Comprehensive Financial and Management Accounting Report: Toyota

VerifiedAdded on 2023/06/07

|21

|4043

|217

Report

AI Summary

This report provides a detailed analysis of Toyota Motor Corporation's financial and management accounting practices, focusing on its environmental and social impacts. It begins with an introduction to Toyota's operations, followed by a discussion of the positive and negative consequences of its manufacturing activities. The report then examines Toyota's compliance with GRI disclosures, comparing the quality and depth of its environmental performance to that of BMW. It explores the benefits of GRI compliance for Toyota's stakeholders and analyzes the cost structures associated with a new 'Smart' vehicle production line, including fixed and variable costs. A break-even analysis is also discussed. The report concludes with an overview of Toyota's environmental and social performance, highlighting its achievements and alignment with GRI standards. Part B presents a cost analysis for the Smart Vehicle and Part C is missing.

RUNNING HEAD: FINANCIAL AND MANAGEMENT ACCOUNTING

Financial accounting

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and management accounting 2

Executive summary

The report focuses on the environmental and social factors of Toyota Corporation. It provides a

brief introduction about the company and later on discusses the positive and negative impacts of

the company’s operations on society and environment. In the later part, it explains about the GRI

disclosures of the company and compares the quality and depth of its environmental performance

with BMW. The report also explains the reasons for the fact that the shareholders of Toyota will

not be benefitted with the GRI compliance of other motor companies. It will increase the

competition and influence them to a great extent. At the last, a conclusion has been provided

summarising all the findings of the report.

Executive summary

The report focuses on the environmental and social factors of Toyota Corporation. It provides a

brief introduction about the company and later on discusses the positive and negative impacts of

the company’s operations on society and environment. In the later part, it explains about the GRI

disclosures of the company and compares the quality and depth of its environmental performance

with BMW. The report also explains the reasons for the fact that the shareholders of Toyota will

not be benefitted with the GRI compliance of other motor companies. It will increase the

competition and influence them to a great extent. At the last, a conclusion has been provided

summarising all the findings of the report.

Financial and management accounting 3

Contents

Part A..........................................................................................................................................................4

Introduction.................................................................................................................................................4

Environmental and social impacts of Toyota’s operations...........................................................................4

Positive impacts.......................................................................................................................................5

Negative impacts.....................................................................................................................................6

Four key GRI disclosures............................................................................................................................6

Comparison of quality and depth.................................................................................................................8

Benefits to the shareholders from the compliance of GRI Reporting standards.........................................10

Conclusion.................................................................................................................................................11

Part B.........................................................................................................................................................11

Part C.........................................................................................................................................................15

References.................................................................................................................................................20

Contents

Part A..........................................................................................................................................................4

Introduction.................................................................................................................................................4

Environmental and social impacts of Toyota’s operations...........................................................................4

Positive impacts.......................................................................................................................................5

Negative impacts.....................................................................................................................................6

Four key GRI disclosures............................................................................................................................6

Comparison of quality and depth.................................................................................................................8

Benefits to the shareholders from the compliance of GRI Reporting standards.........................................10

Conclusion.................................................................................................................................................11

Part B.........................................................................................................................................................11

Part C.........................................................................................................................................................15

References.................................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and management accounting 4

Part A

Introduction

Toyota Motor Corporation is a Japan based multinational automotive company engaged in the

manufacturing of motor cars and vehicles. It was incorporated on 27 August 1937 having its

headquarters situated in Toyota, Aichi. Apart from automotive sector, the company also operates

in finance and other industries. It segments include automotive, financial services and others.

The company covers the market of North America, Japan, Asia and Europe in automobile sector.

It produces its automobile and other related parts through 50 overseas manufacturing companies

and in over 30 countries apart from Japan. As of 2017, the company has 364,445 employees and

was considered as the fifth largest company in terms of revenue. It has also been ranked second

in the list of largest automotive manufacturer. It is the largest listed company in Japan as per its

market capitalization and revenue. Toyota is also listed on London Stock Exchange and New

York Stock Exchange (Reuters. 2018).

This report focuses on the overall evaluation of company’s activities from environmental and

legal aspects. It covers the positive and negative impact of its operations along with the benefits

of GRI disclosures. It also compares the quality and depth of the environmental performance of

Toyota and BMW.

Environmental and social impacts of Toyota’s operations

Being the leading company in automotive sector, the company has a great responsibility towards

the society and environment. The manufacturing of automobiles affects the environment and

society to a great extent. The objective of Toyota is to carry out its activities by keeping two

Part A

Introduction

Toyota Motor Corporation is a Japan based multinational automotive company engaged in the

manufacturing of motor cars and vehicles. It was incorporated on 27 August 1937 having its

headquarters situated in Toyota, Aichi. Apart from automotive sector, the company also operates

in finance and other industries. It segments include automotive, financial services and others.

The company covers the market of North America, Japan, Asia and Europe in automobile sector.

It produces its automobile and other related parts through 50 overseas manufacturing companies

and in over 30 countries apart from Japan. As of 2017, the company has 364,445 employees and

was considered as the fifth largest company in terms of revenue. It has also been ranked second

in the list of largest automotive manufacturer. It is the largest listed company in Japan as per its

market capitalization and revenue. Toyota is also listed on London Stock Exchange and New

York Stock Exchange (Reuters. 2018).

This report focuses on the overall evaluation of company’s activities from environmental and

legal aspects. It covers the positive and negative impact of its operations along with the benefits

of GRI disclosures. It also compares the quality and depth of the environmental performance of

Toyota and BMW.

Environmental and social impacts of Toyota’s operations

Being the leading company in automotive sector, the company has a great responsibility towards

the society and environment. The manufacturing of automobiles affects the environment and

society to a great extent. The objective of Toyota is to carry out its activities by keeping two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and management accounting 5

things in mind which are customers and concern for the environment. However, despite working

with such objective, the manufacturing operations do left a positive and negative impact on the

society and the surroundings. All such impacts are been disclosed in the sustainability report of

the company and also the compliance with GRI disclosures act as the pioneers of environment

and assist in having better understanding about the social and environmental impact of business

activities.

Positive impacts

The following section explains in detail about the positive effects of Toyota’s manufacturing

activities on both the society and the concerned environment. They are as follows:

It has taken suitable measures and initiatives for the purpose of ownership and protection

of forest. The activities include ToyotoShirakawa-Go-Eco-Institute, Toyota

Environmental Activities Grant Program, Toyota Mie Miyagawa Forest Project and

Toyomori. Along with this, it has also conducted a Smart Eco Drive in countries like

Korea (Crane & Matten, 2016).

Showing the concern towards society, the company is involved in promoting the

development of human management and enhancing the living standards of the people. in

lieu of keeping a clean environment, it is addressing the safety of traffic by integrating

cars, traffic and people in order to avoid the traffic casualties as a whole.

Toyota also supports various programs related to dance and music in order to promote

local culture in the society and enhance the youth to be familiar with the society and

culture. The company is also involved in developing and expanding the social welfare

programs (Epstein, 2018).

things in mind which are customers and concern for the environment. However, despite working

with such objective, the manufacturing operations do left a positive and negative impact on the

society and the surroundings. All such impacts are been disclosed in the sustainability report of

the company and also the compliance with GRI disclosures act as the pioneers of environment

and assist in having better understanding about the social and environmental impact of business

activities.

Positive impacts

The following section explains in detail about the positive effects of Toyota’s manufacturing

activities on both the society and the concerned environment. They are as follows:

It has taken suitable measures and initiatives for the purpose of ownership and protection

of forest. The activities include ToyotoShirakawa-Go-Eco-Institute, Toyota

Environmental Activities Grant Program, Toyota Mie Miyagawa Forest Project and

Toyomori. Along with this, it has also conducted a Smart Eco Drive in countries like

Korea (Crane & Matten, 2016).

Showing the concern towards society, the company is involved in promoting the

development of human management and enhancing the living standards of the people. in

lieu of keeping a clean environment, it is addressing the safety of traffic by integrating

cars, traffic and people in order to avoid the traffic casualties as a whole.

Toyota also supports various programs related to dance and music in order to promote

local culture in the society and enhance the youth to be familiar with the society and

culture. The company is also involved in developing and expanding the social welfare

programs (Epstein, 2018).

Financial and management accounting 6

As per its sustainability report, there are 83 distributers and 4233 dealers across 80

countries who participated in the Dealer Environmental Risk Audit, conducted on global

level.

Negative impacts

Despite taking such positive measures, there are some operations also which have impacted the

society and environment negatively. They are as follows:

The manufacturing of motor vehicles involves the huge dependence and consumption of

fossil fuels that affect the environment severely. Such strong use of fuels leads to several

environmental problems among which the most common is pollution. Increasing content

of pollution in the air will eventually affect society to a great extent. It may cause

breathing problems, global warming and increase the demand of petrol and diesel.

Upsurge in prices of gasoline will surely impact the economy and result in environmental

problems (Globalreporting. 2016).

Increase in number of cars on land will results in congestions and hindered mobility.

Moreover, disposal of the same will increase the fleet and become more costly as

compare to landfill.

So, above discussed are some positive and negative effects of the operations and business

activities carried out by Toyota within its organizations.

Four key GRI disclosures

Global Reporting Initiative is an independent standards organization operating on international

level. It helps the government, organizations and businesses to understand the impacts of their

activities on climate change, human rights and corruption. GRI 102: General Disclosures deal

As per its sustainability report, there are 83 distributers and 4233 dealers across 80

countries who participated in the Dealer Environmental Risk Audit, conducted on global

level.

Negative impacts

Despite taking such positive measures, there are some operations also which have impacted the

society and environment negatively. They are as follows:

The manufacturing of motor vehicles involves the huge dependence and consumption of

fossil fuels that affect the environment severely. Such strong use of fuels leads to several

environmental problems among which the most common is pollution. Increasing content

of pollution in the air will eventually affect society to a great extent. It may cause

breathing problems, global warming and increase the demand of petrol and diesel.

Upsurge in prices of gasoline will surely impact the economy and result in environmental

problems (Globalreporting. 2016).

Increase in number of cars on land will results in congestions and hindered mobility.

Moreover, disposal of the same will increase the fleet and become more costly as

compare to landfill.

So, above discussed are some positive and negative effects of the operations and business

activities carried out by Toyota within its organizations.

Four key GRI disclosures

Global Reporting Initiative is an independent standards organization operating on international

level. It helps the government, organizations and businesses to understand the impacts of their

activities on climate change, human rights and corruption. GRI 102: General Disclosures deal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and management accounting 7

with the reporting of information containing profile of the company, strategies, ethics and

integrity, practises of stakeholder engagement and procedure of reporting.

The four key disclosures of GRI that are relevant to the shareholders or stakeholders of Toyota

are as follows:

Energy

Introducing the energy efficient products in the market will help the customers to select their

choice of cars and the one that best suits to their needs and preferences. Toyota uses fuels and

automotive powertrain diversification processes that results in attracting a lot of shareholders and

also enhance the economy of dominant market. Inclusion of products like hybrid vehicles and

full cycle vehicles allow the stakeholders to cover a huge market share (Haider & Kokubu,

2015).

Customer Health and Safety

Toyota also discloses that their human support functions helps in understanding the objectives

and promotes the safety of its customers and enhance their health management. Its products

provide health support and in a way encourage the stakeholders to take the advantage of same.

Effluents, emissions and waste

Toyota is focused on commencing its business by keeping in mind the various environment-

related polices. It clearly indicates that the company has properly followed all the GRI

Disclosures and has aligned to its reporting standards. The Disclosure 102-16 provides the details

about the standards, norms, principles and values. Toyota’s development of Zero emission

with the reporting of information containing profile of the company, strategies, ethics and

integrity, practises of stakeholder engagement and procedure of reporting.

The four key disclosures of GRI that are relevant to the shareholders or stakeholders of Toyota

are as follows:

Energy

Introducing the energy efficient products in the market will help the customers to select their

choice of cars and the one that best suits to their needs and preferences. Toyota uses fuels and

automotive powertrain diversification processes that results in attracting a lot of shareholders and

also enhance the economy of dominant market. Inclusion of products like hybrid vehicles and

full cycle vehicles allow the stakeholders to cover a huge market share (Haider & Kokubu,

2015).

Customer Health and Safety

Toyota also discloses that their human support functions helps in understanding the objectives

and promotes the safety of its customers and enhance their health management. Its products

provide health support and in a way encourage the stakeholders to take the advantage of same.

Effluents, emissions and waste

Toyota is focused on commencing its business by keeping in mind the various environment-

related polices. It clearly indicates that the company has properly followed all the GRI

Disclosures and has aligned to its reporting standards. The Disclosure 102-16 provides the details

about the standards, norms, principles and values. Toyota’s development of Zero emission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and management accounting 8

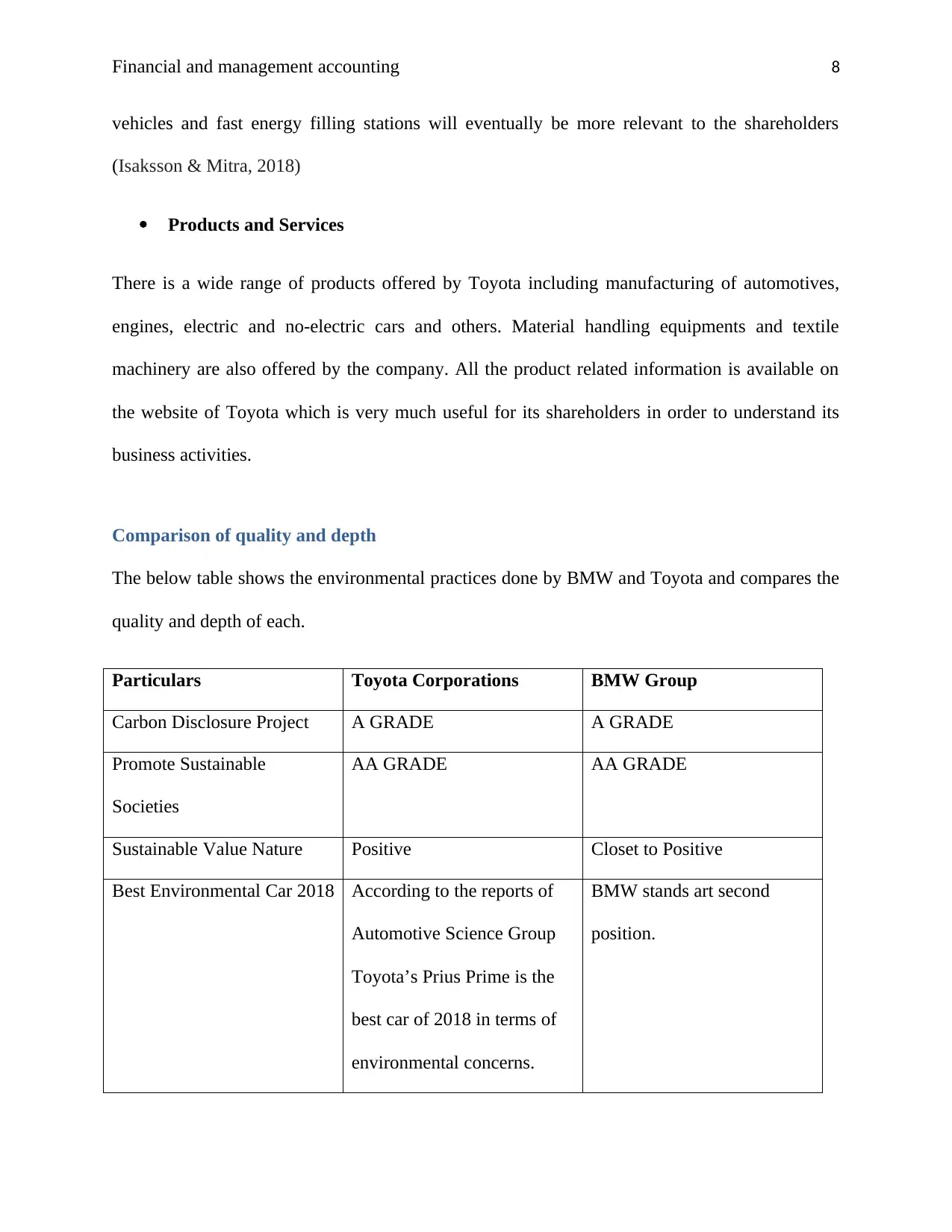

vehicles and fast energy filling stations will eventually be more relevant to the shareholders

(Isaksson & Mitra, 2018)

Products and Services

There is a wide range of products offered by Toyota including manufacturing of automotives,

engines, electric and no-electric cars and others. Material handling equipments and textile

machinery are also offered by the company. All the product related information is available on

the website of Toyota which is very much useful for its shareholders in order to understand its

business activities.

Comparison of quality and depth

The below table shows the environmental practices done by BMW and Toyota and compares the

quality and depth of each.

Particulars Toyota Corporations BMW Group

Carbon Disclosure Project A GRADE A GRADE

Promote Sustainable

Societies

AA GRADE AA GRADE

Sustainable Value Nature Positive Closet to Positive

Best Environmental Car 2018 According to the reports of

Automotive Science Group

Toyota’s Prius Prime is the

best car of 2018 in terms of

environmental concerns.

BMW stands art second

position.

vehicles and fast energy filling stations will eventually be more relevant to the shareholders

(Isaksson & Mitra, 2018)

Products and Services

There is a wide range of products offered by Toyota including manufacturing of automotives,

engines, electric and no-electric cars and others. Material handling equipments and textile

machinery are also offered by the company. All the product related information is available on

the website of Toyota which is very much useful for its shareholders in order to understand its

business activities.

Comparison of quality and depth

The below table shows the environmental practices done by BMW and Toyota and compares the

quality and depth of each.

Particulars Toyota Corporations BMW Group

Carbon Disclosure Project A GRADE A GRADE

Promote Sustainable

Societies

AA GRADE AA GRADE

Sustainable Value Nature Positive Closet to Positive

Best Environmental Car 2018 According to the reports of

Automotive Science Group

Toyota’s Prius Prime is the

best car of 2018 in terms of

environmental concerns.

BMW stands art second

position.

Financial and management accounting 9

CO2 Emissions The efficiency of Toyota

Prius increased to 56 MPG

and CO2-e emissions per

mile raised to 226 grams.

BMW reduces the CO2

emissions by 141 grams per

kilometre with its new

vehicle. Furthermore, the

company is providing

electricity free of CO2

(Globalreporting. 2016).

Initiatives Steps taken in respect of

rainforest restoration.

Campaigning done for

Toyota Traffic Safety.

Electronic Car

Cell Vehicles

Conducted programs

related to HIV and aids at

the workplace.

Created fast energy

stations.

Inzell Initiative

Strategy Adopted KAIZEN costing

system in its organization.

THUMS Model

development.

Eco Electrification

Make use of renewable

energy resources

Create a healthy working

environment for the

workers.

Increasing diversity.

CO2 Emissions The efficiency of Toyota

Prius increased to 56 MPG

and CO2-e emissions per

mile raised to 226 grams.

BMW reduces the CO2

emissions by 141 grams per

kilometre with its new

vehicle. Furthermore, the

company is providing

electricity free of CO2

(Globalreporting. 2016).

Initiatives Steps taken in respect of

rainforest restoration.

Campaigning done for

Toyota Traffic Safety.

Electronic Car

Cell Vehicles

Conducted programs

related to HIV and aids at

the workplace.

Created fast energy

stations.

Inzell Initiative

Strategy Adopted KAIZEN costing

system in its organization.

THUMS Model

development.

Eco Electrification

Make use of renewable

energy resources

Create a healthy working

environment for the

workers.

Increasing diversity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and management accounting 10

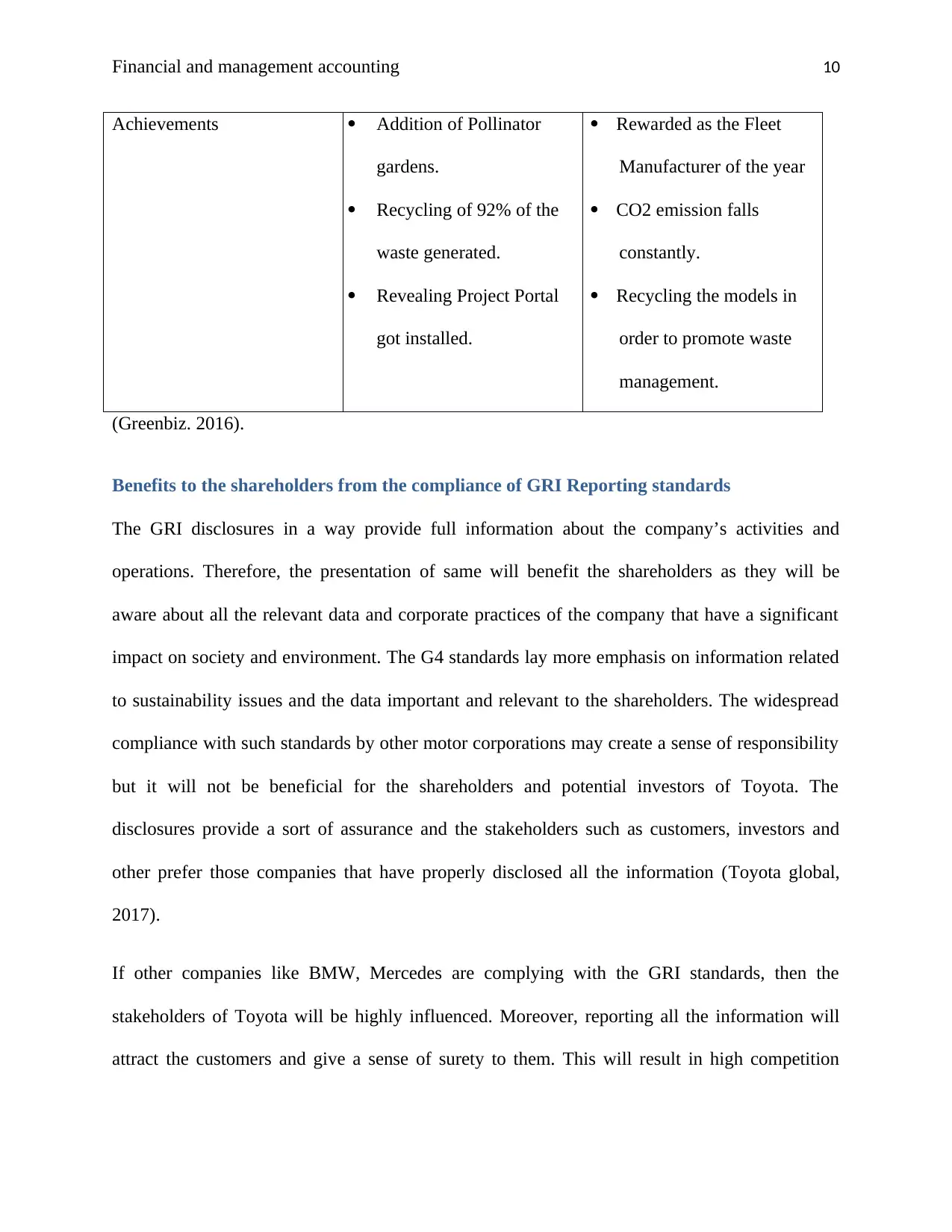

Achievements Addition of Pollinator

gardens.

Recycling of 92% of the

waste generated.

Revealing Project Portal

got installed.

Rewarded as the Fleet

Manufacturer of the year

CO2 emission falls

constantly.

Recycling the models in

order to promote waste

management.

(Greenbiz. 2016).

Benefits to the shareholders from the compliance of GRI Reporting standards

The GRI disclosures in a way provide full information about the company’s activities and

operations. Therefore, the presentation of same will benefit the shareholders as they will be

aware about all the relevant data and corporate practices of the company that have a significant

impact on society and environment. The G4 standards lay more emphasis on information related

to sustainability issues and the data important and relevant to the shareholders. The widespread

compliance with such standards by other motor corporations may create a sense of responsibility

but it will not be beneficial for the shareholders and potential investors of Toyota. The

disclosures provide a sort of assurance and the stakeholders such as customers, investors and

other prefer those companies that have properly disclosed all the information (Toyota global,

2017).

If other companies like BMW, Mercedes are complying with the GRI standards, then the

stakeholders of Toyota will be highly influenced. Moreover, reporting all the information will

attract the customers and give a sense of surety to them. This will result in high competition

Achievements Addition of Pollinator

gardens.

Recycling of 92% of the

waste generated.

Revealing Project Portal

got installed.

Rewarded as the Fleet

Manufacturer of the year

CO2 emission falls

constantly.

Recycling the models in

order to promote waste

management.

(Greenbiz. 2016).

Benefits to the shareholders from the compliance of GRI Reporting standards

The GRI disclosures in a way provide full information about the company’s activities and

operations. Therefore, the presentation of same will benefit the shareholders as they will be

aware about all the relevant data and corporate practices of the company that have a significant

impact on society and environment. The G4 standards lay more emphasis on information related

to sustainability issues and the data important and relevant to the shareholders. The widespread

compliance with such standards by other motor corporations may create a sense of responsibility

but it will not be beneficial for the shareholders and potential investors of Toyota. The

disclosures provide a sort of assurance and the stakeholders such as customers, investors and

other prefer those companies that have properly disclosed all the information (Toyota global,

2017).

If other companies like BMW, Mercedes are complying with the GRI standards, then the

stakeholders of Toyota will be highly influenced. Moreover, reporting all the information will

attract the customers and give a sense of surety to them. This will result in high competition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and management accounting 11

between Toyota and other corporations and will affect its stakeholders to a great extent

(Maginnis, Hapuwatte & Jawahir, 2017).

Conclusion

The above report concludes that the performance of Toyota was quite impressive from the

perspective of environment and society. The company is focused on creating positive impacts on

the surrounding s by adopting various initiatives. Moreover, it has made several achievements as

compare to BMW and has properly aligned with the GRI Standards.

Part B

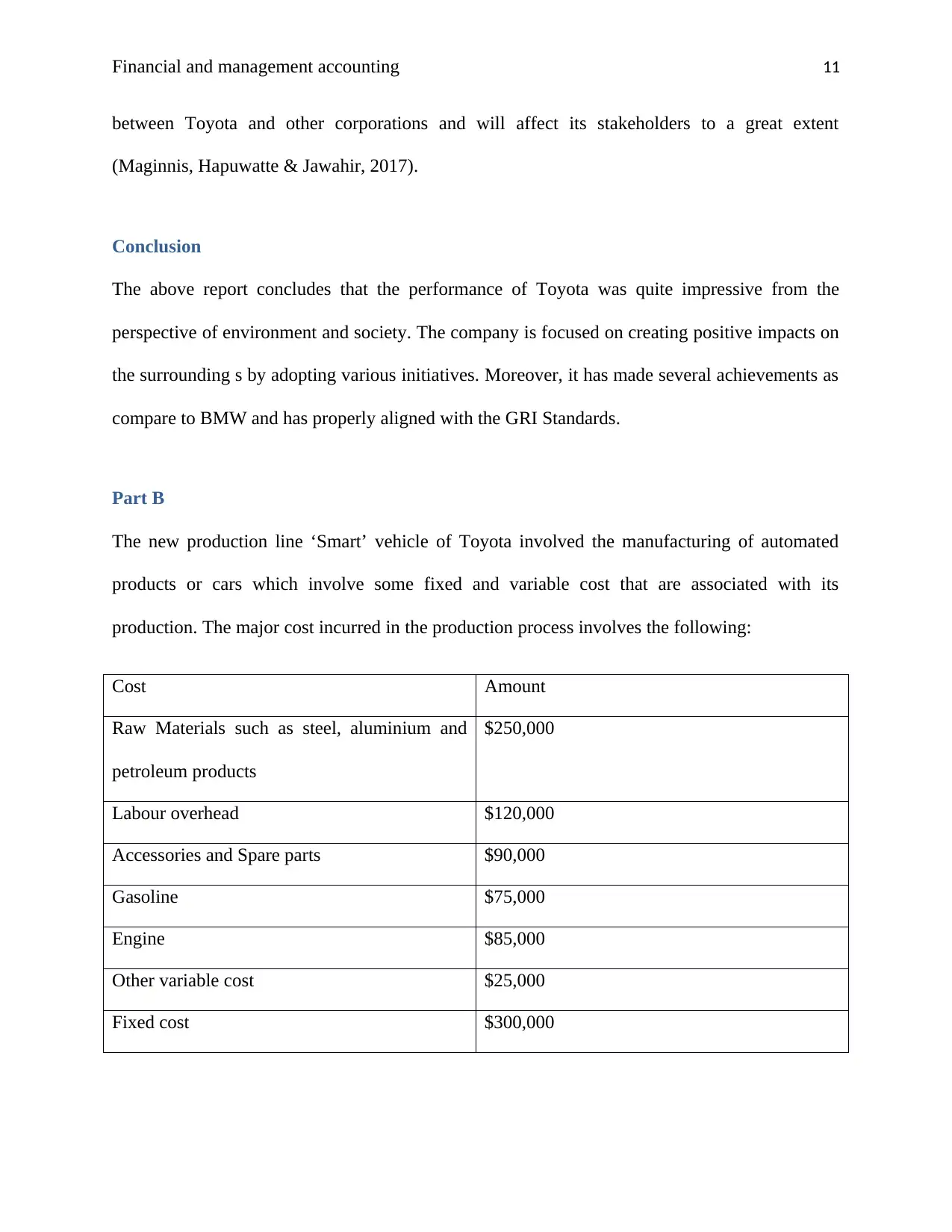

The new production line ‘Smart’ vehicle of Toyota involved the manufacturing of automated

products or cars which involve some fixed and variable cost that are associated with its

production. The major cost incurred in the production process involves the following:

Cost Amount

Raw Materials such as steel, aluminium and

petroleum products

$250,000

Labour overhead $120,000

Accessories and Spare parts $90,000

Gasoline $75,000

Engine $85,000

Other variable cost $25,000

Fixed cost $300,000

between Toyota and other corporations and will affect its stakeholders to a great extent

(Maginnis, Hapuwatte & Jawahir, 2017).

Conclusion

The above report concludes that the performance of Toyota was quite impressive from the

perspective of environment and society. The company is focused on creating positive impacts on

the surrounding s by adopting various initiatives. Moreover, it has made several achievements as

compare to BMW and has properly aligned with the GRI Standards.

Part B

The new production line ‘Smart’ vehicle of Toyota involved the manufacturing of automated

products or cars which involve some fixed and variable cost that are associated with its

production. The major cost incurred in the production process involves the following:

Cost Amount

Raw Materials such as steel, aluminium and

petroleum products

$250,000

Labour overhead $120,000

Accessories and Spare parts $90,000

Gasoline $75,000

Engine $85,000

Other variable cost $25,000

Fixed cost $300,000

Financial and management accounting 12

The cost incurred in the production and shown in the above table can be easily classified on the

basis of their cost behaviour. Fixed costs are generally the ones which do not change or fluctuate

according to the changes in company’s level of production. They remain same at all the levels

and in the production of automated smart vehicle; Toyota has incurred the cost of $300,000 as its

fixed cost.

Variable costs are the ones which change according to the level of production. In the above table

the cost which can be identified as variable are the raw materials such as aluminium, steel

products, labour required and the spare parts and other accessories needed for the production.

Products like Engine and Gasoline are treated as fixed cost (Lucey & Lucey, 2004).

Break even analysis is the concept which is very important for the companies to apply in their

business as it determines the targeted units required to be manufactured where the company earn

not profit and no loss. The manufacturing of the new product require some sort of fixed and

variable costs that are huge in amount. Therefore, it is very much necessary for the companies to

conduct a break even analysis in order to set their selling price and cater to the needs of

customers. BEP will let Toyota know about the targeted units of production and the company can

figure out how much cost is to be incurred on what number of units. It can easily set its revenue

targets in order to book high profits (Ahmed, 2015).

The balanced scorecard attached below explains lead and lag measures along with an objective

for the each perspective in relation to the new production line.

Balanced Score Card: Manufacturing of the Smart Car

Financial

Objectives Measures Initiatives

The cost incurred in the production and shown in the above table can be easily classified on the

basis of their cost behaviour. Fixed costs are generally the ones which do not change or fluctuate

according to the changes in company’s level of production. They remain same at all the levels

and in the production of automated smart vehicle; Toyota has incurred the cost of $300,000 as its

fixed cost.

Variable costs are the ones which change according to the level of production. In the above table

the cost which can be identified as variable are the raw materials such as aluminium, steel

products, labour required and the spare parts and other accessories needed for the production.

Products like Engine and Gasoline are treated as fixed cost (Lucey & Lucey, 2004).

Break even analysis is the concept which is very important for the companies to apply in their

business as it determines the targeted units required to be manufactured where the company earn

not profit and no loss. The manufacturing of the new product require some sort of fixed and

variable costs that are huge in amount. Therefore, it is very much necessary for the companies to

conduct a break even analysis in order to set their selling price and cater to the needs of

customers. BEP will let Toyota know about the targeted units of production and the company can

figure out how much cost is to be incurred on what number of units. It can easily set its revenue

targets in order to book high profits (Ahmed, 2015).

The balanced scorecard attached below explains lead and lag measures along with an objective

for the each perspective in relation to the new production line.

Balanced Score Card: Manufacturing of the Smart Car

Financial

Objectives Measures Initiatives

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.