Analyzing Financial Statements in the Travel and Tourism Sector

VerifiedAdded on 2020/06/04

|13

|3837

|52

AI Summary

The report investigates how CVP analysis aids in managerial decisions in the travel and tourism industry, emphasizing its role in enhancing performance. Through case studies and specific financial statement evaluations—such as income and balance sheets—the assignment demonstrates how management accounting information supports strategic decision-making. Furthermore, it explores various funding sources like loans, equity, and retained earnings for capital projects within this sector.

FINANCE AND FUNDING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explain the importance of costs and volume in financial management of travel and

tourism businesses.......................................................................................................................1

1.2 Analyse pricing methods used in the travel and tourism sector............................................2

1.3 Analyse factors influencing profit for travel and tourism businesses...................................4

TASK 2............................................................................................................................................5

2.1 Different types of management accounting information used in travel and tourism

businesses....................................................................................................................................5

2.2 Use of investment appraisal management accounting information as a decision-making

tool...............................................................................................................................................6

TASK 3............................................................................................................................................7

3.1 Interpret travel and tourism financial accounts.....................................................................7

TASK 4............................................................................................................................................9

4.1 Sources and distribution of funding for the development of capital projects associated with

tourism.........................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explain the importance of costs and volume in financial management of travel and

tourism businesses.......................................................................................................................1

1.2 Analyse pricing methods used in the travel and tourism sector............................................2

1.3 Analyse factors influencing profit for travel and tourism businesses...................................4

TASK 2............................................................................................................................................5

2.1 Different types of management accounting information used in travel and tourism

businesses....................................................................................................................................5

2.2 Use of investment appraisal management accounting information as a decision-making

tool...............................................................................................................................................6

TASK 3............................................................................................................................................7

3.1 Interpret travel and tourism financial accounts.....................................................................7

TASK 4............................................................................................................................................9

4.1 Sources and distribution of funding for the development of capital projects associated with

tourism.........................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance and funding in travel and tourism is becoming is a crucial and important concept

in order to accelerate the travel and tourism sector. This is one of the booming sector which not

only provides job opportunity but also assist the economical structure of nation. This report is

prepared to analyse the importance of cost and volume in financial management. Pricing method

which is used in the travel and tourism sector in order to determine the price is defined. Profit

affecting factors are discussed which impact upon profit (Zapata and Hall, 2012).

Management accounting information which are used in tourism sector also defined in this

report. investment appraisal techniques are illustrated with the investment options and plans.

ATC group of travel and tourism sector is taken to elaborate this concept.

TASK 1

1.1 Explain the importance of costs and volume in financial management of travel and tourism

businesses

Cost is known as the consideration which is incurred to access the functions and the

operations in fluent manner. Expenses which are incurred with in the production and

manufacturing process to attain required sales graph is known as cost. Business operations and

management works for reducing the cost of operation and functions to earn more profit. Various

type of cost controlling techniques and concepts are used by organisations to control the cost and

enhancing the profitability graph. This is one of the essential aspect which helps to consolidate

the cost in single format and efforts are made by management to control cost. There are type of

costs exist in business such as

Variable cost: this cost is vary as per the production units and manufacturing goods.

This cost fluctuates as per the change in production units. Material cost, labour and direct

expenses are the cost which is considered as variable cost.

Fixed cost: this is the cost which remain constant at every level. Variation in productions

and sales units does not effect fixed cost (Yang and Wong, 2012). Organisation have to bear the

fixed cost even after not earning profitability or manufacturing goods and services. Interest on

loans and debentures, rent are the examples of fixed cost.

Cost Volume Profit (C-V-P) concept

1

Finance and funding in travel and tourism is becoming is a crucial and important concept

in order to accelerate the travel and tourism sector. This is one of the booming sector which not

only provides job opportunity but also assist the economical structure of nation. This report is

prepared to analyse the importance of cost and volume in financial management. Pricing method

which is used in the travel and tourism sector in order to determine the price is defined. Profit

affecting factors are discussed which impact upon profit (Zapata and Hall, 2012).

Management accounting information which are used in tourism sector also defined in this

report. investment appraisal techniques are illustrated with the investment options and plans.

ATC group of travel and tourism sector is taken to elaborate this concept.

TASK 1

1.1 Explain the importance of costs and volume in financial management of travel and tourism

businesses

Cost is known as the consideration which is incurred to access the functions and the

operations in fluent manner. Expenses which are incurred with in the production and

manufacturing process to attain required sales graph is known as cost. Business operations and

management works for reducing the cost of operation and functions to earn more profit. Various

type of cost controlling techniques and concepts are used by organisations to control the cost and

enhancing the profitability graph. This is one of the essential aspect which helps to consolidate

the cost in single format and efforts are made by management to control cost. There are type of

costs exist in business such as

Variable cost: this cost is vary as per the production units and manufacturing goods.

This cost fluctuates as per the change in production units. Material cost, labour and direct

expenses are the cost which is considered as variable cost.

Fixed cost: this is the cost which remain constant at every level. Variation in productions

and sales units does not effect fixed cost (Yang and Wong, 2012). Organisation have to bear the

fixed cost even after not earning profitability or manufacturing goods and services. Interest on

loans and debentures, rent are the examples of fixed cost.

Cost Volume Profit (C-V-P) concept

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this is the concept is used to evaluate the selling price, cost, desired sales units and price

of products and services. Evaluation of cost remain based upon structure and nature of business.

Contribution is considered base of this concept. This concept defines the relation between

contribution and fixed cost (Witt, Brooke and Buckley, 2013). There is a centre point is analysed

at which organisation may attain an optimum level of profitability in respect of cost by

producing units. Positive outcomes in terms of returns and profitability reflect the effectiveness

of CVP concept. This concept contains some assumptions in respect of profitability such as sale

price of per unit, variable cost per unit, total fixed cost and cost of produced products and

services, activity charges and the concept of sold units.

Break even analysis is a technique which helps to interact the desired amount of

production units to be sold in units and in amount. This analysis helps to identify the desired

amount of sales which is required to get optimum returns. Break even analysis is calculated in

following ways:

Break even point in (£): contribution margin plays vital role in respect of evaluating the

break even point in sale value. This is one of the essential aspect which is evaluated with the help

of fixed cost. It is calculated as per following formula;

Break even point in

Break even point in (£) = (Contribution / Profit volume ratio or contribution

margin)*100

Break even sales in units: this helps to analyse that how much units are required to

produced to generate optimum revenues and income. This is calculated as per following formula:

BEP (units) = Fixed cost / contribution per unit

With the help of cost volume and profit concept, managers of ATC company be able to

analyse the cost of packages, price of products and volume for the articular time duration.

1.2 Analyse pricing methods used in the travel and tourism sector

Evaluate the cost of products and services is one of the important task for management of

organisation. Pricing techniques are used to analyse the cost of products in various ways. There

are type of products and services are found in travel and tourism sector (Spenceley, 2012).

Accommodation, transportation, retail travel agents, tour operators, residents oriented products

and services, tour packages, reservations and transport facilities the main services which are

considered in this context.

2

of products and services. Evaluation of cost remain based upon structure and nature of business.

Contribution is considered base of this concept. This concept defines the relation between

contribution and fixed cost (Witt, Brooke and Buckley, 2013). There is a centre point is analysed

at which organisation may attain an optimum level of profitability in respect of cost by

producing units. Positive outcomes in terms of returns and profitability reflect the effectiveness

of CVP concept. This concept contains some assumptions in respect of profitability such as sale

price of per unit, variable cost per unit, total fixed cost and cost of produced products and

services, activity charges and the concept of sold units.

Break even analysis is a technique which helps to interact the desired amount of

production units to be sold in units and in amount. This analysis helps to identify the desired

amount of sales which is required to get optimum returns. Break even analysis is calculated in

following ways:

Break even point in (£): contribution margin plays vital role in respect of evaluating the

break even point in sale value. This is one of the essential aspect which is evaluated with the help

of fixed cost. It is calculated as per following formula;

Break even point in

Break even point in (£) = (Contribution / Profit volume ratio or contribution

margin)*100

Break even sales in units: this helps to analyse that how much units are required to

produced to generate optimum revenues and income. This is calculated as per following formula:

BEP (units) = Fixed cost / contribution per unit

With the help of cost volume and profit concept, managers of ATC company be able to

analyse the cost of packages, price of products and volume for the articular time duration.

1.2 Analyse pricing methods used in the travel and tourism sector

Evaluate the cost of products and services is one of the important task for management of

organisation. Pricing techniques are used to analyse the cost of products in various ways. There

are type of products and services are found in travel and tourism sector (Spenceley, 2012).

Accommodation, transportation, retail travel agents, tour operators, residents oriented products

and services, tour packages, reservations and transport facilities the main services which are

considered in this context.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Types of pricing methods and techniques defined in this context which helps to analyse

the cost of operations in better management and price control.

Price skimming

this pricing technique is basically used by organisation to enhance the sale graph of new

products and services. Price skimming remain essential in respect of setting high rates at initial

stage. This not only helps to reduce the cost of but also encourage the customers to buy products

and services of organisation.

Psychology pricing

this technique is basically helps to manage the price of products and services with in the

organisation. Price of products and services are determined and fixed with the help of analysing

the perspective of people and customer. Price is set on logical and emotional levels. Increasing

the demand of customers towards products and services of travel and tourism sector is one of the

prime objective of this pricing strategy (Rodríguez, Williams and Hall, 2014).

Bundle pricing

this is also considered as a limited or boundary line pricing method. Small and medium

scale organisations' products at lower rate that customers could be faced. There are some set of

services remain involve and sold to customers as per their preference and priority. This is also

considered as inseparable pricing strategy due to its nature. Price of bulked products and services

remain inseparable. This create complex situation in respect of determining the price of

immovable products and services.

Most of the travel and tourism industries prevent to use this pricing strategies subject to

identifying the cost and set price of products. Because, bundle services create an expensive

image of products and services.

Seasonal pricing

This pricing technique assist managers to vary the price of products and services by

changing weather conditions. It is observed that the persons and people who lives in cold planes

and regions prefer to visit summer destinations and same as per people belong from warm

geographical structure prefer to visit winter destinations and places.

Markup costing

3

the cost of operations in better management and price control.

Price skimming

this pricing technique is basically used by organisation to enhance the sale graph of new

products and services. Price skimming remain essential in respect of setting high rates at initial

stage. This not only helps to reduce the cost of but also encourage the customers to buy products

and services of organisation.

Psychology pricing

this technique is basically helps to manage the price of products and services with in the

organisation. Price of products and services are determined and fixed with the help of analysing

the perspective of people and customer. Price is set on logical and emotional levels. Increasing

the demand of customers towards products and services of travel and tourism sector is one of the

prime objective of this pricing strategy (Rodríguez, Williams and Hall, 2014).

Bundle pricing

this is also considered as a limited or boundary line pricing method. Small and medium

scale organisations' products at lower rate that customers could be faced. There are some set of

services remain involve and sold to customers as per their preference and priority. This is also

considered as inseparable pricing strategy due to its nature. Price of bulked products and services

remain inseparable. This create complex situation in respect of determining the price of

immovable products and services.

Most of the travel and tourism industries prevent to use this pricing strategies subject to

identifying the cost and set price of products. Because, bundle services create an expensive

image of products and services.

Seasonal pricing

This pricing technique assist managers to vary the price of products and services by

changing weather conditions. It is observed that the persons and people who lives in cold planes

and regions prefer to visit summer destinations and same as per people belong from warm

geographical structure prefer to visit winter destinations and places.

Markup costing

3

Price of products and services are marked up to the cost and sold to customers. All the

additional charges and expenses such as service charge, maintenance and tax rates are considered

in this technique while determining the price of products and services.

Pricing for market penetration

this pricing strategy is basically used to analyse the cost and determine the price of

products and services by analysing market position of substitute products and services

(Lamberton and Lapeyre, 2011). To attain competitive advantages and profitability is one of the

major objective of this pricing technique.

Affordable or social welfare pricing

this pricing technique basically helps to set the price of products and services for those

who can't afford the services. A particular segment is formed to make pordust and services

affordable to customers.

1.3 Analyse factors influencing profit for travel and tourism businesses

Travel and tourism is a sector which basically remain associated with nation's growth and

development. It is analysed that the profitability of organisation get influenced by various factors

which are defined below. There are some relevant factors are defined in this context;

Political environment: there are divers political environment is found in various

countries and regions. There are some political aspects remain associated with profitability and

growth of organisation. Norms, rules and regulations are made for better control and

management of tourism sector. Being a part of national tourism development and growth,

government and political parties support travel and tourism sector.

Events: for increasing the graph of sales of travelling products and services events and

campaigns are organised by the managers of organisation. It helps to promote and support the

travelling and tourism structure of organisation. Attracting more visitors and tourist is one of the

main objective of events. Industry has to pay huge amount on investments for organising events.

Cost of events directly impact upon the price of products and services (Greenwood and

Scharfstein, 2013).

Seasons: this is also one of the price and profit influencing factor which affect the pricing

strategies and plans for better management and growth. Summer and winters are considered as

peak seasons in which travellers prefer to visit adventurous and best tourist destinations. ATC

need to make strategies regarding prices for peak season to get more competitive advantage.

4

additional charges and expenses such as service charge, maintenance and tax rates are considered

in this technique while determining the price of products and services.

Pricing for market penetration

this pricing strategy is basically used to analyse the cost and determine the price of

products and services by analysing market position of substitute products and services

(Lamberton and Lapeyre, 2011). To attain competitive advantages and profitability is one of the

major objective of this pricing technique.

Affordable or social welfare pricing

this pricing technique basically helps to set the price of products and services for those

who can't afford the services. A particular segment is formed to make pordust and services

affordable to customers.

1.3 Analyse factors influencing profit for travel and tourism businesses

Travel and tourism is a sector which basically remain associated with nation's growth and

development. It is analysed that the profitability of organisation get influenced by various factors

which are defined below. There are some relevant factors are defined in this context;

Political environment: there are divers political environment is found in various

countries and regions. There are some political aspects remain associated with profitability and

growth of organisation. Norms, rules and regulations are made for better control and

management of tourism sector. Being a part of national tourism development and growth,

government and political parties support travel and tourism sector.

Events: for increasing the graph of sales of travelling products and services events and

campaigns are organised by the managers of organisation. It helps to promote and support the

travelling and tourism structure of organisation. Attracting more visitors and tourist is one of the

main objective of events. Industry has to pay huge amount on investments for organising events.

Cost of events directly impact upon the price of products and services (Greenwood and

Scharfstein, 2013).

Seasons: this is also one of the price and profit influencing factor which affect the pricing

strategies and plans for better management and growth. Summer and winters are considered as

peak seasons in which travellers prefer to visit adventurous and best tourist destinations. ATC

need to make strategies regarding prices for peak season to get more competitive advantage.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Trend: customer presentation, market trend, culture are the part of trends which

attracts large number of visitors and tourist. This is one of the essential aspect in terms of

evaluate the price and making the strategies as per the market trends and culture.

Natural calamity: geographical position and atmosphere is the only factor which attract

visitors' attraction and tourist interest. But unbalanced climate situation and weather conditions

reduce the visitors' interest and customer vision towards the destination.

Currency rates: this is one of the external factor which affect the pricing strategy with in

the organisation. Different countries have different currencies in which trading activities

happened. Changing tax rates of currencies create complex situations subject to analysing the

profitability and price of products and services (Gabaix, 2012).

TASK 2

2.1 Different types of management accounting information used in travel and tourism businesses

Accounting information helps to analyse the consistency of capital projects and plans for

better growth and development of organisation. There is an internal management accounting

system is used by organisations to better management and control. Information which are

produced under this accounting systems are known as accounting information. Accounting

information assist managers subject to make effective strategies and plans. There are types of

management information are used as decision making tool in travel and tourism sector which are

defined as follows:

Trend line analysis: information which are collected under this method are tells about

the trend line subject to growth and development of organisation. This is one of the important

aspect in terms of analysing the trend line (Coles, Lemmon and Meschke, 2012).

Forecasting information: this information is basically helps to understand the dynamics

of analysis and forecasting the information related to sales and income results. This basically

helps to determine the nature and perception of change. There is a forecasted information and

data are published to analyse the future trend in terms of numbers of visitors and tourists.

Variance analysis: this is an analysis which helps to analyse the difference between the

actual and standard results. There is a future cost projection is prepared in respect of analysing

the actual results and the projected results. Projected cost of operations and management are

compared with actual results and differences are analysed.

5

attracts large number of visitors and tourist. This is one of the essential aspect in terms of

evaluate the price and making the strategies as per the market trends and culture.

Natural calamity: geographical position and atmosphere is the only factor which attract

visitors' attraction and tourist interest. But unbalanced climate situation and weather conditions

reduce the visitors' interest and customer vision towards the destination.

Currency rates: this is one of the external factor which affect the pricing strategy with in

the organisation. Different countries have different currencies in which trading activities

happened. Changing tax rates of currencies create complex situations subject to analysing the

profitability and price of products and services (Gabaix, 2012).

TASK 2

2.1 Different types of management accounting information used in travel and tourism businesses

Accounting information helps to analyse the consistency of capital projects and plans for

better growth and development of organisation. There is an internal management accounting

system is used by organisations to better management and control. Information which are

produced under this accounting systems are known as accounting information. Accounting

information assist managers subject to make effective strategies and plans. There are types of

management information are used as decision making tool in travel and tourism sector which are

defined as follows:

Trend line analysis: information which are collected under this method are tells about

the trend line subject to growth and development of organisation. This is one of the important

aspect in terms of analysing the trend line (Coles, Lemmon and Meschke, 2012).

Forecasting information: this information is basically helps to understand the dynamics

of analysis and forecasting the information related to sales and income results. This basically

helps to determine the nature and perception of change. There is a forecasted information and

data are published to analyse the future trend in terms of numbers of visitors and tourists.

Variance analysis: this is an analysis which helps to analyse the difference between the

actual and standard results. There is a future cost projection is prepared in respect of analysing

the actual results and the projected results. Projected cost of operations and management are

compared with actual results and differences are analysed.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management information: these are the reports which present the financial

position of organisation. Cash flow, income statement and financial position statement is one of

the essential aspect which is considered in this context.

MIS reports: there is a MIS system is found in organisational context which helps to sort

out the complex business situations and equations. This system provides an overview and helps

to reduce the uncertainties and make forecasting process more flexible or viable.

2.2 Use of investment appraisal management accounting information as a decision-making tool

Investment appraisal techniques are made in respect of analysing the capital investment

and capital projects. Investment appraisal techniques are used to evaluate the sustainability and

credibility of investment which remain associated with capital growth and development of

organisation. There are type of investment appraisal techniques are defined in which helps to

analyse the viability of capital projects.

Net present value: this is one of the essential method which helps to analyse the cost of

capital investment and capital project. This depends upon net cash inflows and outflows which

remain associated with capital projects. Capital project which contains the positive net present

value is considered effective and adopted by organisation. It is calculated with the help of

mathematical accounting information. There is a cumulative present value factor is used to

determine the present value of cash inflows for a specific duration (Investment appraisal

techniques, 2017).

Accounting rate of return: this is one of the method which analyse the sustainability

and credibility of project with the help earning rate. Capital projects which contains high

profitability returns and earning rates are accepted. It basically helps to earn high rearing projects

and cash projects are considered and opted by organisation. Initial investment is considered

important aspect while analysing the capital project under this investment appraisal technique.

Payback period method: investments are analysed by analysing recovery period of

investment after a particular duration and time. It simply clarify that how much time capital

investment take to provide optimum earnings and recover the cost incurred at initial stage.

Internal rate of return: A discounted rate of return is given in through which

investments are analysed and cost evaluated with the help of net present value method. Internal

rate of return is based upon efficiency. A discounted rate of return tells the that gives the value is

equal to Zero. It analyse the capital investment subject to analyse efficiency of the capital

6

position of organisation. Cash flow, income statement and financial position statement is one of

the essential aspect which is considered in this context.

MIS reports: there is a MIS system is found in organisational context which helps to sort

out the complex business situations and equations. This system provides an overview and helps

to reduce the uncertainties and make forecasting process more flexible or viable.

2.2 Use of investment appraisal management accounting information as a decision-making tool

Investment appraisal techniques are made in respect of analysing the capital investment

and capital projects. Investment appraisal techniques are used to evaluate the sustainability and

credibility of investment which remain associated with capital growth and development of

organisation. There are type of investment appraisal techniques are defined in which helps to

analyse the viability of capital projects.

Net present value: this is one of the essential method which helps to analyse the cost of

capital investment and capital project. This depends upon net cash inflows and outflows which

remain associated with capital projects. Capital project which contains the positive net present

value is considered effective and adopted by organisation. It is calculated with the help of

mathematical accounting information. There is a cumulative present value factor is used to

determine the present value of cash inflows for a specific duration (Investment appraisal

techniques, 2017).

Accounting rate of return: this is one of the method which analyse the sustainability

and credibility of project with the help earning rate. Capital projects which contains high

profitability returns and earning rates are accepted. It basically helps to earn high rearing projects

and cash projects are considered and opted by organisation. Initial investment is considered

important aspect while analysing the capital project under this investment appraisal technique.

Payback period method: investments are analysed by analysing recovery period of

investment after a particular duration and time. It simply clarify that how much time capital

investment take to provide optimum earnings and recover the cost incurred at initial stage.

Internal rate of return: A discounted rate of return is given in through which

investments are analysed and cost evaluated with the help of net present value method. Internal

rate of return is based upon efficiency. A discounted rate of return tells the that gives the value is

equal to Zero. It analyse the capital investment subject to analyse efficiency of the capital

6

investment. Those capital investments are adopted by organisation which remain greater then the

IRR value.

TASK 3

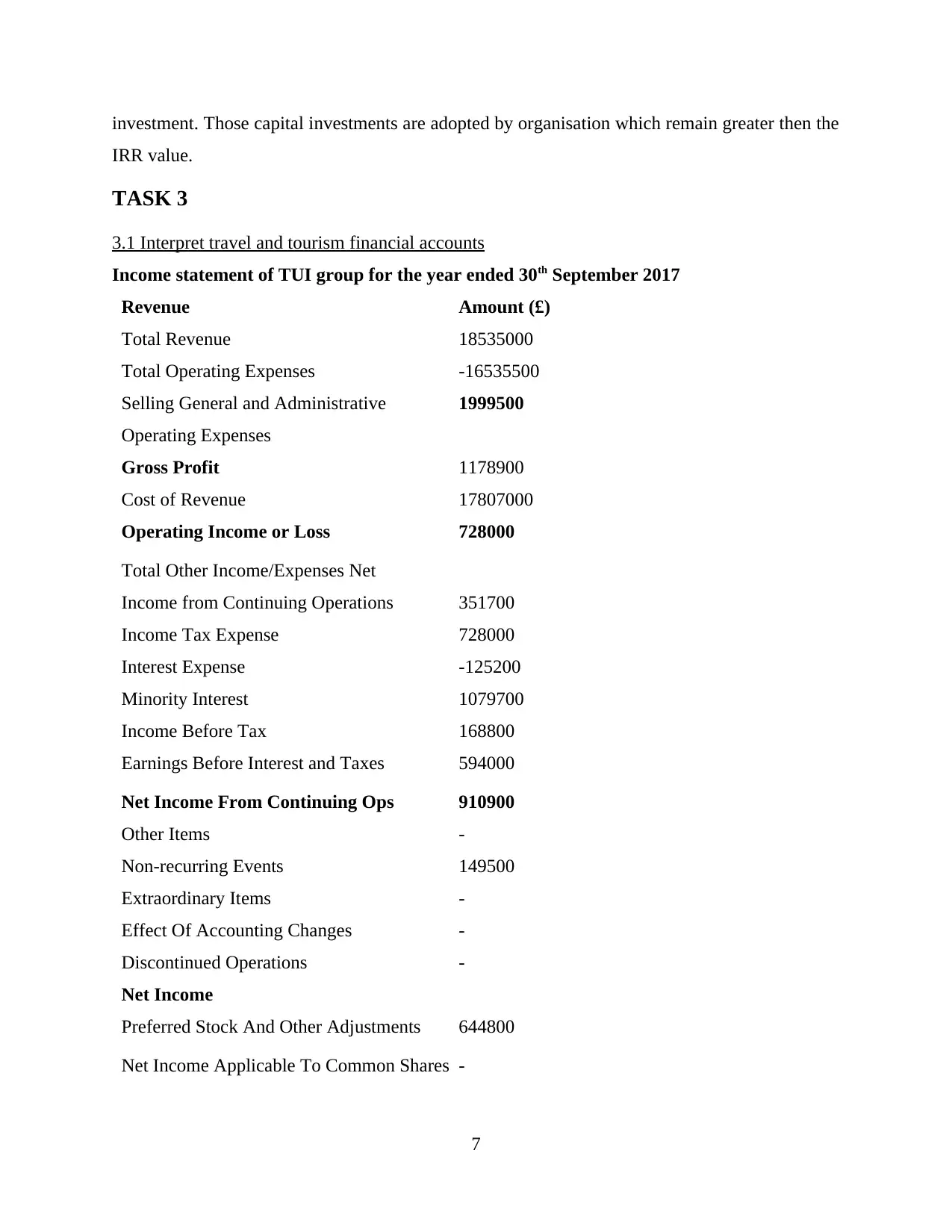

3.1 Interpret travel and tourism financial accounts

Income statement of TUI group for the year ended 30th September 2017

Revenue Amount (£)

Total Revenue 18535000

Total Operating Expenses -16535500

Selling General and Administrative 1999500

Operating Expenses

Gross Profit 1178900

Cost of Revenue 17807000

Operating Income or Loss 728000

Total Other Income/Expenses Net

Income from Continuing Operations 351700

Income Tax Expense 728000

Interest Expense -125200

Minority Interest 1079700

Income Before Tax 168800

Earnings Before Interest and Taxes 594000

Net Income From Continuing Ops 910900

Other Items -

Non-recurring Events 149500

Extraordinary Items -

Effect Of Accounting Changes -

Discontinued Operations -

Net Income

Preferred Stock And Other Adjustments 644800

Net Income Applicable To Common Shares -

7

IRR value.

TASK 3

3.1 Interpret travel and tourism financial accounts

Income statement of TUI group for the year ended 30th September 2017

Revenue Amount (£)

Total Revenue 18535000

Total Operating Expenses -16535500

Selling General and Administrative 1999500

Operating Expenses

Gross Profit 1178900

Cost of Revenue 17807000

Operating Income or Loss 728000

Total Other Income/Expenses Net

Income from Continuing Operations 351700

Income Tax Expense 728000

Interest Expense -125200

Minority Interest 1079700

Income Before Tax 168800

Earnings Before Interest and Taxes 594000

Net Income From Continuing Ops 910900

Other Items -

Non-recurring Events 149500

Extraordinary Items -

Effect Of Accounting Changes -

Discontinued Operations -

Net Income

Preferred Stock And Other Adjustments 644800

Net Income Applicable To Common Shares -

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

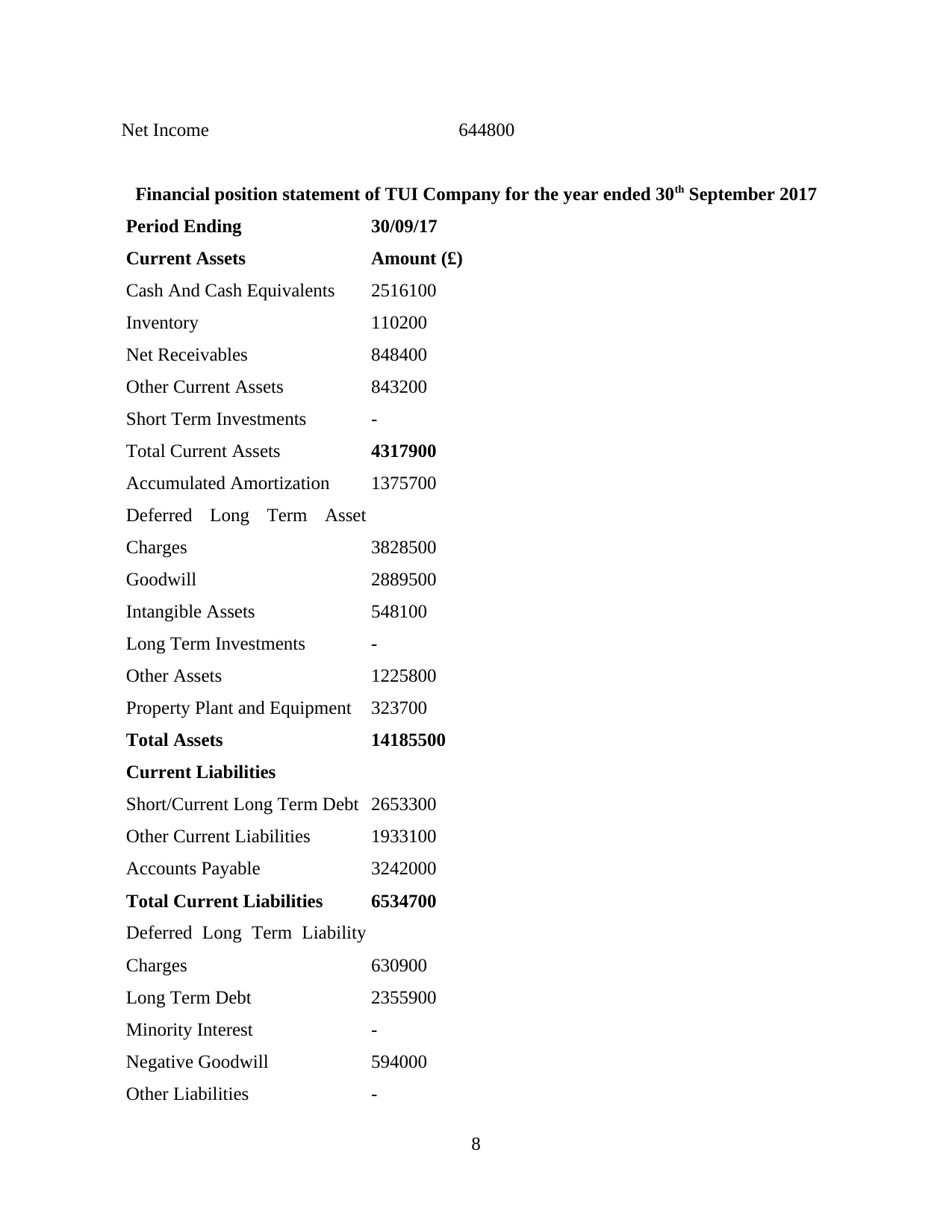

Net Income 644800

Financial position statement of TUI Company for the year ended 30th September 2017

Period Ending 30/09/17

Current Assets Amount (£)

Cash And Cash Equivalents 2516100

Inventory 110200

Net Receivables 848400

Other Current Assets 843200

Short Term Investments -

Total Current Assets 4317900

Accumulated Amortization 1375700

Deferred Long Term Asset

Charges 3828500

Goodwill 2889500

Intangible Assets 548100

Long Term Investments -

Other Assets 1225800

Property Plant and Equipment 323700

Total Assets 14185500

Current Liabilities

Short/Current Long Term Debt 2653300

Other Current Liabilities 1933100

Accounts Payable 3242000

Total Current Liabilities 6534700

Deferred Long Term Liability

Charges 630900

Long Term Debt 2355900

Minority Interest -

Negative Goodwill 594000

Other Liabilities -

8

Financial position statement of TUI Company for the year ended 30th September 2017

Period Ending 30/09/17

Current Assets Amount (£)

Cash And Cash Equivalents 2516100

Inventory 110200

Net Receivables 848400

Other Current Assets 843200

Short Term Investments -

Total Current Assets 4317900

Accumulated Amortization 1375700

Deferred Long Term Asset

Charges 3828500

Goodwill 2889500

Intangible Assets 548100

Long Term Investments -

Other Assets 1225800

Property Plant and Equipment 323700

Total Assets 14185500

Current Liabilities

Short/Current Long Term Debt 2653300

Other Current Liabilities 1933100

Accounts Payable 3242000

Total Current Liabilities 6534700

Deferred Long Term Liability

Charges 630900

Long Term Debt 2355900

Minority Interest -

Negative Goodwill 594000

Other Liabilities -

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

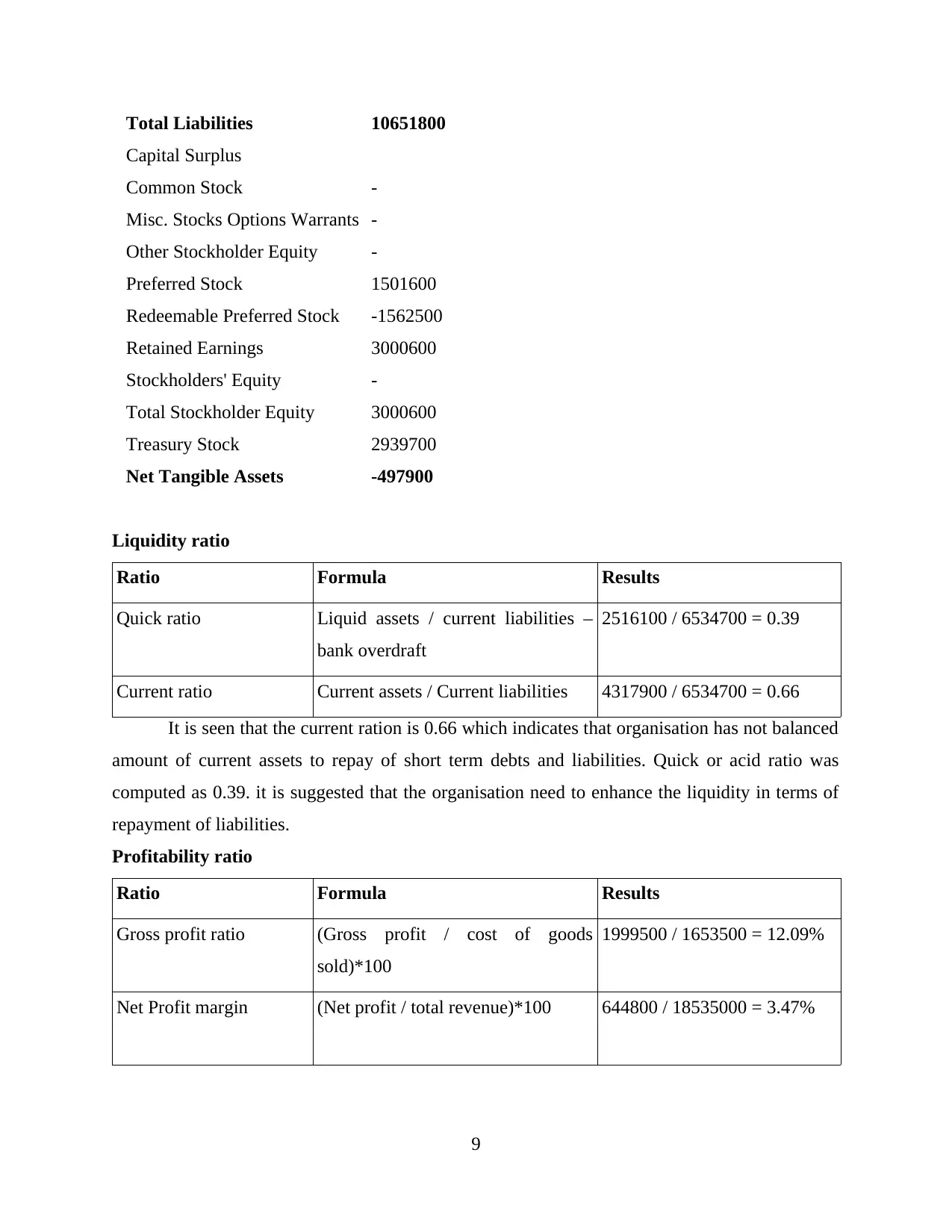

Total Liabilities 10651800

Capital Surplus

Common Stock -

Misc. Stocks Options Warrants -

Other Stockholder Equity -

Preferred Stock 1501600

Redeemable Preferred Stock -1562500

Retained Earnings 3000600

Stockholders' Equity -

Total Stockholder Equity 3000600

Treasury Stock 2939700

Net Tangible Assets -497900

Liquidity ratio

Ratio Formula Results

Quick ratio Liquid assets / current liabilities –

bank overdraft

2516100 / 6534700 = 0.39

Current ratio Current assets / Current liabilities 4317900 / 6534700 = 0.66

It is seen that the current ration is 0.66 which indicates that organisation has not balanced

amount of current assets to repay of short term debts and liabilities. Quick or acid ratio was

computed as 0.39. it is suggested that the organisation need to enhance the liquidity in terms of

repayment of liabilities.

Profitability ratio

Ratio Formula Results

Gross profit ratio (Gross profit / cost of goods

sold)*100

1999500 / 1653500 = 12.09%

Net Profit margin (Net profit / total revenue)*100 644800 / 18535000 = 3.47%

9

Capital Surplus

Common Stock -

Misc. Stocks Options Warrants -

Other Stockholder Equity -

Preferred Stock 1501600

Redeemable Preferred Stock -1562500

Retained Earnings 3000600

Stockholders' Equity -

Total Stockholder Equity 3000600

Treasury Stock 2939700

Net Tangible Assets -497900

Liquidity ratio

Ratio Formula Results

Quick ratio Liquid assets / current liabilities –

bank overdraft

2516100 / 6534700 = 0.39

Current ratio Current assets / Current liabilities 4317900 / 6534700 = 0.66

It is seen that the current ration is 0.66 which indicates that organisation has not balanced

amount of current assets to repay of short term debts and liabilities. Quick or acid ratio was

computed as 0.39. it is suggested that the organisation need to enhance the liquidity in terms of

repayment of liabilities.

Profitability ratio

Ratio Formula Results

Gross profit ratio (Gross profit / cost of goods

sold)*100

1999500 / 1653500 = 12.09%

Net Profit margin (Net profit / total revenue)*100 644800 / 18535000 = 3.47%

9

As per analysing the profitability position of organisation it is seen that organisation

earned the gross profit margin of 12.09% and the net profit margin 3.47%. overall position

present the positive image in terms of profitability and financial position.

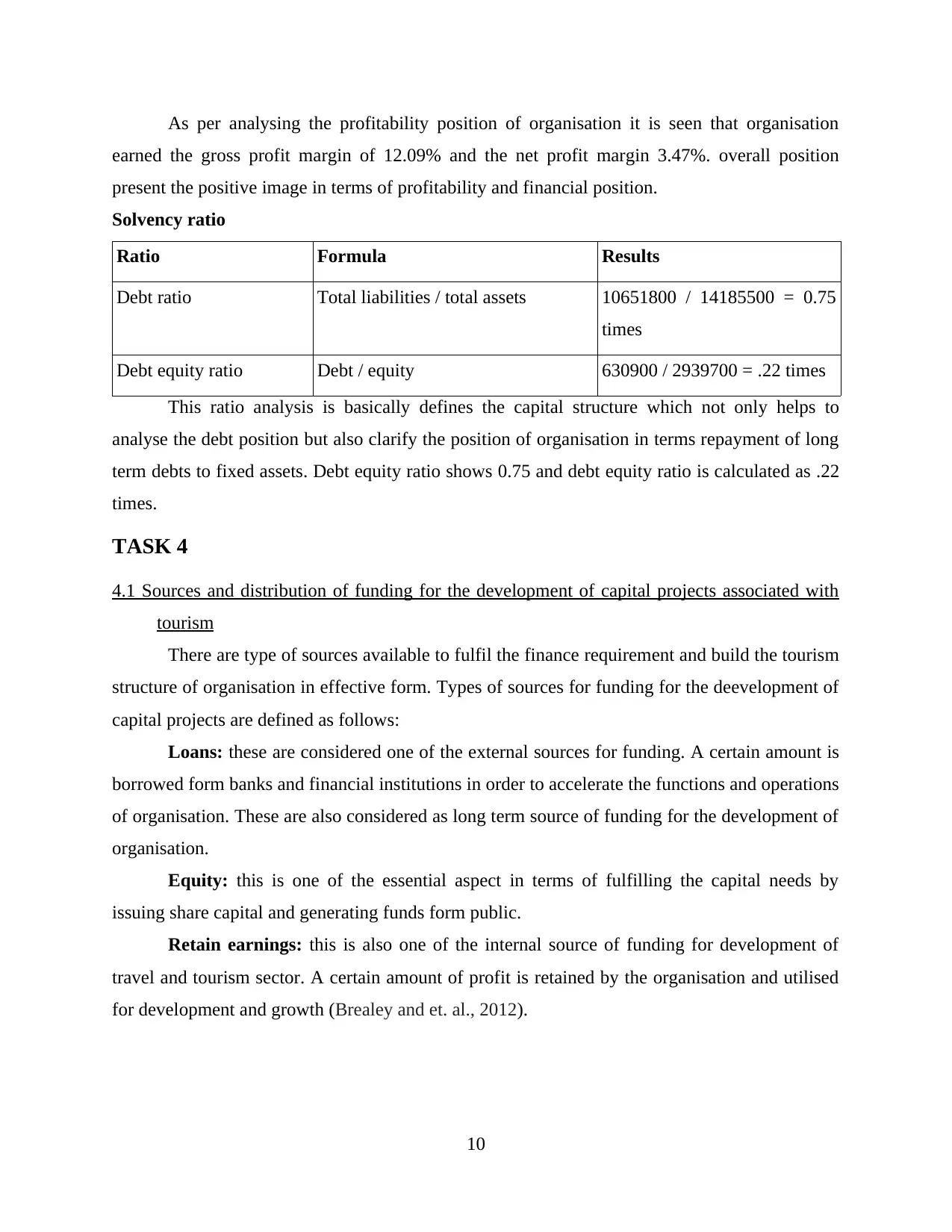

Solvency ratio

Ratio Formula Results

Debt ratio Total liabilities / total assets 10651800 / 14185500 = 0.75

times

Debt equity ratio Debt / equity 630900 / 2939700 = .22 times

This ratio analysis is basically defines the capital structure which not only helps to

analyse the debt position but also clarify the position of organisation in terms repayment of long

term debts to fixed assets. Debt equity ratio shows 0.75 and debt equity ratio is calculated as .22

times.

TASK 4

4.1 Sources and distribution of funding for the development of capital projects associated with

tourism

There are type of sources available to fulfil the finance requirement and build the tourism

structure of organisation in effective form. Types of sources for funding for the deevelopment of

capital projects are defined as follows:

Loans: these are considered one of the external sources for funding. A certain amount is

borrowed form banks and financial institutions in order to accelerate the functions and operations

of organisation. These are also considered as long term source of funding for the development of

organisation.

Equity: this is one of the essential aspect in terms of fulfilling the capital needs by

issuing share capital and generating funds form public.

Retain earnings: this is also one of the internal source of funding for development of

travel and tourism sector. A certain amount of profit is retained by the organisation and utilised

for development and growth (Brealey and et. al., 2012).

10

earned the gross profit margin of 12.09% and the net profit margin 3.47%. overall position

present the positive image in terms of profitability and financial position.

Solvency ratio

Ratio Formula Results

Debt ratio Total liabilities / total assets 10651800 / 14185500 = 0.75

times

Debt equity ratio Debt / equity 630900 / 2939700 = .22 times

This ratio analysis is basically defines the capital structure which not only helps to

analyse the debt position but also clarify the position of organisation in terms repayment of long

term debts to fixed assets. Debt equity ratio shows 0.75 and debt equity ratio is calculated as .22

times.

TASK 4

4.1 Sources and distribution of funding for the development of capital projects associated with

tourism

There are type of sources available to fulfil the finance requirement and build the tourism

structure of organisation in effective form. Types of sources for funding for the deevelopment of

capital projects are defined as follows:

Loans: these are considered one of the external sources for funding. A certain amount is

borrowed form banks and financial institutions in order to accelerate the functions and operations

of organisation. These are also considered as long term source of funding for the development of

organisation.

Equity: this is one of the essential aspect in terms of fulfilling the capital needs by

issuing share capital and generating funds form public.

Retain earnings: this is also one of the internal source of funding for development of

travel and tourism sector. A certain amount of profit is retained by the organisation and utilised

for development and growth (Brealey and et. al., 2012).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.