Tom and Jerry Ltd: Financial Analysis and Investment Appraisal

VerifiedAdded on 2023/06/16

|17

|3839

|64

Project

AI Summary

This project provides a comprehensive financial analysis of Tom and Jerry Ltd, including an income statement and balance sheet analysis. It delves into investment appraisal techniques such as payback period, accounting rate of return (ARR), and net present value (NPV) calculations, offering a recommendation based on the analysis. The project also explores break-even point analysis, margin of safety, and the impact of advertising strategies on profitability. Furthermore, it discusses the merits and limitations of various investment appraisal techniques and the benefits and limitations of using budgets as a strategic planning tool. The document concludes with a detailed examination of the assumptions underlying the break-even model and their practical applicability across different business contexts.

PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION-1..................................................................................................................................3

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020.....................3

Financial Position of Tom and Jerry Ltd as at 31 December 2020.............................................4

QUESTION-2..................................................................................................................................5

a) calculation of contribution.......................................................................................................5

b) Breakeven point and margin of safety.....................................................................................5

c) calculation of profit.................................................................................................................6

d) Analysis of strategy.................................................................................................................7

e) assumption in relation with the breakeven model...................................................................8

QUESTION 3..................................................................................................................................9

a) calculation of payback, accounting rate of return and net present value of the company.......9

b) Merits and limitation of various investment appraisal techniques........................................11

c) Benefits and limitations of using budget as a tool in the context of strategic planning........13

REFERENCES..............................................................................................................................16

QUESTION-1..................................................................................................................................3

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020.....................3

Financial Position of Tom and Jerry Ltd as at 31 December 2020.............................................4

QUESTION-2..................................................................................................................................5

a) calculation of contribution.......................................................................................................5

b) Breakeven point and margin of safety.....................................................................................5

c) calculation of profit.................................................................................................................6

d) Analysis of strategy.................................................................................................................7

e) assumption in relation with the breakeven model...................................................................8

QUESTION 3..................................................................................................................................9

a) calculation of payback, accounting rate of return and net present value of the company.......9

b) Merits and limitation of various investment appraisal techniques........................................11

c) Benefits and limitations of using budget as a tool in the context of strategic planning........13

REFERENCES..............................................................................................................................16

QUESTION-1

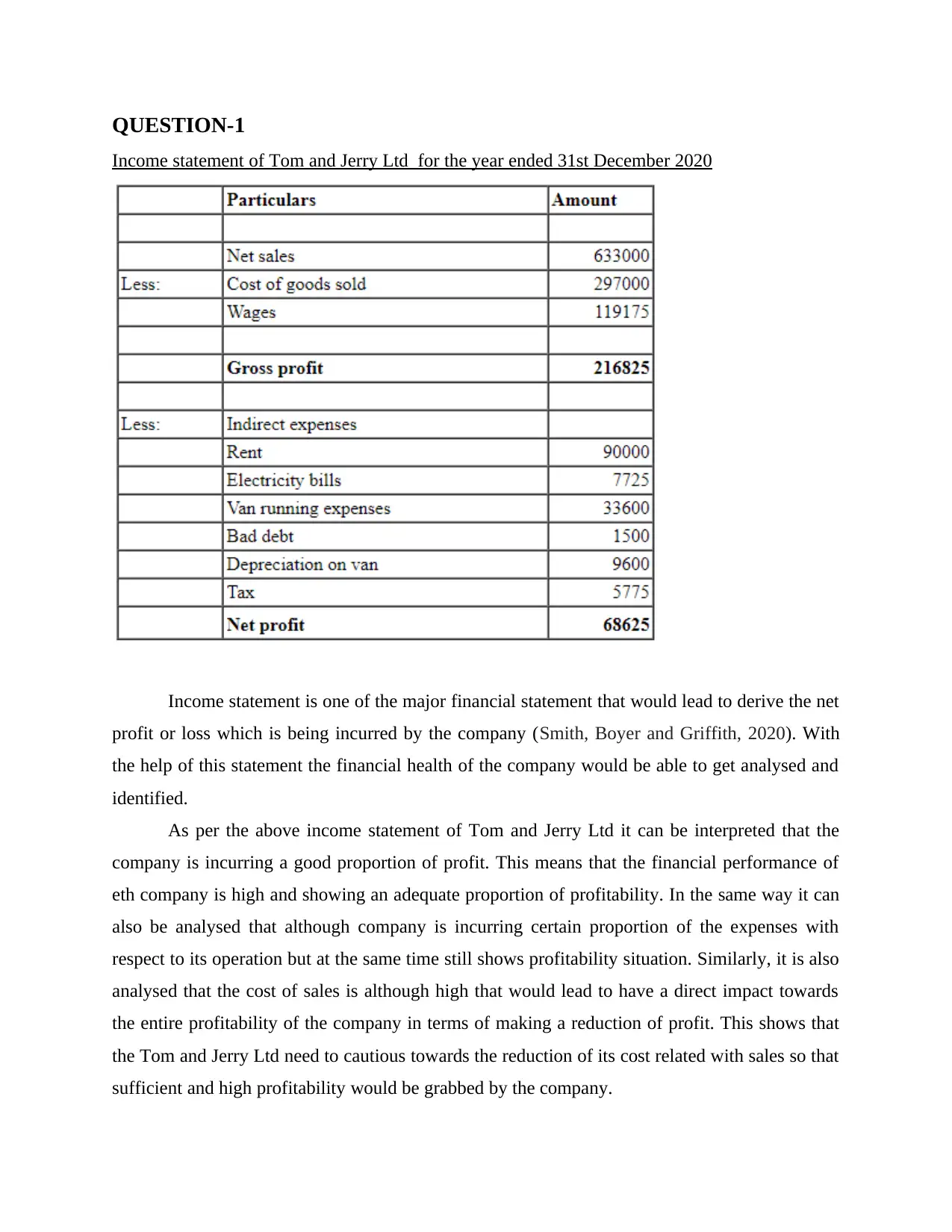

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020

Income statement is one of the major financial statement that would lead to derive the net

profit or loss which is being incurred by the company (Smith, Boyer and Griffith, 2020). With

the help of this statement the financial health of the company would be able to get analysed and

identified.

As per the above income statement of Tom and Jerry Ltd it can be interpreted that the

company is incurring a good proportion of profit. This means that the financial performance of

eth company is high and showing an adequate proportion of profitability. In the same way it can

also be analysed that although company is incurring certain proportion of the expenses with

respect to its operation but at the same time still shows profitability situation. Similarly, it is also

analysed that the cost of sales is although high that would lead to have a direct impact towards

the entire profitability of the company in terms of making a reduction of profit. This shows that

the Tom and Jerry Ltd need to cautious towards the reduction of its cost related with sales so that

sufficient and high profitability would be grabbed by the company.

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020

Income statement is one of the major financial statement that would lead to derive the net

profit or loss which is being incurred by the company (Smith, Boyer and Griffith, 2020). With

the help of this statement the financial health of the company would be able to get analysed and

identified.

As per the above income statement of Tom and Jerry Ltd it can be interpreted that the

company is incurring a good proportion of profit. This means that the financial performance of

eth company is high and showing an adequate proportion of profitability. In the same way it can

also be analysed that although company is incurring certain proportion of the expenses with

respect to its operation but at the same time still shows profitability situation. Similarly, it is also

analysed that the cost of sales is although high that would lead to have a direct impact towards

the entire profitability of the company in terms of making a reduction of profit. This shows that

the Tom and Jerry Ltd need to cautious towards the reduction of its cost related with sales so that

sufficient and high profitability would be grabbed by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

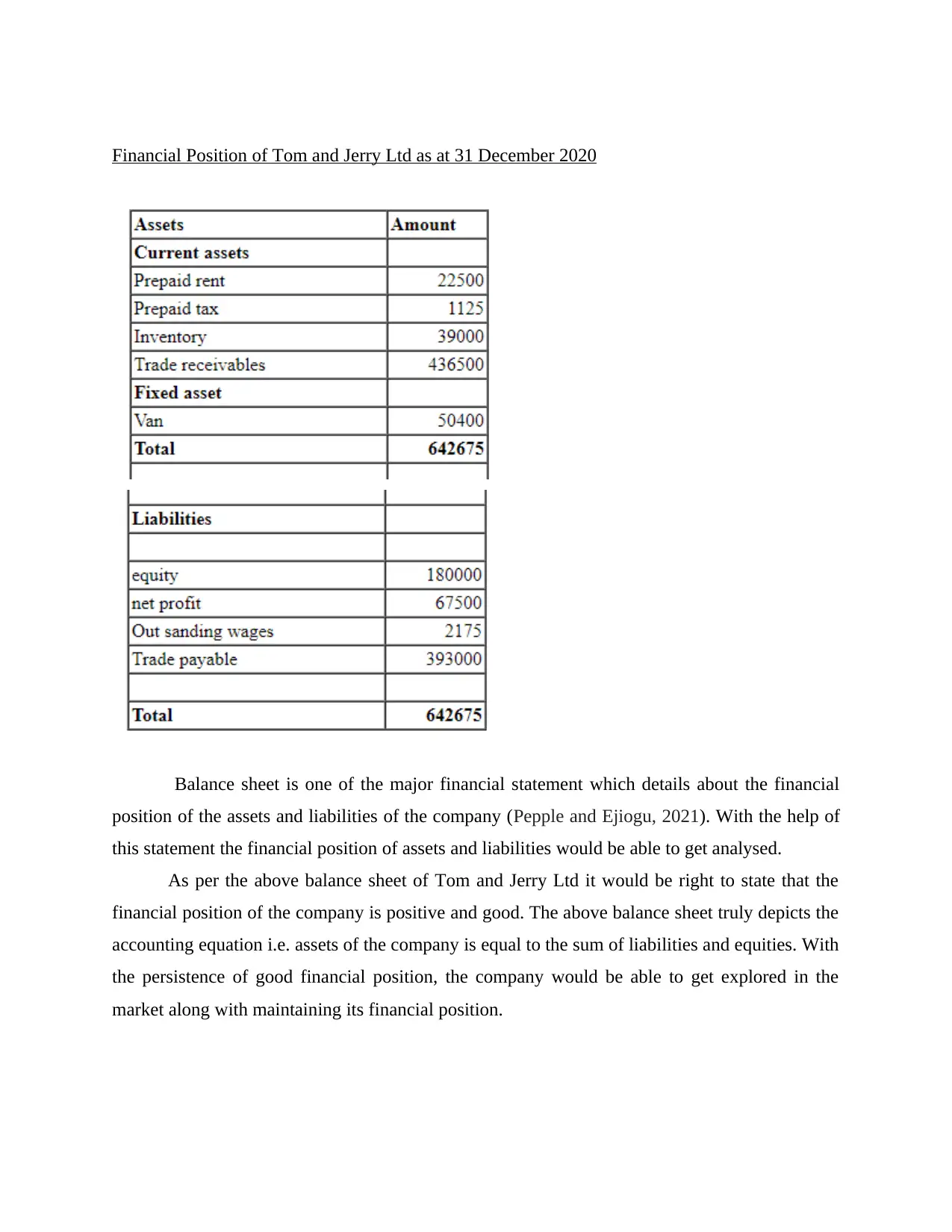

Financial Position of Tom and Jerry Ltd as at 31 December 2020

Balance sheet is one of the major financial statement which details about the financial

position of the assets and liabilities of the company (Pepple and Ejiogu, 2021). With the help of

this statement the financial position of assets and liabilities would be able to get analysed.

As per the above balance sheet of Tom and Jerry Ltd it would be right to state that the

financial position of the company is positive and good. The above balance sheet truly depicts the

accounting equation i.e. assets of the company is equal to the sum of liabilities and equities. With

the persistence of good financial position, the company would be able to get explored in the

market along with maintaining its financial position.

Balance sheet is one of the major financial statement which details about the financial

position of the assets and liabilities of the company (Pepple and Ejiogu, 2021). With the help of

this statement the financial position of assets and liabilities would be able to get analysed.

As per the above balance sheet of Tom and Jerry Ltd it would be right to state that the

financial position of the company is positive and good. The above balance sheet truly depicts the

accounting equation i.e. assets of the company is equal to the sum of liabilities and equities. With

the persistence of good financial position, the company would be able to get explored in the

market along with maintaining its financial position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION-2

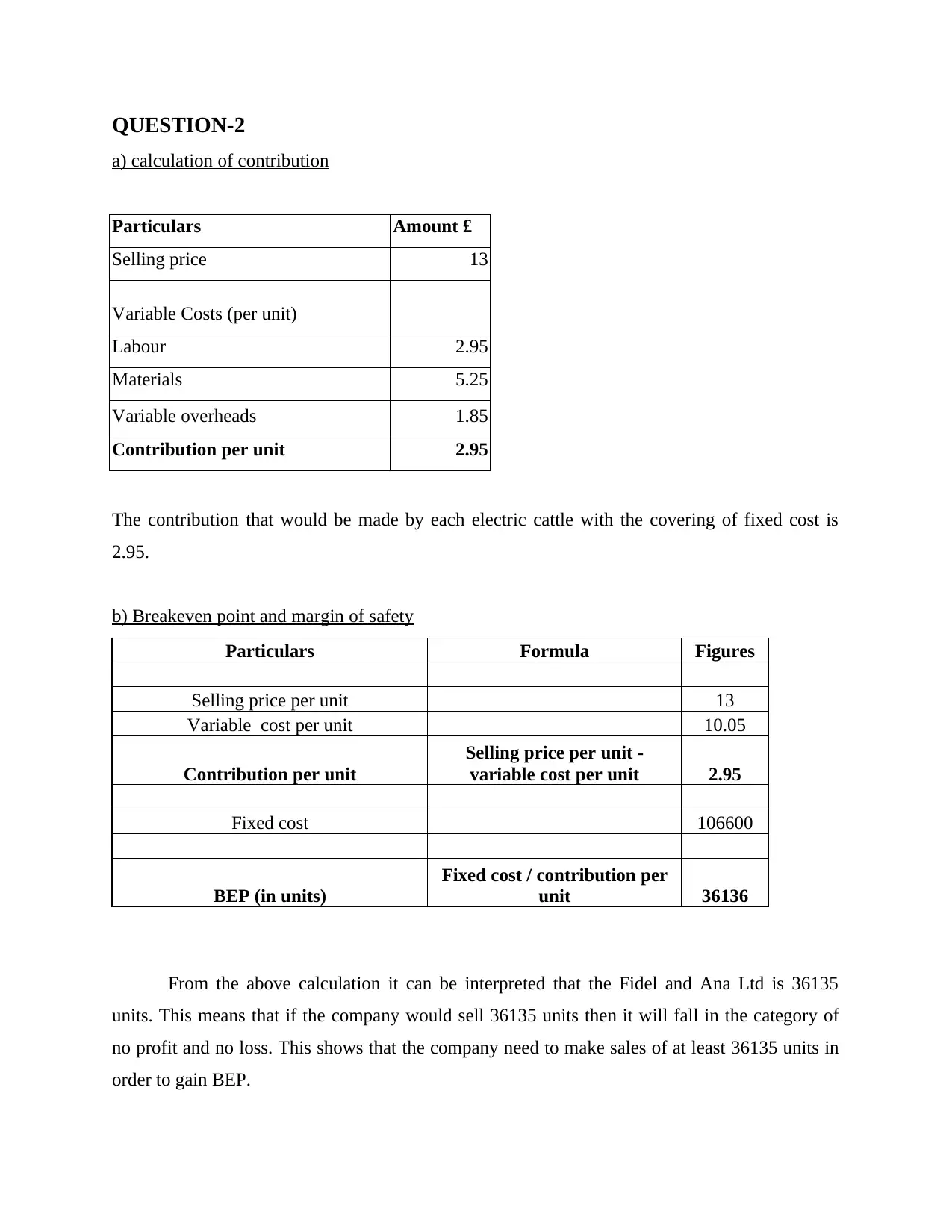

a) calculation of contribution

Particulars Amount £

Selling price 13

Variable Costs (per unit)

Labour 2.95

Materials 5.25

Variable overheads 1.85

Contribution per unit 2.95

The contribution that would be made by each electric cattle with the covering of fixed cost is

2.95.

b) Breakeven point and margin of safety

Particulars Formula Figures

Selling price per unit 13

Variable cost per unit 10.05

Contribution per unit

Selling price per unit -

variable cost per unit 2.95

Fixed cost 106600

BEP (in units)

Fixed cost / contribution per

unit 36136

From the above calculation it can be interpreted that the Fidel and Ana Ltd is 36135

units. This means that if the company would sell 36135 units then it will fall in the category of

no profit and no loss. This shows that the company need to make sales of at least 36135 units in

order to gain BEP.

a) calculation of contribution

Particulars Amount £

Selling price 13

Variable Costs (per unit)

Labour 2.95

Materials 5.25

Variable overheads 1.85

Contribution per unit 2.95

The contribution that would be made by each electric cattle with the covering of fixed cost is

2.95.

b) Breakeven point and margin of safety

Particulars Formula Figures

Selling price per unit 13

Variable cost per unit 10.05

Contribution per unit

Selling price per unit -

variable cost per unit 2.95

Fixed cost 106600

BEP (in units)

Fixed cost / contribution per

unit 36136

From the above calculation it can be interpreted that the Fidel and Ana Ltd is 36135

units. This means that if the company would sell 36135 units then it will fall in the category of

no profit and no loss. This shows that the company need to make sales of at least 36135 units in

order to gain BEP.

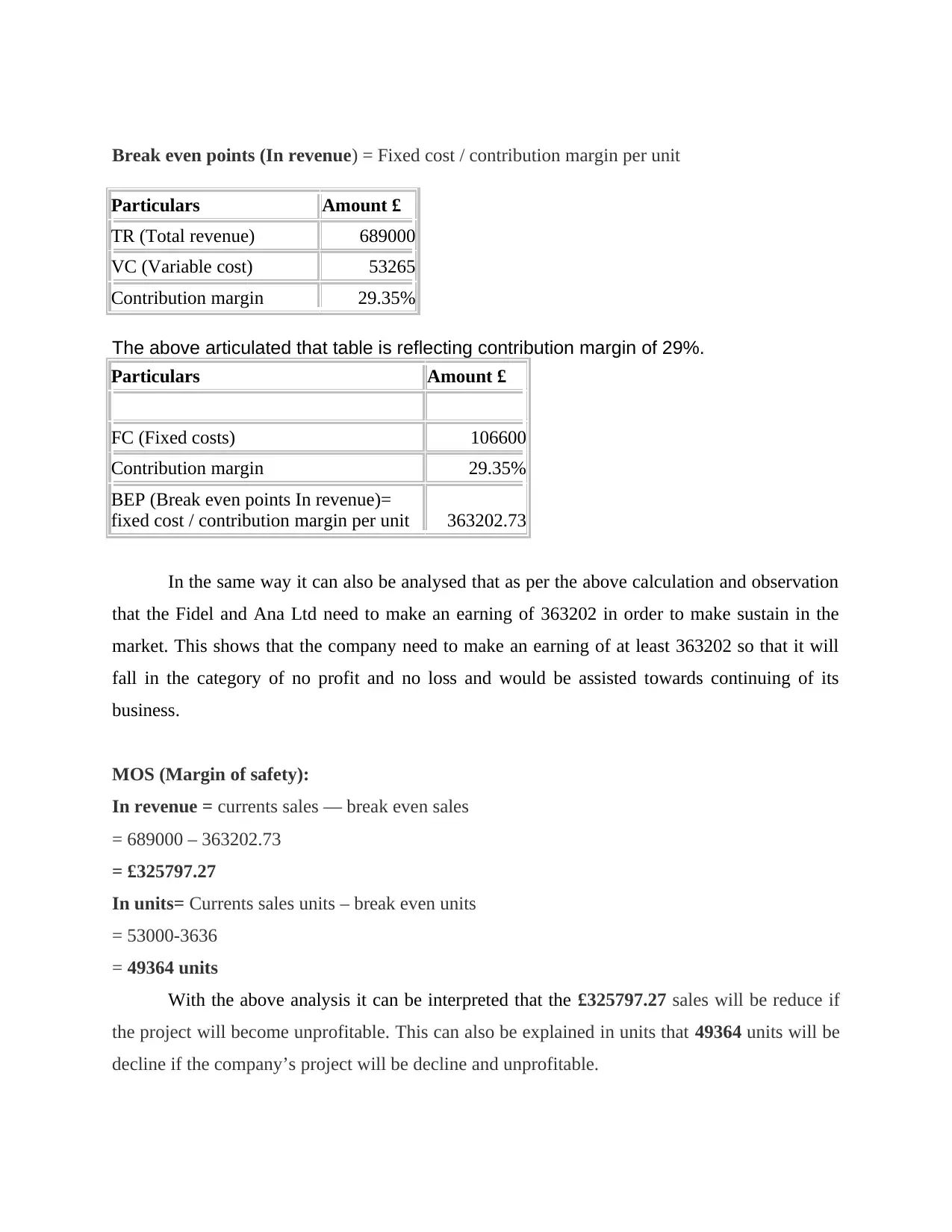

Break even points (In revenue) = Fixed cost / contribution margin per unit

Particulars Amount £

TR (Total revenue) 689000

VC (Variable cost) 53265

Contribution margin 29.35%

The above articulated that table is reflecting contribution margin of 29%.

Particulars Amount £

FC (Fixed costs) 106600

Contribution margin 29.35%

BEP (Break even points In revenue)=

fixed cost / contribution margin per unit 363202.73

In the same way it can also be analysed that as per the above calculation and observation

that the Fidel and Ana Ltd need to make an earning of 363202 in order to make sustain in the

market. This shows that the company need to make an earning of at least 363202 so that it will

fall in the category of no profit and no loss and would be assisted towards continuing of its

business.

MOS (Margin of safety):

In revenue = currents sales — break even sales

= 689000 – 363202.73

= £325797.27

In units= Currents sales units – break even units

= 53000-3636

= 49364 units

With the above analysis it can be interpreted that the £325797.27 sales will be reduce if

the project will become unprofitable. This can also be explained in units that 49364 units will be

decline if the company’s project will be decline and unprofitable.

Particulars Amount £

TR (Total revenue) 689000

VC (Variable cost) 53265

Contribution margin 29.35%

The above articulated that table is reflecting contribution margin of 29%.

Particulars Amount £

FC (Fixed costs) 106600

Contribution margin 29.35%

BEP (Break even points In revenue)=

fixed cost / contribution margin per unit 363202.73

In the same way it can also be analysed that as per the above calculation and observation

that the Fidel and Ana Ltd need to make an earning of 363202 in order to make sustain in the

market. This shows that the company need to make an earning of at least 363202 so that it will

fall in the category of no profit and no loss and would be assisted towards continuing of its

business.

MOS (Margin of safety):

In revenue = currents sales — break even sales

= 689000 – 363202.73

= £325797.27

In units= Currents sales units – break even units

= 53000-3636

= 49364 units

With the above analysis it can be interpreted that the £325797.27 sales will be reduce if

the project will become unprofitable. This can also be explained in units that 49364 units will be

decline if the company’s project will be decline and unprofitable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

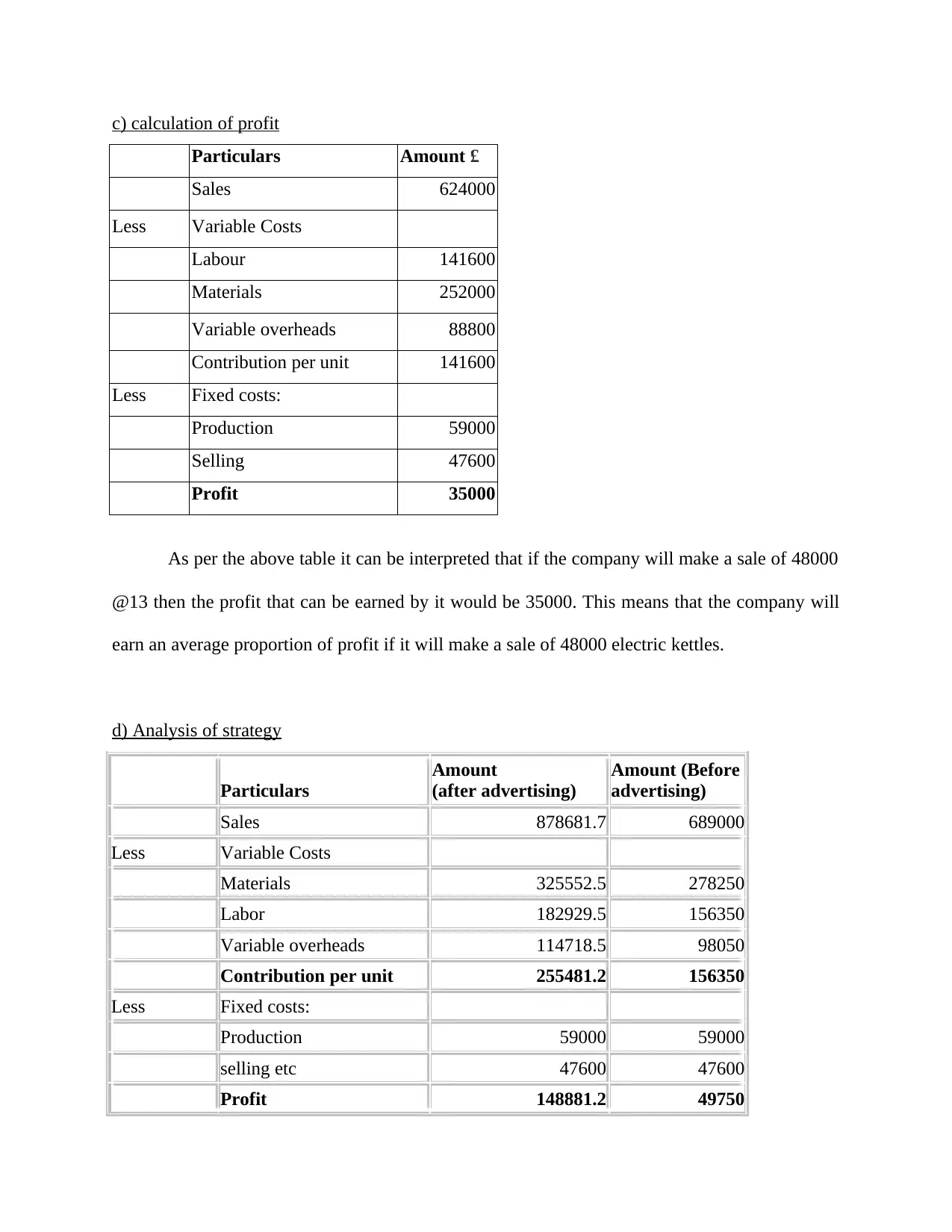

c) calculation of profit

Particulars Amount £

Sales 624000

Less Variable Costs

Labour 141600

Materials 252000

Variable overheads 88800

Contribution per unit 141600

Less Fixed costs:

Production 59000

Selling 47600

Profit 35000

As per the above table it can be interpreted that if the company will make a sale of 48000

@13 then the profit that can be earned by it would be 35000. This means that the company will

earn an average proportion of profit if it will make a sale of 48000 electric kettles.

d) Analysis of strategy

Particulars

Amount

(after advertising)

Amount (Before

advertising)

Sales 878681.7 689000

Less Variable Costs

Materials 325552.5 278250

Labor 182929.5 156350

Variable overheads 114718.5 98050

Contribution per unit 255481.2 156350

Less Fixed costs:

Production 59000 59000

selling etc 47600 47600

Profit 148881.2 49750

Particulars Amount £

Sales 624000

Less Variable Costs

Labour 141600

Materials 252000

Variable overheads 88800

Contribution per unit 141600

Less Fixed costs:

Production 59000

Selling 47600

Profit 35000

As per the above table it can be interpreted that if the company will make a sale of 48000

@13 then the profit that can be earned by it would be 35000. This means that the company will

earn an average proportion of profit if it will make a sale of 48000 electric kettles.

d) Analysis of strategy

Particulars

Amount

(after advertising)

Amount (Before

advertising)

Sales 878681.7 689000

Less Variable Costs

Materials 325552.5 278250

Labor 182929.5 156350

Variable overheads 114718.5 98050

Contribution per unit 255481.2 156350

Less Fixed costs:

Production 59000 59000

selling etc 47600 47600

Profit 148881.2 49750

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e) assumption in relation with the breakeven model

The breakeven analysis refers to that point of sales and aspect within the business that

would assist eth business in terms of analysing the situation of no profit and no loss (Tannen,

2020). This means that it is the unit or the value which if earned by company then it will fall in

the category of no profit and loss.

There are certain assumption which would be made implied in the BEP analysis. These

would include: the fixed cost would remain same with all the level of output, the all other cost

would be counted as either the fixed or the variable, the sales volume is the only aspect that

would affect the cost and sales revenue, other factors including the production, technology,

efficiency would remain unchanged, the business would be considered with the constant product

mix which shows that the company will produce only one type of the product, the sales price

remain constant throughout the level of output, constant inventory at the end of accounting

period and various other (Kostjukova, 2018).

With the persistence of these assumption it would be right to state that this model is not

equally applicable to all the form of business. This is because practically it is not possible that

the cost and aspect of technology would remain same (SHROTRIYA, 2019). Likewise, the

concept that the company would have the same product mix would not be possible because no

company would make the production of only one kind of product. In the same way the aspect the

sales volume would not only have an impact towards the cost and sales revenue because there are

various other factors that may have an impact towards the sales revenue and may impact the

expenses of the company. the assumption that inventory would remain same as per the BEP

model would also not be practically implacable because the value of inventory would remain

fluctuating and not need to be constant throughout the year.

As every business would run and operate in a varied form that would be right to state that

the company’s BEP would not be remain same and its assumption would not remain equally

applicable to every kind of business (Lohmann, 2020). This is because every business has

different working and operational procedure which clearly state that the assumption of the BEP

will not be equally applicable towards every company.

The breakeven analysis refers to that point of sales and aspect within the business that

would assist eth business in terms of analysing the situation of no profit and no loss (Tannen,

2020). This means that it is the unit or the value which if earned by company then it will fall in

the category of no profit and loss.

There are certain assumption which would be made implied in the BEP analysis. These

would include: the fixed cost would remain same with all the level of output, the all other cost

would be counted as either the fixed or the variable, the sales volume is the only aspect that

would affect the cost and sales revenue, other factors including the production, technology,

efficiency would remain unchanged, the business would be considered with the constant product

mix which shows that the company will produce only one type of the product, the sales price

remain constant throughout the level of output, constant inventory at the end of accounting

period and various other (Kostjukova, 2018).

With the persistence of these assumption it would be right to state that this model is not

equally applicable to all the form of business. This is because practically it is not possible that

the cost and aspect of technology would remain same (SHROTRIYA, 2019). Likewise, the

concept that the company would have the same product mix would not be possible because no

company would make the production of only one kind of product. In the same way the aspect the

sales volume would not only have an impact towards the cost and sales revenue because there are

various other factors that may have an impact towards the sales revenue and may impact the

expenses of the company. the assumption that inventory would remain same as per the BEP

model would also not be practically implacable because the value of inventory would remain

fluctuating and not need to be constant throughout the year.

As every business would run and operate in a varied form that would be right to state that

the company’s BEP would not be remain same and its assumption would not remain equally

applicable to every kind of business (Lohmann, 2020). This is because every business has

different working and operational procedure which clearly state that the assumption of the BEP

will not be equally applicable towards every company.

QUESTION 3

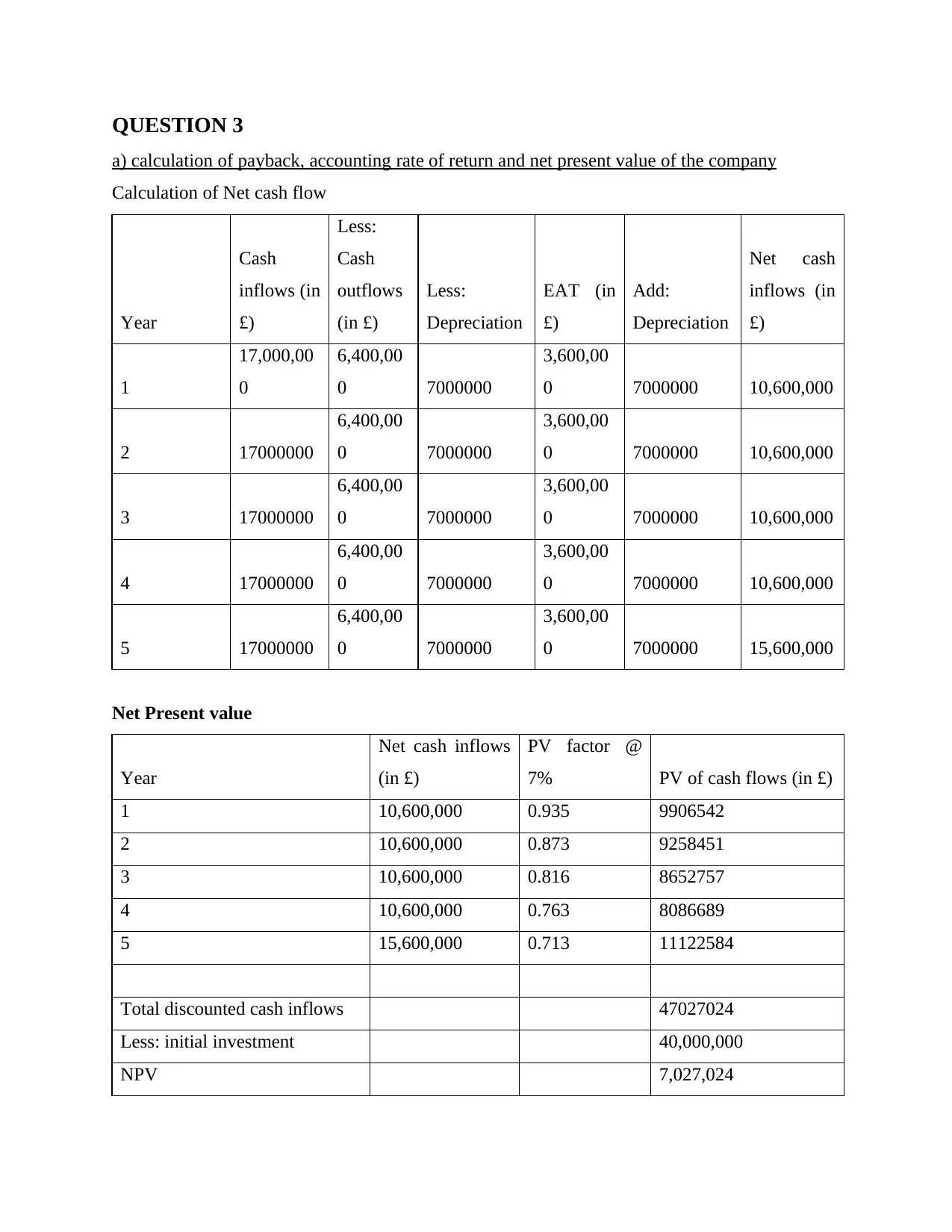

a) calculation of payback, accounting rate of return and net present value of the company

Calculation of Net cash flow

Year

Cash

inflows (in

£)

Less:

Cash

outflows

(in £)

Less:

Depreciation

EAT (in

£)

Add:

Depreciation

Net cash

inflows (in

£)

1

17,000,00

0

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

2 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

3 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

4 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

5 17000000

6,400,00

0 7000000

3,600,00

0 7000000 15,600,000

Net Present value

Year

Net cash inflows

(in £)

PV factor @

7% PV of cash flows (in £)

1 10,600,000 0.935 9906542

2 10,600,000 0.873 9258451

3 10,600,000 0.816 8652757

4 10,600,000 0.763 8086689

5 15,600,000 0.713 11122584

Total discounted cash inflows 47027024

Less: initial investment 40,000,000

NPV 7,027,024

a) calculation of payback, accounting rate of return and net present value of the company

Calculation of Net cash flow

Year

Cash

inflows (in

£)

Less:

Cash

outflows

(in £)

Less:

Depreciation

EAT (in

£)

Add:

Depreciation

Net cash

inflows (in

£)

1

17,000,00

0

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

2 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

3 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

4 17000000

6,400,00

0 7000000

3,600,00

0 7000000 10,600,000

5 17000000

6,400,00

0 7000000

3,600,00

0 7000000 15,600,000

Net Present value

Year

Net cash inflows

(in £)

PV factor @

7% PV of cash flows (in £)

1 10,600,000 0.935 9906542

2 10,600,000 0.873 9258451

3 10,600,000 0.816 8652757

4 10,600,000 0.763 8086689

5 15,600,000 0.713 11122584

Total discounted cash inflows 47027024

Less: initial investment 40,000,000

NPV 7,027,024

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

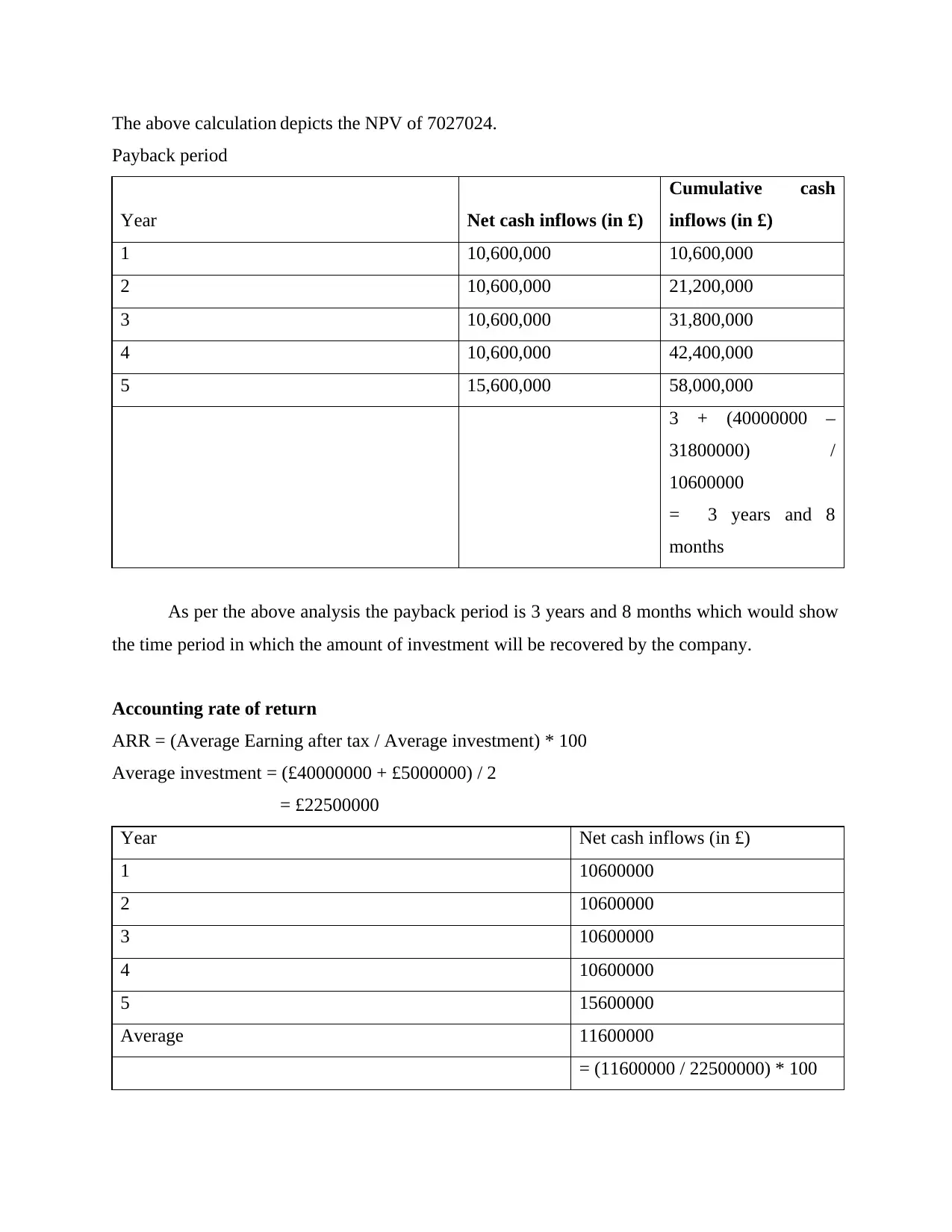

The above calculation depicts the NPV of 7027024.

Payback period

Year Net cash inflows (in £)

Cumulative cash

inflows (in £)

1 10,600,000 10,600,000

2 10,600,000 21,200,000

3 10,600,000 31,800,000

4 10,600,000 42,400,000

5 15,600,000 58,000,000

3 + (40000000 –

31800000) /

10600000

= 3 years and 8

months

As per the above analysis the payback period is 3 years and 8 months which would show

the time period in which the amount of investment will be recovered by the company.

Accounting rate of return

ARR = (Average Earning after tax / Average investment) * 100

Average investment = (£40000000 + £5000000) / 2

= £22500000

Year Net cash inflows (in £)

1 10600000

2 10600000

3 10600000

4 10600000

5 15600000

Average 11600000

= (11600000 / 22500000) * 100

Payback period

Year Net cash inflows (in £)

Cumulative cash

inflows (in £)

1 10,600,000 10,600,000

2 10,600,000 21,200,000

3 10,600,000 31,800,000

4 10,600,000 42,400,000

5 15,600,000 58,000,000

3 + (40000000 –

31800000) /

10600000

= 3 years and 8

months

As per the above analysis the payback period is 3 years and 8 months which would show

the time period in which the amount of investment will be recovered by the company.

Accounting rate of return

ARR = (Average Earning after tax / Average investment) * 100

Average investment = (£40000000 + £5000000) / 2

= £22500000

Year Net cash inflows (in £)

1 10600000

2 10600000

3 10600000

4 10600000

5 15600000

Average 11600000

= (11600000 / 22500000) * 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

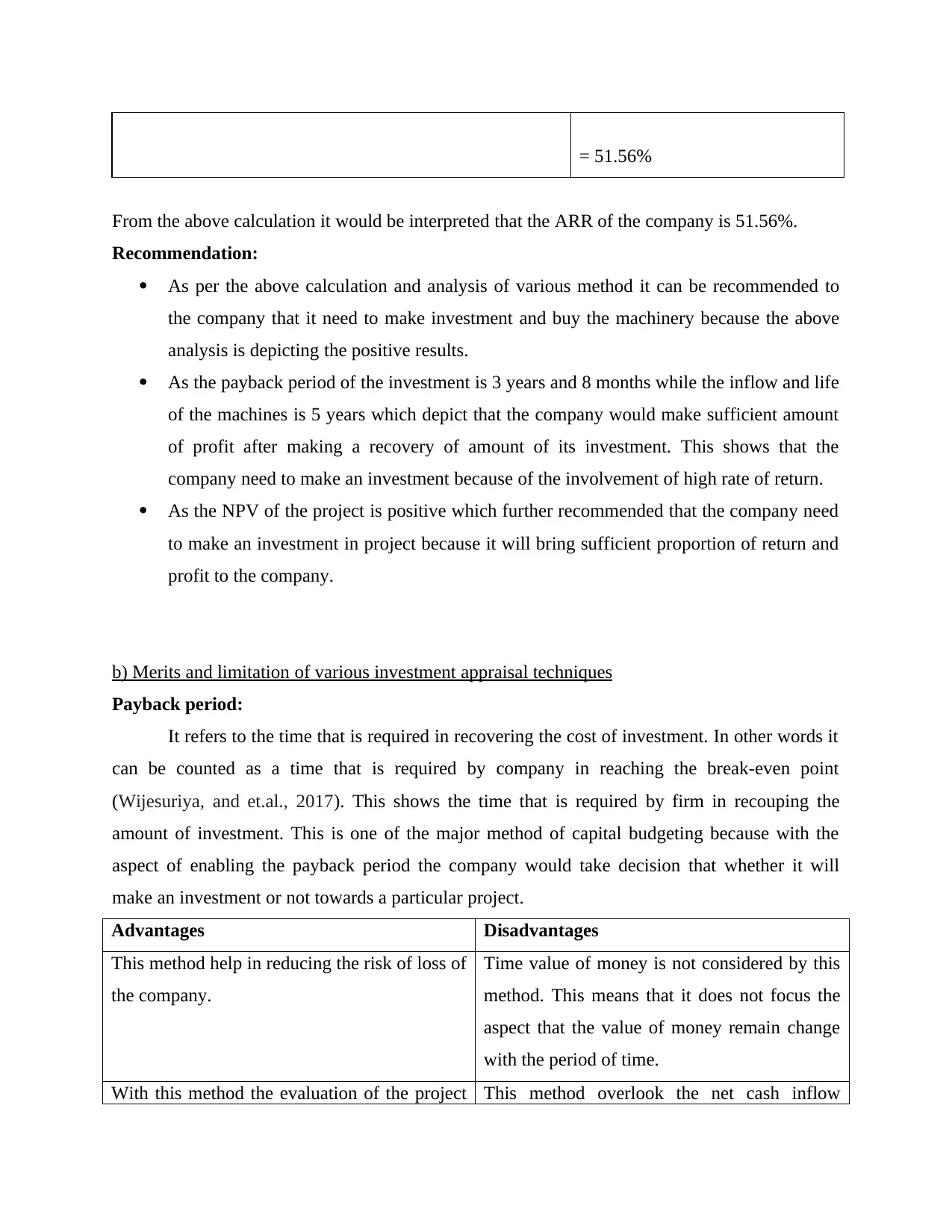

= 51.56%

From the above calculation it would be interpreted that the ARR of the company is 51.56%.

Recommendation:

As per the above calculation and analysis of various method it can be recommended to

the company that it need to make investment and buy the machinery because the above

analysis is depicting the positive results.

As the payback period of the investment is 3 years and 8 months while the inflow and life

of the machines is 5 years which depict that the company would make sufficient amount

of profit after making a recovery of amount of its investment. This shows that the

company need to make an investment because of the involvement of high rate of return.

As the NPV of the project is positive which further recommended that the company need

to make an investment in project because it will bring sufficient proportion of return and

profit to the company.

b) Merits and limitation of various investment appraisal techniques

Payback period:

It refers to the time that is required in recovering the cost of investment. In other words it

can be counted as a time that is required by company in reaching the break-even point

(Wijesuriya, and et.al., 2017). This shows the time that is required by firm in recouping the

amount of investment. This is one of the major method of capital budgeting because with the

aspect of enabling the payback period the company would take decision that whether it will

make an investment or not towards a particular project.

Advantages Disadvantages

This method help in reducing the risk of loss of

the company.

Time value of money is not considered by this

method. This means that it does not focus the

aspect that the value of money remain change

with the period of time.

With this method the evaluation of the project This method overlook the net cash inflow

From the above calculation it would be interpreted that the ARR of the company is 51.56%.

Recommendation:

As per the above calculation and analysis of various method it can be recommended to

the company that it need to make investment and buy the machinery because the above

analysis is depicting the positive results.

As the payback period of the investment is 3 years and 8 months while the inflow and life

of the machines is 5 years which depict that the company would make sufficient amount

of profit after making a recovery of amount of its investment. This shows that the

company need to make an investment because of the involvement of high rate of return.

As the NPV of the project is positive which further recommended that the company need

to make an investment in project because it will bring sufficient proportion of return and

profit to the company.

b) Merits and limitation of various investment appraisal techniques

Payback period:

It refers to the time that is required in recovering the cost of investment. In other words it

can be counted as a time that is required by company in reaching the break-even point

(Wijesuriya, and et.al., 2017). This shows the time that is required by firm in recouping the

amount of investment. This is one of the major method of capital budgeting because with the

aspect of enabling the payback period the company would take decision that whether it will

make an investment or not towards a particular project.

Advantages Disadvantages

This method help in reducing the risk of loss of

the company.

Time value of money is not considered by this

method. This means that it does not focus the

aspect that the value of money remain change

with the period of time.

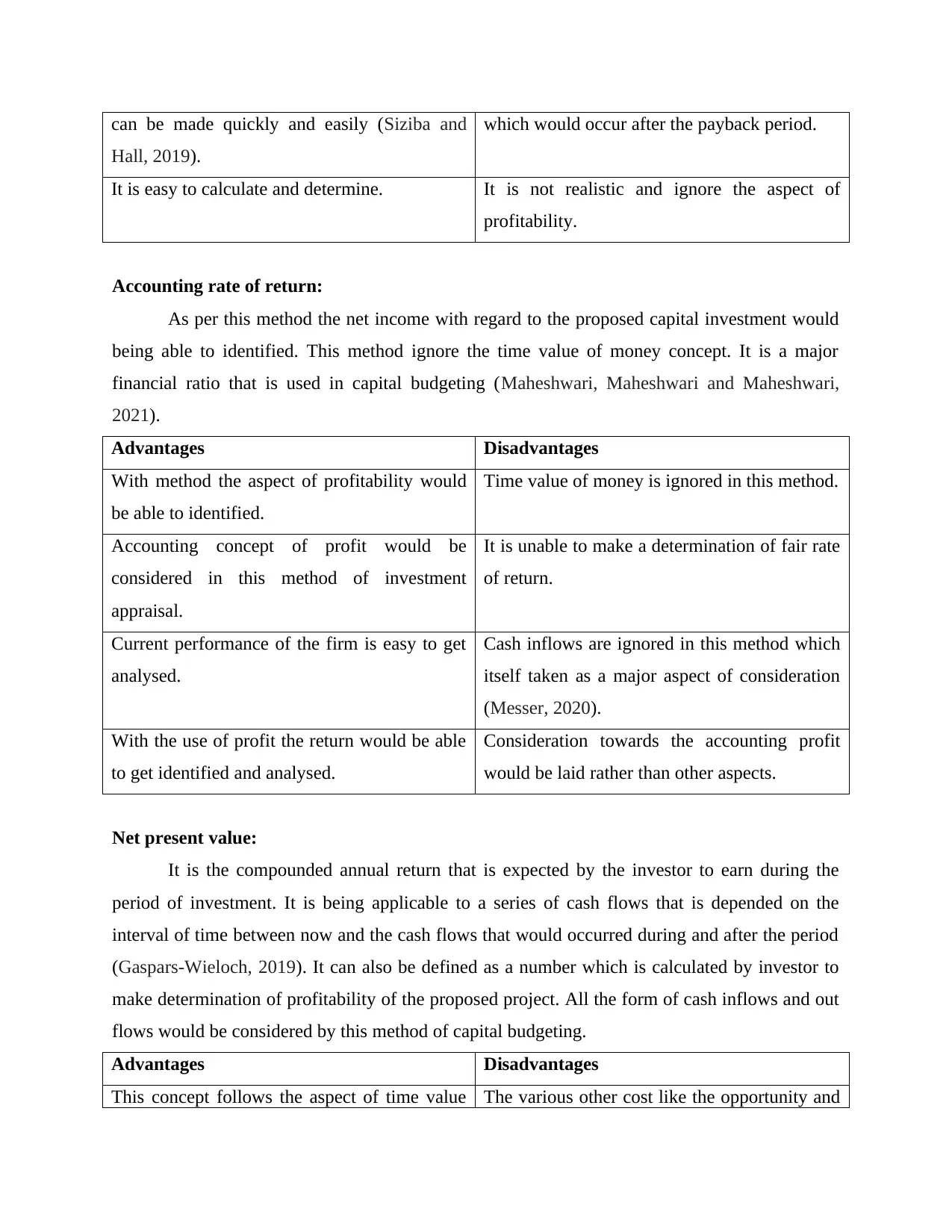

With this method the evaluation of the project This method overlook the net cash inflow

can be made quickly and easily (Siziba and

Hall, 2019).

which would occur after the payback period.

It is easy to calculate and determine. It is not realistic and ignore the aspect of

profitability.

Accounting rate of return:

As per this method the net income with regard to the proposed capital investment would

being able to identified. This method ignore the time value of money concept. It is a major

financial ratio that is used in capital budgeting (Maheshwari, Maheshwari and Maheshwari,

2021).

Advantages Disadvantages

With method the aspect of profitability would

be able to identified.

Time value of money is ignored in this method.

Accounting concept of profit would be

considered in this method of investment

appraisal.

It is unable to make a determination of fair rate

of return.

Current performance of the firm is easy to get

analysed.

Cash inflows are ignored in this method which

itself taken as a major aspect of consideration

(Messer, 2020).

With the use of profit the return would be able

to get identified and analysed.

Consideration towards the accounting profit

would be laid rather than other aspects.

Net present value:

It is the compounded annual return that is expected by the investor to earn during the

period of investment. It is being applicable to a series of cash flows that is depended on the

interval of time between now and the cash flows that would occurred during and after the period

(Gaspars-Wieloch, 2019). It can also be defined as a number which is calculated by investor to

make determination of profitability of the proposed project. All the form of cash inflows and out

flows would be considered by this method of capital budgeting.

Advantages Disadvantages

This concept follows the aspect of time value The various other cost like the opportunity and

Hall, 2019).

which would occur after the payback period.

It is easy to calculate and determine. It is not realistic and ignore the aspect of

profitability.

Accounting rate of return:

As per this method the net income with regard to the proposed capital investment would

being able to identified. This method ignore the time value of money concept. It is a major

financial ratio that is used in capital budgeting (Maheshwari, Maheshwari and Maheshwari,

2021).

Advantages Disadvantages

With method the aspect of profitability would

be able to identified.

Time value of money is ignored in this method.

Accounting concept of profit would be

considered in this method of investment

appraisal.

It is unable to make a determination of fair rate

of return.

Current performance of the firm is easy to get

analysed.

Cash inflows are ignored in this method which

itself taken as a major aspect of consideration

(Messer, 2020).

With the use of profit the return would be able

to get identified and analysed.

Consideration towards the accounting profit

would be laid rather than other aspects.

Net present value:

It is the compounded annual return that is expected by the investor to earn during the

period of investment. It is being applicable to a series of cash flows that is depended on the

interval of time between now and the cash flows that would occurred during and after the period

(Gaspars-Wieloch, 2019). It can also be defined as a number which is calculated by investor to

make determination of profitability of the proposed project. All the form of cash inflows and out

flows would be considered by this method of capital budgeting.

Advantages Disadvantages

This concept follows the aspect of time value The various other cost like the opportunity and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.