TPG Telecom Limited: Audit, Assurance, and Compliance Evaluation

VerifiedAdded on 2023/06/05

|14

|3514

|264

Report

AI Summary

This report evaluates the compliance of TPG Telecom Limited with various provisions and regulations related to the audit of financial statements, including enhanced audit reporting requirements for listed companies. It discusses auditor independence, transparency in reporting, non-audit services, and auditor remuneration. The report also examines the role, functions, and composition of the Audit Committee, the independent auditor's report to shareholders, and a review of key audit matters and associated audit procedures. The analysis indicates that while all compliances have been followed, there is room for improvement in clarity regarding non-audit services and the composition and role of audit committees. The audit was conducted by KPMG, who provided an unqualified opinion on TPG Telecom's financial statements.

Audit, Assurance and Compliance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Evaluating the compliance of various provisions and regulations related to audit of financial

statements has been done in this report. In addition to this, enhanced audit reporting requirements

that have been followed by listed companies has also been studied. The company chosen for this

purpose is TPG Telecom Limited.

Discussion on independence of an auditor and how can the reporting be made more transparent

has been done in this report. Matters related to non-audit services and remuneration has also been

discussed.

Evaluating the compliance of various provisions and regulations related to audit of financial

statements has been done in this report. In addition to this, enhanced audit reporting requirements

that have been followed by listed companies has also been studied. The company chosen for this

purpose is TPG Telecom Limited.

Discussion on independence of an auditor and how can the reporting be made more transparent

has been done in this report. Matters related to non-audit services and remuneration has also been

discussed.

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Conclusion...................................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration....................................................................................4

2) Independent auditor’s report.................................................................................................6

3) Non-Audit services performed by the Auditor.....................................................................7

4) Auditors’ Remuneration.......................................................................................................8

5) Role, functions and composition of the Audit Committee...................................................9

6) Independent Auditors report to the members (shareholders).............................................10

7) Review all Key Audit Matters noted and the associated audit procedures.........................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction

Background of the Report

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Conclusion...................................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration....................................................................................4

2) Independent auditor’s report.................................................................................................6

3) Non-Audit services performed by the Auditor.....................................................................7

4) Auditors’ Remuneration.......................................................................................................8

5) Role, functions and composition of the Audit Committee...................................................9

6) Independent Auditors report to the members (shareholders).............................................10

7) Review all Key Audit Matters noted and the associated audit procedures.........................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction

Background of the Report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

One of the most essential aspects that an auditor is required to keep in mind is that the reporting

of the audit matters must be done cautiously. There are several laws that have been framed by the

regulatory authorities of different countries across the world. The auditors are required to

conduct audit based on such laws and regulations. Thus, this report analyses transparency in

reporting by the auditors.

Scope of the Project

This report discusses transparency in reporting through seven headings, which are, Independent

Auditor’s Report; Audit Committee; Non-audit services given by the auditor; Auditor’s

Remuneration; Auditor’s Independence Declaration; Independent Auditor’s Report to the

members of the company and; Key Audit Matters Review.

Conclusion

All the compliances have been followed. However, more clarity can be given on non audit

services performed and composition and role of audit committees

Discussion

1) Auditor’s Independence Declaration

In Australia, the auditors of the companies are required to follow the provisions specified in the

Corporations Act, 2001 (CCH Australia Limited, 2011). One of the major compliances that an

auditor is required to comply with is related to the independence of an auditor. An auditor is

supposed to act independently from the company in which he is performing the audit. This is

necessary as per the rules specified in the act and regulations prescribed by the professional

bodies. The auditing standards that have been issued also stress on independence of an auditor

and further require the auditor to act vigilantly and keeping away all sorts of biasness while

framing an audit opinion based on his audit (CAANZ, 2016). Opinion given by the auditors can

of the audit matters must be done cautiously. There are several laws that have been framed by the

regulatory authorities of different countries across the world. The auditors are required to

conduct audit based on such laws and regulations. Thus, this report analyses transparency in

reporting by the auditors.

Scope of the Project

This report discusses transparency in reporting through seven headings, which are, Independent

Auditor’s Report; Audit Committee; Non-audit services given by the auditor; Auditor’s

Remuneration; Auditor’s Independence Declaration; Independent Auditor’s Report to the

members of the company and; Key Audit Matters Review.

Conclusion

All the compliances have been followed. However, more clarity can be given on non audit

services performed and composition and role of audit committees

Discussion

1) Auditor’s Independence Declaration

In Australia, the auditors of the companies are required to follow the provisions specified in the

Corporations Act, 2001 (CCH Australia Limited, 2011). One of the major compliances that an

auditor is required to comply with is related to the independence of an auditor. An auditor is

supposed to act independently from the company in which he is performing the audit. This is

necessary as per the rules specified in the act and regulations prescribed by the professional

bodies. The auditing standards that have been issued also stress on independence of an auditor

and further require the auditor to act vigilantly and keeping away all sorts of biasness while

framing an audit opinion based on his audit (CAANZ, 2016). Opinion given by the auditors can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be considered as reliable only when he has declared himself independent from the company and

proved that there has been no personal interest while giving audit opinion.

In Australia, various laws have been framed for ensuring that the auditor remains independent

throughout the audit phase and such regulations have to be adhered to by all auditors. Laws

framed with respect to independence of an auditor include the following:

The auditor is required to present a statement in the annual report of the company

declaring his independence from the company in which he is appointed as the auditor.

This requirement is to be fulfilled as per section 307C that of the Corporations Act, 2001.

. As per the provisions that have been framed in this section, an auditor of a company

must declare compulsorily that he is performing the audit independently from the

company. This particular information is required to be given in the Independence

Declaration by the auditor of the company. In addition to thus, various other provisions

have also been specified in this act. One of them is the Divisions 3, 4 and 5 of Part 2M.4

(Wolters Kluwer, 2018).

Some other provisions have also been framed in addition to the Corporations Act, 2001,

which must be followed while performing the audit. One such standard is APES 110

which includes some ethical codes of conduct which apply to the auditors of an

organization. As per the standard, the auditor must declare his independence. In addition,

they must also state that they have been following ethics through the audit procedures. A

declaration of independence is required to inform shareholders and members of the

company that audit has been completed by discharging duties with utmost care and all the

ethical responsibilities have been fulfilled throughout the assignment (Australian

Government, 2018).

proved that there has been no personal interest while giving audit opinion.

In Australia, various laws have been framed for ensuring that the auditor remains independent

throughout the audit phase and such regulations have to be adhered to by all auditors. Laws

framed with respect to independence of an auditor include the following:

The auditor is required to present a statement in the annual report of the company

declaring his independence from the company in which he is appointed as the auditor.

This requirement is to be fulfilled as per section 307C that of the Corporations Act, 2001.

. As per the provisions that have been framed in this section, an auditor of a company

must declare compulsorily that he is performing the audit independently from the

company. This particular information is required to be given in the Independence

Declaration by the auditor of the company. In addition to thus, various other provisions

have also been specified in this act. One of them is the Divisions 3, 4 and 5 of Part 2M.4

(Wolters Kluwer, 2018).

Some other provisions have also been framed in addition to the Corporations Act, 2001,

which must be followed while performing the audit. One such standard is APES 110

which includes some ethical codes of conduct which apply to the auditors of an

organization. As per the standard, the auditor must declare his independence. In addition,

they must also state that they have been following ethics through the audit procedures. A

declaration of independence is required to inform shareholders and members of the

company that audit has been completed by discharging duties with utmost care and all the

ethical responsibilities have been fulfilled throughout the assignment (Australian

Government, 2018).

The audit of TPG Telecom Limited has been carried out by KPMG and they served as the lead

auditor of the company. The auditors have given a declaration of independence in the auditor’s

report attached with annual report of the company. This statement by the auditor’s states that

they have complied with the provisions of Corporation Act 2001 and also they have followed the

ethical code of conduct as has been mentioned in APES 110. They have also stated that there

have been no contraventions in both the requirements. As stated in the code of ethics, auditors

have been careful to apply them throughout the audit. The requirement to give a statement of

declaration is given under the Corporations Act, 2001. The declaration is given on page number

36 of the annual report (TPG Telecom Limited, 2017).

2) Independent auditor’s report

The main reason behind appointing an external auditor to audit the financial statements of a

company is finding out the performance of the company and also that the dealings of the

company are in line with the objectives of its formation. The auditors are required to express a

true and fair view on the financial statements and express an opinion based on such an audit.

Such an opinion is then read by members and shareholders of the company to evaluate whether

they must continue their investments in the company or not (Porter et al., 2014). Hence,

expression of opinion by the auditor is quite significant since all major decisions of members are

based on such an opinion. There are four types of opinion which an auditor can express, such as:

Unqualified Opinion;

Adverse Opinion

Qualified Opinion; and

Disclaimer of Opinion (Leung, 2009)

auditor of the company. The auditors have given a declaration of independence in the auditor’s

report attached with annual report of the company. This statement by the auditor’s states that

they have complied with the provisions of Corporation Act 2001 and also they have followed the

ethical code of conduct as has been mentioned in APES 110. They have also stated that there

have been no contraventions in both the requirements. As stated in the code of ethics, auditors

have been careful to apply them throughout the audit. The requirement to give a statement of

declaration is given under the Corporations Act, 2001. The declaration is given on page number

36 of the annual report (TPG Telecom Limited, 2017).

2) Independent auditor’s report

The main reason behind appointing an external auditor to audit the financial statements of a

company is finding out the performance of the company and also that the dealings of the

company are in line with the objectives of its formation. The auditors are required to express a

true and fair view on the financial statements and express an opinion based on such an audit.

Such an opinion is then read by members and shareholders of the company to evaluate whether

they must continue their investments in the company or not (Porter et al., 2014). Hence,

expression of opinion by the auditor is quite significant since all major decisions of members are

based on such an opinion. There are four types of opinion which an auditor can express, such as:

Unqualified Opinion;

Adverse Opinion

Qualified Opinion; and

Disclaimer of Opinion (Leung, 2009)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of the audit of financial statements, KPMG opined that the financial report of TPG

Telecom Limited is as per the provisions of the Corporations Act, 2001 and the financial

statements reflect a true and fair view of various dealings of the company. In addition to this, the

auditors have also opined that other compliance requirements such as Australian accounting

standards and Corporations Regulations, 2001 have also been followed. In other words, KPMG

has given an unqualified audit opinion on the financial statements of TPG Telecom Limited

(TPG Telecom Limited, 2017). The opinion so expressed is given on page number 92 of the

annual report.

3) Non-Audit services performed by the Auditor

Services which are accepted and performed by an auditor in addition to his acceptance of audit

and assurance services in the same company are called as non-audit services. However, there are

possibilities that the independence of an auditor might get affected because of such services. The

auditor might gain personal interests while performing non audit services which might create

some sort of biasness in his mind. Quality of audit might get negatively affected because of this.

Thus, non audit services have become significant to be assessed while evaluating independence

of an auditor (Frankel, 2018).

However, not all the countries across the world allow the auditors of the company to take up

these two tasks simultaneously. In other words, in such countries an auditor will not be able to

take up both audit work as well as non audit work. United States of America is an example of

this. Sarbanes and Oxley Act that has been framed by the authorities in the US, has prohibited

the auditors of the company to perform non audit services in the same company in which they

are giving assurance and audit services (Mitchell, 2018). In Australia, however, there is no such

provision that restricts the auditors, which means the auditors are permitted to perform as many

Telecom Limited is as per the provisions of the Corporations Act, 2001 and the financial

statements reflect a true and fair view of various dealings of the company. In addition to this, the

auditors have also opined that other compliance requirements such as Australian accounting

standards and Corporations Regulations, 2001 have also been followed. In other words, KPMG

has given an unqualified audit opinion on the financial statements of TPG Telecom Limited

(TPG Telecom Limited, 2017). The opinion so expressed is given on page number 92 of the

annual report.

3) Non-Audit services performed by the Auditor

Services which are accepted and performed by an auditor in addition to his acceptance of audit

and assurance services in the same company are called as non-audit services. However, there are

possibilities that the independence of an auditor might get affected because of such services. The

auditor might gain personal interests while performing non audit services which might create

some sort of biasness in his mind. Quality of audit might get negatively affected because of this.

Thus, non audit services have become significant to be assessed while evaluating independence

of an auditor (Frankel, 2018).

However, not all the countries across the world allow the auditors of the company to take up

these two tasks simultaneously. In other words, in such countries an auditor will not be able to

take up both audit work as well as non audit work. United States of America is an example of

this. Sarbanes and Oxley Act that has been framed by the authorities in the US, has prohibited

the auditors of the company to perform non audit services in the same company in which they

are giving assurance and audit services (Mitchell, 2018). In Australia, however, there is no such

provision that restricts the auditors, which means the auditors are permitted to perform as many

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

types of services as they want, provided they do not affect his independence. Such declaration is

required to be given in writing in the annual report of the company along with auditor’s report

(Clarke et al., 2016). Wherever an auditor feels that there might be a conflict of interest, he must

not accept such non audit services. This means onus to prove independence lies with auditor

(ASIC, 2018).

KPMG who are the auditors of TPG Telecom Limited have carried out some non-audit services

along with their audit and assurance services. However, the directors in their report have

specified that the audit and risk committee has personally been involved to evaluate that such

services have not in any manner affected independence of the auditor. Furthermore, the non audit

services have not in any way undermined principles set out in APES 110 has also been ensured.

The non audit services performed by KPMG in addition to audit services include performance of

certain taxation and other services. However, there is no mention of other services in detail in the

report (TPG Telecom Limited, 2017).

4) Auditors’ Remuneration

Remuneration to auditors is the fees paid to them for various audit as well as non audit services

performed by them (Caanz, 2015).

KPMG who were the lead auditors of TPG Telecom Limited have performed both services. In

the table below, the remuneration charged by them for 2017 and 2016 has been given along with

percentage increase or decrease.

(in $ '000)

Particulars 2017 2016 Percentage Change

Audit or review of the financial report 925 1,059 -13%

Other regulatory audit services 8 8 0%

required to be given in writing in the annual report of the company along with auditor’s report

(Clarke et al., 2016). Wherever an auditor feels that there might be a conflict of interest, he must

not accept such non audit services. This means onus to prove independence lies with auditor

(ASIC, 2018).

KPMG who are the auditors of TPG Telecom Limited have carried out some non-audit services

along with their audit and assurance services. However, the directors in their report have

specified that the audit and risk committee has personally been involved to evaluate that such

services have not in any manner affected independence of the auditor. Furthermore, the non audit

services have not in any way undermined principles set out in APES 110 has also been ensured.

The non audit services performed by KPMG in addition to audit services include performance of

certain taxation and other services. However, there is no mention of other services in detail in the

report (TPG Telecom Limited, 2017).

4) Auditors’ Remuneration

Remuneration to auditors is the fees paid to them for various audit as well as non audit services

performed by them (Caanz, 2015).

KPMG who were the lead auditors of TPG Telecom Limited have performed both services. In

the table below, the remuneration charged by them for 2017 and 2016 has been given along with

percentage increase or decrease.

(in $ '000)

Particulars 2017 2016 Percentage Change

Audit or review of the financial report 925 1,059 -13%

Other regulatory audit services 8 8 0%

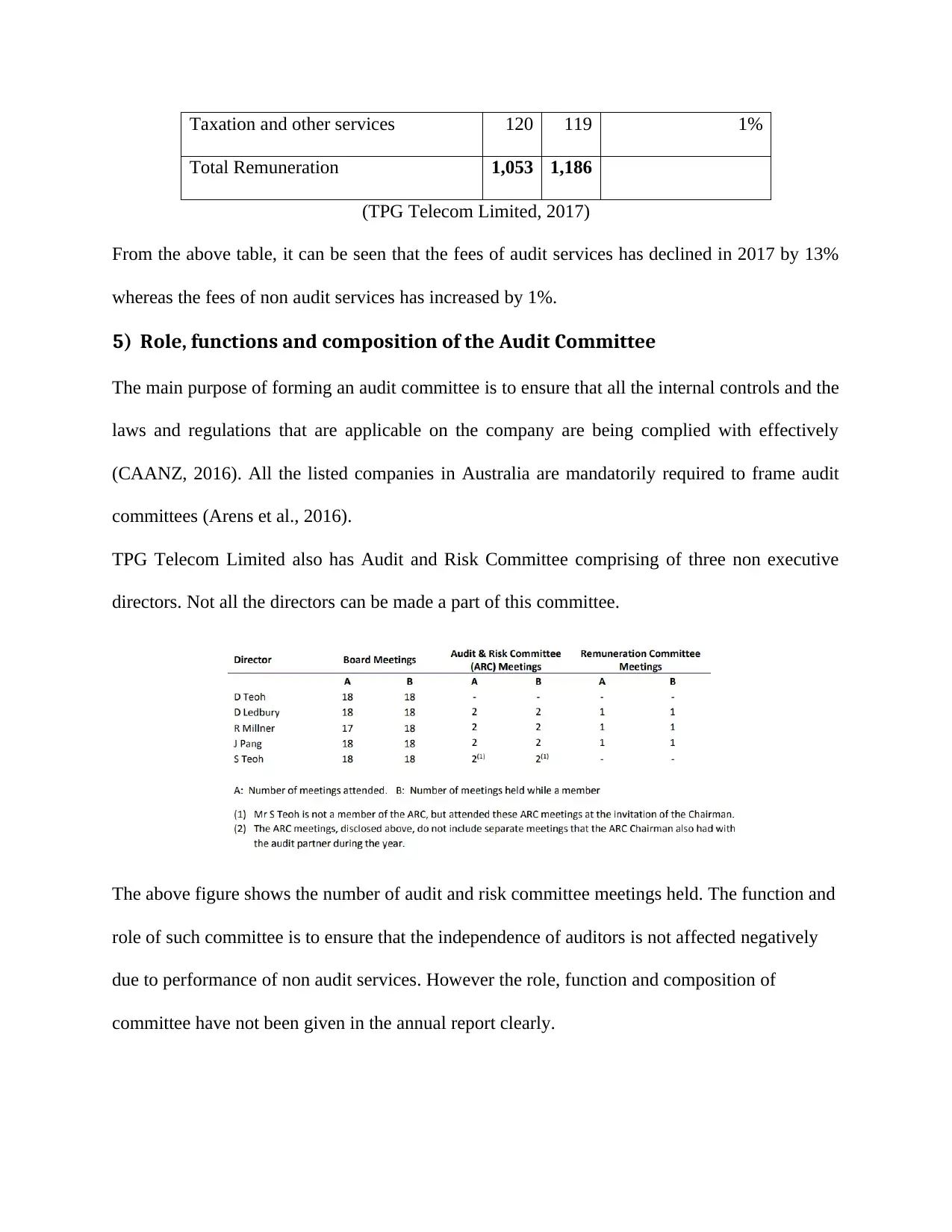

Taxation and other services 120 119 1%

Total Remuneration 1,053 1,186

(TPG Telecom Limited, 2017)

From the above table, it can be seen that the fees of audit services has declined in 2017 by 13%

whereas the fees of non audit services has increased by 1%.

5) Role, functions and composition of the Audit Committee

The main purpose of forming an audit committee is to ensure that all the internal controls and the

laws and regulations that are applicable on the company are being complied with effectively

(CAANZ, 2016). All the listed companies in Australia are mandatorily required to frame audit

committees (Arens et al., 2016).

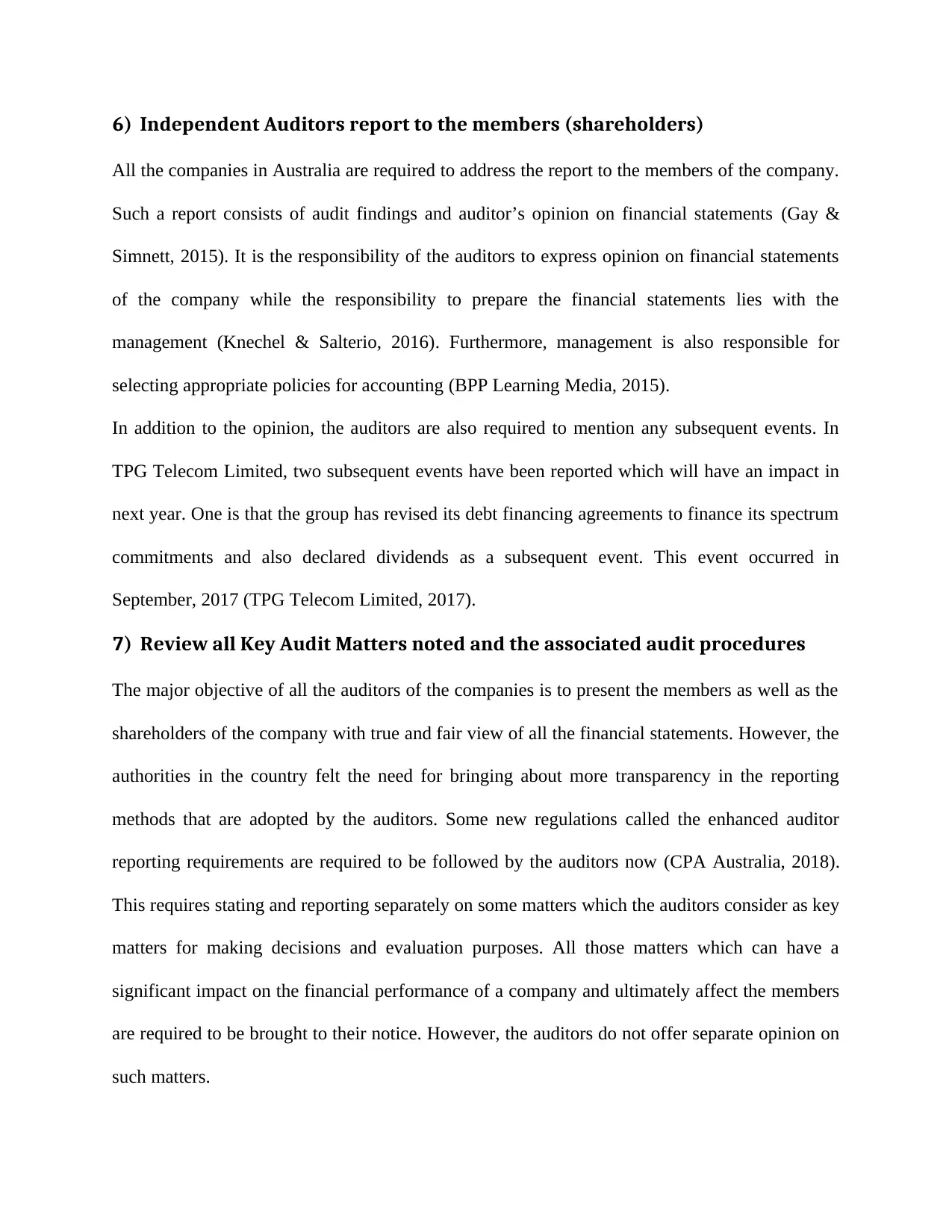

TPG Telecom Limited also has Audit and Risk Committee comprising of three non executive

directors. Not all the directors can be made a part of this committee.

The above figure shows the number of audit and risk committee meetings held. The function and

role of such committee is to ensure that the independence of auditors is not affected negatively

due to performance of non audit services. However the role, function and composition of

committee have not been given in the annual report clearly.

Total Remuneration 1,053 1,186

(TPG Telecom Limited, 2017)

From the above table, it can be seen that the fees of audit services has declined in 2017 by 13%

whereas the fees of non audit services has increased by 1%.

5) Role, functions and composition of the Audit Committee

The main purpose of forming an audit committee is to ensure that all the internal controls and the

laws and regulations that are applicable on the company are being complied with effectively

(CAANZ, 2016). All the listed companies in Australia are mandatorily required to frame audit

committees (Arens et al., 2016).

TPG Telecom Limited also has Audit and Risk Committee comprising of three non executive

directors. Not all the directors can be made a part of this committee.

The above figure shows the number of audit and risk committee meetings held. The function and

role of such committee is to ensure that the independence of auditors is not affected negatively

due to performance of non audit services. However the role, function and composition of

committee have not been given in the annual report clearly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6) Independent Auditors report to the members (shareholders)

All the companies in Australia are required to address the report to the members of the company.

Such a report consists of audit findings and auditor’s opinion on financial statements (Gay &

Simnett, 2015). It is the responsibility of the auditors to express opinion on financial statements

of the company while the responsibility to prepare the financial statements lies with the

management (Knechel & Salterio, 2016). Furthermore, management is also responsible for

selecting appropriate policies for accounting (BPP Learning Media, 2015).

In addition to the opinion, the auditors are also required to mention any subsequent events. In

TPG Telecom Limited, two subsequent events have been reported which will have an impact in

next year. One is that the group has revised its debt financing agreements to finance its spectrum

commitments and also declared dividends as a subsequent event. This event occurred in

September, 2017 (TPG Telecom Limited, 2017).

7) Review all Key Audit Matters noted and the associated audit procedures

The major objective of all the auditors of the companies is to present the members as well as the

shareholders of the company with true and fair view of all the financial statements. However, the

authorities in the country felt the need for bringing about more transparency in the reporting

methods that are adopted by the auditors. Some new regulations called the enhanced auditor

reporting requirements are required to be followed by the auditors now (CPA Australia, 2018).

This requires stating and reporting separately on some matters which the auditors consider as key

matters for making decisions and evaluation purposes. All those matters which can have a

significant impact on the financial performance of a company and ultimately affect the members

are required to be brought to their notice. However, the auditors do not offer separate opinion on

such matters.

All the companies in Australia are required to address the report to the members of the company.

Such a report consists of audit findings and auditor’s opinion on financial statements (Gay &

Simnett, 2015). It is the responsibility of the auditors to express opinion on financial statements

of the company while the responsibility to prepare the financial statements lies with the

management (Knechel & Salterio, 2016). Furthermore, management is also responsible for

selecting appropriate policies for accounting (BPP Learning Media, 2015).

In addition to the opinion, the auditors are also required to mention any subsequent events. In

TPG Telecom Limited, two subsequent events have been reported which will have an impact in

next year. One is that the group has revised its debt financing agreements to finance its spectrum

commitments and also declared dividends as a subsequent event. This event occurred in

September, 2017 (TPG Telecom Limited, 2017).

7) Review all Key Audit Matters noted and the associated audit procedures

The major objective of all the auditors of the companies is to present the members as well as the

shareholders of the company with true and fair view of all the financial statements. However, the

authorities in the country felt the need for bringing about more transparency in the reporting

methods that are adopted by the auditors. Some new regulations called the enhanced auditor

reporting requirements are required to be followed by the auditors now (CPA Australia, 2018).

This requires stating and reporting separately on some matters which the auditors consider as key

matters for making decisions and evaluation purposes. All those matters which can have a

significant impact on the financial performance of a company and ultimately affect the members

are required to be brought to their notice. However, the auditors do not offer separate opinion on

such matters.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

KPMG, the audit firm of the company, in their audit report to members have stated two key audit

areas, which include the following: Revenue Recognition Carrying Value of Goodwill

The auditors further have stated that it is as per their professional judgment that the above two

mentioned matters have been addressed by them as key audit matters. Detailed explanation is as

follows:

Revenue Recognition- The major revenue of the company comes from telecommunication

services provided by them to the customers. Their customers include individuals, wholesale

customers as well as corporate customers. The revenue from provision of telecommunication

services is considered to be key audit matter because of the large scale operations. Various

telecommunication services are offered to the customers that operate on various networks. Such

services are billed using systems which are highly automated and they also use various sub

systems in order to recognize revenue. All these factors required the auditors to appoint their

own IT team for the task and this enhanced the complexity of the audit. Furthermore, due to

pressure from competitors, the rates charged from customers are not consistent and thus, these

frequent price changes increases the number of audit data points.

KPMG applied Test of Controls to test the control procedures adopted by the management of

the company to bill revenue streams. The auditors also performed substantive test of details

and analytical procedures which included confirmation of revenue from major corporations

and also performing sample tests to check accuracy of bills generated.

Carrying value of Goodwill- The auditors have considered this as a key audit matter because of

the size of its asset and is the largest asset of the company. The matter required the auditors to

areas, which include the following: Revenue Recognition Carrying Value of Goodwill

The auditors further have stated that it is as per their professional judgment that the above two

mentioned matters have been addressed by them as key audit matters. Detailed explanation is as

follows:

Revenue Recognition- The major revenue of the company comes from telecommunication

services provided by them to the customers. Their customers include individuals, wholesale

customers as well as corporate customers. The revenue from provision of telecommunication

services is considered to be key audit matter because of the large scale operations. Various

telecommunication services are offered to the customers that operate on various networks. Such

services are billed using systems which are highly automated and they also use various sub

systems in order to recognize revenue. All these factors required the auditors to appoint their

own IT team for the task and this enhanced the complexity of the audit. Furthermore, due to

pressure from competitors, the rates charged from customers are not consistent and thus, these

frequent price changes increases the number of audit data points.

KPMG applied Test of Controls to test the control procedures adopted by the management of

the company to bill revenue streams. The auditors also performed substantive test of details

and analytical procedures which included confirmation of revenue from major corporations

and also performing sample tests to check accuracy of bills generated.

Carrying value of Goodwill- The auditors have considered this as a key audit matter because of

the size of its asset and is the largest asset of the company. The matter required the auditors to

use a significant level of judgment to evaluate the estimates of carrying value of goodwill.

Furthermore, the industry in which the company is operating in has a huge impact of change in

technology. The forecasts are always at risk because of the constantly changing prices. The

auditors focused upon assessing the carrying amount of company’s goodwill by evaluating the

valuation models for specific cash generating unit. Discount rates and key assumptions taken by

the company in relation to forecasts were assessed by the auditors while evaluating the market

demand of the services. Several of the senior audit team members were involved in the process.

In order to test the key audit matter related to carrying value of goodwill, KPMG adopted

analytical procedures to compare demand forecasts against industry reports and evaluate the

data in various valuation models. The auditors also focused on evaluating methods of forecasting

accuracy. These are called as substantive test of details (Knowledge Equity, 2018). The

auditors also performed substantive tests as a part of substantive tests of details. This information

is specified on page number 94 of the annual report.

Conclusion

The objective or reviewing the audit report of TPG Telecom Limited was to ensure that the

auditors have keenly followed the provisions regarding audit or not. However, after reviewing it

appears that the auditors have complied with all the major laws and regulations. However,

information related to composition of audit and risk committee has not been provided in the

annual report. Hence, it is advised that the relevant information is given in such a manner that it

does not get lost amidst irrelevant information. However, a follow up question to the auditors is

about the type of non audit services performed by them. What exactly is meant by taxation and

‘other services’?

Furthermore, the industry in which the company is operating in has a huge impact of change in

technology. The forecasts are always at risk because of the constantly changing prices. The

auditors focused upon assessing the carrying amount of company’s goodwill by evaluating the

valuation models for specific cash generating unit. Discount rates and key assumptions taken by

the company in relation to forecasts were assessed by the auditors while evaluating the market

demand of the services. Several of the senior audit team members were involved in the process.

In order to test the key audit matter related to carrying value of goodwill, KPMG adopted

analytical procedures to compare demand forecasts against industry reports and evaluate the

data in various valuation models. The auditors also focused on evaluating methods of forecasting

accuracy. These are called as substantive test of details (Knowledge Equity, 2018). The

auditors also performed substantive tests as a part of substantive tests of details. This information

is specified on page number 94 of the annual report.

Conclusion

The objective or reviewing the audit report of TPG Telecom Limited was to ensure that the

auditors have keenly followed the provisions regarding audit or not. However, after reviewing it

appears that the auditors have complied with all the major laws and regulations. However,

information related to composition of audit and risk committee has not been provided in the

annual report. Hence, it is advised that the relevant information is given in such a manner that it

does not get lost amidst irrelevant information. However, a follow up question to the auditors is

about the type of non audit services performed by them. What exactly is meant by taxation and

‘other services’?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.