Taxation Law Assignment - TLAW603, University Name, Semester 2, 2019

VerifiedAdded on 2022/10/01

|11

|2253

|17

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing various aspects of Australian tax law. The assignment delves into the tax implications of income earned through personal exertion, including salary and gifts, and explores the deductibility of various expenses such as entertainment, clothing, and self-education. It examines the tax treatment of business income, hobby income, and depreciation of assets. Furthermore, the solution analyzes superannuation, including the taxation of withdrawals from foreign super funds and strategies for tax reduction, such as re-contribution strategies. The assignment also covers the deductibility of expenses related to self-education and attending conferences. The case study involves a sessional lecturer, Piper, and her financial activities, providing practical application of tax principles. The solution references relevant legislation and case law to support its arguments and conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

References:.................................................................................................................................9

2TAXATION LAW

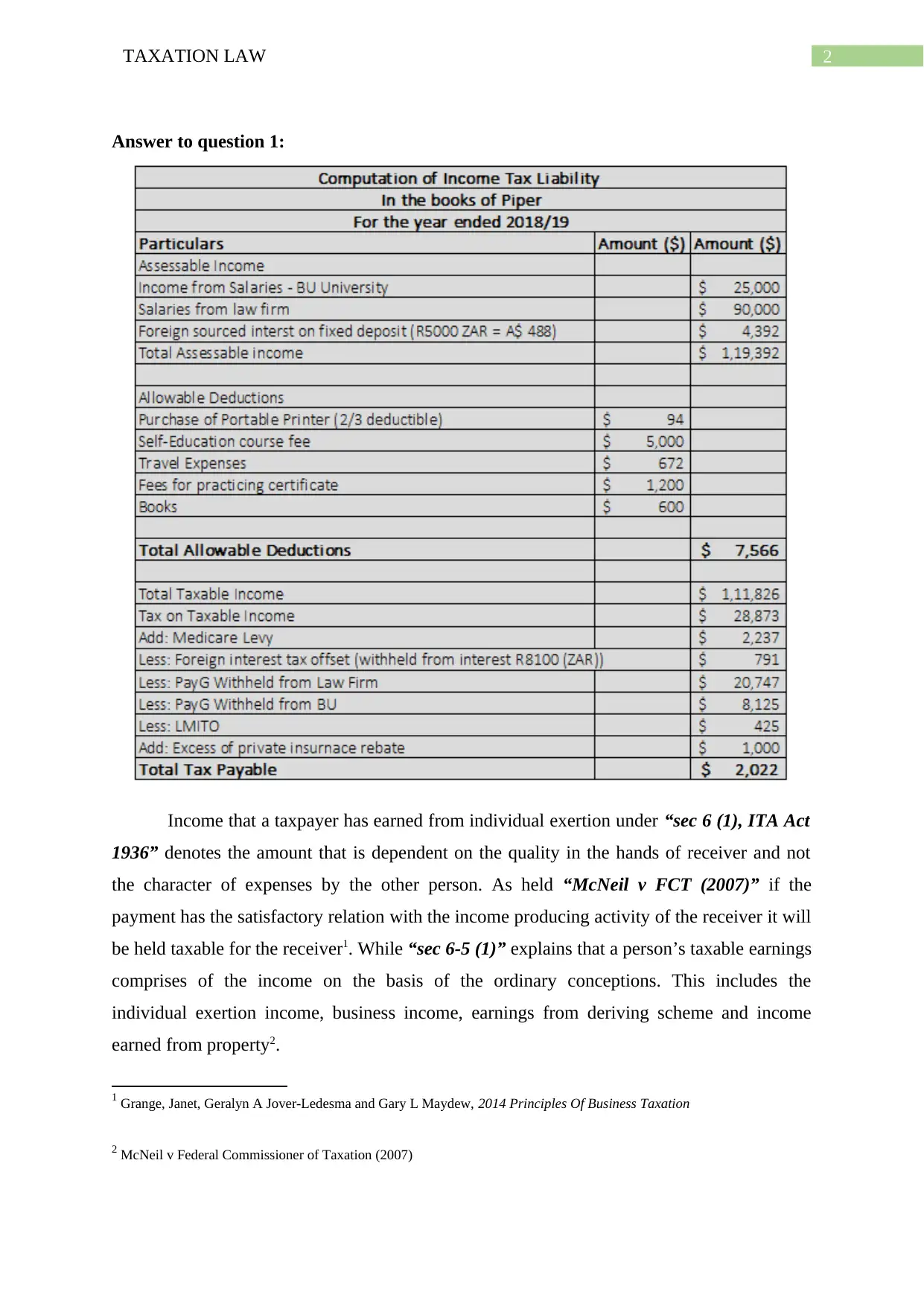

Answer to question 1:

Income that a taxpayer has earned from individual exertion under “sec 6 (1), ITA Act

1936” denotes the amount that is dependent on the quality in the hands of receiver and not

the character of expenses by the other person. As held “McNeil v FCT (2007)” if the

payment has the satisfactory relation with the income producing activity of the receiver it will

be held taxable for the receiver1. While “sec 6-5 (1)” explains that a person’s taxable earnings

comprises of the income on the basis of the ordinary conceptions. This includes the

individual exertion income, business income, earnings from deriving scheme and income

earned from property2.

1 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

2 McNeil v Federal Commissioner of Taxation (2007)

Answer to question 1:

Income that a taxpayer has earned from individual exertion under “sec 6 (1), ITA Act

1936” denotes the amount that is dependent on the quality in the hands of receiver and not

the character of expenses by the other person. As held “McNeil v FCT (2007)” if the

payment has the satisfactory relation with the income producing activity of the receiver it will

be held taxable for the receiver1. While “sec 6-5 (1)” explains that a person’s taxable earnings

comprises of the income on the basis of the ordinary conceptions. This includes the

individual exertion income, business income, earnings from deriving scheme and income

earned from property2.

1 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

2 McNeil v Federal Commissioner of Taxation (2007)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

The salary received by piper from part-time employment in BU is a personal exertion

income under “sec 6 (1), ITA Act 1936”. Denoting “McNeil v FCT (2007)” the salary will

be chargeable as ordinary earnings within “sec 6-5 (1)”.

Payment that a taxpayer has receive from previous employer or service providers is

not usually treated having income nature when it is given out of personal relationship

between the receiver and the payee3. In “Scott v FCT (1966)” gift of shares given to

accountant by the previous employer was not an assessable income. The Woolworths gift

voucher received for free advice does not amounts to assessable income for piper4. Referring

to “Scott v FCT (1966)” the gift voucher does not has any commercial relation and therefore

non-taxable under “sec 6-5, ITAA 97”.

Usually no deduction is allowed for entertainment expenses under “sec 32-10, ITAA

1997” that involves food, drink or recreation5. The expense of $360 reported by Piper on soft

drink and meal is an entertainment expenses and not deductible under “sec 32-10, ITAA

1997”. Expenses on ordinary article of clothes is termed as personal expenses and non-

deductible under “sec.8-1, ITAA 1997”. The decision in “FCT v Mansfield (1996)” noted

that outgoings on ordinary clothing items is denied deductibility irrespective of whether it is

important in a particular job or profession6. Piper will be denied deduction under “sec.8-1,

ITAA 1997” for spending $5000 on clothes for maintaining a professional job appearance as

it is not related to production of income.

Receipts derived from any business activity is characterised as ordinary business

income under “sec 6-5, ITAA 1997”. Whereas receipts from non-business acts such as from

hobby or recreational activities is a non-taxable income. Regular indicators of business

includes nature of activity and the degree of capital or level of turnover. In “JR Walker v

FCT (1985)” small activities may hold the nature of business if there is any adequate

character7. During the year Piper made income from occasional cooking of meal to her

neighbours. She received around $25 per meal and there were four different occasions where

3 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

4 Scott v Federal Commissioner of Taxation (1966)

5 Krever, Richard E, Australian Taxation Law Cases 2015 (Thomson Reuters, 2015)

6 Federal Commissioner of Taxation v Mansfield (1996)

The salary received by piper from part-time employment in BU is a personal exertion

income under “sec 6 (1), ITA Act 1936”. Denoting “McNeil v FCT (2007)” the salary will

be chargeable as ordinary earnings within “sec 6-5 (1)”.

Payment that a taxpayer has receive from previous employer or service providers is

not usually treated having income nature when it is given out of personal relationship

between the receiver and the payee3. In “Scott v FCT (1966)” gift of shares given to

accountant by the previous employer was not an assessable income. The Woolworths gift

voucher received for free advice does not amounts to assessable income for piper4. Referring

to “Scott v FCT (1966)” the gift voucher does not has any commercial relation and therefore

non-taxable under “sec 6-5, ITAA 97”.

Usually no deduction is allowed for entertainment expenses under “sec 32-10, ITAA

1997” that involves food, drink or recreation5. The expense of $360 reported by Piper on soft

drink and meal is an entertainment expenses and not deductible under “sec 32-10, ITAA

1997”. Expenses on ordinary article of clothes is termed as personal expenses and non-

deductible under “sec.8-1, ITAA 1997”. The decision in “FCT v Mansfield (1996)” noted

that outgoings on ordinary clothing items is denied deductibility irrespective of whether it is

important in a particular job or profession6. Piper will be denied deduction under “sec.8-1,

ITAA 1997” for spending $5000 on clothes for maintaining a professional job appearance as

it is not related to production of income.

Receipts derived from any business activity is characterised as ordinary business

income under “sec 6-5, ITAA 1997”. Whereas receipts from non-business acts such as from

hobby or recreational activities is a non-taxable income. Regular indicators of business

includes nature of activity and the degree of capital or level of turnover. In “JR Walker v

FCT (1985)” small activities may hold the nature of business if there is any adequate

character7. During the year Piper made income from occasional cooking of meal to her

neighbours. She received around $25 per meal and there were four different occasions where

3 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

4 Scott v Federal Commissioner of Taxation (1966)

5 Krever, Richard E, Australian Taxation Law Cases 2015 (Thomson Reuters, 2015)

6 Federal Commissioner of Taxation v Mansfield (1996)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

she reported such kind of receipts. Referring to “JR Walker v FCT (1985)” the receipts

earned from supply of meal is not a business income because there is no such commercial

intent nor any capital is employed by Piper. The receipt of $25 is a hobby or recreational

activity and cannot be considered chargeable as business income8.

Notably “sec 40.25 (2)” permits the taxpayer to seek deduction for the depreciating

asset till the extent that is used for generating assessable income and excluding any private

portion of the asset. In case of Piper, a deduction for decline in value of printer is permissible

within “sec 40.25 (2)” till two-third extent which is actually used in production of her

assessable income.

As it is noted within “sec 8-1, ITAA 97” a deduction for self-education outgoing

when incurred by taxpayer in maintaining or improving their occupational skills where they

are presently working, particularly where the outgoings are improving the prospect of

promotion and income producing purpose. In “Highfield v FCT (1982)” deductions was

permitted to taxpayer for outgoings that were occurred in self-education purpose because they

were treated relevant and incidental to the taxpayer’s occupation. Piper will be allowed to get

deduction for self-education course fees incurred in master degree under “sec 8-1, ITAA

97”9. Referring to “Finn v FCT (1982)” the outgoing should be considered relevant and

incidental to the Piper’s profession.

Where a taxpayer reports travel outgoings related to the self-education purpose then

they may allowed for deduction when has sufficient nexus with the income generating

activities of the taxpayer10. In “Finn v FCT (1961)” the architect employee was given

deduction under “sec 8-1, ITAA 97” for travel outgoings occurred in travelling overseas for

studying architect because the expenses were related to generation of income11.

7 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia,

2013)

8 JR Walker v Federal Commissioner of Taxation (1985)

9 Highfield v Federal Commissioner of Taxation (1982)

10 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook Co./Thomson Reuters, 2013)

11 Finn v Federal Commissioner of Taxation (1961)

she reported such kind of receipts. Referring to “JR Walker v FCT (1985)” the receipts

earned from supply of meal is not a business income because there is no such commercial

intent nor any capital is employed by Piper. The receipt of $25 is a hobby or recreational

activity and cannot be considered chargeable as business income8.

Notably “sec 40.25 (2)” permits the taxpayer to seek deduction for the depreciating

asset till the extent that is used for generating assessable income and excluding any private

portion of the asset. In case of Piper, a deduction for decline in value of printer is permissible

within “sec 40.25 (2)” till two-third extent which is actually used in production of her

assessable income.

As it is noted within “sec 8-1, ITAA 97” a deduction for self-education outgoing

when incurred by taxpayer in maintaining or improving their occupational skills where they

are presently working, particularly where the outgoings are improving the prospect of

promotion and income producing purpose. In “Highfield v FCT (1982)” deductions was

permitted to taxpayer for outgoings that were occurred in self-education purpose because they

were treated relevant and incidental to the taxpayer’s occupation. Piper will be allowed to get

deduction for self-education course fees incurred in master degree under “sec 8-1, ITAA

97”9. Referring to “Finn v FCT (1982)” the outgoing should be considered relevant and

incidental to the Piper’s profession.

Where a taxpayer reports travel outgoings related to the self-education purpose then

they may allowed for deduction when has sufficient nexus with the income generating

activities of the taxpayer10. In “Finn v FCT (1961)” the architect employee was given

deduction under “sec 8-1, ITAA 97” for travel outgoings occurred in travelling overseas for

studying architect because the expenses were related to generation of income11.

7 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia,

2013)

8 JR Walker v Federal Commissioner of Taxation (1985)

9 Highfield v Federal Commissioner of Taxation (1982)

10 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook Co./Thomson Reuters, 2013)

11 Finn v Federal Commissioner of Taxation (1961)

5TAXATION LAW

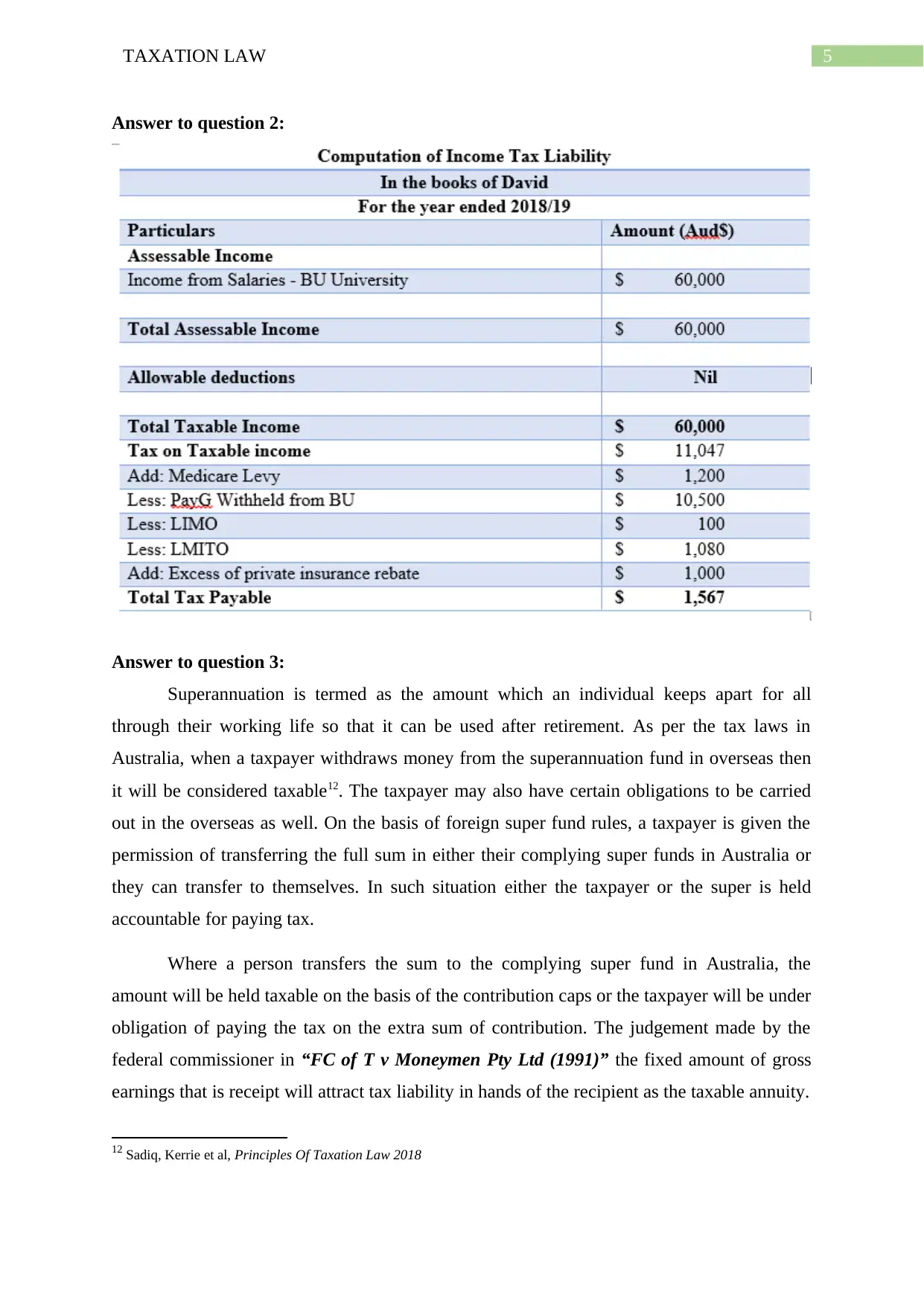

Answer to question 2:

Answer to question 3:

Superannuation is termed as the amount which an individual keeps apart for all

through their working life so that it can be used after retirement. As per the tax laws in

Australia, when a taxpayer withdraws money from the superannuation fund in overseas then

it will be considered taxable12. The taxpayer may also have certain obligations to be carried

out in the overseas as well. On the basis of foreign super fund rules, a taxpayer is given the

permission of transferring the full sum in either their complying super funds in Australia or

they can transfer to themselves. In such situation either the taxpayer or the super is held

accountable for paying tax.

Where a person transfers the sum to the complying super fund in Australia, the

amount will be held taxable on the basis of the contribution caps or the taxpayer will be under

obligation of paying the tax on the extra sum of contribution. The judgement made by the

federal commissioner in “FC of T v Moneymen Pty Ltd (1991)” the fixed amount of gross

earnings that is receipt will attract tax liability in hands of the recipient as the taxable annuity.

12 Sadiq, Kerrie et al, Principles Of Taxation Law 2018

Answer to question 2:

Answer to question 3:

Superannuation is termed as the amount which an individual keeps apart for all

through their working life so that it can be used after retirement. As per the tax laws in

Australia, when a taxpayer withdraws money from the superannuation fund in overseas then

it will be considered taxable12. The taxpayer may also have certain obligations to be carried

out in the overseas as well. On the basis of foreign super fund rules, a taxpayer is given the

permission of transferring the full sum in either their complying super funds in Australia or

they can transfer to themselves. In such situation either the taxpayer or the super is held

accountable for paying tax.

Where a person transfers the sum to the complying super fund in Australia, the

amount will be held taxable on the basis of the contribution caps or the taxpayer will be under

obligation of paying the tax on the extra sum of contribution. The judgement made by the

federal commissioner in “FC of T v Moneymen Pty Ltd (1991)” the fixed amount of gross

earnings that is receipt will attract tax liability in hands of the recipient as the taxable annuity.

12 Sadiq, Kerrie et al, Principles Of Taxation Law 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

When a taxpayer gets the lump sum amount, then the assessable extent of the money

along with the associated funds must be included in the assessable income of the taxpayer.

The amount will be held taxable on the basis of the marginal tax rate13. Whereas the rest of

transfer amount that exceeds the amount of investment at the time of transfer will be included

in their assessable income. Similarly, the earnings made from the applicable fund constitute

the income which the taxpayer has earned from the foreign super interest which has accrued

from the day when an individual turns into an Australian occupant.

The present case facts that is obtained suggest that Piper has realised retirement

investment annuity and has transferred the cash in his Australian bank account. The lump

sum that is received will be held as the taxable lump sum from the foreign super fund.

Referring to the decision given in “FC of T v Moneymen Pty Ltd (1991)” the applicable

funds income will form the part of Piper’s assessable income and will be held chargeable on

the basis of the marginal rate14.

While to reduce the tax liability of Piper relating to withdrawal from the foreign

retirement fund, she should make use of re-contribution strategy as it is a useful in lowering

her tax liability15. There are certain number of areas where the re-contribution strategy can be

used by her. These are as follows;

Estate Planning:

Piper should use the re-distribution strategy to reduce the taxable component of her

retirement fund benefit by allocating it to a non-tax dependent. Piper can simply entrust the

fund on the non-dependents who are below 18 years since they are not required to pay tax on

income.

Tax Planning:

The case study provides that Piper is below the age of 60 years. She is advised to use

the money to pay her income stream in her super account until she attains her retirement age.

The taxable component of her income stream will be considered taxable on the basis of the

13 Taylor, C. J et al, Understanding Taxation Law 2018

14 Federal Commissioner of Taxation v Moneymen Pty Ltd (1991)

15 Taylor, C. J et al, Understanding Taxation Law 2018

When a taxpayer gets the lump sum amount, then the assessable extent of the money

along with the associated funds must be included in the assessable income of the taxpayer.

The amount will be held taxable on the basis of the marginal tax rate13. Whereas the rest of

transfer amount that exceeds the amount of investment at the time of transfer will be included

in their assessable income. Similarly, the earnings made from the applicable fund constitute

the income which the taxpayer has earned from the foreign super interest which has accrued

from the day when an individual turns into an Australian occupant.

The present case facts that is obtained suggest that Piper has realised retirement

investment annuity and has transferred the cash in his Australian bank account. The lump

sum that is received will be held as the taxable lump sum from the foreign super fund.

Referring to the decision given in “FC of T v Moneymen Pty Ltd (1991)” the applicable

funds income will form the part of Piper’s assessable income and will be held chargeable on

the basis of the marginal rate14.

While to reduce the tax liability of Piper relating to withdrawal from the foreign

retirement fund, she should make use of re-contribution strategy as it is a useful in lowering

her tax liability15. There are certain number of areas where the re-contribution strategy can be

used by her. These are as follows;

Estate Planning:

Piper should use the re-distribution strategy to reduce the taxable component of her

retirement fund benefit by allocating it to a non-tax dependent. Piper can simply entrust the

fund on the non-dependents who are below 18 years since they are not required to pay tax on

income.

Tax Planning:

The case study provides that Piper is below the age of 60 years. She is advised to use

the money to pay her income stream in her super account until she attains her retirement age.

The taxable component of her income stream will be considered taxable on the basis of the

13 Taylor, C. J et al, Understanding Taxation Law 2018

14 Federal Commissioner of Taxation v Moneymen Pty Ltd (1991)

15 Taylor, C. J et al, Understanding Taxation Law 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

marginal tax rate after the 15% tax offsets16. The tax free part of the fund will be paid in her

account and Piper by making use of her re-contribution strategy she can easily convert her

taxable component into a tax-free component. Using this strategy will help in reducing her

tax bill.

Answer to question 4:

The general rule explains that the taxpayer is given the permission of claiming the

deduction relating to the cost occurred in attending seminars, education workshops and

sessions that has sufficient relation with the employment activities of the taxpayer. This

generally comprises of the recognized training course expenditure that are imparted by

special associations17. If on attending the conference involves travel, the taxpayer in such a

situation is required to keep the records of expenses which shows that the taxpayer has

occurred outgoings for self-education purpose and should simply ignore the private portion of

expenses occurred in the tour.

The general deduction rule given in “sec 8-1, ITAA 1997” allows the taxpayer to get

the deduction for the self-education purpose provided that the self-education expenses are

very much relevant in their present employment. The decision given in “FC of T v Studdert

(1991)” permitted the deduction to the flight engineer for the cost occurred in self-education

purpose because the expenses were mainly directed towards improving the performance of

the taxpayer in his present employment and simultaneously increasing the promotional

aspects as well.

While the ATO says that a taxpayer is given the permission of claiming deduction in

the year in which the expenses takes place18. Commonly, deductions is permitted for training,

seminars and workshops that has nexus with employment. The outgoings should be incurred

by the taxpayer by themselves and should not be reimbursed. The outgoings should relate

with the income producing acts and the taxpayer should maintain the records of the expenses

so that they can prove it while claiming deductions.

16 Taylor, C. J et al, Understanding Taxation Law 2018

17 Section 8-1, Income Tax Assessment Act 1997 (Cth).

18 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford

University Press, 2018.

marginal tax rate after the 15% tax offsets16. The tax free part of the fund will be paid in her

account and Piper by making use of her re-contribution strategy she can easily convert her

taxable component into a tax-free component. Using this strategy will help in reducing her

tax bill.

Answer to question 4:

The general rule explains that the taxpayer is given the permission of claiming the

deduction relating to the cost occurred in attending seminars, education workshops and

sessions that has sufficient relation with the employment activities of the taxpayer. This

generally comprises of the recognized training course expenditure that are imparted by

special associations17. If on attending the conference involves travel, the taxpayer in such a

situation is required to keep the records of expenses which shows that the taxpayer has

occurred outgoings for self-education purpose and should simply ignore the private portion of

expenses occurred in the tour.

The general deduction rule given in “sec 8-1, ITAA 1997” allows the taxpayer to get

the deduction for the self-education purpose provided that the self-education expenses are

very much relevant in their present employment. The decision given in “FC of T v Studdert

(1991)” permitted the deduction to the flight engineer for the cost occurred in self-education

purpose because the expenses were mainly directed towards improving the performance of

the taxpayer in his present employment and simultaneously increasing the promotional

aspects as well.

While the ATO says that a taxpayer is given the permission of claiming deduction in

the year in which the expenses takes place18. Commonly, deductions is permitted for training,

seminars and workshops that has nexus with employment. The outgoings should be incurred

by the taxpayer by themselves and should not be reimbursed. The outgoings should relate

with the income producing acts and the taxpayer should maintain the records of the expenses

so that they can prove it while claiming deductions.

16 Taylor, C. J et al, Understanding Taxation Law 2018

17 Section 8-1, Income Tax Assessment Act 1997 (Cth).

18 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford

University Press, 2018.

8TAXATION LAW

As apparent from the circumstantial evidences of Piper, she plans to attend self-

education conference. The conference is schedule to take place on 1st September 2019 in

Berlin. As evident Piper is looking forward to claim the expenses. Referring to “FC of T v

Studdert (1991)” the expenses were mainly occurred for the self-education purpose of Piper.

It can be stated that the expenses is allowed to claim by Piper only during the year in which it

will take place19. Hence, in the present income year this outgoings cannot be allowed for

deduction but Piper is permitted to claim the deduction for the expenses in the subsequent

income year of 2019-20.

19 Federal Commissioner of Taxation v Studdert (1991)

As apparent from the circumstantial evidences of Piper, she plans to attend self-

education conference. The conference is schedule to take place on 1st September 2019 in

Berlin. As evident Piper is looking forward to claim the expenses. Referring to “FC of T v

Studdert (1991)” the expenses were mainly occurred for the self-education purpose of Piper.

It can be stated that the expenses is allowed to claim by Piper only during the year in which it

will take place19. Hence, in the present income year this outgoings cannot be allowed for

deduction but Piper is permitted to claim the deduction for the expenses in the subsequent

income year of 2019-20.

19 Federal Commissioner of Taxation v Studdert (1991)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Federal Commissioner of Taxation v Mansfield (1996)

Federal Commissioner of Taxation v Moneymen Pty Ltd (1991)

Federal Commissioner of Taxation v Studdert (1991)

Finn v Federal Commissioner of Taxation (1961)

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

Highfield v Federal Commissioner of Taxation (1982)

JR Walker v Federal Commissioner of Taxation (1985)

Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

Krever, Richard E, Australian Taxation Law Cases 2015 (Thomson Reuters, 2015)

McNeil v Federal Commissioner of Taxation (2007)

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013)

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook

Co./Thomson Reuters, 2013)

Sadiq, Kerrie et al, Principles Of Taxation Law 2018

Scott v Federal Commissioner of Taxation (1966)

Section 8-1, Income Tax Assessment Act 1997 (Cth).

Taylor, C. J et al, Understanding Taxation Law 2018

Woellner, R. H, Australian Taxation Law Select 2017 (CCH Australia, 2017)

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Federal Commissioner of Taxation v Mansfield (1996)

Federal Commissioner of Taxation v Moneymen Pty Ltd (1991)

Federal Commissioner of Taxation v Studdert (1991)

Finn v Federal Commissioner of Taxation (1961)

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

Highfield v Federal Commissioner of Taxation (1982)

JR Walker v Federal Commissioner of Taxation (1985)

Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

Krever, Richard E, Australian Taxation Law Cases 2015 (Thomson Reuters, 2015)

McNeil v Federal Commissioner of Taxation (2007)

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013)

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook

Co./Thomson Reuters, 2013)

Sadiq, Kerrie et al, Principles Of Taxation Law 2018

Scott v Federal Commissioner of Taxation (1966)

Section 8-1, Income Tax Assessment Act 1997 (Cth).

Taylor, C. J et al, Understanding Taxation Law 2018

Woellner, R. H, Australian Taxation Law Select 2017 (CCH Australia, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.