Analysis of Toyota RAV4 Models: Pricing, Costs, and Profit Margins

VerifiedAdded on 2023/01/12

|9

|2331

|73

Report

AI Summary

This report provides a comprehensive analysis of the pricing strategies, cost structures, and profit margins of three Toyota RAV4 hybrid models in the Australian market. It examines the current pricing methods, which combine market-oriented and value-based approaches, and analyzes the target costs and profit margins of each model. The report delves into the application of cost-based pricing and market-based pricing strategies, evaluates their advantages and disadvantages, and offers recommendations for maintaining target profit margins through lean manufacturing, value chain analysis, and supply chain optimization. It also explores opportunities to reduce costs, identify value-added and non-value-added activities, and make recommendations regarding the final prices of the product to increase market share and profitability. The report concludes with insights into the mixed pricing strategies employed by Toyota, emphasizing the importance of cost control, supply chain management, and value chain analysis in achieving and sustaining profitability within the competitive automotive market.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

Analysis of the target cost of the three RAV4’ models reviewed in the given target profit

margins........................................................................................................................................1

Recommendations over maintaining the target profit margins....................................................2

Value chain analysis may help in identifying value added & non value added activities...........2

Recommendations over current pricing strategy comparing pricing strategies...........................3

Recommendation over the final prices of the product.................................................................4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................6

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

Analysis of the target cost of the three RAV4’ models reviewed in the given target profit

margins........................................................................................................................................1

Recommendations over maintaining the target profit margins....................................................2

Value chain analysis may help in identifying value added & non value added activities...........2

Recommendations over current pricing strategy comparing pricing strategies...........................3

Recommendation over the final prices of the product.................................................................4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................6

INTRODUTION

Toyota is global market leader in sales of the hybrid electric cars. It is also among the largest

company for encouraging the mass market adoption of the hybrid vehicles around the globe. It is

an automobile manufacturing company that is known for building cars for manufacturing the

cars in Toyota Motors. Toyota Australia is subsidiary of the Toyota Moto Corporation, based in

Japan. Present report is based on the product pricing and supply chain management of Toyota

Australia. Company market products of Toyota and manage motorsport. It is also engaged in

advertising and managing the operation of Toyota.

REPORT

Analysis of the target cost of the three RAV4’ models reviewed in the given target profit

margins.

Review over the current pricing strategy of the 3 vehicles in the RAV4 Hybrid range.

RAV4 GX2WD Hybrid,

RAV4 GXLAWD Hybrid &

RAV4 CRUISER 2WD Hybrid.

Toyota uses combination of the pricing strategies for the three models. Two of the mainly

used pricing strategies of Toyota are market oriented pricing strategy and the value based pricing

strategy. Market based pricing strategy of Toyota is used for analysing then similar cars running

in the market that can influence the sales of the three models. As there are not many car

manufactures in Australia prices are kept analysing the market of Toyota in Australia. All the

three cars are having high performance and have advance d features that helped the company in

keeping its prices considerably higher. Along with this it also uses value based approach for

deciding the prices of its product. Toyota decides the prices of product after measuring the cost

incurred for manufacturing the vehicle. This helps the business in deciding its target profit

margins to be kept above the cost of the vehicle (Aoki and Wilhelm, 2017). Current pricing

strategy is adopted after analysing the current market of Australia and the value provided to its

users by its cars. Products are performing excellently well in the Australian market that is

helping the company to retain its pricing strategy.

Cost pricing strategy of the Toyota motors of the three RAV4 hybrid models. (Toyota

Australia Prices, 2019)

Particulars GX2WD GXLAWD CRUISER Margins

1

Toyota is global market leader in sales of the hybrid electric cars. It is also among the largest

company for encouraging the mass market adoption of the hybrid vehicles around the globe. It is

an automobile manufacturing company that is known for building cars for manufacturing the

cars in Toyota Motors. Toyota Australia is subsidiary of the Toyota Moto Corporation, based in

Japan. Present report is based on the product pricing and supply chain management of Toyota

Australia. Company market products of Toyota and manage motorsport. It is also engaged in

advertising and managing the operation of Toyota.

REPORT

Analysis of the target cost of the three RAV4’ models reviewed in the given target profit

margins.

Review over the current pricing strategy of the 3 vehicles in the RAV4 Hybrid range.

RAV4 GX2WD Hybrid,

RAV4 GXLAWD Hybrid &

RAV4 CRUISER 2WD Hybrid.

Toyota uses combination of the pricing strategies for the three models. Two of the mainly

used pricing strategies of Toyota are market oriented pricing strategy and the value based pricing

strategy. Market based pricing strategy of Toyota is used for analysing then similar cars running

in the market that can influence the sales of the three models. As there are not many car

manufactures in Australia prices are kept analysing the market of Toyota in Australia. All the

three cars are having high performance and have advance d features that helped the company in

keeping its prices considerably higher. Along with this it also uses value based approach for

deciding the prices of its product. Toyota decides the prices of product after measuring the cost

incurred for manufacturing the vehicle. This helps the business in deciding its target profit

margins to be kept above the cost of the vehicle (Aoki and Wilhelm, 2017). Current pricing

strategy is adopted after analysing the current market of Australia and the value provided to its

users by its cars. Products are performing excellently well in the Australian market that is

helping the company to retain its pricing strategy.

Cost pricing strategy of the Toyota motors of the three RAV4 hybrid models. (Toyota

Australia Prices, 2019)

Particulars GX2WD GXLAWD CRUISER Margins

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

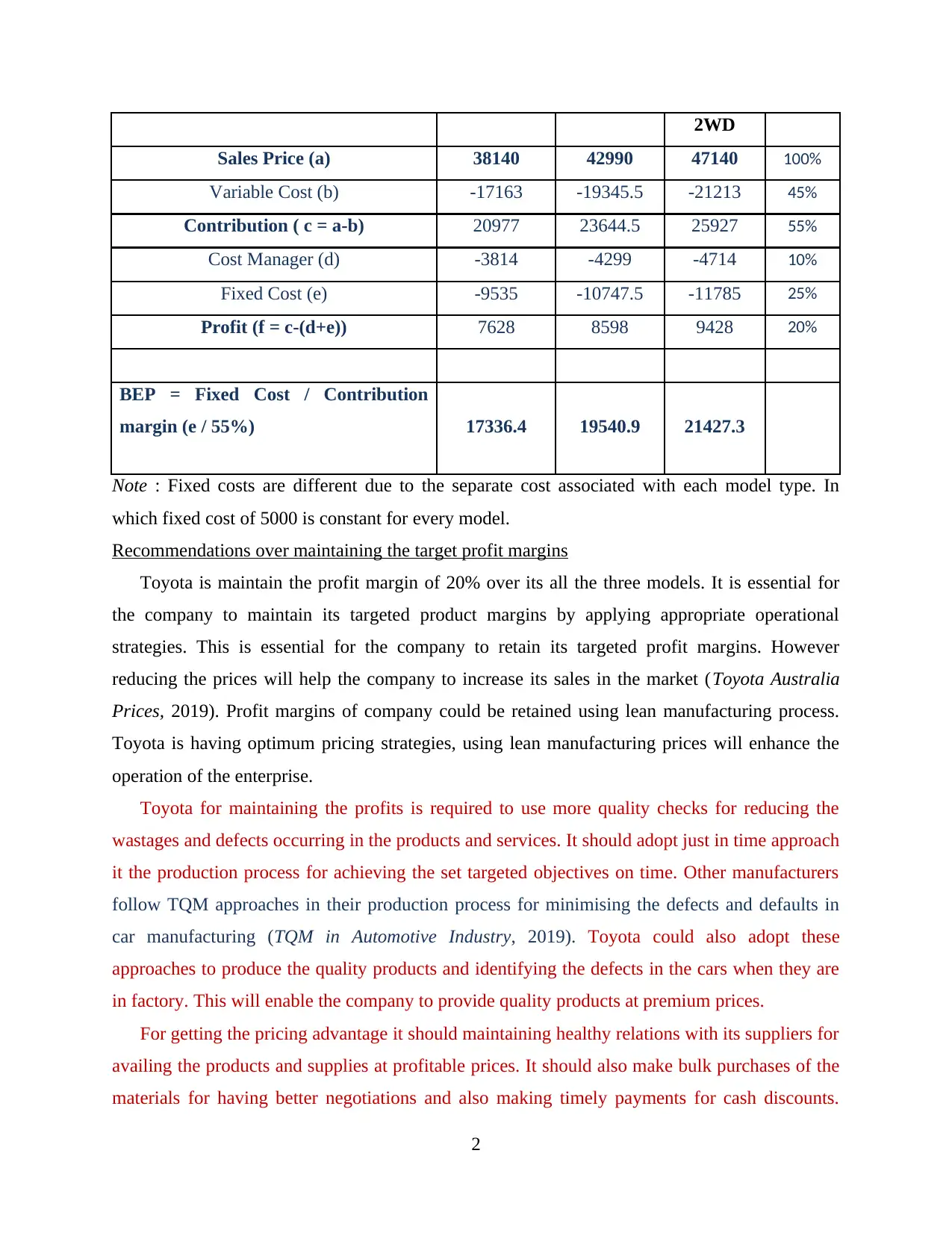

2WD

Sales Price (a) 38140 42990 47140 100%

Variable Cost (b) -17163 -19345.5 -21213 45%

Contribution ( c = a-b) 20977 23644.5 25927 55%

Cost Manager (d) -3814 -4299 -4714 10%

Fixed Cost (e) -9535 -10747.5 -11785 25%

Profit (f = c-(d+e)) 7628 8598 9428 20%

BEP = Fixed Cost / Contribution

margin (e / 55%) 17336.4 19540.9 21427.3

Note : Fixed costs are different due to the separate cost associated with each model type. In

which fixed cost of 5000 is constant for every model.

Recommendations over maintaining the target profit margins

Toyota is maintain the profit margin of 20% over its all the three models. It is essential for

the company to maintain its targeted product margins by applying appropriate operational

strategies. This is essential for the company to retain its targeted profit margins. However

reducing the prices will help the company to increase its sales in the market (Toyota Australia

Prices, 2019). Profit margins of company could be retained using lean manufacturing process.

Toyota is having optimum pricing strategies, using lean manufacturing prices will enhance the

operation of the enterprise.

Toyota for maintaining the profits is required to use more quality checks for reducing the

wastages and defects occurring in the products and services. It should adopt just in time approach

it the production process for achieving the set targeted objectives on time. Other manufacturers

follow TQM approaches in their production process for minimising the defects and defaults in

car manufacturing (TQM in Automotive Industry, 2019). Toyota could also adopt these

approaches to produce the quality products and identifying the defects in the cars when they are

in factory. This will enable the company to provide quality products at premium prices.

For getting the pricing advantage it should maintaining healthy relations with its suppliers for

availing the products and supplies at profitable prices. It should also make bulk purchases of the

materials for having better negotiations and also making timely payments for cash discounts.

2

Sales Price (a) 38140 42990 47140 100%

Variable Cost (b) -17163 -19345.5 -21213 45%

Contribution ( c = a-b) 20977 23644.5 25927 55%

Cost Manager (d) -3814 -4299 -4714 10%

Fixed Cost (e) -9535 -10747.5 -11785 25%

Profit (f = c-(d+e)) 7628 8598 9428 20%

BEP = Fixed Cost / Contribution

margin (e / 55%) 17336.4 19540.9 21427.3

Note : Fixed costs are different due to the separate cost associated with each model type. In

which fixed cost of 5000 is constant for every model.

Recommendations over maintaining the target profit margins

Toyota is maintain the profit margin of 20% over its all the three models. It is essential for

the company to maintain its targeted product margins by applying appropriate operational

strategies. This is essential for the company to retain its targeted profit margins. However

reducing the prices will help the company to increase its sales in the market (Toyota Australia

Prices, 2019). Profit margins of company could be retained using lean manufacturing process.

Toyota is having optimum pricing strategies, using lean manufacturing prices will enhance the

operation of the enterprise.

Toyota for maintaining the profits is required to use more quality checks for reducing the

wastages and defects occurring in the products and services. It should adopt just in time approach

it the production process for achieving the set targeted objectives on time. Other manufacturers

follow TQM approaches in their production process for minimising the defects and defaults in

car manufacturing (TQM in Automotive Industry, 2019). Toyota could also adopt these

approaches to produce the quality products and identifying the defects in the cars when they are

in factory. This will enable the company to provide quality products at premium prices.

For getting the pricing advantage it should maintaining healthy relations with its suppliers for

availing the products and supplies at profitable prices. It should also make bulk purchases of the

materials for having better negotiations and also making timely payments for cash discounts.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Also close monitoring will be required over all the production process so that the resources are

utilised efficiently by the enterprise. Keeping the internal costs of the product will enable the

managers to have pricing advantage of the models.

Following recommendation may help in maintaining the target profit margins.

It could be recommended that it should adopt just in time for manufacturing as per the

market demand. This will prevent the carrying cost of company.

Theory of constraints will enable it to identify the operations of business that needs

improvement (Özcan And et.al., 2019). Corrective measures will enable smooth flow of

products to the customers.

It should enhance the TQM process by setting more quality checks for inspecting the

quality of product before entering and before leaving the factory.

Reducing the wastage to the minimum by close monitoring of the resources used in the

production process.

Strategies that are cost efficient should be adopted. It could combine some of the

processes eliminating the separate costs.

Value chain analysis may help in identifying value added & non value added activities.

Supply Chain opportunities for improving the costs.

Supply chain consumes considerable part of the cost of company. Therefore, special focus

is given over reducing the cost incurred in supply chain and having the opportunities for

reducing the costs. Company can establish its plants in locations that are most beneficial for it.

This will reduce various costs of company such as materials and parts transportation costs.

Supply chain should be designed the company that have least costs considering the other factors

that could increase the cost in other ways. Such as establishing in parts that costs high company

to make the products available to the end customers. The available resources of the company

should be used in the best manner by controlling the costs and increasing the productivity.

Value chain analysis helps the business enterprise to identify the activities that are adding

value to their products and non value adding activities that are consuming unnecessary costs of

the products (Chiarini, Baccarani and Mascherpa, 2018). This is essential for the company to

become cost efficient and keep it under control. This provides sustainability to the business and

helps in making cost improvements.

3

utilised efficiently by the enterprise. Keeping the internal costs of the product will enable the

managers to have pricing advantage of the models.

Following recommendation may help in maintaining the target profit margins.

It could be recommended that it should adopt just in time for manufacturing as per the

market demand. This will prevent the carrying cost of company.

Theory of constraints will enable it to identify the operations of business that needs

improvement (Özcan And et.al., 2019). Corrective measures will enable smooth flow of

products to the customers.

It should enhance the TQM process by setting more quality checks for inspecting the

quality of product before entering and before leaving the factory.

Reducing the wastage to the minimum by close monitoring of the resources used in the

production process.

Strategies that are cost efficient should be adopted. It could combine some of the

processes eliminating the separate costs.

Value chain analysis may help in identifying value added & non value added activities.

Supply Chain opportunities for improving the costs.

Supply chain consumes considerable part of the cost of company. Therefore, special focus

is given over reducing the cost incurred in supply chain and having the opportunities for

reducing the costs. Company can establish its plants in locations that are most beneficial for it.

This will reduce various costs of company such as materials and parts transportation costs.

Supply chain should be designed the company that have least costs considering the other factors

that could increase the cost in other ways. Such as establishing in parts that costs high company

to make the products available to the end customers. The available resources of the company

should be used in the best manner by controlling the costs and increasing the productivity.

Value chain analysis helps the business enterprise to identify the activities that are adding

value to their products and non value adding activities that are consuming unnecessary costs of

the products (Chiarini, Baccarani and Mascherpa, 2018). This is essential for the company to

become cost efficient and keep it under control. This provides sustainability to the business and

helps in making cost improvements.

3

Value adding activities

These are the activities that gives value to the customer for its price paid for the product.

From the company point of view value adding activity benefits company in ;:

Premium prices – It will help company to focus more over the activity and premium prices could

be charged for it.

Loyalty – When customer gets added value for its prices they tend to become more loyal towards

the company.

Market share – Specific features of the car not provided by other competitors will help in

gaining new market share.

Non value adding activities.

These are the activities that are not productive and are consuming cost of company. With

the value chain analysis it could identify the activities that are generating return or adding value

to the process or product. Eliminating such costs will help the company in improving its cost

structure.

Recommendations over current pricing strategy comparing pricing strategies.

Cost based pricing method

Cost based pricing method is been used by Toyota Australia currently for the sales of their

cars. Cost based pricing is one of the pricing methods of determining the selling price of a

product by the company, wherein the price of a product is determined by adding a profit element

(percentage) in addition to the cost of making the product. This type of pricing strategy when

used by Toyota has assisted them in earning certain amount of profit which is really necessary

for their growth and also for the expansion of their services. This pricing strategy has assisted

them in gaining competitive advantage. It has also been analysed that making use of cost based

pricing strategy have some type of advantages and disadvantages. This includes the following:

Advantages of cost based pricing method

It has been analysed that this type of pricing method is really easy for the employees of

Toyota Australia to calculate (Cusumano, 2020). It also takes less amount of time in finding out

the end results. This pricing target can help company in making sure that all incurred costs are

been covered by them. This pricing strategy when used by organization can also assist them in

gaining competitive advantage. Cost based pricing method also provides faire results.

Disadvantages of cost based pricing method

4

These are the activities that gives value to the customer for its price paid for the product.

From the company point of view value adding activity benefits company in ;:

Premium prices – It will help company to focus more over the activity and premium prices could

be charged for it.

Loyalty – When customer gets added value for its prices they tend to become more loyal towards

the company.

Market share – Specific features of the car not provided by other competitors will help in

gaining new market share.

Non value adding activities.

These are the activities that are not productive and are consuming cost of company. With

the value chain analysis it could identify the activities that are generating return or adding value

to the process or product. Eliminating such costs will help the company in improving its cost

structure.

Recommendations over current pricing strategy comparing pricing strategies.

Cost based pricing method

Cost based pricing method is been used by Toyota Australia currently for the sales of their

cars. Cost based pricing is one of the pricing methods of determining the selling price of a

product by the company, wherein the price of a product is determined by adding a profit element

(percentage) in addition to the cost of making the product. This type of pricing strategy when

used by Toyota has assisted them in earning certain amount of profit which is really necessary

for their growth and also for the expansion of their services. This pricing strategy has assisted

them in gaining competitive advantage. It has also been analysed that making use of cost based

pricing strategy have some type of advantages and disadvantages. This includes the following:

Advantages of cost based pricing method

It has been analysed that this type of pricing method is really easy for the employees of

Toyota Australia to calculate (Cusumano, 2020). It also takes less amount of time in finding out

the end results. This pricing target can help company in making sure that all incurred costs are

been covered by them. This pricing strategy when used by organization can also assist them in

gaining competitive advantage. Cost based pricing method also provides faire results.

Disadvantages of cost based pricing method

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This type or pricing strategy is not been useful when Toyota Australia is bringing out some

kind of new and innovative products. This type overpricing method is also inflexible; it cannot

be changed when once used.

Market based pricing strategy

It is also used by Toyota Australia for increasing the sales of their SUV segments in car. In

this type of strategy the price is been set up the company according to the conditions of market

(Monden, 2019). It has been analyse that before going for this type of strategy it is really

necessary for the Toyota Australia to be engaged in doing some sort of market research. This

pricing strategy can assist them in having and sharing a place in market. This will support them

in increasing the value of goods and services which has been sold up by them. It will help the

company in growing and achieving their goals and objectives.

Advantages of market based pricing

This type of pricing strategy assisted Toyota Australia in gaining competitive advantage. It

will assist them in setting their place in market. Market based pricing strategy can help Toyota

Australia in creating consumer loyalty. It will assist them in increasing their market share, profit

as well as loyalty.

Disadvantage of market based pricing method

The main disadvantage of this method is that it does not take into account the pricing

strategy which has been taken by competitors. This can reduce the productivity, production and

sales aspects of Toyota Australia. It can also reduce the number of cars which has been sold up

them. They also do not take in consideration the cost related to production.

Recommendation over the final prices of the product.

Manager should have slight decrease in its prices by controlling the cost of its variable

expenses. In its prices, product comprises of 45% of the variable costs. Using the lean strategies

and value chain activities should reduce the cost of its operations. Slight decrease in prices will

help the company to increase its market share. Reducing the prices will lower the margins of

company but for increasing the market share it can reduce its profit margins by 2% - 3%. This

will also affect the market share of the company being served and hence the existing prices are

favourable for the cmpany.

5

kind of new and innovative products. This type overpricing method is also inflexible; it cannot

be changed when once used.

Market based pricing strategy

It is also used by Toyota Australia for increasing the sales of their SUV segments in car. In

this type of strategy the price is been set up the company according to the conditions of market

(Monden, 2019). It has been analyse that before going for this type of strategy it is really

necessary for the Toyota Australia to be engaged in doing some sort of market research. This

pricing strategy can assist them in having and sharing a place in market. This will support them

in increasing the value of goods and services which has been sold up by them. It will help the

company in growing and achieving their goals and objectives.

Advantages of market based pricing

This type of pricing strategy assisted Toyota Australia in gaining competitive advantage. It

will assist them in setting their place in market. Market based pricing strategy can help Toyota

Australia in creating consumer loyalty. It will assist them in increasing their market share, profit

as well as loyalty.

Disadvantage of market based pricing method

The main disadvantage of this method is that it does not take into account the pricing

strategy which has been taken by competitors. This can reduce the productivity, production and

sales aspects of Toyota Australia. It can also reduce the number of cars which has been sold up

them. They also do not take in consideration the cost related to production.

Recommendation over the final prices of the product.

Manager should have slight decrease in its prices by controlling the cost of its variable

expenses. In its prices, product comprises of 45% of the variable costs. Using the lean strategies

and value chain activities should reduce the cost of its operations. Slight decrease in prices will

help the company to increase its market share. Reducing the prices will lower the margins of

company but for increasing the market share it can reduce its profit margins by 2% - 3%. This

will also affect the market share of the company being served and hence the existing prices are

favourable for the cmpany.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it could be concluded that Toyota uses mixed pricing strategies for its

three RAV4 models in Australian market. Pricing strategies are enabling the company to earn the

target profit margin of 20% over its product. With the help of value chain analysis it is promoting

value added activities and eliminating non value adding activities. Supply chain opportunities

help the company in analysing its cost strategies and improving its cost structure.

6

From the above report it could be concluded that Toyota uses mixed pricing strategies for its

three RAV4 models in Australian market. Pricing strategies are enabling the company to earn the

target profit margin of 20% over its product. With the help of value chain analysis it is promoting

value added activities and eliminating non value adding activities. Supply chain opportunities

help the company in analysing its cost strategies and improving its cost structure.

6

REFERENCES

Books and Journals

Cusumano, M.A., 2020. The Japanese automobile industry: Technology and management at

Nissan and Toyota. Brill.

Monden, Y., 2019. Toyota management system: Linking the seven key functional areas.

Routledge.

Chiarini, A., Baccarani, C. and Mascherpa, V., 2018. Lean production, Toyota Production

System and Kaizen philosophy. The TQM Journal.

Aoki, K. and Wilhelm, M., 2017. The role of ambidexterity in managing buyer–supplier

relationships: The Toyota case. Organization Science.28(6).pp.1080-1097.

Özcan, E. And et.al., 2019. The Case of Toyota Motor Europe. Foundations in Sound Design for

Embedded Media: A Multidisciplinary Approach.

Online

Toyota Australia Prices. 2019. [Online]. Available through :

< https://www.toyota.com.au/rav4/prices>.

TQM in Automotive Industry. 2019. [Online]. Available through :

< https://www.cebos.com/blog/total-quality-management-in-automotive-industry/>.

7

Books and Journals

Cusumano, M.A., 2020. The Japanese automobile industry: Technology and management at

Nissan and Toyota. Brill.

Monden, Y., 2019. Toyota management system: Linking the seven key functional areas.

Routledge.

Chiarini, A., Baccarani, C. and Mascherpa, V., 2018. Lean production, Toyota Production

System and Kaizen philosophy. The TQM Journal.

Aoki, K. and Wilhelm, M., 2017. The role of ambidexterity in managing buyer–supplier

relationships: The Toyota case. Organization Science.28(6).pp.1080-1097.

Özcan, E. And et.al., 2019. The Case of Toyota Motor Europe. Foundations in Sound Design for

Embedded Media: A Multidisciplinary Approach.

Online

Toyota Australia Prices. 2019. [Online]. Available through :

< https://www.toyota.com.au/rav4/prices>.

TQM in Automotive Industry. 2019. [Online]. Available through :

< https://www.cebos.com/blog/total-quality-management-in-automotive-industry/>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.