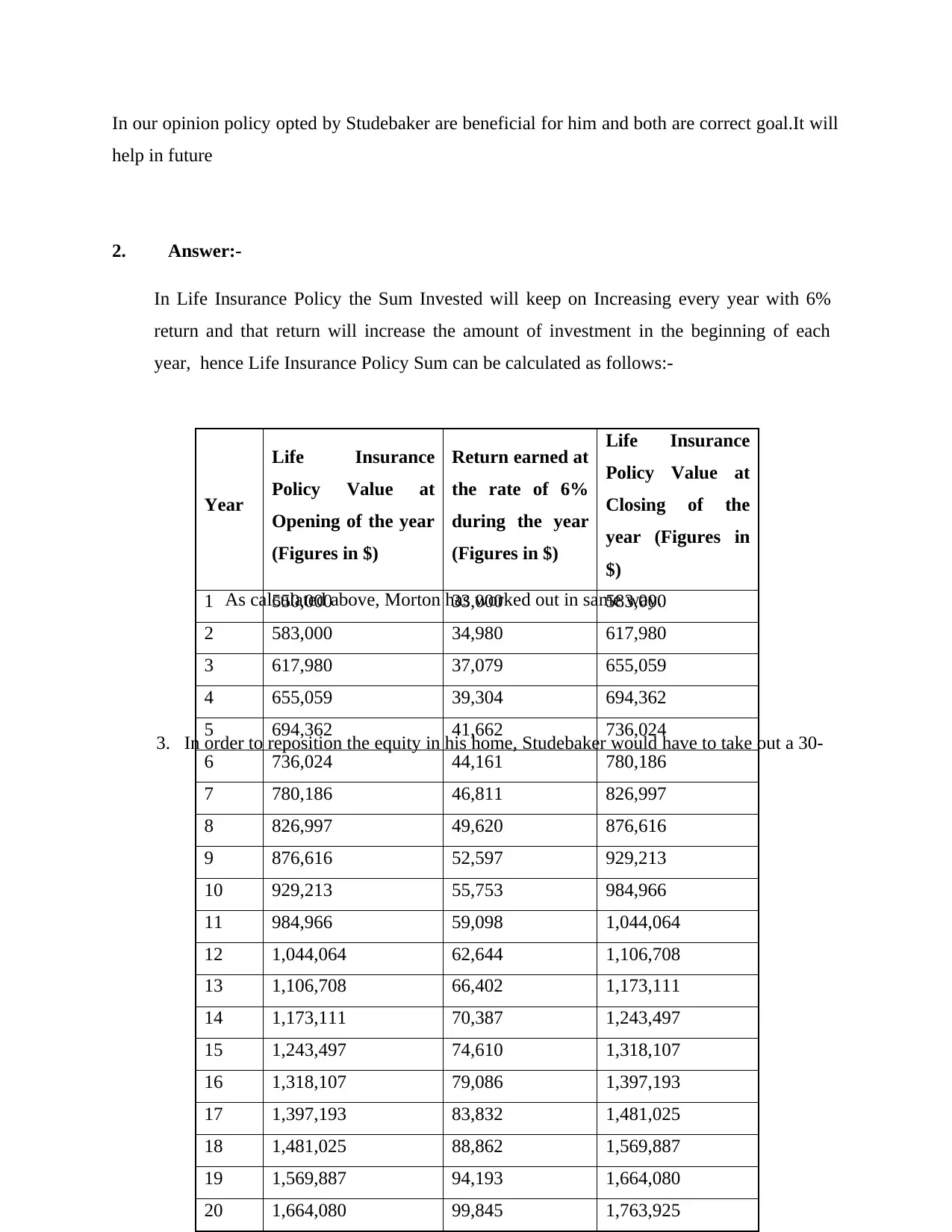

2. Answer:-

In Life Insurance Policy the Sum Invested will keep on Increasing every year with 6%

return and that return will increase the amount of investment in the beginning of each

year, hence Life Insurance Policy Sum can be calculated as follows:-

As calculated above, Morton has worked out in same way.

3. In order to reposition the equity in his home, Studebaker would have to take out a 30-

Year

Life Insurance

Policy Value at

Opening of the year

(Figures in $)

Return earned at

the rate of 6%

during the year

(Figures in $)

Life Insurance

Policy Value at

Closing of the

year (Figures in

$)

1 550,000 33,000 583,000

2 583,000 34,980 617,980

3 617,980 37,079 655,059

4 655,059 39,304 694,362

5 694,362 41,662 736,024

6 736,024 44,161 780,186

7 780,186 46,811 826,997

8 826,997 49,620 876,616

9 876,616 52,597 929,213

10 929,213 55,753 984,966

11 984,966 59,098 1,044,064

12 1,044,064 62,644 1,106,708

13 1,106,708 66,402 1,173,111

14 1,173,111 70,387 1,243,497

15 1,243,497 74,610 1,318,107

16 1,318,107 79,086 1,397,193

17 1,397,193 83,832 1,481,025

18 1,481,025 88,862 1,569,887

19 1,569,887 94,193 1,664,080

20 1,664,080 99,845 1,763,925

help in future

2. Answer:-

In Life Insurance Policy the Sum Invested will keep on Increasing every year with 6%

return and that return will increase the amount of investment in the beginning of each

year, hence Life Insurance Policy Sum can be calculated as follows:-

As calculated above, Morton has worked out in same way.

3. In order to reposition the equity in his home, Studebaker would have to take out a 30-

Year

Life Insurance

Policy Value at

Opening of the year

(Figures in $)

Return earned at

the rate of 6%

during the year

(Figures in $)

Life Insurance

Policy Value at

Closing of the

year (Figures in

$)

1 550,000 33,000 583,000

2 583,000 34,980 617,980

3 617,980 37,079 655,059

4 655,059 39,304 694,362

5 694,362 41,662 736,024

6 736,024 44,161 780,186

7 780,186 46,811 826,997

8 826,997 49,620 876,616

9 876,616 52,597 929,213

10 929,213 55,753 984,966

11 984,966 59,098 1,044,064

12 1,044,064 62,644 1,106,708

13 1,106,708 66,402 1,173,111

14 1,173,111 70,387 1,243,497

15 1,243,497 74,610 1,318,107

16 1,318,107 79,086 1,397,193

17 1,397,193 83,832 1,481,025

18 1,481,025 88,862 1,569,887

19 1,569,887 94,193 1,664,080

20 1,664,080 99,845 1,763,925

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

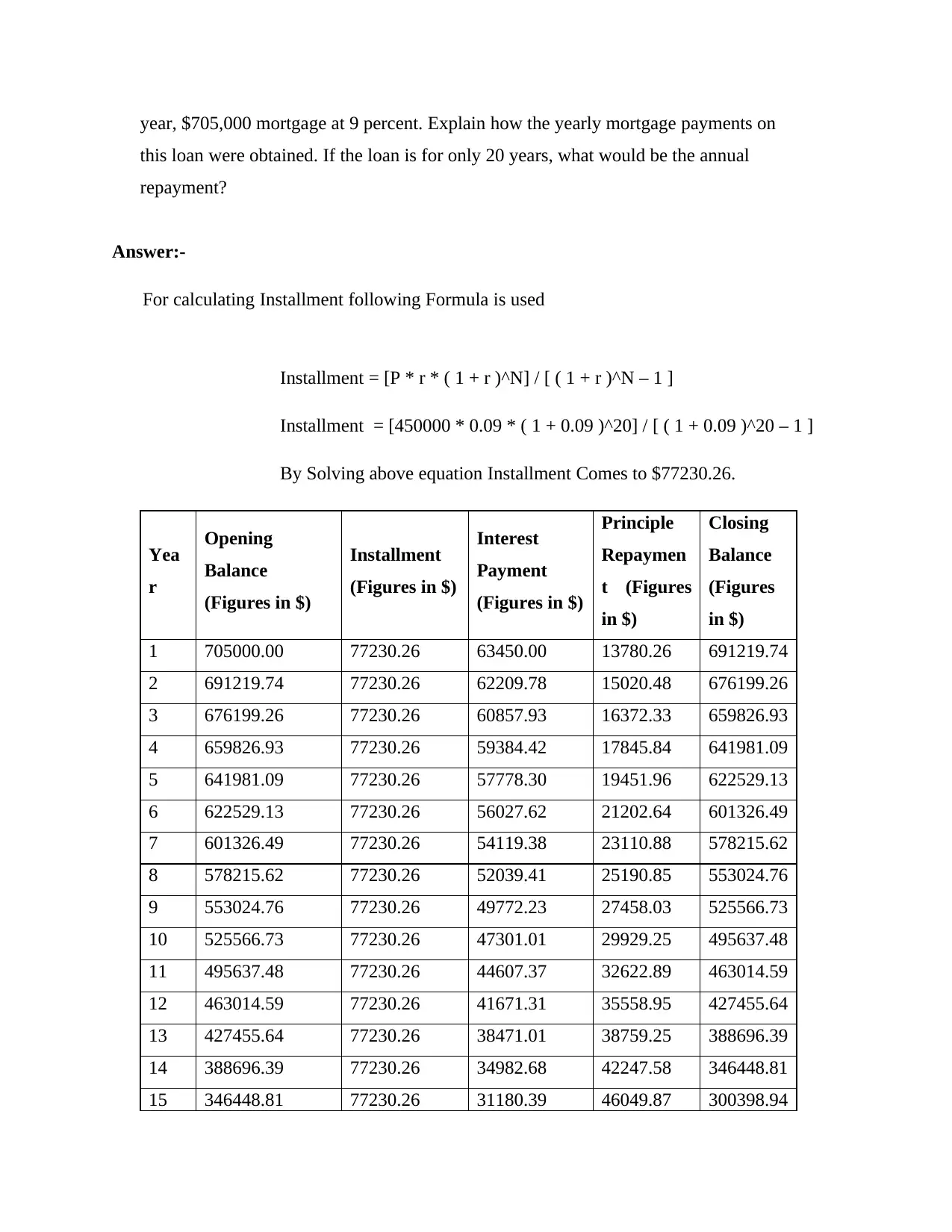

year, $705,000 mortgage at 9 percent. Explain how the yearly mortgage payments on

this loan were obtained. If the loan is for only 20 years, what would be the annual

repayment?

Answer:-

For calculating Installment following Formula is used

Installment = [P * r * ( 1 + r )^N] / [ ( 1 + r )^N – 1 ]

Installment = [450000 * 0.09 * ( 1 + 0.09 )^20] / [ ( 1 + 0.09 )^20 – 1 ]

By Solving above equation Installment Comes to $77230.26.

Yea

r

Opening

Balance

(Figures in $)

Installment

(Figures in $)

Interest

Payment

(Figures in $)

Principle

Repaymen

t (Figures

in $)

Closing

Balance

(Figures

in $)

1 705000.00 77230.26 63450.00 13780.26 691219.74

2 691219.74 77230.26 62209.78 15020.48 676199.26

3 676199.26 77230.26 60857.93 16372.33 659826.93

4 659826.93 77230.26 59384.42 17845.84 641981.09

5 641981.09 77230.26 57778.30 19451.96 622529.13

6 622529.13 77230.26 56027.62 21202.64 601326.49

7 601326.49 77230.26 54119.38 23110.88 578215.62

8 578215.62 77230.26 52039.41 25190.85 553024.76

9 553024.76 77230.26 49772.23 27458.03 525566.73

10 525566.73 77230.26 47301.01 29929.25 495637.48

11 495637.48 77230.26 44607.37 32622.89 463014.59

12 463014.59 77230.26 41671.31 35558.95 427455.64

13 427455.64 77230.26 38471.01 38759.25 388696.39

14 388696.39 77230.26 34982.68 42247.58 346448.81

15 346448.81 77230.26 31180.39 46049.87 300398.94

this loan were obtained. If the loan is for only 20 years, what would be the annual

repayment?

Answer:-

For calculating Installment following Formula is used

Installment = [P * r * ( 1 + r )^N] / [ ( 1 + r )^N – 1 ]

Installment = [450000 * 0.09 * ( 1 + 0.09 )^20] / [ ( 1 + 0.09 )^20 – 1 ]

By Solving above equation Installment Comes to $77230.26.

Yea

r

Opening

Balance

(Figures in $)

Installment

(Figures in $)

Interest

Payment

(Figures in $)

Principle

Repaymen

t (Figures

in $)

Closing

Balance

(Figures

in $)

1 705000.00 77230.26 63450.00 13780.26 691219.74

2 691219.74 77230.26 62209.78 15020.48 676199.26

3 676199.26 77230.26 60857.93 16372.33 659826.93

4 659826.93 77230.26 59384.42 17845.84 641981.09

5 641981.09 77230.26 57778.30 19451.96 622529.13

6 622529.13 77230.26 56027.62 21202.64 601326.49

7 601326.49 77230.26 54119.38 23110.88 578215.62

8 578215.62 77230.26 52039.41 25190.85 553024.76

9 553024.76 77230.26 49772.23 27458.03 525566.73

10 525566.73 77230.26 47301.01 29929.25 495637.48

11 495637.48 77230.26 44607.37 32622.89 463014.59

12 463014.59 77230.26 41671.31 35558.95 427455.64

13 427455.64 77230.26 38471.01 38759.25 388696.39

14 388696.39 77230.26 34982.68 42247.58 346448.81

15 346448.81 77230.26 31180.39 46049.87 300398.94

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

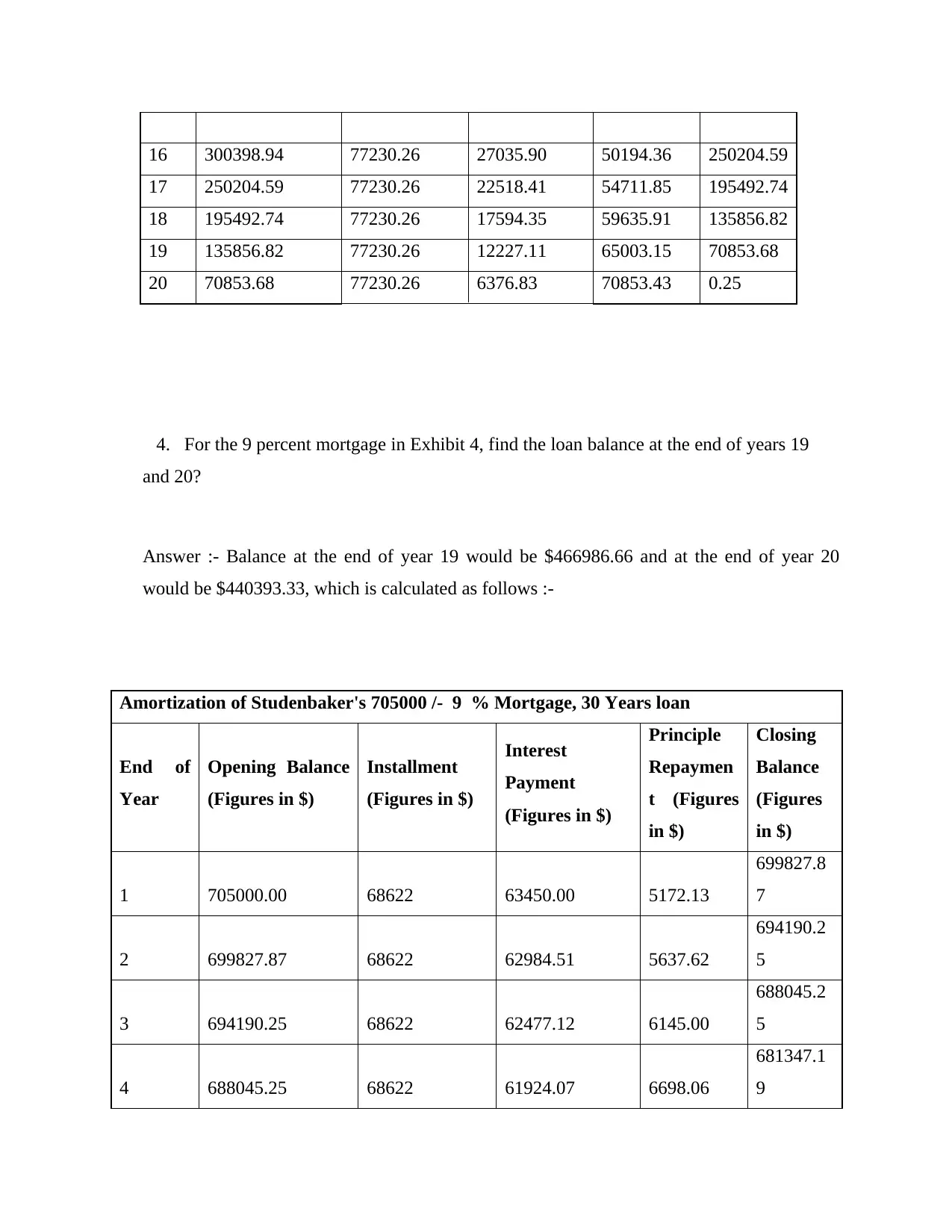

16 300398.94 77230.26 27035.90 50194.36 250204.59

17 250204.59 77230.26 22518.41 54711.85 195492.74

18 195492.74 77230.26 17594.35 59635.91 135856.82

19 135856.82 77230.26 12227.11 65003.15 70853.68

20 70853.68 77230.26 6376.83 70853.43 0.25

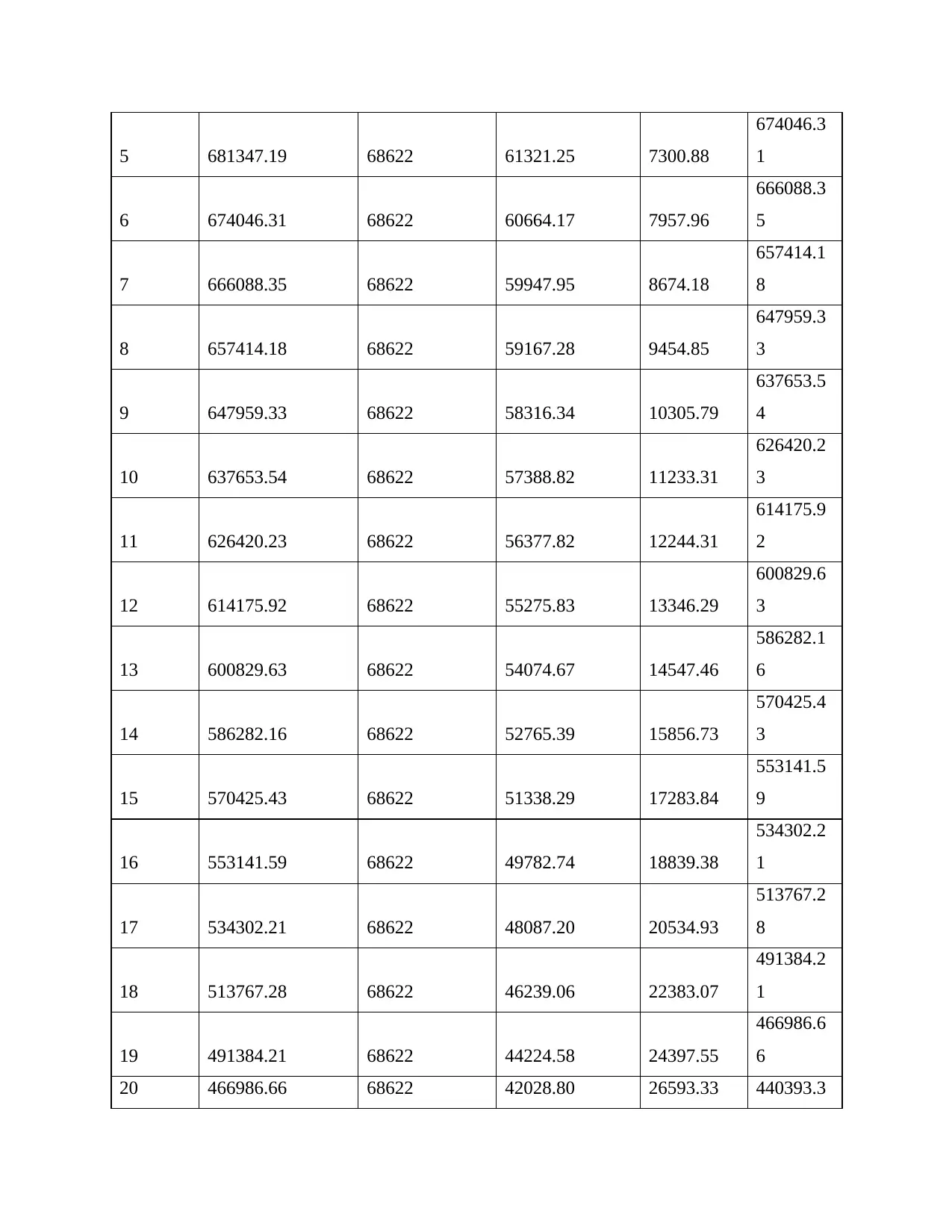

4. For the 9 percent mortgage in Exhibit 4, find the loan balance at the end of years 19

and 20?

Answer :- Balance at the end of year 19 would be $466986.66 and at the end of year 20

would be $440393.33, which is calculated as follows :-

Amortization of Studenbaker's 705000 /- 9 % Mortgage, 30 Years loan

End of

Year

Opening Balance

(Figures in $)

Installment

(Figures in $)

Interest

Payment

(Figures in $)

Principle

Repaymen

t (Figures

in $)

Closing

Balance

(Figures

in $)

1 705000.00 68622 63450.00 5172.13

699827.8

7

2 699827.87 68622 62984.51 5637.62

694190.2

5

3 694190.25 68622 62477.12 6145.00

688045.2

5

4 688045.25 68622 61924.07 6698.06

681347.1

9

17 250204.59 77230.26 22518.41 54711.85 195492.74

18 195492.74 77230.26 17594.35 59635.91 135856.82

19 135856.82 77230.26 12227.11 65003.15 70853.68

20 70853.68 77230.26 6376.83 70853.43 0.25

4. For the 9 percent mortgage in Exhibit 4, find the loan balance at the end of years 19

and 20?

Answer :- Balance at the end of year 19 would be $466986.66 and at the end of year 20

would be $440393.33, which is calculated as follows :-

Amortization of Studenbaker's 705000 /- 9 % Mortgage, 30 Years loan

End of

Year

Opening Balance

(Figures in $)

Installment

(Figures in $)

Interest

Payment

(Figures in $)

Principle

Repaymen

t (Figures

in $)

Closing

Balance

(Figures

in $)

1 705000.00 68622 63450.00 5172.13

699827.8

7

2 699827.87 68622 62984.51 5637.62

694190.2

5

3 694190.25 68622 62477.12 6145.00

688045.2

5

4 688045.25 68622 61924.07 6698.06

681347.1

9

5 681347.19 68622 61321.25 7300.88

674046.3

1

6 674046.31 68622 60664.17 7957.96

666088.3

5

7 666088.35 68622 59947.95 8674.18

657414.1

8

8 657414.18 68622 59167.28 9454.85

647959.3

3

9 647959.33 68622 58316.34 10305.79

637653.5

4

10 637653.54 68622 57388.82 11233.31

626420.2

3

11 626420.23 68622 56377.82 12244.31

614175.9

2

12 614175.92 68622 55275.83 13346.29

600829.6

3

13 600829.63 68622 54074.67 14547.46

586282.1

6

14 586282.16 68622 52765.39 15856.73

570425.4

3

15 570425.43 68622 51338.29 17283.84

553141.5

9

16 553141.59 68622 49782.74 18839.38

534302.2

1

17 534302.21 68622 48087.20 20534.93

513767.2

8

18 513767.28 68622 46239.06 22383.07

491384.2

1

19 491384.21 68622 44224.58 24397.55

466986.6

6

20 466986.66 68622 42028.80 26593.33 440393.3

674046.3

1

6 674046.31 68622 60664.17 7957.96

666088.3

5

7 666088.35 68622 59947.95 8674.18

657414.1

8

8 657414.18 68622 59167.28 9454.85

647959.3

3

9 647959.33 68622 58316.34 10305.79

637653.5

4

10 637653.54 68622 57388.82 11233.31

626420.2

3

11 626420.23 68622 56377.82 12244.31

614175.9

2

12 614175.92 68622 55275.83 13346.29

600829.6

3

13 600829.63 68622 54074.67 14547.46

586282.1

6

14 586282.16 68622 52765.39 15856.73

570425.4

3

15 570425.43 68622 51338.29 17283.84

553141.5

9

16 553141.59 68622 49782.74 18839.38

534302.2

1

17 534302.21 68622 48087.20 20534.93

513767.2

8

18 513767.28 68622 46239.06 22383.07

491384.2

1

19 491384.21 68622 44224.58 24397.55

466986.6

6

20 466986.66 68622 42028.80 26593.33 440393.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

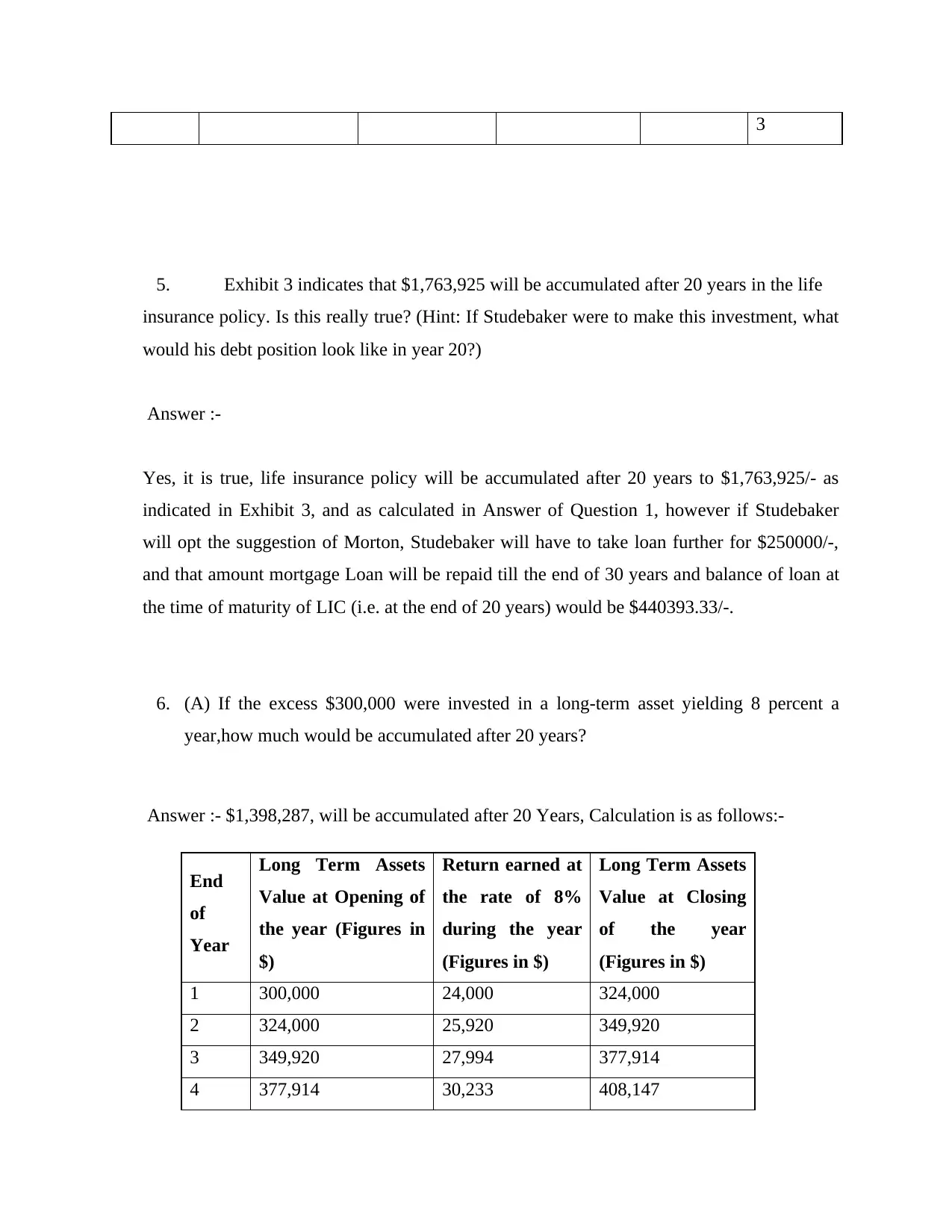

5. Exhibit 3 indicates that $1,763,925 will be accumulated after 20 years in the life

insurance policy. Is this really true? (Hint: If Studebaker were to make this investment, what

would his debt position look like in year 20?)

Answer :-

Yes, it is true, life insurance policy will be accumulated after 20 years to $1,763,925/- as

indicated in Exhibit 3, and as calculated in Answer of Question 1, however if Studebaker

will opt the suggestion of Morton, Studebaker will have to take loan further for $250000/-,

and that amount mortgage Loan will be repaid till the end of 30 years and balance of loan at

the time of maturity of LIC (i.e. at the end of 20 years) would be $440393.33/-.

6. (A) If the excess $300,000 were invested in a long-term asset yielding 8 percent a

year,how much would be accumulated after 20 years?

Answer :- $1,398,287, will be accumulated after 20 Years, Calculation is as follows:-

End

of

Year

Long Term Assets

Value at Opening of

the year (Figures in

$)

Return earned at

the rate of 8%

during the year

(Figures in $)

Long Term Assets

Value at Closing

of the year

(Figures in $)

1 300,000 24,000 324,000

2 324,000 25,920 349,920

3 349,920 27,994 377,914

4 377,914 30,233 408,147

5. Exhibit 3 indicates that $1,763,925 will be accumulated after 20 years in the life

insurance policy. Is this really true? (Hint: If Studebaker were to make this investment, what

would his debt position look like in year 20?)

Answer :-

Yes, it is true, life insurance policy will be accumulated after 20 years to $1,763,925/- as

indicated in Exhibit 3, and as calculated in Answer of Question 1, however if Studebaker

will opt the suggestion of Morton, Studebaker will have to take loan further for $250000/-,

and that amount mortgage Loan will be repaid till the end of 30 years and balance of loan at

the time of maturity of LIC (i.e. at the end of 20 years) would be $440393.33/-.

6. (A) If the excess $300,000 were invested in a long-term asset yielding 8 percent a

year,how much would be accumulated after 20 years?

Answer :- $1,398,287, will be accumulated after 20 Years, Calculation is as follows:-

End

of

Year

Long Term Assets

Value at Opening of

the year (Figures in

$)

Return earned at

the rate of 8%

during the year

(Figures in $)

Long Term Assets

Value at Closing

of the year

(Figures in $)

1 300,000 24,000 324,000

2 324,000 25,920 349,920

3 349,920 27,994 377,914

4 377,914 30,233 408,147

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 408,147 32,652 440,798

6 440,798 35,264 476,062

7 476,062 38,085 514,147

8 514,147 41,132 555,279

9 555,279 44,422 599,701

10 599,701 47,976 647,677

11 647,677 51,814 699,492

12 699,492 55,959 755,451

13 755,451 60,436 815,887

14 815,887 65,271 881,158

15 881,158 70,493 951,651

16 951,651 76,132 1,027,783

17 1,027,783 82,223 1,110,005

18 1,110,005 88,800 1,198,806

19 1,198,806 95,904 1,294,710

20 1,294,710 103,577 1,398,287

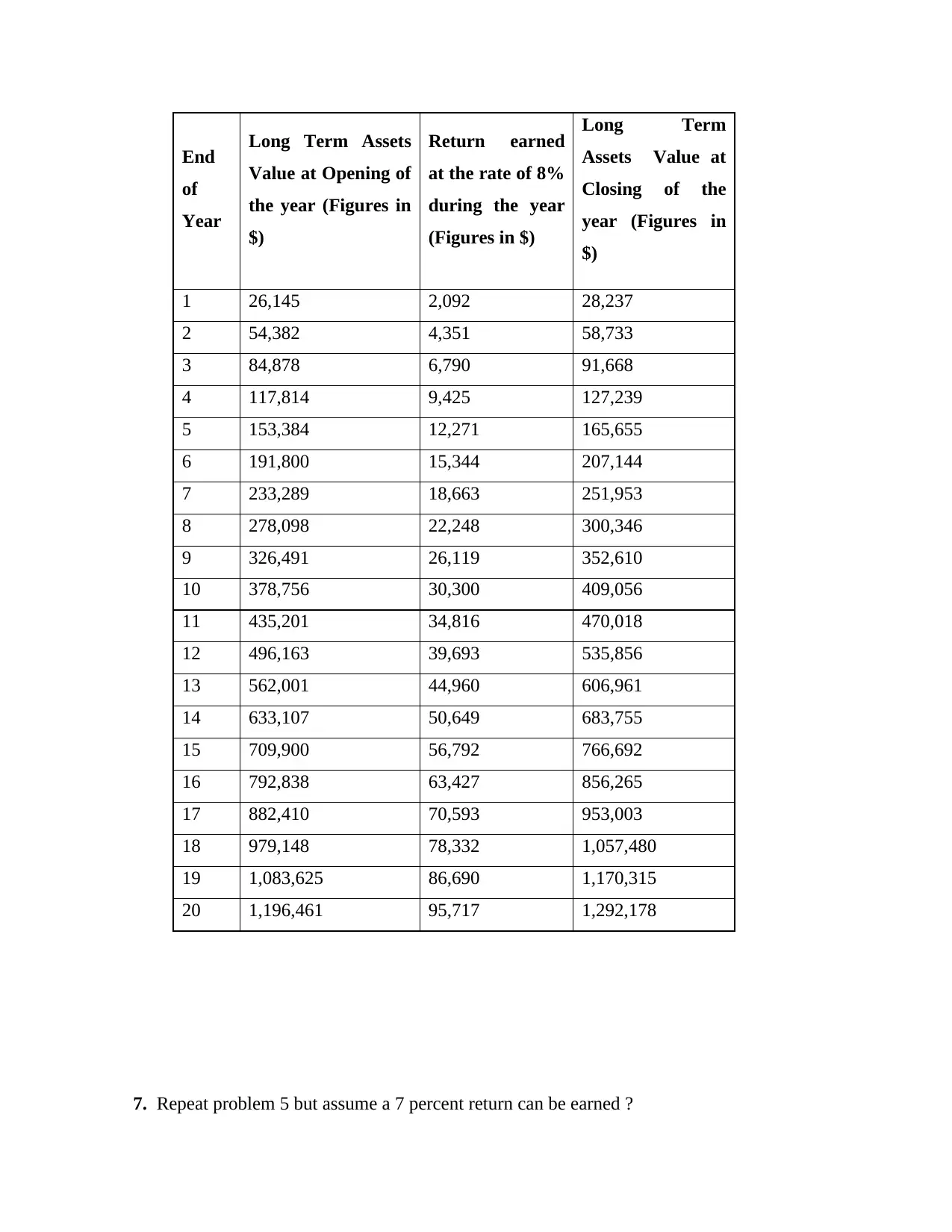

6. (B) Suppose Studebaker placed $26,145.31 a year into a long-term investment paying 8

percent a year. How much would be accumulated after 20 years (amounts invested

at the end of each year)?

Answer :-

$1,292,178/- will be accumulated after 20 Years, if Studebaker Invests $26145.31/- every

year together will earlier Investment, Calculation is as follows:-

6 440,798 35,264 476,062

7 476,062 38,085 514,147

8 514,147 41,132 555,279

9 555,279 44,422 599,701

10 599,701 47,976 647,677

11 647,677 51,814 699,492

12 699,492 55,959 755,451

13 755,451 60,436 815,887

14 815,887 65,271 881,158

15 881,158 70,493 951,651

16 951,651 76,132 1,027,783

17 1,027,783 82,223 1,110,005

18 1,110,005 88,800 1,198,806

19 1,198,806 95,904 1,294,710

20 1,294,710 103,577 1,398,287

6. (B) Suppose Studebaker placed $26,145.31 a year into a long-term investment paying 8

percent a year. How much would be accumulated after 20 years (amounts invested

at the end of each year)?

Answer :-

$1,292,178/- will be accumulated after 20 Years, if Studebaker Invests $26145.31/- every

year together will earlier Investment, Calculation is as follows:-

End

of

Year

Long Term Assets

Value at Opening of

the year (Figures in

$)

Return earned

at the rate of 8%

during the year

(Figures in $)

Long Term

Assets Value at

Closing of the

year (Figures in

$)

1 26,145 2,092 28,237

2 54,382 4,351 58,733

3 84,878 6,790 91,668

4 117,814 9,425 127,239

5 153,384 12,271 165,655

6 191,800 15,344 207,144

7 233,289 18,663 251,953

8 278,098 22,248 300,346

9 326,491 26,119 352,610

10 378,756 30,300 409,056

11 435,201 34,816 470,018

12 496,163 39,693 535,856

13 562,001 44,960 606,961

14 633,107 50,649 683,755

15 709,900 56,792 766,692

16 792,838 63,427 856,265

17 882,410 70,593 953,003

18 979,148 78,332 1,057,480

19 1,083,625 86,690 1,170,315

20 1,196,461 95,717 1,292,178

7. Repeat problem 5 but assume a 7 percent return can be earned ?

of

Year

Long Term Assets

Value at Opening of

the year (Figures in

$)

Return earned

at the rate of 8%

during the year

(Figures in $)

Long Term

Assets Value at

Closing of the

year (Figures in

$)

1 26,145 2,092 28,237

2 54,382 4,351 58,733

3 84,878 6,790 91,668

4 117,814 9,425 127,239

5 153,384 12,271 165,655

6 191,800 15,344 207,144

7 233,289 18,663 251,953

8 278,098 22,248 300,346

9 326,491 26,119 352,610

10 378,756 30,300 409,056

11 435,201 34,816 470,018

12 496,163 39,693 535,856

13 562,001 44,960 606,961

14 633,107 50,649 683,755

15 709,900 56,792 766,692

16 792,838 63,427 856,265

17 882,410 70,593 953,003

18 979,148 78,332 1,057,480

19 1,083,625 86,690 1,170,315

20 1,196,461 95,717 1,292,178

7. Repeat problem 5 but assume a 7 percent return can be earned ?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.