Business Finance: Traditional and Alternative Budgeting Report

VerifiedAdded on 2020/10/22

|11

|3361

|163

Report

AI Summary

This report provides a comprehensive analysis of budgeting within the context of business finance. It begins by outlining the purpose, process, and benefits of preparing a budget, emphasizing its role in planning, coordination, and control. The report then demonstrates the application of traditional budgeting approaches, including incremental budgeting, and evaluates their appropriateness in the current business environment. Furthermore, it explores alternative budgeting methods such as zero-based, rolling, and activity-based budgeting, discussing their respective merits and drawbacks. The report concludes by analyzing the effectiveness of different budgeting methods and combinations, offering insights into which approaches are most beneficial for a business entity. The content covers key aspects of financial planning, resource allocation, and performance evaluation, providing a detailed overview of budgeting techniques and their practical implications.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Purpose of preparing budget with its process and its benefits to business model...................1

2. Demonstrating application of traditional budgeting approaches along with incremental

budgeting.....................................................................................................................................2

3. Analysing traditional budgetary system is appropriate or not.................................................3

PART 2............................................................................................................................................5

4. Understanding on alternative budget method with its merits and drawbacks.........................5

5. Application of these methods with elements of budgeting as alternative method..................7

6. Analysing that one or combination method is beneficial to business entity............................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Purpose of preparing budget with its process and its benefits to business model...................1

2. Demonstrating application of traditional budgeting approaches along with incremental

budgeting.....................................................................................................................................2

3. Analysing traditional budgetary system is appropriate or not.................................................3

PART 2............................................................................................................................................5

4. Understanding on alternative budget method with its merits and drawbacks.........................5

5. Application of these methods with elements of budgeting as alternative method..................7

6. Analysing that one or combination method is beneficial to business entity............................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Business finance is consider as very important aspect for business perspective, as this report

will give brief description about budgeting which is beneficial to business model. It will

demonstrate application traditional budgeting approaches. It will analyse about that traditional

budgetary which is appropriate or not. This report will discuss about alternative budget methods

such as zero, rolling and activity based budgets with its merits and demerits along with perfect

combination or individual to be mix.

PART 1

1. Purpose of preparing budget with its process and its benefits to business model

Budgeting is considered as process for implementing, operating and designing budget. It

is referred as managerial process of preparing and planning budget, budgetary control along with

each related procedure. With context of accounting, it is at highest level as in future it indicates

definite action course and not reporting merely. It should be not known as forecasting as it helps

in predicting budget but here this process is physically replicated as detailed analysis and

planning with absence of prognosticating future outcome. The overall objective of budgeting is

to plan about multiple phases of operations of business and to coordinate activities of different

departments of business entity for ensuring about effective control (Bassemir and Novotny‐

Farkas, 2018).

The firm’s future financial condition is anticipated and future requirements for funds are

employed in business with perspective of keeping business as solvent. The composition of

capitalisation has been decided for ensuring about funds availability at reasonable cost. The

efficiency about operations has been accelerated among divisions, departments and firm's cost

centres. Further, the responsibilities are fix on basis of different departmental heads. The

effective control has been ensured about its inventory, sales and cash. It also facilitates

centralised control over business entity over budgetary system.

The process of budgeting for big companies directly initiates prior to four to six months

before the financial year as some might take whole financial year for completing it. The budget

could be set and undertakes variance analysis on monthly aspect. The initial planning stage,

organization will go via series of stage and appropriate implementation. The most common

process considers communication in executive management, setting targets and objectives,

1

Business finance is consider as very important aspect for business perspective, as this report

will give brief description about budgeting which is beneficial to business model. It will

demonstrate application traditional budgeting approaches. It will analyse about that traditional

budgetary which is appropriate or not. This report will discuss about alternative budget methods

such as zero, rolling and activity based budgets with its merits and demerits along with perfect

combination or individual to be mix.

PART 1

1. Purpose of preparing budget with its process and its benefits to business model

Budgeting is considered as process for implementing, operating and designing budget. It

is referred as managerial process of preparing and planning budget, budgetary control along with

each related procedure. With context of accounting, it is at highest level as in future it indicates

definite action course and not reporting merely. It should be not known as forecasting as it helps

in predicting budget but here this process is physically replicated as detailed analysis and

planning with absence of prognosticating future outcome. The overall objective of budgeting is

to plan about multiple phases of operations of business and to coordinate activities of different

departments of business entity for ensuring about effective control (Bassemir and Novotny‐

Farkas, 2018).

The firm’s future financial condition is anticipated and future requirements for funds are

employed in business with perspective of keeping business as solvent. The composition of

capitalisation has been decided for ensuring about funds availability at reasonable cost. The

efficiency about operations has been accelerated among divisions, departments and firm's cost

centres. Further, the responsibilities are fix on basis of different departmental heads. The

effective control has been ensured about its inventory, sales and cash. It also facilitates

centralised control over business entity over budgetary system.

The process of budgeting for big companies directly initiates prior to four to six months

before the financial year as some might take whole financial year for completing it. The budget

could be set and undertakes variance analysis on monthly aspect. The initial planning stage,

organization will go via series of stage and appropriate implementation. The most common

process considers communication in executive management, setting targets and objectives,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

developing detailed budget, revision and compilation of budget model, review about budget

committee along with board approval.

The budget will give benefit to business which considers ability for purpose of following

management strategy for raising market share, earning margin and to raise current margin. This

will be avoiding multiple pitfalls which will put small companies not in business. The expansion

plan about operations and application for financing, there is request from bank loan officer with

projection of future budget. Simultaneously, business plan consists of applying to federal for

granting money then budgeting is referred as necessity.

2. Demonstrating application of traditional budgeting approaches along with incremental

budgeting

In the present scenario, rapid changing conditions and technology of modern world are

forcing organizations for reviewing budget system and management. In the similar aspect, there

is maintenance of sustainable organization as company management should optimize availability

of multiple financial resources through planning and controlling. The most widely used

management tool for planning and controlling is budgeting (Black and et.al., 2018). It main

objective is to produce system for performance evaluation and to raise employee motivation

through enhancing communication and coordination among companies subsections. On the

contrary, approach of traditional budgeting is refereed as method for preparing budget where last

year's budget is considered as base. The budget of present year is prepared for making alterations

to budget of past year with adjustments of expenses on basis of rate of inflation, market situation,

consumer demand etc. The revenue and cost through integral part of budget of current year.

There is only identification of items which are to be justified in over and above budget of last

year in traditional budgets.

Particulars January February March April May June

Cash inflows

Opening cash inflow 7000 7840 11335 14913.98 18575.79 22319.15

Total revenue 13000 13260 13525.2 13796 14072 14353

Other income 5000 5000 5000 5000 5000 5000

Sum of cash inflows 25000 26100 29860.2 33709.68 37647.41 41672.2

2

committee along with board approval.

The budget will give benefit to business which considers ability for purpose of following

management strategy for raising market share, earning margin and to raise current margin. This

will be avoiding multiple pitfalls which will put small companies not in business. The expansion

plan about operations and application for financing, there is request from bank loan officer with

projection of future budget. Simultaneously, business plan consists of applying to federal for

granting money then budgeting is referred as necessity.

2. Demonstrating application of traditional budgeting approaches along with incremental

budgeting

In the present scenario, rapid changing conditions and technology of modern world are

forcing organizations for reviewing budget system and management. In the similar aspect, there

is maintenance of sustainable organization as company management should optimize availability

of multiple financial resources through planning and controlling. The most widely used

management tool for planning and controlling is budgeting (Black and et.al., 2018). It main

objective is to produce system for performance evaluation and to raise employee motivation

through enhancing communication and coordination among companies subsections. On the

contrary, approach of traditional budgeting is refereed as method for preparing budget where last

year's budget is considered as base. The budget of present year is prepared for making alterations

to budget of past year with adjustments of expenses on basis of rate of inflation, market situation,

consumer demand etc. The revenue and cost through integral part of budget of current year.

There is only identification of items which are to be justified in over and above budget of last

year in traditional budgets.

Particulars January February March April May June

Cash inflows

Opening cash inflow 7000 7840 11335 14913.98 18575.79 22319.15

Total revenue 13000 13260 13525.2 13796 14072 14353

Other income 5000 5000 5000 5000 5000 5000

Sum of cash inflows 25000 26100 29860.2 33709.68 37647.41 41672.2

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

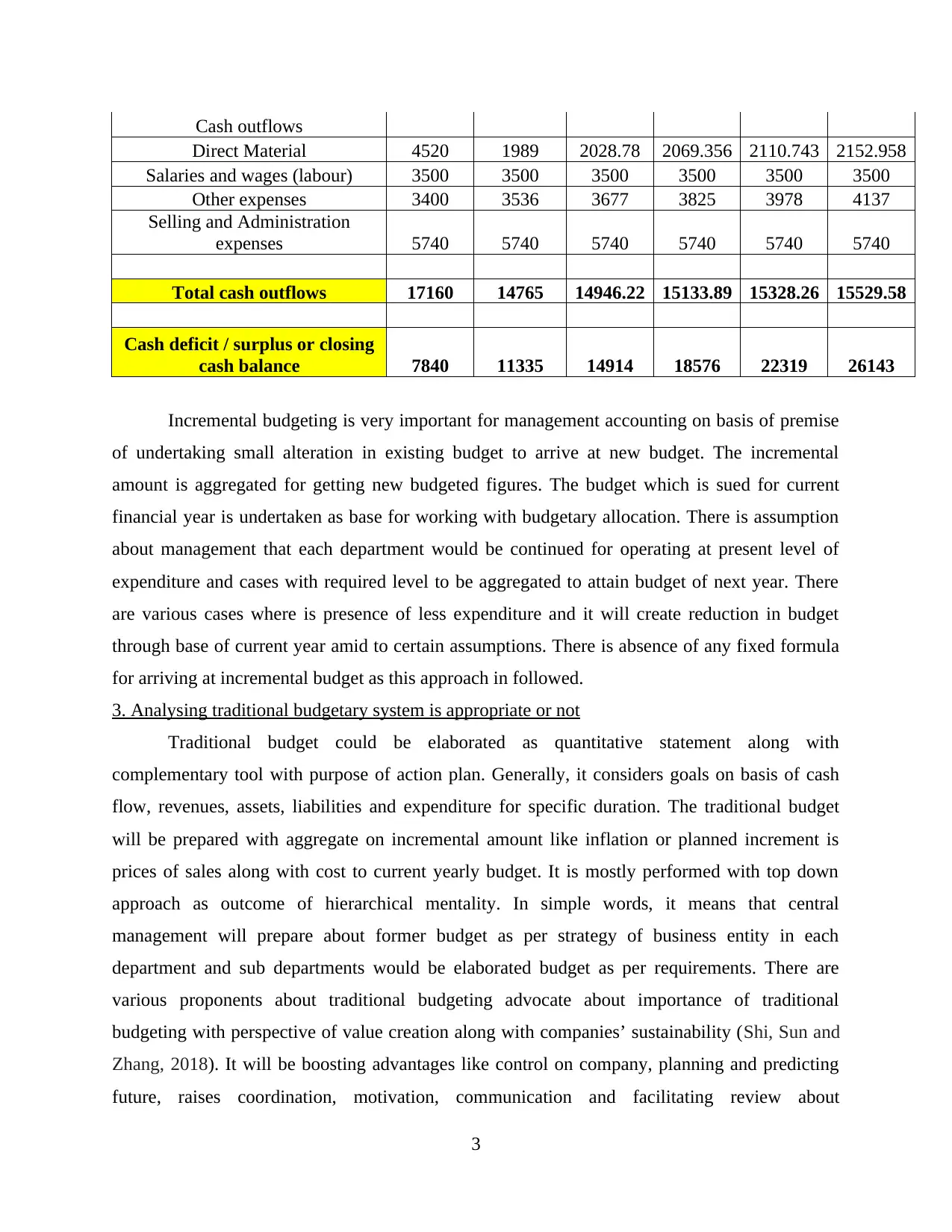

Cash outflows

Direct Material 4520 1989 2028.78 2069.356 2110.743 2152.958

Salaries and wages (labour) 3500 3500 3500 3500 3500 3500

Other expenses 3400 3536 3677 3825 3978 4137

Selling and Administration

expenses 5740 5740 5740 5740 5740 5740

Total cash outflows 17160 14765 14946.22 15133.89 15328.26 15529.58

Cash deficit / surplus or closing

cash balance 7840 11335 14914 18576 22319 26143

Incremental budgeting is very important for management accounting on basis of premise

of undertaking small alteration in existing budget to arrive at new budget. The incremental

amount is aggregated for getting new budgeted figures. The budget which is sued for current

financial year is undertaken as base for working with budgetary allocation. There is assumption

about management that each department would be continued for operating at present level of

expenditure and cases with required level to be aggregated to attain budget of next year. There

are various cases where is presence of less expenditure and it will create reduction in budget

through base of current year amid to certain assumptions. There is absence of any fixed formula

for arriving at incremental budget as this approach in followed.

3. Analysing traditional budgetary system is appropriate or not

Traditional budget could be elaborated as quantitative statement along with

complementary tool with purpose of action plan. Generally, it considers goals on basis of cash

flow, revenues, assets, liabilities and expenditure for specific duration. The traditional budget

will be prepared with aggregate on incremental amount like inflation or planned increment is

prices of sales along with cost to current yearly budget. It is mostly performed with top down

approach as outcome of hierarchical mentality. In simple words, it means that central

management will prepare about former budget as per strategy of business entity in each

department and sub departments would be elaborated budget as per requirements. There are

various proponents about traditional budgeting advocate about importance of traditional

budgeting with perspective of value creation along with companies’ sustainability (Shi, Sun and

Zhang, 2018). It will be boosting advantages like control on company, planning and predicting

future, raises coordination, motivation, communication and facilitating review about

3

Direct Material 4520 1989 2028.78 2069.356 2110.743 2152.958

Salaries and wages (labour) 3500 3500 3500 3500 3500 3500

Other expenses 3400 3536 3677 3825 3978 4137

Selling and Administration

expenses 5740 5740 5740 5740 5740 5740

Total cash outflows 17160 14765 14946.22 15133.89 15328.26 15529.58

Cash deficit / surplus or closing

cash balance 7840 11335 14914 18576 22319 26143

Incremental budgeting is very important for management accounting on basis of premise

of undertaking small alteration in existing budget to arrive at new budget. The incremental

amount is aggregated for getting new budgeted figures. The budget which is sued for current

financial year is undertaken as base for working with budgetary allocation. There is assumption

about management that each department would be continued for operating at present level of

expenditure and cases with required level to be aggregated to attain budget of next year. There

are various cases where is presence of less expenditure and it will create reduction in budget

through base of current year amid to certain assumptions. There is absence of any fixed formula

for arriving at incremental budget as this approach in followed.

3. Analysing traditional budgetary system is appropriate or not

Traditional budget could be elaborated as quantitative statement along with

complementary tool with purpose of action plan. Generally, it considers goals on basis of cash

flow, revenues, assets, liabilities and expenditure for specific duration. The traditional budget

will be prepared with aggregate on incremental amount like inflation or planned increment is

prices of sales along with cost to current yearly budget. It is mostly performed with top down

approach as outcome of hierarchical mentality. In simple words, it means that central

management will prepare about former budget as per strategy of business entity in each

department and sub departments would be elaborated budget as per requirements. There are

various proponents about traditional budgeting advocate about importance of traditional

budgeting with perspective of value creation along with companies’ sustainability (Shi, Sun and

Zhang, 2018). It will be boosting advantages like control on company, planning and predicting

future, raises coordination, motivation, communication and facilitating review about

3

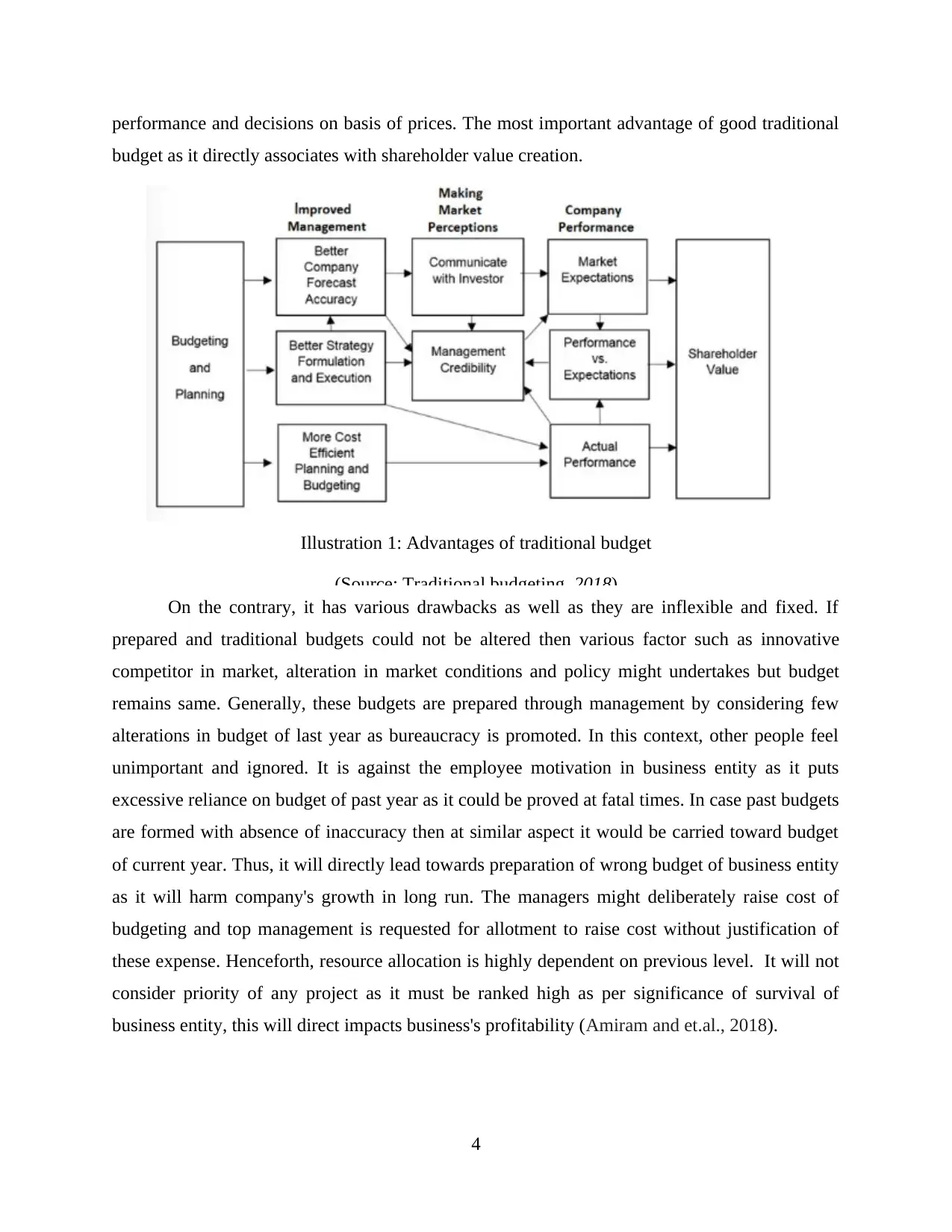

performance and decisions on basis of prices. The most important advantage of good traditional

budget as it directly associates with shareholder value creation.

Illustration 1: Advantages of traditional budget

(Source: Traditional budgeting, 2018)

On the contrary, it has various drawbacks as well as they are inflexible and fixed. If

prepared and traditional budgets could not be altered then various factor such as innovative

competitor in market, alteration in market conditions and policy might undertakes but budget

remains same. Generally, these budgets are prepared through management by considering few

alterations in budget of last year as bureaucracy is promoted. In this context, other people feel

unimportant and ignored. It is against the employee motivation in business entity as it puts

excessive reliance on budget of past year as it could be proved at fatal times. In case past budgets

are formed with absence of inaccuracy then at similar aspect it would be carried toward budget

of current year. Thus, it will directly lead towards preparation of wrong budget of business entity

as it will harm company's growth in long run. The managers might deliberately raise cost of

budgeting and top management is requested for allotment to raise cost without justification of

these expense. Henceforth, resource allocation is highly dependent on previous level. It will not

consider priority of any project as it must be ranked high as per significance of survival of

business entity, this will direct impacts business's profitability (Amiram and et.al., 2018).

4

budget as it directly associates with shareholder value creation.

Illustration 1: Advantages of traditional budget

(Source: Traditional budgeting, 2018)

On the contrary, it has various drawbacks as well as they are inflexible and fixed. If

prepared and traditional budgets could not be altered then various factor such as innovative

competitor in market, alteration in market conditions and policy might undertakes but budget

remains same. Generally, these budgets are prepared through management by considering few

alterations in budget of last year as bureaucracy is promoted. In this context, other people feel

unimportant and ignored. It is against the employee motivation in business entity as it puts

excessive reliance on budget of past year as it could be proved at fatal times. In case past budgets

are formed with absence of inaccuracy then at similar aspect it would be carried toward budget

of current year. Thus, it will directly lead towards preparation of wrong budget of business entity

as it will harm company's growth in long run. The managers might deliberately raise cost of

budgeting and top management is requested for allotment to raise cost without justification of

these expense. Henceforth, resource allocation is highly dependent on previous level. It will not

consider priority of any project as it must be ranked high as per significance of survival of

business entity, this will direct impacts business's profitability (Amiram and et.al., 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2

4. Understanding on alternative budget method with its merits and drawbacks

Rolling budget: It is updated on continual aspect as it will aggregate new period of

budget as with completion of recent budget period. It considers huge attention through

management as in this case organisation forms one year static budget as some activities of

budgeting should be repeated at each month. If there is usage of participative budgeting for

purpose of creating budget on rolling aspect, the total employee time will be used over

substantial course of year. Conversely, it is best for adapting leaner approach for rolling budget

as very less people are engaged in this process.

Merits

It helps in controlling and planning in accurate aspect as it will decrease uncertainty

about budgeting. The plan for rolling budget is for near term future rather than long term. This

will help management for information that business entity with perspective of profitability and

sales. The 12 months period budgets are replicated for long term due to technological

advancement. The technology will alter at foster rate. It might lead the business entity for

altering with advanced technology. So budget has requirement to be updated with reference to

assumptions.

Demerits

It has huge requirement of more money, efforts and time as employees spend money on

determined opportunities. It is tool for decision making as it is the best practice of team for few

people engaged in updating and involving preparation of rolling budget. It is resource and time

intensive as managers might find as constant revision about budget unsettling along with

disruptive. The rolling budget could be updated on monthly, quarterly and yearly aspect as in this

update, recent duration is deleted and new period is directly appended at end of present budget.

Conversely, manager’s time spent on process of budget instead of operational problems which

could give negative impact on performance of company. It is also changing objectives of

managers as he has to attain objectives set through original budget as compared to set objectives

revised with this rolling budget as they will not fully commit in process of budget (Torfs, 2018).

Zero based budget: It is in management accounting which has huge involvement of preparing

budget through scratch with zero as base. In the similar aspect, it will involve reevaluating each

item in cash flow statement and expenditure is justified with incurrence by department. Hence, in

5

4. Understanding on alternative budget method with its merits and drawbacks

Rolling budget: It is updated on continual aspect as it will aggregate new period of

budget as with completion of recent budget period. It considers huge attention through

management as in this case organisation forms one year static budget as some activities of

budgeting should be repeated at each month. If there is usage of participative budgeting for

purpose of creating budget on rolling aspect, the total employee time will be used over

substantial course of year. Conversely, it is best for adapting leaner approach for rolling budget

as very less people are engaged in this process.

Merits

It helps in controlling and planning in accurate aspect as it will decrease uncertainty

about budgeting. The plan for rolling budget is for near term future rather than long term. This

will help management for information that business entity with perspective of profitability and

sales. The 12 months period budgets are replicated for long term due to technological

advancement. The technology will alter at foster rate. It might lead the business entity for

altering with advanced technology. So budget has requirement to be updated with reference to

assumptions.

Demerits

It has huge requirement of more money, efforts and time as employees spend money on

determined opportunities. It is tool for decision making as it is the best practice of team for few

people engaged in updating and involving preparation of rolling budget. It is resource and time

intensive as managers might find as constant revision about budget unsettling along with

disruptive. The rolling budget could be updated on monthly, quarterly and yearly aspect as in this

update, recent duration is deleted and new period is directly appended at end of present budget.

Conversely, manager’s time spent on process of budget instead of operational problems which

could give negative impact on performance of company. It is also changing objectives of

managers as he has to attain objectives set through original budget as compared to set objectives

revised with this rolling budget as they will not fully commit in process of budget (Torfs, 2018).

Zero based budget: It is in management accounting which has huge involvement of preparing

budget through scratch with zero as base. In the similar aspect, it will involve reevaluating each

item in cash flow statement and expenditure is justified with incurrence by department. Hence, in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this method each expense for innovative period with calculation with reference to actual

expenses which is going to be incurred but not on differential aspect as it engages alteration in

expenses with account change in operational activity.

Merits

It will lead to accuracy as it involves some arbitrary alterations from budget of previous

year as this helps department for relooking each and every aspect of cash flow and computation

of operating cost. It will help in allocation of resources in efficient manner as it leads to

determine opportunities and very cost effective method of performing thing by ridding each

unproductive and redundant activity. It overcomes weakness of budgeting on incremental aspect

with context of budget inflation (Gachoka and et.al., 2018).

Demerits

It is highly time consuming as very time extensive for government funded entities and

company which is far easier method as it has requirement of high manpower as various

department does not have adequate human resource and time .It has lack of expertise because it

gives explanation to each line item and every cost is difficult task with need of appropriate

training to managers.

Activity based budget: It is a system which records, analyses and researches activities which

will lead to cost of particular business. It is more than merely adjusting past budgets for inflation

account or with business development.

Merits

It helps for evaluating every cost driver and considers each step in activity as it

substitutes each type of unnecessary activities so cost is decreased. In simple words, it gives

competitive edge in market as this technique helps to view business as one unit but not in context

of departments. It helps in improving relationship among its customers and organization as its

main objective is for eliminating all useless activities and best quality has been served.

Demerits

It has need of deep understanding of multiple functional areas of business as it is very

complex in nature. It has consumption of numerous resources as it employs top officials for

purpose of analysis. This activity implementation has need of trained employees so there is need

of high cost thus it is very expensive (Block and et.al., 2018).

6

expenses which is going to be incurred but not on differential aspect as it engages alteration in

expenses with account change in operational activity.

Merits

It will lead to accuracy as it involves some arbitrary alterations from budget of previous

year as this helps department for relooking each and every aspect of cash flow and computation

of operating cost. It will help in allocation of resources in efficient manner as it leads to

determine opportunities and very cost effective method of performing thing by ridding each

unproductive and redundant activity. It overcomes weakness of budgeting on incremental aspect

with context of budget inflation (Gachoka and et.al., 2018).

Demerits

It is highly time consuming as very time extensive for government funded entities and

company which is far easier method as it has requirement of high manpower as various

department does not have adequate human resource and time .It has lack of expertise because it

gives explanation to each line item and every cost is difficult task with need of appropriate

training to managers.

Activity based budget: It is a system which records, analyses and researches activities which

will lead to cost of particular business. It is more than merely adjusting past budgets for inflation

account or with business development.

Merits

It helps for evaluating every cost driver and considers each step in activity as it

substitutes each type of unnecessary activities so cost is decreased. In simple words, it gives

competitive edge in market as this technique helps to view business as one unit but not in context

of departments. It helps in improving relationship among its customers and organization as its

main objective is for eliminating all useless activities and best quality has been served.

Demerits

It has need of deep understanding of multiple functional areas of business as it is very

complex in nature. It has consumption of numerous resources as it employs top officials for

purpose of analysis. This activity implementation has need of trained employees so there is need

of high cost thus it is very expensive (Block and et.al., 2018).

6

5. Application of these methods with elements of budgeting as alternative method

Traditional budgeting is referred as easiest method as it considers consumption and

budgets adjusts through budget with reflection of altering assumptions for coming year and some

incremental cost is fully based on increment in price assumption. But along with this approach

maintenance managers strive for spending entire budget of year, so there is absence of surplus at

ending of year. Developing budget is considered as necessary element for purpose of financial

and operational success within business entity (Hirshman, Pope and Song, 2018). The method of

budgeting with its application of current budget and aggregates with certain percentage there is

increment for arriving at innovative budget. For example, if monthly budget for small business is

about 5000 and as per inflation its business expense has to take aggregate 5%, then innovative

budget as 5250.In the similar aspect, zero based budgeting is very popular method for personal

and household expenses as it could be used for budget of business as well.

In this manner, budgeting examines for every cost about business for ensuring about

necessity. Each expense should be justified as it could be substituted. It could give outcome for

decrease in business expenses as budget is slashed to core. Further, cost could increase with this

method as it determines needs which were unfulfilled along with innovative computer for

conducting business in quicker aspect. It is contrary to incremental budgeting as it is very

difficult for preparing and understanding as well. It is not beneficial to large business as it might

be not manageable because of time involved (Shaukat and Trojanowski, 2018).

6. Analysing that one or combination method is beneficial to business entity

The budget always rises with less effort for observing cost optimization. On the contrary,

zero based budgeting consumes too much time as it is full based on activities and jobs performed

along with continued operation must be justified with reference to usefulness and requirement of

business entity. According to appropriate analysis combination of activity, traditional and zero

based budgeting is beneficial to business entity. Zero based budgeting helps for aligning

allocation of resource with strategic objective as it could be time consuming and hard for

quantifying returns with some expenditure. In the similar aspect, activity based budgeting

determine needs of eliminating various activities for adding value to equipment and product

(Activity Based Budgeting, 2018).

The important aspect with this approach is to hold goods for planning maintenance activities

and unplanned activities and breakdowns with dependency on level of maturity about reliabilitiy

7

Traditional budgeting is referred as easiest method as it considers consumption and

budgets adjusts through budget with reflection of altering assumptions for coming year and some

incremental cost is fully based on increment in price assumption. But along with this approach

maintenance managers strive for spending entire budget of year, so there is absence of surplus at

ending of year. Developing budget is considered as necessary element for purpose of financial

and operational success within business entity (Hirshman, Pope and Song, 2018). The method of

budgeting with its application of current budget and aggregates with certain percentage there is

increment for arriving at innovative budget. For example, if monthly budget for small business is

about 5000 and as per inflation its business expense has to take aggregate 5%, then innovative

budget as 5250.In the similar aspect, zero based budgeting is very popular method for personal

and household expenses as it could be used for budget of business as well.

In this manner, budgeting examines for every cost about business for ensuring about

necessity. Each expense should be justified as it could be substituted. It could give outcome for

decrease in business expenses as budget is slashed to core. Further, cost could increase with this

method as it determines needs which were unfulfilled along with innovative computer for

conducting business in quicker aspect. It is contrary to incremental budgeting as it is very

difficult for preparing and understanding as well. It is not beneficial to large business as it might

be not manageable because of time involved (Shaukat and Trojanowski, 2018).

6. Analysing that one or combination method is beneficial to business entity

The budget always rises with less effort for observing cost optimization. On the contrary,

zero based budgeting consumes too much time as it is full based on activities and jobs performed

along with continued operation must be justified with reference to usefulness and requirement of

business entity. According to appropriate analysis combination of activity, traditional and zero

based budgeting is beneficial to business entity. Zero based budgeting helps for aligning

allocation of resource with strategic objective as it could be time consuming and hard for

quantifying returns with some expenditure. In the similar aspect, activity based budgeting

determine needs of eliminating various activities for adding value to equipment and product

(Activity Based Budgeting, 2018).

The important aspect with this approach is to hold goods for planning maintenance activities

and unplanned activities and breakdowns with dependency on level of maturity about reliabilitiy

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and maintenance program. The optimal solution is undertaken in two for large scale of operating

plants in regular aspect. Further, the best approach is combination of traditional, activity and zero

based budgeting (Lepone and Wong, 2018).

CONCLUSION

From the above study it had been concluded that budgets are very important for business

perspective. It has shown that budget evaluates effectiveness of company and also decreases

unnecessary combination of activities as per ability for gauging performance with application of

budget. It could be summarised that budget allows business for operating in business with

application of resources in efficient manner.

8

plants in regular aspect. Further, the best approach is combination of traditional, activity and zero

based budgeting (Lepone and Wong, 2018).

CONCLUSION

From the above study it had been concluded that budgets are very important for business

perspective. It has shown that budget evaluates effectiveness of company and also decreases

unnecessary combination of activities as per ability for gauging performance with application of

budget. It could be summarised that budget allows business for operating in business with

application of resources in efficient manner.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Amiram, D. and et.al., 2018. How are analysts’ forecasts affected by high uncertainty?. Journal

of Business Finance & Accounting. 45(3-4). pp.295-318.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting. 45(7-8).

pp.759-796.

Black, D. E., and et.al., 2018. Non‐GAAP reporting: Evidence from academia and current

practice. Journal of Business Finance & Accounting. 45(3-4). pp.259-294.

Block, J. H., and et.al., 2018. New players in entrepreneurial finance and why they are

there. Small Business Economics. 50(2). pp.239-250.

Gachoka, N. and et.al., 2018. The Moderating Effect of Organizational Characteristics on the

Relationship Between Budgeting Process and Performance of Churches in Kenya. Journal

of Finance and Investment Analysis. 7(2), pp.1-5.

Hirshman, S., Pope, D. and Song, J., 2018. Mental Budgeting versus Relative Thinking. In AEA

Papers and Proceedings (Vol. 108, pp. 148-52).

Lepone, A. and Wong, J. B., 2018. The impact of mandatory IFRS reporting on institutional

trading costs: Evidence from Australia. Journal of Business Finance & Accounting. 45(7-

8). pp.797-817.

Shaukat, A. and Trojanowski, G., 2018. Board governance and corporate performance. Journal

of Business Finance & Accounting. 45(1-2). pp.184-208.

Shi, G., Sun, J. and Zhang, L., 2018. Product market competition and earnings management: A

firm‐level analysis. Journal of Business Finance & Accounting. 45(5-6). pp.604-624.

Torfs, W., 2018. EIF SME Access to Finance Index-June 2018 update (No. 2018/49). EIF

Working Paper.

ONLINE

Activity Based Budgeting. 2018. [Online]. Available through

<https://efinancemanagement.com/budgeting/activity-based-budgeting>.

Traditional budgeting. 2018. [Online]. Available through

<https://www.wallstreetmojo.com/traditional-budgeting/>.

9

Books and Journals

Amiram, D. and et.al., 2018. How are analysts’ forecasts affected by high uncertainty?. Journal

of Business Finance & Accounting. 45(3-4). pp.295-318.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting. 45(7-8).

pp.759-796.

Black, D. E., and et.al., 2018. Non‐GAAP reporting: Evidence from academia and current

practice. Journal of Business Finance & Accounting. 45(3-4). pp.259-294.

Block, J. H., and et.al., 2018. New players in entrepreneurial finance and why they are

there. Small Business Economics. 50(2). pp.239-250.

Gachoka, N. and et.al., 2018. The Moderating Effect of Organizational Characteristics on the

Relationship Between Budgeting Process and Performance of Churches in Kenya. Journal

of Finance and Investment Analysis. 7(2), pp.1-5.

Hirshman, S., Pope, D. and Song, J., 2018. Mental Budgeting versus Relative Thinking. In AEA

Papers and Proceedings (Vol. 108, pp. 148-52).

Lepone, A. and Wong, J. B., 2018. The impact of mandatory IFRS reporting on institutional

trading costs: Evidence from Australia. Journal of Business Finance & Accounting. 45(7-

8). pp.797-817.

Shaukat, A. and Trojanowski, G., 2018. Board governance and corporate performance. Journal

of Business Finance & Accounting. 45(1-2). pp.184-208.

Shi, G., Sun, J. and Zhang, L., 2018. Product market competition and earnings management: A

firm‐level analysis. Journal of Business Finance & Accounting. 45(5-6). pp.604-624.

Torfs, W., 2018. EIF SME Access to Finance Index-June 2018 update (No. 2018/49). EIF

Working Paper.

ONLINE

Activity Based Budgeting. 2018. [Online]. Available through

<https://efinancemanagement.com/budgeting/activity-based-budgeting>.

Traditional budgeting. 2018. [Online]. Available through

<https://www.wallstreetmojo.com/traditional-budgeting/>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.