Critical Use of Accounting Information: TPG Telecom Limited Analysis

VerifiedAdded on 2019/10/31

|10

|1596

|162

Report

AI Summary

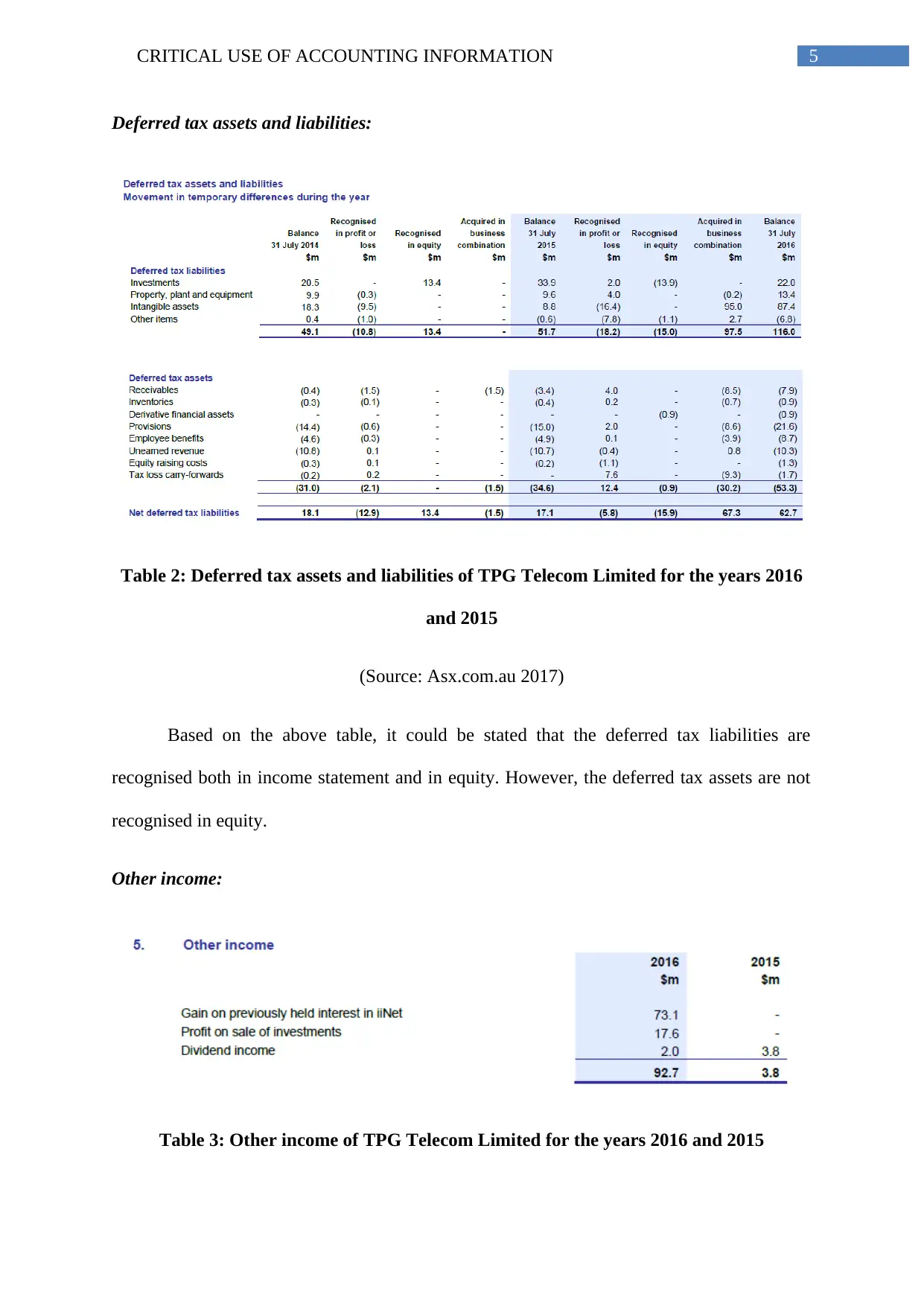

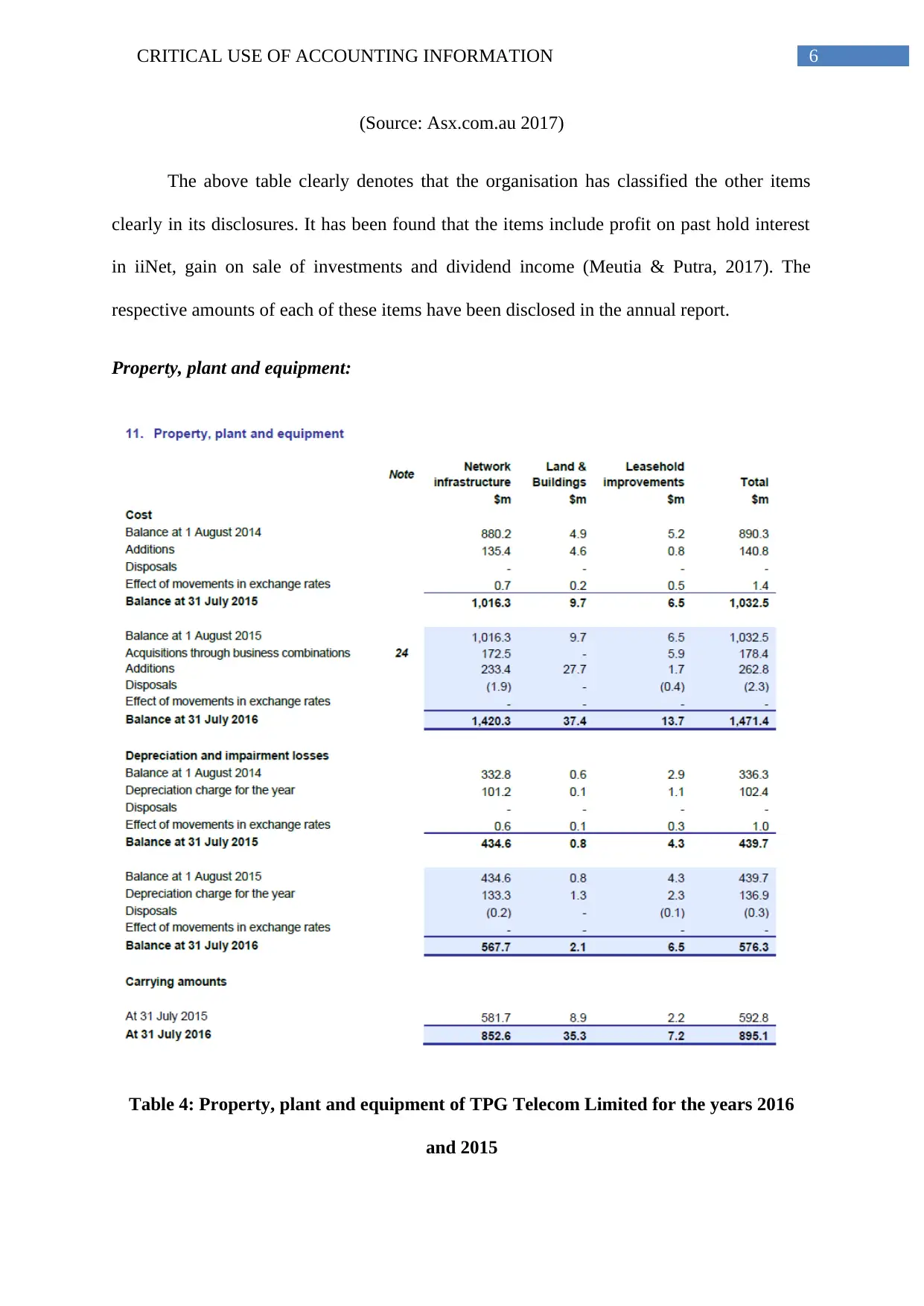

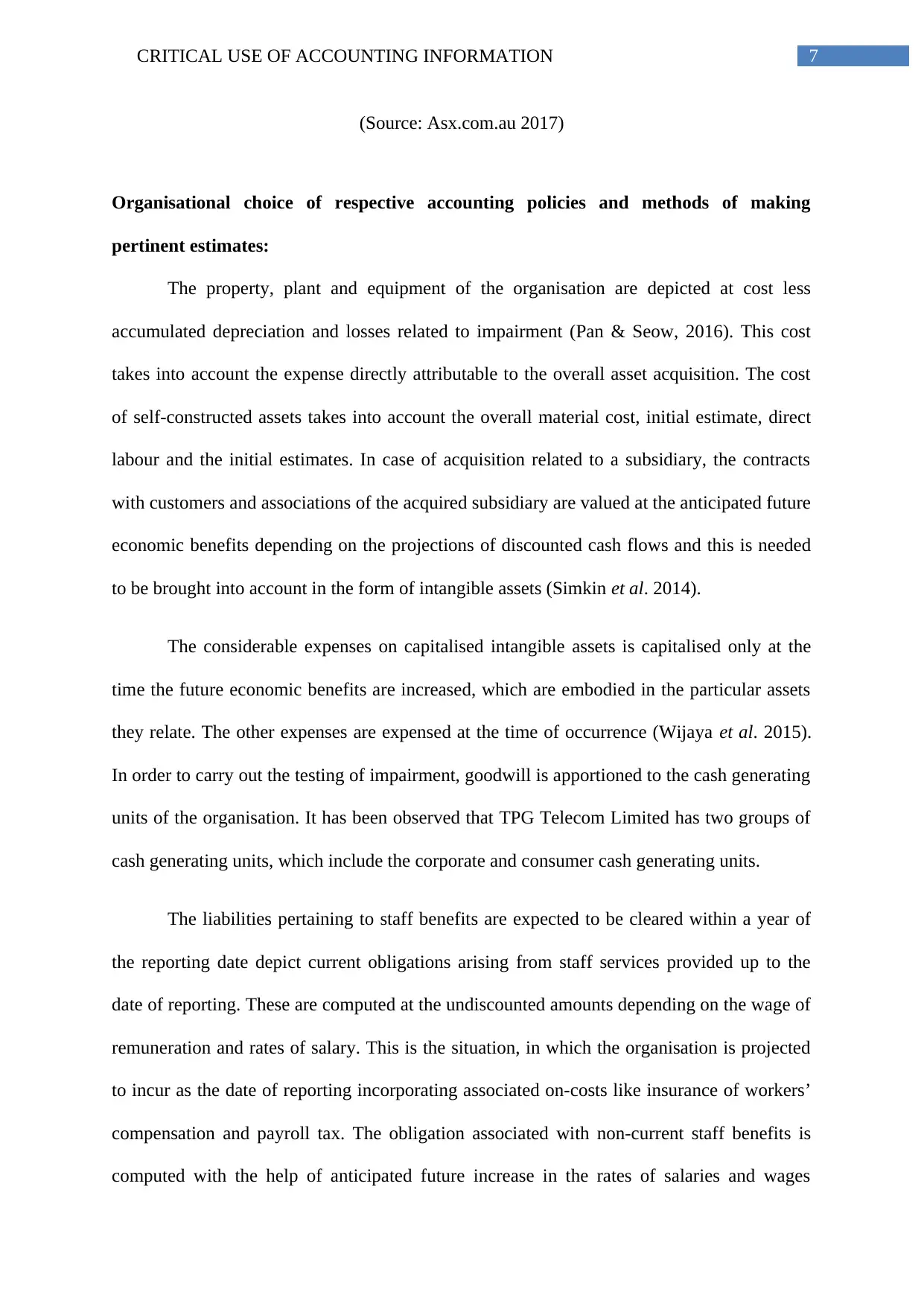

This report provides a critical analysis of accounting information, focusing on the financial performance of TPG Telecom Limited. It begins by examining the use of Return on Assets (ROA) as a key performance indicator, explaining its calculation and significance in evaluating an organization's efficiency in generating wealth from its assets. The report then delves into a detailed review of TPG Telecom Limited's financial data from 2014 to 2016, highlighting trends in ROA and identifying crucial asset categories such as property, plant, and equipment, along with deferred tax assets and liabilities that require close attention. Furthermore, it explores key income statement items, including segment reporting and other income, providing insights into how these components impact the company's overall financial position. The report also discusses the accounting policies and methods used by TPG Telecom Limited, including the valuation of property, plant, and equipment, and the treatment of staff benefits and goodwill impairment. Through this comprehensive analysis, the report offers a thorough understanding of the critical role accounting information plays in assessing the financial health and operational effectiveness of TPG Telecom Limited.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.