Contemporary Accounting Theory Report: TPG Telecom Sustainability

VerifiedAdded on 2022/10/13

|17

|3881

|15

Report

AI Summary

This report delves into contemporary accounting theory, focusing on the significance of corporate social responsibility (CSR) for firms with financial objectives. It distinguishes sustainability reporting from CSR, presenting a holistic view of corporate responsibility. The report identifies and explains the stakeholder theory and legitimacy theory, which provide insights into the essence of sustainability reporting. Applying this theoretical knowledge, the report examines the sustainability reporting practices of TPG Telecom Limited, an Australian telecommunications company. It provides an overview of TPG Telecom's governance, ownership, and financial performance. A sustainability reporting scoring index, based on GRI guidelines, is developed to evaluate the quality and extent of the company's sustainability disclosures. The analysis assesses TPG Telecom's environmental performance, social initiatives, and governance practices, drawing conclusions on the effectiveness of its sustainability reporting efforts and its alignment with theoretical frameworks.

Running head: CONTEMPORARY ACCOUNTING THEORY

Contemporary accounting theory

Name of the Student

Name of the University

Author Note

Contemporary accounting theory

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Executive summary:

The paper is developed to explore the theoretical knowledge about the importance of

sustainability reporting to the firms by reviewing the literature. The holistic view of the

corporate sustainability reporting is provided by explaining the sustainability reporting versus

corporate social responsibility. In addition to this, paper also demonstrates the theories that

helps in explaining the sustainability reporting essence. The application of theoretical

knowledge of the importance of sustainability reporting is done by explaining the reporting

practices of the one of the leading telecommunication service provider that is TPG Telecom

limited. The sustainability scoring index in accordance with the principles of GRI has been

depicted for evaluating the quality of sustainability disclosures of TPG Telecom limited with

the help of information retrieved from the sustainability report or the financial report

published by the company.

Executive summary:

The paper is developed to explore the theoretical knowledge about the importance of

sustainability reporting to the firms by reviewing the literature. The holistic view of the

corporate sustainability reporting is provided by explaining the sustainability reporting versus

corporate social responsibility. In addition to this, paper also demonstrates the theories that

helps in explaining the sustainability reporting essence. The application of theoretical

knowledge of the importance of sustainability reporting is done by explaining the reporting

practices of the one of the leading telecommunication service provider that is TPG Telecom

limited. The sustainability scoring index in accordance with the principles of GRI has been

depicted for evaluating the quality of sustainability disclosures of TPG Telecom limited with

the help of information retrieved from the sustainability report or the financial report

published by the company.

CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................3

i. Evaluating the importance of corporate social responsibility for the firms having

financial objectives:...................................................................................................................3

ii. Evaluating the sustainability reporting in contrast with the corporate social

responsibility:.............................................................................................................................3

iii. Identifying the theories explaining the essence of sustainability reporting:...................3

Part B:.........................................................................................................................................3

iv. Presenting the overview of the governance, ownership and financial performance of

TPG telecom:.............................................................................................................................3

v. Preparing the sustainability reporting scoring index:.........................................................3

vi. Explaining the quality and extent of sustainability reporting of the company against

the sustainability reporting scoring index:.................................................................................3

Conclusion:................................................................................................................................3

Table of Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................3

i. Evaluating the importance of corporate social responsibility for the firms having

financial objectives:...................................................................................................................3

ii. Evaluating the sustainability reporting in contrast with the corporate social

responsibility:.............................................................................................................................3

iii. Identifying the theories explaining the essence of sustainability reporting:...................3

Part B:.........................................................................................................................................3

iv. Presenting the overview of the governance, ownership and financial performance of

TPG telecom:.............................................................................................................................3

v. Preparing the sustainability reporting scoring index:.........................................................3

vi. Explaining the quality and extent of sustainability reporting of the company against

the sustainability reporting scoring index:.................................................................................3

Conclusion:................................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

Introduction:

The report is divided into two sections, with one section depicting the importance of

corporate social responsibility and sustainability reporting and the link between them, while

other section depicting the application of such knowledge to explain the quality and essence

of sustainability reporting practices by the organization. The essence of sustainability

reporting and how the efforts of organization is shaped for addressing sustainable matters is

done by identification of two relevant theories. The sustainability disclosure of the chosen

company that is TPG Telecom is explained by evaluating the facts and the information

disclosed in the sustainability report by referring to the scoring index.

Part A:

i. Evaluating the importance of corporate social responsibility for the firms having

financial objectives:

Corporate social responsibility is becoming one of the most prominent business

practices in this era. For every individual company, the major objective is to produce output

and creates a positive effect on the society. The major objective of corporate social

responsibility is to make sure that the all the companies practicing CSR in their organization

should carry out their business in an ethical manner. This also takes into account the social,

economic and the environmental impact thereby taking the human rights also into

consideration. Every company aims to obtain a positive result on the society as a whole also

there should be a maximum creation of the shared value for the owners of the enterprise

which includes its employees, shareholders and stakeholders (Hawn & Ioannou, 2016).

Introduction:

The report is divided into two sections, with one section depicting the importance of

corporate social responsibility and sustainability reporting and the link between them, while

other section depicting the application of such knowledge to explain the quality and essence

of sustainability reporting practices by the organization. The essence of sustainability

reporting and how the efforts of organization is shaped for addressing sustainable matters is

done by identification of two relevant theories. The sustainability disclosure of the chosen

company that is TPG Telecom is explained by evaluating the facts and the information

disclosed in the sustainability report by referring to the scoring index.

Part A:

i. Evaluating the importance of corporate social responsibility for the firms having

financial objectives:

Corporate social responsibility is becoming one of the most prominent business

practices in this era. For every individual company, the major objective is to produce output

and creates a positive effect on the society. The major objective of corporate social

responsibility is to make sure that the all the companies practicing CSR in their organization

should carry out their business in an ethical manner. This also takes into account the social,

economic and the environmental impact thereby taking the human rights also into

consideration. Every company aims to obtain a positive result on the society as a whole also

there should be a maximum creation of the shared value for the owners of the enterprise

which includes its employees, shareholders and stakeholders (Hawn & Ioannou, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

The companies are nowadays increasingly taking their focus into social responsibility

which might include several social and economic practices into the organization like

championing women’s rights, protecting the environment, or the effort to reduce or eliminate

poverty globally. For any operating firm, the implementation of corporate social

responsibility is becoming an indispensable part of their organization as from the optical

perspective, socially responsible companies’ project more and more attractive. In simpler

words it can be said that corporate social responsibility is to how a company manage their

business processes so as to obtain the overall positive impact. It is often believed by the

company’s executives that CSR can improve profits of the organization. It is also significant

for the CSR to promote the respect for their company in the marketplace which would

eventually result in higher productivity thereby higher sales. It also results in enhancing the

staff loyalty and eventually attracts more and more personnel to the organization. Corporate

social responsibility is sometimes also termed as the corporate citizenship (Mirvis et al.,

2016).

CSR has a strategy which they need to implement into the organization so as to obtain

the maximum profitability from it and thereby matching the changing needs of today’s top

talent that is innovation. CSR has to allocate the resources and do the research and

development for integrating the socially responsible methods and the materials in production.

ii. Evaluating the sustainability reporting in contrast with the corporate social

responsibility:

Talking about the corporate responsibility and sustainability, it can be said that the

companies incorporate the social, environmental as well as economic creation. It helps to

improve the management of the risks associated with business and the arising opportunities

which will eventually result in enhancing the long term social and environmental

The companies are nowadays increasingly taking their focus into social responsibility

which might include several social and economic practices into the organization like

championing women’s rights, protecting the environment, or the effort to reduce or eliminate

poverty globally. For any operating firm, the implementation of corporate social

responsibility is becoming an indispensable part of their organization as from the optical

perspective, socially responsible companies’ project more and more attractive. In simpler

words it can be said that corporate social responsibility is to how a company manage their

business processes so as to obtain the overall positive impact. It is often believed by the

company’s executives that CSR can improve profits of the organization. It is also significant

for the CSR to promote the respect for their company in the marketplace which would

eventually result in higher productivity thereby higher sales. It also results in enhancing the

staff loyalty and eventually attracts more and more personnel to the organization. Corporate

social responsibility is sometimes also termed as the corporate citizenship (Mirvis et al.,

2016).

CSR has a strategy which they need to implement into the organization so as to obtain

the maximum profitability from it and thereby matching the changing needs of today’s top

talent that is innovation. CSR has to allocate the resources and do the research and

development for integrating the socially responsible methods and the materials in production.

ii. Evaluating the sustainability reporting in contrast with the corporate social

responsibility:

Talking about the corporate responsibility and sustainability, it can be said that the

companies incorporate the social, environmental as well as economic creation. It helps to

improve the management of the risks associated with business and the arising opportunities

which will eventually result in enhancing the long term social and environmental

CONTEMPORARY ACCOUNTING THEORY

sustainability. It can often said that sustainability is a comprehensive approach to manage the

organization thereby focusing on making and maximizing the economic, social and

environmental value on a very long term basis. When the word sustainability comes into play,

it is a much broader term since the organization is facing growing accountability needs which

varies in a wide range of stakeholders are needed to disclose the environmental and social

customs and tradition of the businesses (Epstein, 2018).

Additionally a rising number of it has assured to divide the corporate social

responsibilities into strategies and operations, thereby making and developing robust

measurements and reporting frameworks so as to obtain both the strategic implementation of

CSR and measurement and consequently reporting frameworks in order to implement CSR

and respond to the stakeholders’ accountability requirements. But designing the sustainability

performance measurement systems within the organization for supporting the strategic

changes and the alterations which the CSR needs to make in the specific issues the company

has to face which is not appropriately reflected in the generic sustainability reporting

frameworks. For understanding the relationship in between the SPM and SR there needs to

make a number of exploratory cases. Thereby it can be said that the corporate social

responsibility enables the companies to create the different values including the social,

environmental and economic values into the core strategy and operations. It will ultimately

assist in bringing in more and more opportunities whilst enhancing long term social and

environmental sustainability. CSR is a self-regulating business practice that helps any

company in being socially accountable. That means ranging from the company itself, to its

stakeholders and finally the public (Bradford et al., 2016).

sustainability. It can often said that sustainability is a comprehensive approach to manage the

organization thereby focusing on making and maximizing the economic, social and

environmental value on a very long term basis. When the word sustainability comes into play,

it is a much broader term since the organization is facing growing accountability needs which

varies in a wide range of stakeholders are needed to disclose the environmental and social

customs and tradition of the businesses (Epstein, 2018).

Additionally a rising number of it has assured to divide the corporate social

responsibilities into strategies and operations, thereby making and developing robust

measurements and reporting frameworks so as to obtain both the strategic implementation of

CSR and measurement and consequently reporting frameworks in order to implement CSR

and respond to the stakeholders’ accountability requirements. But designing the sustainability

performance measurement systems within the organization for supporting the strategic

changes and the alterations which the CSR needs to make in the specific issues the company

has to face which is not appropriately reflected in the generic sustainability reporting

frameworks. For understanding the relationship in between the SPM and SR there needs to

make a number of exploratory cases. Thereby it can be said that the corporate social

responsibility enables the companies to create the different values including the social,

environmental and economic values into the core strategy and operations. It will ultimately

assist in bringing in more and more opportunities whilst enhancing long term social and

environmental sustainability. CSR is a self-regulating business practice that helps any

company in being socially accountable. That means ranging from the company itself, to its

stakeholders and finally the public (Bradford et al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

iii. Identifying the theories explaining the essence of sustainability reporting:

The essence of sustainability reporting can be explained with the help of stakeholder

theory and legitimacy theory and they provide different perspective in explaining the

phenomena of sustainability reporting. Legitimacy theory explains and helps in

understanding the factors leading to variation in the disclosure concerning sustainability. It

also determines how the actions of organization is influenced by the variable of interest in

seeking legitimacy. Moreover, it has been argued by some authors that legitimacy of an

organization can be explained in the best way using corporate disclosure. The theory posits

that the implicit contract between the society and business entity forms the basis of business

legitimacy to carry out its business in society. Therefore, as per the legitimacy theory, in the

event of change in any expectation of entities or the norms of society, business entities take

effort to legitimize their operation, they adopt social and environmental responsibility

reporting (Crane et al., 2019).

The stakeholder theory opines that there are two reasons why an organization engages

itself in the disclosure and reporting of CSR. An increase in the financial return is witnessed

because of creation of fruitful relation with the stakeholders that arises due to their social and

environmental disclosures. This also creates the view that the expectation and norms of the

stakeholders are being met which forms the legitimacy instruments. It is suggested by the

theory that the stakeholders are convinced about the operations of business and that the

organization are meeting their expectation, the disclosure of CSR is an important mode of

communication (Mishra & Modi, 2016). In order for the behavior of organization to be

perceived as legitimate, disclosure of appropriate environmental information is made by the

organization.

iii. Identifying the theories explaining the essence of sustainability reporting:

The essence of sustainability reporting can be explained with the help of stakeholder

theory and legitimacy theory and they provide different perspective in explaining the

phenomena of sustainability reporting. Legitimacy theory explains and helps in

understanding the factors leading to variation in the disclosure concerning sustainability. It

also determines how the actions of organization is influenced by the variable of interest in

seeking legitimacy. Moreover, it has been argued by some authors that legitimacy of an

organization can be explained in the best way using corporate disclosure. The theory posits

that the implicit contract between the society and business entity forms the basis of business

legitimacy to carry out its business in society. Therefore, as per the legitimacy theory, in the

event of change in any expectation of entities or the norms of society, business entities take

effort to legitimize their operation, they adopt social and environmental responsibility

reporting (Crane et al., 2019).

The stakeholder theory opines that there are two reasons why an organization engages

itself in the disclosure and reporting of CSR. An increase in the financial return is witnessed

because of creation of fruitful relation with the stakeholders that arises due to their social and

environmental disclosures. This also creates the view that the expectation and norms of the

stakeholders are being met which forms the legitimacy instruments. It is suggested by the

theory that the stakeholders are convinced about the operations of business and that the

organization are meeting their expectation, the disclosure of CSR is an important mode of

communication (Mishra & Modi, 2016). In order for the behavior of organization to be

perceived as legitimate, disclosure of appropriate environmental information is made by the

organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Part B:

iv. Presenting the overview of the governance, ownership and financial performance

of TPG telecom:

TPG telecom limited is the information technology and telecommunication company

operating in Australia with specialization in the business internet, consumer services and

service of mobile phone. They are engaged in providing diversified range of communication

services to small and medium enterprises, residential users, wholesale customers and large

corporate enterprises. In the previous years of operation, TPG acquired AAPT, PIPE network

and acquisition of intra power and become forth mobile operator of Singapore in year 2016.

In the previous financial year that is 2018, strong cash flow was delivered by the group and

an increase in the revenue of corporate segment along with the reduction in total expenses. In

addition to this, there was a fall in profit before tax by 1% and a decrease in the earning per

share (Cooper, 2017). The fall in revenue is attributable to decline in fixed voice usage due to

declining industrial trend. As against previous year, an increase in the cost of consumer

segment was witnessed along with proportional increase in revenue in year 2018. Over the

year 2018, the average debt balance was in line with the previous year. Total amount of

dividend paid to the shareholders reduced and such reduction was reflected in the fiscally

prudent decision of the board intended to retain greater proportion of profits. Furthermore,

the financial performance of the group is impacted by increased competition due to rollout of

NBN and thereby affecting the ability of company to make money from offerings of service

and growth of customer base.

The most appropriate arrangement of the corporate governance, which is consistent

with stakeholder responsibilities is determined by the board of directors of TPG Telecom

limited and such governance is in the best interest of shareholder and company. In addition to

Part B:

iv. Presenting the overview of the governance, ownership and financial performance

of TPG telecom:

TPG telecom limited is the information technology and telecommunication company

operating in Australia with specialization in the business internet, consumer services and

service of mobile phone. They are engaged in providing diversified range of communication

services to small and medium enterprises, residential users, wholesale customers and large

corporate enterprises. In the previous years of operation, TPG acquired AAPT, PIPE network

and acquisition of intra power and become forth mobile operator of Singapore in year 2016.

In the previous financial year that is 2018, strong cash flow was delivered by the group and

an increase in the revenue of corporate segment along with the reduction in total expenses. In

addition to this, there was a fall in profit before tax by 1% and a decrease in the earning per

share (Cooper, 2017). The fall in revenue is attributable to decline in fixed voice usage due to

declining industrial trend. As against previous year, an increase in the cost of consumer

segment was witnessed along with proportional increase in revenue in year 2018. Over the

year 2018, the average debt balance was in line with the previous year. Total amount of

dividend paid to the shareholders reduced and such reduction was reflected in the fiscally

prudent decision of the board intended to retain greater proportion of profits. Furthermore,

the financial performance of the group is impacted by increased competition due to rollout of

NBN and thereby affecting the ability of company to make money from offerings of service

and growth of customer base.

The most appropriate arrangement of the corporate governance, which is consistent

with stakeholder responsibilities is determined by the board of directors of TPG Telecom

limited and such governance is in the best interest of shareholder and company. In addition to

CONTEMPORARY ACCOUNTING THEORY

this, the governance practices of the company complies with the recommendation and

principles of the corporate governance of ASX. The disclosure of the governance

performance of the company is based on the eight principles of the recommendation council

of corporate governance. The board of director of TPG Telecom consists of chairman, two

independent director, two independent non-executive director that is there is a total of five

directors, of which four are is non-executive and independent director (Ali et al., 2017).

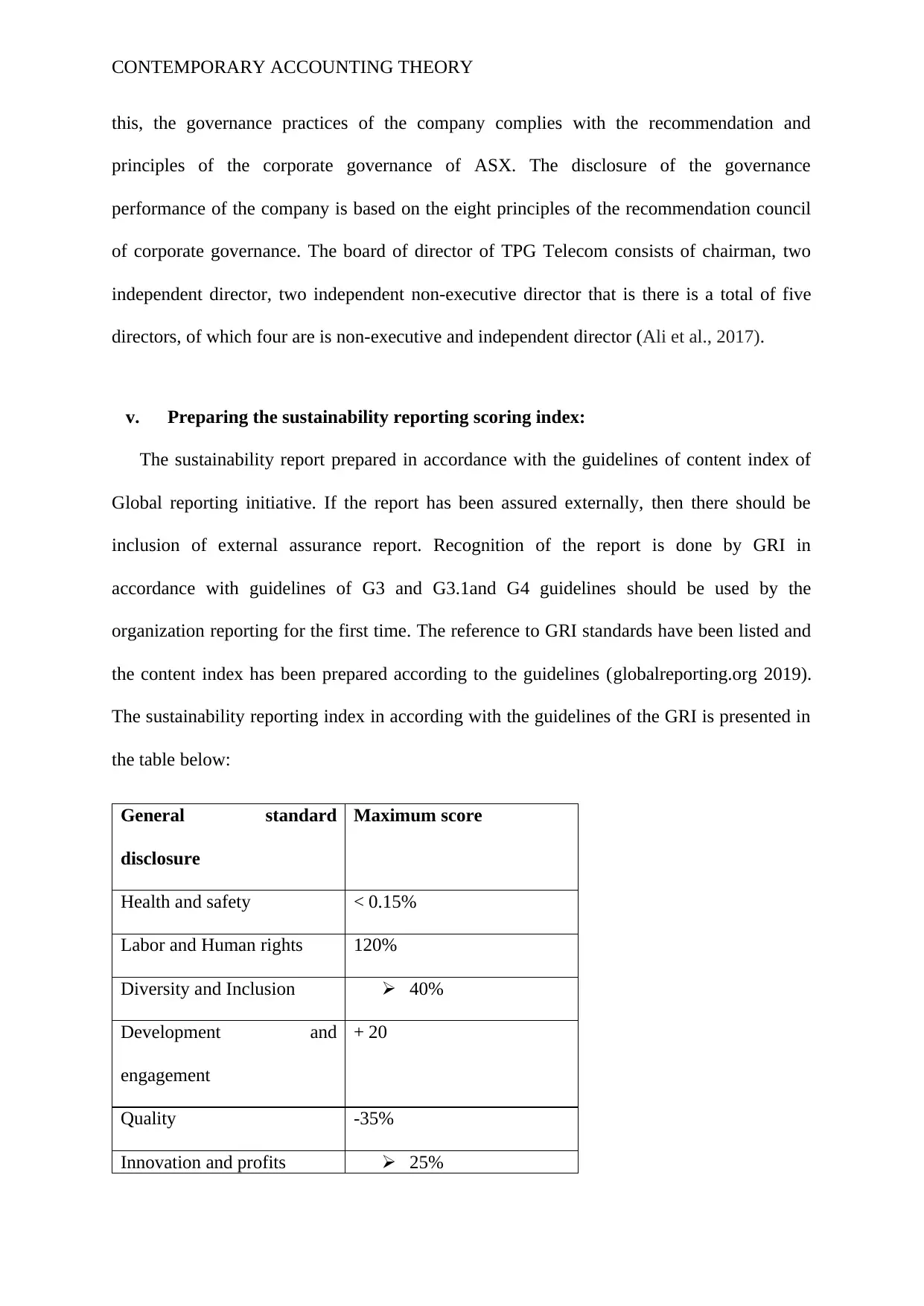

v. Preparing the sustainability reporting scoring index:

The sustainability report prepared in accordance with the guidelines of content index of

Global reporting initiative. If the report has been assured externally, then there should be

inclusion of external assurance report. Recognition of the report is done by GRI in

accordance with guidelines of G3 and G3.1and G4 guidelines should be used by the

organization reporting for the first time. The reference to GRI standards have been listed and

the content index has been prepared according to the guidelines (globalreporting.org 2019).

The sustainability reporting index in according with the guidelines of the GRI is presented in

the table below:

General standard

disclosure

Maximum score

Health and safety < 0.15%

Labor and Human rights 120%

Diversity and Inclusion 40%

Development and

engagement

+ 20

Quality -35%

Innovation and profits 25%

this, the governance practices of the company complies with the recommendation and

principles of the corporate governance of ASX. The disclosure of the governance

performance of the company is based on the eight principles of the recommendation council

of corporate governance. The board of director of TPG Telecom consists of chairman, two

independent director, two independent non-executive director that is there is a total of five

directors, of which four are is non-executive and independent director (Ali et al., 2017).

v. Preparing the sustainability reporting scoring index:

The sustainability report prepared in accordance with the guidelines of content index of

Global reporting initiative. If the report has been assured externally, then there should be

inclusion of external assurance report. Recognition of the report is done by GRI in

accordance with guidelines of G3 and G3.1and G4 guidelines should be used by the

organization reporting for the first time. The reference to GRI standards have been listed and

the content index has been prepared according to the guidelines (globalreporting.org 2019).

The sustainability reporting index in according with the guidelines of the GRI is presented in

the table below:

General standard

disclosure

Maximum score

Health and safety < 0.15%

Labor and Human rights 120%

Diversity and Inclusion 40%

Development and

engagement

+ 20

Quality -35%

Innovation and profits 25%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

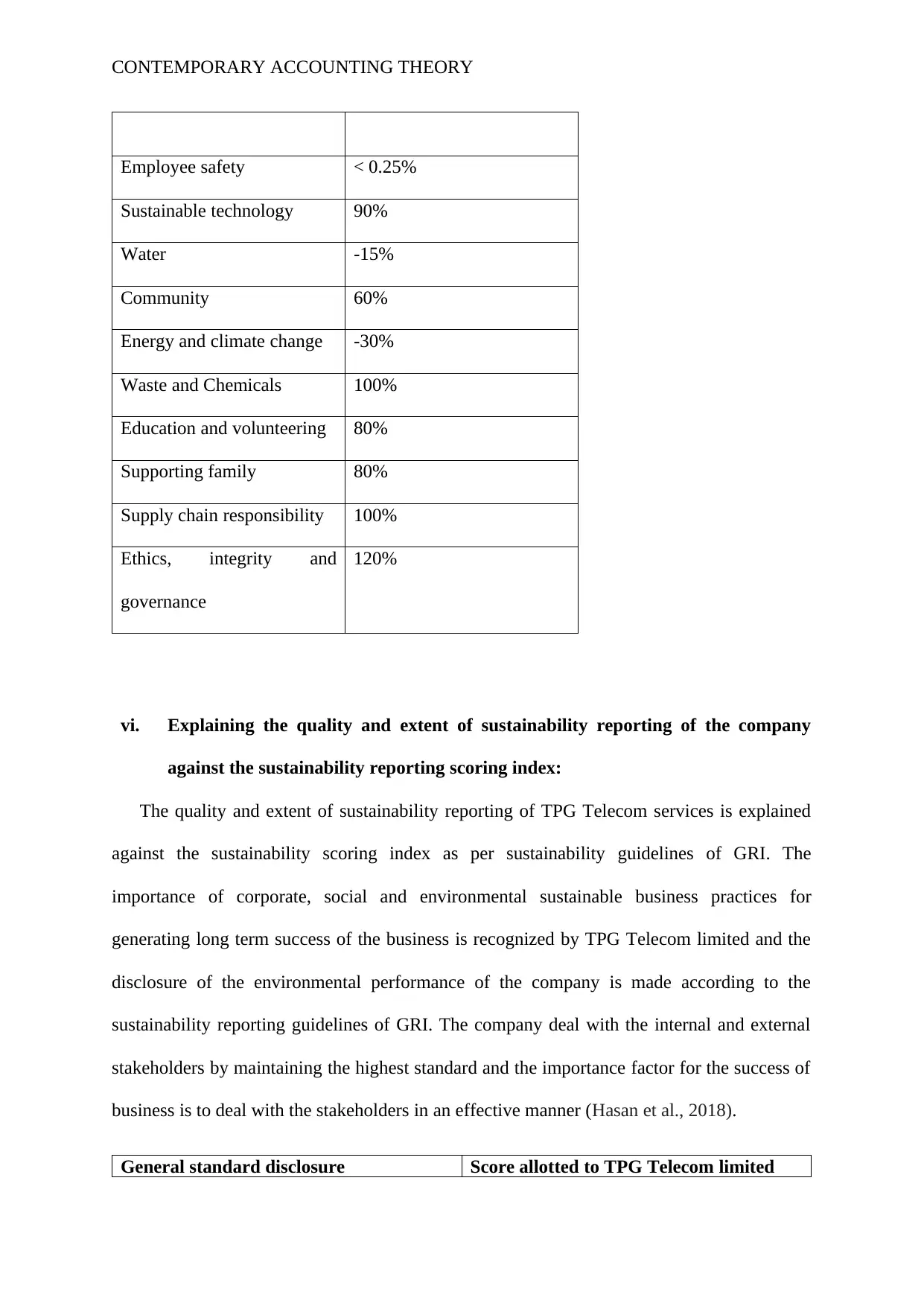

Employee safety < 0.25%

Sustainable technology 90%

Water -15%

Community 60%

Energy and climate change -30%

Waste and Chemicals 100%

Education and volunteering 80%

Supporting family 80%

Supply chain responsibility 100%

Ethics, integrity and

governance

120%

vi. Explaining the quality and extent of sustainability reporting of the company

against the sustainability reporting scoring index:

The quality and extent of sustainability reporting of TPG Telecom services is explained

against the sustainability scoring index as per sustainability guidelines of GRI. The

importance of corporate, social and environmental sustainable business practices for

generating long term success of the business is recognized by TPG Telecom limited and the

disclosure of the environmental performance of the company is made according to the

sustainability reporting guidelines of GRI. The company deal with the internal and external

stakeholders by maintaining the highest standard and the importance factor for the success of

business is to deal with the stakeholders in an effective manner (Hasan et al., 2018).

General standard disclosure Score allotted to TPG Telecom limited

Employee safety < 0.25%

Sustainable technology 90%

Water -15%

Community 60%

Energy and climate change -30%

Waste and Chemicals 100%

Education and volunteering 80%

Supporting family 80%

Supply chain responsibility 100%

Ethics, integrity and

governance

120%

vi. Explaining the quality and extent of sustainability reporting of the company

against the sustainability reporting scoring index:

The quality and extent of sustainability reporting of TPG Telecom services is explained

against the sustainability scoring index as per sustainability guidelines of GRI. The

importance of corporate, social and environmental sustainable business practices for

generating long term success of the business is recognized by TPG Telecom limited and the

disclosure of the environmental performance of the company is made according to the

sustainability reporting guidelines of GRI. The company deal with the internal and external

stakeholders by maintaining the highest standard and the importance factor for the success of

business is to deal with the stakeholders in an effective manner (Hasan et al., 2018).

General standard disclosure Score allotted to TPG Telecom limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

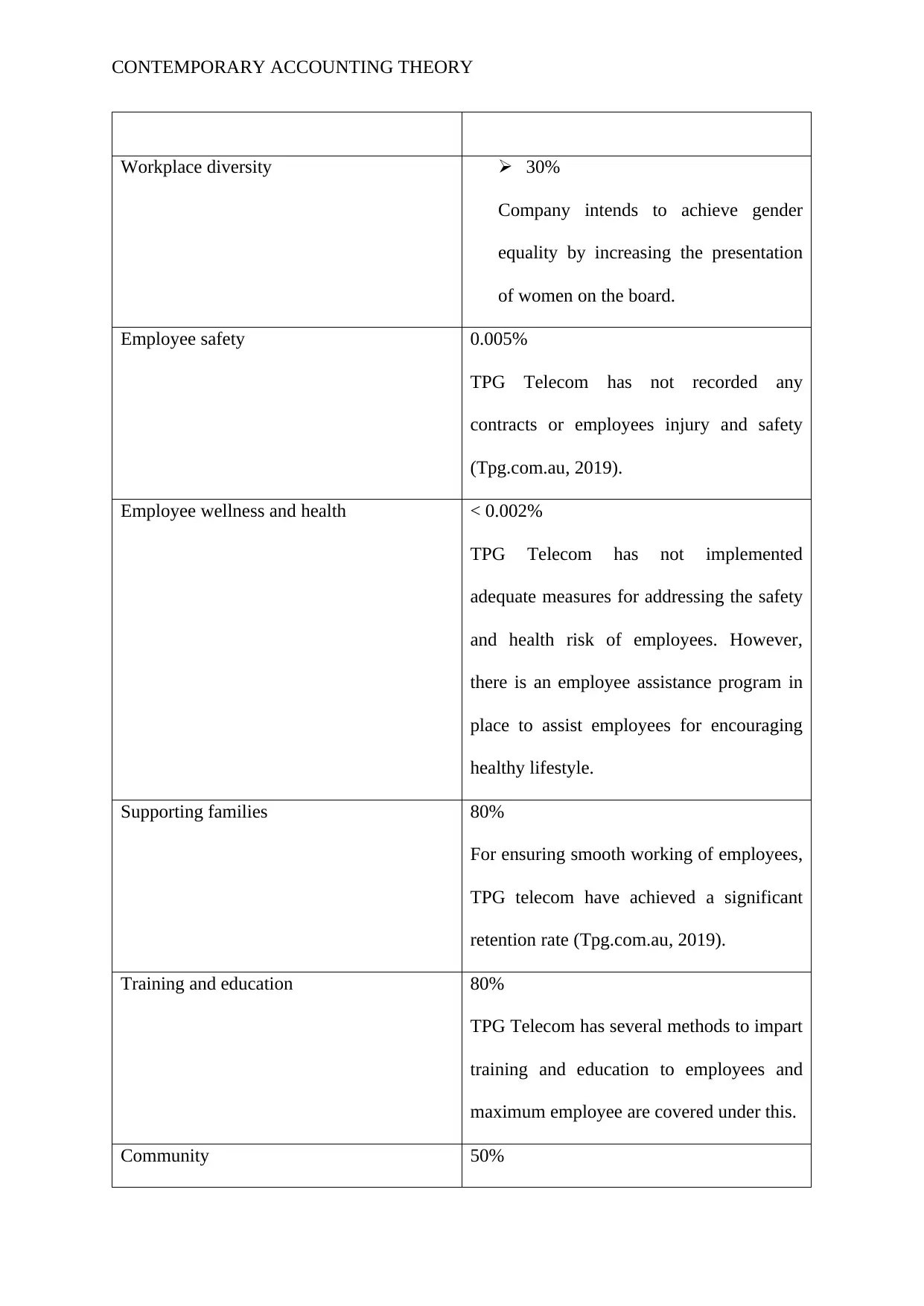

Workplace diversity 30%

Company intends to achieve gender

equality by increasing the presentation

of women on the board.

Employee safety 0.005%

TPG Telecom has not recorded any

contracts or employees injury and safety

(Tpg.com.au, 2019).

Employee wellness and health < 0.002%

TPG Telecom has not implemented

adequate measures for addressing the safety

and health risk of employees. However,

there is an employee assistance program in

place to assist employees for encouraging

healthy lifestyle.

Supporting families 80%

For ensuring smooth working of employees,

TPG telecom have achieved a significant

retention rate (Tpg.com.au, 2019).

Training and education 80%

TPG Telecom has several methods to impart

training and education to employees and

maximum employee are covered under this.

Community 50%

Workplace diversity 30%

Company intends to achieve gender

equality by increasing the presentation

of women on the board.

Employee safety 0.005%

TPG Telecom has not recorded any

contracts or employees injury and safety

(Tpg.com.au, 2019).

Employee wellness and health < 0.002%

TPG Telecom has not implemented

adequate measures for addressing the safety

and health risk of employees. However,

there is an employee assistance program in

place to assist employees for encouraging

healthy lifestyle.

Supporting families 80%

For ensuring smooth working of employees,

TPG telecom have achieved a significant

retention rate (Tpg.com.au, 2019).

Training and education 80%

TPG Telecom has several methods to impart

training and education to employees and

maximum employee are covered under this.

Community 50%

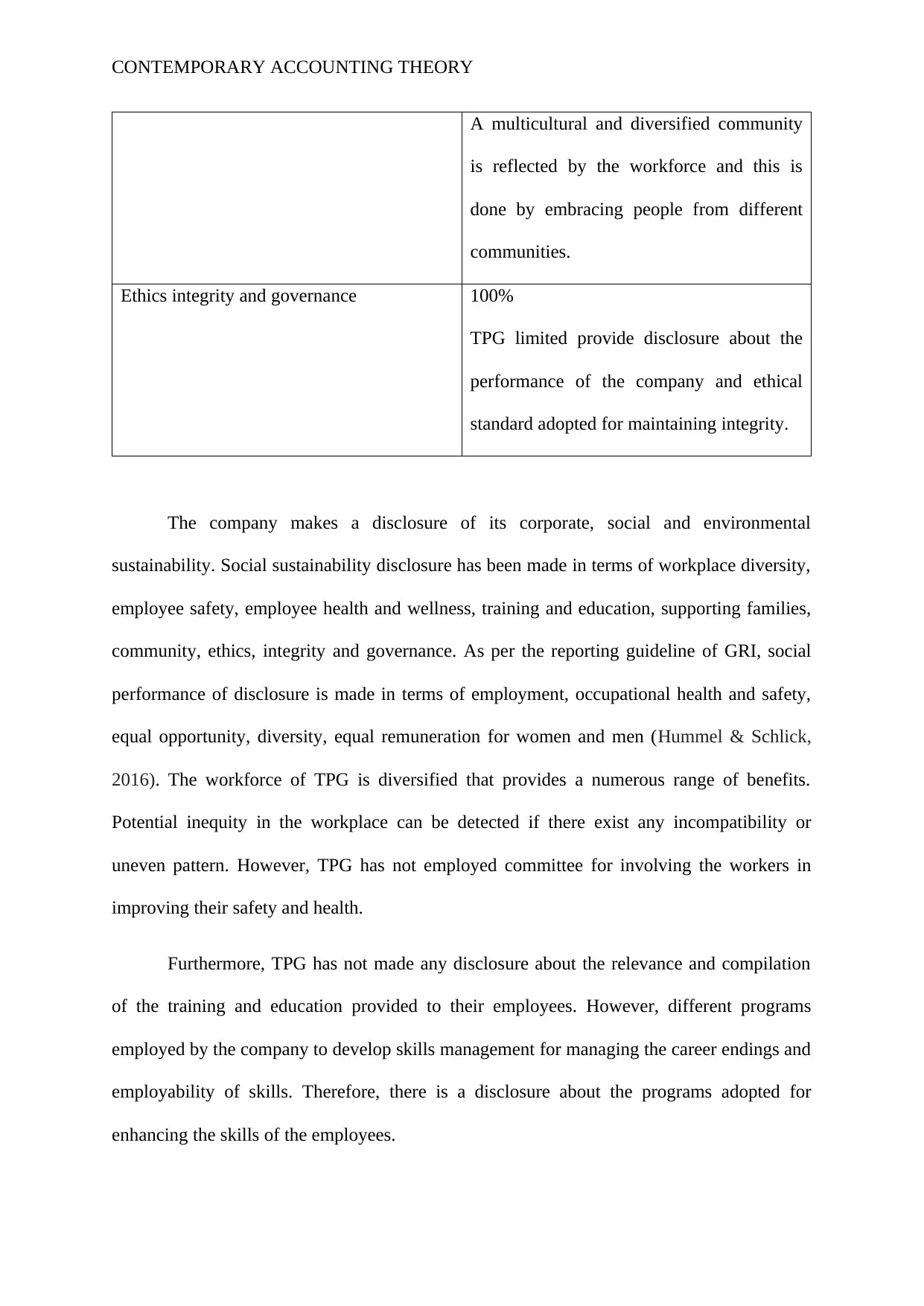

CONTEMPORARY ACCOUNTING THEORY

A multicultural and diversified community

is reflected by the workforce and this is

done by embracing people from different

communities.

Ethics integrity and governance 100%

TPG limited provide disclosure about the

performance of the company and ethical

standard adopted for maintaining integrity.

The company makes a disclosure of its corporate, social and environmental

sustainability. Social sustainability disclosure has been made in terms of workplace diversity,

employee safety, employee health and wellness, training and education, supporting families,

community, ethics, integrity and governance. As per the reporting guideline of GRI, social

performance of disclosure is made in terms of employment, occupational health and safety,

equal opportunity, diversity, equal remuneration for women and men (Hummel & Schlick,

2016). The workforce of TPG is diversified that provides a numerous range of benefits.

Potential inequity in the workplace can be detected if there exist any incompatibility or

uneven pattern. However, TPG has not employed committee for involving the workers in

improving their safety and health.

Furthermore, TPG has not made any disclosure about the relevance and compilation

of the training and education provided to their employees. However, different programs

employed by the company to develop skills management for managing the career endings and

employability of skills. Therefore, there is a disclosure about the programs adopted for

enhancing the skills of the employees.

A multicultural and diversified community

is reflected by the workforce and this is

done by embracing people from different

communities.

Ethics integrity and governance 100%

TPG limited provide disclosure about the

performance of the company and ethical

standard adopted for maintaining integrity.

The company makes a disclosure of its corporate, social and environmental

sustainability. Social sustainability disclosure has been made in terms of workplace diversity,

employee safety, employee health and wellness, training and education, supporting families,

community, ethics, integrity and governance. As per the reporting guideline of GRI, social

performance of disclosure is made in terms of employment, occupational health and safety,

equal opportunity, diversity, equal remuneration for women and men (Hummel & Schlick,

2016). The workforce of TPG is diversified that provides a numerous range of benefits.

Potential inequity in the workplace can be detected if there exist any incompatibility or

uneven pattern. However, TPG has not employed committee for involving the workers in

improving their safety and health.

Furthermore, TPG has not made any disclosure about the relevance and compilation

of the training and education provided to their employees. However, different programs

employed by the company to develop skills management for managing the career endings and

employability of skills. Therefore, there is a disclosure about the programs adopted for

enhancing the skills of the employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.