Comprehensive Management Accounting Report: Toyota Motors

VerifiedAdded on 2020/07/22

|19

|6104

|33

Report

AI Summary

This report provides a comprehensive analysis of Toyota Motors' management accounting practices. It begins with an introduction to management accounting, its importance, and various tools and techniques used for financial analysis, including financial statement analysis, ratio analysis, and budgeting. The report then delves into the specific application of these tools to Toyota Motors, examining different methods of management accounting reporting, such as budget reporting, accounts receivable and payable reporting, and inventory costing. The report further explores income statements using both absorption and marginal costing methods, providing calculations and examples relevant to Toyota's operations. Additionally, the report discusses different types of planning tools used in budgetary control and analyzes how Toyota responds to financial problems using management accounting techniques. The report concludes with an overview of the key findings and references relevant sources. This report is designed to give insights into Toyota's financial strategies.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1. Management accounting and essential requirements of its different types......................1

P2. Different methods used for management accounting reporting.......................................3

TASK 2............................................................................................................................................5

P3. Income statements through absorption and marginal costing of Toyota.........................5

TASK 3 ........................................................................................................................................9

P4. Different types of planning tools used in budgetary control............................................9

TASK 4 .........................................................................................................................................11

P5. Organisation’s response towards financial problems by using management accounting11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1. Management accounting and essential requirements of its different types......................1

P2. Different methods used for management accounting reporting.......................................3

TASK 2............................................................................................................................................5

P3. Income statements through absorption and marginal costing of Toyota.........................5

TASK 3 ........................................................................................................................................9

P4. Different types of planning tools used in budgetary control............................................9

TASK 4 .........................................................................................................................................11

P5. Organisation’s response towards financial problems by using management accounting11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting provides solution on future possibilities which can be happen in

the company. It is related to identification, analyses and presenting financial information. The

planning, decision making and controlling activities can prove to be effective only with proper

utilisation of information provided by such system of accounting. There are various tools and

techniques available with management accounting to provide administration with the necessary

information. A manager has to perform various functions of planning, organising, staffing,

directing and controlling. It includes techniques that are important for planning activities which

definitely help in controlling the performance of organisation. This project is based on the

Toyota Motors. This project will be provide information on different types of management

accounting, budgeting and costing methods which can be used by the company in making

provisions. Planning tools are also required for the organisation in budget making which will be

discuss in this project. At the end of this project will provide actions taken by managers towards

financials problems by using management accounting tools and techniques.

TASK 1

P1. Management accounting and essential requirements of its different types

A management accounting provides administration with various tools and techniques.

Financial statement analysis, ratio analysis, cash flow statement, fund flow statement, budget and

budgetary control, marginal accounting, cost-volume profit analysis are the common tools used

in management accounting. Toyota motors is the most successful company of Japan because of

its appropriate decisions at right time. Management accounting, an important kind of accounting

has generally provide administration with various reports and analyses of budgets that help

company to set targets and accomplish the same. The successful planning and analysis can only

be achieved with the help of management accounting. Making financial data as the most reliable

information is the main key of management accounting. For surviving in a dynamic

environment, smooth and effective functioning of various operations is must. That too can be

impossible without use of management accounting. Financial accounting only provides statement

of income and Balance sheet. The same can be of no use without analysing them. Management

accounting analyse such financial information and extract advantageous decision making data.

Toyota is the highest car producer organisation in world. They have ton deal with day to day

1

Management accounting provides solution on future possibilities which can be happen in

the company. It is related to identification, analyses and presenting financial information. The

planning, decision making and controlling activities can prove to be effective only with proper

utilisation of information provided by such system of accounting. There are various tools and

techniques available with management accounting to provide administration with the necessary

information. A manager has to perform various functions of planning, organising, staffing,

directing and controlling. It includes techniques that are important for planning activities which

definitely help in controlling the performance of organisation. This project is based on the

Toyota Motors. This project will be provide information on different types of management

accounting, budgeting and costing methods which can be used by the company in making

provisions. Planning tools are also required for the organisation in budget making which will be

discuss in this project. At the end of this project will provide actions taken by managers towards

financials problems by using management accounting tools and techniques.

TASK 1

P1. Management accounting and essential requirements of its different types

A management accounting provides administration with various tools and techniques.

Financial statement analysis, ratio analysis, cash flow statement, fund flow statement, budget and

budgetary control, marginal accounting, cost-volume profit analysis are the common tools used

in management accounting. Toyota motors is the most successful company of Japan because of

its appropriate decisions at right time. Management accounting, an important kind of accounting

has generally provide administration with various reports and analyses of budgets that help

company to set targets and accomplish the same. The successful planning and analysis can only

be achieved with the help of management accounting. Making financial data as the most reliable

information is the main key of management accounting. For surviving in a dynamic

environment, smooth and effective functioning of various operations is must. That too can be

impossible without use of management accounting. Financial accounting only provides statement

of income and Balance sheet. The same can be of no use without analysing them. Management

accounting analyse such financial information and extract advantageous decision making data.

Toyota is the highest car producer organisation in world. They have ton deal with day to day

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

challenges that has been arise with them time to-time. A manager has to perform its managerial

functions of planning, organising, staffing, directing and controlling. Such type of accounting

helps in various aspects of supply of raw materials, debtors, creditors, finance, budgets, revenue

generation, credibility and profit analysis. To have effective operations, management prepare

budgets such as cash budget, purchase budget, sales budget, and flexible budget too. The targets

are set based on such budgets and each division has to achieve its pre-determined targets. They

can able to frame various strategies of business to deal in dynamic environment with the help of

such system of accounting. It contributes to strategies formulation and gaining an advantage over

its rivals.

The environment in which an organisation deals became complex. The competition has

become cut-throat and surviving in such environment with presence of numerous rivals is very

difficult. Despite of these facts, Toyota Motors has made enormous growth and gained huge

profitability. They are among successful companies in auto mobile sector. Management

accounting is helping administration with determination of financial cost and managerial

performance of business organisation. Effective in managerial functions is the essence of

business. The reports are being presented to administration on a daily, weekly and monthly basis.

They needs to spend massive amount of time considering such reports for taking important

decisions in business. Modern techniques focuses on providing reports even on a daily basis. The

budgets are prepared based on historical data. The targets are set and accomplish within

stipulated time. If found any deviation or variance, the same needs to be addressed and

supportive plans are being prepared. Management accounting is the accounting done for

administration of business organisation. Different kinds of management accounting can be

classified as follows-

Cost accounting system- Cost accounting system is one of the most kind of accounting.

Toyota is the highest car producer company in world. They needs to analyse cost of

manufacturing cars. Raw materials, components and parts that are being used. This overall helps

in determination of profitability of products and services that Toyota is offering. This system, of

accounting helps in cost determination and profitability. There are cost accounting professionals

that manage such system of finance.

Inventory management system- Inventory management system helps in management of

stocks in warehouses. They are the manufacturing company, hence required various tools, parts,

2

functions of planning, organising, staffing, directing and controlling. Such type of accounting

helps in various aspects of supply of raw materials, debtors, creditors, finance, budgets, revenue

generation, credibility and profit analysis. To have effective operations, management prepare

budgets such as cash budget, purchase budget, sales budget, and flexible budget too. The targets

are set based on such budgets and each division has to achieve its pre-determined targets. They

can able to frame various strategies of business to deal in dynamic environment with the help of

such system of accounting. It contributes to strategies formulation and gaining an advantage over

its rivals.

The environment in which an organisation deals became complex. The competition has

become cut-throat and surviving in such environment with presence of numerous rivals is very

difficult. Despite of these facts, Toyota Motors has made enormous growth and gained huge

profitability. They are among successful companies in auto mobile sector. Management

accounting is helping administration with determination of financial cost and managerial

performance of business organisation. Effective in managerial functions is the essence of

business. The reports are being presented to administration on a daily, weekly and monthly basis.

They needs to spend massive amount of time considering such reports for taking important

decisions in business. Modern techniques focuses on providing reports even on a daily basis. The

budgets are prepared based on historical data. The targets are set and accomplish within

stipulated time. If found any deviation or variance, the same needs to be addressed and

supportive plans are being prepared. Management accounting is the accounting done for

administration of business organisation. Different kinds of management accounting can be

classified as follows-

Cost accounting system- Cost accounting system is one of the most kind of accounting.

Toyota is the highest car producer company in world. They needs to analyse cost of

manufacturing cars. Raw materials, components and parts that are being used. This overall helps

in determination of profitability of products and services that Toyota is offering. This system, of

accounting helps in cost determination and profitability. There are cost accounting professionals

that manage such system of finance.

Inventory management system- Inventory management system helps in management of

stocks in warehouses. They are the manufacturing company, hence required various tools, parts,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

components and other raw materials. They needs to identify how much stock gets in and out

from their warehouse. Each and every part that is moved in and from warehouse must be noticed.

This system is also known as stock controlling method of accounting. Wastage of products must

be reduced and eliminated. Future contingencies should also be kept in mind.

Job costing- An auto mobile company such as Toyota needs to keep track of cost of each

job. The work performed by an individual should be notice to increase their efficiency and

productivity. The cost of performing job in each project should be identified. To identify the cost

of task assigned to a given employee must be seen and evaluated. The main aim is to increase

effective of work assigned to each job performance. Every job that is performed is of utmost

importance and must be performed effectively as per customer specification. It consider both

direct and indirect cost involving in each job.

Price optimisation- The response of customers towards price fluctuations must be

determined. Toyota also follow leadership pricing policy. It is one of the kind of mathematical

analysis and are of utmost importance for business organisation. It generally involves cost of

operations, inventory and historical prices of products and services offered by an organisation. It

also calculates the variances arises in demands of products and services with using different

pricing policy. The company has various models which are made for various segments of market.

It determines value creation for company external customers. Their behaviours towards various

prices must be noticed.

P2. Different methods used for management accounting reporting

Toyota motors has huge turnover by serving worldwide. The management accounting

helps in assessing performance of business. The management accounting reporting are prepared

on the requirement basis i.e. as and when required. These all depends on type of project, manager

is dealing in along with time sensitivity. The management accounting reports are being prepared

on a daily, weekly and monthly basis. This overall gives complete view point of performance of

business organisation. The manager has great importance with such system of accounting.

Toyota give more emphasis on decision making aspect of business organisation. No matter in

what field of business, a firm is dealing in. This helps in achievement of organisational objective

along with greater profitability, improvement in financial stability. The financial reports are only

limited to statements. The administration is need of business information from time-to-time. This

3

from their warehouse. Each and every part that is moved in and from warehouse must be noticed.

This system is also known as stock controlling method of accounting. Wastage of products must

be reduced and eliminated. Future contingencies should also be kept in mind.

Job costing- An auto mobile company such as Toyota needs to keep track of cost of each

job. The work performed by an individual should be notice to increase their efficiency and

productivity. The cost of performing job in each project should be identified. To identify the cost

of task assigned to a given employee must be seen and evaluated. The main aim is to increase

effective of work assigned to each job performance. Every job that is performed is of utmost

importance and must be performed effectively as per customer specification. It consider both

direct and indirect cost involving in each job.

Price optimisation- The response of customers towards price fluctuations must be

determined. Toyota also follow leadership pricing policy. It is one of the kind of mathematical

analysis and are of utmost importance for business organisation. It generally involves cost of

operations, inventory and historical prices of products and services offered by an organisation. It

also calculates the variances arises in demands of products and services with using different

pricing policy. The company has various models which are made for various segments of market.

It determines value creation for company external customers. Their behaviours towards various

prices must be noticed.

P2. Different methods used for management accounting reporting

Toyota motors has huge turnover by serving worldwide. The management accounting

helps in assessing performance of business. The management accounting reporting are prepared

on the requirement basis i.e. as and when required. These all depends on type of project, manager

is dealing in along with time sensitivity. The management accounting reports are being prepared

on a daily, weekly and monthly basis. This overall gives complete view point of performance of

business organisation. The manager has great importance with such system of accounting.

Toyota give more emphasis on decision making aspect of business organisation. No matter in

what field of business, a firm is dealing in. This helps in achievement of organisational objective

along with greater profitability, improvement in financial stability. The financial reports are only

limited to statements. The administration is need of business information from time-to-time. This

3

can be possible only with management accounting. These reports are generally prepared by

professionals. The different methods used for management accounting reporting are as follows-

Budget reporting- The management use to make plan for every aspects of business

organisation, often termed as profit plan or budget plan. The firm has limited resources. The

allocation and control of cost incurred on expenses is must. Budget preparation overall

contributes in achievement of such objectives. The management of business organisation prepare

budget plan of sales, purchase, cash and capital also. The target are being set and plan

accordingly. The management wants to attain business targets within stipulated time frame.

Extensive research and past records are required by team to frame targets that best fit to

organisation. It is also termed as quantitative plan on a daily, weekly and monthly basis. The

financial performance of business concern are being controlled by budget preparation.

Accounts receivable reporting- The accounts receivable reporting is also needed for

organisation like Toyota motors. If company deliver its products and services on a credit basis,

such reporting are of utmost importance. Debtors are the real assets of firm. The credit balances

of such debtors needs to be maintained in order get an overview of them. The collection process

of organisation must be boosted. Reporting is done so that it will reduce the possibility of bad

debts.

Accounts payable reporting- Accounts payable reporting is done to satisfy creditors and

have good relation with them. The records of creditors and timely payment to them is needed for

smooth functioning of business organisation. The suppliers of organisation need to be addressed

effectively. Toyota also buy several raw materials, tools, components

Inventory costing reporting- Inventory costing reporting is regarding inventory in and

out from warehouse. The main aim is to eliminate the wastage of raw material and stock. Toyota

is engaged in delivering high-quality cars to its customers. Thus, maintenance of stock and

inventory is essential. It helps in collecting data regarding inventory cost, labour and other

overheads.

Job costing reporting- Job costing reporting is regarding cost of job involved in projects

of organisation. The cost incurred by company on performing each job is up to mark or not. The

firm needs to frame various strategies and policies to tackle with the additional cost incurring on

performing each task. Effectiveness in job performance is very important from company’s point

of view.

4

professionals. The different methods used for management accounting reporting are as follows-

Budget reporting- The management use to make plan for every aspects of business

organisation, often termed as profit plan or budget plan. The firm has limited resources. The

allocation and control of cost incurred on expenses is must. Budget preparation overall

contributes in achievement of such objectives. The management of business organisation prepare

budget plan of sales, purchase, cash and capital also. The target are being set and plan

accordingly. The management wants to attain business targets within stipulated time frame.

Extensive research and past records are required by team to frame targets that best fit to

organisation. It is also termed as quantitative plan on a daily, weekly and monthly basis. The

financial performance of business concern are being controlled by budget preparation.

Accounts receivable reporting- The accounts receivable reporting is also needed for

organisation like Toyota motors. If company deliver its products and services on a credit basis,

such reporting are of utmost importance. Debtors are the real assets of firm. The credit balances

of such debtors needs to be maintained in order get an overview of them. The collection process

of organisation must be boosted. Reporting is done so that it will reduce the possibility of bad

debts.

Accounts payable reporting- Accounts payable reporting is done to satisfy creditors and

have good relation with them. The records of creditors and timely payment to them is needed for

smooth functioning of business organisation. The suppliers of organisation need to be addressed

effectively. Toyota also buy several raw materials, tools, components

Inventory costing reporting- Inventory costing reporting is regarding inventory in and

out from warehouse. The main aim is to eliminate the wastage of raw material and stock. Toyota

is engaged in delivering high-quality cars to its customers. Thus, maintenance of stock and

inventory is essential. It helps in collecting data regarding inventory cost, labour and other

overheads.

Job costing reporting- Job costing reporting is regarding cost of job involved in projects

of organisation. The cost incurred by company on performing each job is up to mark or not. The

firm needs to frame various strategies and policies to tackle with the additional cost incurring on

performing each task. Effectiveness in job performance is very important from company’s point

of view.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance reporting- Every organisation has keen interest in knowing performance

of business. They wants to improve the business performance for growth and expansion

purposes. Performance must be evaluated and thus, improvement will be done. Every business

has several aspects of business. Each component performance must be assessed and taken care of

to improve profitability of firm. Balanced scorecard is one such performance management tool

that overall helps in improving performance of various functions. Employees performance must

be seek and improvement must be done. Employees of firm are assessed based on sales and

profit. Stakeholders of company have more interest towards performance of business. Toyota

Motors is giving regular consideration on performance of each function (Weißenberger and

Angelkort, 2011). Thus, an organisation has performed so well and gained huge success in

present period of time.

TASK 2

P3. Income statements through absorption and marginal costing of Toyota

a) Calculation of number of units completed and packed

Number of units completed during the year = 2000 units

Number of units packed during the year:

Number of units completed during the year = 2000 units

Less: Units Unpacked = 400 units

Total units packed during the year = 1600 units

Calculations of variable and fixed costs:

Calculation of variable and fixed costs

Units

$ per

unit Total cost

Direct material cost 2000 45 90000

Direct labour Cost: Units

$ per

hour Hours

Total cost

($)

Total

prod

uctio

n Per unit ($)

Machining department 20 2000 5 100 500 2000 0.25

5

of business. They wants to improve the business performance for growth and expansion

purposes. Performance must be evaluated and thus, improvement will be done. Every business

has several aspects of business. Each component performance must be assessed and taken care of

to improve profitability of firm. Balanced scorecard is one such performance management tool

that overall helps in improving performance of various functions. Employees performance must

be seek and improvement must be done. Employees of firm are assessed based on sales and

profit. Stakeholders of company have more interest towards performance of business. Toyota

Motors is giving regular consideration on performance of each function (Weißenberger and

Angelkort, 2011). Thus, an organisation has performed so well and gained huge success in

present period of time.

TASK 2

P3. Income statements through absorption and marginal costing of Toyota

a) Calculation of number of units completed and packed

Number of units completed during the year = 2000 units

Number of units packed during the year:

Number of units completed during the year = 2000 units

Less: Units Unpacked = 400 units

Total units packed during the year = 1600 units

Calculations of variable and fixed costs:

Calculation of variable and fixed costs

Units

$ per

unit Total cost

Direct material cost 2000 45 90000

Direct labour Cost: Units

$ per

hour Hours

Total cost

($)

Total

prod

uctio

n Per unit ($)

Machining department 20 2000 5 100 500 2000 0.25

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

units/hr.

Finishing department

5units/hr. 2000 6 400 2400 2000 1.2

Dispatch department 20

units/hr. 2000 5 100 500 2000 0.25

Packing boxes 1600 0.5 800 0.5

Total variable overheads: 94200

Hours/

unit

Total

produ

ction

Total

hours

Absorbed

Rate($)

Total

cost($)

Total

prod

uctio

n

Price Per

unit ($)

Fixed overhead:

Machine department 0.05 2000 100 7 700 2000 0.35

Finishing department 0.2 2000 400 5 2000 2000 1

Dispatch department 0.5 2000 1000 1 1000 2000 0.5

3700

Variable costs: Variable cost costs that are good in the production of a business or in

proportion to the service. For example, variable manufacturing costs overhead costs are

unlimited costs, direct costs, not convertible costs are sometimes called unit-level costs because

they differ with the number of units produced.

Fixed costs: In economics, fixed costs, indirect costs or overheads are business expenses,

which are not dependent on the level of goods or services produced by the business. They are

related to the time, like pay or rent is paid per month, and is often known as overhead cost.

In the above calculation of fixed and variable costs, Machine, Finishing and dispatching

departments which is measuring by multiplying it with per hour is variable costs. On the other

hand, all fixed variables which is calculated on the basis of absorption rates are fixed costs which

doesn't changed with total production of units (Ward, 2012). It always remain constant until or

unless new plant is purchases.

b) Income statements for the period:

1) Income statements for the period using Absorption costing:

6

Finishing department

5units/hr. 2000 6 400 2400 2000 1.2

Dispatch department 20

units/hr. 2000 5 100 500 2000 0.25

Packing boxes 1600 0.5 800 0.5

Total variable overheads: 94200

Hours/

unit

Total

produ

ction

Total

hours

Absorbed

Rate($)

Total

cost($)

Total

prod

uctio

n

Price Per

unit ($)

Fixed overhead:

Machine department 0.05 2000 100 7 700 2000 0.35

Finishing department 0.2 2000 400 5 2000 2000 1

Dispatch department 0.5 2000 1000 1 1000 2000 0.5

3700

Variable costs: Variable cost costs that are good in the production of a business or in

proportion to the service. For example, variable manufacturing costs overhead costs are

unlimited costs, direct costs, not convertible costs are sometimes called unit-level costs because

they differ with the number of units produced.

Fixed costs: In economics, fixed costs, indirect costs or overheads are business expenses,

which are not dependent on the level of goods or services produced by the business. They are

related to the time, like pay or rent is paid per month, and is often known as overhead cost.

In the above calculation of fixed and variable costs, Machine, Finishing and dispatching

departments which is measuring by multiplying it with per hour is variable costs. On the other

hand, all fixed variables which is calculated on the basis of absorption rates are fixed costs which

doesn't changed with total production of units (Ward, 2012). It always remain constant until or

unless new plant is purchases.

b) Income statements for the period:

1) Income statements for the period using Absorption costing:

6

Total absorption cost (TAC) is a method of accounting cost that emphasizes the full cost

of manufacturing or providing services. TAC not only includes the cost of materials and labor,

but also all manufacturing overheads (whether 'fixed' or 'variable') are also not included. Cost of

each cost centre can be direct or indirect costs.

Income statement by absorption costing for the period:

Price per

unit($) Total Units Amount ($) Amount ($)

Sales revenue 200 1500 300000

Less: Cost of sales:

Direct Material 45 2000 90000

Direct Labour:

Machine department 0.6 2000 1200

Finishing department 2.2 2000 4400

Dispatch department 1.25 2000 2500

Less: Unpacked 0.5 -400 -200

Closing Stock 49.05 -100 -4905

92995

Gross Profit 207005

Interpretation: In the above table, company is receiving gross profit of around $207005.

This gross profit is identified after reducing all variable and fixed overhead costs from sales

revenue. As there's no separate selling and distribution costs, net profit is not calculated through

absorption costing (Soin and Collier, 2013.). There are total 400 finished products which are not

yet packed, hence these 400 products are reduced from dispatched departments (Scapens and

Bromwich, 2010). Also this unpacked goods are not considered under closing stock.

2) Income statements for the period using Marginal costing:

Marginal Costing is a costing method wherein the marginal cost like variable cost is

charged to units of cost, while the fixed cost for the period is completely written off against the

contribution.

7

of manufacturing or providing services. TAC not only includes the cost of materials and labor,

but also all manufacturing overheads (whether 'fixed' or 'variable') are also not included. Cost of

each cost centre can be direct or indirect costs.

Income statement by absorption costing for the period:

Price per

unit($) Total Units Amount ($) Amount ($)

Sales revenue 200 1500 300000

Less: Cost of sales:

Direct Material 45 2000 90000

Direct Labour:

Machine department 0.6 2000 1200

Finishing department 2.2 2000 4400

Dispatch department 1.25 2000 2500

Less: Unpacked 0.5 -400 -200

Closing Stock 49.05 -100 -4905

92995

Gross Profit 207005

Interpretation: In the above table, company is receiving gross profit of around $207005.

This gross profit is identified after reducing all variable and fixed overhead costs from sales

revenue. As there's no separate selling and distribution costs, net profit is not calculated through

absorption costing (Soin and Collier, 2013.). There are total 400 finished products which are not

yet packed, hence these 400 products are reduced from dispatched departments (Scapens and

Bromwich, 2010). Also this unpacked goods are not considered under closing stock.

2) Income statements for the period using Marginal costing:

Marginal Costing is a costing method wherein the marginal cost like variable cost is

charged to units of cost, while the fixed cost for the period is completely written off against the

contribution.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

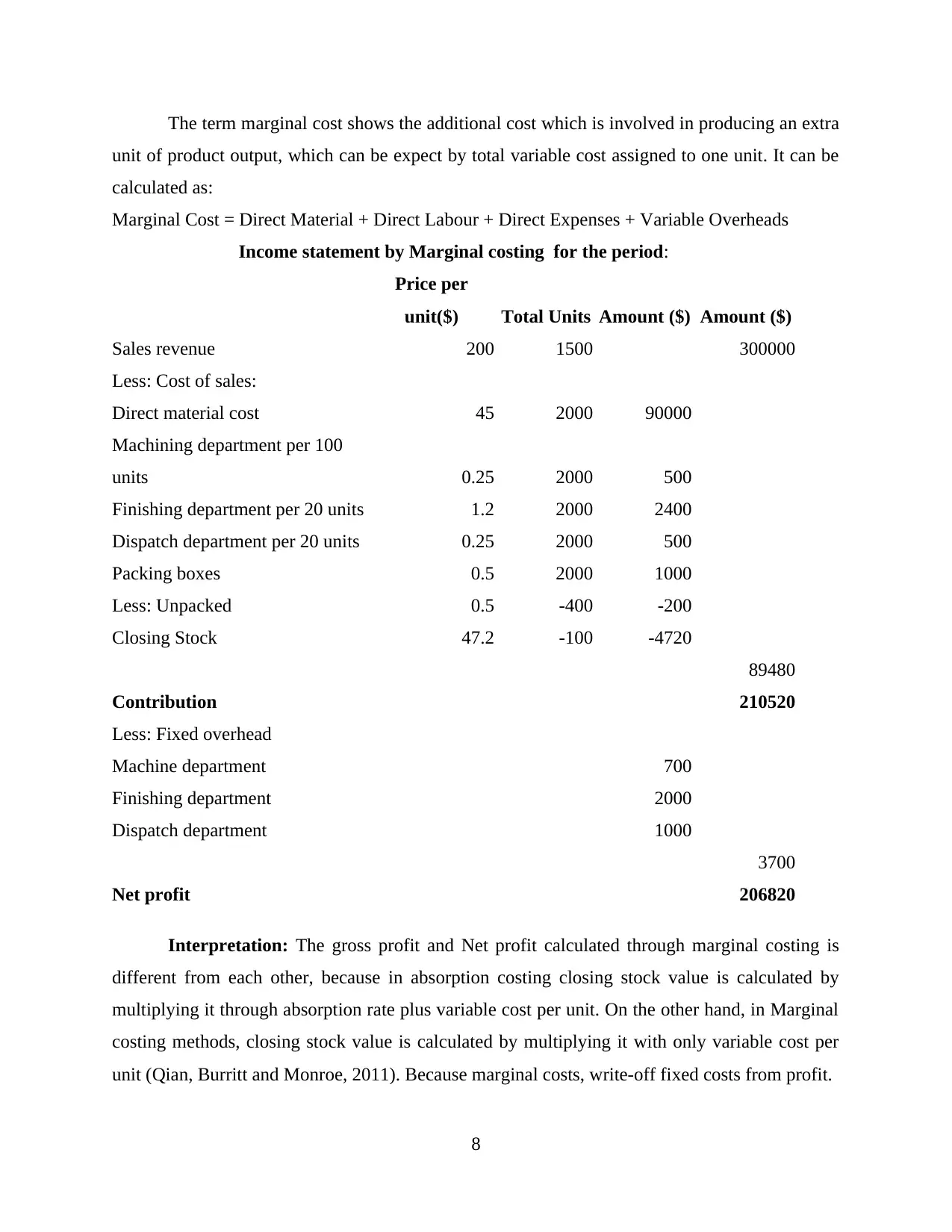

The term marginal cost shows the additional cost which is involved in producing an extra

unit of product output, which can be expect by total variable cost assigned to one unit. It can be

calculated as:

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

Income statement by Marginal costing for the period:

Price per

unit($) Total Units Amount ($) Amount ($)

Sales revenue 200 1500 300000

Less: Cost of sales:

Direct material cost 45 2000 90000

Machining department per 100

units 0.25 2000 500

Finishing department per 20 units 1.2 2000 2400

Dispatch department per 20 units 0.25 2000 500

Packing boxes 0.5 2000 1000

Less: Unpacked 0.5 -400 -200

Closing Stock 47.2 -100 -4720

89480

Contribution 210520

Less: Fixed overhead

Machine department 700

Finishing department 2000

Dispatch department 1000

3700

Net profit 206820

Interpretation: The gross profit and Net profit calculated through marginal costing is

different from each other, because in absorption costing closing stock value is calculated by

multiplying it through absorption rate plus variable cost per unit. On the other hand, in Marginal

costing methods, closing stock value is calculated by multiplying it with only variable cost per

unit (Qian, Burritt and Monroe, 2011). Because marginal costs, write-off fixed costs from profit.

8

unit of product output, which can be expect by total variable cost assigned to one unit. It can be

calculated as:

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

Income statement by Marginal costing for the period:

Price per

unit($) Total Units Amount ($) Amount ($)

Sales revenue 200 1500 300000

Less: Cost of sales:

Direct material cost 45 2000 90000

Machining department per 100

units 0.25 2000 500

Finishing department per 20 units 1.2 2000 2400

Dispatch department per 20 units 0.25 2000 500

Packing boxes 0.5 2000 1000

Less: Unpacked 0.5 -400 -200

Closing Stock 47.2 -100 -4720

89480

Contribution 210520

Less: Fixed overhead

Machine department 700

Finishing department 2000

Dispatch department 1000

3700

Net profit 206820

Interpretation: The gross profit and Net profit calculated through marginal costing is

different from each other, because in absorption costing closing stock value is calculated by

multiplying it through absorption rate plus variable cost per unit. On the other hand, in Marginal

costing methods, closing stock value is calculated by multiplying it with only variable cost per

unit (Qian, Burritt and Monroe, 2011). Because marginal costs, write-off fixed costs from profit.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

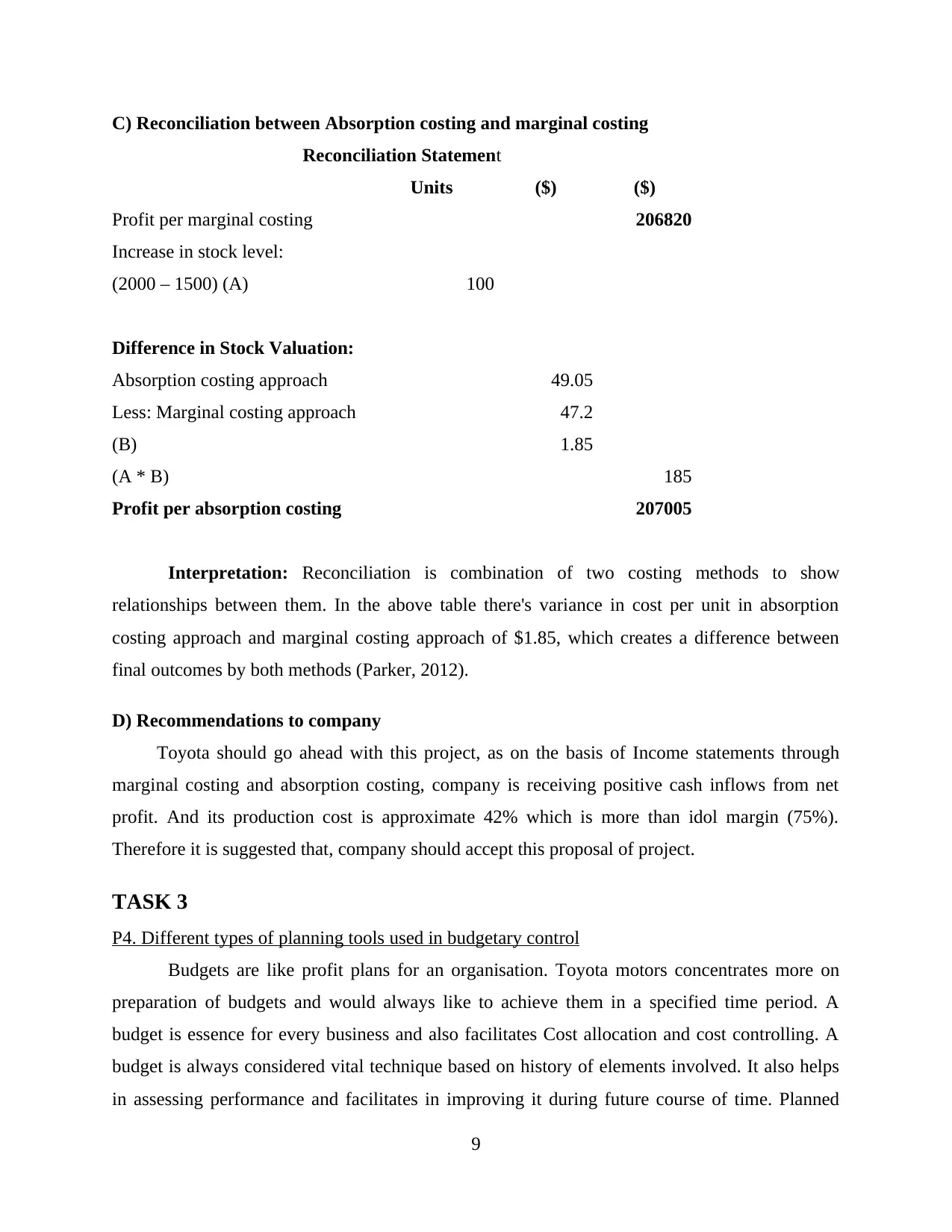

C) Reconciliation between Absorption costing and marginal costing

Reconciliation Statement

Units ($) ($)

Profit per marginal costing 206820

Increase in stock level:

(2000 – 1500) (A) 100

Difference in Stock Valuation:

Absorption costing approach 49.05

Less: Marginal costing approach 47.2

(B) 1.85

(A * B) 185

Profit per absorption costing 207005

Interpretation: Reconciliation is combination of two costing methods to show

relationships between them. In the above table there's variance in cost per unit in absorption

costing approach and marginal costing approach of $1.85, which creates a difference between

final outcomes by both methods (Parker, 2012).

D) Recommendations to company

Toyota should go ahead with this project, as on the basis of Income statements through

marginal costing and absorption costing, company is receiving positive cash inflows from net

profit. And its production cost is approximate 42% which is more than idol margin (75%).

Therefore it is suggested that, company should accept this proposal of project.

TASK 3

P4. Different types of planning tools used in budgetary control

Budgets are like profit plans for an organisation. Toyota motors concentrates more on

preparation of budgets and would always like to achieve them in a specified time period. A

budget is essence for every business and also facilitates Cost allocation and cost controlling. A

budget is always considered vital technique based on history of elements involved. It also helps

in assessing performance and facilitates in improving it during future course of time. Planned

9

Reconciliation Statement

Units ($) ($)

Profit per marginal costing 206820

Increase in stock level:

(2000 – 1500) (A) 100

Difference in Stock Valuation:

Absorption costing approach 49.05

Less: Marginal costing approach 47.2

(B) 1.85

(A * B) 185

Profit per absorption costing 207005

Interpretation: Reconciliation is combination of two costing methods to show

relationships between them. In the above table there's variance in cost per unit in absorption

costing approach and marginal costing approach of $1.85, which creates a difference between

final outcomes by both methods (Parker, 2012).

D) Recommendations to company

Toyota should go ahead with this project, as on the basis of Income statements through

marginal costing and absorption costing, company is receiving positive cash inflows from net

profit. And its production cost is approximate 42% which is more than idol margin (75%).

Therefore it is suggested that, company should accept this proposal of project.

TASK 3

P4. Different types of planning tools used in budgetary control

Budgets are like profit plans for an organisation. Toyota motors concentrates more on

preparation of budgets and would always like to achieve them in a specified time period. A

budget is essence for every business and also facilitates Cost allocation and cost controlling. A

budget is always considered vital technique based on history of elements involved. It also helps

in assessing performance and facilitates in improving it during future course of time. Planned

9

budgets are being compared with actual performance, if find any deviation or variance. The same

will be sorted out as quickly as possible. The important decisions of business will be based on

such budgets only. The budgets are being prepared based on various aspects and divisions. Thus,

it facilitates smooth functioning of business operations. Toyota motors is the highest car

manufacturing company. They needs to make plan for each and every element of business.

Administration set up various targets and try to achieve them in specified period of time (Otley

and Emmanuel, 2013). Every department is required to work as per planned budget and try to

achieve the said target.

Source: Manage and Understand the Purpose of Budgets.

Toyota motors uses plenty of budgets that are classified as follows-

Cash flow budget- Cash inflow and outflow are one of the most important concern for

business organisation like Toyota motors. Cash availability is of utmost importance. To keep an

eye on cash aspect of business is necessary. Cash flow management gives an idea to

administration as how much funds will be raised from what activities and how to effectively use

those funds (Nandan, 2010). Cash management is necessary for any management of business

concern.

10

Illustration 1: Different types of budget.

will be sorted out as quickly as possible. The important decisions of business will be based on

such budgets only. The budgets are being prepared based on various aspects and divisions. Thus,

it facilitates smooth functioning of business operations. Toyota motors is the highest car

manufacturing company. They needs to make plan for each and every element of business.

Administration set up various targets and try to achieve them in specified period of time (Otley

and Emmanuel, 2013). Every department is required to work as per planned budget and try to

achieve the said target.

Source: Manage and Understand the Purpose of Budgets.

Toyota motors uses plenty of budgets that are classified as follows-

Cash flow budget- Cash inflow and outflow are one of the most important concern for

business organisation like Toyota motors. Cash availability is of utmost importance. To keep an

eye on cash aspect of business is necessary. Cash flow management gives an idea to

administration as how much funds will be raised from what activities and how to effectively use

those funds (Nandan, 2010). Cash management is necessary for any management of business

concern.

10

Illustration 1: Different types of budget.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.