Analysis of Toshiba's Accounting Scandal and Its Business Impact

VerifiedAdded on 2023/05/08

|14

|3316

|71

Report

AI Summary

This report provides a comprehensive review and analysis of the Toshiba accounting scandal. It begins with background information on Toshiba, including its history, key business areas, and organizational structure. The report then summarizes the key findings of the scandal, detailing the fraudulent accounting practices and their consequences. It explores relevant theoretical frameworks such as agency theory, stakeholder theory, and the fraud triangle to understand the causes and implications of the scandal. Furthermore, it examines the company's corporate culture, management practices, and the impact on its reputation and financial performance. The report also discusses potential future performance, challenges, and strategies for Toshiba to regain its competitive advantage and overcome the negative impact of the scandal. The report concludes with a summary of the main findings and the importance of ethical behavior and corporate governance for long-term business success.

"A load of tosh?" Toshiba's accounting scandal

Article Review

APRIL 3, 2023

Article Review

APRIL 3, 2023

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................2

SECTION 1.....................................................................................................................................2

SECTION 2:....................................................................................................................................3

SECTION 3.....................................................................................................................................4

SECTION 4.....................................................................................................................................4

SECTION 5.....................................................................................................................................7

REFERENCES................................................................................................................................9

APPENDICES...............................................................................................................................11

TIMELINE OF KEY EVENTS.................................................................................................11

TOSHIBA'S FINANCIAL STATEMENTS BEFORE AND AFTER THE ACCOUNTING

SCANDAL................................................................................................................................12

COMPARISON OF THE STOCK PRICES OF TOSHIBA CORPORATION AND ITS

COMPETITORS........................................................................................................................13

INTRODUCTION...........................................................................................................................2

SECTION 1.....................................................................................................................................2

SECTION 2:....................................................................................................................................3

SECTION 3.....................................................................................................................................4

SECTION 4.....................................................................................................................................4

SECTION 5.....................................................................................................................................7

REFERENCES................................................................................................................................9

APPENDICES...............................................................................................................................11

TIMELINE OF KEY EVENTS.................................................................................................11

TOSHIBA'S FINANCIAL STATEMENTS BEFORE AND AFTER THE ACCOUNTING

SCANDAL................................................................................................................................12

COMPARISON OF THE STOCK PRICES OF TOSHIBA CORPORATION AND ITS

COMPETITORS........................................................................................................................13

INTRODUCTION

This assignment aims to review and analyze the business case of the Toshiba accounting scandal,

which was widely reported in the media in 2015. The assignment is divided into five sections,

each focusing on a different aspect of the case.

In the first and second sections, we provide background information about Toshiba as a

company, including its history, key business areas, and organizational structure. In the third

section, we summarize the key findings of the Toshiba accounting scandal, including the factors

that contributed to the fraudulent accounting practices and the consequences for the company.

The fourth section of the assignment examines the theoretical frameworks, models, and concepts

that are relevant to the Toshiba case. We discuss how these theories can help us understand the

causes and consequences of the scandal, as well as the implications for corporate governance and

ethics.

In the fifth section, we offer our views and ideas about how Toshiba is or will be performing in

the future, considering the reputational damage caused by the accounting scandal and the

challenges the company faces in its key markets. We also discuss how the company can sustain

its competitive advantage over rivals and overcome any problems it may face in the future.

Finally, in the conclusion, we provide a summary of our main findings and conclusions about the

Toshiba accounting scandal, highlighting the importance of ethical behavior and corporate

governance for long-term business success. Overall, this assignment provides a comprehensive

review and analysis of a significant business case that has important implications for companies

and stakeholders around the world.

SECTION 1

Title: "A load of tosh?" Toshiba's accounting scandal

Author: Theo Leggett

URL: https://www.bbc.com/news/business-33514415

This assignment aims to review and analyze the business case of the Toshiba accounting scandal,

which was widely reported in the media in 2015. The assignment is divided into five sections,

each focusing on a different aspect of the case.

In the first and second sections, we provide background information about Toshiba as a

company, including its history, key business areas, and organizational structure. In the third

section, we summarize the key findings of the Toshiba accounting scandal, including the factors

that contributed to the fraudulent accounting practices and the consequences for the company.

The fourth section of the assignment examines the theoretical frameworks, models, and concepts

that are relevant to the Toshiba case. We discuss how these theories can help us understand the

causes and consequences of the scandal, as well as the implications for corporate governance and

ethics.

In the fifth section, we offer our views and ideas about how Toshiba is or will be performing in

the future, considering the reputational damage caused by the accounting scandal and the

challenges the company faces in its key markets. We also discuss how the company can sustain

its competitive advantage over rivals and overcome any problems it may face in the future.

Finally, in the conclusion, we provide a summary of our main findings and conclusions about the

Toshiba accounting scandal, highlighting the importance of ethical behavior and corporate

governance for long-term business success. Overall, this assignment provides a comprehensive

review and analysis of a significant business case that has important implications for companies

and stakeholders around the world.

SECTION 1

Title: "A load of tosh?" Toshiba's accounting scandal

Author: Theo Leggett

URL: https://www.bbc.com/news/business-33514415

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SECTION 2:

Toshiba Corporation is a Japanese multinational conglomerate that specializes in various fields

such as electronics, energy, and infrastructure. The company was founded in 1939 and has since

become one of Japan's leading manufacturers of electronic products, including laptops,

televisions, and home appliances. Toshiba also provides services related to power generation and

distribution, nuclear energy, and smart community solutions (BBC News, 2015).

In 2015, Toshiba was embroiled in a major accounting scandal that shook the company's

reputation and raised serious concerns about the Japanese corporate governance system. The

scandal centered around the overstatement of profits in its nuclear energy and semiconductor

businesses, which amounted to a total of $1.2 billion. The company's management had been

systematically inflating profits over a period of several years, hiding losses and manipulating

accounting data to meet ambitious financial target (Arora, 2017).

The scandal came to light when a whistleblower within Toshiba reported the irregularities to the

company's audit committee. This triggered an investigation, which revealed that the company

had been engaging in fraudulent accounting practices for over a decade. As a result, the

company's top executives were forced to resign, including the CEO, Hisao Tanaka, who took

responsibility for the scandal (BBC News, 2015).

The fallout from the scandal was severe, as Toshiba faced lawsuits, regulatory fines, and a loss

of investor confidence. The company's reputation was severely tarnished, and it struggled to

recover from the scandal. The incident also highlighted the systemic issues in Japan's corporate

governance system, which had long been criticized for lacking transparency and accountability

(Chugh, 2017).

In response to the scandal, Toshiba implemented a number of reforms aimed at improving

corporate governance and restoring investor confidence. These included the appointment of new

independent directors, the strengthening of internal controls and risk management, and the

establishment of a whistle-blower hotline (Conyon & He, 2017). However, the incident remains

a cautionary tale for companies around the world, illustrating the importance of ethical business

practices and the need for effective corporate governance mechanisms to prevent fraud and

misconduct (Fujimura, 2017).

Toshiba Corporation is a Japanese multinational conglomerate that specializes in various fields

such as electronics, energy, and infrastructure. The company was founded in 1939 and has since

become one of Japan's leading manufacturers of electronic products, including laptops,

televisions, and home appliances. Toshiba also provides services related to power generation and

distribution, nuclear energy, and smart community solutions (BBC News, 2015).

In 2015, Toshiba was embroiled in a major accounting scandal that shook the company's

reputation and raised serious concerns about the Japanese corporate governance system. The

scandal centered around the overstatement of profits in its nuclear energy and semiconductor

businesses, which amounted to a total of $1.2 billion. The company's management had been

systematically inflating profits over a period of several years, hiding losses and manipulating

accounting data to meet ambitious financial target (Arora, 2017).

The scandal came to light when a whistleblower within Toshiba reported the irregularities to the

company's audit committee. This triggered an investigation, which revealed that the company

had been engaging in fraudulent accounting practices for over a decade. As a result, the

company's top executives were forced to resign, including the CEO, Hisao Tanaka, who took

responsibility for the scandal (BBC News, 2015).

The fallout from the scandal was severe, as Toshiba faced lawsuits, regulatory fines, and a loss

of investor confidence. The company's reputation was severely tarnished, and it struggled to

recover from the scandal. The incident also highlighted the systemic issues in Japan's corporate

governance system, which had long been criticized for lacking transparency and accountability

(Chugh, 2017).

In response to the scandal, Toshiba implemented a number of reforms aimed at improving

corporate governance and restoring investor confidence. These included the appointment of new

independent directors, the strengthening of internal controls and risk management, and the

establishment of a whistle-blower hotline (Conyon & He, 2017). However, the incident remains

a cautionary tale for companies around the world, illustrating the importance of ethical business

practices and the need for effective corporate governance mechanisms to prevent fraud and

misconduct (Fujimura, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION 3

Toshiba Corporation, a Japanese multinational conglomerate, was involved in a major

accounting scandal in 2015. The scandal was related to the overstatement of profits in its nuclear

energy and semiconductor businesses, which amounted to a total of $1.2 billion. The company's

management had been systematically inflating profits over a period of several years, hiding

losses and manipulating accounting data to meet ambitious financial targets (BBC News, 2015).

The scandal came to light when a whistleblower reported the irregularities to the company's audit

committee. Toshiba subsequently launched an investigation that revealed the company had been

engaging in fraudulent accounting practices for over a decade. The company's top executives,

including the CEO, Hisao Tanaka, were forced to resign in the wake of the scandal.

The scandal had a severe impact on Toshiba's reputation, with lawsuits, regulatory fines, and a

loss of investor confidence. The incident highlighted the systemic issues in Japan's corporate

governance system, which had long been criticized for lacking transparency and accountability.

The article discusses the corporate culture and management practices that may have contributed

to the scandal, noting that Toshiba had prioritized short-term profits over long-term stability. The

article also highlights the implications of the scandal for Toshiba's reputation and the Japanese

corporate sector as a whole.

In response to the scandal, Toshiba implemented a number of reforms aimed at improving

corporate governance and restoring investor confidence. These included the appointment of new

independent directors, the strengthening of internal controls and risk management, and the

establishment of a whistle-blower hotline.

The scandal at Toshiba serves as a cautionary tale for companies around the world, illustrating

the importance of ethical business practices and the need for effective corporate governance

mechanisms to prevent fraud and misconduct.

SECTION 4

The case of Toshiba's accounting scandal highlights the importance of internal controls in

preventing fraud and misconduct. The scandal was largely attributed to weak internal controls

Toshiba Corporation, a Japanese multinational conglomerate, was involved in a major

accounting scandal in 2015. The scandal was related to the overstatement of profits in its nuclear

energy and semiconductor businesses, which amounted to a total of $1.2 billion. The company's

management had been systematically inflating profits over a period of several years, hiding

losses and manipulating accounting data to meet ambitious financial targets (BBC News, 2015).

The scandal came to light when a whistleblower reported the irregularities to the company's audit

committee. Toshiba subsequently launched an investigation that revealed the company had been

engaging in fraudulent accounting practices for over a decade. The company's top executives,

including the CEO, Hisao Tanaka, were forced to resign in the wake of the scandal.

The scandal had a severe impact on Toshiba's reputation, with lawsuits, regulatory fines, and a

loss of investor confidence. The incident highlighted the systemic issues in Japan's corporate

governance system, which had long been criticized for lacking transparency and accountability.

The article discusses the corporate culture and management practices that may have contributed

to the scandal, noting that Toshiba had prioritized short-term profits over long-term stability. The

article also highlights the implications of the scandal for Toshiba's reputation and the Japanese

corporate sector as a whole.

In response to the scandal, Toshiba implemented a number of reforms aimed at improving

corporate governance and restoring investor confidence. These included the appointment of new

independent directors, the strengthening of internal controls and risk management, and the

establishment of a whistle-blower hotline.

The scandal at Toshiba serves as a cautionary tale for companies around the world, illustrating

the importance of ethical business practices and the need for effective corporate governance

mechanisms to prevent fraud and misconduct.

SECTION 4

The case of Toshiba's accounting scandal highlights the importance of internal controls in

preventing fraud and misconduct. The scandal was largely attributed to weak internal controls

and inadequate oversight by the board of directors. The company's management was able to

manipulate accounting data due to a lack of effective checks and balances, and employees were

reportedly under intense pressure to achieve ambitious financial targets. The scandal underscores

the need for companies to establish strong internal controls and risk management systems, and to

regularly monitor and assess these systems to ensure their effectiveness (Conyon & He, 2017).

The Toshiba scandal highlights the importance of effective corporate governance mechanisms.

The company's management had been engaging in fraudulent accounting practices for over a

decade, which went undetected due to weak internal controls and a lack of oversight. In response

to the scandal, Toshiba implemented a number of reforms aimed at improving corporate

governance, including the appointment of new independent directors, the strengthening of

internal controls and risk management, and the establishment of a whistle-blower hotline

(Daisuke, 2015).

Agency theory is a model that explains the relationship between principals (such as shareholders)

and agents (such as managers) in a company. The theory assumes that the agents have their own

interests, which may differ from those of the principals, and that there is a risk of agency costs

arising from this misalignment of interests. Agency costs refer to the costs incurred by principals

in monitoring and controlling the agents to ensure that they act in the best interests of the

company. The Toshiba scandal can be analyzed through the lens of agency theory (Lee & Li,

2017). The company's management may have been incentivized to engage in fraudulent

accounting practices to meet ambitious financial targets, even if it meant hiding losses and

manipulating accounting data. This misalignment of interests between management and

shareholders led to agency costs, as shareholders suffered financial losses due to the scandal

(Fisman & Miguel, 2015).

Short-termism refers to a focus on short-term profits and performance at the expense of long-

term sustainability and value creation. Short-termism can lead to a number of negative

consequences, including a lack of investment in research and development, employee training,

and other activities that are important for long-term success. The Toshiba scandal can be seen as

a manifestation of short-termism. The company's management had been prioritizing short-term

profits over long-term stability, which led to fraudulent accounting practices and a loss of

investor confidence. The scandal highlights the need for companies to balance short-term and

manipulate accounting data due to a lack of effective checks and balances, and employees were

reportedly under intense pressure to achieve ambitious financial targets. The scandal underscores

the need for companies to establish strong internal controls and risk management systems, and to

regularly monitor and assess these systems to ensure their effectiveness (Conyon & He, 2017).

The Toshiba scandal highlights the importance of effective corporate governance mechanisms.

The company's management had been engaging in fraudulent accounting practices for over a

decade, which went undetected due to weak internal controls and a lack of oversight. In response

to the scandal, Toshiba implemented a number of reforms aimed at improving corporate

governance, including the appointment of new independent directors, the strengthening of

internal controls and risk management, and the establishment of a whistle-blower hotline

(Daisuke, 2015).

Agency theory is a model that explains the relationship between principals (such as shareholders)

and agents (such as managers) in a company. The theory assumes that the agents have their own

interests, which may differ from those of the principals, and that there is a risk of agency costs

arising from this misalignment of interests. Agency costs refer to the costs incurred by principals

in monitoring and controlling the agents to ensure that they act in the best interests of the

company. The Toshiba scandal can be analyzed through the lens of agency theory (Lee & Li,

2017). The company's management may have been incentivized to engage in fraudulent

accounting practices to meet ambitious financial targets, even if it meant hiding losses and

manipulating accounting data. This misalignment of interests between management and

shareholders led to agency costs, as shareholders suffered financial losses due to the scandal

(Fisman & Miguel, 2015).

Short-termism refers to a focus on short-term profits and performance at the expense of long-

term sustainability and value creation. Short-termism can lead to a number of negative

consequences, including a lack of investment in research and development, employee training,

and other activities that are important for long-term success. The Toshiba scandal can be seen as

a manifestation of short-termism. The company's management had been prioritizing short-term

profits over long-term stability, which led to fraudulent accounting practices and a loss of

investor confidence. The scandal highlights the need for companies to balance short-term and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

long-term objectives, and to prioritize sustainable value creation over short-term gains

(Fujimura, 2017).

Cultural theory refers to the idea that organizational culture can have a significant impact on a

company's operations and outcomes. Organizational culture encompasses the shared values,

beliefs, norms, and behaviors that shape the attitudes and actions of employees and managers. A

strong, positive organizational culture can lead to high employee morale, strong performance,

and a good reputation, while a negative culture can lead to low morale, poor performance, and

reputational damage (Daisuke, 2015). The Toshiba scandal can be seen as a failure of

organizational culture. The company's culture was criticized for prioritizing short-term profits

over long-term stability, and for lacking transparency and accountability. The scandal highlights

the importance of a strong, ethical culture that promotes transparency, accountability, and long-

term value creation (Shimizu & Hagiwara, 2016).

Stakeholder theory is a model that emphasizes the importance of considering the interests of all

stakeholders in a company, rather than just focusing on the interests of shareholders. According

to stakeholder theory, companies have a responsibility to balance the interests of stakeholders

such as employees, customers, suppliers, and the community, in addition to shareholders. The

Toshiba scandal highlights the importance of stakeholder theory. The company's management

had been prioritizing the interests of shareholders over those of other stakeholders, which led to

fraudulent accounting practices and reputational damage. The scandal shows the need for

companies to adopt a stakeholder-oriented approach that balances the interests of all stakeholders

(Fisman & Miguel, 2015).

Whistleblowing refers to the act of reporting unethical or illegal behavior within an organization.

Whistleblowers are typically employees or insiders who have knowledge of misconduct and

choose to report it, often at great personal risk. The Toshiba scandal shows the importance of

whistleblowing as a mechanism for detecting and preventing corporate misconduct (Osono &

Shimizu, 2016). After the scandal was exposed, it was revealed that several employees had

attempted to blow the whistle on the fraudulent accounting practices, but had been ignored or

retaliated against by management. The case highlights the need for companies to establish

effective whistleblower protections and reporting mechanisms (Daisuke, 2015).

(Fujimura, 2017).

Cultural theory refers to the idea that organizational culture can have a significant impact on a

company's operations and outcomes. Organizational culture encompasses the shared values,

beliefs, norms, and behaviors that shape the attitudes and actions of employees and managers. A

strong, positive organizational culture can lead to high employee morale, strong performance,

and a good reputation, while a negative culture can lead to low morale, poor performance, and

reputational damage (Daisuke, 2015). The Toshiba scandal can be seen as a failure of

organizational culture. The company's culture was criticized for prioritizing short-term profits

over long-term stability, and for lacking transparency and accountability. The scandal highlights

the importance of a strong, ethical culture that promotes transparency, accountability, and long-

term value creation (Shimizu & Hagiwara, 2016).

Stakeholder theory is a model that emphasizes the importance of considering the interests of all

stakeholders in a company, rather than just focusing on the interests of shareholders. According

to stakeholder theory, companies have a responsibility to balance the interests of stakeholders

such as employees, customers, suppliers, and the community, in addition to shareholders. The

Toshiba scandal highlights the importance of stakeholder theory. The company's management

had been prioritizing the interests of shareholders over those of other stakeholders, which led to

fraudulent accounting practices and reputational damage. The scandal shows the need for

companies to adopt a stakeholder-oriented approach that balances the interests of all stakeholders

(Fisman & Miguel, 2015).

Whistleblowing refers to the act of reporting unethical or illegal behavior within an organization.

Whistleblowers are typically employees or insiders who have knowledge of misconduct and

choose to report it, often at great personal risk. The Toshiba scandal shows the importance of

whistleblowing as a mechanism for detecting and preventing corporate misconduct (Osono &

Shimizu, 2016). After the scandal was exposed, it was revealed that several employees had

attempted to blow the whistle on the fraudulent accounting practices, but had been ignored or

retaliated against by management. The case highlights the need for companies to establish

effective whistleblower protections and reporting mechanisms (Daisuke, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The fraud triangle is a model that explains the three factors that are typically present in cases of

fraud: opportunity, rationalization, and pressure. Opportunity refers to the ability to commit

fraud, such as weak internal controls or a lack of oversight. Rationalization refers to the ability to

justify fraudulent behavior, such as a belief that it is necessary to meet financial targets

(Martynova & Renneboog, 2017). Pressure refers to the factors that create the need for fraud,

such as financial difficulties or the desire to maintain a certain lifestyle. The Toshiba scandal can

be analyzed through the lens of the fraud triangle. The company's management had the

opportunity to engage in fraudulent accounting practices due to weak internal controls and a lack

of oversight. They rationalized their behavior by believing it was necessary to meet ambitious

financial targets. And they felt pressure to maintain the appearance of financial stability, even if

it meant hiding losses and manipulating accounting data (Conyon & He, 2017).

SECTION 5

The Toshiba accounting scandal revealed serious issues with the company's corporate

governance, accounting practices, and culture. The company had engaged in fraudulent

accounting practices for several years, which led to an overstatement of profits and the

concealment of losses. The scandal resulted in significant reputational damage for Toshiba, as

well as financial penalties and regulatory scrutiny (Martynova & Renneboog, 2017).

Moving forward, it is unclear how Toshiba will perform in the future. The company has

undergone significant changes in recent years, including a restructuring of its business units and

a shift towards renewable energy and other growth areas. However, the reputational damage

caused by the accounting scandal may make it difficult for Toshiba to attract new customers and

investors (Ministry of Economy Trade and Industry, 2015). Additionally, the company faces

significant competition in many of its key markets, including semiconductors, laptops, and other

electronics.

To sustain its competitive advantage over rivals, Toshiba will need to prioritize ethical and

sustainable business practices, and establish effective corporate governance mechanisms. This

will require a commitment to transparency, accountability, and stakeholder engagement, as well

as ongoing efforts to build a strong culture of integrity and compliance (Martynova &

Renneboog, 2017).

fraud: opportunity, rationalization, and pressure. Opportunity refers to the ability to commit

fraud, such as weak internal controls or a lack of oversight. Rationalization refers to the ability to

justify fraudulent behavior, such as a belief that it is necessary to meet financial targets

(Martynova & Renneboog, 2017). Pressure refers to the factors that create the need for fraud,

such as financial difficulties or the desire to maintain a certain lifestyle. The Toshiba scandal can

be analyzed through the lens of the fraud triangle. The company's management had the

opportunity to engage in fraudulent accounting practices due to weak internal controls and a lack

of oversight. They rationalized their behavior by believing it was necessary to meet ambitious

financial targets. And they felt pressure to maintain the appearance of financial stability, even if

it meant hiding losses and manipulating accounting data (Conyon & He, 2017).

SECTION 5

The Toshiba accounting scandal revealed serious issues with the company's corporate

governance, accounting practices, and culture. The company had engaged in fraudulent

accounting practices for several years, which led to an overstatement of profits and the

concealment of losses. The scandal resulted in significant reputational damage for Toshiba, as

well as financial penalties and regulatory scrutiny (Martynova & Renneboog, 2017).

Moving forward, it is unclear how Toshiba will perform in the future. The company has

undergone significant changes in recent years, including a restructuring of its business units and

a shift towards renewable energy and other growth areas. However, the reputational damage

caused by the accounting scandal may make it difficult for Toshiba to attract new customers and

investors (Ministry of Economy Trade and Industry, 2015). Additionally, the company faces

significant competition in many of its key markets, including semiconductors, laptops, and other

electronics.

To sustain its competitive advantage over rivals, Toshiba will need to prioritize ethical and

sustainable business practices, and establish effective corporate governance mechanisms. This

will require a commitment to transparency, accountability, and stakeholder engagement, as well

as ongoing efforts to build a strong culture of integrity and compliance (Martynova &

Renneboog, 2017).

In my opinion, the Toshiba accounting scandal serves as a cautionary tale for companies about

the importance of ethical behavior and corporate governance. The scandal highlights the risks

associated with a focus on short-term profits and aggressive financial targets, and the importance

of balancing the interests of all stakeholders. To prevent similar incidents from occurring in the

future, companies must prioritize ethical and sustainable business practices, and establish

effective mechanisms for detecting and reporting misconduct. Ultimately, the success of a

company depends not just on its financial performance, but also on its ability to act with integrity

and accountability.

the importance of ethical behavior and corporate governance. The scandal highlights the risks

associated with a focus on short-term profits and aggressive financial targets, and the importance

of balancing the interests of all stakeholders. To prevent similar incidents from occurring in the

future, companies must prioritize ethical and sustainable business practices, and establish

effective mechanisms for detecting and reporting misconduct. Ultimately, the success of a

company depends not just on its financial performance, but also on its ability to act with integrity

and accountability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Arora, P., 2017. Corporate governance and ethical practices in Japan: The Toshiba scandal.

Journal of Business and Management, 1(19), pp. 21-30.

BBC News, 2015. Toshiba accounting scandal: Five things you need to know.. [Online]

Available at: https://www.bbc.com/news/business-33514085

[Accessed 2 March 2023].

Chugh, A., 2017. The Toshiba accounting scandal: How did it happen and what can be learned?.

International Journal of Corporate Governance, 2(8), pp. 107-121.

Conyon, M. & He, L., 2017. The Toshiba scandal and the implications for Japanese corporate

governance. Journal of Management and Governance, 1(21), pp. 1-21.

Daisuke, H., 2015. Toshiba's accounting scandal and corporate governance in Japan.. Asian

Economic Policy Review, 2(10), pp. 292-309.

Fisman, R. & Miguel, E., 2015. Cultures of corruption: Evidence from diplomatic parking

tickets. Journal of Political Econom, 2(123), pp. 371-417.

Fujimura, S., 2017. Toshiba accounting scandal: From corporate governance to personal ethics.

Journal of Business Ethics, 4(143), pp. 677-693.

Lee, T. & Li, X., 2017. Board gender diversity, corporate governance, and the Toshiba

accounting scandal. Journal of Applied Accounting Research, 1(18), pp. 2-19.

Makino, M., 2016. The Toshiba accounting scandal: Corporate governance and culture failures.

Journal of Accounting, Auditing & Finance, 1(31), pp. 5-12.

Martynova, M. & Renneboog, L., 2017. Corporate governance and financial misconduct:

Evidence from scandals. Journal of Corporate Finance, Volume 43, pp. 174-194.

Ministry of Economy Trade and Industry, 2015. Report of the Third Party Committee on

Toshiba's Inappropriate Accounting Treatment and Its Historical Background.. [Online]

Available at: https://www.meti.go.jp/english/press/2015/0722_01.html

[Accessed 2 March 2023].

Arora, P., 2017. Corporate governance and ethical practices in Japan: The Toshiba scandal.

Journal of Business and Management, 1(19), pp. 21-30.

BBC News, 2015. Toshiba accounting scandal: Five things you need to know.. [Online]

Available at: https://www.bbc.com/news/business-33514085

[Accessed 2 March 2023].

Chugh, A., 2017. The Toshiba accounting scandal: How did it happen and what can be learned?.

International Journal of Corporate Governance, 2(8), pp. 107-121.

Conyon, M. & He, L., 2017. The Toshiba scandal and the implications for Japanese corporate

governance. Journal of Management and Governance, 1(21), pp. 1-21.

Daisuke, H., 2015. Toshiba's accounting scandal and corporate governance in Japan.. Asian

Economic Policy Review, 2(10), pp. 292-309.

Fisman, R. & Miguel, E., 2015. Cultures of corruption: Evidence from diplomatic parking

tickets. Journal of Political Econom, 2(123), pp. 371-417.

Fujimura, S., 2017. Toshiba accounting scandal: From corporate governance to personal ethics.

Journal of Business Ethics, 4(143), pp. 677-693.

Lee, T. & Li, X., 2017. Board gender diversity, corporate governance, and the Toshiba

accounting scandal. Journal of Applied Accounting Research, 1(18), pp. 2-19.

Makino, M., 2016. The Toshiba accounting scandal: Corporate governance and culture failures.

Journal of Accounting, Auditing & Finance, 1(31), pp. 5-12.

Martynova, M. & Renneboog, L., 2017. Corporate governance and financial misconduct:

Evidence from scandals. Journal of Corporate Finance, Volume 43, pp. 174-194.

Ministry of Economy Trade and Industry, 2015. Report of the Third Party Committee on

Toshiba's Inappropriate Accounting Treatment and Its Historical Background.. [Online]

Available at: https://www.meti.go.jp/english/press/2015/0722_01.html

[Accessed 2 March 2023].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Osono, E. & Shimizu, S., 2016. Can Japanese boards go beyond "monitoring"?: Lessons from

the Toshiba accounting scandal. Journal of Business Strategy, 1(37), pp. 3-12.

Shimizu, K. & Hagiwara, N., 2016. Financial statement fraud detection: An analysis of statistical

and machine learning algorithms.. Journal of Accounting Research, 2(54), pp. 475-508.

Toshiba Corporation, 2021. About Toshiba.. [Online]

Available at: https://www.toshiba.co.jp/worldwide/about/index.html

[Accessed 2 April 2023].

Yamaoka, N., 2017. The Toshiba scandal and accounting standards.. International Journal of

Accounting, Auditing and Performance Evaluation, 1(13), pp. 71-86.

the Toshiba accounting scandal. Journal of Business Strategy, 1(37), pp. 3-12.

Shimizu, K. & Hagiwara, N., 2016. Financial statement fraud detection: An analysis of statistical

and machine learning algorithms.. Journal of Accounting Research, 2(54), pp. 475-508.

Toshiba Corporation, 2021. About Toshiba.. [Online]

Available at: https://www.toshiba.co.jp/worldwide/about/index.html

[Accessed 2 April 2023].

Yamaoka, N., 2017. The Toshiba scandal and accounting standards.. International Journal of

Accounting, Auditing and Performance Evaluation, 1(13), pp. 71-86.

APPENDICES

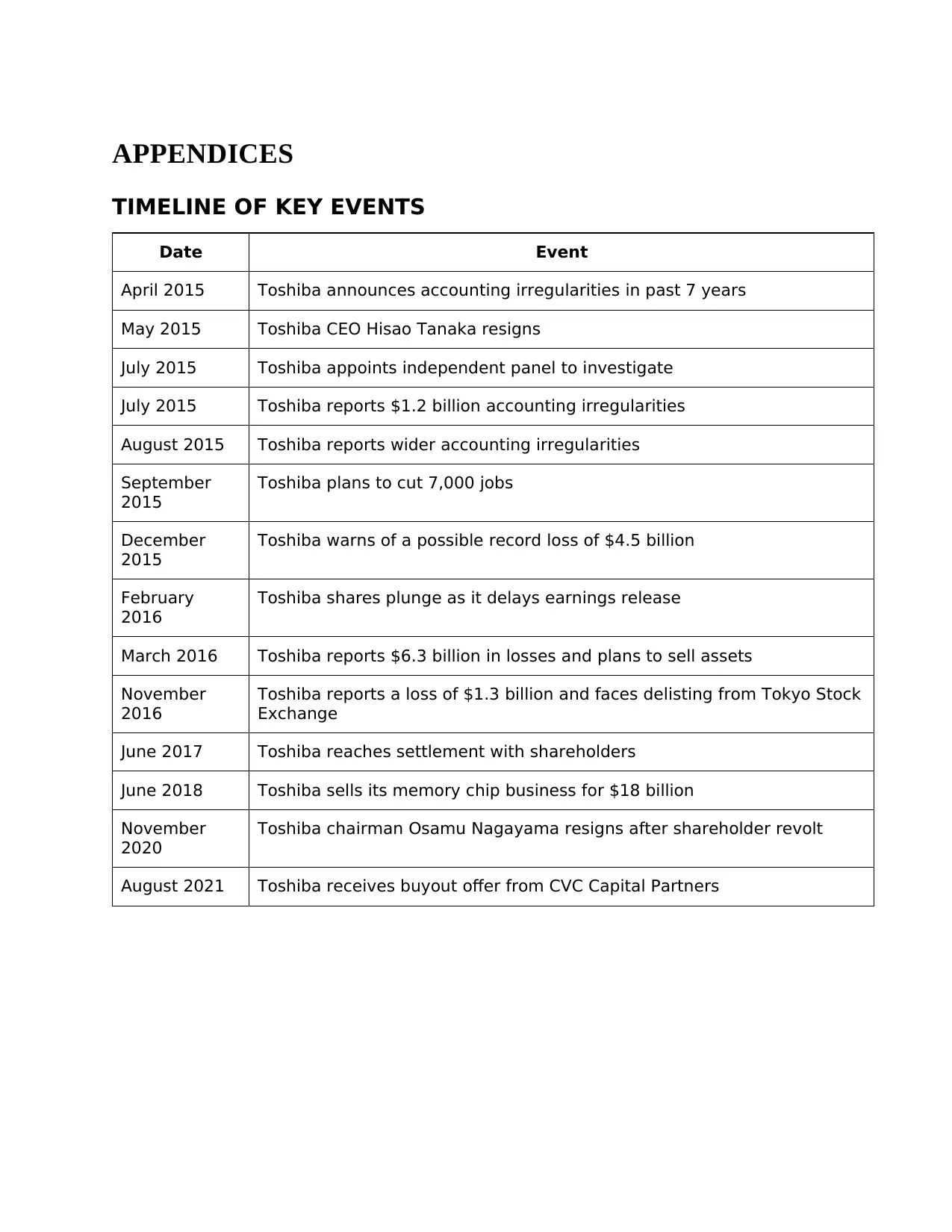

TIMELINE OF KEY EVENTS

Date Event

April 2015 Toshiba announces accounting irregularities in past 7 years

May 2015 Toshiba CEO Hisao Tanaka resigns

July 2015 Toshiba appoints independent panel to investigate

July 2015 Toshiba reports $1.2 billion accounting irregularities

August 2015 Toshiba reports wider accounting irregularities

September

2015

Toshiba plans to cut 7,000 jobs

December

2015

Toshiba warns of a possible record loss of $4.5 billion

February

2016

Toshiba shares plunge as it delays earnings release

March 2016 Toshiba reports $6.3 billion in losses and plans to sell assets

November

2016

Toshiba reports a loss of $1.3 billion and faces delisting from Tokyo Stock

Exchange

June 2017 Toshiba reaches settlement with shareholders

June 2018 Toshiba sells its memory chip business for $18 billion

November

2020

Toshiba chairman Osamu Nagayama resigns after shareholder revolt

August 2021 Toshiba receives buyout offer from CVC Capital Partners

TIMELINE OF KEY EVENTS

Date Event

April 2015 Toshiba announces accounting irregularities in past 7 years

May 2015 Toshiba CEO Hisao Tanaka resigns

July 2015 Toshiba appoints independent panel to investigate

July 2015 Toshiba reports $1.2 billion accounting irregularities

August 2015 Toshiba reports wider accounting irregularities

September

2015

Toshiba plans to cut 7,000 jobs

December

2015

Toshiba warns of a possible record loss of $4.5 billion

February

2016

Toshiba shares plunge as it delays earnings release

March 2016 Toshiba reports $6.3 billion in losses and plans to sell assets

November

2016

Toshiba reports a loss of $1.3 billion and faces delisting from Tokyo Stock

Exchange

June 2017 Toshiba reaches settlement with shareholders

June 2018 Toshiba sells its memory chip business for $18 billion

November

2020

Toshiba chairman Osamu Nagayama resigns after shareholder revolt

August 2021 Toshiba receives buyout offer from CVC Capital Partners

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.