Accounting Theory Report: TPG Telecom Financial Analysis, 2017

VerifiedAdded on 2020/04/01

|15

|3383

|105

Report

AI Summary

This report provides a detailed analysis of TPG Telecom's accounting practices, focusing on its compliance with the AASB and IFRS frameworks. It examines the company's financial statements, accounting policies, and estimates, comparing them to those of a major competitor, Telstra. The report investigates the influence of political and economic pressures on TPG Telecom's decisions and actions. Furthermore, it assesses the accounting flexibility employed by the company's managers and evaluates the overall reporting strategy, including an investigative report on the managers' accounting strategy. The report concludes with recommendations for improvement and highlights key aspects of the company's financial reporting.

Accounting

Theory

Theory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 20 September , 2017.

1 | P a g e

By student name

Professor

University

Date: 20 September , 2017.

1 | P a g e

2

Executive summary

Preparation and presentation of the financial statements of the company as per specific conceptual

framework requirements is an important part of the overall accounting scenario and all the companies

are required to follow the same. In this report we will analyze the accounting policies and accounting

assumptions of one of the major telecommunication companies of Australia and explore whether the

books of the company are prepared based on standard regulation. Different aspects of the same will be

discussed In detail and proper recommendation will be given by which the company may improve its

overall all operations. The company in picture is TPG Telecom which one of the biggest

telecommunication company in Australia

2 | P a g e

Executive summary

Preparation and presentation of the financial statements of the company as per specific conceptual

framework requirements is an important part of the overall accounting scenario and all the companies

are required to follow the same. In this report we will analyze the accounting policies and accounting

assumptions of one of the major telecommunication companies of Australia and explore whether the

books of the company are prepared based on standard regulation. Different aspects of the same will be

discussed In detail and proper recommendation will be given by which the company may improve its

overall all operations. The company in picture is TPG Telecom which one of the biggest

telecommunication company in Australia

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Introduction…………………………………………………………………...3

Section b…..…………………………………………………………………...3

Section c…..…………………………………………………………………....6

Section d…..…………………………………………………………………...9

Conclusion………………………………………………………………………11

Refrences.....………………………………………………………………......12

3 | P a g e

Contents

Introduction…………………………………………………………………...3

Section b…..…………………………………………………………………...3

Section c…..…………………………………………………………………....6

Section d…..…………………………………………………………………...9

Conclusion………………………………………………………………………11

Refrences.....………………………………………………………………......12

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

The TPG Telecom Company is the leading telecommunication company in Australia that provides

variety of services in this field which include various mobile and dth services. It has its own mobile

network and is the second largest supplier of internet in Australia. On the basis of the annual reports of

the company the company is performing extremely well, given its high revenue and market share. The

company is also trying to expand in other areas of the world and improve its annual position (Abbott &

Kantor, 2017). It is trying to make its presence in the international market with its high data services and

efficient broad band network. The company has large number of subsidiaries that provides bundle

services to large number of companies. The accounting policies and the estimates of the company will

be discussed in brief in this report.

There are various accounting standard and provisions that has been set as per the conceptual

framework network that has been prepared by the regulatory authorities to help the company in the

preparation and presentation of their financial statements. The most important of these are US GAAP

and IFRS that has large number of provisions that the company requires to follow. The conceptual

framework is a conceptual tool that is used by companies to take conceptual decisions and make

rational choices. The IFRS is a global framework that is trying to unify the accounting policies around the

world so that all the companies follow the same method and it helps in removing barriers between the

nations (Alexander, 2016). The main purpose of these accounting policies and programs is to provide a

system of logics and ideas that can be used to provide a consistent set of various rules and standards. It

helps in defining the nature of the financial statements and sets specific rules for the same. In the given

case we will analyze the annual report of the stated company.

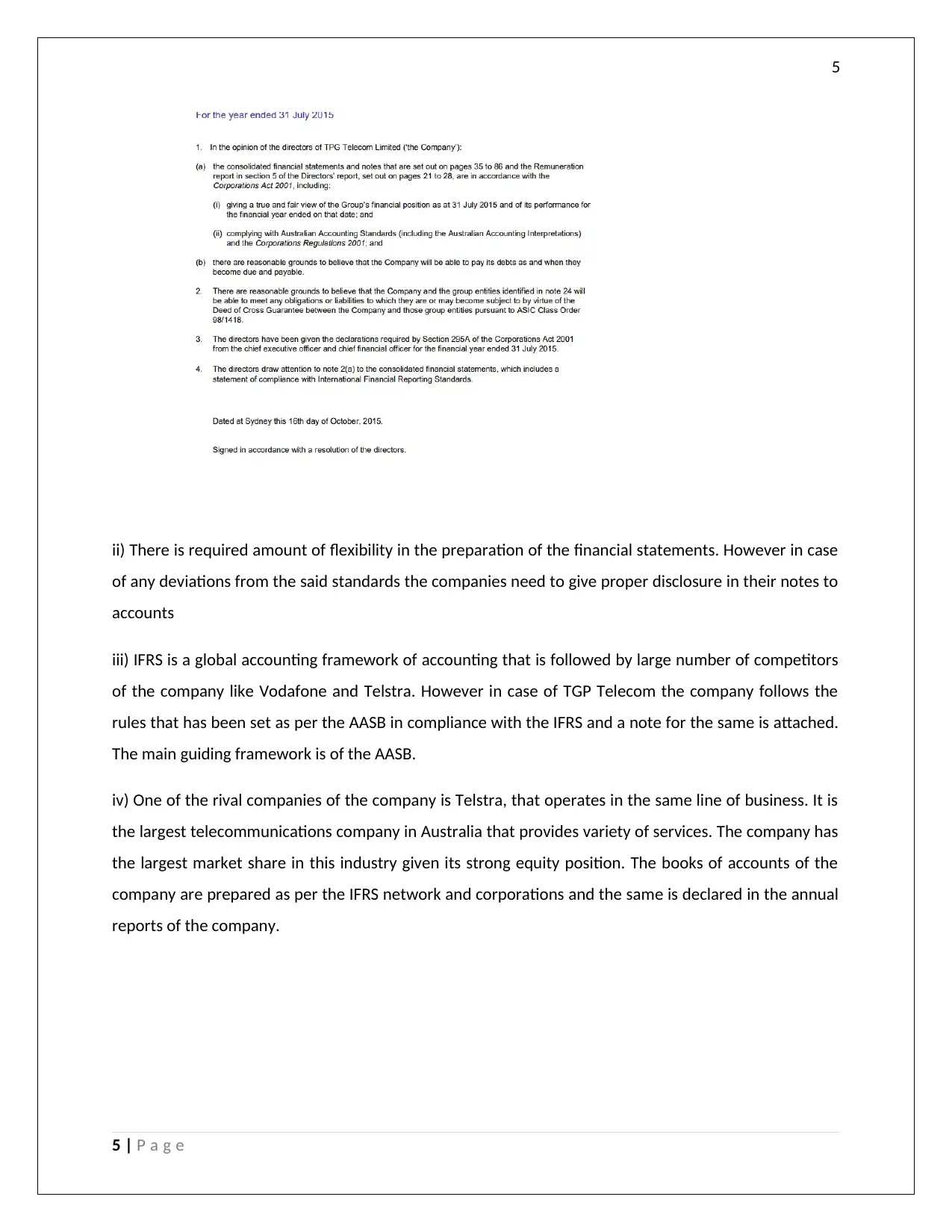

Section b

i. The consolidated statements of the company are prepared as per the AASB 101 conceptual

framework of accounting which has been issued by the Australian Accounting Standard Board .

The books of the company are prepared as per the IFRS and the same has been followed very

accurately. All the notes of account are accurate and proper disclosures has been given by the

company. The accounting policies of the firm are stated in the report of the director, an extract

of the same is attached below.

4 | P a g e

Introduction

The TPG Telecom Company is the leading telecommunication company in Australia that provides

variety of services in this field which include various mobile and dth services. It has its own mobile

network and is the second largest supplier of internet in Australia. On the basis of the annual reports of

the company the company is performing extremely well, given its high revenue and market share. The

company is also trying to expand in other areas of the world and improve its annual position (Abbott &

Kantor, 2017). It is trying to make its presence in the international market with its high data services and

efficient broad band network. The company has large number of subsidiaries that provides bundle

services to large number of companies. The accounting policies and the estimates of the company will

be discussed in brief in this report.

There are various accounting standard and provisions that has been set as per the conceptual

framework network that has been prepared by the regulatory authorities to help the company in the

preparation and presentation of their financial statements. The most important of these are US GAAP

and IFRS that has large number of provisions that the company requires to follow. The conceptual

framework is a conceptual tool that is used by companies to take conceptual decisions and make

rational choices. The IFRS is a global framework that is trying to unify the accounting policies around the

world so that all the companies follow the same method and it helps in removing barriers between the

nations (Alexander, 2016). The main purpose of these accounting policies and programs is to provide a

system of logics and ideas that can be used to provide a consistent set of various rules and standards. It

helps in defining the nature of the financial statements and sets specific rules for the same. In the given

case we will analyze the annual report of the stated company.

Section b

i. The consolidated statements of the company are prepared as per the AASB 101 conceptual

framework of accounting which has been issued by the Australian Accounting Standard Board .

The books of the company are prepared as per the IFRS and the same has been followed very

accurately. All the notes of account are accurate and proper disclosures has been given by the

company. The accounting policies of the firm are stated in the report of the director, an extract

of the same is attached below.

4 | P a g e

5

ii) There is required amount of flexibility in the preparation of the financial statements. However in case

of any deviations from the said standards the companies need to give proper disclosure in their notes to

accounts

iii) IFRS is a global accounting framework of accounting that is followed by large number of competitors

of the company like Vodafone and Telstra. However in case of TGP Telecom the company follows the

rules that has been set as per the AASB in compliance with the IFRS and a note for the same is attached.

The main guiding framework is of the AASB.

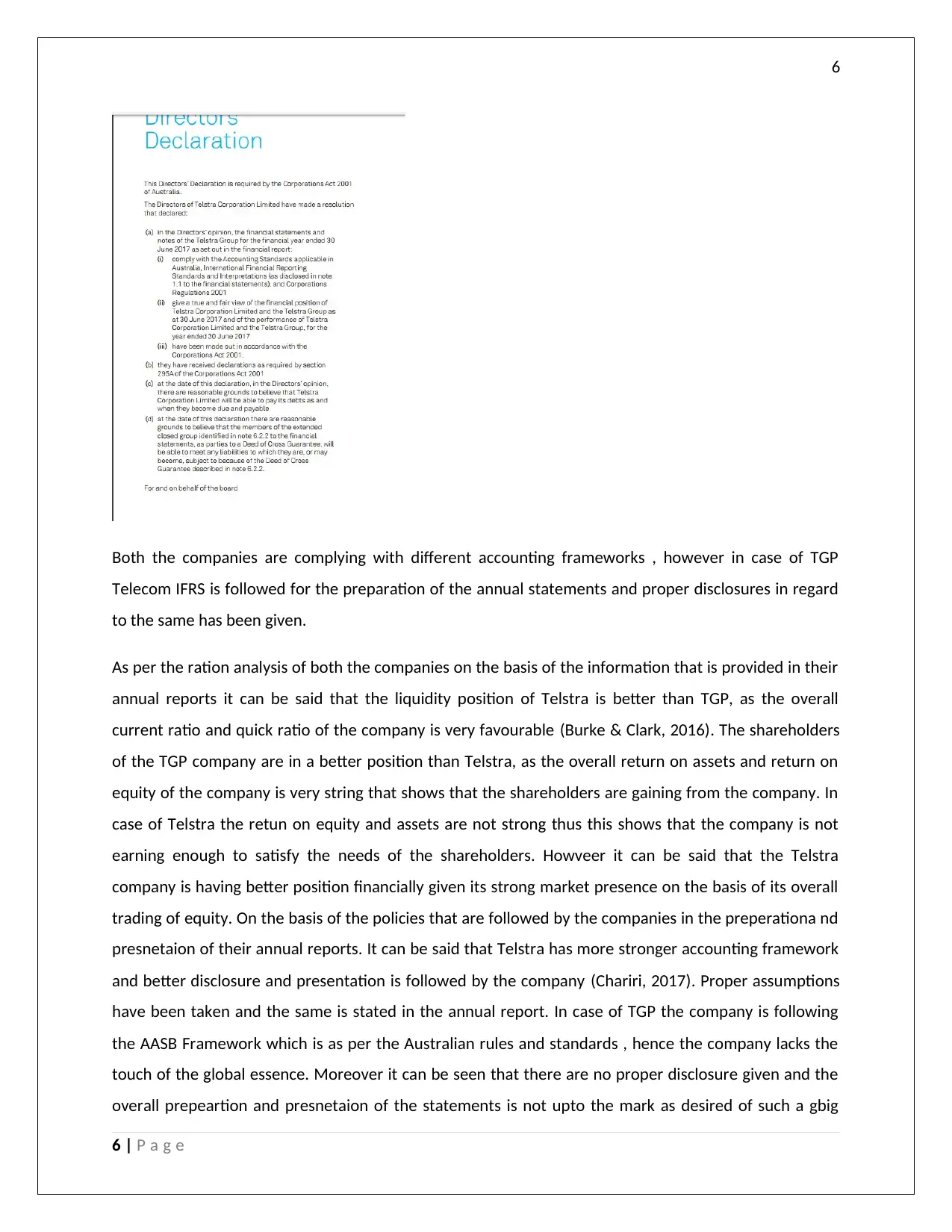

iv) One of the rival companies of the company is Telstra, that operates in the same line of business. It is

the largest telecommunications company in Australia that provides variety of services. The company has

the largest market share in this industry given its strong equity position. The books of accounts of the

company are prepared as per the IFRS network and corporations and the same is declared in the annual

reports of the company.

5 | P a g e

ii) There is required amount of flexibility in the preparation of the financial statements. However in case

of any deviations from the said standards the companies need to give proper disclosure in their notes to

accounts

iii) IFRS is a global accounting framework of accounting that is followed by large number of competitors

of the company like Vodafone and Telstra. However in case of TGP Telecom the company follows the

rules that has been set as per the AASB in compliance with the IFRS and a note for the same is attached.

The main guiding framework is of the AASB.

iv) One of the rival companies of the company is Telstra, that operates in the same line of business. It is

the largest telecommunications company in Australia that provides variety of services. The company has

the largest market share in this industry given its strong equity position. The books of accounts of the

company are prepared as per the IFRS network and corporations and the same is declared in the annual

reports of the company.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Both the companies are complying with different accounting frameworks , however in case of TGP

Telecom IFRS is followed for the preparation of the annual statements and proper disclosures in regard

to the same has been given.

As per the ration analysis of both the companies on the basis of the information that is provided in their

annual reports it can be said that the liquidity position of Telstra is better than TGP, as the overall

current ratio and quick ratio of the company is very favourable (Burke & Clark, 2016). The shareholders

of the TGP company are in a better position than Telstra, as the overall return on assets and return on

equity of the company is very string that shows that the shareholders are gaining from the company. In

case of Telstra the retun on equity and assets are not strong thus this shows that the company is not

earning enough to satisfy the needs of the shareholders. Howveer it can be said that the Telstra

company is having better position financially given its strong market presence on the basis of its overall

trading of equity. On the basis of the policies that are followed by the companies in the preperationa nd

presnetaion of their annual reports. It can be said that Telstra has more stronger accounting framework

and better disclosure and presentation is followed by the company (Chariri, 2017). Proper assumptions

have been taken and the same is stated in the annual report. In case of TGP the company is following

the AASB Framework which is as per the Australian rules and standards , hence the company lacks the

touch of the global essence. Moreover it can be seen that there are no proper disclosure given and the

overall prepeartion and presnetaion of the statements is not upto the mark as desired of such a gbig

6 | P a g e

Both the companies are complying with different accounting frameworks , however in case of TGP

Telecom IFRS is followed for the preparation of the annual statements and proper disclosures in regard

to the same has been given.

As per the ration analysis of both the companies on the basis of the information that is provided in their

annual reports it can be said that the liquidity position of Telstra is better than TGP, as the overall

current ratio and quick ratio of the company is very favourable (Burke & Clark, 2016). The shareholders

of the TGP company are in a better position than Telstra, as the overall return on assets and return on

equity of the company is very string that shows that the shareholders are gaining from the company. In

case of Telstra the retun on equity and assets are not strong thus this shows that the company is not

earning enough to satisfy the needs of the shareholders. Howveer it can be said that the Telstra

company is having better position financially given its strong market presence on the basis of its overall

trading of equity. On the basis of the policies that are followed by the companies in the preperationa nd

presnetaion of their annual reports. It can be said that Telstra has more stronger accounting framework

and better disclosure and presentation is followed by the company (Chariri, 2017). Proper assumptions

have been taken and the same is stated in the annual report. In case of TGP the company is following

the AASB Framework which is as per the Australian rules and standards , hence the company lacks the

touch of the global essence. Moreover it can be seen that there are no proper disclosure given and the

overall prepeartion and presnetaion of the statements is not upto the mark as desired of such a gbig

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

company. In comparison of both the company, the policies of Telstra are more stronger than the TGP

Telecom company (Crosby & Henneberry, 2016).

iv) Yes I agree with the polices and estimates. No matter what accounting framework does the

companies follow they need to comply with all the relevant accounting assumptions and proper

disclosures must be given in their notes to accounts.

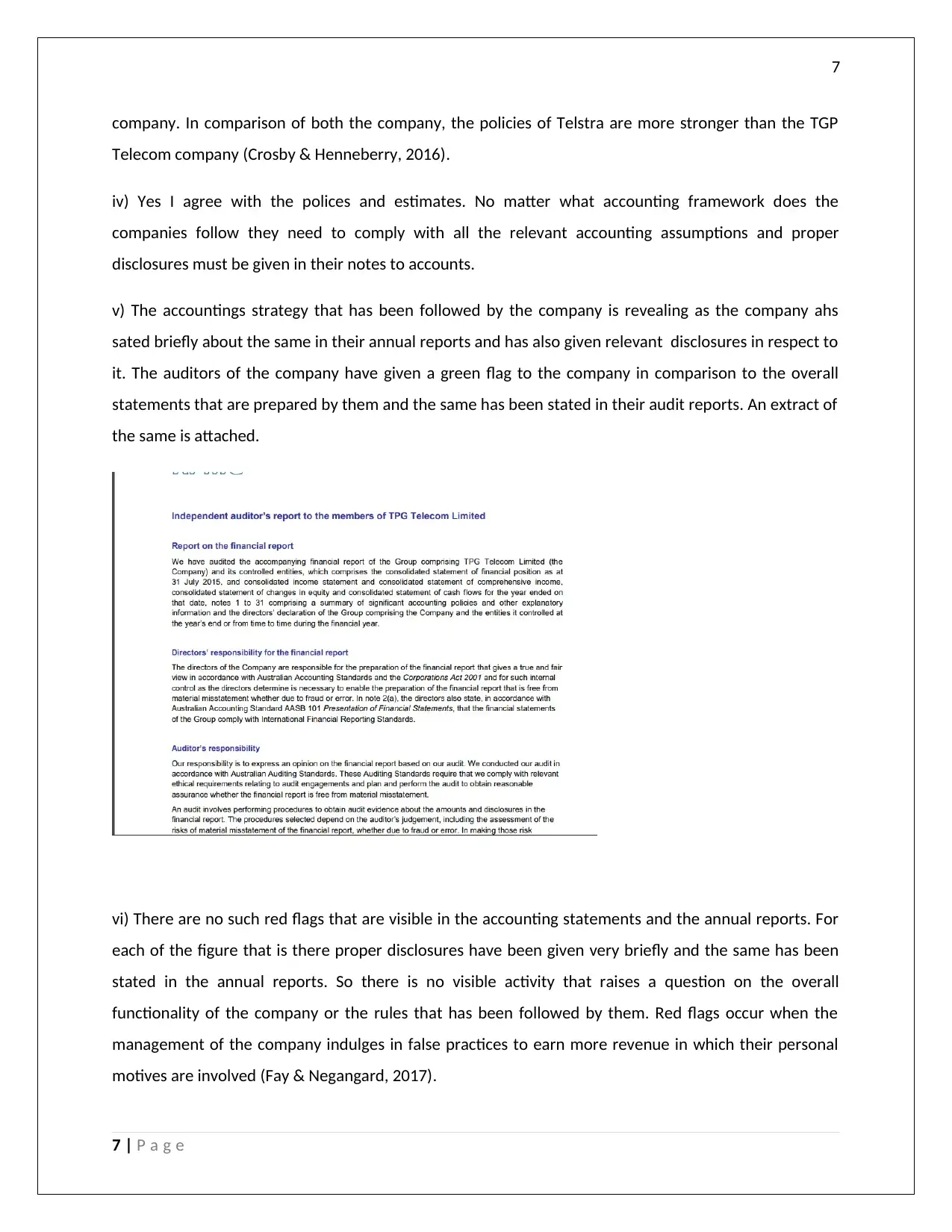

v) The accountings strategy that has been followed by the company is revealing as the company ahs

sated briefly about the same in their annual reports and has also given relevant disclosures in respect to

it. The auditors of the company have given a green flag to the company in comparison to the overall

statements that are prepared by them and the same has been stated in their audit reports. An extract of

the same is attached.

vi) There are no such red flags that are visible in the accounting statements and the annual reports. For

each of the figure that is there proper disclosures have been given very briefly and the same has been

stated in the annual reports. So there is no visible activity that raises a question on the overall

functionality of the company or the rules that has been followed by them. Red flags occur when the

management of the company indulges in false practices to earn more revenue in which their personal

motives are involved (Fay & Negangard, 2017).

7 | P a g e

company. In comparison of both the company, the policies of Telstra are more stronger than the TGP

Telecom company (Crosby & Henneberry, 2016).

iv) Yes I agree with the polices and estimates. No matter what accounting framework does the

companies follow they need to comply with all the relevant accounting assumptions and proper

disclosures must be given in their notes to accounts.

v) The accountings strategy that has been followed by the company is revealing as the company ahs

sated briefly about the same in their annual reports and has also given relevant disclosures in respect to

it. The auditors of the company have given a green flag to the company in comparison to the overall

statements that are prepared by them and the same has been stated in their audit reports. An extract of

the same is attached.

vi) There are no such red flags that are visible in the accounting statements and the annual reports. For

each of the figure that is there proper disclosures have been given very briefly and the same has been

stated in the annual reports. So there is no visible activity that raises a question on the overall

functionality of the company or the rules that has been followed by them. Red flags occur when the

management of the company indulges in false practices to earn more revenue in which their personal

motives are involved (Fay & Negangard, 2017).

7 | P a g e

8

Section c

i)There are many pressures that exist on these companies that influence their overall decisions

and actions. The major political influences that affect the functioning of the company and their overall

operations are that there are a lot of regulations that are very complex in nature and that the companies

have to comply with. The major issues are present in the various trade barriers, complex networks,

national radio spectrums that affect the position of these companies in the market (Fay & Negangard,

2017). The companies need to comply with all these and in any case if they fail they will be penalized.

The only political factors that are working in the favor of these companies are deregulation and

privatization. Deregulation and privatization helps the company to avoid unwanted political interference

and hence help them in doing their work as per their own wish (Prasad & Chand, 2017).

ii) Every company makes certain accounting assumptions while prepration of their financial

ststemnts and gives the relevant disclosures for the same. The companies needs to prove the main logic

behind these estimate and how it is reasonable for them (Dichev, 2017). The same thought must be

supported by the auditors and it should be in line with the guidng conceptual framework that the

company is following. In any case if the company has made certain estimates but no disclosure is given

in regard to the same than the company will be held liable and in the long run they have to justify their

action. In case of TGP the company has made certain assumptions and gave relevant disclosures for the

same. These are mianly stated in the notes to account of the company, relevant disclosures in regard to

the same has been in it.

8 | P a g e

Section c

i)There are many pressures that exist on these companies that influence their overall decisions

and actions. The major political influences that affect the functioning of the company and their overall

operations are that there are a lot of regulations that are very complex in nature and that the companies

have to comply with. The major issues are present in the various trade barriers, complex networks,

national radio spectrums that affect the position of these companies in the market (Fay & Negangard,

2017). The companies need to comply with all these and in any case if they fail they will be penalized.

The only political factors that are working in the favor of these companies are deregulation and

privatization. Deregulation and privatization helps the company to avoid unwanted political interference

and hence help them in doing their work as per their own wish (Prasad & Chand, 2017).

ii) Every company makes certain accounting assumptions while prepration of their financial

ststemnts and gives the relevant disclosures for the same. The companies needs to prove the main logic

behind these estimate and how it is reasonable for them (Dichev, 2017). The same thought must be

supported by the auditors and it should be in line with the guidng conceptual framework that the

company is following. In any case if the company has made certain estimates but no disclosure is given

in regard to the same than the company will be held liable and in the long run they have to justify their

action. In case of TGP the company has made certain assumptions and gave relevant disclosures for the

same. These are mianly stated in the notes to account of the company, relevant disclosures in regard to

the same has been in it.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

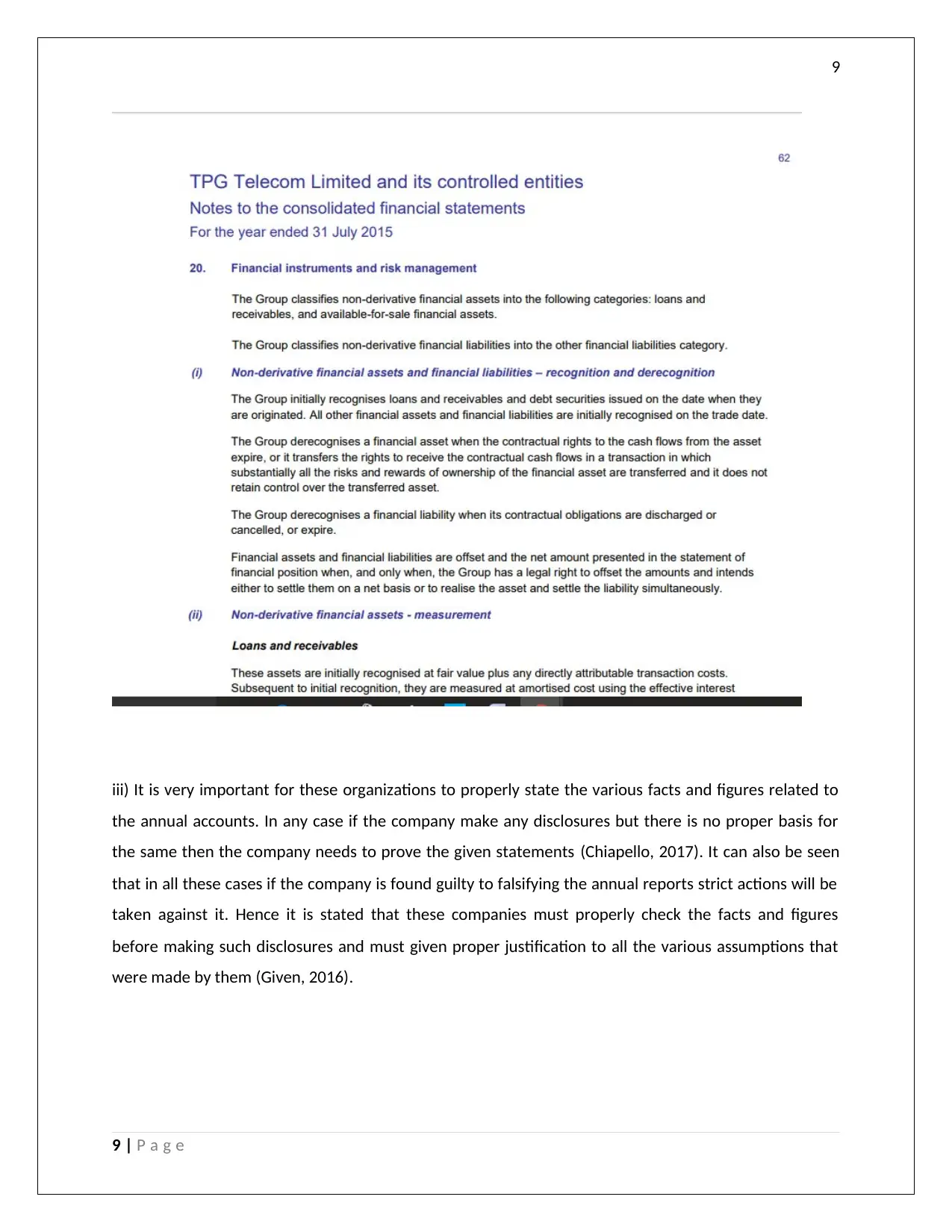

iii) It is very important for these organizations to properly state the various facts and figures related to

the annual accounts. In any case if the company make any disclosures but there is no proper basis for

the same then the company needs to prove the given statements (Chiapello, 2017). It can also be seen

that in all these cases if the company is found guilty to falsifying the annual reports strict actions will be

taken against it. Hence it is stated that these companies must properly check the facts and figures

before making such disclosures and must given proper justification to all the various assumptions that

were made by them (Given, 2016).

9 | P a g e

iii) It is very important for these organizations to properly state the various facts and figures related to

the annual accounts. In any case if the company make any disclosures but there is no proper basis for

the same then the company needs to prove the given statements (Chiapello, 2017). It can also be seen

that in all these cases if the company is found guilty to falsifying the annual reports strict actions will be

taken against it. Hence it is stated that these companies must properly check the facts and figures

before making such disclosures and must given proper justification to all the various assumptions that

were made by them (Given, 2016).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Section d. Investigative report on the Managers’ Accounting Strategy and Reporting Strategy

The managers of the company are the main people who are given the responsibility to supervise the

overall formulation and presentation of the annual reports of the company. In case the auditors find any

issues then the managers need to help the auditors in solving the same. In the given case we will

prepare a report on the overall actions of the managers and the necessary steps that can be taken by

them

Section 1: key accounting policies

In the given company the books of the company are prepared as the AASB framework in compliance

with the IFRS in the preparation and presentation of the annual reports of the company. Relevant

disclosures have been given in the various notes to account and the company has also attached proper

declaration for all the actions that has been taken by them. In any case if the company malpractices than

the management of the company will be held liable (Guragai, et al., 2017). The managers must see that

all the disclosures are clear and price and in any case if they notice any red flags immediate actions must

be taken for the same. Proper presentation and disclosure is very important for the overall success of

the company (Crosby & Henneberry, 2016).

Section 2: Assess Accounting Flexibility

In case the managers of the company are not able to follow a single rule for the preparation of the

consolidated statements there are high chances that the information will be distorted. It will lead to lack

of uniformity in the accounts over the years, and the companies may not be able to follow a single path

for their analysis (Han, et al., 2017). It is thus important that the managers do not indulge in large

amount of fluctuations, a single accounting framework must be followed over the years that makes the

overall accounting clear and free from all kind of distortions and will be helpful for the investors also as

they will be able to make necessary comparisons while taking important decisions in regard to the

company and its operations.

Section 3: Evaluation of the Accounting Strategies

If there is high amount of flexibility involved in the overall preparation of the financial statements than

that might lead to huge amount of distortions and sometimes it is good also because the managers will

10 | P a g e

Section d. Investigative report on the Managers’ Accounting Strategy and Reporting Strategy

The managers of the company are the main people who are given the responsibility to supervise the

overall formulation and presentation of the annual reports of the company. In case the auditors find any

issues then the managers need to help the auditors in solving the same. In the given case we will

prepare a report on the overall actions of the managers and the necessary steps that can be taken by

them

Section 1: key accounting policies

In the given company the books of the company are prepared as the AASB framework in compliance

with the IFRS in the preparation and presentation of the annual reports of the company. Relevant

disclosures have been given in the various notes to account and the company has also attached proper

declaration for all the actions that has been taken by them. In any case if the company malpractices than

the management of the company will be held liable (Guragai, et al., 2017). The managers must see that

all the disclosures are clear and price and in any case if they notice any red flags immediate actions must

be taken for the same. Proper presentation and disclosure is very important for the overall success of

the company (Crosby & Henneberry, 2016).

Section 2: Assess Accounting Flexibility

In case the managers of the company are not able to follow a single rule for the preparation of the

consolidated statements there are high chances that the information will be distorted. It will lead to lack

of uniformity in the accounts over the years, and the companies may not be able to follow a single path

for their analysis (Han, et al., 2017). It is thus important that the managers do not indulge in large

amount of fluctuations, a single accounting framework must be followed over the years that makes the

overall accounting clear and free from all kind of distortions and will be helpful for the investors also as

they will be able to make necessary comparisons while taking important decisions in regard to the

company and its operations.

Section 3: Evaluation of the Accounting Strategies

If there is high amount of flexibility involved in the overall preparation of the financial statements than

that might lead to huge amount of distortions and sometimes it is good also because the managers will

10 | P a g e

11

be able to convey such economic decisions that they otherwise might not be able to convey to people.

This is where the decision making abilities of the management comes into play and can be helpful in the

long run. It is important that the mangers use the standards that are as per the industry guidelines and

norms (Kew & Stredwick, 2017). It is important that there must not be any personal motives involved in

case of the managers. In case the management is considering changes in the accounting policies then

there must be basis for the same and the rationality must be established. It must be seen whether

certain transactions have been structured to achieve particular objectives of the company. Like in case

of TGP we see that the consolidated financial statements the same has been prepared on the basis of

historical cost, except the all over assets and the liabilities that have been valued on the basis of the fair

value. This is done to make the correct valuation of the assets of the company (Laursen & Thorlund,

2016).

Section 4: Evaluation of the Quality of disclosure

It is important for the mangers of the company to see whether all the disclosures that has been given is

in line with the accounting standards that has been followed. In case of TGP all the necessary disclosures

are adequate and price. They are sufficient with the current norms. The US GAAP do not restricts the

company with respect to the disclosures they can make. Proper segment disclosures have been done in

case of TGP as per the respective guidelines (Maynard, 2017).

Section 5: Identify Potential Red Flags

Red flags refer to certain disclosures in the accounts of the company that are not relevant and

consistent with the activities of the company. It is an indication that there might be certain malpractices

on part of the management that might hamper their overall performance (Minnis & Sutherland, 2017).

But in this case we see that there are no potential red flags in the system that might affect their

performance. The company has given relevant disclosures for the all their actions and all is properly

defined (Birt, et al., 2017).

Section 6: Compliant with the Conceptual Framework

In this report we can say that the company has complied with the relevant accounting framework and

has given proper disclosures in regard to the same. The fact has been supported by the management of

the company and relevant actions have been taken to make sure that the books are free from all kind of

errors and issues (Sweeting, 2017).

11 | P a g e

be able to convey such economic decisions that they otherwise might not be able to convey to people.

This is where the decision making abilities of the management comes into play and can be helpful in the

long run. It is important that the mangers use the standards that are as per the industry guidelines and

norms (Kew & Stredwick, 2017). It is important that there must not be any personal motives involved in

case of the managers. In case the management is considering changes in the accounting policies then

there must be basis for the same and the rationality must be established. It must be seen whether

certain transactions have been structured to achieve particular objectives of the company. Like in case

of TGP we see that the consolidated financial statements the same has been prepared on the basis of

historical cost, except the all over assets and the liabilities that have been valued on the basis of the fair

value. This is done to make the correct valuation of the assets of the company (Laursen & Thorlund,

2016).

Section 4: Evaluation of the Quality of disclosure

It is important for the mangers of the company to see whether all the disclosures that has been given is

in line with the accounting standards that has been followed. In case of TGP all the necessary disclosures

are adequate and price. They are sufficient with the current norms. The US GAAP do not restricts the

company with respect to the disclosures they can make. Proper segment disclosures have been done in

case of TGP as per the respective guidelines (Maynard, 2017).

Section 5: Identify Potential Red Flags

Red flags refer to certain disclosures in the accounts of the company that are not relevant and

consistent with the activities of the company. It is an indication that there might be certain malpractices

on part of the management that might hamper their overall performance (Minnis & Sutherland, 2017).

But in this case we see that there are no potential red flags in the system that might affect their

performance. The company has given relevant disclosures for the all their actions and all is properly

defined (Birt, et al., 2017).

Section 6: Compliant with the Conceptual Framework

In this report we can say that the company has complied with the relevant accounting framework and

has given proper disclosures in regard to the same. The fact has been supported by the management of

the company and relevant actions have been taken to make sure that the books are free from all kind of

errors and issues (Sweeting, 2017).

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.