Management Accounting Techniques and Reporting for TMA Engineering Ltd

VerifiedAdded on 2020/01/16

|18

|5086

|359

Report

AI Summary

This report provides a detailed analysis of management accounting techniques, focusing on their application within a small business context (TMA Engineering Ltd.). It begins with an introduction to management accounting and its various types, including lean accounting, traditional systems, and transfer pricing. The report then delves into different management accounting reporting methods, such as performance reports, job costing reports, variable analysis reports, and budgets, including traditional costing. The core of the report compares marginal and absorption costing through income statements, highlighting their impact on profitability. Furthermore, it explores planning tools used for budgetary control, discussing their advantages and limitations. Finally, the report examines how organizations adapt management accounting systems to address financial problems, followed by a conclusion summarizing the key findings and a list of references. The report emphasizes cost-effectiveness, financial reporting, and the importance of adapting to financial challenges.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1...........................................................................................................................................3

P1 Management accounting and its different types....................................................................3

P2 Different methods for management accounting reporting....................................................5

P3 Income statement of marginal and absorption costing..........................................................7

TASK 3..........................................................................................................................................10

P4 Different types of planning tools used for budgetary control with their advantages and

limitations..................................................................................................................................10

TASK 4..........................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to

financial problem......................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1...........................................................................................................................................3

P1 Management accounting and its different types....................................................................3

P2 Different methods for management accounting reporting....................................................5

P3 Income statement of marginal and absorption costing..........................................................7

TASK 3..........................................................................................................................................10

P4 Different types of planning tools used for budgetary control with their advantages and

limitations..................................................................................................................................10

TASK 4..........................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to

financial problem......................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting plays vital role in planning and organising the available

financial resources and find out the effective business action to ensure the profitability of the

concern. Therefore, according to American Accounting Association, management accounting is

the effective process to choose best option among the various alternatives available, in the light

of their feasibility and profitability in near future (Ahadiat, 2013). This method helps to interpret

and evaluate the pre and post effects of the projects undertaken through various management

accounting techniques like Annual rate of return method, net present value method or various

budgetary control techniques based on the nature of the project need to be evaluated. In the

present report T.M.A engineering Ltd. is the small business venture with 25 employees and

turnover less than 500000 Pounds is planning to take effective management accounting

techniques like absorption costing, marginal costing or cost volume profit analysis to improve its

cost effectiveness and ensuring better presentation of its accounting reports for its stakeholders.

This report explains various types of management accounting systems wit their benefits and

limitations. Moreover, it signifies the merits and demerits of various budgetary control

techniques. An income statement is also prepared to compare the marginal and absorption

techniques and their effectiveness to improve the performance of the organisation (Albelda,

2011).

TASK 1

P1 Management accounting and its different types

Management accounting is an appropriate method of analysing overall financial

statement which act as a effective tool while estimating the future capital. It is a process to

analyse the results of the goals which was previously planned and find out the reasons of the

variances achieved. Variance means the difference between the standards maintained and the

actual results obtained. Management accounting is the effective process to calculate the

difference occurred and analyse the reason behind, which might be happened due to the internal

inefficiency or external challenges as well as it provides impressive suggestions to remove all the

obstacles and inefficiencies. This process don't have any fixed norms to be followed thus, its

presentation and analysis is based upon the nature and size of the organisation.

Management accounting divided into different parts-

Management accounting plays vital role in planning and organising the available

financial resources and find out the effective business action to ensure the profitability of the

concern. Therefore, according to American Accounting Association, management accounting is

the effective process to choose best option among the various alternatives available, in the light

of their feasibility and profitability in near future (Ahadiat, 2013). This method helps to interpret

and evaluate the pre and post effects of the projects undertaken through various management

accounting techniques like Annual rate of return method, net present value method or various

budgetary control techniques based on the nature of the project need to be evaluated. In the

present report T.M.A engineering Ltd. is the small business venture with 25 employees and

turnover less than 500000 Pounds is planning to take effective management accounting

techniques like absorption costing, marginal costing or cost volume profit analysis to improve its

cost effectiveness and ensuring better presentation of its accounting reports for its stakeholders.

This report explains various types of management accounting systems wit their benefits and

limitations. Moreover, it signifies the merits and demerits of various budgetary control

techniques. An income statement is also prepared to compare the marginal and absorption

techniques and their effectiveness to improve the performance of the organisation (Albelda,

2011).

TASK 1

P1 Management accounting and its different types

Management accounting is an appropriate method of analysing overall financial

statement which act as a effective tool while estimating the future capital. It is a process to

analyse the results of the goals which was previously planned and find out the reasons of the

variances achieved. Variance means the difference between the standards maintained and the

actual results obtained. Management accounting is the effective process to calculate the

difference occurred and analyse the reason behind, which might be happened due to the internal

inefficiency or external challenges as well as it provides impressive suggestions to remove all the

obstacles and inefficiencies. This process don't have any fixed norms to be followed thus, its

presentation and analysis is based upon the nature and size of the organisation.

Management accounting divided into different parts-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lean accounting – According to this accounting system first priority is given to

formulation of various effective strategies which will be very supportive in reducing the

cost. The main reason behind reducing cost is to remove the level of wastage which

might be arises in manufacturing process. In fact there are many more cost which

occurred during producing goods which must be eliminated from this process and to

achieve this accurate information or evidences is required with the help of this system.

Accurate data is very much indispensable to control extra and unused cost or expenditure.

Traditional management accounting system- It is also known as conventional method

which was used earlier by financial accounting system to manage overall enterprise

budget or control cost with the help of various techniques. In fact job order costing or

process costing is included in this method to track various other cost. Basically job

costing method is used when there is a presence of individual allocation whereas process

costing is used or needed in case of many process exist in a production of product. Apart

from this traditional methods was applied by previous companies because it consider as

previous tools.

Transfer pricing- In this accounting system pricing strategy is mainly based on

movement in existing goods which occurs while manufacturing products by different

departments. In fact two important or indispensable cost which included in this

accounting system are variable cost and opportunity cost. Therefore cost increases due to

the increase in production of units which influence the price of product.

Job Costing: Job costing is the method in which cost and expenses of any project are

charged on job rather than process. This method is used by the large manufacturing

companies who has the time limit to complete their orders on time and satisfy the high

demands in market otherwise the order could be replaced by the other competitor in the

market. This method is also used by the organisation who cannot invest high in the

expensive machines and equipments to produce high quality products as per the demands

of its customers in the market, so they join hands with the other job providers who have

the effective machines to produce the quality products.

Apart from this management accounting is very helpful and useful in reducing the extra

and unused cost of an enterprise to maximize their profits by minimizing their losses with the

formulation of various effective strategies which will be very supportive in reducing the

cost. The main reason behind reducing cost is to remove the level of wastage which

might be arises in manufacturing process. In fact there are many more cost which

occurred during producing goods which must be eliminated from this process and to

achieve this accurate information or evidences is required with the help of this system.

Accurate data is very much indispensable to control extra and unused cost or expenditure.

Traditional management accounting system- It is also known as conventional method

which was used earlier by financial accounting system to manage overall enterprise

budget or control cost with the help of various techniques. In fact job order costing or

process costing is included in this method to track various other cost. Basically job

costing method is used when there is a presence of individual allocation whereas process

costing is used or needed in case of many process exist in a production of product. Apart

from this traditional methods was applied by previous companies because it consider as

previous tools.

Transfer pricing- In this accounting system pricing strategy is mainly based on

movement in existing goods which occurs while manufacturing products by different

departments. In fact two important or indispensable cost which included in this

accounting system are variable cost and opportunity cost. Therefore cost increases due to

the increase in production of units which influence the price of product.

Job Costing: Job costing is the method in which cost and expenses of any project are

charged on job rather than process. This method is used by the large manufacturing

companies who has the time limit to complete their orders on time and satisfy the high

demands in market otherwise the order could be replaced by the other competitor in the

market. This method is also used by the organisation who cannot invest high in the

expensive machines and equipments to produce high quality products as per the demands

of its customers in the market, so they join hands with the other job providers who have

the effective machines to produce the quality products.

Apart from this management accounting is very helpful and useful in reducing the extra

and unused cost of an enterprise to maximize their profits by minimizing their losses with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

help of impressive methods. In additional finance system plays a very eminent role in hedging or

controlling business risk or challenges. On the other hand it also helpful in estimating future cost.

P2 Different methods for management accounting reporting

Most of the enterprise try to prepare their own financial statements by considering

essential factors apart from nominal one. In fact report of management accounting is very helpful

in monitoring the company overall performance with the help of various reports for example-

Performance reports - In this report an enterprise can mentioned the actual role of an

individual towards their organization. In fact performance report is consist of

measurement of presentation of employees with the help of sufficient capital. To prepare

this report it is very indispensable to collect accurate data and information of employees

performance. Apart from this financial report needs to consider quantitative research

technique to acquire data for preparing impressive reports with the help of various

measurement techniques. Therefore performance must be evaluated by considering this

report of candidates as well as mangers try to overcome the obstacles to improve the

whole performance of a organization. The main motive of this report is to provide

reliable or authentic information about performance of employees.

Job costing reports- It consist of various cost as well as revenues of an enterprise which

is very helpful in decision making process of budgetary system. In fact it consist of

overall production cost which occurs while manufacturing innovative products. Basically

costing of job is recorded in a ledger accounts over the life or batch after that it

summarized in final trial balance before making of a job costing report or manufacturing

statement. Apart from this it is process of identifying the raw materials and labour cost of

specific job in proper systematic manner after that they use effective or accurate data or

information to create a punctuation for the clients. Therefore it is adopted by every

company to record their whole cost in a single statement which plays a very eminent role

in decision making process.

Variable analysis reports- While manufacturing a product or running any business there

is a occurrence of many more cost from which there is also presence of variable cost

which always fluctuate due to the change in a production unit. In fact variable analysis is

a report consist of records of all the other cost which always changes due to increase in

controlling business risk or challenges. On the other hand it also helpful in estimating future cost.

P2 Different methods for management accounting reporting

Most of the enterprise try to prepare their own financial statements by considering

essential factors apart from nominal one. In fact report of management accounting is very helpful

in monitoring the company overall performance with the help of various reports for example-

Performance reports - In this report an enterprise can mentioned the actual role of an

individual towards their organization. In fact performance report is consist of

measurement of presentation of employees with the help of sufficient capital. To prepare

this report it is very indispensable to collect accurate data and information of employees

performance. Apart from this financial report needs to consider quantitative research

technique to acquire data for preparing impressive reports with the help of various

measurement techniques. Therefore performance must be evaluated by considering this

report of candidates as well as mangers try to overcome the obstacles to improve the

whole performance of a organization. The main motive of this report is to provide

reliable or authentic information about performance of employees.

Job costing reports- It consist of various cost as well as revenues of an enterprise which

is very helpful in decision making process of budgetary system. In fact it consist of

overall production cost which occurs while manufacturing innovative products. Basically

costing of job is recorded in a ledger accounts over the life or batch after that it

summarized in final trial balance before making of a job costing report or manufacturing

statement. Apart from this it is process of identifying the raw materials and labour cost of

specific job in proper systematic manner after that they use effective or accurate data or

information to create a punctuation for the clients. Therefore it is adopted by every

company to record their whole cost in a single statement which plays a very eminent role

in decision making process.

Variable analysis reports- While manufacturing a product or running any business there

is a occurrence of many more cost from which there is also presence of variable cost

which always fluctuate due to the change in a production unit. In fact variable analysis is

a report consist of records of all the other cost which always changes due to increase in

unit of production. Therefore variable costing is mainly depend upon various other cost

which might be occurred while producing creative goods to attract millions of customers.

Apart from this, preparation of variable report is helpful in analysing the other cost.

Budgets- One of the major or indispensable part of financial accounting because it

describes the overall cost of an enterprise and helpful in estimating the future cost. To

prepare the budget of a company it is very important to consider all the past and present

facts or figures as well as details of an organization. It is not easy to prepare an effective

or impressive budget for whole department because it requires to gather accurate data and

information to maximize their profit by minimizing losses. The main motive of budget

report is to describe the actual usage of overall capital while running a particular business

by satisfying the needs and wants of a whole society or customers. Apart from this it

covers all the activities or task which are need to be achieved by the organization for

attainment of their goals and objectives.

Traditional Costing: Traditional costing is method to allocate the direct cost associated

with the product, labour and material to the cost of the product. Thus it is the method to

calculate the cost of the product with the help of a cost driver which signifies the basic

factor, constitutes the cost such as machine hours, direct labour hours and direct material

hours. It is the method to assign the manufacturing overhead to the units produced. One

of the basic advantage of the traditional costing is that it follows GAAP i.e. Generally

Accepted Accounting principles so it is common and easy implemented method. This

technique is common in small business enterprise like T.M.A Engineering Ltd. But with

the change in technological development and emerging of the computer world this

process is now outdated

Inventory control reports- Its all about controlling or regulating of stock in a proper

manner because it plays a very vital role in production process. In fact it is very helpful in

securing raw materials of a company by utilising all the resources appropriately. There

are many more reason behind preparation of inventory report and these are-

1. Preventing an enterprise from extra and unused wastage.

2. Helpful in removing inventory barriers or obstacles.

3. Useful in protecting stock or raw materials from any harmful effect or damages.

4. Store inventory stock for future.

which might be occurred while producing creative goods to attract millions of customers.

Apart from this, preparation of variable report is helpful in analysing the other cost.

Budgets- One of the major or indispensable part of financial accounting because it

describes the overall cost of an enterprise and helpful in estimating the future cost. To

prepare the budget of a company it is very important to consider all the past and present

facts or figures as well as details of an organization. It is not easy to prepare an effective

or impressive budget for whole department because it requires to gather accurate data and

information to maximize their profit by minimizing losses. The main motive of budget

report is to describe the actual usage of overall capital while running a particular business

by satisfying the needs and wants of a whole society or customers. Apart from this it

covers all the activities or task which are need to be achieved by the organization for

attainment of their goals and objectives.

Traditional Costing: Traditional costing is method to allocate the direct cost associated

with the product, labour and material to the cost of the product. Thus it is the method to

calculate the cost of the product with the help of a cost driver which signifies the basic

factor, constitutes the cost such as machine hours, direct labour hours and direct material

hours. It is the method to assign the manufacturing overhead to the units produced. One

of the basic advantage of the traditional costing is that it follows GAAP i.e. Generally

Accepted Accounting principles so it is common and easy implemented method. This

technique is common in small business enterprise like T.M.A Engineering Ltd. But with

the change in technological development and emerging of the computer world this

process is now outdated

Inventory control reports- Its all about controlling or regulating of stock in a proper

manner because it plays a very vital role in production process. In fact it is very helpful in

securing raw materials of a company by utilising all the resources appropriately. There

are many more reason behind preparation of inventory report and these are-

1. Preventing an enterprise from extra and unused wastage.

2. Helpful in removing inventory barriers or obstacles.

3. Useful in protecting stock or raw materials from any harmful effect or damages.

4. Store inventory stock for future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Apart from this inventory control report covers all the necessary stock and helpful in protecting

products from wastage or damages.

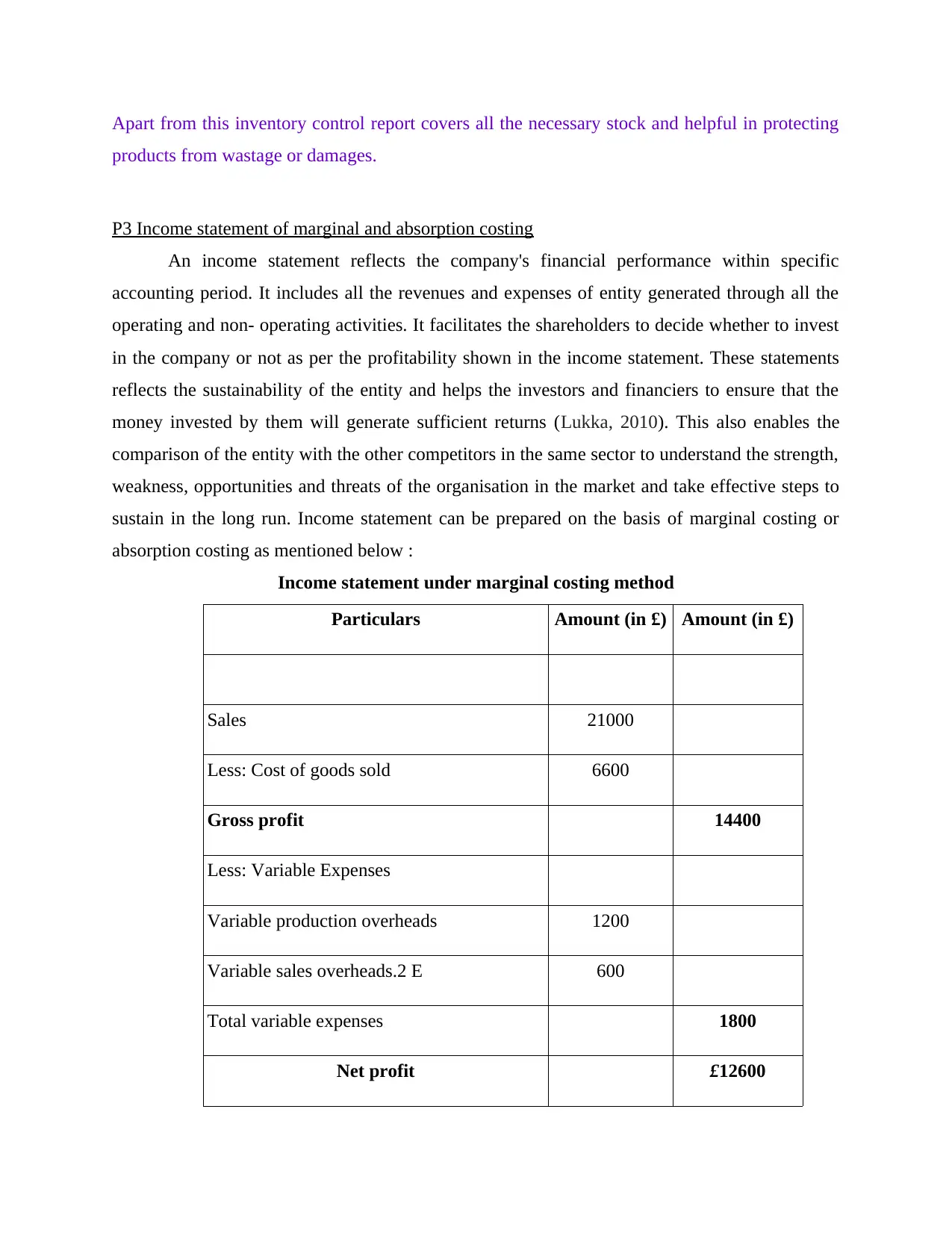

P3 Income statement of marginal and absorption costing

An income statement reflects the company's financial performance within specific

accounting period. It includes all the revenues and expenses of entity generated through all the

operating and non- operating activities. It facilitates the shareholders to decide whether to invest

in the company or not as per the profitability shown in the income statement. These statements

reflects the sustainability of the entity and helps the investors and financiers to ensure that the

money invested by them will generate sufficient returns (Lukka, 2010). This also enables the

comparison of the entity with the other competitors in the same sector to understand the strength,

weakness, opportunities and threats of the organisation in the market and take effective steps to

sustain in the long run. Income statement can be prepared on the basis of marginal costing or

absorption costing as mentioned below :

Income statement under marginal costing method

Particulars Amount (in £) Amount (in £)

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads.2 E 600

Total variable expenses 1800

Net profit £12600

products from wastage or damages.

P3 Income statement of marginal and absorption costing

An income statement reflects the company's financial performance within specific

accounting period. It includes all the revenues and expenses of entity generated through all the

operating and non- operating activities. It facilitates the shareholders to decide whether to invest

in the company or not as per the profitability shown in the income statement. These statements

reflects the sustainability of the entity and helps the investors and financiers to ensure that the

money invested by them will generate sufficient returns (Lukka, 2010). This also enables the

comparison of the entity with the other competitors in the same sector to understand the strength,

weakness, opportunities and threats of the organisation in the market and take effective steps to

sustain in the long run. Income statement can be prepared on the basis of marginal costing or

absorption costing as mentioned below :

Income statement under marginal costing method

Particulars Amount (in £) Amount (in £)

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads.2 E 600

Total variable expenses 1800

Net profit £12600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

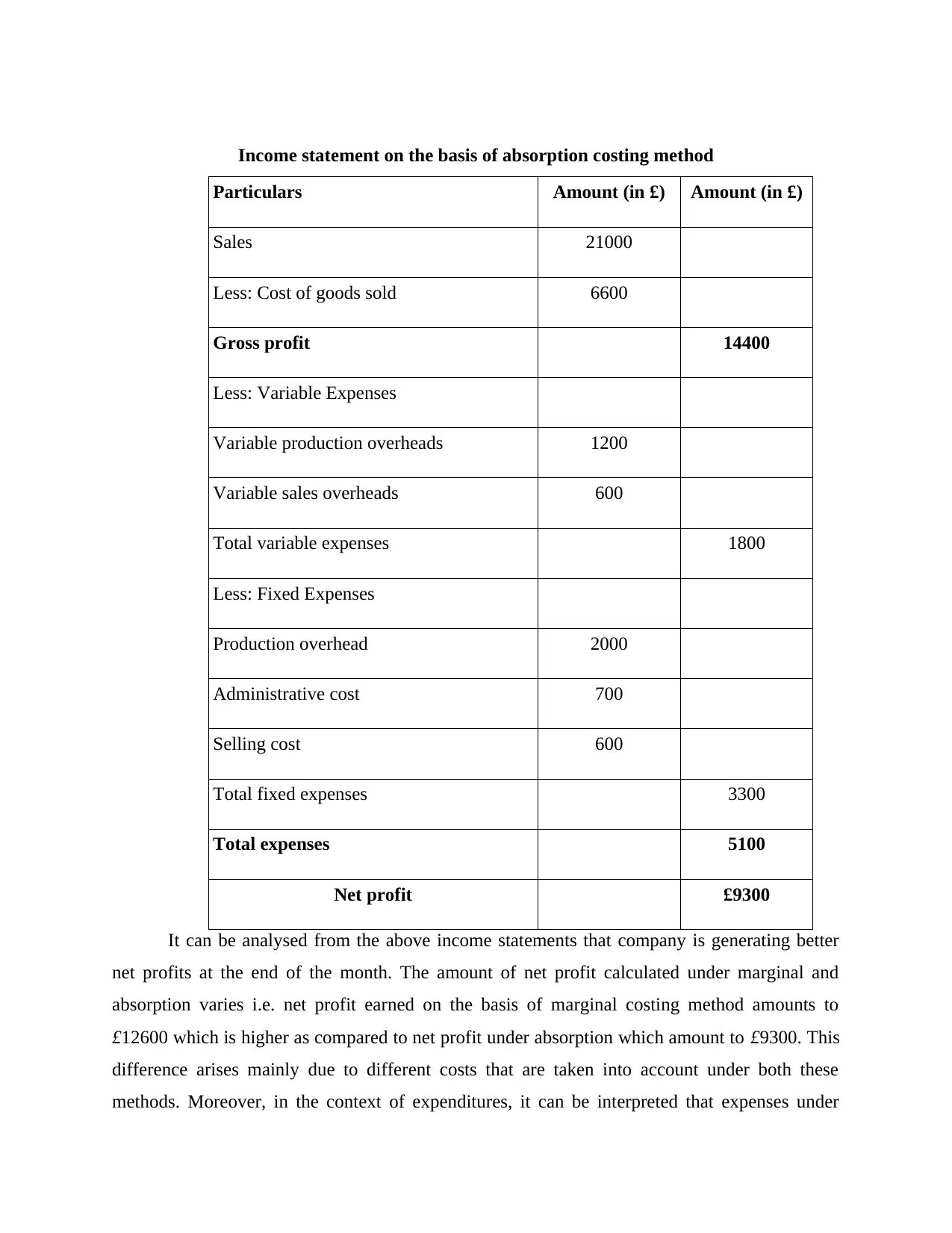

Income statement on the basis of absorption costing method

Particulars Amount (in £) Amount (in £)

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit £9300

It can be analysed from the above income statements that company is generating better

net profits at the end of the month. The amount of net profit calculated under marginal and

absorption varies i.e. net profit earned on the basis of marginal costing method amounts to

£12600 which is higher as compared to net profit under absorption which amount to £9300. This

difference arises mainly due to different costs that are taken into account under both these

methods. Moreover, in the context of expenditures, it can be interpreted that expenses under

Particulars Amount (in £) Amount (in £)

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit £9300

It can be analysed from the above income statements that company is generating better

net profits at the end of the month. The amount of net profit calculated under marginal and

absorption varies i.e. net profit earned on the basis of marginal costing method amounts to

£12600 which is higher as compared to net profit under absorption which amount to £9300. This

difference arises mainly due to different costs that are taken into account under both these

methods. Moreover, in the context of expenditures, it can be interpreted that expenses under

absorption are more i.e. £5100 because it considers both fixed costs and variable costs. Whereas,

expenses as per marginal amounts to £1800 which is quite less because only variable

expenditures are considered in this method.

Generally, most of the companies prefer absorption costing method over marginal costing

method as it taken into account both fixed as well as variable expenditures of an organisation.

Therefore, absorption costing method helps to prepare income statement that shows clear and

appropriate financial performance with regard to profitability of an organisation at the period

end.

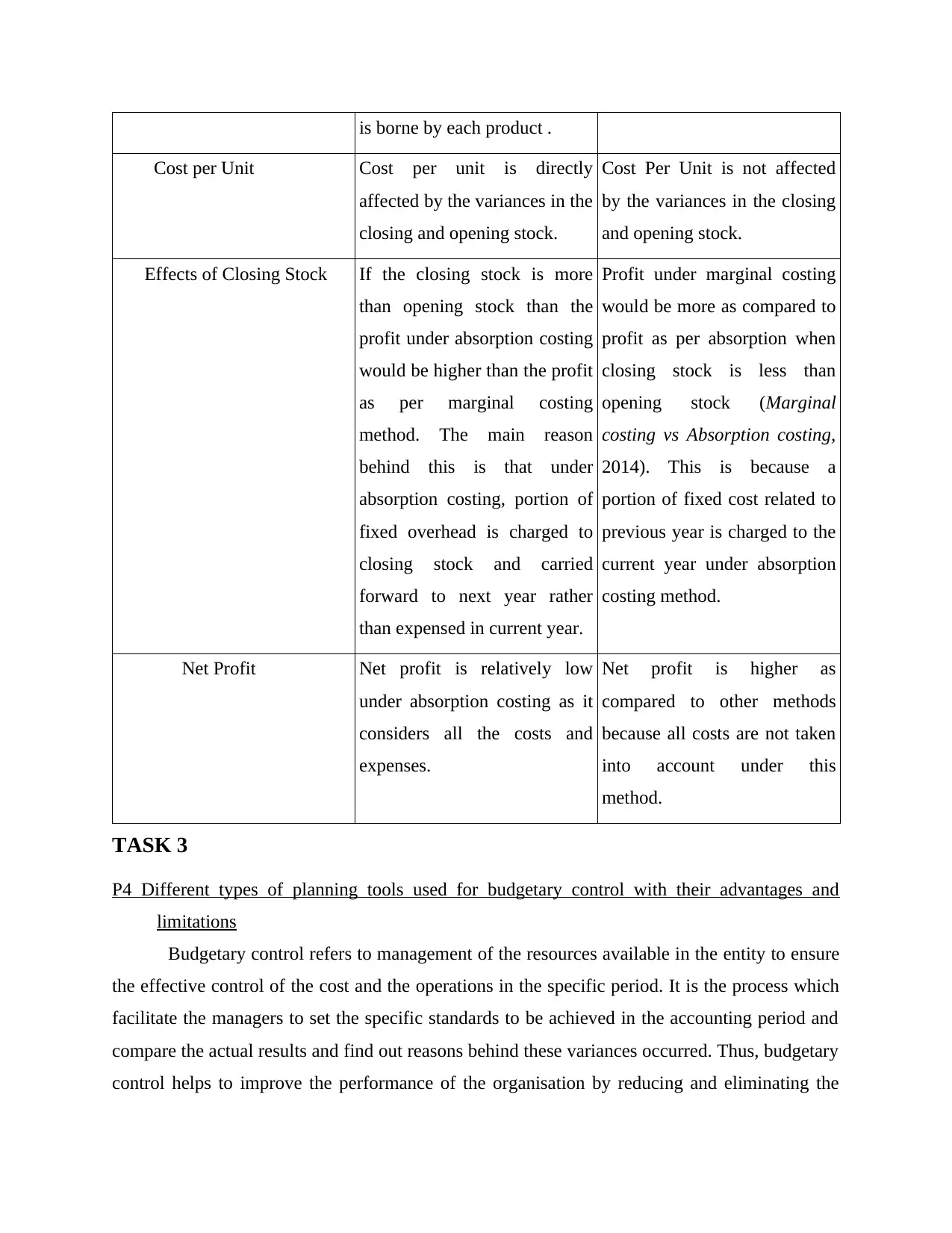

Difference between absorption costing and marginal costing

Basis Absorption Costing Marginal Costing

Meaning Method to calculate the total

cost of production by

allocating the total cost to the

cost centres determined.

Method to calculate total cost

of production to facilitate the

decision making process.

Cost Category For valuation of inventory and

product costing, both variable

costs and fixed costs are

considered.

Under marginal costing, only

variable cost is taken into

account for inventory

valuation and costing of

products.

Classification of Indirect

Expenses also known as

Overheads.

Overheads are classified under

different heads – production,

administration, selling and

distribution.

The basis of classification of

overheads is fixed cost and

variable costs.

Profit Determination Under absorption costing,

fixed cost is charged to the

cost of production (Macintosh,

and Quattrone, 2010).

Therefore, the profitability of a

product is affected by the

apportioned fixed cost which

Fixed costs are considered as a

period cost and profitability of

different products is assessed

by Profit volume ratio (P/V

ratio).

expenses as per marginal amounts to £1800 which is quite less because only variable

expenditures are considered in this method.

Generally, most of the companies prefer absorption costing method over marginal costing

method as it taken into account both fixed as well as variable expenditures of an organisation.

Therefore, absorption costing method helps to prepare income statement that shows clear and

appropriate financial performance with regard to profitability of an organisation at the period

end.

Difference between absorption costing and marginal costing

Basis Absorption Costing Marginal Costing

Meaning Method to calculate the total

cost of production by

allocating the total cost to the

cost centres determined.

Method to calculate total cost

of production to facilitate the

decision making process.

Cost Category For valuation of inventory and

product costing, both variable

costs and fixed costs are

considered.

Under marginal costing, only

variable cost is taken into

account for inventory

valuation and costing of

products.

Classification of Indirect

Expenses also known as

Overheads.

Overheads are classified under

different heads – production,

administration, selling and

distribution.

The basis of classification of

overheads is fixed cost and

variable costs.

Profit Determination Under absorption costing,

fixed cost is charged to the

cost of production (Macintosh,

and Quattrone, 2010).

Therefore, the profitability of a

product is affected by the

apportioned fixed cost which

Fixed costs are considered as a

period cost and profitability of

different products is assessed

by Profit volume ratio (P/V

ratio).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is borne by each product .

Cost per Unit Cost per unit is directly

affected by the variances in the

closing and opening stock.

Cost Per Unit is not affected

by the variances in the closing

and opening stock.

Effects of Closing Stock If the closing stock is more

than opening stock than the

profit under absorption costing

would be higher than the profit

as per marginal costing

method. The main reason

behind this is that under

absorption costing, portion of

fixed overhead is charged to

closing stock and carried

forward to next year rather

than expensed in current year.

Profit under marginal costing

would be more as compared to

profit as per absorption when

closing stock is less than

opening stock (Marginal

costing vs Absorption costing,

2014). This is because a

portion of fixed cost related to

previous year is charged to the

current year under absorption

costing method.

Net Profit Net profit is relatively low

under absorption costing as it

considers all the costs and

expenses.

Net profit is higher as

compared to other methods

because all costs are not taken

into account under this

method.

TASK 3

P4 Different types of planning tools used for budgetary control with their advantages and

limitations

Budgetary control refers to management of the resources available in the entity to ensure

the effective control of the cost and the operations in the specific period. It is the process which

facilitate the managers to set the specific standards to be achieved in the accounting period and

compare the actual results and find out reasons behind these variances occurred. Thus, budgetary

control helps to improve the performance of the organisation by reducing and eliminating the

Cost per Unit Cost per unit is directly

affected by the variances in the

closing and opening stock.

Cost Per Unit is not affected

by the variances in the closing

and opening stock.

Effects of Closing Stock If the closing stock is more

than opening stock than the

profit under absorption costing

would be higher than the profit

as per marginal costing

method. The main reason

behind this is that under

absorption costing, portion of

fixed overhead is charged to

closing stock and carried

forward to next year rather

than expensed in current year.

Profit under marginal costing

would be more as compared to

profit as per absorption when

closing stock is less than

opening stock (Marginal

costing vs Absorption costing,

2014). This is because a

portion of fixed cost related to

previous year is charged to the

current year under absorption

costing method.

Net Profit Net profit is relatively low

under absorption costing as it

considers all the costs and

expenses.

Net profit is higher as

compared to other methods

because all costs are not taken

into account under this

method.

TASK 3

P4 Different types of planning tools used for budgetary control with their advantages and

limitations

Budgetary control refers to management of the resources available in the entity to ensure

the effective control of the cost and the operations in the specific period. It is the process which

facilitate the managers to set the specific standards to be achieved in the accounting period and

compare the actual results and find out reasons behind these variances occurred. Thus, budgetary

control helps to improve the performance of the organisation by reducing and eliminating the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unfavourable operations and strengthen the core areas (Renz, 2016). For maintaining control

over disposals, management uses various types of budgetary control techniques. The three major

techniques used by T.M.A Engineering Ltd. are capital budgeting techniques, preparation of

budget and ratio analysis. These three methods along with their benefits and limitations are

explained as follows :

1. Capital Budgeting Techniques: Capital Budgeting is the effective process to

evaluate the feasibility of the large investment projects such as new plant and

machinery and other projects that directly affect the capital structure of the cited

entity. Large investment projects need to be evaluated through various techniques

like Annual Rate Of Return, Net Present Value and internal Rate Of Return to

calculate the exact viability of the projects and choose the project with low risk

and high return (.Scapens, and Bromwich, 2010).

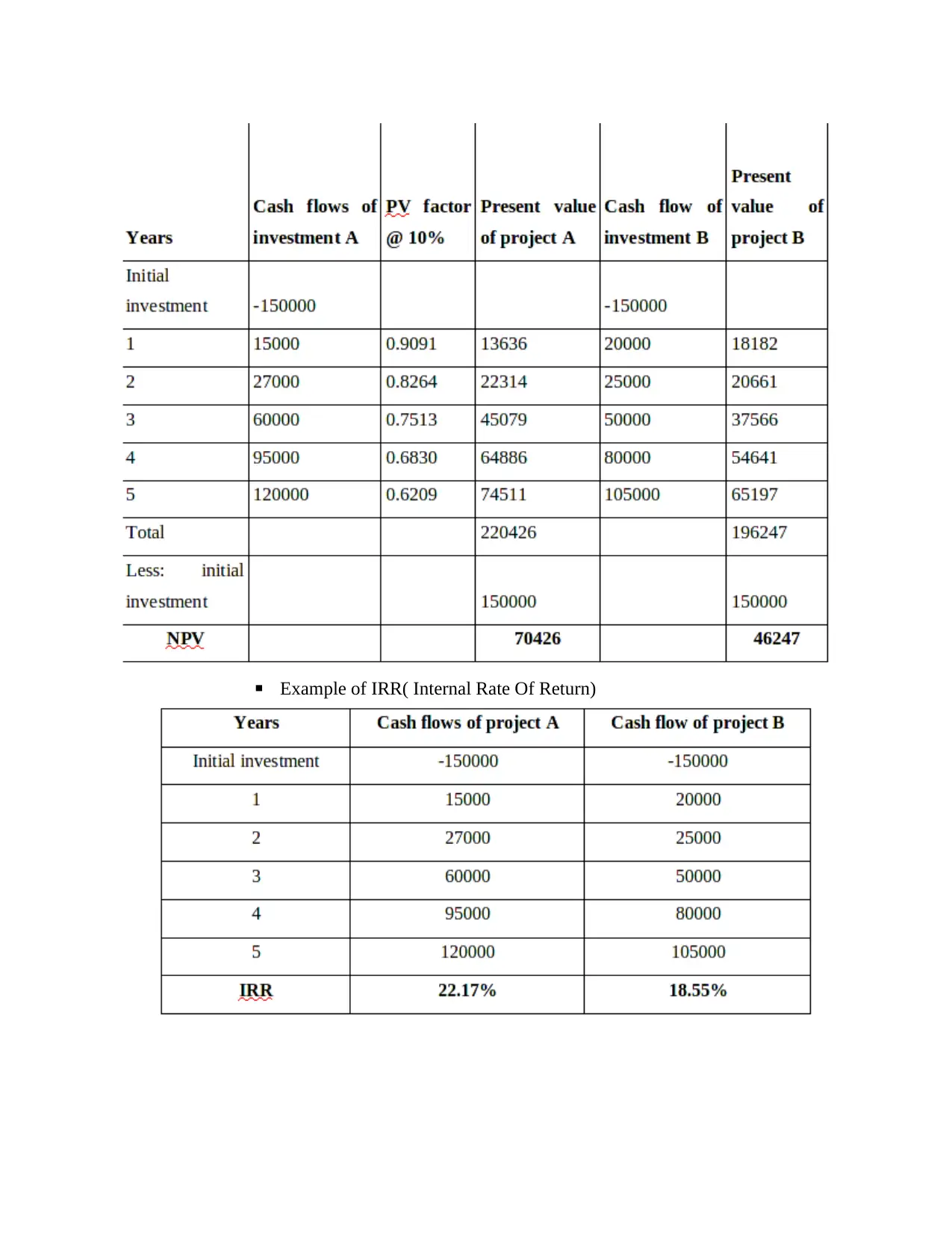

T.M.A Engineering Ltd is planning to invest their money in one of the projects but can't decide

which is to be selected so they have use the following two capital budgeting techniques two

evaluate the feasibility and profitability of both the projects :

▪ Example of NPV (Net Present Value)

over disposals, management uses various types of budgetary control techniques. The three major

techniques used by T.M.A Engineering Ltd. are capital budgeting techniques, preparation of

budget and ratio analysis. These three methods along with their benefits and limitations are

explained as follows :

1. Capital Budgeting Techniques: Capital Budgeting is the effective process to

evaluate the feasibility of the large investment projects such as new plant and

machinery and other projects that directly affect the capital structure of the cited

entity. Large investment projects need to be evaluated through various techniques

like Annual Rate Of Return, Net Present Value and internal Rate Of Return to

calculate the exact viability of the projects and choose the project with low risk

and high return (.Scapens, and Bromwich, 2010).

T.M.A Engineering Ltd is planning to invest their money in one of the projects but can't decide

which is to be selected so they have use the following two capital budgeting techniques two

evaluate the feasibility and profitability of both the projects :

▪ Example of NPV (Net Present Value)

▪ Example of IRR( Internal Rate Of Return)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.