Management Accounting Assignment: Traditional vs. ABC Costing Analysis

VerifiedAdded on 2020/01/07

|4

|606

|260

Homework Assignment

AI Summary

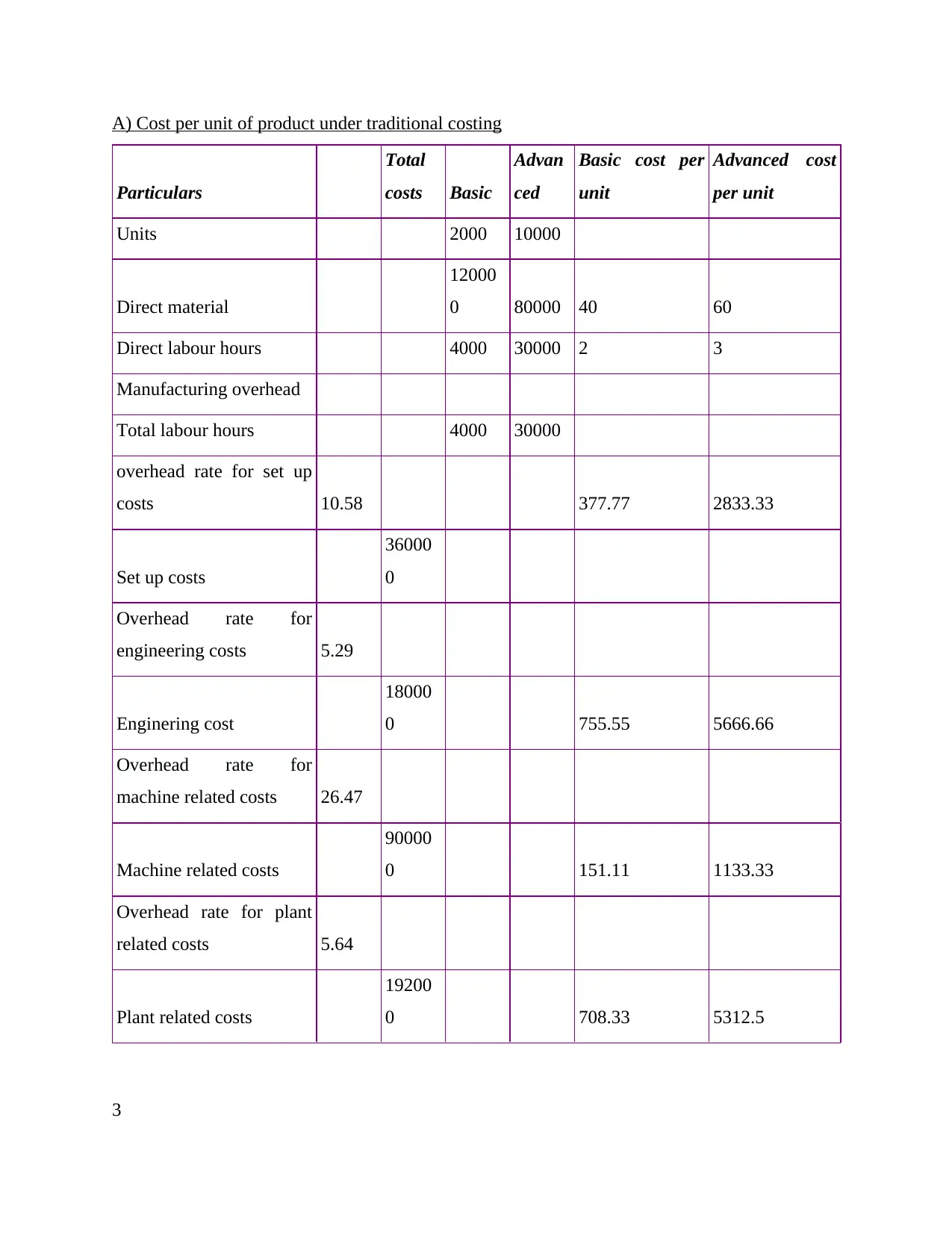

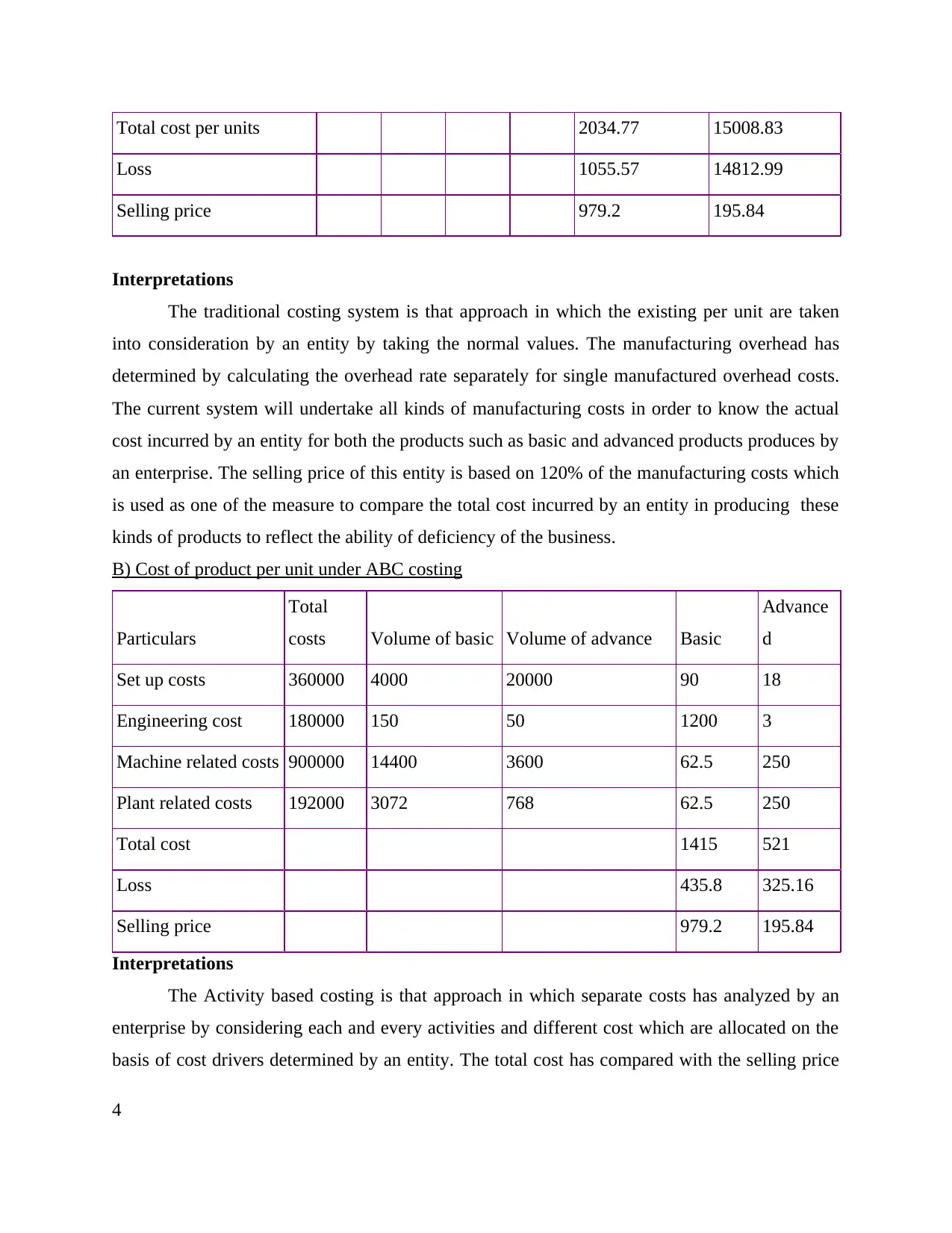

This assignment presents a comparative analysis of traditional and Activity-Based Costing (ABC) methods within the context of management accounting. The solution begins by calculating the cost per unit of product using traditional costing, detailing direct materials, direct labor, and various manufacturing overhead costs, such as set up, engineering, machine-related, and plant-related costs. The solution then interprets the results, explaining how the traditional costing system determines per-unit costs by considering normal values and separate overhead rates. The assignment then transitions to ABC costing, where costs are analyzed based on specific activities and cost drivers, again calculating the cost per unit for both basic and advanced products. The assignment includes calculations for set up costs, engineering costs, machine-related costs, and plant-related costs. The final step involves comparing the total costs with the selling price to determine the profit or loss incurred by the entity under both costing methods, thereby illustrating the differences and implications of each approach.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.