Detailed Management Accounting Report for Toyota Plc Ltd

VerifiedAdded on 2020/07/23

|20

|5255

|55

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Toyota Plc Ltd. The introduction highlights the importance of management accounting in financial reporting, decision-making, and resource management. Task 1 defines management accounting, its functions (planning, organizing, controlling, and decision-making), and contrasts it with financial accounting. It explores essential accounting systems like cost accounting, inventory management, price optimization, lean accounting, and job costing, emphasizing their roles in monitoring and controlling business operations. Task 2 discusses various management accounting reporting methods, including performance reporting, inventory management, accounts receivable, job costing, and operating budget reports. Task 3 delves into different costing methods, such as standard costing, and their impact on net profitability. It also examines the benefits and limitations of planning tools and their role in resolving financial issues. Task 4 focuses on measures to resolve financial problems and evaluates the financial issues faced by Toyota Plc Ltd. The report concludes by summarizing the key findings and recommendations for improving management accounting practices within the company.

Management

and

Accounting

and

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system.....1

P2. Techniques of management accounting reporting methods..................................................3

M1: Benefits of accounting system.............................................................................................5

D1:Critical analysis of reporting system.....................................................................................5

TASK 2............................................................................................................................................5

P3. Different costing method to determine Net profitability......................................................5

M2: Evaluation of management accounting techniques.............................................................8

D2: Analysis of income statements.............................................................................................8

TASK 3............................................................................................................................................8

P4: Benefits and limitation of using planning tools....................................................................8

M3: Evaluation of planning tools..............................................................................................10

D3: Tools used for resolving financial issues...........................................................................10

TASK 4..........................................................................................................................................11

P5: Various measures to resolve financial problems................................................................11

M4: Evaluation of financial issues............................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................13

...................................................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system.....1

P2. Techniques of management accounting reporting methods..................................................3

M1: Benefits of accounting system.............................................................................................5

D1:Critical analysis of reporting system.....................................................................................5

TASK 2............................................................................................................................................5

P3. Different costing method to determine Net profitability......................................................5

M2: Evaluation of management accounting techniques.............................................................8

D2: Analysis of income statements.............................................................................................8

TASK 3............................................................................................................................................8

P4: Benefits and limitation of using planning tools....................................................................8

M3: Evaluation of planning tools..............................................................................................10

D3: Tools used for resolving financial issues...........................................................................10

TASK 4..........................................................................................................................................11

P5: Various measures to resolve financial problems................................................................11

M4: Evaluation of financial issues............................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................13

...................................................................................................................................................14

INTRODUCTION

Management Accounting is necessarily required in every business in order to manage and

control accounting reports and informations of business organisation which help them to know

their true and fair financial position of business. The manager of accounts and finance

department is held responsible to prepare financial reports using different accounting and

reporting system through which they get accurate and reliable result. The main motive of

preparing this report is to evaluate the importance of management accounting system in

formulating effective decision of an business operations of an organisation (Ahmad and

Kamilah. 2013). Using different planning tools and techniques by manager in order to resolve

financial issues are briefly discussed in this project report. This project also covers various

costing methods which help in analysing profitability of company. As mentioned in brief of this

report, Company named Toyota Plc Ltd which deals in auto mobile sector is selected for the

preparation of this report.

TASK 1

P1. Management accounting and essential requirements of its different accounting system

Definition of management accounting:

As per Management Accounting Practices Committee(MAPC) it refers to process of

identifying, measuring, preparing and interpreting the financial information which help

manager to formulate effective plan in order to ensure proper utilisation of resources.

As per Chartered Institute of Management Accountants(CIMA) it is considered as an

integral part of management which is related with identifying and interpreting financial

information in order to formulate strategy and effective decision making process.

Functions of Management accounting:

Planning: The manager need to formulate effective plan and strategy related to the

effective utilisation of resources while achieving desired goals and objectives within specified

time period.

Organising: It is a process of organising organisational structure and accordingly

delegate responsibilities to employees to achieve desired targets (Bodie, 2013). There are

different managers in different departments of an organisation and it is important to provide them

their roles and responsibilities with the help of which they perform in better way.

1

Management Accounting is necessarily required in every business in order to manage and

control accounting reports and informations of business organisation which help them to know

their true and fair financial position of business. The manager of accounts and finance

department is held responsible to prepare financial reports using different accounting and

reporting system through which they get accurate and reliable result. The main motive of

preparing this report is to evaluate the importance of management accounting system in

formulating effective decision of an business operations of an organisation (Ahmad and

Kamilah. 2013). Using different planning tools and techniques by manager in order to resolve

financial issues are briefly discussed in this project report. This project also covers various

costing methods which help in analysing profitability of company. As mentioned in brief of this

report, Company named Toyota Plc Ltd which deals in auto mobile sector is selected for the

preparation of this report.

TASK 1

P1. Management accounting and essential requirements of its different accounting system

Definition of management accounting:

As per Management Accounting Practices Committee(MAPC) it refers to process of

identifying, measuring, preparing and interpreting the financial information which help

manager to formulate effective plan in order to ensure proper utilisation of resources.

As per Chartered Institute of Management Accountants(CIMA) it is considered as an

integral part of management which is related with identifying and interpreting financial

information in order to formulate strategy and effective decision making process.

Functions of Management accounting:

Planning: The manager need to formulate effective plan and strategy related to the

effective utilisation of resources while achieving desired goals and objectives within specified

time period.

Organising: It is a process of organising organisational structure and accordingly

delegate responsibilities to employees to achieve desired targets (Bodie, 2013). There are

different managers in different departments of an organisation and it is important to provide them

their roles and responsibilities with the help of which they perform in better way.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Controlling: It is a process of identifying the deviations and problems that an

organisation faces during business process and therefore control such deviations in order to

achieve desired objectives (DRURY, 2013). The manager need to focus on controlling the

activities of misrepresentation's of data in order to get accurate and reliable result.

Decision-making: With the help of available resources the manager need to make

effective decision which help in motivating and directing employees to perform their delegated

task in an effective manner in order to achieve desired goals and objectives.

Difference between Management accounting and financial accounting:

Basis of Difference Management accounting Financial accounting

Main objective Its main aim is to manage and

control accounting reports and

information which help in

making effective decision to

achieve desired targets.

Its main aim is to provide

details to outside parties such

as creditors, investors etc.

which help them in taking

informed decision.

Regulatory Requirements Institutes such as CIMA,

ICWAI frame some standard

and guidelines to regulate

management activity.

It is essentially required for

company to follow company's

law and regulation

implemented and governed by

government.

Principles of governing There us no basis of preparing

management accounting.

With the help of Generally

Accepted Accounting

Principles(GAAP) financial

accounting statements are

prepared.

Perspective It has futuristic perspective. It has historic perspective.

Essential requirements of different accounting system:

To monitor and control business operation it is essentially required for manger of Toyota

Plc Ltd. to adopt various types of accounting systems:

2

organisation faces during business process and therefore control such deviations in order to

achieve desired objectives (DRURY, 2013). The manager need to focus on controlling the

activities of misrepresentation's of data in order to get accurate and reliable result.

Decision-making: With the help of available resources the manager need to make

effective decision which help in motivating and directing employees to perform their delegated

task in an effective manner in order to achieve desired goals and objectives.

Difference between Management accounting and financial accounting:

Basis of Difference Management accounting Financial accounting

Main objective Its main aim is to manage and

control accounting reports and

information which help in

making effective decision to

achieve desired targets.

Its main aim is to provide

details to outside parties such

as creditors, investors etc.

which help them in taking

informed decision.

Regulatory Requirements Institutes such as CIMA,

ICWAI frame some standard

and guidelines to regulate

management activity.

It is essentially required for

company to follow company's

law and regulation

implemented and governed by

government.

Principles of governing There us no basis of preparing

management accounting.

With the help of Generally

Accepted Accounting

Principles(GAAP) financial

accounting statements are

prepared.

Perspective It has futuristic perspective. It has historic perspective.

Essential requirements of different accounting system:

To monitor and control business operation it is essentially required for manger of Toyota

Plc Ltd. to adopt various types of accounting systems:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system: Its main motive is to control and minimise irrelevant cost

incurred in the manufacturing process and should focus on investing money in important areas of

department where they get more outcome. Therefore manager of Toyota company need to

effectively use cost accounting system in order to ascertain profitability and productivity of

company (Herzig and et. al., 2012). For example Using various cost such as normal, actual and

standard cost to analyse cost incurred in manufacturing process. Using this tool the manager can

control cost incurred in business operation of Toyota company through which they can provide

products at less cost to the targeted customers.

Inventory management system: With the help of this system the company reduces

inventory storage cost. The manager need to decide when to order stock and how much which

help them in minimising storage cost as well as help in eliminating any wastage or spoilage of

stock. The manager of Toyota company need to manage their inventory on regular basis and also

need to use ABC costing and stock turnover ratios in order to forecast the actual position of

inventory.

Price optimisation system: It is considered as an important tool used by company to set

the prices of their product that their customers can afford. It is done through mathematical

analysis in order to determine that how customers will react towards the prices of their products

and services. Therefore it is important of manager to set the effective price of their product

which can fulfil both customers and company's objectives. It is essentially required for company

to adopt this system through adding value to the product which attracts large number of

customers to purchase their product.

Lean accounting: This accounting system is used to change accounting and management

process of Toyota company that will help them in cacheing profitability. This techniques should

used by product engineers of Toyota company to know the cost accounting information which

help in taking effective decision about secondary materials (Kotas and Richardoutledge, 2014).

The main objective of this system is to engage employees in reducing cost and improvement

operations in order to achieve profitability of company.

Job costing system: It is a system used by company in order to gather information about

the cost incurred in the production process. It is considered as an efficient method which help

company to calculate material required in manufacturing process such as materials, labours and

overhead. This will help in evaluating profitability and help company in deciding whether they

3

incurred in the manufacturing process and should focus on investing money in important areas of

department where they get more outcome. Therefore manager of Toyota company need to

effectively use cost accounting system in order to ascertain profitability and productivity of

company (Herzig and et. al., 2012). For example Using various cost such as normal, actual and

standard cost to analyse cost incurred in manufacturing process. Using this tool the manager can

control cost incurred in business operation of Toyota company through which they can provide

products at less cost to the targeted customers.

Inventory management system: With the help of this system the company reduces

inventory storage cost. The manager need to decide when to order stock and how much which

help them in minimising storage cost as well as help in eliminating any wastage or spoilage of

stock. The manager of Toyota company need to manage their inventory on regular basis and also

need to use ABC costing and stock turnover ratios in order to forecast the actual position of

inventory.

Price optimisation system: It is considered as an important tool used by company to set

the prices of their product that their customers can afford. It is done through mathematical

analysis in order to determine that how customers will react towards the prices of their products

and services. Therefore it is important of manager to set the effective price of their product

which can fulfil both customers and company's objectives. It is essentially required for company

to adopt this system through adding value to the product which attracts large number of

customers to purchase their product.

Lean accounting: This accounting system is used to change accounting and management

process of Toyota company that will help them in cacheing profitability. This techniques should

used by product engineers of Toyota company to know the cost accounting information which

help in taking effective decision about secondary materials (Kotas and Richardoutledge, 2014).

The main objective of this system is to engage employees in reducing cost and improvement

operations in order to achieve profitability of company.

Job costing system: It is a system used by company in order to gather information about

the cost incurred in the production process. It is considered as an efficient method which help

company to calculate material required in manufacturing process such as materials, labours and

overhead. This will help in evaluating profitability and help company in deciding whether they

3

want to product that product or not. The gathered information helps company to assign cost to

manufacture a particular product.

P2. Techniques of management accounting reporting methods

Accounting reports contains material accounting information and data of Toyota

company which further help company in making effective decision (Nixon and Burns, 2012).

Such accounting reports include profit and loss statement, balance sheet and cash flow statement

which represent the true and accurate financial position of company. With the help of accounting

reports, investors has easily attracted towards the company and decided whether they want to

invest in particular company or not. Therefore it is important for manager of company to prepare

accounting reports to determine their exact demand and position of company. Through getting

accurate information the company able ton understand their actual position in competitive market

which help them in formulate effective plans and decision making to achieve future

sustainability and profitability (Quinn, 2014). Therefore it is necessarily required for accounting

manager to collect accurate and correct information and on the basis of which they can prepare

the reliable accounting reports. Ii is helpful in analysing and comparing the actual performance

with the standard performance of different departments of company which directly help in

achieving their desired goals and objectives. If the manager fail to collect true and accurate data

and information and show the wrong accounting reports to their investors and public then it will

damage the goodwill and reputation of company in competitive market world (Ward, 2012.

Therefore accounting reports represent the overall performance of company. Through accounting

reports the company can able to forecast their future sustainability and growth.

Types of reporting system:

Performance reporting system: The manager should prepared accounting reports

containing accurate and true information and data which shows the true and fair financial

performance of Toyota company. This will help company in analysing the performance of

employees as well as organisation during the accounting year.

Inventory management system: Its main objective is to manage and control inventories

through recording various material information about inventory position. There are various tools

such as Economic Order Quantity(EOQ), ABC costing and inventory turnover ratio which help

company to record their inventories in proper manner.

4

manufacture a particular product.

P2. Techniques of management accounting reporting methods

Accounting reports contains material accounting information and data of Toyota

company which further help company in making effective decision (Nixon and Burns, 2012).

Such accounting reports include profit and loss statement, balance sheet and cash flow statement

which represent the true and accurate financial position of company. With the help of accounting

reports, investors has easily attracted towards the company and decided whether they want to

invest in particular company or not. Therefore it is important for manager of company to prepare

accounting reports to determine their exact demand and position of company. Through getting

accurate information the company able ton understand their actual position in competitive market

which help them in formulate effective plans and decision making to achieve future

sustainability and profitability (Quinn, 2014). Therefore it is necessarily required for accounting

manager to collect accurate and correct information and on the basis of which they can prepare

the reliable accounting reports. Ii is helpful in analysing and comparing the actual performance

with the standard performance of different departments of company which directly help in

achieving their desired goals and objectives. If the manager fail to collect true and accurate data

and information and show the wrong accounting reports to their investors and public then it will

damage the goodwill and reputation of company in competitive market world (Ward, 2012.

Therefore accounting reports represent the overall performance of company. Through accounting

reports the company can able to forecast their future sustainability and growth.

Types of reporting system:

Performance reporting system: The manager should prepared accounting reports

containing accurate and true information and data which shows the true and fair financial

performance of Toyota company. This will help company in analysing the performance of

employees as well as organisation during the accounting year.

Inventory management system: Its main objective is to manage and control inventories

through recording various material information about inventory position. There are various tools

such as Economic Order Quantity(EOQ), ABC costing and inventory turnover ratio which help

company to record their inventories in proper manner.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivable report: This reports shows the receipt and payment made by

company. It will help company in knowing that to which party they want to make payment and

from which party they want to receive (Renz, 2016). This will help company to examine the total

time and amount that to be recovered in future from different clients of company..

Job costing report: This report indicates the total amount that to be incurred in

production process of goods and services during the accounting year. The manager need to

collect information about resources such as materiel, labour and overhead that to be used by

company while manufacturing their products.

Operating budget report: The manager need to use this system to obtain information

about the cost that to be incurred by company during one accounting year (ter Bogt and van

Helden, 2012). This will help company in estimating budget for the upcoming years which help

them in preventing shortage of funds situations through which they can get accurate and positive

result

M1: Benefits of accounting system

Job costing systems:

Advantages:

It helps management to assign cost to manufacture specific product after analysing the

outcomes received in future.

It improves the performance of different departments.

Inventory management system:

Advantages:

It ensures production department to get raw material used in production process on time

through which they can produce demanded products and meet customer's requirements.

It helps in minimising inventory cost due to storing required stock only in warehouses.

In order to control and analyse the financial statements of Toyota company the manager

need to use management accounting system such as price optimisation and inventory

management in order to achieve best possible outcomes. Through managing and evaluating

accounting reports and policies the company can easily achieve efficiency and profitability

which help them in attain desired goals within specified period of time (P. Tucker and D. Lowe,

2014).

5

company. It will help company in knowing that to which party they want to make payment and

from which party they want to receive (Renz, 2016). This will help company to examine the total

time and amount that to be recovered in future from different clients of company..

Job costing report: This report indicates the total amount that to be incurred in

production process of goods and services during the accounting year. The manager need to

collect information about resources such as materiel, labour and overhead that to be used by

company while manufacturing their products.

Operating budget report: The manager need to use this system to obtain information

about the cost that to be incurred by company during one accounting year (ter Bogt and van

Helden, 2012). This will help company in estimating budget for the upcoming years which help

them in preventing shortage of funds situations through which they can get accurate and positive

result

M1: Benefits of accounting system

Job costing systems:

Advantages:

It helps management to assign cost to manufacture specific product after analysing the

outcomes received in future.

It improves the performance of different departments.

Inventory management system:

Advantages:

It ensures production department to get raw material used in production process on time

through which they can produce demanded products and meet customer's requirements.

It helps in minimising inventory cost due to storing required stock only in warehouses.

In order to control and analyse the financial statements of Toyota company the manager

need to use management accounting system such as price optimisation and inventory

management in order to achieve best possible outcomes. Through managing and evaluating

accounting reports and policies the company can easily achieve efficiency and profitability

which help them in attain desired goals within specified period of time (P. Tucker and D. Lowe,

2014).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1:Critical analysis of reporting system

Types of reporting Integration with organisational process

Account receivable report It helps manager of Toyota to identify unpaid

debtors and take corrective measures to

recover unpaid amount from them.

Job cost report It helps in allocation of cost to produce specific

product which reduce the chances of wastage.

TASK 2

P3. Different costing method to determine Net profitability

Costing refers to expenses incurred in manufacturing products and services by the

company with the available resources. If the company focuses on adding features or enhance the

quality of its products then the company need to invest more amount which affect the

profitability as well as growth of company (Luft and Shields, 2010). Therefore in order to

manufacture product the company need to incur other costs such as normal, standard and actual

cost. These all such cost are related with cost of production. Manager of Toyota company should

target tom minimise cost with a motive of generating huge profits. Therefore manager need to

allocate and utilise resources in diffe4rent areas of department where the chances of getting

positive result will be high. In recent years the company prefer to use ABC costing which help

them in getting cost effective result. For Toyota company. Therefore in order to enhance

performance and productivity of company the manager need to use following costing methods in

an effective and efficient manner.

Marginal costing: It is the cost which is incurred by company to manufacture additional

unit with the same resources. Through prime cost the manager able to calculate marginal cost

incurred during production process. Its main part is that it avoids fixed cost (Cinquini and

Tenucci, 2010). This will help manager to obtain information about profits and sales of

company.

Absorption costing: It includes direct cost associated with production process such as

wages paid to workers to manufacture product or raw material which are used in manufacturing a

6

Types of reporting Integration with organisational process

Account receivable report It helps manager of Toyota to identify unpaid

debtors and take corrective measures to

recover unpaid amount from them.

Job cost report It helps in allocation of cost to produce specific

product which reduce the chances of wastage.

TASK 2

P3. Different costing method to determine Net profitability

Costing refers to expenses incurred in manufacturing products and services by the

company with the available resources. If the company focuses on adding features or enhance the

quality of its products then the company need to invest more amount which affect the

profitability as well as growth of company (Luft and Shields, 2010). Therefore in order to

manufacture product the company need to incur other costs such as normal, standard and actual

cost. These all such cost are related with cost of production. Manager of Toyota company should

target tom minimise cost with a motive of generating huge profits. Therefore manager need to

allocate and utilise resources in diffe4rent areas of department where the chances of getting

positive result will be high. In recent years the company prefer to use ABC costing which help

them in getting cost effective result. For Toyota company. Therefore in order to enhance

performance and productivity of company the manager need to use following costing methods in

an effective and efficient manner.

Marginal costing: It is the cost which is incurred by company to manufacture additional

unit with the same resources. Through prime cost the manager able to calculate marginal cost

incurred during production process. Its main part is that it avoids fixed cost (Cinquini and

Tenucci, 2010). This will help manager to obtain information about profits and sales of

company.

Absorption costing: It includes direct cost associated with production process such as

wages paid to workers to manufacture product or raw material which are used in manufacturing a

6

product and overhead cost which improves utility of product. In this costing fixed cost is used to

determine the bet profitability of company.

Difference between Absorption and marginal costing:

Marginal costing Absorption costing

It is used in making effective decision to

achieve desired targets.

It is used to prepared report for outside parties.

In this, variable are valued at variable cost of

production.

In this, the values of inventory are higher than

in absorption costing as compare to marginal

costing because inventories are valued are total

production cost.

It is considered as effective costing methods

which help manager to take future decision.

It is not effective while taking effective

decision.

Cost per unit remain same during production

level.

With the help of this costing method cost per

unit should decreases whereas cost of

production increases.

7

determine the bet profitability of company.

Difference between Absorption and marginal costing:

Marginal costing Absorption costing

It is used in making effective decision to

achieve desired targets.

It is used to prepared report for outside parties.

In this, variable are valued at variable cost of

production.

In this, the values of inventory are higher than

in absorption costing as compare to marginal

costing because inventories are valued are total

production cost.

It is considered as effective costing methods

which help manager to take future decision.

It is not effective while taking effective

decision.

Cost per unit remain same during production

level.

With the help of this costing method cost per

unit should decreases whereas cost of

production increases.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

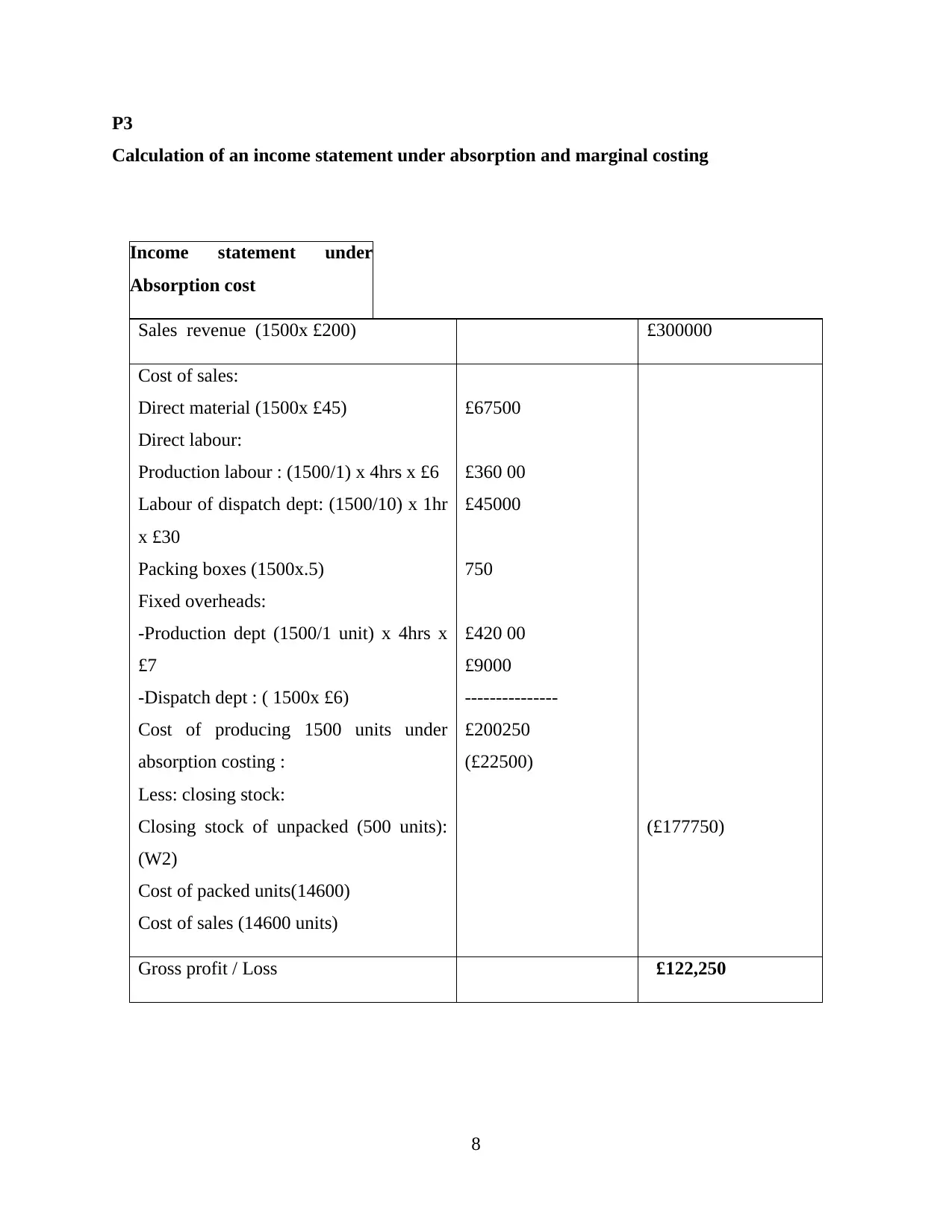

P3

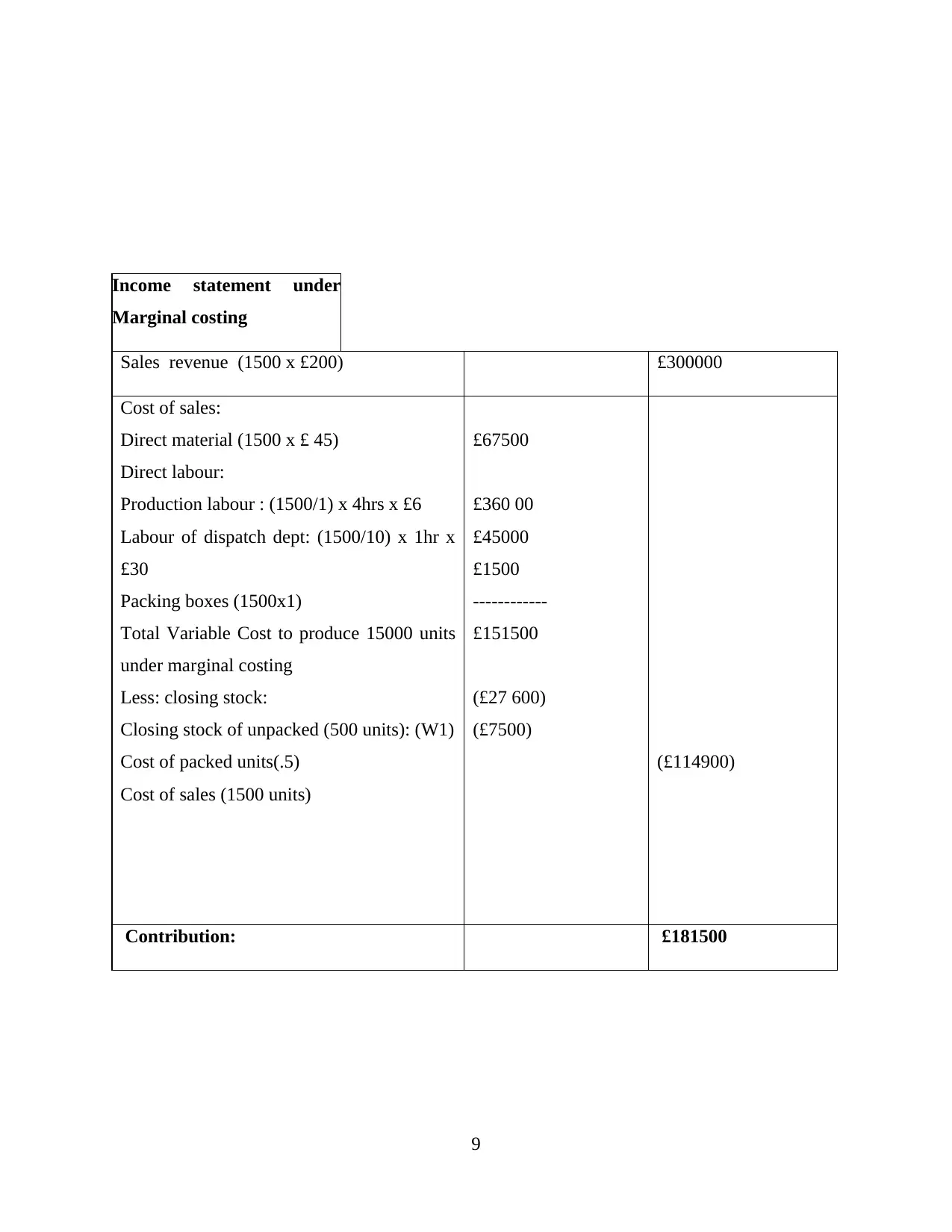

Calculation of an income statement under absorption and marginal costing

Income statement under

Absorption cost

Sales revenue (1500x £200) £300000

Cost of sales:

Direct material (1500x £45)

Direct labour:

Production labour : (1500/1) x 4hrs x £6

Labour of dispatch dept: (1500/10) x 1hr

x £30

Packing boxes (1500x.5)

Fixed overheads:

-Production dept (1500/1 unit) x 4hrs x

£7

-Dispatch dept : ( 1500x £6)

Cost of producing 1500 units under

absorption costing :

Less: closing stock:

Closing stock of unpacked (500 units):

(W2)

Cost of packed units(14600)

Cost of sales (14600 units)

£67500

£360 00

£45000

750

£420 00

£9000

---------------

£200250

(£22500)

(£177750)

Gross profit / Loss £122,250

8

Calculation of an income statement under absorption and marginal costing

Income statement under

Absorption cost

Sales revenue (1500x £200) £300000

Cost of sales:

Direct material (1500x £45)

Direct labour:

Production labour : (1500/1) x 4hrs x £6

Labour of dispatch dept: (1500/10) x 1hr

x £30

Packing boxes (1500x.5)

Fixed overheads:

-Production dept (1500/1 unit) x 4hrs x

£7

-Dispatch dept : ( 1500x £6)

Cost of producing 1500 units under

absorption costing :

Less: closing stock:

Closing stock of unpacked (500 units):

(W2)

Cost of packed units(14600)

Cost of sales (14600 units)

£67500

£360 00

£45000

750

£420 00

£9000

---------------

£200250

(£22500)

(£177750)

Gross profit / Loss £122,250

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement under

Marginal costing

Sales revenue (1500 x £200) £300000

Cost of sales:

Direct material (1500 x £ 45)

Direct labour:

Production labour : (1500/1) x 4hrs x £6

Labour of dispatch dept: (1500/10) x 1hr x

£30

Packing boxes (1500x1)

Total Variable Cost to produce 15000 units

under marginal costing

Less: closing stock:

Closing stock of unpacked (500 units): (W1)

Cost of packed units(.5)

Cost of sales (1500 units)

£67500

£360 00

£45000

£1500

------------

£151500

(£27 600)

(£7500)

(£114900)

Contribution: £181500

9

Marginal costing

Sales revenue (1500 x £200) £300000

Cost of sales:

Direct material (1500 x £ 45)

Direct labour:

Production labour : (1500/1) x 4hrs x £6

Labour of dispatch dept: (1500/10) x 1hr x

£30

Packing boxes (1500x1)

Total Variable Cost to produce 15000 units

under marginal costing

Less: closing stock:

Closing stock of unpacked (500 units): (W1)

Cost of packed units(.5)

Cost of sales (1500 units)

£67500

£360 00

£45000

£1500

------------

£151500

(£27 600)

(£7500)

(£114900)

Contribution: £181500

9

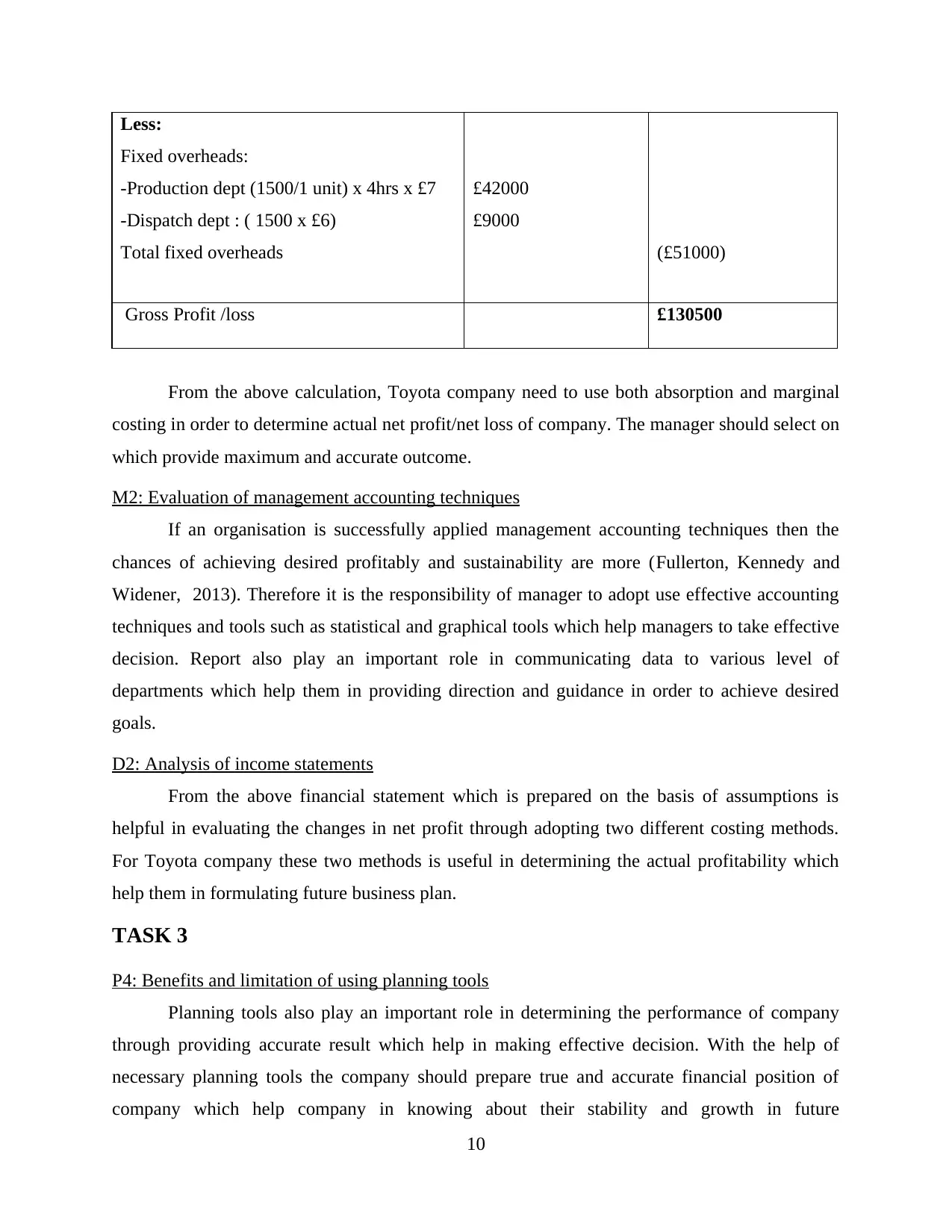

Less:

Fixed overheads:

-Production dept (1500/1 unit) x 4hrs x £7

-Dispatch dept : ( 1500 x £6)

Total fixed overheads

£42000

£9000

(£51000)

Gross Profit /loss £130500

From the above calculation, Toyota company need to use both absorption and marginal

costing in order to determine actual net profit/net loss of company. The manager should select on

which provide maximum and accurate outcome.

M2: Evaluation of management accounting techniques

If an organisation is successfully applied management accounting techniques then the

chances of achieving desired profitably and sustainability are more (Fullerton, Kennedy and

Widener, 2013). Therefore it is the responsibility of manager to adopt use effective accounting

techniques and tools such as statistical and graphical tools which help managers to take effective

decision. Report also play an important role in communicating data to various level of

departments which help them in providing direction and guidance in order to achieve desired

goals.

D2: Analysis of income statements

From the above financial statement which is prepared on the basis of assumptions is

helpful in evaluating the changes in net profit through adopting two different costing methods.

For Toyota company these two methods is useful in determining the actual profitability which

help them in formulating future business plan.

TASK 3

P4: Benefits and limitation of using planning tools

Planning tools also play an important role in determining the performance of company

through providing accurate result which help in making effective decision. With the help of

necessary planning tools the company should prepare true and accurate financial position of

company which help company in knowing about their stability and growth in future

10

Fixed overheads:

-Production dept (1500/1 unit) x 4hrs x £7

-Dispatch dept : ( 1500 x £6)

Total fixed overheads

£42000

£9000

(£51000)

Gross Profit /loss £130500

From the above calculation, Toyota company need to use both absorption and marginal

costing in order to determine actual net profit/net loss of company. The manager should select on

which provide maximum and accurate outcome.

M2: Evaluation of management accounting techniques

If an organisation is successfully applied management accounting techniques then the

chances of achieving desired profitably and sustainability are more (Fullerton, Kennedy and

Widener, 2013). Therefore it is the responsibility of manager to adopt use effective accounting

techniques and tools such as statistical and graphical tools which help managers to take effective

decision. Report also play an important role in communicating data to various level of

departments which help them in providing direction and guidance in order to achieve desired

goals.

D2: Analysis of income statements

From the above financial statement which is prepared on the basis of assumptions is

helpful in evaluating the changes in net profit through adopting two different costing methods.

For Toyota company these two methods is useful in determining the actual profitability which

help them in formulating future business plan.

TASK 3

P4: Benefits and limitation of using planning tools

Planning tools also play an important role in determining the performance of company

through providing accurate result which help in making effective decision. With the help of

necessary planning tools the company should prepare true and accurate financial position of

company which help company in knowing about their stability and growth in future

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.