Analyzing Portfolio Performance Using Tracking Error Metrics

VerifiedAdded on 2020/04/07

|9

|1958

|49

AI Summary

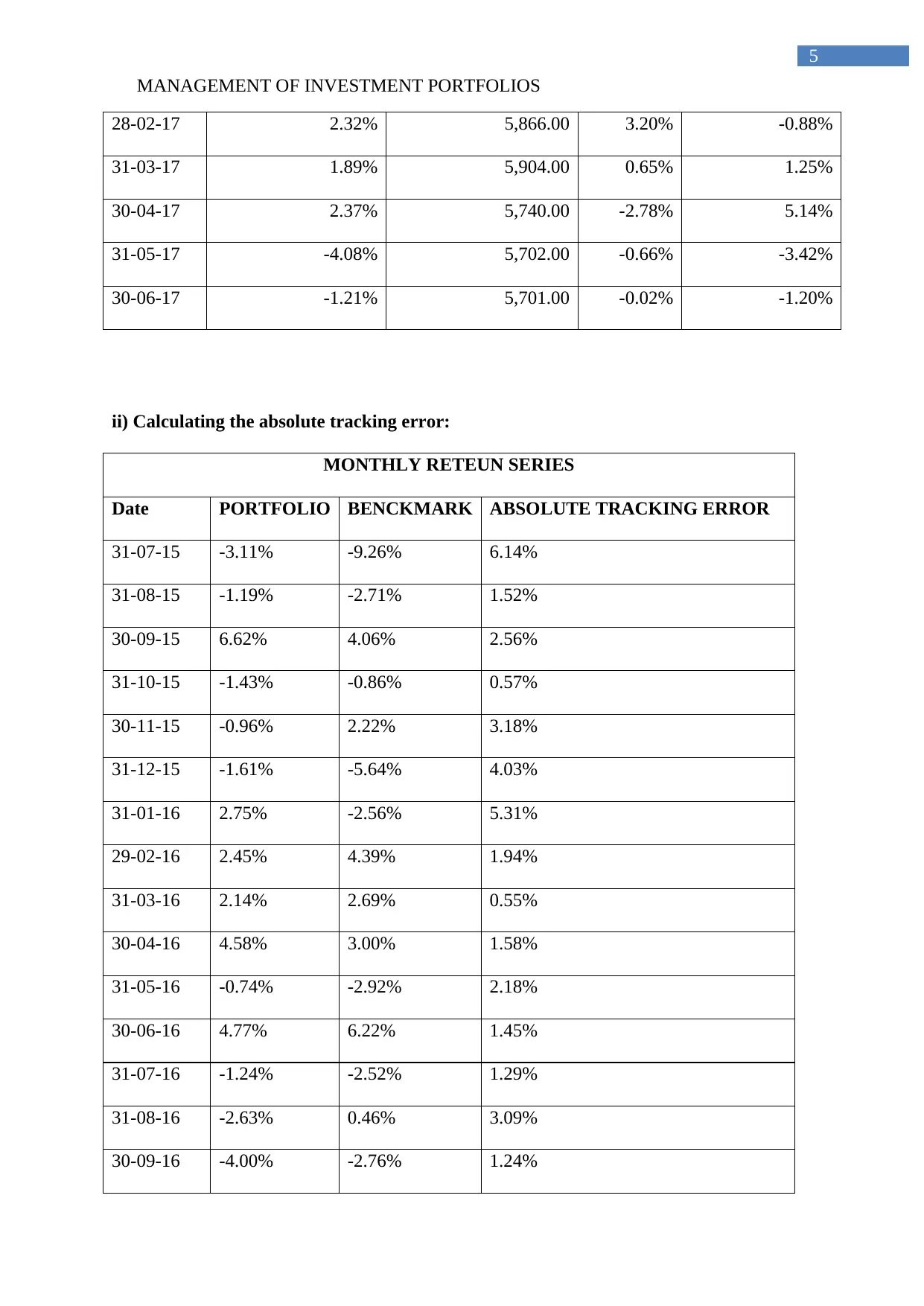

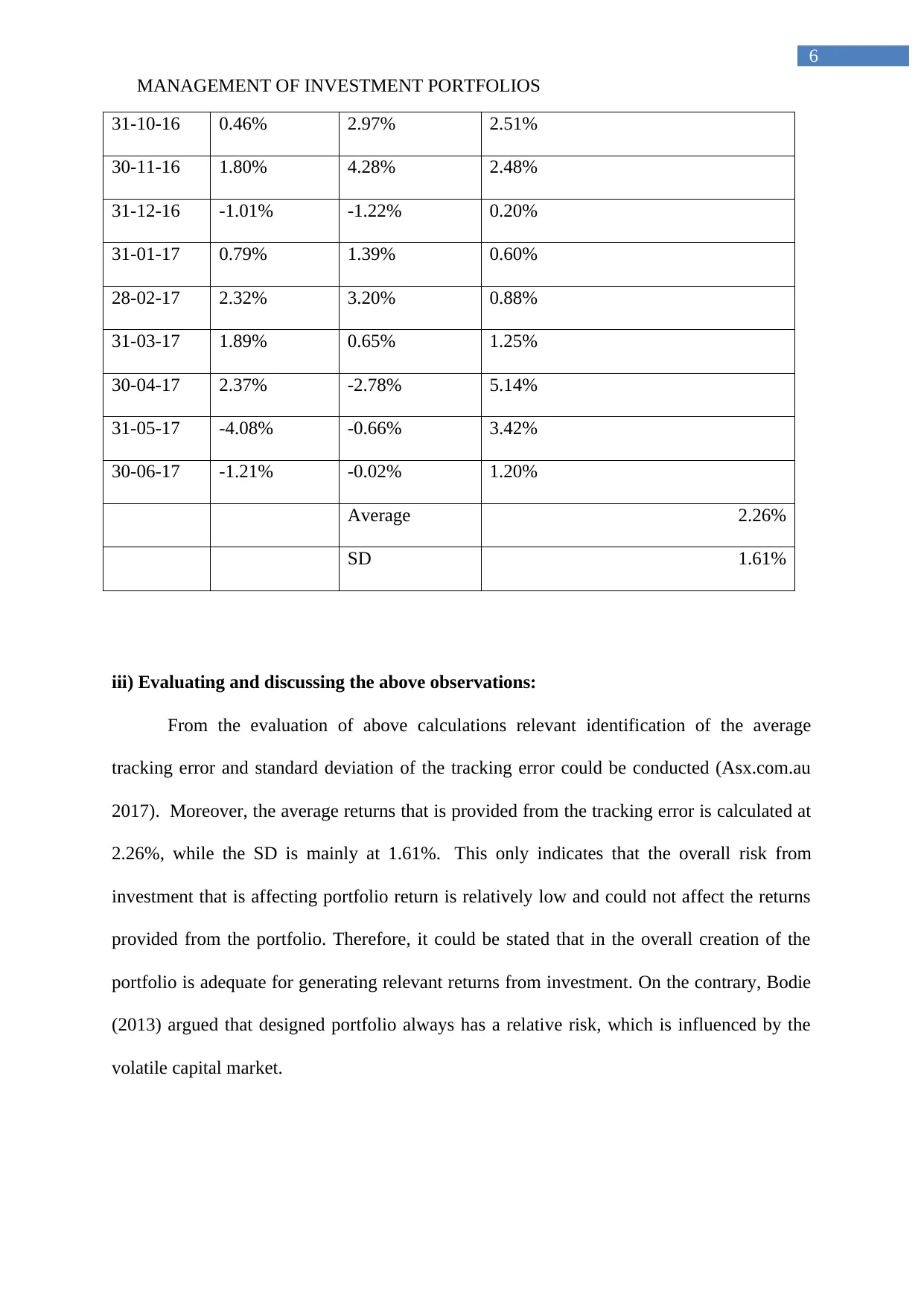

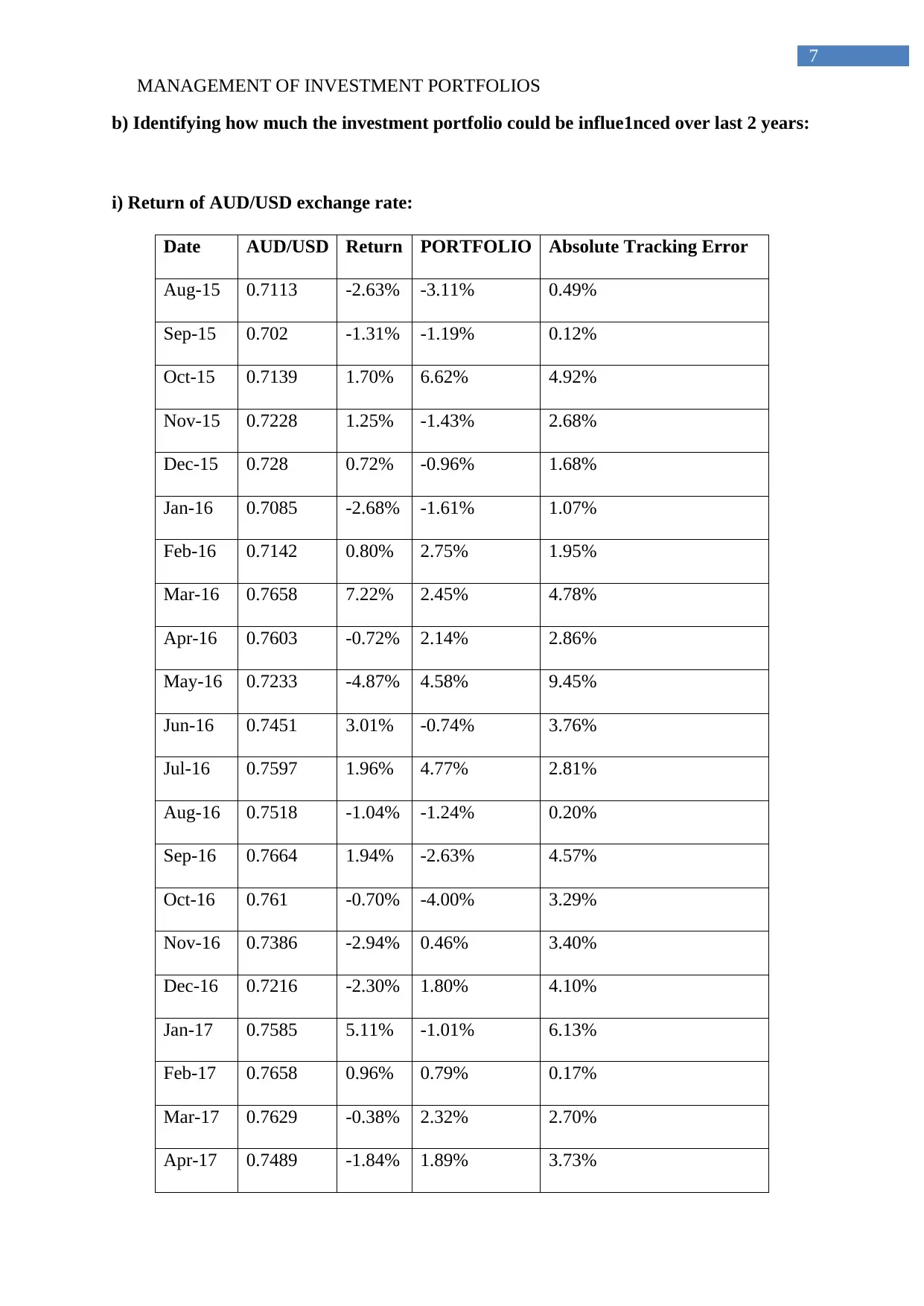

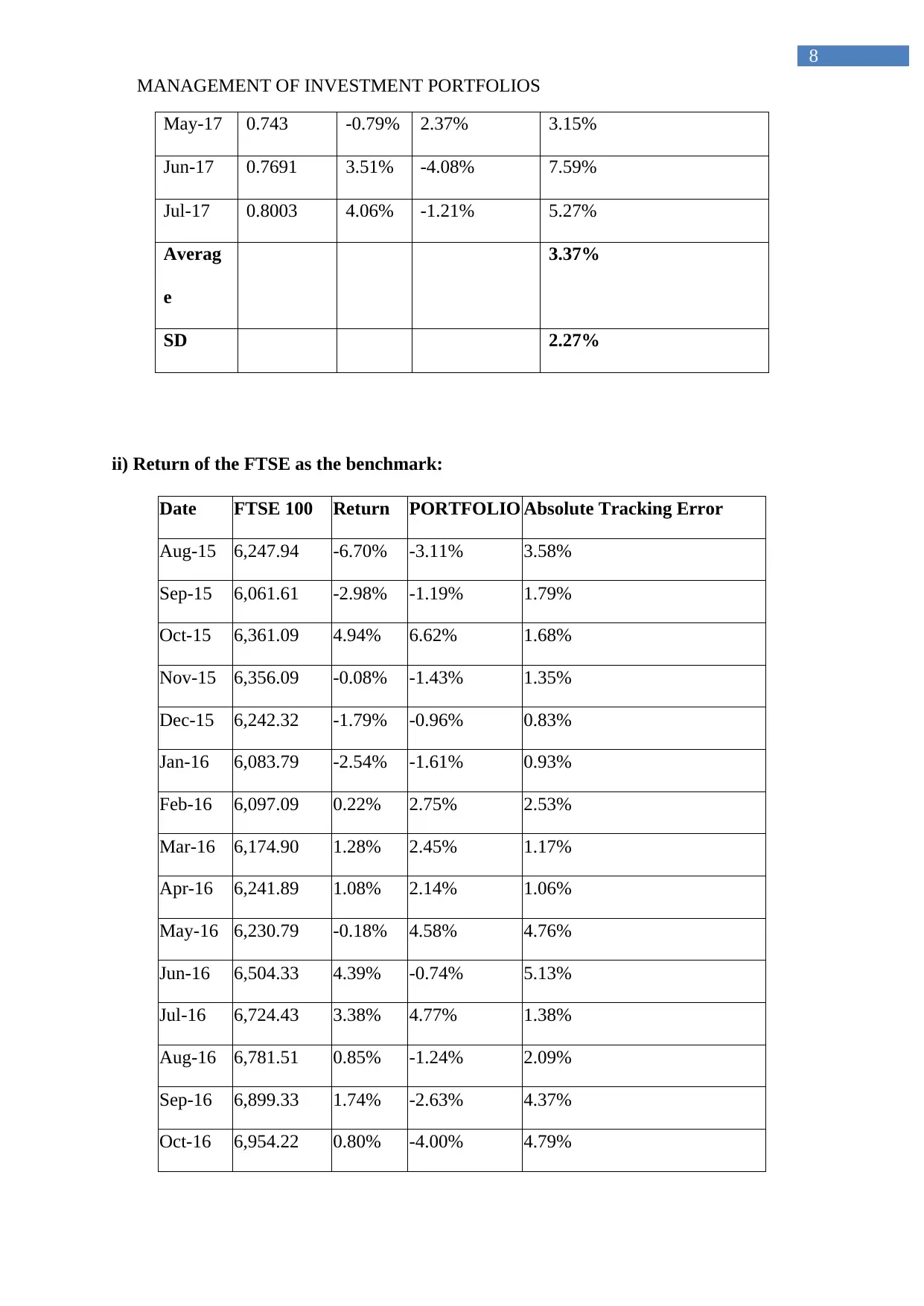

The task is to analyze the portfolio’s performance by comparing its monthly returns with those of a benchmark index and several currency pairs from January 2016 through July 2017. Key performance indicators such as annualized excess return, tracking error, information ratio, and Sharpe ratio will be calculated for both the portfolio and each currency pair. The analysis aims to identify how well the portfolio performed relative to the chosen benchmark and currencies, considering aspects like risk-adjusted returns and volatility. Additionally, the impact of currency fluctuations on investment performance is explored, with a specific focus on the AUD/USD exchange rate due to its significant influence during this period. This comprehensive review will provide insights into the effectiveness of the investment strategy employed and suggest potential areas for improvement.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.