Report on Pricing Strategies for Toyota Australia's RAV4 Models

VerifiedAdded on 2022/09/05

|14

|2493

|19

Report

AI Summary

This report analyzes the pricing strategies employed by Toyota Australia, focusing on three RAV4 models: GX 2WD Hybrid, GXL AWD Hybrid, and CRUISER 2WD Hybrid. It begins by discussing various pricing strategies, with a detailed comparison between cost-based and market-based approaches. The analysis involves determining target costs for each model and recommending strategies to achieve these targets, including supply chain optimization and value-chain analysis to identify value-added and non-value-added activities. The report also compares the advantages and disadvantages of both market-based and cost-based pricing for each model, offering specific recommendations for final pricing adjustments to maximize profitability. The conclusion emphasizes the importance of aligning pricing strategies with business objectives and maintaining a focus on cost reduction while preserving quality and customer satisfaction.

Running head: PRICING STRATEGY

PRICING STRATEGY

Name of the Student

Name of the University

Author note

PRICING STRATEGY

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRICING STRATEGY

Executive Summary

This paper aims at discussing various pricing strategies and to draw a comparison between cost-

based and market-based pricing strategy. The comparison is drawn by analyzing the current

pricing strategy of Toyota Australia. For analyzing the pricing strategy, only three models of

RAV4 series are selected.

Executive Summary

This paper aims at discussing various pricing strategies and to draw a comparison between cost-

based and market-based pricing strategy. The comparison is drawn by analyzing the current

pricing strategy of Toyota Australia. For analyzing the pricing strategy, only three models of

RAV4 series are selected.

2PRICING STRATEGY

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Analysis of target cost of three models –.....................................................................................3

Recommendation to achieve target cost and profit......................................................................4

Value-chain analysis for improving cost.....................................................................................5

Recommendation and comparison of pricing strategy................................................................6

Recommendation for final price..................................................................................................8

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Appendix........................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Analysis of target cost of three models –.....................................................................................3

Recommendation to achieve target cost and profit......................................................................4

Value-chain analysis for improving cost.....................................................................................5

Recommendation and comparison of pricing strategy................................................................6

Recommendation for final price..................................................................................................8

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Appendix........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRICING STRATEGY

Introduction

This report aims at reviewing and evaluating the pricing strategy for three models of

Toyota Australia. Toyota Australia is the subsidiary company of Toyota Motor Corporation,

which is located in Japan. This report explains the different pricing strategies and aims at

recommending a better strategy for the company to achieve the desired profits and business

objectives.

Discussion

Analysis of target cost of three models –

Target costing is a method to determine the price of the product based on the prevailing

market conditions after considering various other factors (de Lautour 2018). Target cost is

determined by deducting the target profit margin from the market selling prices. It is identified so

that management can control the costs as they have less control over the market selling price (Al-

Khasawneh et al. 2019). The target cost for the three models are determined and is provided in

the Appendix. The current prices for the three models – (i) 2019 Toyota RAV4 GX 2WD

Hybrid, (ii) 2019 Toyota RAV4 GXL AWD Hybrid and (iii) 2019 Toyota RAV4 CRUISER

2WD Hybrid, are available and the market selling prices of respective models are taken for

analysis (https://www.toyota.com.au/ 2020). The target profit margin of the company is 20% on

the cost, hence profit on selling price will be 1/6th of sales. Target cost for Rav4 Gx 2WD hybrid

is the lowest since it has the lowest selling price in market. The target cost is determined by

deducting 20% of profit margin from the respective selling prices of all the three models.

Target cost = selling price – target profit margin

Introduction

This report aims at reviewing and evaluating the pricing strategy for three models of

Toyota Australia. Toyota Australia is the subsidiary company of Toyota Motor Corporation,

which is located in Japan. This report explains the different pricing strategies and aims at

recommending a better strategy for the company to achieve the desired profits and business

objectives.

Discussion

Analysis of target cost of three models –

Target costing is a method to determine the price of the product based on the prevailing

market conditions after considering various other factors (de Lautour 2018). Target cost is

determined by deducting the target profit margin from the market selling prices. It is identified so

that management can control the costs as they have less control over the market selling price (Al-

Khasawneh et al. 2019). The target cost for the three models are determined and is provided in

the Appendix. The current prices for the three models – (i) 2019 Toyota RAV4 GX 2WD

Hybrid, (ii) 2019 Toyota RAV4 GXL AWD Hybrid and (iii) 2019 Toyota RAV4 CRUISER

2WD Hybrid, are available and the market selling prices of respective models are taken for

analysis (https://www.toyota.com.au/ 2020). The target profit margin of the company is 20% on

the cost, hence profit on selling price will be 1/6th of sales. Target cost for Rav4 Gx 2WD hybrid

is the lowest since it has the lowest selling price in market. The target cost is determined by

deducting 20% of profit margin from the respective selling prices of all the three models.

Target cost = selling price – target profit margin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

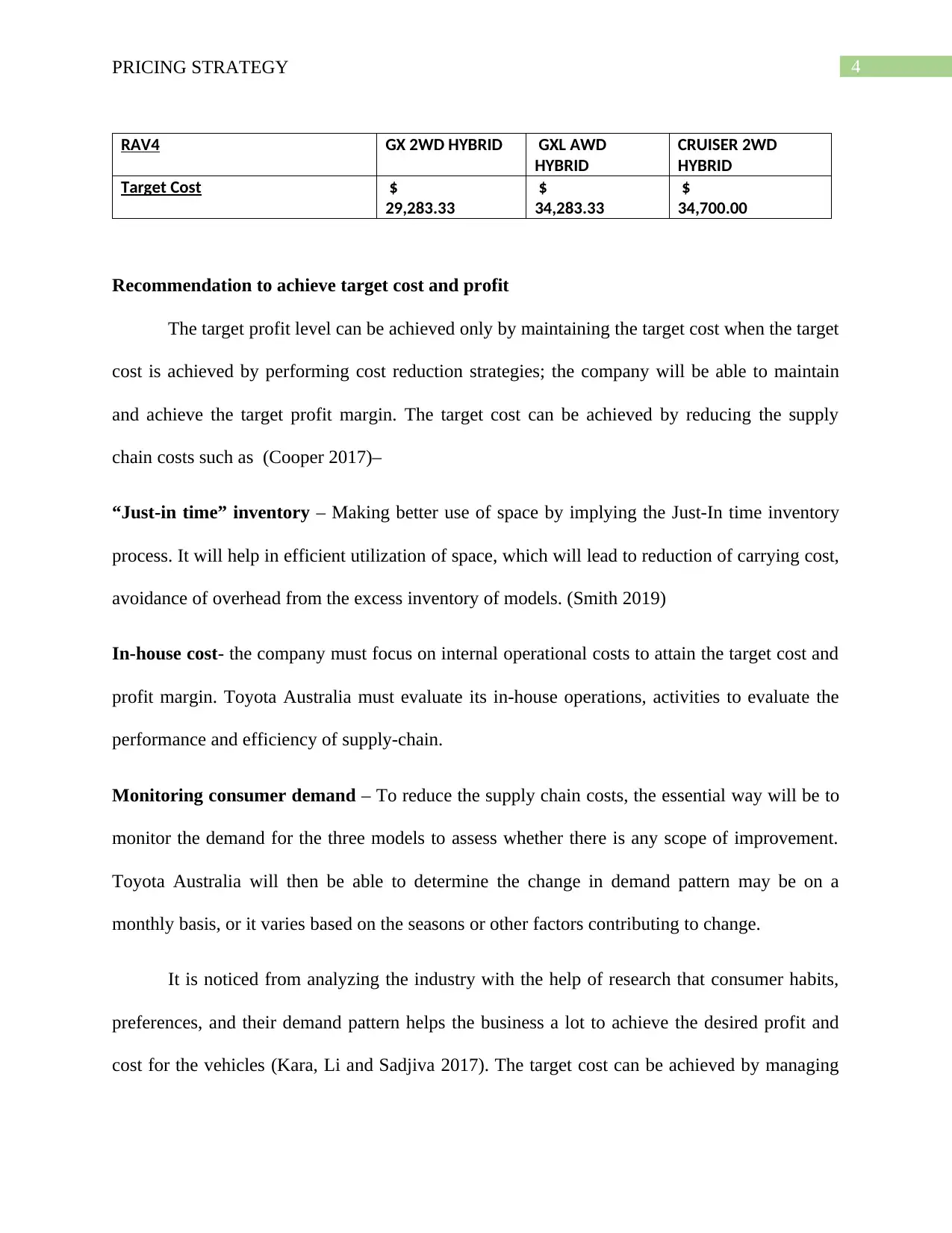

4PRICING STRATEGY

RAV4 GX 2WD HYBRID GXL AWD

HYBRID

CRUISER 2WD

HYBRID

Target Cost $

29,283.33

$

34,283.33

$

34,700.00

Recommendation to achieve target cost and profit

The target profit level can be achieved only by maintaining the target cost when the target

cost is achieved by performing cost reduction strategies; the company will be able to maintain

and achieve the target profit margin. The target cost can be achieved by reducing the supply

chain costs such as (Cooper 2017)–

“Just-in time” inventory – Making better use of space by implying the Just-In time inventory

process. It will help in efficient utilization of space, which will lead to reduction of carrying cost,

avoidance of overhead from the excess inventory of models. (Smith 2019)

In-house cost- the company must focus on internal operational costs to attain the target cost and

profit margin. Toyota Australia must evaluate its in-house operations, activities to evaluate the

performance and efficiency of supply-chain.

Monitoring consumer demand – To reduce the supply chain costs, the essential way will be to

monitor the demand for the three models to assess whether there is any scope of improvement.

Toyota Australia will then be able to determine the change in demand pattern may be on a

monthly basis, or it varies based on the seasons or other factors contributing to change.

It is noticed from analyzing the industry with the help of research that consumer habits,

preferences, and their demand pattern helps the business a lot to achieve the desired profit and

cost for the vehicles (Kara, Li and Sadjiva 2017). The target cost can be achieved by managing

RAV4 GX 2WD HYBRID GXL AWD

HYBRID

CRUISER 2WD

HYBRID

Target Cost $

29,283.33

$

34,283.33

$

34,700.00

Recommendation to achieve target cost and profit

The target profit level can be achieved only by maintaining the target cost when the target

cost is achieved by performing cost reduction strategies; the company will be able to maintain

and achieve the target profit margin. The target cost can be achieved by reducing the supply

chain costs such as (Cooper 2017)–

“Just-in time” inventory – Making better use of space by implying the Just-In time inventory

process. It will help in efficient utilization of space, which will lead to reduction of carrying cost,

avoidance of overhead from the excess inventory of models. (Smith 2019)

In-house cost- the company must focus on internal operational costs to attain the target cost and

profit margin. Toyota Australia must evaluate its in-house operations, activities to evaluate the

performance and efficiency of supply-chain.

Monitoring consumer demand – To reduce the supply chain costs, the essential way will be to

monitor the demand for the three models to assess whether there is any scope of improvement.

Toyota Australia will then be able to determine the change in demand pattern may be on a

monthly basis, or it varies based on the seasons or other factors contributing to change.

It is noticed from analyzing the industry with the help of research that consumer habits,

preferences, and their demand pattern helps the business a lot to achieve the desired profit and

cost for the vehicles (Kara, Li and Sadjiva 2017). The target cost can be achieved by managing

5PRICING STRATEGY

supplier relationships. Toyota Australia can achieve the desired target profit margin by achieving

the desired cost, which is through sourcing the parts, determining the target.

Value-chain analysis for improving cost

Analyzing the customer demand pattern is key to improving cost, and value chain

analysis will help in identifying the consumer’s specific strategic needs. The value-chain will

help in identifying all the business activities from beginning to end, that takes place to produce a

product. The value-added activities for Toyota Australia will be those which enhance the value

and quality of the car from the customer perspective. The non-value added activities would be

that do not increase the value and quality of the car delivered to the consumer. (Shou et al. 2020)

Example - Activities that Toyota Australia should eliminate since these do not enhance value

and instead raise the cost, so to improve cost, following non-value added activities should be

eliminated –

Over-production of vehicles irrespective of demand pattern (Ismail and Yusof 2016)

Waste in inventory, parts for the vehicle (Sutrisno et al. 2018)

Repairs – cost will be increased unnecessarily for providing repairs for the cars.

Examples of value-added activities – Toyota Australia must take actions to improve cost and to

focus on these value-added activities –

Logistics – Toyota Australia must focus on inbound logistics, to improve material handling,

imply inventory control, and return to the supplier. (Hines 2016)

Operational activities - They must also strive to enhance machining, assembling processes,

maintenance of equipment, and testing of car models.

supplier relationships. Toyota Australia can achieve the desired target profit margin by achieving

the desired cost, which is through sourcing the parts, determining the target.

Value-chain analysis for improving cost

Analyzing the customer demand pattern is key to improving cost, and value chain

analysis will help in identifying the consumer’s specific strategic needs. The value-chain will

help in identifying all the business activities from beginning to end, that takes place to produce a

product. The value-added activities for Toyota Australia will be those which enhance the value

and quality of the car from the customer perspective. The non-value added activities would be

that do not increase the value and quality of the car delivered to the consumer. (Shou et al. 2020)

Example - Activities that Toyota Australia should eliminate since these do not enhance value

and instead raise the cost, so to improve cost, following non-value added activities should be

eliminated –

Over-production of vehicles irrespective of demand pattern (Ismail and Yusof 2016)

Waste in inventory, parts for the vehicle (Sutrisno et al. 2018)

Repairs – cost will be increased unnecessarily for providing repairs for the cars.

Examples of value-added activities – Toyota Australia must take actions to improve cost and to

focus on these value-added activities –

Logistics – Toyota Australia must focus on inbound logistics, to improve material handling,

imply inventory control, and return to the supplier. (Hines 2016)

Operational activities - They must also strive to enhance machining, assembling processes,

maintenance of equipment, and testing of car models.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRICING STRATEGY

Outbound Logistics – Toyota Australia should assure that the right model is delivered to the

right client on time. Cars will be sent directly to the dealers or directly to distributed overseas

through waterways and containers.

Marketing and sales - It is essential to focus on product mix and marketing communications.

Service – It includes after-sale service, quality services by qualified personnel, training, and final

checking.

Focusing on these value-added and non-value added activities will help in improving cost

and will lead to increased customer satisfaction.

Recommendation and comparison of pricing strategy

The company currently uses a combination of market-based and value-based pricing

strategy to determine accurate and appropriate prices (Madoh et al. 2019). Market-based pricing

is determined based on the market conditions, prices set by competitors. This marketing mix

reflects that Toyota Australia sets prices for these three models based on market conditions and

customer perspective. The target costing is calculated for all three models and is attached in the

Appendix. The target profit margin is 20%, and the current selling prices are obtained from

research.

Advantage – The car models are created based on customer’s expectations, and therefore cost is

set on the same lines. Thus consumer feels that the more value is delivered to them.

Disadvantage – It can lead to an increase in production time since the design team may require

several iterations before it can design products that meet customer expectations and meets the set

target margin.

Outbound Logistics – Toyota Australia should assure that the right model is delivered to the

right client on time. Cars will be sent directly to the dealers or directly to distributed overseas

through waterways and containers.

Marketing and sales - It is essential to focus on product mix and marketing communications.

Service – It includes after-sale service, quality services by qualified personnel, training, and final

checking.

Focusing on these value-added and non-value added activities will help in improving cost

and will lead to increased customer satisfaction.

Recommendation and comparison of pricing strategy

The company currently uses a combination of market-based and value-based pricing

strategy to determine accurate and appropriate prices (Madoh et al. 2019). Market-based pricing

is determined based on the market conditions, prices set by competitors. This marketing mix

reflects that Toyota Australia sets prices for these three models based on market conditions and

customer perspective. The target costing is calculated for all three models and is attached in the

Appendix. The target profit margin is 20%, and the current selling prices are obtained from

research.

Advantage – The car models are created based on customer’s expectations, and therefore cost is

set on the same lines. Thus consumer feels that the more value is delivered to them.

Disadvantage – It can lead to an increase in production time since the design team may require

several iterations before it can design products that meet customer expectations and meets the set

target margin.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRICING STRATEGY

The cost-based pricing is will be based on the cost-plus pricing method, where the price

is determined by adding a profit margin to the cost of manufacturing the car models (Guerreiro

and Amaral 2018). In the given situation, the costs for producing the three models are taken on

basis of research and on basis of estimation. After determining the cost of manufacturing, the

20% profit margin is added to determine the price. Fleet discount will be deducted from the price

of respective model to determine the selling prices.

Advantages –There is a justification when there is an increase in prices, and the increased cost

can be passed on to the consumer. There is a probability of stability in prices when competitors

also adopt the same method and cost structure.

Disadvantages – There is no attempt to establish an optimum price for the product, and there is

no guarantee that a fixed profit will be earned.

Comparison for the three models –

2019 Toyota RAV4 GX 2WD Hybrid – The market selling price is high in cost-based

accounting, and cost is also minimum under cost-based. The company should implement ways to

reduce the target cost through supply chain and other factors.

2019 Toyota RAV4 GXL AWD Hybrid – For this model the price and cost, both are efficient

under market-based pricing. It must maintain the value and quality to deliver the best car at best

prices to the customer, to increase satisfaction. The company should follow market-based

costing.

The cost-based pricing is will be based on the cost-plus pricing method, where the price

is determined by adding a profit margin to the cost of manufacturing the car models (Guerreiro

and Amaral 2018). In the given situation, the costs for producing the three models are taken on

basis of research and on basis of estimation. After determining the cost of manufacturing, the

20% profit margin is added to determine the price. Fleet discount will be deducted from the price

of respective model to determine the selling prices.

Advantages –There is a justification when there is an increase in prices, and the increased cost

can be passed on to the consumer. There is a probability of stability in prices when competitors

also adopt the same method and cost structure.

Disadvantages – There is no attempt to establish an optimum price for the product, and there is

no guarantee that a fixed profit will be earned.

Comparison for the three models –

2019 Toyota RAV4 GX 2WD Hybrid – The market selling price is high in cost-based

accounting, and cost is also minimum under cost-based. The company should implement ways to

reduce the target cost through supply chain and other factors.

2019 Toyota RAV4 GXL AWD Hybrid – For this model the price and cost, both are efficient

under market-based pricing. It must maintain the value and quality to deliver the best car at best

prices to the customer, to increase satisfaction. The company should follow market-based

costing.

8PRICING STRATEGY

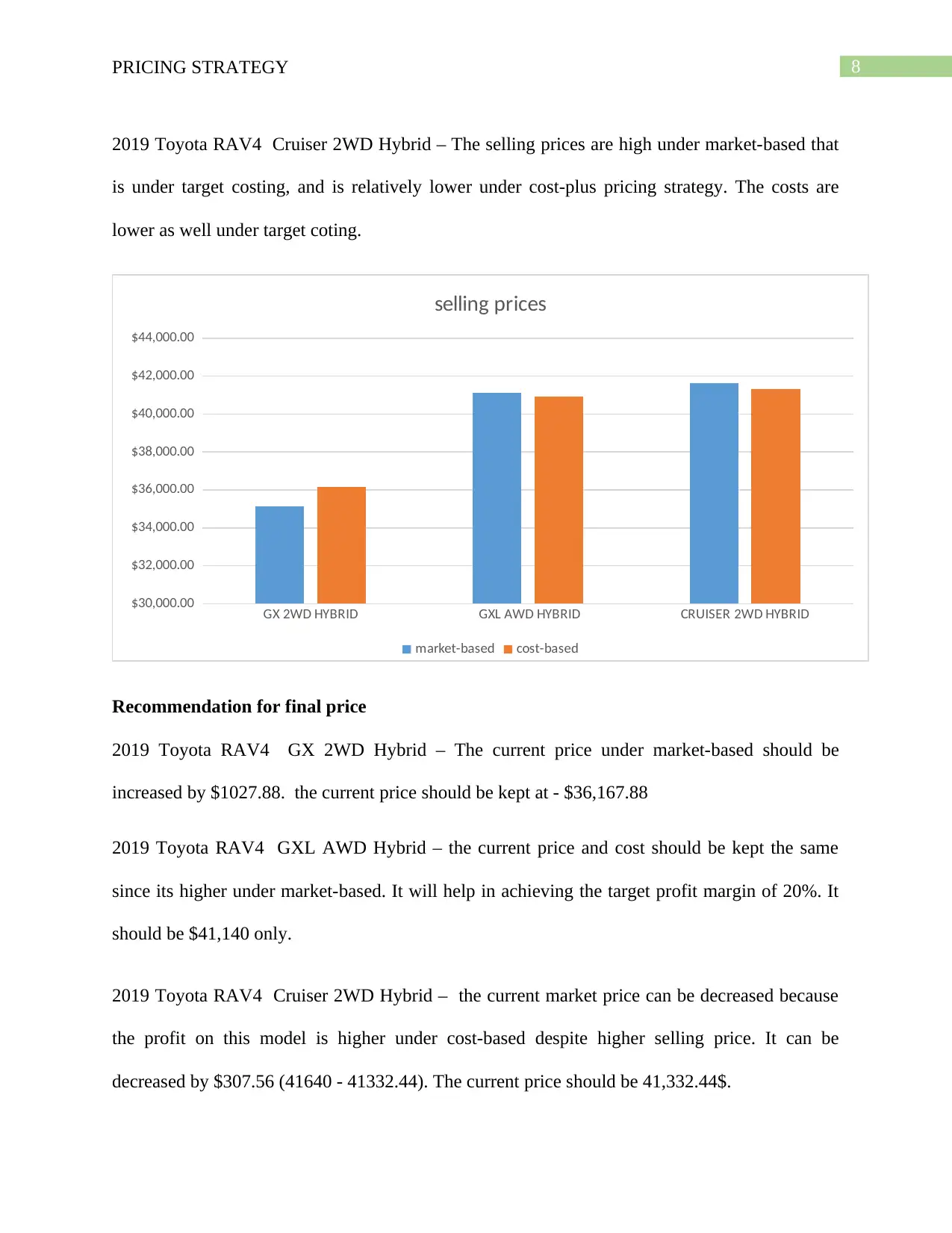

2019 Toyota RAV4 Cruiser 2WD Hybrid – The selling prices are high under market-based that

is under target costing, and is relatively lower under cost-plus pricing strategy. The costs are

lower as well under target coting.

GX 2WD HYBRID GXL AWD HYBRID CRUISER 2WD HYBRID

$30,000.00

$32,000.00

$34,000.00

$36,000.00

$38,000.00

$40,000.00

$42,000.00

$44,000.00

selling prices

market-based cost-based

Recommendation for final price

2019 Toyota RAV4 GX 2WD Hybrid – The current price under market-based should be

increased by $1027.88. the current price should be kept at - $36,167.88

2019 Toyota RAV4 GXL AWD Hybrid – the current price and cost should be kept the same

since its higher under market-based. It will help in achieving the target profit margin of 20%. It

should be $41,140 only.

2019 Toyota RAV4 Cruiser 2WD Hybrid – the current market price can be decreased because

the profit on this model is higher under cost-based despite higher selling price. It can be

decreased by $307.56 (41640 - 41332.44). The current price should be 41,332.44$.

2019 Toyota RAV4 Cruiser 2WD Hybrid – The selling prices are high under market-based that

is under target costing, and is relatively lower under cost-plus pricing strategy. The costs are

lower as well under target coting.

GX 2WD HYBRID GXL AWD HYBRID CRUISER 2WD HYBRID

$30,000.00

$32,000.00

$34,000.00

$36,000.00

$38,000.00

$40,000.00

$42,000.00

$44,000.00

selling prices

market-based cost-based

Recommendation for final price

2019 Toyota RAV4 GX 2WD Hybrid – The current price under market-based should be

increased by $1027.88. the current price should be kept at - $36,167.88

2019 Toyota RAV4 GXL AWD Hybrid – the current price and cost should be kept the same

since its higher under market-based. It will help in achieving the target profit margin of 20%. It

should be $41,140 only.

2019 Toyota RAV4 Cruiser 2WD Hybrid – the current market price can be decreased because

the profit on this model is higher under cost-based despite higher selling price. It can be

decreased by $307.56 (41640 - 41332.44). The current price should be 41,332.44$.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRICING STRATEGY

Conclusion

Therefore it can be concluded that the pricing strategy depends on the objectives of the

business. The pricing strategy of Toyota Australia is a market-based pricing strategy and is

efficient, but it should focus on cost reduction without compromising the quality and value.

There is a comparison between target costing and cost-plus pricing strategy to evaluate the

efficient price for the three models for Toyota Australia. The company should identify value-

added, and non-value added activities. The main objective is to deliver value to the customer and

to increase customer satisfaction.

Conclusion

Therefore it can be concluded that the pricing strategy depends on the objectives of the

business. The pricing strategy of Toyota Australia is a market-based pricing strategy and is

efficient, but it should focus on cost reduction without compromising the quality and value.

There is a comparison between target costing and cost-plus pricing strategy to evaluate the

efficient price for the three models for Toyota Australia. The company should identify value-

added, and non-value added activities. The main objective is to deliver value to the customer and

to increase customer satisfaction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRICING STRATEGY

References

Al-Khasawneh, S.M., Jrairah, T.S., Endut, W.A. and Rashid, N.M.N.N.M., 2019. The

Relationship between Target Costing Method and Pricing-Development of Products in Industrial

Companies. International Business and Accounting Research Journal, 3(2), pp.107-118.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

de Lautour, V.J., 2018. Product Life Cycle Accounting and Target Costing. In Strategic

Management Accounting, Volume I (pp. 55-90). Palgrave Macmillan, Cham.

Guerreiro, R. and Amaral, J.V., 2018. Cost-based price and value-based price: are they

conflicting approaches?. Journal of Business & Industrial Marketing, 33(3), pp.390-404.Hines,

P., 2016. Toyota supplier system in Japan and the UK. In Developments in Logistics and Supply

Chain Management (pp. 113-124). Palgrave Macmillan, London.

https://www.toyota.com.au/, 2020. New Cars Toyota Australia: Prices, Service Centres,

Dealers, Test Drives. [online] New Cars Toyota Australia: Prices, Service Centres, Dealers, Test

Drives. Available at: <https://www.toyota.com.au/> [Accessed 28 March 2020].

Ismail, H. and Yusof, Z.M., 2016. Perceptions towards non-value-adding activities during the

construction process. In MATEC Web of Conferences (Vol. 66, p. 00015). EDP Sciences.

Kara, S., Li, W. and Sadjiva, N., 2017. Life cycle cost analysis of electrical vehicles in

Australia. Procedia CIRP, 61, pp.767-772.

References

Al-Khasawneh, S.M., Jrairah, T.S., Endut, W.A. and Rashid, N.M.N.N.M., 2019. The

Relationship between Target Costing Method and Pricing-Development of Products in Industrial

Companies. International Business and Accounting Research Journal, 3(2), pp.107-118.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

de Lautour, V.J., 2018. Product Life Cycle Accounting and Target Costing. In Strategic

Management Accounting, Volume I (pp. 55-90). Palgrave Macmillan, Cham.

Guerreiro, R. and Amaral, J.V., 2018. Cost-based price and value-based price: are they

conflicting approaches?. Journal of Business & Industrial Marketing, 33(3), pp.390-404.Hines,

P., 2016. Toyota supplier system in Japan and the UK. In Developments in Logistics and Supply

Chain Management (pp. 113-124). Palgrave Macmillan, London.

https://www.toyota.com.au/, 2020. New Cars Toyota Australia: Prices, Service Centres,

Dealers, Test Drives. [online] New Cars Toyota Australia: Prices, Service Centres, Dealers, Test

Drives. Available at: <https://www.toyota.com.au/> [Accessed 28 March 2020].

Ismail, H. and Yusof, Z.M., 2016. Perceptions towards non-value-adding activities during the

construction process. In MATEC Web of Conferences (Vol. 66, p. 00015). EDP Sciences.

Kara, S., Li, W. and Sadjiva, N., 2017. Life cycle cost analysis of electrical vehicles in

Australia. Procedia CIRP, 61, pp.767-772.

11PRICING STRATEGY

Madoh, A., Alenazi, J., Alkhamees, L. and Panwar, A., 2019. Case Study on Market Mix

Strategies of Toyota Motor Corporation. Asia Pacific Journal of Management and

Education, 2(3), pp.70-78.

Shou, W., Wang, J., Wu, P. and Wang, X., 2020. Value adding and non-value adding activities in

turnaround maintenance process: classification, validation, and benefits. Production Planning &

Control, 31(1), pp.60-77.

Smith, A.D., 2019. JIT Inventory Management Strategy. In Handbook of Research on

Transdisciplinary Knowledge Generation (pp. 57-74). IGI Global.

Sutrisno, A., Vanany, I., Gunawan, I. and Asjad, M., 2018, April. Lean waste classification

model to support the sustainable operational practice. In IOP Conference Series: Materials

Science and Engineering (Vol. 337, No. 1, p. 012067). IOP Publishing.

Madoh, A., Alenazi, J., Alkhamees, L. and Panwar, A., 2019. Case Study on Market Mix

Strategies of Toyota Motor Corporation. Asia Pacific Journal of Management and

Education, 2(3), pp.70-78.

Shou, W., Wang, J., Wu, P. and Wang, X., 2020. Value adding and non-value adding activities in

turnaround maintenance process: classification, validation, and benefits. Production Planning &

Control, 31(1), pp.60-77.

Smith, A.D., 2019. JIT Inventory Management Strategy. In Handbook of Research on

Transdisciplinary Knowledge Generation (pp. 57-74). IGI Global.

Sutrisno, A., Vanany, I., Gunawan, I. and Asjad, M., 2018, April. Lean waste classification

model to support the sustainable operational practice. In IOP Conference Series: Materials

Science and Engineering (Vol. 337, No. 1, p. 012067). IOP Publishing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.