Management Accounting Report: Toyota's Strategic Business Analysis

VerifiedAdded on 2020/06/03

|24

|6575

|1280

Report

AI Summary

This report delves into the realm of management accounting, using Toyota as a case study to illustrate key concepts and practical applications. It begins by defining management accounting and exploring various system types, including inventory, price optimization, and cost accounting systems. The report then examines different management accounting reporting methods such as inventory and manufacturing reports, budget reports, and job cost reports, highlighting their significance in monitoring organizational performance. It further analyzes income statements using marginal and absorption costing, and discusses different types of budgetary control, along with their advantages and disadvantages, in the context of Toyota. The report concludes by addressing the adaptation of management accounting systems to address financial problems, and evaluating the role of planning tools in preparing and forecasting budgets, ultimately showcasing how management accounting systems contribute to an organization's sustainable success. This report provides a detailed overview of management accounting practices and strategies, offering valuable insights into financial analysis and decision-making within a large multinational corporation.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting definition and different types of management accounting system

................................................................................................................................................1

P2 Various methods for management accounting reporting..................................................5

M1 Evaluating the benefits of management accounting systems and their application within an

organisational context.............................................................................................................8

D1 Assessing how management accounting systems and management accounting reporting is

integrated within organisational processes.............................................................................9

TASK 2............................................................................................................................................9

P3, M and M3 Income statements using marginal and absorption cost.................................9

TASK 3..........................................................................................................................................11

P4 Different types of budgetary control and their advantages & disadvantage in the Toyota11

TASK 4..........................................................................................................................................15

P5 Adapting the management accounting system for financial problems...........................15

M3 Analyzing the use of different planning tools and their application for preparing as well as

forecasting budgets...............................................................................................................17

M4 Presenting how management accounting systems lead organisation’s sustainable success

..............................................................................................................................................17

D3 Evaluating the manner in which planning tools help in responding or solving appropriately

to solving financial problems...............................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting definition and different types of management accounting system

................................................................................................................................................1

P2 Various methods for management accounting reporting..................................................5

M1 Evaluating the benefits of management accounting systems and their application within an

organisational context.............................................................................................................8

D1 Assessing how management accounting systems and management accounting reporting is

integrated within organisational processes.............................................................................9

TASK 2............................................................................................................................................9

P3, M and M3 Income statements using marginal and absorption cost.................................9

TASK 3..........................................................................................................................................11

P4 Different types of budgetary control and their advantages & disadvantage in the Toyota11

TASK 4..........................................................................................................................................15

P5 Adapting the management accounting system for financial problems...........................15

M3 Analyzing the use of different planning tools and their application for preparing as well as

forecasting budgets...............................................................................................................17

M4 Presenting how management accounting systems lead organisation’s sustainable success

..............................................................................................................................................17

D3 Evaluating the manner in which planning tools help in responding or solving appropriately

to solving financial problems...............................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management accounting is the process of identifying, measurement, analysing,

interpreting and communicating information for the pursuance of organisation's goals.

Management accounting cover each fields of accounting aimed at informing management of

enterprise operation metrics. The present report is based on Toyota company which is a Japanese

multinational automotive manufacture organisation in Japan. It is the world's largest and first

auto mobile manufacture company which produce more than 10 million vehicles per year. In this

report, explanation of management accounting and requirement of different types of management

accounting system are covered. Other than that, methods of management accounting report and

appropriate techniques of cost analysis are discussed. Along with this, in the report advantages

and disadvantage of the budgetary control and effective management accounting system are

covered.

TASK 1

P1 Management accounting definition and different types of management accounting system

Management accounting is a process of making report and accounts which provide the

accurate financial information. Through it, managers can take their daily basis decision at their

work place. Management accounting handle the margin analysis, the amount of profit or cash

flow generated by the sale from a particular goods, customers, and store. Management

accounting also known as managerial or cost accounting (Wijaya and Prihatiningtias, 2015). It

is different from financial accounting, because it produces reports of entire finance sector of the

company. Management accounting very useful process in the Toyota organisation, because they

need the different types of reports and it can be made by the only management accounting. There

are different types of management accounting system in the organisation, but Toyota company

should use some following management accounting system for their business:

1

Management accounting is the process of identifying, measurement, analysing,

interpreting and communicating information for the pursuance of organisation's goals.

Management accounting cover each fields of accounting aimed at informing management of

enterprise operation metrics. The present report is based on Toyota company which is a Japanese

multinational automotive manufacture organisation in Japan. It is the world's largest and first

auto mobile manufacture company which produce more than 10 million vehicles per year. In this

report, explanation of management accounting and requirement of different types of management

accounting system are covered. Other than that, methods of management accounting report and

appropriate techniques of cost analysis are discussed. Along with this, in the report advantages

and disadvantage of the budgetary control and effective management accounting system are

covered.

TASK 1

P1 Management accounting definition and different types of management accounting system

Management accounting is a process of making report and accounts which provide the

accurate financial information. Through it, managers can take their daily basis decision at their

work place. Management accounting handle the margin analysis, the amount of profit or cash

flow generated by the sale from a particular goods, customers, and store. Management

accounting also known as managerial or cost accounting (Wijaya and Prihatiningtias, 2015). It

is different from financial accounting, because it produces reports of entire finance sector of the

company. Management accounting very useful process in the Toyota organisation, because they

need the different types of reports and it can be made by the only management accounting. There

are different types of management accounting system in the organisation, but Toyota company

should use some following management accounting system for their business:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management system of Inventory: - It is very important management accounting system

in the company, because inventory management system is able to keep entire data and

information in safe place. However, it is very useful cost accounting system for the

Toyota organisation. Toyota is the biggest company In the world which is providing their

products and services In the entire world. If they are able to producing, selling and

promoting their products and services then they should use the inventory management

system in their business. Through this system, Toyota company can make lots of reports

which is very necessary for the business. Other than that, they can make a report of sales,

purchase, profit and loss, and balance sheet from the inventory system. It is very easy

process to keep entire data and information in very safe place. Along with this, if

company is not able to maintain their entire data in another system then they can use

2

Illustration 1: Management accounting definition

(Source : Management accounting definition, 2018)

in the company, because inventory management system is able to keep entire data and

information in safe place. However, it is very useful cost accounting system for the

Toyota organisation. Toyota is the biggest company In the world which is providing their

products and services In the entire world. If they are able to producing, selling and

promoting their products and services then they should use the inventory management

system in their business. Through this system, Toyota company can make lots of reports

which is very necessary for the business. Other than that, they can make a report of sales,

purchase, profit and loss, and balance sheet from the inventory system. It is very easy

process to keep entire data and information in very safe place. Along with this, if

company is not able to maintain their entire data in another system then they can use

2

Illustration 1: Management accounting definition

(Source : Management accounting definition, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory system, and they can safe their data in safe locations (Otley, 2016). Moreover,

Toyota company can track their data when they need it, so it can be easily tracked

anytime whenever requirement of the company. When company sale their products, they

should have to mention their sale in the inventory system,so managers can able to

evaluate of profit and loss through the inventory management system.

Price optimising management system: - It is the mathematical analysis for know the

response of the all customers. Through price optimising management system, manager

can know the response and satisfaction of the entire customers. Customers can respond

for the different prices of the products and services of the Toyota company. In this

organisation, they are selling lots of cars and it all have different price and features. So it

is very important to know that how customers will respond to different prices for their

products and services through different stores. This management system utilizes analysis

of large data to product the behaviour of potential buyers to different prices. Toyota

company can use their management system in their business, and know the respond of the

customers (Management accounting, 2018). Other than that, if they will use price

optimising management system in their business, then they will be able to collect big data

of the customers who are responding for their different prices of different products and

services.

Cost accounting system,: - One of the important management system is the cost

accounting system in the Toyota company. They can use this management system in their

organisation. It is also known as products costing system and costing system. Toyota

group can use this system for identity the cost of their products for profitability analysis.

Other than that, they can analysis of the entire cost of the goods and services then they

can control the expenses which is not beneficial for the company. There are two main

cost accounting system which can be used by the Toyota company (Cooper and Qu,

2017). First one is job order costing which is a cost accounting system that accumulated

manufacturing cost separately for each job. Second one is process costing which is cost

accounting that calculate manufacturing cost separately for each process.

Job costing system: - It is also the very useful accounting system in the Toyota company.

Through it, they can track the cost and revenues by job and enables standardized

3

Toyota company can track their data when they need it, so it can be easily tracked

anytime whenever requirement of the company. When company sale their products, they

should have to mention their sale in the inventory system,so managers can able to

evaluate of profit and loss through the inventory management system.

Price optimising management system: - It is the mathematical analysis for know the

response of the all customers. Through price optimising management system, manager

can know the response and satisfaction of the entire customers. Customers can respond

for the different prices of the products and services of the Toyota company. In this

organisation, they are selling lots of cars and it all have different price and features. So it

is very important to know that how customers will respond to different prices for their

products and services through different stores. This management system utilizes analysis

of large data to product the behaviour of potential buyers to different prices. Toyota

company can use their management system in their business, and know the respond of the

customers (Management accounting, 2018). Other than that, if they will use price

optimising management system in their business, then they will be able to collect big data

of the customers who are responding for their different prices of different products and

services.

Cost accounting system,: - One of the important management system is the cost

accounting system in the Toyota company. They can use this management system in their

organisation. It is also known as products costing system and costing system. Toyota

group can use this system for identity the cost of their products for profitability analysis.

Other than that, they can analysis of the entire cost of the goods and services then they

can control the expenses which is not beneficial for the company. There are two main

cost accounting system which can be used by the Toyota company (Cooper and Qu,

2017). First one is job order costing which is a cost accounting system that accumulated

manufacturing cost separately for each job. Second one is process costing which is cost

accounting that calculate manufacturing cost separately for each process.

Job costing system: - It is also the very useful accounting system in the Toyota company.

Through it, they can track the cost and revenues by job and enables standardized

3

reporting of the profitability. This accounting system is very important in the Toyota,

because it will know them a productivity of the entire employees. Other than that, they

can identity the cost and revenues by job. In the company, there are number of employees

and department work together, but they can not able to know the cost of their job.

However, job costing system is a process to identify the cost of each job and process of

the company. This management accounting system involves the material, labour, and

overhead in their accounts activities. Along with this, job costing system can track the

particular cost of the individual job. Through job costing system, company can

accumulate the cost of component and then assigns these costs to a good or project once

the components are used. Other than that, they can evaluate the productivity of the labour

and employees (Lorenz, 2015). This is the effective management accounting system

which is providing the accurate data of the job costing to the Toyota company.

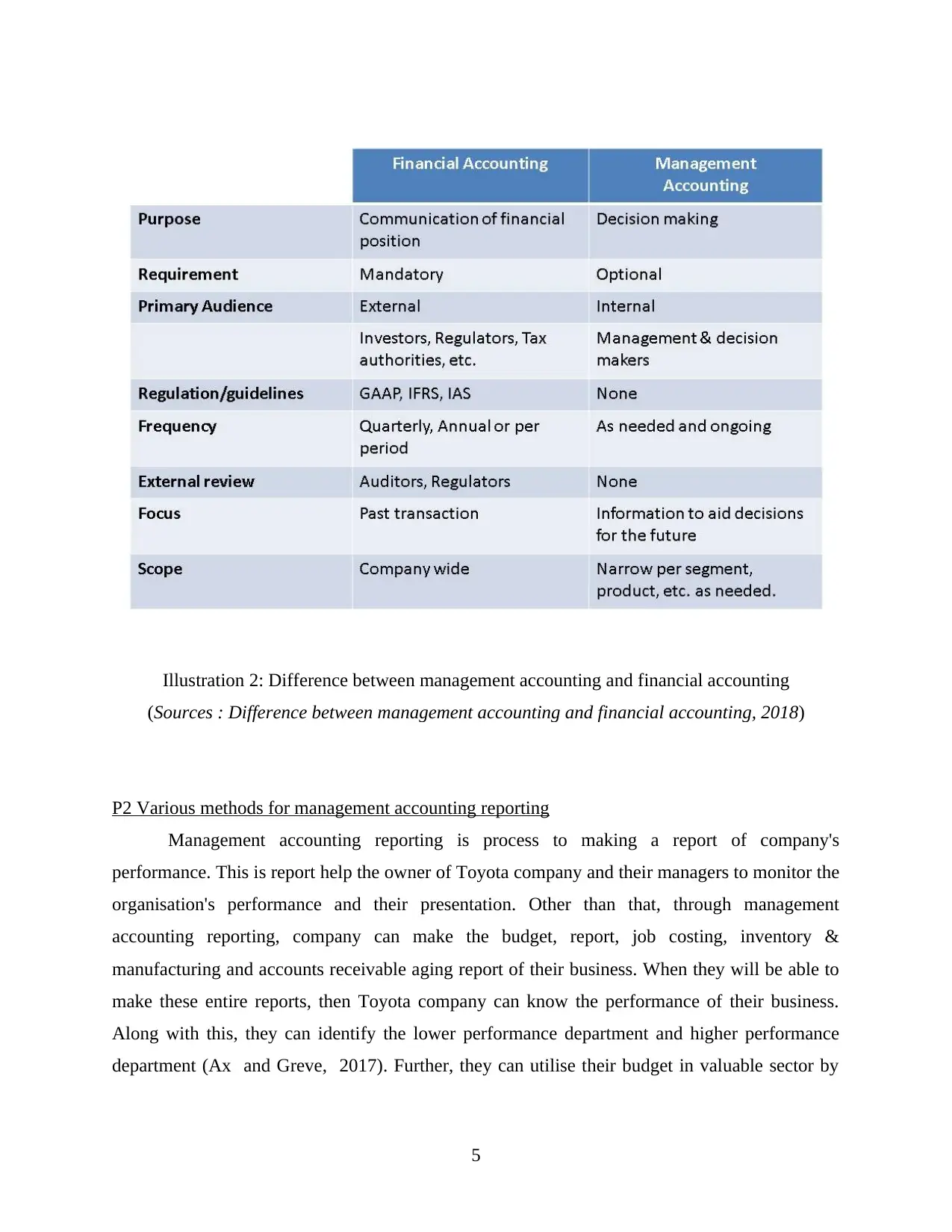

Difference between management accounting and financial accounting: -

Efficiency: - Financial report is based on the profitability of the business and

management accounting is based on the particular problems and their effective solution in

the business.

Focus of the reporting: - Financial accounting provide the report of financial statement,

and management accounting provide the reports of entire operations work within the

company (Lavia López and Hiebl, 2014).

Time period: - Management accounting may address budgets and forecast, so it have

future orientation. Financial accounting is concerned with the financial results that a

enterprise has already achieved, so it has historical orientation.

Valuation: - Financial accounting provide the proper valuation of the assets and liabilities

of the company and management accounting provide only the productivity of the

business. It is not provide the vale of the assets and any liabilities In the business.

4

because it will know them a productivity of the entire employees. Other than that, they

can identity the cost and revenues by job. In the company, there are number of employees

and department work together, but they can not able to know the cost of their job.

However, job costing system is a process to identify the cost of each job and process of

the company. This management accounting system involves the material, labour, and

overhead in their accounts activities. Along with this, job costing system can track the

particular cost of the individual job. Through job costing system, company can

accumulate the cost of component and then assigns these costs to a good or project once

the components are used. Other than that, they can evaluate the productivity of the labour

and employees (Lorenz, 2015). This is the effective management accounting system

which is providing the accurate data of the job costing to the Toyota company.

Difference between management accounting and financial accounting: -

Efficiency: - Financial report is based on the profitability of the business and

management accounting is based on the particular problems and their effective solution in

the business.

Focus of the reporting: - Financial accounting provide the report of financial statement,

and management accounting provide the reports of entire operations work within the

company (Lavia López and Hiebl, 2014).

Time period: - Management accounting may address budgets and forecast, so it have

future orientation. Financial accounting is concerned with the financial results that a

enterprise has already achieved, so it has historical orientation.

Valuation: - Financial accounting provide the proper valuation of the assets and liabilities

of the company and management accounting provide only the productivity of the

business. It is not provide the vale of the assets and any liabilities In the business.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2 Various methods for management accounting reporting

Management accounting reporting is process to making a report of company's

performance. This is report help the owner of Toyota company and their managers to monitor the

organisation's performance and their presentation. Other than that, through management

accounting reporting, company can make the budget, report, job costing, inventory &

manufacturing and accounts receivable aging report of their business. When they will be able to

make these entire reports, then Toyota company can know the performance of their business.

Along with this, they can identify the lower performance department and higher performance

department (Ax and Greve, 2017). Further, they can utilise their budget in valuable sector by

5

Illustration 2: Difference between management accounting and financial accounting

(Sources : Difference between management accounting and financial accounting, 2018)

Management accounting reporting is process to making a report of company's

performance. This is report help the owner of Toyota company and their managers to monitor the

organisation's performance and their presentation. Other than that, through management

accounting reporting, company can make the budget, report, job costing, inventory &

manufacturing and accounts receivable aging report of their business. When they will be able to

make these entire reports, then Toyota company can know the performance of their business.

Along with this, they can identify the lower performance department and higher performance

department (Ax and Greve, 2017). Further, they can utilise their budget in valuable sector by

5

Illustration 2: Difference between management accounting and financial accounting

(Sources : Difference between management accounting and financial accounting, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

using the methods of management accounting reporting. There are several different kinds of

management accounting reports company should develop regularly:

Inventory and manufacturing report: - There are number of products and services is

providing by the Toyota auto mobile company. They are selling the vehicles in the entire

market and in order to increase their sale, they are producing the lot of products from the

manufacture unit. When they produce the products, they should use the inventory account

system and then they can make a report of inventory in their business. It is very useful

and effective report which can be made by the Toyota organisation for their enterprise.

There are selling the products, and purchasing the raw materials from outside, and it is

necessary to keep the all information and data in very safe place. Inventory and

manufacture report help them in saving their data and information in the software. Other

than that, they can use this method of management accounting report, and able to increase

their profitability and brand value in the market. It is very important process in the

organisation for their business (Tucker and Lowe, 2014). Through it they can maintain

their all data and information in inventory and manufacture report. Whenever they need

the data, they can track the all report from the inventory and management report.

Budget report: -In the Toyota organisation different types of department and employee

are working and company allotted to different types of task to them. There are number of

employees who are not able to give their effective performance to the company, so they

can analysis about lower performance employee and can take action against them. There

are large number of employees who are giving their effective performance so company

can provide them incentives or bonuses for their good work. Other than that, thorough

this budget report, they can make a report of the productivity of the employees and

department, then they can analysis that, which department is giving their best at their

work place. Further, they can increase their budget on the higher performance of the

department. This entire process can be used by the budget report. This report help

company in increasing their profitability and brand value in the market. So Toyota

company should use the management accounting report and make the budget report of

their business (Van der Stede, 2016).

6

management accounting reports company should develop regularly:

Inventory and manufacturing report: - There are number of products and services is

providing by the Toyota auto mobile company. They are selling the vehicles in the entire

market and in order to increase their sale, they are producing the lot of products from the

manufacture unit. When they produce the products, they should use the inventory account

system and then they can make a report of inventory in their business. It is very useful

and effective report which can be made by the Toyota organisation for their enterprise.

There are selling the products, and purchasing the raw materials from outside, and it is

necessary to keep the all information and data in very safe place. Inventory and

manufacture report help them in saving their data and information in the software. Other

than that, they can use this method of management accounting report, and able to increase

their profitability and brand value in the market. It is very important process in the

organisation for their business (Tucker and Lowe, 2014). Through it they can maintain

their all data and information in inventory and manufacture report. Whenever they need

the data, they can track the all report from the inventory and management report.

Budget report: -In the Toyota organisation different types of department and employee

are working and company allotted to different types of task to them. There are number of

employees who are not able to give their effective performance to the company, so they

can analysis about lower performance employee and can take action against them. There

are large number of employees who are giving their effective performance so company

can provide them incentives or bonuses for their good work. Other than that, thorough

this budget report, they can make a report of the productivity of the employees and

department, then they can analysis that, which department is giving their best at their

work place. Further, they can increase their budget on the higher performance of the

department. This entire process can be used by the budget report. This report help

company in increasing their profitability and brand value in the market. So Toyota

company should use the management accounting report and make the budget report of

their business (Van der Stede, 2016).

6

Job cost report: - This report identify the all expenses for a particular project and job. In

this report, company can identify the productivity of the employees, labour and

departments. Other than that, they can examined about the profitability sector of the

Toyota company. There are numbers of department in the organisation, but that all are

not able to provide their performance to the company, so Toyota organisation can take

action against the lower performance department. Along with this, they can know the

reason and then provide them solution. When they know that their employees has not

abilities and skills for any of the task, then they can arrange the training session and

development program for the employees, labour and managers. Through it, they will be

able to get appropriate knowledge, information, skills and ability. When this all effective

thing got by the employees, then they are able to work at their place. Other than that.,

they can able to give their better performance to the company, so they can able to provide

their budget in the departments. Along with this, in this report company mention all about

the job costing and their outcomes. When they get the employees who are giving their

effective performance to the company, then managers can provide them incentives and

bonuses for their good job (Kotas, 2014). So, Toyota company should use the

management accounting reporting and in this system they can make report of job costing.

Through this report company can increase their productivity of the employees and

profitability. Along with this, this report shows them all expense which done by the

organisation for their department. Further, they can reduce their expenses on the lower

performance department. However, company can increase their brad value ad

profitability from the management accounting reporting.

Accounts receivable aging: - This is the critical tool for the managing cash flow of the

Toyota company. This report is based on the credit which given by the company to their

customers. Toyota company provide their products to the their customers, and they are

providing some credit services to them by instalment payment services. There are

numbers of customers who are paying their outstanding amount or instalment on the time,

but some customers are not able to paying their outstanding amount on time. When

company identify about that types of customers, then they will give them notice on first

due payment. Further, customers are not able to pay their pending amount or instalment

then company send them a notice and then warning that if they are not able to pay their

7

this report, company can identify the productivity of the employees, labour and

departments. Other than that, they can examined about the profitability sector of the

Toyota company. There are numbers of department in the organisation, but that all are

not able to provide their performance to the company, so Toyota organisation can take

action against the lower performance department. Along with this, they can know the

reason and then provide them solution. When they know that their employees has not

abilities and skills for any of the task, then they can arrange the training session and

development program for the employees, labour and managers. Through it, they will be

able to get appropriate knowledge, information, skills and ability. When this all effective

thing got by the employees, then they are able to work at their place. Other than that.,

they can able to give their better performance to the company, so they can able to provide

their budget in the departments. Along with this, in this report company mention all about

the job costing and their outcomes. When they get the employees who are giving their

effective performance to the company, then managers can provide them incentives and

bonuses for their good job (Kotas, 2014). So, Toyota company should use the

management accounting reporting and in this system they can make report of job costing.

Through this report company can increase their productivity of the employees and

profitability. Along with this, this report shows them all expense which done by the

organisation for their department. Further, they can reduce their expenses on the lower

performance department. However, company can increase their brad value ad

profitability from the management accounting reporting.

Accounts receivable aging: - This is the critical tool for the managing cash flow of the

Toyota company. This report is based on the credit which given by the company to their

customers. Toyota company provide their products to the their customers, and they are

providing some credit services to them by instalment payment services. There are

numbers of customers who are paying their outstanding amount or instalment on the time,

but some customers are not able to paying their outstanding amount on time. When

company identify about that types of customers, then they will give them notice on first

due payment. Further, customers are not able to pay their pending amount or instalment

then company send them a notice and then warning that if they are not able to pay their

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount then company can take some serious action against them. This report show the

entire customers who are not paying their instalment on time , so Toyota company can

take an action against them. Organisation provide the cars and many more products to the

customers in instalment services. This services is very valuable for the customers, but

some time they are not able to pay their instalment on time (Lopez-Valeiras and

Naranjo-Gil, 2015). It is very critical for the customers and company. In that condition,

they both can lose their relationship with one another. Through this report company can

increase their profitability from getting the outstanding amount from the customers.

When Toyota company will use this management accounting reporting, then they will

able to make all reports which are mentioned above. Through these reports, they can able to

identify about the expenses, credit services, outstanding amount of the customers, budget, and

job costing. If they will be able to know about these things, then they can able to make an

appropriate planing for the system. Other than that, through these management accounting

reporting they can follow the entire rules and regulation of the reporting system for getting the

effective result from the business. So, Toyota company should use these management accounting

reporting in their business, so they will get the better result fro this system.

M1 Evaluating the benefits of management accounting systems and their application within an

organisational context

Cost accounting

Advantages Disadvantages

Manager of Toyota can avoid wastage,

loss and inefficiencies using the system

of cost accounting

Assists in reducing cost and enhancing

profit margin

Gives input for assessing reasons take

place behind profit or loss

The main concern of the firm is to take

suitable decisions about future aspects,

whereas such accounting system

provides information about past

performance.

In the case of partial capacity

utilization such system does not present

suitable solution.

Job costing

8

entire customers who are not paying their instalment on time , so Toyota company can

take an action against them. Organisation provide the cars and many more products to the

customers in instalment services. This services is very valuable for the customers, but

some time they are not able to pay their instalment on time (Lopez-Valeiras and

Naranjo-Gil, 2015). It is very critical for the customers and company. In that condition,

they both can lose their relationship with one another. Through this report company can

increase their profitability from getting the outstanding amount from the customers.

When Toyota company will use this management accounting reporting, then they will

able to make all reports which are mentioned above. Through these reports, they can able to

identify about the expenses, credit services, outstanding amount of the customers, budget, and

job costing. If they will be able to know about these things, then they can able to make an

appropriate planing for the system. Other than that, through these management accounting

reporting they can follow the entire rules and regulation of the reporting system for getting the

effective result from the business. So, Toyota company should use these management accounting

reporting in their business, so they will get the better result fro this system.

M1 Evaluating the benefits of management accounting systems and their application within an

organisational context

Cost accounting

Advantages Disadvantages

Manager of Toyota can avoid wastage,

loss and inefficiencies using the system

of cost accounting

Assists in reducing cost and enhancing

profit margin

Gives input for assessing reasons take

place behind profit or loss

The main concern of the firm is to take

suitable decisions about future aspects,

whereas such accounting system

provides information about past

performance.

In the case of partial capacity

utilization such system does not present

suitable solution.

Job costing

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages Disadvantages

Facilitates cost estimation on the basis

of past records

Helps in assessing cost at every stage

of job completion

Requires more clerical work

Lack of possibility in relation to

controlling cost

D1 Assessing how management accounting systems and management accounting reporting is

integrated within organisational processes

From assessment, it has identified that systems of management accounting is highly

integrated with the process and functions of an organization. Using managerial accounting

systems manager of Toyota can set price and become able to take suitable decision about

inventory management, cost control as well as profit enhancement. Thus, using managerial

accounting systems Toyota’s manager can improve organizational process and thereby attain

goals.

TASK 2

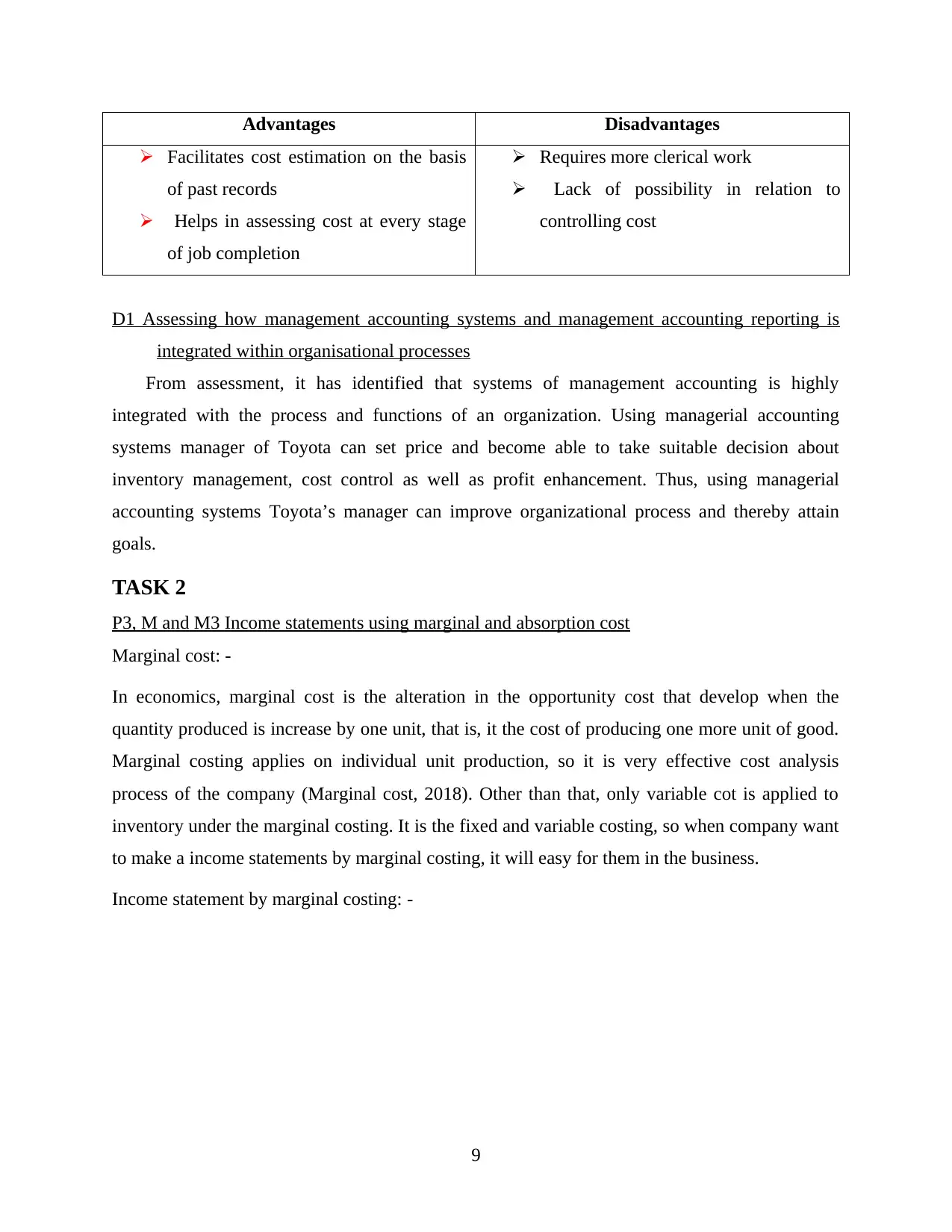

P3, M and M3 Income statements using marginal and absorption cost

Marginal cost: -

In economics, marginal cost is the alteration in the opportunity cost that develop when the

quantity produced is increase by one unit, that is, it the cost of producing one more unit of good.

Marginal costing applies on individual unit production, so it is very effective cost analysis

process of the company (Marginal cost, 2018). Other than that, only variable cot is applied to

inventory under the marginal costing. It is the fixed and variable costing, so when company want

to make a income statements by marginal costing, it will easy for them in the business.

Income statement by marginal costing: -

9

Facilitates cost estimation on the basis

of past records

Helps in assessing cost at every stage

of job completion

Requires more clerical work

Lack of possibility in relation to

controlling cost

D1 Assessing how management accounting systems and management accounting reporting is

integrated within organisational processes

From assessment, it has identified that systems of management accounting is highly

integrated with the process and functions of an organization. Using managerial accounting

systems manager of Toyota can set price and become able to take suitable decision about

inventory management, cost control as well as profit enhancement. Thus, using managerial

accounting systems Toyota’s manager can improve organizational process and thereby attain

goals.

TASK 2

P3, M and M3 Income statements using marginal and absorption cost

Marginal cost: -

In economics, marginal cost is the alteration in the opportunity cost that develop when the

quantity produced is increase by one unit, that is, it the cost of producing one more unit of good.

Marginal costing applies on individual unit production, so it is very effective cost analysis

process of the company (Marginal cost, 2018). Other than that, only variable cot is applied to

inventory under the marginal costing. It is the fixed and variable costing, so when company want

to make a income statements by marginal costing, it will easy for them in the business.

Income statement by marginal costing: -

9

Absorption cost: -

There are different types companies who are using absorption costing to make a income

statements. Toyota company should use this system for their income statements, because it is

very useful and effective cost system in the business. Other than that, absorption costing applies

on all production costs to all units produced. Only fixed overhead costs re applied under the

absorption costing. Along with this, profitability will appear to be lower in the absorption costing

and this costing is production, selling and distribution.

Income statement by absorption costing: -

10

There are different types companies who are using absorption costing to make a income

statements. Toyota company should use this system for their income statements, because it is

very useful and effective cost system in the business. Other than that, absorption costing applies

on all production costs to all units produced. Only fixed overhead costs re applied under the

absorption costing. Along with this, profitability will appear to be lower in the absorption costing

and this costing is production, selling and distribution.

Income statement by absorption costing: -

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.