Finance and Funding in Travel and Tourism: Akaglo Tours Report

VerifiedAdded on 2020/06/04

|16

|4426

|36

Report

AI Summary

This report provides a comprehensive analysis of financial management within the travel and tourism sector, using Akaglo Tours as a case study. It delves into the significance of cost and volume in financial planning, exploring various cost types, allocation methods, and break-even analysis. The report examines different pricing methods, including rack rates, last-minute pricing, and package deals, while also identifying factors influencing profit, such as festive seasons, income levels, and foreign exchange rates. Furthermore, it covers management accounting information and its role in decision-making, along with the financial statements of the travel and tourism sector. The report concludes by discussing sources and distribution of funding for capital projects, offering a complete overview of financial strategies in the industry.

Finance and Funding in

travel and tourism

travel and tourism

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Significance of cost and volume in financial management of travel and tourism...............1

1.2: Pricing methods used in travel and tourism sector..............................................................3

1.3: Factors influencing profit for travel and tourism.................................................................4

TASK 2............................................................................................................................................5

2.1: Various types of management accounting information.......................................................5

2.2: Management accounting information as a decision making tool.........................................6

TASK 3............................................................................................................................................7

3.1: Financial statement of Travel and Tourism sector...............................................................7

TASK 4..........................................................................................................................................10

4.1: Sources and distribution of funding for growth of capital projects associated with tourism

...................................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Significance of cost and volume in financial management of travel and tourism...............1

1.2: Pricing methods used in travel and tourism sector..............................................................3

1.3: Factors influencing profit for travel and tourism.................................................................4

TASK 2............................................................................................................................................5

2.1: Various types of management accounting information.......................................................5

2.2: Management accounting information as a decision making tool.........................................6

TASK 3............................................................................................................................................7

3.1: Financial statement of Travel and Tourism sector...............................................................7

TASK 4..........................................................................................................................................10

4.1: Sources and distribution of funding for growth of capital projects associated with tourism

...................................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Travel and Tourism sector is one of the fast growing sector in the world which gives

maximum support to the economy of the country through regarding large number of

employment opportunities and increases income of the government. Therefore received

maximum support by the government and private companies. It motivates countries as well to

develop their valuable destinations and tourism sites in order to attract maximum number of

visitors. The present assignment is based on the Akaglo Tours Company (ATC) which deals in

offering cruise yacht to the tourist in order to reach their desired destinations is selected for the

purpose of preparing this report. The project includes the various pricing methods which is used

by travel and tourism companies. Different types of management information and several factors

which influences profit of travel and tourism business is also covered under this report (Chio,

2014).

TASK 1

1.1: Significance of cost and volume in financial management of travel and tourism

Akaglo Tours Company (ATC) is a trip organiser who provides all services to the

travellers that they want from the beginning of the trip to the end of trip such as providing cruise

yacht in order to help customers to reach it their desired destination as well as also provide

accommodation facilities for tourists. Therefore, there are various cost the company had incurred

in providing sufficient services to the tourists. Such cost has been discussed under the following:

Direct cost: It refers to such cost which directly incurred in producing quality products

and services. It can be also considered as variable cost if such cost is inconsistent and changes

amounts often. Labour cost, Raw Materials cost are few examples pf direct cost.

Indirect cost: It refers to such cost which is used to execute different activities but cannot

assigned to specific cost objects. Such costs are stable for a wide range of production and are

grouped under fixed cost. Salary paid to workers, rent expenses are some few examples of

indirect costs (Choi and Turk, 2011).

Variable cost: It refers to such cost which changes according to the production of goods

and services the company offered. Such cost rises with the increases in production and reduce

with the falls in the total output. Raw materials, packaging are few example of variable cost.

1

Travel and Tourism sector is one of the fast growing sector in the world which gives

maximum support to the economy of the country through regarding large number of

employment opportunities and increases income of the government. Therefore received

maximum support by the government and private companies. It motivates countries as well to

develop their valuable destinations and tourism sites in order to attract maximum number of

visitors. The present assignment is based on the Akaglo Tours Company (ATC) which deals in

offering cruise yacht to the tourist in order to reach their desired destinations is selected for the

purpose of preparing this report. The project includes the various pricing methods which is used

by travel and tourism companies. Different types of management information and several factors

which influences profit of travel and tourism business is also covered under this report (Chio,

2014).

TASK 1

1.1: Significance of cost and volume in financial management of travel and tourism

Akaglo Tours Company (ATC) is a trip organiser who provides all services to the

travellers that they want from the beginning of the trip to the end of trip such as providing cruise

yacht in order to help customers to reach it their desired destination as well as also provide

accommodation facilities for tourists. Therefore, there are various cost the company had incurred

in providing sufficient services to the tourists. Such cost has been discussed under the following:

Direct cost: It refers to such cost which directly incurred in producing quality products

and services. It can be also considered as variable cost if such cost is inconsistent and changes

amounts often. Labour cost, Raw Materials cost are few examples pf direct cost.

Indirect cost: It refers to such cost which is used to execute different activities but cannot

assigned to specific cost objects. Such costs are stable for a wide range of production and are

grouped under fixed cost. Salary paid to workers, rent expenses are some few examples of

indirect costs (Choi and Turk, 2011).

Variable cost: It refers to such cost which changes according to the production of goods

and services the company offered. Such cost rises with the increases in production and reduce

with the falls in the total output. Raw materials, packaging are few example of variable cost.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed cost: It refers to such cost which are not changes with the changes in level of

output thus not depend on the production level. Insurance, loan payment are the few examples of

fixed costs.

Allocation and Apportionment: It refers to the process of allocating cost to different

department on the basis of their needs and requirements so as to achieve profitable result in

return. Therefore, the management if fails to recognise departmental needs then it may difficult

for them to allocate cost on suitable basis.

Break-even analysis: It is the situation where the company earn either no profit or no

loss. Such analysis help company in determining what amount of products to be sell in order to

cover cost of doing business. Such analysis report can be generated on monthly, quarterly and

yearly basis (Evans, Stonehouse and Campbell, 2012).

Economise of scale: It refers to the company receiving cost advanced through expanding

their production level. Increasing the level of output produced will reducing the per unit fixed

cost. It will also decreases average variable cost due to increase in output. The main objective of

ATC is to expand their business activities in order to reduce its per unit of cost.

Diseconomies of scale: It refers to the situation where the company as well as

government accrue due to expansion of business operations. As if ATC expand its business

operations then it will faces specific diseconomies of scale which includes lack of coordination

and communication between the members working in company. ATC increases its business

operation due to which they need huge workforce thus it becomes difficult for management of

company in more effectively manner.

Importance of cost in the financial management of travel and tourism business

Decision making: Cost factor are considered while making an effective decision on

capital budgeting in order to get maximum return in future.

Improving management performance: It helps in enhancing the financial management

performance as allocation of cost to particular project is not easy task.

Designing financial structure: The business have developed and designed financial

structure on the basis of tourism activities that will be performed in near future and cost incurred

in executing such activities.

2

output thus not depend on the production level. Insurance, loan payment are the few examples of

fixed costs.

Allocation and Apportionment: It refers to the process of allocating cost to different

department on the basis of their needs and requirements so as to achieve profitable result in

return. Therefore, the management if fails to recognise departmental needs then it may difficult

for them to allocate cost on suitable basis.

Break-even analysis: It is the situation where the company earn either no profit or no

loss. Such analysis help company in determining what amount of products to be sell in order to

cover cost of doing business. Such analysis report can be generated on monthly, quarterly and

yearly basis (Evans, Stonehouse and Campbell, 2012).

Economise of scale: It refers to the company receiving cost advanced through expanding

their production level. Increasing the level of output produced will reducing the per unit fixed

cost. It will also decreases average variable cost due to increase in output. The main objective of

ATC is to expand their business activities in order to reduce its per unit of cost.

Diseconomies of scale: It refers to the situation where the company as well as

government accrue due to expansion of business operations. As if ATC expand its business

operations then it will faces specific diseconomies of scale which includes lack of coordination

and communication between the members working in company. ATC increases its business

operation due to which they need huge workforce thus it becomes difficult for management of

company in more effectively manner.

Importance of cost in the financial management of travel and tourism business

Decision making: Cost factor are considered while making an effective decision on

capital budgeting in order to get maximum return in future.

Improving management performance: It helps in enhancing the financial management

performance as allocation of cost to particular project is not easy task.

Designing financial structure: The business have developed and designed financial

structure on the basis of tourism activities that will be performed in near future and cost incurred

in executing such activities.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2: Pricing methods used in travel and tourism sector

Travel and Tourism sector is one of the fast growing sector which generates huge income

every year. Therefore, ATC need to focus on their pricing policies and opt on which ensures

them in getting profitable outcome in near future. Profitable outcomes can be inform of earning

profits, or retaining customers for longer period of time. There are several methods which need

to be considered by ATC which are determined as below:

Rack rates: It is normal price of any tourism products or services excluding discounts.

This price has been charged by company when the customers requested company to provide

accommodation and other related tourism facilities without any prior booking arrangements. For

example, three hours before, the customers requested ATC to provide them accommodation

facilities near to tourism destination then the company must charged such price in order to grab

opportunity to earn profit (Hall and Page, 2014).

Last minute pricing: This price has been charged by company in order to fulfil the seats

available with them just before departure to tourism destinations. In this, the company normally

offers huge discount on accommodation prices in order to fulfil those last-minute gaps. For

example, if ATC feels that there is any shortage of customers on the basis of accommodation

they have, then to fulfil the rooms available with them they offered huge discounts to customers

in order to fulfil all rooms.

Seasonal pricing: This price is charged on the basis of seasons. As the travellers mostly

preferred to visit tourism places during festivals thus to grab such opportunity, the company

offered seasonal prices in which discount wilt available for them. For example, During

Christmas the number of customers are increased due to which the company offered them

tourism services at seasonal price.

Discounting: Such pricing strategies are made juts to attract large number of customers

to get particular services of company. It is generally offered on market price of service.

Therefore, lowering the price of tourism services will help company in gaining new customers as

well as retain loyal customers which directly increases their profit.

Package deals: It includes multiple services the company offered to traveller in one

package. Sometimes, the customers can’t get particular tourism services due to shortage thus It is

considered as most effective pricing strategy as the company offers all services in one package

which can easily attract large number of customers (Nielsen and Spenceley, 2011).

3

Travel and Tourism sector is one of the fast growing sector which generates huge income

every year. Therefore, ATC need to focus on their pricing policies and opt on which ensures

them in getting profitable outcome in near future. Profitable outcomes can be inform of earning

profits, or retaining customers for longer period of time. There are several methods which need

to be considered by ATC which are determined as below:

Rack rates: It is normal price of any tourism products or services excluding discounts.

This price has been charged by company when the customers requested company to provide

accommodation and other related tourism facilities without any prior booking arrangements. For

example, three hours before, the customers requested ATC to provide them accommodation

facilities near to tourism destination then the company must charged such price in order to grab

opportunity to earn profit (Hall and Page, 2014).

Last minute pricing: This price has been charged by company in order to fulfil the seats

available with them just before departure to tourism destinations. In this, the company normally

offers huge discount on accommodation prices in order to fulfil those last-minute gaps. For

example, if ATC feels that there is any shortage of customers on the basis of accommodation

they have, then to fulfil the rooms available with them they offered huge discounts to customers

in order to fulfil all rooms.

Seasonal pricing: This price is charged on the basis of seasons. As the travellers mostly

preferred to visit tourism places during festivals thus to grab such opportunity, the company

offered seasonal prices in which discount wilt available for them. For example, During

Christmas the number of customers are increased due to which the company offered them

tourism services at seasonal price.

Discounting: Such pricing strategies are made juts to attract large number of customers

to get particular services of company. It is generally offered on market price of service.

Therefore, lowering the price of tourism services will help company in gaining new customers as

well as retain loyal customers which directly increases their profit.

Package deals: It includes multiple services the company offered to traveller in one

package. Sometimes, the customers can’t get particular tourism services due to shortage thus It is

considered as most effective pricing strategy as the company offers all services in one package

which can easily attract large number of customers (Nielsen and Spenceley, 2011).

3

Other methods of Pricing:

Along with above mentioned pricing strategies, here are some other methods of pricing

which the company preferred to charge:

Market oriented method: In this, the company first analyse the price that are prevailing

in market and on the basis of information, the company decide to set the price of tourism services

they offered in market. The company depends on market demand and accordingly fixing the

pricing policies. Therefore, the management find no difficulties in setting up prices as they just

need to follow market demand.

Cost oriented method: In this method, the company first identify and analyse the cost

incurred in providing services to the customers and accordingly set up the prices after adding

some margin on it. It brings beneficial result to both company as well as customers as they both

get what they desired.

1.3: Factors influencing profit for travel and tourism

There are several factors which may affects the revenue earned by travel and tourism

companies thus need to carefully analyse such factors in order to achieve desired goals and

objectives. ATC also required to consider such influencing factors and frame an effective pricing

strategies accordingly so as to attract large number of customers. Such factors includes festival

time, special event etc. which are briefly described as below:

Festive season: Mostly the traveller would likely to visit at tourism places during festive

seasons such as Christmas etc. due to which the tourism companies may either huge income on

the basis of price they charged as compared to their rivals. Thus, ATC should also required to

prepare in advance with tourism services and discounts in order to attract large number of

customers (Pike, 2012).

Income: Visiting tourism places is not basic need of an individual as they visit at such

places with a motive of spending some leisure time with their families or relatives. Therefore,

High income people preferred more to visit at various destinations as compared to low income

group. This may affect the revenue of tourism companies.

Technology: Technology easily attracts customers thus providing an effective

technologies such as internet, transportation facilities etc. by tourism companies help in

attracting large number of customers. If the company fails to provide such facilities them the

chances of losing customers are more due to which income will be also goes down.

4

Along with above mentioned pricing strategies, here are some other methods of pricing

which the company preferred to charge:

Market oriented method: In this, the company first analyse the price that are prevailing

in market and on the basis of information, the company decide to set the price of tourism services

they offered in market. The company depends on market demand and accordingly fixing the

pricing policies. Therefore, the management find no difficulties in setting up prices as they just

need to follow market demand.

Cost oriented method: In this method, the company first identify and analyse the cost

incurred in providing services to the customers and accordingly set up the prices after adding

some margin on it. It brings beneficial result to both company as well as customers as they both

get what they desired.

1.3: Factors influencing profit for travel and tourism

There are several factors which may affects the revenue earned by travel and tourism

companies thus need to carefully analyse such factors in order to achieve desired goals and

objectives. ATC also required to consider such influencing factors and frame an effective pricing

strategies accordingly so as to attract large number of customers. Such factors includes festival

time, special event etc. which are briefly described as below:

Festive season: Mostly the traveller would likely to visit at tourism places during festive

seasons such as Christmas etc. due to which the tourism companies may either huge income on

the basis of price they charged as compared to their rivals. Thus, ATC should also required to

prepare in advance with tourism services and discounts in order to attract large number of

customers (Pike, 2012).

Income: Visiting tourism places is not basic need of an individual as they visit at such

places with a motive of spending some leisure time with their families or relatives. Therefore,

High income people preferred more to visit at various destinations as compared to low income

group. This may affect the revenue of tourism companies.

Technology: Technology easily attracts customers thus providing an effective

technologies such as internet, transportation facilities etc. by tourism companies help in

attracting large number of customers. If the company fails to provide such facilities them the

chances of losing customers are more due to which income will be also goes down.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Leisure time: Every individual are doing savings with a motive of visiting attractive

tourism places at once in a life in order to spend some leisure time with their relatives, friends,

families etc. Therefore, it will bring advantaged to tourism companies and chances of increasing

growth of tourism sector will be high.

Foreign exchange rates: The currency rate of country will make huge impact on

decision making of customers whether to travel at such country or not. The travellers who live in

low domestic currency may hesitate to visit at tourism places located at developed counties due

to high currency rates as it becomes expensive for them. This will affects the profitability and

demand of tourism companies (Pocock and Phua, 2011).

Terrorism: Any terrorism activities occurred in past in countries may restricts travellers

to visit at such country. The people are not preferred to travel at such places where terrorist

activities are high as their mainly concerned is to get safety. Thus, it affects the sales of

company.

Factors influence profit on trip Price changed per tourist: It is observed that the price paid by the tourists are different

because of their preferences and paying capacity. This will have direct impact upon the

profitability of tour organisation. Number of tourists: The number of tourists has direct relation with the profit earning

capacity of organisation. In seasonal time number of tourists are more which helps to

improve revenue figures

Cost incurred by ATC: The costs which are incurred has direct impact upon the profit

earning capacity of organisation. If the amount of costs which are incurred to carry tourist

activities is increased than this will reduces their profit margin.

TASK 2

2.1: Various types of management accounting information

Every organisation which deals in either retailer sector, manufacturing sector or tourism

sector wants to survive their own market for longer period of time. And it can be possible only

when the management can able to make an effective decisions and plans suing management

accounting information the company kept with the help of using modern IT systems. ATC also

5

tourism places at once in a life in order to spend some leisure time with their relatives, friends,

families etc. Therefore, it will bring advantaged to tourism companies and chances of increasing

growth of tourism sector will be high.

Foreign exchange rates: The currency rate of country will make huge impact on

decision making of customers whether to travel at such country or not. The travellers who live in

low domestic currency may hesitate to visit at tourism places located at developed counties due

to high currency rates as it becomes expensive for them. This will affects the profitability and

demand of tourism companies (Pocock and Phua, 2011).

Terrorism: Any terrorism activities occurred in past in countries may restricts travellers

to visit at such country. The people are not preferred to travel at such places where terrorist

activities are high as their mainly concerned is to get safety. Thus, it affects the sales of

company.

Factors influence profit on trip Price changed per tourist: It is observed that the price paid by the tourists are different

because of their preferences and paying capacity. This will have direct impact upon the

profitability of tour organisation. Number of tourists: The number of tourists has direct relation with the profit earning

capacity of organisation. In seasonal time number of tourists are more which helps to

improve revenue figures

Cost incurred by ATC: The costs which are incurred has direct impact upon the profit

earning capacity of organisation. If the amount of costs which are incurred to carry tourist

activities is increased than this will reduces their profit margin.

TASK 2

2.1: Various types of management accounting information

Every organisation which deals in either retailer sector, manufacturing sector or tourism

sector wants to survive their own market for longer period of time. And it can be possible only

when the management can able to make an effective decisions and plans suing management

accounting information the company kept with the help of using modern IT systems. ATC also

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required to keep important accounting information in order to identity their actual financial

position in market. Different management accounting information are briefly described as below:

Budget Report: It is useful for companies in order to determine actual capabilities and

ultimate outcome. It is prepared by every companies at the beginning of accounting year so as to

determine what amount of sales and revenues they need to generate in month, quarter or year

(Ritchie, Amaya Molinar and Frechtling, 2010). ATC is operating its business operation across

worldwide thus essentially required to prepare budget report after determining the cost incurred

in future tourism activities. It also help management of ATC to make an effective decision and

strategies regarding generating huge profits and sales.

Variance analysis: Such analysis is helpful for company to determine whether they have

achieved their desired goals and objectives or not. It can be done through analysing by

comparing actual result with standard and if, any variance found then the management are able to

make an effective decisions to eliminate such variances.

Financial statement: Preparation of financial statements after the end of each accounting

period will help company in identifying the actual and true financial position in market.

Financial statement includes P&L a/c, Balance sheet, cash flow statement etc. It contains all

relevant information about the transactions the company made during whole accounting year.

Therefore, It directs management to make corrective decision and plans if the financial position

of company is not as much as expected.

Management accounting system: Through such system, the company can easily get

relevant information about the transaction happened on daily basis. In includes preparation of

reports, evaluation of data etc. in order to make an effective decision and strategies for future

tourism activities. It also helps in finding out the errors the company made which further should

be resolved by them in an effective and efficient manner (Spenceley, 2012).

2.2: Management accounting information as a decision making tool

Management accounting provides relevant and crucial information to company regarding

the expenditures incurred on daily business operations which help them in controlling cost and

utilise available resources in an optimum manner. With the help of such useful information, the

management can able to make future decision in order to achieve desired goals and objectives.

Following are the some factors which help in making an effective decisions and plans:

6

position in market. Different management accounting information are briefly described as below:

Budget Report: It is useful for companies in order to determine actual capabilities and

ultimate outcome. It is prepared by every companies at the beginning of accounting year so as to

determine what amount of sales and revenues they need to generate in month, quarter or year

(Ritchie, Amaya Molinar and Frechtling, 2010). ATC is operating its business operation across

worldwide thus essentially required to prepare budget report after determining the cost incurred

in future tourism activities. It also help management of ATC to make an effective decision and

strategies regarding generating huge profits and sales.

Variance analysis: Such analysis is helpful for company to determine whether they have

achieved their desired goals and objectives or not. It can be done through analysing by

comparing actual result with standard and if, any variance found then the management are able to

make an effective decisions to eliminate such variances.

Financial statement: Preparation of financial statements after the end of each accounting

period will help company in identifying the actual and true financial position in market.

Financial statement includes P&L a/c, Balance sheet, cash flow statement etc. It contains all

relevant information about the transactions the company made during whole accounting year.

Therefore, It directs management to make corrective decision and plans if the financial position

of company is not as much as expected.

Management accounting system: Through such system, the company can easily get

relevant information about the transaction happened on daily basis. In includes preparation of

reports, evaluation of data etc. in order to make an effective decision and strategies for future

tourism activities. It also helps in finding out the errors the company made which further should

be resolved by them in an effective and efficient manner (Spenceley, 2012).

2.2: Management accounting information as a decision making tool

Management accounting provides relevant and crucial information to company regarding

the expenditures incurred on daily business operations which help them in controlling cost and

utilise available resources in an optimum manner. With the help of such useful information, the

management can able to make future decision in order to achieve desired goals and objectives.

Following are the some factors which help in making an effective decisions and plans:

6

Forecasting sales: Such forecast regarding sales has been made at the beginning of

quarter or year and analyse has been made at the end of period in order to find out whether the

company has achieved desired sales or not and if not, then what are the reasons. This will help

management to make crucial decisions and corrective measures in order to rectify such reason.

For example, the management of ATC has defined sales target to their subordinates and then if

not achieved then subordinates are liable to provide them genuine reason.

Raising capital: ATC company if decide to expand its business to large scale then they

should required to raise capital from different sources such as financial institution, investors,

stakeholders etc. Therefore, the management accounting infraction provide all details about the

shareholding of their stakeholders and on the basis of that, the management approach them to

provide financial help in order to get maximum return in future (Spenceley, 2012).

Profitability issues: Due to high competition, ATC required to analyse their competitors

pricing strategies, tourism packages they offered etc. which help in making an effective decision

and strategies. Thus, such crucial and competitive information comes through accounting

information.

New product and service: ATC offered various tourism services such as providing

accommodation, transportation services etc. due to which they generated huge profits. In order to

expand their goals and objectives, the company should required to engage in providing other

services as well such as conducting tourism programs, cultural and fun activities etc. which help

them in attain huge customer strengths and profits as well.

Investment appraisal techniques

NPV: It is a tool which helps in considering time period required by business structure

for recovering of the amount of money which is incurred in project. It helps company to provides

the opportunity regarding evaluation whether project is profitable or not.

IRR: This technique helps in determination of rate through which can receive the return

from project in future period of time. Higher rate of depicts that project is profitable to carry in

future.

ARR: It is known as accounting rate of return which depicts the amount of profit or

return which is expected to attain from their investments made. The formula which is used

regarding determination of their this rate of return includes division of actual profit by the

amount of initial investment.

7

quarter or year and analyse has been made at the end of period in order to find out whether the

company has achieved desired sales or not and if not, then what are the reasons. This will help

management to make crucial decisions and corrective measures in order to rectify such reason.

For example, the management of ATC has defined sales target to their subordinates and then if

not achieved then subordinates are liable to provide them genuine reason.

Raising capital: ATC company if decide to expand its business to large scale then they

should required to raise capital from different sources such as financial institution, investors,

stakeholders etc. Therefore, the management accounting infraction provide all details about the

shareholding of their stakeholders and on the basis of that, the management approach them to

provide financial help in order to get maximum return in future (Spenceley, 2012).

Profitability issues: Due to high competition, ATC required to analyse their competitors

pricing strategies, tourism packages they offered etc. which help in making an effective decision

and strategies. Thus, such crucial and competitive information comes through accounting

information.

New product and service: ATC offered various tourism services such as providing

accommodation, transportation services etc. due to which they generated huge profits. In order to

expand their goals and objectives, the company should required to engage in providing other

services as well such as conducting tourism programs, cultural and fun activities etc. which help

them in attain huge customer strengths and profits as well.

Investment appraisal techniques

NPV: It is a tool which helps in considering time period required by business structure

for recovering of the amount of money which is incurred in project. It helps company to provides

the opportunity regarding evaluation whether project is profitable or not.

IRR: This technique helps in determination of rate through which can receive the return

from project in future period of time. Higher rate of depicts that project is profitable to carry in

future.

ARR: It is known as accounting rate of return which depicts the amount of profit or

return which is expected to attain from their investments made. The formula which is used

regarding determination of their this rate of return includes division of actual profit by the

amount of initial investment.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pay back period: Application of this method helps to understand length of time period

which is needed to recover the costs which are incurred while making investments. This will

improves the decision-making of management regarding undertaking of the activities of project

or not.

TASK 3

3.1: Financial statement of Travel and Tourism sector

Ratio analysis

It is refers as the quantitative analysis of information which is present in the financial

statements of organisation. This will provides the opportunity to the manager about assessment

of the operating and financial performance through determination of their efficiency, liquidity,

profitability and solvency.

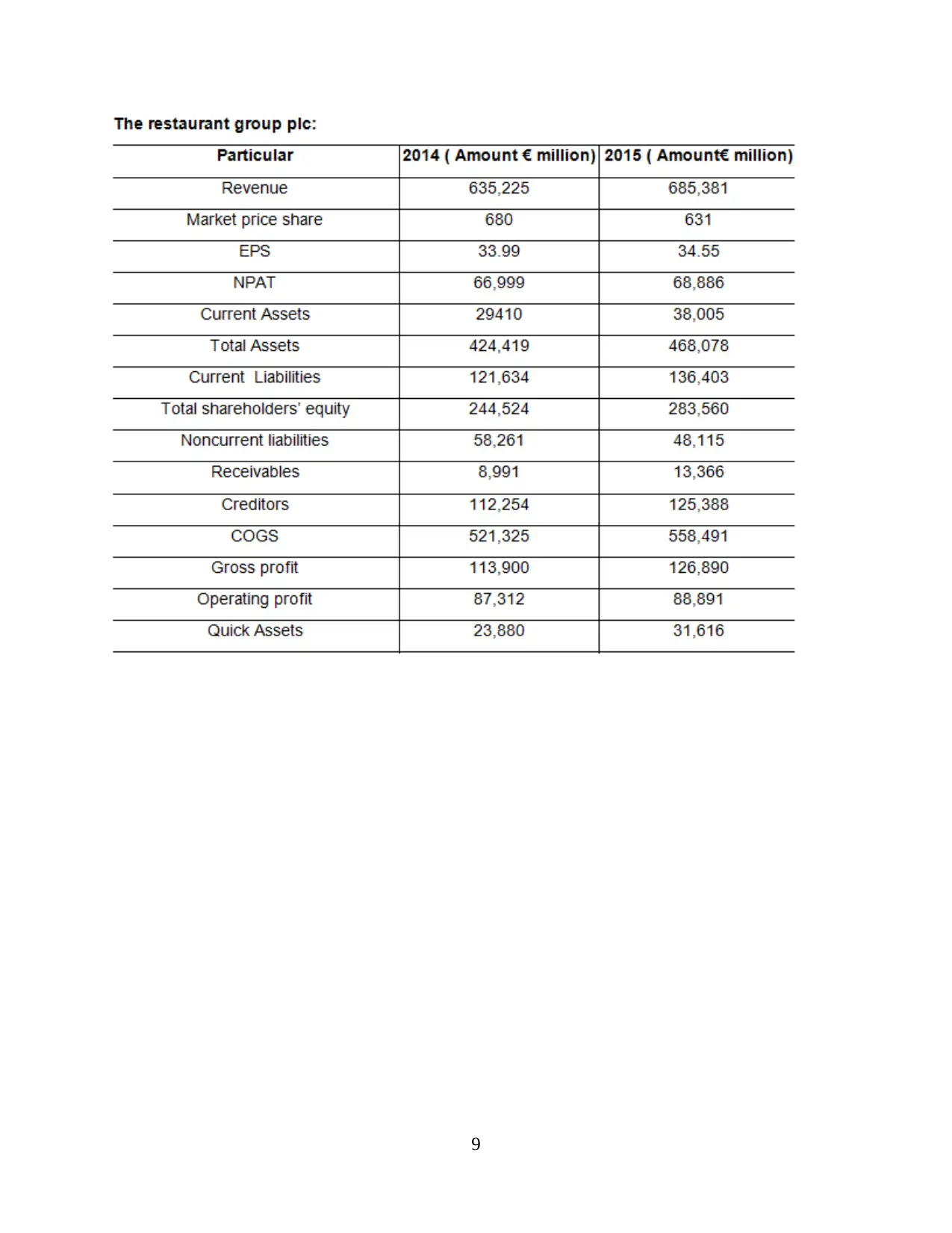

The main objective of preparing financial statements is to identify the actual financial

position of company in market which help them in taking further actions. ATC deals in providing

various tourism services to the travellers in order to help them in experiencing valuable

memories while travelling (Springer, Dordrecht.Ma and Hassink,2014). Thus, in comparison

with them, Restaurant group also engaged in travel and tourism sector. The company has done

pretty well between 2015 and 2016. Here are the financial statement of The restaurant group:

8

which is needed to recover the costs which are incurred while making investments. This will

improves the decision-making of management regarding undertaking of the activities of project

or not.

TASK 3

3.1: Financial statement of Travel and Tourism sector

Ratio analysis

It is refers as the quantitative analysis of information which is present in the financial

statements of organisation. This will provides the opportunity to the manager about assessment

of the operating and financial performance through determination of their efficiency, liquidity,

profitability and solvency.

The main objective of preparing financial statements is to identify the actual financial

position of company in market which help them in taking further actions. ATC deals in providing

various tourism services to the travellers in order to help them in experiencing valuable

memories while travelling (Springer, Dordrecht.Ma and Hassink,2014). Thus, in comparison

with them, Restaurant group also engaged in travel and tourism sector. The company has done

pretty well between 2015 and 2016. Here are the financial statement of The restaurant group:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

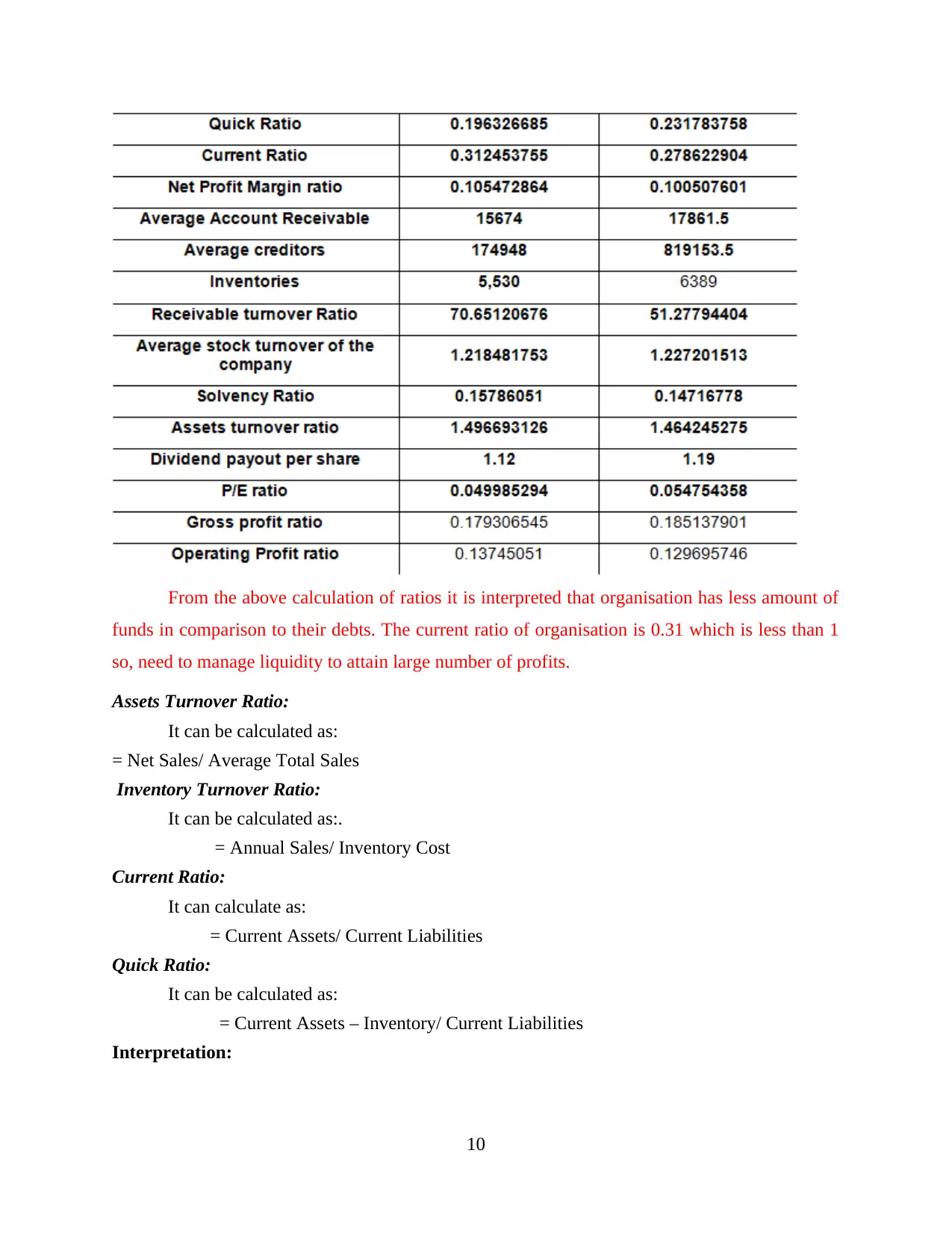

From the above calculation of ratios it is interpreted that organisation has less amount of

funds in comparison to their debts. The current ratio of organisation is 0.31 which is less than 1

so, need to manage liquidity to attain large number of profits.

Assets Turnover Ratio:

It can be calculated as:

= Net Sales/ Average Total Sales

Inventory Turnover Ratio:

It can be calculated as:.

= Annual Sales/ Inventory Cost

Current Ratio:

It can calculate as:

= Current Assets/ Current Liabilities

Quick Ratio:

It can be calculated as:

= Current Assets – Inventory/ Current Liabilities

Interpretation:

10

funds in comparison to their debts. The current ratio of organisation is 0.31 which is less than 1

so, need to manage liquidity to attain large number of profits.

Assets Turnover Ratio:

It can be calculated as:

= Net Sales/ Average Total Sales

Inventory Turnover Ratio:

It can be calculated as:.

= Annual Sales/ Inventory Cost

Current Ratio:

It can calculate as:

= Current Assets/ Current Liabilities

Quick Ratio:

It can be calculated as:

= Current Assets – Inventory/ Current Liabilities

Interpretation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.