Scenario Easy: Traditional and Activity-Based Costing Analysis

VerifiedAdded on 2020/11/23

|11

|2793

|436

Report

AI Summary

This report provides a comprehensive analysis of costing methods, specifically comparing traditional and activity-based costing systems within the context of Scenario Easy Pvt Ltd, a manufacturing company with basic and advanced models. The report begins by calculating the cost per unit for both models using traditional costing, including manufacturing overhead and labor costs. It then applies activity-based costing (ABC) to determine unit costs, detailing overhead costs, activity rates, and activity usage. The report explores the reasons behind overseas buyers' preference for advanced models, considering cost efficiency and profit maximization. It also addresses the issue of fluctuating overheads, recommending ways to manage them. Furthermore, the report examines the merits and demerits of the ABC system, highlighting its accuracy, cost behavior insights, and ability to track costs, while also acknowledging its complexity and potential for implementation challenges. Finally, the report concludes with a summary of the findings and recommendations for the company.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Q1 Cost per unit of basic and advance models under current traditional costing system...........1

Q2 Cost per unit of basic and advance models under Activity based costing system................2

Q3 Explaining the major reason in context of overseas buyers for buying advanced model.....5

Q4 Explaining reasons on the basis of same overheads and recommending ways for dealing

with its fluctuations.....................................................................................................................6

Q5 Merits and demerits of activity based costing system...........................................................6

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Q1 Cost per unit of basic and advance models under current traditional costing system...........1

Q2 Cost per unit of basic and advance models under Activity based costing system................2

Q3 Explaining the major reason in context of overseas buyers for buying advanced model.....5

Q4 Explaining reasons on the basis of same overheads and recommending ways for dealing

with its fluctuations.....................................................................................................................6

Q5 Merits and demerits of activity based costing system...........................................................6

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting can be referred as process of preparing accounts and reports

which will be helping manager for finding financials which are accurate and even the

information which will be useful for short term decision making such as statistical information.

On the perspective of business unit, better planning has been ensured by management accounting

and proper control over the organization. This report is totally based on case scenario of Scenario

easy pvt ltd whose business model can be described as basic and advanced especially in

manufacturing context. The main objective of organization is to enhance the base of customer

and profit level should be maximised as each business units has a desire to explore there

operations at global level. This report is giving very deep insight about two methods i.e.

traditional based costing and activity based costing. The report will be elaborating there merits as

well as demerits.

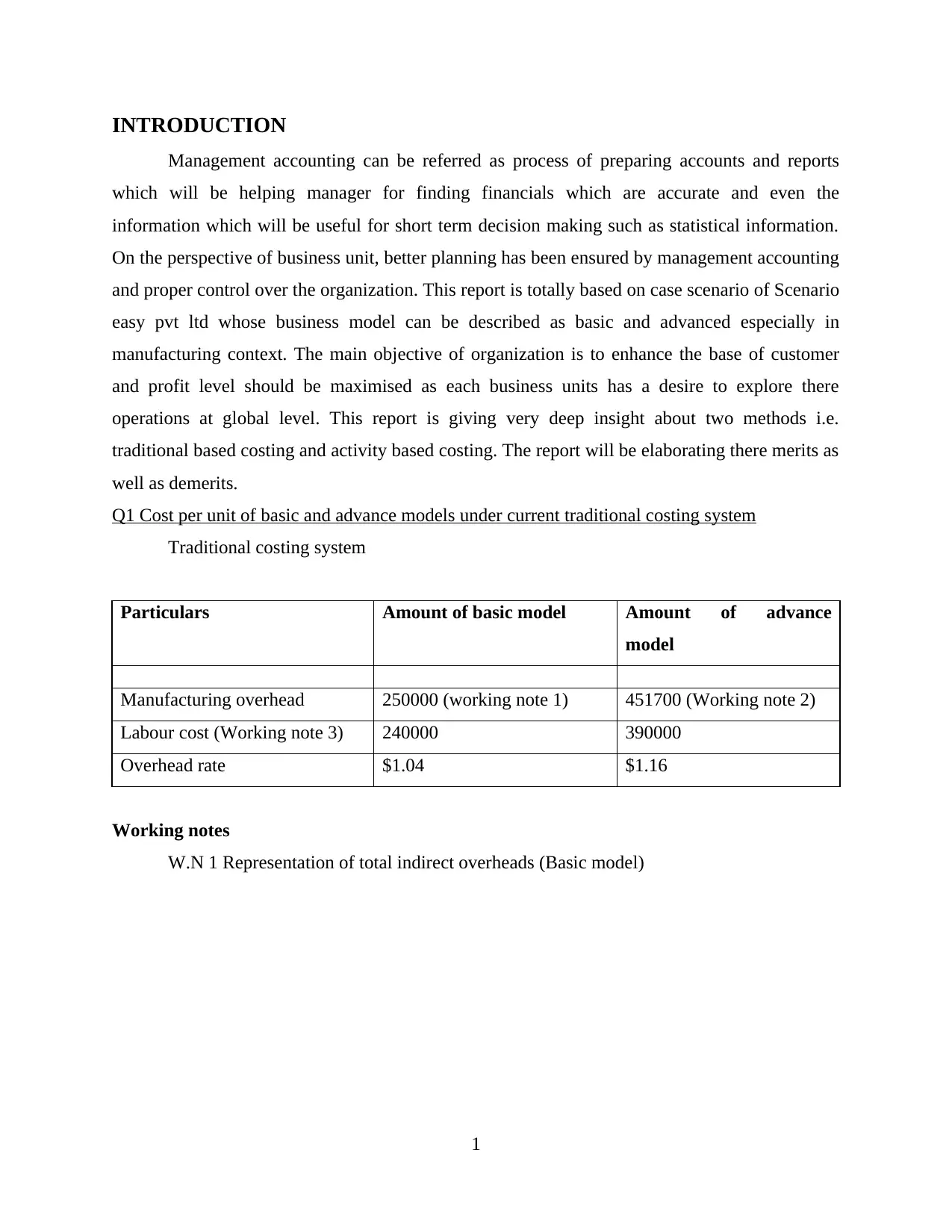

Q1 Cost per unit of basic and advance models under current traditional costing system

Traditional costing system

Particulars Amount of basic model Amount of advance

model

Manufacturing overhead 250000 (working note 1) 451700 (Working note 2)

Labour cost (Working note 3) 240000 390000

Overhead rate $1.04 $1.16

Working notes

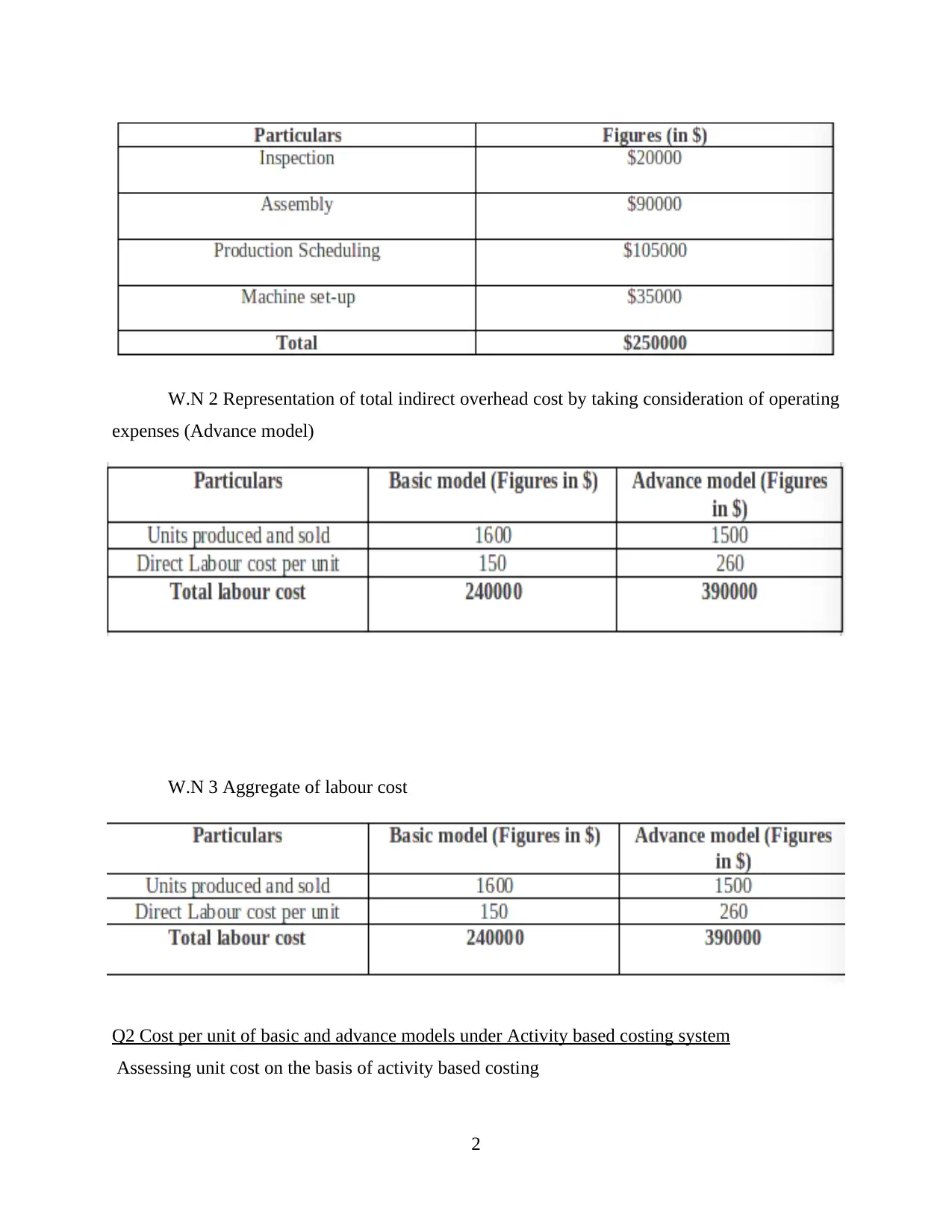

W.N 1 Representation of total indirect overheads (Basic model)

1

Management accounting can be referred as process of preparing accounts and reports

which will be helping manager for finding financials which are accurate and even the

information which will be useful for short term decision making such as statistical information.

On the perspective of business unit, better planning has been ensured by management accounting

and proper control over the organization. This report is totally based on case scenario of Scenario

easy pvt ltd whose business model can be described as basic and advanced especially in

manufacturing context. The main objective of organization is to enhance the base of customer

and profit level should be maximised as each business units has a desire to explore there

operations at global level. This report is giving very deep insight about two methods i.e.

traditional based costing and activity based costing. The report will be elaborating there merits as

well as demerits.

Q1 Cost per unit of basic and advance models under current traditional costing system

Traditional costing system

Particulars Amount of basic model Amount of advance

model

Manufacturing overhead 250000 (working note 1) 451700 (Working note 2)

Labour cost (Working note 3) 240000 390000

Overhead rate $1.04 $1.16

Working notes

W.N 1 Representation of total indirect overheads (Basic model)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

W.N 2 Representation of total indirect overhead cost by taking consideration of operating

expenses (Advance model)

W.N 3 Aggregate of labour cost

Q2 Cost per unit of basic and advance models under Activity based costing system

Assessing unit cost on the basis of activity based costing

2

expenses (Advance model)

W.N 3 Aggregate of labour cost

Q2 Cost per unit of basic and advance models under Activity based costing system

Assessing unit cost on the basis of activity based costing

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

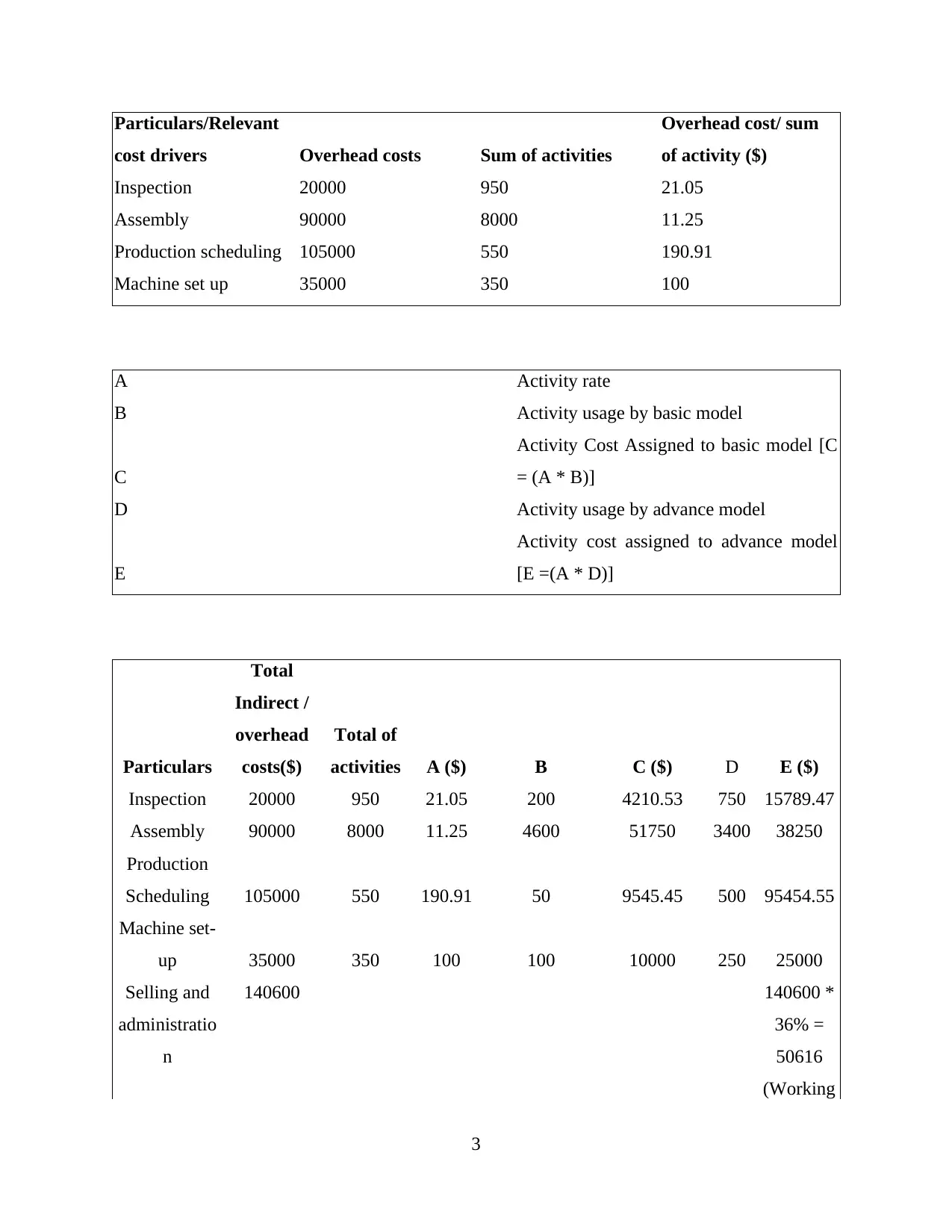

Particulars/Relevant

cost drivers Overhead costs Sum of activities

Overhead cost/ sum

of activity ($)

Inspection 20000 950 21.05

Assembly 90000 8000 11.25

Production scheduling 105000 550 190.91

Machine set up 35000 350 100

A Activity rate

B Activity usage by basic model

C

Activity Cost Assigned to basic model [C

= (A * B)]

D Activity usage by advance model

E

Activity cost assigned to advance model

[E =(A * D)]

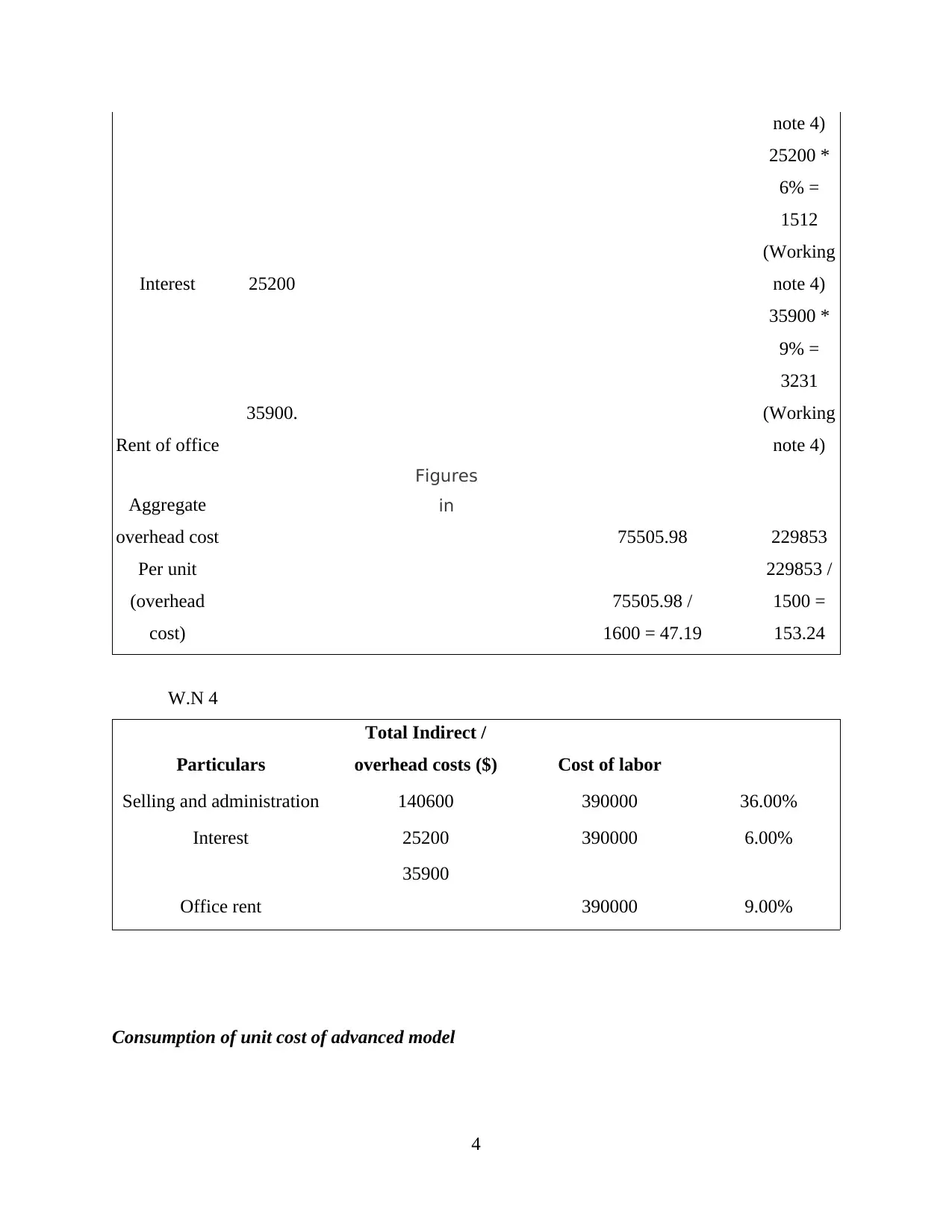

Particulars

Total

Indirect /

overhead

costs($)

Total of

activities A ($) B C ($) D E ($)

Inspection 20000 950 21.05 200 4210.53 750 15789.47

Assembly 90000 8000 11.25 4600 51750 3400 38250

Production

Scheduling 105000 550 190.91 50 9545.45 500 95454.55

Machine set-

up 35000 350 100 100 10000 250 25000

Selling and

administratio

n

140600 140600 *

36% =

50616

(Working

3

cost drivers Overhead costs Sum of activities

Overhead cost/ sum

of activity ($)

Inspection 20000 950 21.05

Assembly 90000 8000 11.25

Production scheduling 105000 550 190.91

Machine set up 35000 350 100

A Activity rate

B Activity usage by basic model

C

Activity Cost Assigned to basic model [C

= (A * B)]

D Activity usage by advance model

E

Activity cost assigned to advance model

[E =(A * D)]

Particulars

Total

Indirect /

overhead

costs($)

Total of

activities A ($) B C ($) D E ($)

Inspection 20000 950 21.05 200 4210.53 750 15789.47

Assembly 90000 8000 11.25 4600 51750 3400 38250

Production

Scheduling 105000 550 190.91 50 9545.45 500 95454.55

Machine set-

up 35000 350 100 100 10000 250 25000

Selling and

administratio

n

140600 140600 *

36% =

50616

(Working

3

note 4)

Interest 25200

25200 *

6% =

1512

(Working

note 4)

Rent of office

35900.

35900 *

9% =

3231

(Working

note 4)

Aggregate

overhead cost

Figures

in

75505.98 229853

Per unit

(overhead

cost)

75505.98 /

1600 = 47.19

229853 /

1500 =

153.24

W.N 4

Particulars

Total Indirect /

overhead costs ($) Cost of labor

Selling and administration 140600 390000 36.00%

Interest 25200 390000 6.00%

Office rent

35900

390000 9.00%

Consumption of unit cost of advanced model

4

Interest 25200

25200 *

6% =

1512

(Working

note 4)

Rent of office

35900.

35900 *

9% =

3231

(Working

note 4)

Aggregate

overhead cost

Figures

in

75505.98 229853

Per unit

(overhead

cost)

75505.98 /

1600 = 47.19

229853 /

1500 =

153.24

W.N 4

Particulars

Total Indirect /

overhead costs ($) Cost of labor

Selling and administration 140600 390000 36.00%

Interest 25200 390000 6.00%

Office rent

35900

390000 9.00%

Consumption of unit cost of advanced model

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

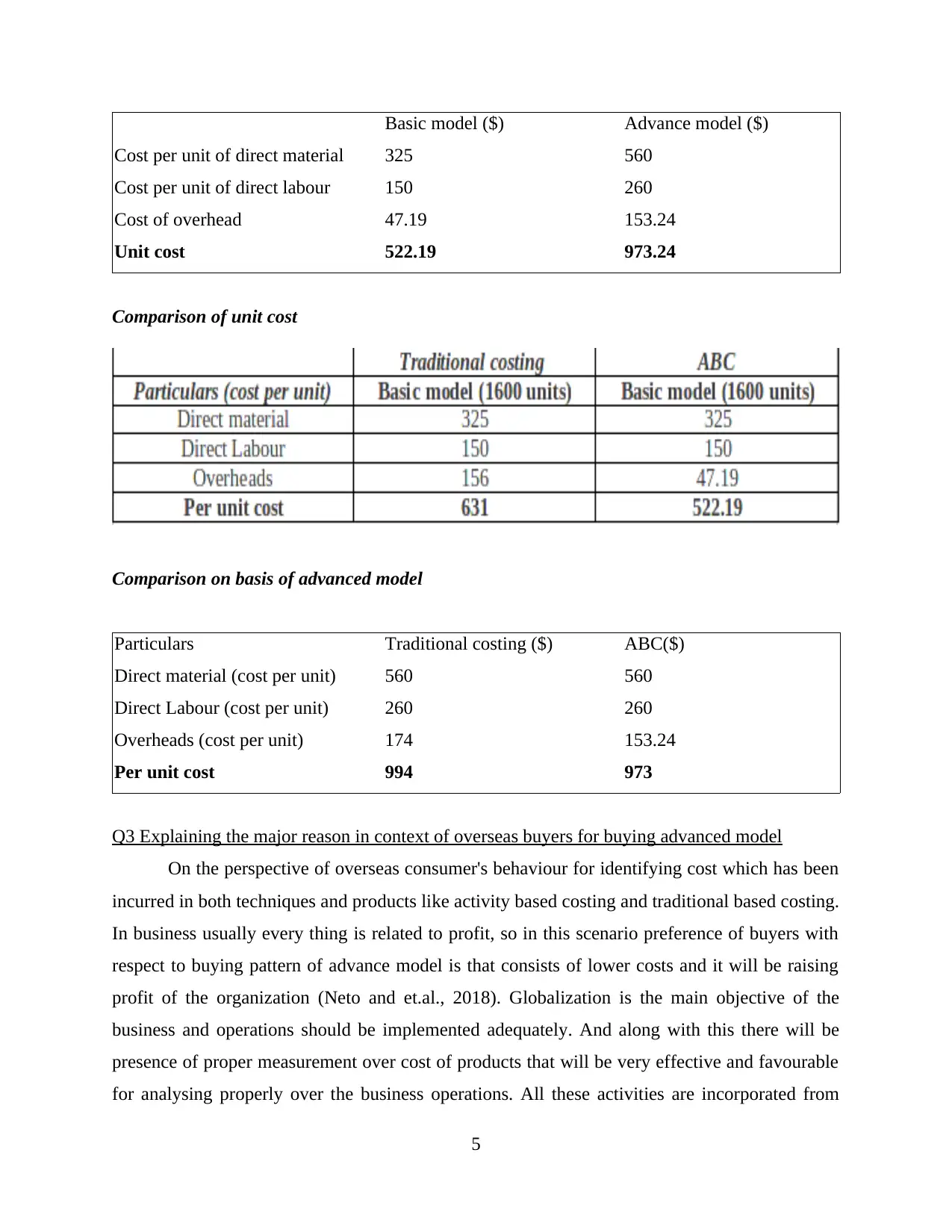

Basic model ($) Advance model ($)

Cost per unit of direct material 325 560

Cost per unit of direct labour 150 260

Cost of overhead 47.19 153.24

Unit cost 522.19 973.24

Comparison of unit cost

Comparison on basis of advanced model

Particulars Traditional costing ($) ABC($)

Direct material (cost per unit) 560 560

Direct Labour (cost per unit) 260 260

Overheads (cost per unit) 174 153.24

Per unit cost 994 973

Q3 Explaining the major reason in context of overseas buyers for buying advanced model

On the perspective of overseas consumer's behaviour for identifying cost which has been

incurred in both techniques and products like activity based costing and traditional based costing.

In business usually every thing is related to profit, so in this scenario preference of buyers with

respect to buying pattern of advance model is that consists of lower costs and it will be raising

profit of the organization (Neto and et.al., 2018). Globalization is the main objective of the

business and operations should be implemented adequately. And along with this there will be

presence of proper measurement over cost of products that will be very effective and favourable

for analysing properly over the business operations. All these activities are incorporated from

5

Cost per unit of direct material 325 560

Cost per unit of direct labour 150 260

Cost of overhead 47.19 153.24

Unit cost 522.19 973.24

Comparison of unit cost

Comparison on basis of advanced model

Particulars Traditional costing ($) ABC($)

Direct material (cost per unit) 560 560

Direct Labour (cost per unit) 260 260

Overheads (cost per unit) 174 153.24

Per unit cost 994 973

Q3 Explaining the major reason in context of overseas buyers for buying advanced model

On the perspective of overseas consumer's behaviour for identifying cost which has been

incurred in both techniques and products like activity based costing and traditional based costing.

In business usually every thing is related to profit, so in this scenario preference of buyers with

respect to buying pattern of advance model is that consists of lower costs and it will be raising

profit of the organization (Neto and et.al., 2018). Globalization is the main objective of the

business and operations should be implemented adequately. And along with this there will be

presence of proper measurement over cost of products that will be very effective and favourable

for analysing properly over the business operations. All these activities are incorporated from

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

control which is suitable and its execution of the spending of the firm i.e. over purchasing and

good manufacturing. As there are many other methods and techniques will be creating help for

managing the operations which are related to business and costing of product is totally relevant

for allocating cost, information related to related inventory for managing business management.

Q4 Explaining reasons on the basis of same overheads and recommending ways for dealing with

its fluctuations.

To run a business, there is requirement of overhead but they are not attributed directly to

any specific or particular business activity. As they do not directly link to generating profits but

overheads are every essential because they give captious support for profit making activity. In

the same series example of overheads are depreciation, insurance, licenses and government fees,

property taxes, rent, utilities and administrative salaries etc.

On the linear perspective of traditional costing techniques there will be proper

identification of betterment rate which will be very beneficial for managing the operation which

are related to business and along with that the overhead expenses which are related to business.

Consequently, there are no possibilities which are affiliated to overhead and will be under

absorbed or over absorbed cost (Islam and et.al., 2017). There is basic treatment which are

relevant with under absorbed and over absorbed overheads in cost accounts which be benefiting

the organisation by managing the operations like:

The past period's amount has been brought or carry forward in the next period which will

be providing a brief analysis over the expenses which are related to overhead.

There will be presence of write off an amount of money to costing of firm's account in

profit and loss statement and it will be creating efficiency, effective and assistive analysis

over each and every firm's activities.

On the basis of production process rate of supplementary rate has been worked out

properly.

Q5 Merits and demerits of activity based costing system

Activity based costing system can be identified as managerial accounting method which

keeps track on overhead costs of activities and these activities are been assigned to objects i.e.

process of allocating overhead, indirect costs to each and every department and costs which has

been generating costs in process of production. Usually it keeps track on activities which has

been identified or process of production which can be an alternative to job. Under this system all

6

good manufacturing. As there are many other methods and techniques will be creating help for

managing the operations which are related to business and costing of product is totally relevant

for allocating cost, information related to related inventory for managing business management.

Q4 Explaining reasons on the basis of same overheads and recommending ways for dealing with

its fluctuations.

To run a business, there is requirement of overhead but they are not attributed directly to

any specific or particular business activity. As they do not directly link to generating profits but

overheads are every essential because they give captious support for profit making activity. In

the same series example of overheads are depreciation, insurance, licenses and government fees,

property taxes, rent, utilities and administrative salaries etc.

On the linear perspective of traditional costing techniques there will be proper

identification of betterment rate which will be very beneficial for managing the operation which

are related to business and along with that the overhead expenses which are related to business.

Consequently, there are no possibilities which are affiliated to overhead and will be under

absorbed or over absorbed cost (Islam and et.al., 2017). There is basic treatment which are

relevant with under absorbed and over absorbed overheads in cost accounts which be benefiting

the organisation by managing the operations like:

The past period's amount has been brought or carry forward in the next period which will

be providing a brief analysis over the expenses which are related to overhead.

There will be presence of write off an amount of money to costing of firm's account in

profit and loss statement and it will be creating efficiency, effective and assistive analysis

over each and every firm's activities.

On the basis of production process rate of supplementary rate has been worked out

properly.

Q5 Merits and demerits of activity based costing system

Activity based costing system can be identified as managerial accounting method which

keeps track on overhead costs of activities and these activities are been assigned to objects i.e.

process of allocating overhead, indirect costs to each and every department and costs which has

been generating costs in process of production. Usually it keeps track on activities which has

been identified or process of production which can be an alternative to job. Under this system all

6

activities are collaborated with same processes into pool of cost which is accompanying to single

activity cost driver.

Merits:

Accuracy in product's cost: This method gives an indication toward accuracy and

reliability in cost of product and identification by giving major importance to cause and

effect relationship in cost occurrence (Dhubea, Salim and Al-Riami, 2017). The

activities are recognized which incur cost but not products and it is considered as product

which consumes activities. Realistic products costs has been provided by this system.

Information related to cost behaviour: The real nature of cost behaviour has been

identified by this method which will be a medium to reduce cost and activities which are

not related to adding value to any product (Zhuang and Chang, 2017). Fixed overhead

cost can be controlled by managers of this system by putting more efforts on control over

activities which has lead to create cost of fixed overhead.

To keep track on activities which are related to cost object: In this system many cost

drivers are used and transaction which are based instead of volume of product. And this

method is purely concerned with every activity i.e. within or factory behind for tracking

more overheads to each products.

To keep track on overhead costs: The cost of managerial responsibility, customers,

processes and departments which are besides the cost of product has been traced in this

activity based method (Advantages of Activity Based Costing, 2018).

Managing cost: Activity based costing gives a cost driver rates and every transaction's

information and there volume which is beneficiary for management for managing cost

and appraisal of performance of ever responsibility centres (Kaddoura, Kröger and

Nagel, 2017). For designing new product or existing product cost driver rates is an

advantage because of indication of overhead costs which has to be usually applied in

product's costing.

More usage of capacity and reducing cost: ABC system is refereed as a process of

pooling activity costs and its cost drivers have been identified which leads to

application's range. It consists of identifying the spare capacity and cost reduction should

be foster by comparing resources under ABC system and currently given resources. The

7

activity cost driver.

Merits:

Accuracy in product's cost: This method gives an indication toward accuracy and

reliability in cost of product and identification by giving major importance to cause and

effect relationship in cost occurrence (Dhubea, Salim and Al-Riami, 2017). The

activities are recognized which incur cost but not products and it is considered as product

which consumes activities. Realistic products costs has been provided by this system.

Information related to cost behaviour: The real nature of cost behaviour has been

identified by this method which will be a medium to reduce cost and activities which are

not related to adding value to any product (Zhuang and Chang, 2017). Fixed overhead

cost can be controlled by managers of this system by putting more efforts on control over

activities which has lead to create cost of fixed overhead.

To keep track on activities which are related to cost object: In this system many cost

drivers are used and transaction which are based instead of volume of product. And this

method is purely concerned with every activity i.e. within or factory behind for tracking

more overheads to each products.

To keep track on overhead costs: The cost of managerial responsibility, customers,

processes and departments which are besides the cost of product has been traced in this

activity based method (Advantages of Activity Based Costing, 2018).

Managing cost: Activity based costing gives a cost driver rates and every transaction's

information and there volume which is beneficiary for management for managing cost

and appraisal of performance of ever responsibility centres (Kaddoura, Kröger and

Nagel, 2017). For designing new product or existing product cost driver rates is an

advantage because of indication of overhead costs which has to be usually applied in

product's costing.

More usage of capacity and reducing cost: ABC system is refereed as a process of

pooling activity costs and its cost drivers have been identified which leads to

application's range. It consists of identifying the spare capacity and cost reduction should

be foster by comparing resources under ABC system and currently given resources. The

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

platform for development has been given in this system which can be used for

forecasting requirements of future resources.

Service industry has been benefited: Usually organizations like banks, government

department and hospitals does not have direct costs, usually there is presence of

overheads. So on this perspective it gives better information of costing and management

helps to efficiently manage and better understanding of competitive advantage of firm,

their strength and weakness has been gained.

Demerits

Complexity and expensive: This method has many cost pools and cost drivers and they

are more complex as compared to traditional method, this will also lead to be expensive

for managing activity based costing system.

Choosing drivers: While implementing ABC system there are many difficulties which

has been emerged like choosing cost drivers, common cost assignments which varies

from cost driver rates (Oseifuah, 2018).

Smaller firms are in disadvantage: As in this method there are different levels for

utility in many organisations like many manufacturing organisation can take advantage of

this method while comparing with smaller organizations. Usually firms which are

dependent on cost and even pricing which will be gaining advantage from ABC as

accuracy of product's cost has been provided (Biondi and et.al., 2018). But on the

contrary side market based prices are against ABC system. Application of ABC has been

affected by level of technology and manufacturing environment which prevails in various

other firms.

Difficulties are been measured: The main disadvantage of Activity based costing

system is that implementation of various measurements are very necessary. In this

method there is requirement of management for estimating costs of activity pools and to

measure and determine cost drivers for serving better base of cost allocation. Various

other calculations are required in ABC system for identifying cost of each product and

services (Fang, Ma and Luo, 2018). As this leads to very expensive especially

measurements and activity based costing should be updated on regular basis.

Data set has been misrepresented

8

forecasting requirements of future resources.

Service industry has been benefited: Usually organizations like banks, government

department and hospitals does not have direct costs, usually there is presence of

overheads. So on this perspective it gives better information of costing and management

helps to efficiently manage and better understanding of competitive advantage of firm,

their strength and weakness has been gained.

Demerits

Complexity and expensive: This method has many cost pools and cost drivers and they

are more complex as compared to traditional method, this will also lead to be expensive

for managing activity based costing system.

Choosing drivers: While implementing ABC system there are many difficulties which

has been emerged like choosing cost drivers, common cost assignments which varies

from cost driver rates (Oseifuah, 2018).

Smaller firms are in disadvantage: As in this method there are different levels for

utility in many organisations like many manufacturing organisation can take advantage of

this method while comparing with smaller organizations. Usually firms which are

dependent on cost and even pricing which will be gaining advantage from ABC as

accuracy of product's cost has been provided (Biondi and et.al., 2018). But on the

contrary side market based prices are against ABC system. Application of ABC has been

affected by level of technology and manufacturing environment which prevails in various

other firms.

Difficulties are been measured: The main disadvantage of Activity based costing

system is that implementation of various measurements are very necessary. In this

method there is requirement of management for estimating costs of activity pools and to

measure and determine cost drivers for serving better base of cost allocation. Various

other calculations are required in ABC system for identifying cost of each product and

services (Fang, Ma and Luo, 2018). As this leads to very expensive especially

measurements and activity based costing should be updated on regular basis.

Data set has been misrepresented

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it has been concluded that management accounting plays vital role

in any business or organization. In the present scenario, traditional costing is not giving highly

effective results or there is lack of efficiency. As activity based costing system provides

manufacturing overhead cost in very systematic and logic manner instead of allocating all

expenses on the perspective of machine hours. Activity based costing system is highly

recommended to Sewing easy ltd because of its perfect suitability to the modern environment.

With applying ABC system this company will be easily setting appropriate cost of both basic and

advanced model and even many more entities also has huge demand for the same.

9

From the above report it has been concluded that management accounting plays vital role

in any business or organization. In the present scenario, traditional costing is not giving highly

effective results or there is lack of efficiency. As activity based costing system provides

manufacturing overhead cost in very systematic and logic manner instead of allocating all

expenses on the perspective of machine hours. Activity based costing system is highly

recommended to Sewing easy ltd because of its perfect suitability to the modern environment.

With applying ABC system this company will be easily setting appropriate cost of both basic and

advanced model and even many more entities also has huge demand for the same.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.