University of Phoenix FP/100: Time Value of Money, Taxes Worksheet

VerifiedAdded on 2020/05/28

|8

|1924

|132

Homework Assignment

AI Summary

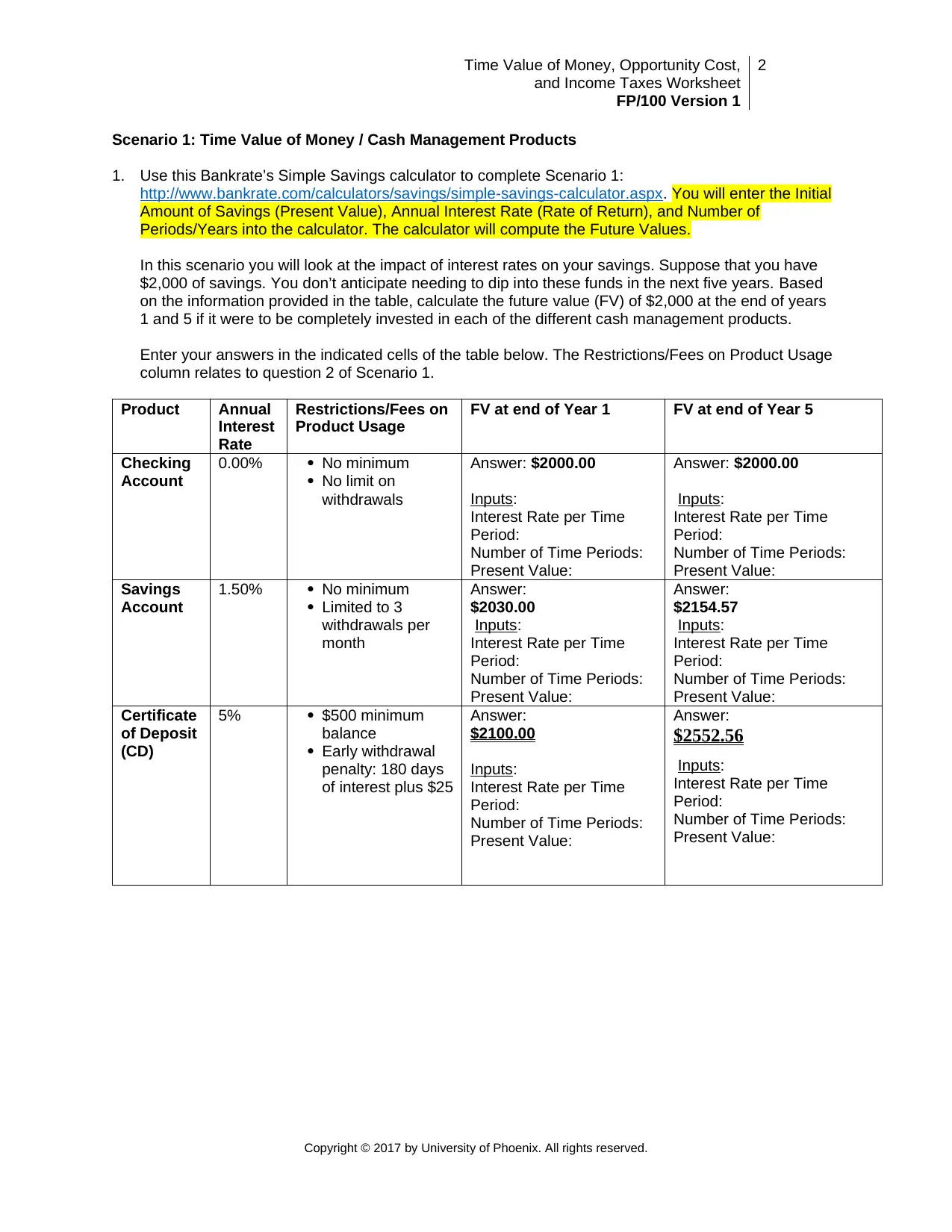

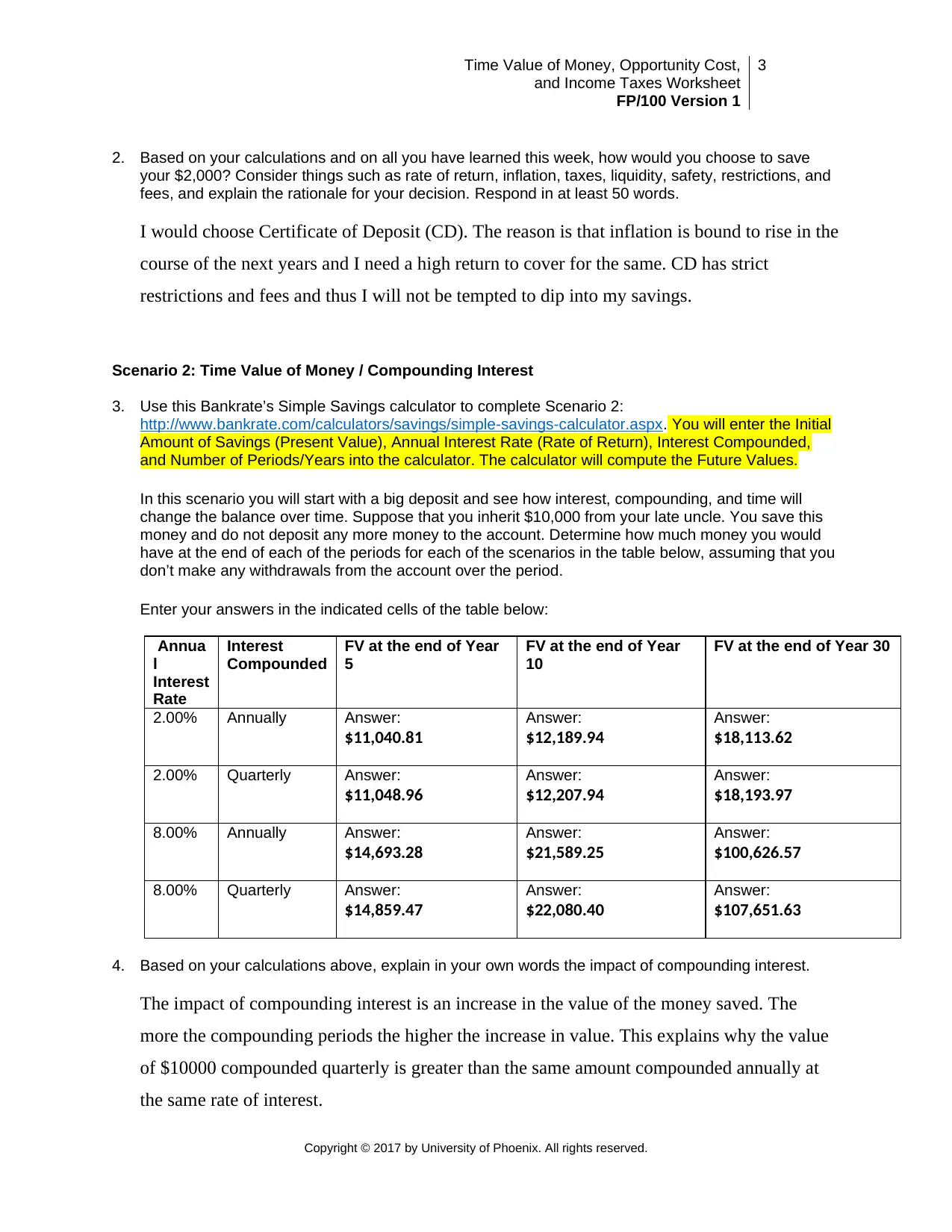

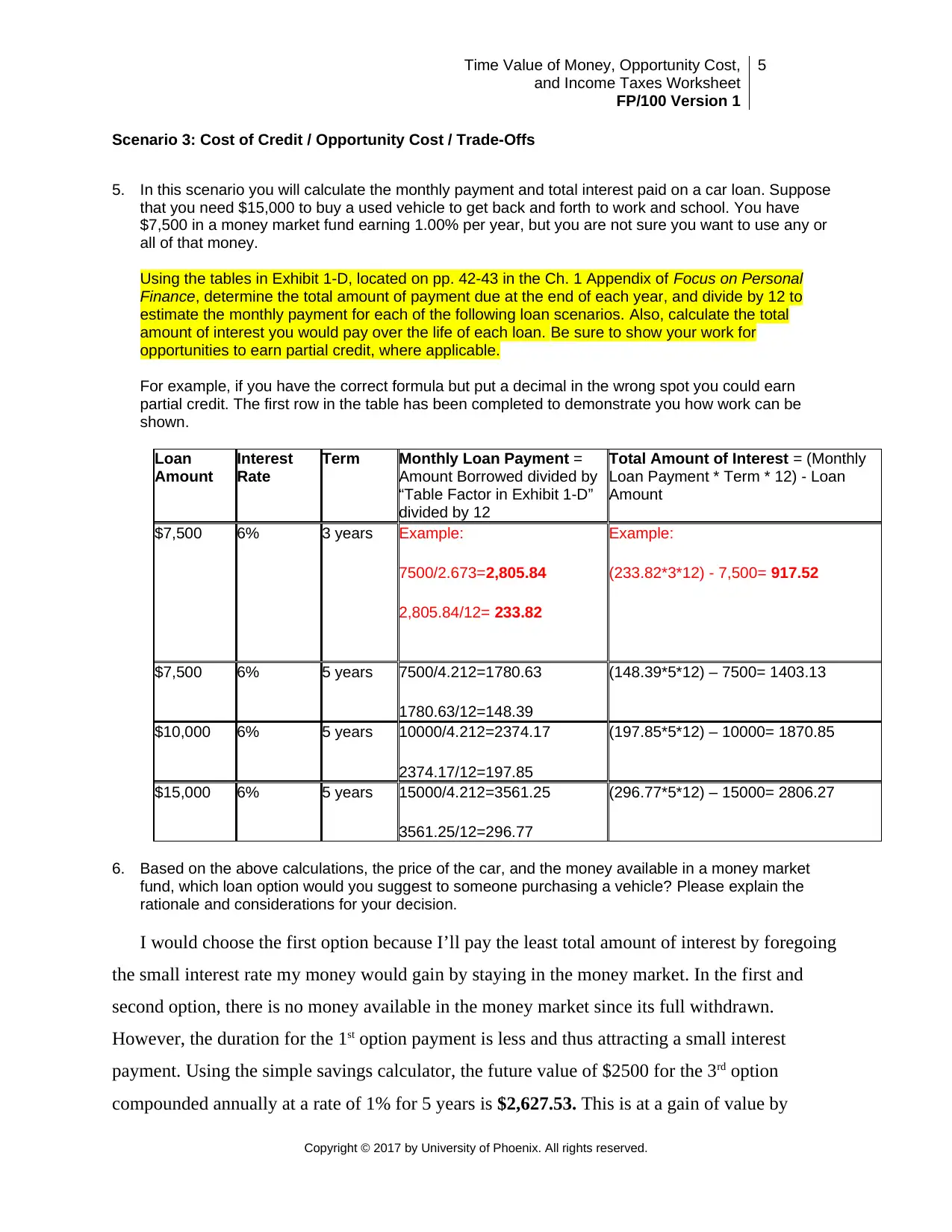

This assignment is a comprehensive finance worksheet exploring key financial concepts. It begins with scenarios on the time value of money, using a savings calculator to assess the impact of interest rates on investments, and the effects of compounding interest over time. The assignment then delves into the cost of credit, opportunity cost, and trade-offs involved in purchasing a vehicle, calculating loan payments and interest paid under different scenarios. Finally, the worksheet addresses income taxes, differentiating between taxable income and adjusted gross income, and defining tax deductions, exemptions, and tax credits. The student provides detailed calculations, explanations, and rationales for their financial decisions, demonstrating an understanding of these critical financial planning principles.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.