Enhancing Corporate Performance through Effective Financial Management

VerifiedAdded on 2020/10/04

|10

|2522

|43

AI Summary

The report examines the financial performance of an organization by analyzing its financial statements in comparison with industry averages. Key areas include revenue, expenses, profit margins, and debt levels, focusing on deviations from standard practices. The analysis highlights strengths such as stable cash flows and identifies weaknesses like high operating costs. Management strategies are critiqued for their impact on efficiency and profitability, emphasizing the need for optimized financial management tools to enhance future performance. Recommendations include reducing debt and improving cost control measures.

Managing Financial

Resources

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK1 ...........................................................................................................................................1

(a) Difference between financial accounts and management accounts..................................1

b). Identify and make analyse of vital objectives of using financial statements....................3

Resources

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK1 ...........................................................................................................................................1

(a) Difference between financial accounts and management accounts..................................1

b). Identify and make analyse of vital objectives of using financial statements....................3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c). Various group of stakeholders and evaluating their vital data..........................................4

TASK 2............................................................................................................................................5

a): Calculation of various ratios.............................................................................................5

b). Compare overall performance and current position:.........................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

TASK 2............................................................................................................................................5

a): Calculation of various ratios.............................................................................................5

b). Compare overall performance and current position:.........................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Finance is the most important aspect which helps the organisation to attain success. It

Provides the opportunity to the manager is to try innovations in business functions which helps

in development of the efficiency of employees (Ding, 2010). Lacks of funds affects their

working capacity which also impacts their decision making. It helps the organisation to attain

sustainability in their operations. Stratford Yachts Ltd. Provides their services in UK.

In the present report explain about, difference between financial and management

accounts, identification of the purpose of different financial statements which are used in profit

and non profit organisation and identification of the different types of shareholders and

evaluation of the information which is needed for decision making. Also, calculation of different

types of ratios and preparation of report about organisational performance in terms of

profitability and liquidity.

TASK1

(a) Difference between financial accounts and management accounts

Management accounting is the process which includes use of different accounting

methods which helps in effective management of different functions of organisation. On the

basis of such informations reports are prepared which is used by the internal parties of

organisation to improve their decision making. It provides the opportunity regarding

development of the understanding between the different departments and employees. This will

improves the efficiency of manager to formulate different policies which provides direction

regarding development of their existing skills. It is one of the broad concept which includes the

provision of both cost and management accounting. This concept is different from financial

accounting. It includes the preparation of financial accounts which is used by the external parties

to take better investment related decisions (Goldman, 2010).

Stratford Yachts Ltd. Faces many issues regarding earning of large number of revenues.

They feel need to adopt effective management accounting systems which helps in proper

management of finance. It helps in effective management of turnover and overall performance. It

is required by Stratford Yachts Ltd. Because they faces many issues in their product lines.

Difference between management and financial accounting

Basis Financial accounting Management accounting

1

Finance is the most important aspect which helps the organisation to attain success. It

Provides the opportunity to the manager is to try innovations in business functions which helps

in development of the efficiency of employees (Ding, 2010). Lacks of funds affects their

working capacity which also impacts their decision making. It helps the organisation to attain

sustainability in their operations. Stratford Yachts Ltd. Provides their services in UK.

In the present report explain about, difference between financial and management

accounts, identification of the purpose of different financial statements which are used in profit

and non profit organisation and identification of the different types of shareholders and

evaluation of the information which is needed for decision making. Also, calculation of different

types of ratios and preparation of report about organisational performance in terms of

profitability and liquidity.

TASK1

(a) Difference between financial accounts and management accounts

Management accounting is the process which includes use of different accounting

methods which helps in effective management of different functions of organisation. On the

basis of such informations reports are prepared which is used by the internal parties of

organisation to improve their decision making. It provides the opportunity regarding

development of the understanding between the different departments and employees. This will

improves the efficiency of manager to formulate different policies which provides direction

regarding development of their existing skills. It is one of the broad concept which includes the

provision of both cost and management accounting. This concept is different from financial

accounting. It includes the preparation of financial accounts which is used by the external parties

to take better investment related decisions (Goldman, 2010).

Stratford Yachts Ltd. Faces many issues regarding earning of large number of revenues.

They feel need to adopt effective management accounting systems which helps in proper

management of finance. It helps in effective management of turnover and overall performance. It

is required by Stratford Yachts Ltd. Because they faces many issues in their product lines.

Difference between management and financial accounting

Basis Financial accounting Management accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

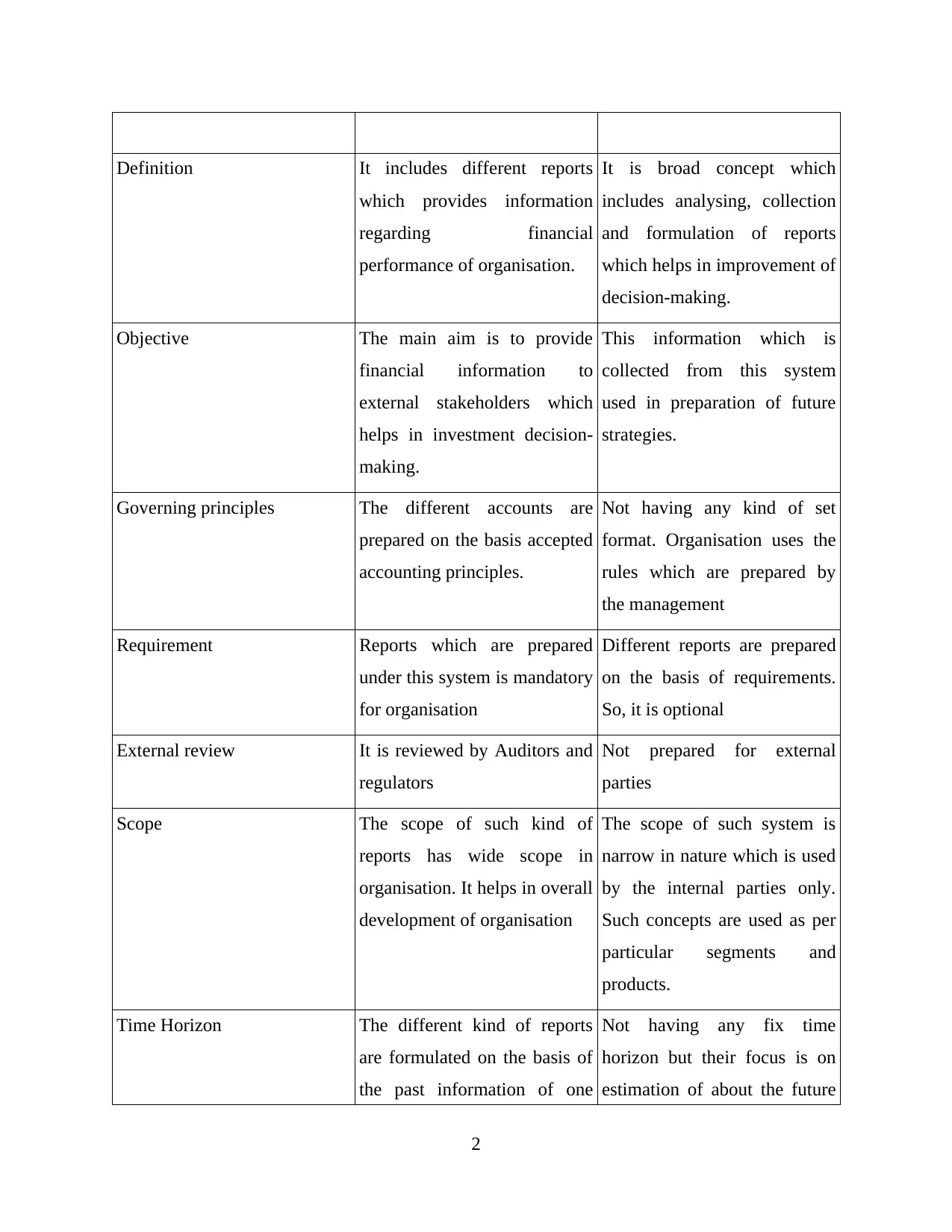

Definition It includes different reports

which provides information

regarding financial

performance of organisation.

It is broad concept which

includes analysing, collection

and formulation of reports

which helps in improvement of

decision-making.

Objective The main aim is to provide

financial information to

external stakeholders which

helps in investment decision-

making.

This information which is

collected from this system

used in preparation of future

strategies.

Governing principles The different accounts are

prepared on the basis accepted

accounting principles.

Not having any kind of set

format. Organisation uses the

rules which are prepared by

the management

Requirement Reports which are prepared

under this system is mandatory

for organisation

Different reports are prepared

on the basis of requirements.

So, it is optional

External review It is reviewed by Auditors and

regulators

Not prepared for external

parties

Scope The scope of such kind of

reports has wide scope in

organisation. It helps in overall

development of organisation

The scope of such system is

narrow in nature which is used

by the internal parties only.

Such concepts are used as per

particular segments and

products.

Time Horizon The different kind of reports

are formulated on the basis of

the past information of one

Not having any fix time

horizon but their focus is on

estimation of about the future

2

which provides information

regarding financial

performance of organisation.

It is broad concept which

includes analysing, collection

and formulation of reports

which helps in improvement of

decision-making.

Objective The main aim is to provide

financial information to

external stakeholders which

helps in investment decision-

making.

This information which is

collected from this system

used in preparation of future

strategies.

Governing principles The different accounts are

prepared on the basis accepted

accounting principles.

Not having any kind of set

format. Organisation uses the

rules which are prepared by

the management

Requirement Reports which are prepared

under this system is mandatory

for organisation

Different reports are prepared

on the basis of requirements.

So, it is optional

External review It is reviewed by Auditors and

regulators

Not prepared for external

parties

Scope The scope of such kind of

reports has wide scope in

organisation. It helps in overall

development of organisation

The scope of such system is

narrow in nature which is used

by the internal parties only.

Such concepts are used as per

particular segments and

products.

Time Horizon The different kind of reports

are formulated on the basis of

the past information of one

Not having any fix time

horizon but their focus is on

estimation of about the future

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial year. (Jackie, 2012) period of time.

b). Identify and make analyse of vital objectives of using financial statements

Financial statements are important for every kind of organisation irrespective of their

nature. Financial statements includes the preparation of different kind of reports like profit and

loss account, balance sheet, cash flow statements etc. It provides the opportunity to the

management of both profit and non profit organisation is to interpret important information

which helps to draw important conclusions (Chartier, 2014). The main aim of profit organisation

is to work for earning large number of profits. In this regard, manager of organisation need to

optimally their resources. On other hand, non profit organisation working for the benefit of

society not for the purpose of earning large number of profits.

All the reports have their different objectives. Profit and loss account used to ascertain

profitability, balance sheet is used to gather the information about total number of assets and

liabilities and cash flow statements provides about inflow and outflow of cash. It helps in

effective management of cash requirements in organisation. There are many similarities and

differences in profit and non profit which are defined below:

Basis Profit organisation Non-profit organisation

Meaning Main objective is to maximise

profits

Provides support to society for

development

Form of organisation Sole traders, partnership Club, charitable trust, public

hospitals

Sources of income They earn profits from sell of

their different products

Raise income from donations,

subscriptions, fees

Different kind of reports formulate by both organisations are mentioned below:

For-profit Non-profit

Balance sheet Statement of financial position

3

b). Identify and make analyse of vital objectives of using financial statements

Financial statements are important for every kind of organisation irrespective of their

nature. Financial statements includes the preparation of different kind of reports like profit and

loss account, balance sheet, cash flow statements etc. It provides the opportunity to the

management of both profit and non profit organisation is to interpret important information

which helps to draw important conclusions (Chartier, 2014). The main aim of profit organisation

is to work for earning large number of profits. In this regard, manager of organisation need to

optimally their resources. On other hand, non profit organisation working for the benefit of

society not for the purpose of earning large number of profits.

All the reports have their different objectives. Profit and loss account used to ascertain

profitability, balance sheet is used to gather the information about total number of assets and

liabilities and cash flow statements provides about inflow and outflow of cash. It helps in

effective management of cash requirements in organisation. There are many similarities and

differences in profit and non profit which are defined below:

Basis Profit organisation Non-profit organisation

Meaning Main objective is to maximise

profits

Provides support to society for

development

Form of organisation Sole traders, partnership Club, charitable trust, public

hospitals

Sources of income They earn profits from sell of

their different products

Raise income from donations,

subscriptions, fees

Different kind of reports formulate by both organisations are mentioned below:

For-profit Non-profit

Balance sheet Statement of financial position

3

Income statements

cash-flow statements

cash floe report

activity detail summary

c). Various group of stakeholders and evaluating their vital data

The management of “Stratford Yachts Ltd” need to analyse their different financial

reports which helps in ascertainment of their current financial position. They have the obligation

to identifies their different internal and external stakeholders which helps to earn maximum

profit. Management need to identifies the interest of each and every stakeholder in organisation

to take effective decisions.

Stakeholders

These are considered as important personalities which helps to increase the image of

organisation through effective guidance in decision-making process. Stakeholder are classified

into two categories primary and secondary which are mentioned below:

Primary stakeholders

It includes all such individuals which have direct interest and related to organisation.

They plays an crucial part in decision making activities in Stratford Yachts Ltd.

Employees: These are assets of organisation. To improve profits need to understand their

issues. It helps in removal of obligations which in improvement of overall performance.

Partners: These includes person which have share in the the net profit of organisation.

They work to improve image of organisation (Hunter, 2016).

Customers: One of the important stakeholder which helps the organisation to attain good

position in market. Fulfilment of their different requirement helps in attain their trust

which contributes to make long term bond.

Secondary Stakeholders: This means to the outside stakeholders that understand that

organisation identifies that they are required to have specific stake in them and take care of

outcome. They are various efficient parties which are linked with secondary stakeholders. Few

of them are explained hereunder:

4

cash-flow statements

cash floe report

activity detail summary

c). Various group of stakeholders and evaluating their vital data

The management of “Stratford Yachts Ltd” need to analyse their different financial

reports which helps in ascertainment of their current financial position. They have the obligation

to identifies their different internal and external stakeholders which helps to earn maximum

profit. Management need to identifies the interest of each and every stakeholder in organisation

to take effective decisions.

Stakeholders

These are considered as important personalities which helps to increase the image of

organisation through effective guidance in decision-making process. Stakeholder are classified

into two categories primary and secondary which are mentioned below:

Primary stakeholders

It includes all such individuals which have direct interest and related to organisation.

They plays an crucial part in decision making activities in Stratford Yachts Ltd.

Employees: These are assets of organisation. To improve profits need to understand their

issues. It helps in removal of obligations which in improvement of overall performance.

Partners: These includes person which have share in the the net profit of organisation.

They work to improve image of organisation (Hunter, 2016).

Customers: One of the important stakeholder which helps the organisation to attain good

position in market. Fulfilment of their different requirement helps in attain their trust

which contributes to make long term bond.

Secondary Stakeholders: This means to the outside stakeholders that understand that

organisation identifies that they are required to have specific stake in them and take care of

outcome. They are various efficient parties which are linked with secondary stakeholders. Few

of them are explained hereunder:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Competitors: They are the one who are accountable to form an efficient impacts on the

operation of any organisation. Other than performing main role which are required to be

the essential part of secondary stakeholders.

Government: In request to influence essential rule and control each business concern

need to take earlier permission from local experts (Genet and et. al., 2011). At that point

after they can work their day by day activities in more viable way.

Media: It suggest as urgent individuals from organization for making advancement of

their items and administrations in different parts of the country. They are displayed from

start of any new pursuit.

Banks: As a secondary stakeholders, there essential part is give important sum fund to

oversee and arrange their regular business exchanges in more precisely.

TASK 2

a): Calculation of various ratios

For resolving the solution, there is a need to compute specific ratios which could aid in

interpreting limited outcomes for forming comparison to Industry average (Kane, 2011). There

are different ratios which are connected with explaining profitability of the organisation in fast

manner. Few of them are discoursed underneath:

Ratio Formula 2015 2016

ROCE

Operating profit / capital employed

*100

27.88461538

46

22.4783861

671

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets

1.698717948

7

1.90201729

11

Net profit margin Profit after tax / Net sales *100

16.41509433

96

11.8181818

182

Current ratio Current assets / current liabilities

1.224358974

4

1.31052631

58

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities

0.871794871

8

0.99473684

21

Debtors collection period Trade creditor / sales *365 90.90566037 101.757575

5

operation of any organisation. Other than performing main role which are required to be

the essential part of secondary stakeholders.

Government: In request to influence essential rule and control each business concern

need to take earlier permission from local experts (Genet and et. al., 2011). At that point

after they can work their day by day activities in more viable way.

Media: It suggest as urgent individuals from organization for making advancement of

their items and administrations in different parts of the country. They are displayed from

start of any new pursuit.

Banks: As a secondary stakeholders, there essential part is give important sum fund to

oversee and arrange their regular business exchanges in more precisely.

TASK 2

a): Calculation of various ratios

For resolving the solution, there is a need to compute specific ratios which could aid in

interpreting limited outcomes for forming comparison to Industry average (Kane, 2011). There

are different ratios which are connected with explaining profitability of the organisation in fast

manner. Few of them are discoursed underneath:

Ratio Formula 2015 2016

ROCE

Operating profit / capital employed

*100

27.88461538

46

22.4783861

671

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets

1.698717948

7

1.90201729

11

Net profit margin Profit after tax / Net sales *100

16.41509433

96

11.8181818

182

Current ratio Current assets / current liabilities

1.224358974

4

1.31052631

58

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities

0.871794871

8

0.99473684

21

Debtors collection period Trade creditor / sales *365 90.90566037 101.757575

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

74 7576

Gearing ratio

Long term liabilities/ Capital

employed *100

70.83333333

33

63.6887608

069

Labour cost as % of sales Total labour/ sales*100

18.49056603

77

18.9393939

394

Operating costs as % of sales Operating cost/ total sales*100

83.58490566

04

88.1818181

818

Distribution costs as % of sales Distribution cost/ Total sales*100

9.245283018

9

9.09090909

09

Administrative costs as % of

sales

Administrative cost / Total

sales*100

4.150943396

2

4.09090909

09

b). Compare overall performance and current position:

This report is based for evaluating the financial position of the organisation. At the time

of evaluating financial condition, this is huge to use an efficient formula which could help out in

more effective understanding of positive outcomes (Kabra, Ramesh and Arshinder, 2015). After

forming an adequate assessment of diverse ratios, this can be said that performance of “Stratford

Yacths Ltd” is highly positive in 2016 as compare to 2015. There are specific varying which is

being overviewed in overall measurement of specific ratios. If owners could overviewed in order

to net profits margin which could assess that total gain which is higher in previous year with

16% which had lead to lower to 11%. this could be mostly form affect on developing and

reputation of “Stratford Yatch Ltd”. Account receivable period set up from industry point of time

which is forming optimum time to generate their total amounts. Although, liquidity position of

the organisation is rendering particular information about total assets as they are gaining 1.22

and 1.31 within the relevant time frame. Liquid ratio is close to their perfect ratio which is 1:1.

In addition to this, total labour cost will be 18% in both year. In addition to this, operating

costs for the organisation out of total sales in enhanced from previous from previous year as

88%. Distribution and selling costs which are ordinary which means that they are investment

same amount on these expenses. In addition to this, management costs are likewise higher more

same along with 4% out of total sales during those two years (Singer and et. al., 2011). The

entire performance of a company is having higher effective results for enhancing optimum

6

Gearing ratio

Long term liabilities/ Capital

employed *100

70.83333333

33

63.6887608

069

Labour cost as % of sales Total labour/ sales*100

18.49056603

77

18.9393939

394

Operating costs as % of sales Operating cost/ total sales*100

83.58490566

04

88.1818181

818

Distribution costs as % of sales Distribution cost/ Total sales*100

9.245283018

9

9.09090909

09

Administrative costs as % of

sales

Administrative cost / Total

sales*100

4.150943396

2

4.09090909

09

b). Compare overall performance and current position:

This report is based for evaluating the financial position of the organisation. At the time

of evaluating financial condition, this is huge to use an efficient formula which could help out in

more effective understanding of positive outcomes (Kabra, Ramesh and Arshinder, 2015). After

forming an adequate assessment of diverse ratios, this can be said that performance of “Stratford

Yacths Ltd” is highly positive in 2016 as compare to 2015. There are specific varying which is

being overviewed in overall measurement of specific ratios. If owners could overviewed in order

to net profits margin which could assess that total gain which is higher in previous year with

16% which had lead to lower to 11%. this could be mostly form affect on developing and

reputation of “Stratford Yatch Ltd”. Account receivable period set up from industry point of time

which is forming optimum time to generate their total amounts. Although, liquidity position of

the organisation is rendering particular information about total assets as they are gaining 1.22

and 1.31 within the relevant time frame. Liquid ratio is close to their perfect ratio which is 1:1.

In addition to this, total labour cost will be 18% in both year. In addition to this, operating

costs for the organisation out of total sales in enhanced from previous from previous year as

88%. Distribution and selling costs which are ordinary which means that they are investment

same amount on these expenses. In addition to this, management costs are likewise higher more

same along with 4% out of total sales during those two years (Singer and et. al., 2011). The

entire performance of a company is having higher effective results for enhancing optimum

6

revenue in the near future. The total interest amount assessed from profits and loss statements as

which gearing ratios is lower from last year performances. The entire comparison emerged from

total industry average which is not emerged as much as efficient. They are below asking

standards which are being fixed by forming by taking entire average of the organisation.

CONCLUSION

From the above mentioned report, this can be said that the for managing finance, various

things are to be considered in each organisation. The results gathered out of the entire

performance of the cited organisation is evaluated in a most efficient manner. For this aim, they

are required to be effectively compare between financial management accounts. Henceforth,

actual deviation could be identified in a most effective manner. In addition to this, assessment is

produce precious data in order to assess the profits and non-profit firm in the financial

statements. The entire report helps in measuring particular ratios those are being usable in

incorporating among fix industry objectives. At the end, use of data for effective of financial

tools in relating to enhance better development and performance in forthcoming year.

7

which gearing ratios is lower from last year performances. The entire comparison emerged from

total industry average which is not emerged as much as efficient. They are below asking

standards which are being fixed by forming by taking entire average of the organisation.

CONCLUSION

From the above mentioned report, this can be said that the for managing finance, various

things are to be considered in each organisation. The results gathered out of the entire

performance of the cited organisation is evaluated in a most efficient manner. For this aim, they

are required to be effectively compare between financial management accounts. Henceforth,

actual deviation could be identified in a most effective manner. In addition to this, assessment is

produce precious data in order to assess the profits and non-profit firm in the financial

statements. The entire report helps in measuring particular ratios those are being usable in

incorporating among fix industry objectives. At the end, use of data for effective of financial

tools in relating to enhance better development and performance in forthcoming year.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Singer, S. J. and et. al., 2011. Defining and measuring integrated patient care: promoting the next

frontier in health care delivery. Medical Care Research and Review. 68(1). pp.112-127.

Genet, N. and et. al., 2011. Home care in Europe: a systematic literature review. BMC health

services research. 11(1). p.207.

Hunter, D. J., 2016. Desperately seeking solutions: rationing Health Care. Routledge.

Richard, A.A. and Shea, K., 2011. Delineation of self‐care and associated concepts.

Journal of Nursing Scholarship. 43(3). pp.255-264.

Chartier, Y. ed., 2014. Safe management of wastes from health-care activities. World Health

Organization.

Ding, Y., 2010. Study on the management of intellectual capital. International Journal of

business and Management. 5(2). p.213.

Goldman, C., 2010. Joint financing across health and social care: money matters, but outcomes

matter more. Journal of Integrated Care. 18(1). pp.3-10.

Kabra, G., Ramesh, A. and Arshinder, K., 2015. Identification and prioritization of coordination

barriers in humanitarian supply chain management. International Journal of Disaster

Risk Reduction. 13. pp.128-138

Online

Jackie, 2012. [Online]. Available through: <http://hoileongchan.blogspot.in/2012/09/the-

differences-between-financial.html>.

8

Books and Journals

Singer, S. J. and et. al., 2011. Defining and measuring integrated patient care: promoting the next

frontier in health care delivery. Medical Care Research and Review. 68(1). pp.112-127.

Genet, N. and et. al., 2011. Home care in Europe: a systematic literature review. BMC health

services research. 11(1). p.207.

Hunter, D. J., 2016. Desperately seeking solutions: rationing Health Care. Routledge.

Richard, A.A. and Shea, K., 2011. Delineation of self‐care and associated concepts.

Journal of Nursing Scholarship. 43(3). pp.255-264.

Chartier, Y. ed., 2014. Safe management of wastes from health-care activities. World Health

Organization.

Ding, Y., 2010. Study on the management of intellectual capital. International Journal of

business and Management. 5(2). p.213.

Goldman, C., 2010. Joint financing across health and social care: money matters, but outcomes

matter more. Journal of Integrated Care. 18(1). pp.3-10.

Kabra, G., Ramesh, A. and Arshinder, K., 2015. Identification and prioritization of coordination

barriers in humanitarian supply chain management. International Journal of Disaster

Risk Reduction. 13. pp.128-138

Online

Jackie, 2012. [Online]. Available through: <http://hoileongchan.blogspot.in/2012/09/the-

differences-between-financial.html>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.