381ACC - Traditional Budgeting: Relevance in Performance Management

VerifiedAdded on 2023/06/11

|12

|2627

|138

Essay

AI Summary

This essay critically examines the traditional budgeting technique as a planning and control tool, highlighting its perceived irrelevance in modern organizations due to factors like unstable customer demands, technological advancements, and environmental instability. It contrasts traditional budgeting with modern techniques like activity-based budgeting and value-based budgeting, arguing that the former's inflexibility, focus on cost reduction rather than value creation, and centralized process make it less effective in today's dynamic business environment. The essay also addresses the changing mindset of employees and the increasing importance of strategic alignment. While acknowledging the limitations, the conclusion suggests that traditional budgeting can still be valuable if organizations address its weaknesses and adapt it to their specific needs, considering their environmental and technological contexts.

Traditional Budgeting PAGE \* MERGEFORMAT 9

TRADITIONAL BUDGETARY CONTROL

TRADITIONAL BUDGETARY CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional Budgeting PAGE \* MERGEFORMAT 9

TRADITIONAL BUDGETARY CONTROL

Table of Contents

ABSTRACT....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Figure 1: The Traditional Budgeting model............................................................................4

WHY TRADITIONAL BUDGETING MAY NOT BE IRRELEVANT........................................5

Unstable customer demands and preference................................................................................5

Unstable Technology...................................................................................................................5

Figure 2: Budgeting Evolution Vs Degree of Impact .............................................................6

Unstable environment..................................................................................................................6

Hierarchical structure of organization.........................................................................................7

High competition.........................................................................................................................7

Figure 3: Comparing Traditional and Modern Budgeting Techniques...................................8

The mindset of today’s employees..............................................................................................8

Lack of value creation.................................................................................................................8

Centralization of the traditional budgeting process.....................................................................9

Companies’ Strategy....................................................................................................................9

CONCLUSION AND RECOMMENDATION..............................................................................9

References......................................................................................................................................11

TRADITIONAL BUDGETARY CONTROL

Table of Contents

ABSTRACT....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Figure 1: The Traditional Budgeting model............................................................................4

WHY TRADITIONAL BUDGETING MAY NOT BE IRRELEVANT........................................5

Unstable customer demands and preference................................................................................5

Unstable Technology...................................................................................................................5

Figure 2: Budgeting Evolution Vs Degree of Impact .............................................................6

Unstable environment..................................................................................................................6

Hierarchical structure of organization.........................................................................................7

High competition.........................................................................................................................7

Figure 3: Comparing Traditional and Modern Budgeting Techniques...................................8

The mindset of today’s employees..............................................................................................8

Lack of value creation.................................................................................................................8

Centralization of the traditional budgeting process.....................................................................9

Companies’ Strategy....................................................................................................................9

CONCLUSION AND RECOMMENDATION..............................................................................9

References......................................................................................................................................11

Traditional Budgeting PAGE \* MERGEFORMAT 9

ABSTRACT

Traditional budgeting technique has been used as a planning and control tool in most of

the organizations, however it has faced more criticism in the modern organization due to its

inefficiency to address the current organizational needs. Its opponents introduced other

techniques such as activity –based budgeting, value-based budgeting and profit planning

budgeting, which in turn replaced the use of traditional budgeting. Many writers have pointed out

that the technique cannot be applied in the unstable sectors since no comparisons can be made.

The fact that it is also inflexible and only focuses on resource allocation has rendered the

technique so dissatisfying that managers have been forced to adopt other techniques to help them

carry out planning. Today organizations are focusing on the customers’ needs and value creation

and not necessarily on cost reduction hence the need for a Sophisticated budgeting technique that

will enable organization to improve its performance.

INTRODUCTION

A budget is an approximation of the total income and expenses over a given period of

time. In Accounting, it is used as tool to help one in forecasting and analyzing business’s income

and expenditures (Zeller and Metzger, 2013). Traditional budgeting is the act of being able to

foresee your business’s income and revenue for the subsequent year based on the previous

budget. For a company to remain in business, it has to strictly monitor and maintain its budget so

that the expenses does not exceed the revenue and hence a good reputation to a company. By

comparing the actual previous expenditures with the actual current expenditures, one is able to

trace where there was unnecessary spending and reduce the expense incurred or look for a

supplier that will supply the same product/service at a relatively cheaper price (Andrews and

Hill, 2003). In addition, the budget can be used to obtain money from the financers. With the

ABSTRACT

Traditional budgeting technique has been used as a planning and control tool in most of

the organizations, however it has faced more criticism in the modern organization due to its

inefficiency to address the current organizational needs. Its opponents introduced other

techniques such as activity –based budgeting, value-based budgeting and profit planning

budgeting, which in turn replaced the use of traditional budgeting. Many writers have pointed out

that the technique cannot be applied in the unstable sectors since no comparisons can be made.

The fact that it is also inflexible and only focuses on resource allocation has rendered the

technique so dissatisfying that managers have been forced to adopt other techniques to help them

carry out planning. Today organizations are focusing on the customers’ needs and value creation

and not necessarily on cost reduction hence the need for a Sophisticated budgeting technique that

will enable organization to improve its performance.

INTRODUCTION

A budget is an approximation of the total income and expenses over a given period of

time. In Accounting, it is used as tool to help one in forecasting and analyzing business’s income

and expenditures (Zeller and Metzger, 2013). Traditional budgeting is the act of being able to

foresee your business’s income and revenue for the subsequent year based on the previous

budget. For a company to remain in business, it has to strictly monitor and maintain its budget so

that the expenses does not exceed the revenue and hence a good reputation to a company. By

comparing the actual previous expenditures with the actual current expenditures, one is able to

trace where there was unnecessary spending and reduce the expense incurred or look for a

supplier that will supply the same product/service at a relatively cheaper price (Andrews and

Hill, 2003). In addition, the budget can be used to obtain money from the financers. With the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Traditional Budgeting PAGE \* MERGEFORMAT 9

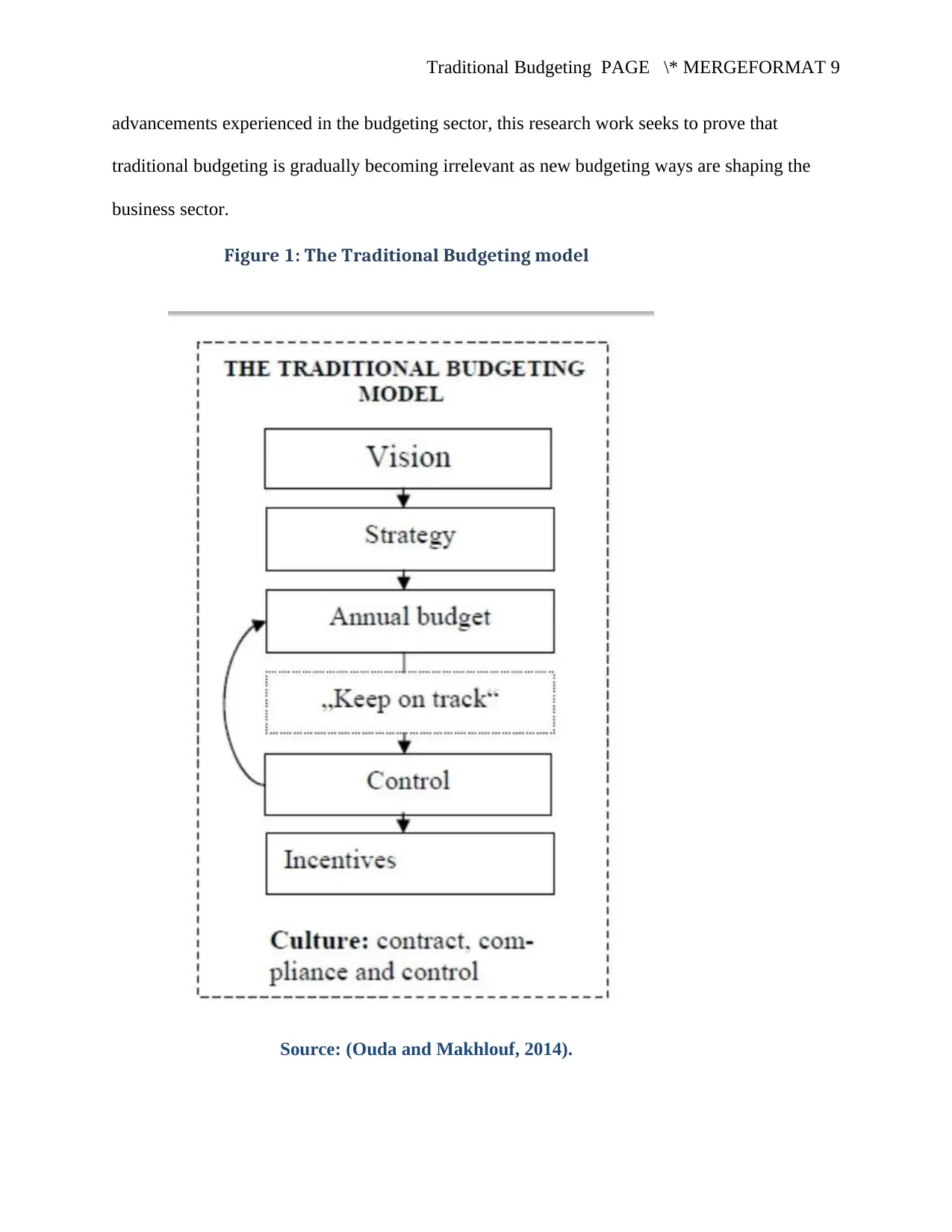

advancements experienced in the budgeting sector, this research work seeks to prove that

traditional budgeting is gradually becoming irrelevant as new budgeting ways are shaping the

business sector.

Figure 1: The Traditional Budgeting model

Source: (Ouda and Makhlouf, 2014).

advancements experienced in the budgeting sector, this research work seeks to prove that

traditional budgeting is gradually becoming irrelevant as new budgeting ways are shaping the

business sector.

Figure 1: The Traditional Budgeting model

Source: (Ouda and Makhlouf, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional Budgeting PAGE \* MERGEFORMAT 9

Companies are forced to adopt the technological and environmental changes in order to

thrive well in today’s economy. The directors are therefore left with no option but to ensure that

the management and the budget systems are reviewed from time to time so as to ensure that the

planning and control as a function of management is achieved. (Zimmerman and Yahya-Zadeh,

2011).

WHY TRADITIONAL BUDGETING MAY NOT BE IRRELEVANT

Even though budgeting is one of the most widely used management tool for planning and

controlling, however today, the traditional budgeting may not be as relevant as in the 20th century

due to the following;

Unstable customer demands and preference

Due to the unstable economy, customers cannot predict how much to stock for the future,

moreover, their preferences also change from time to time hence rendering traditional budgeting

un-useful (Popesko and Socova, 2016). For instance, a customer may prefer Infinix to Techno

today but because he/she did not get the utility expected from infinix, the customer may switch

to Techno or other brands (Ramey, 2013).

Unstable Technology

Technology is a body of knowledge devoted to creating tools, processing actions and the

extracting of materials (Ramey, 2013). Technology keeps on changing from time to time, and for

a company to survive today, it has to adopt with the changing technology so as to guarantee

quality products/services, maintain its customers and acquire new ones. The technology that was

used in the previous year’s budget may not be necessarily the same technology that would be

Companies are forced to adopt the technological and environmental changes in order to

thrive well in today’s economy. The directors are therefore left with no option but to ensure that

the management and the budget systems are reviewed from time to time so as to ensure that the

planning and control as a function of management is achieved. (Zimmerman and Yahya-Zadeh,

2011).

WHY TRADITIONAL BUDGETING MAY NOT BE IRRELEVANT

Even though budgeting is one of the most widely used management tool for planning and

controlling, however today, the traditional budgeting may not be as relevant as in the 20th century

due to the following;

Unstable customer demands and preference

Due to the unstable economy, customers cannot predict how much to stock for the future,

moreover, their preferences also change from time to time hence rendering traditional budgeting

un-useful (Popesko and Socova, 2016). For instance, a customer may prefer Infinix to Techno

today but because he/she did not get the utility expected from infinix, the customer may switch

to Techno or other brands (Ramey, 2013).

Unstable Technology

Technology is a body of knowledge devoted to creating tools, processing actions and the

extracting of materials (Ramey, 2013). Technology keeps on changing from time to time, and for

a company to survive today, it has to adopt with the changing technology so as to guarantee

quality products/services, maintain its customers and acquire new ones. The technology that was

used in the previous year’s budget may not be necessarily the same technology that would be

Traditional Budgeting PAGE \* MERGEFORMAT 9

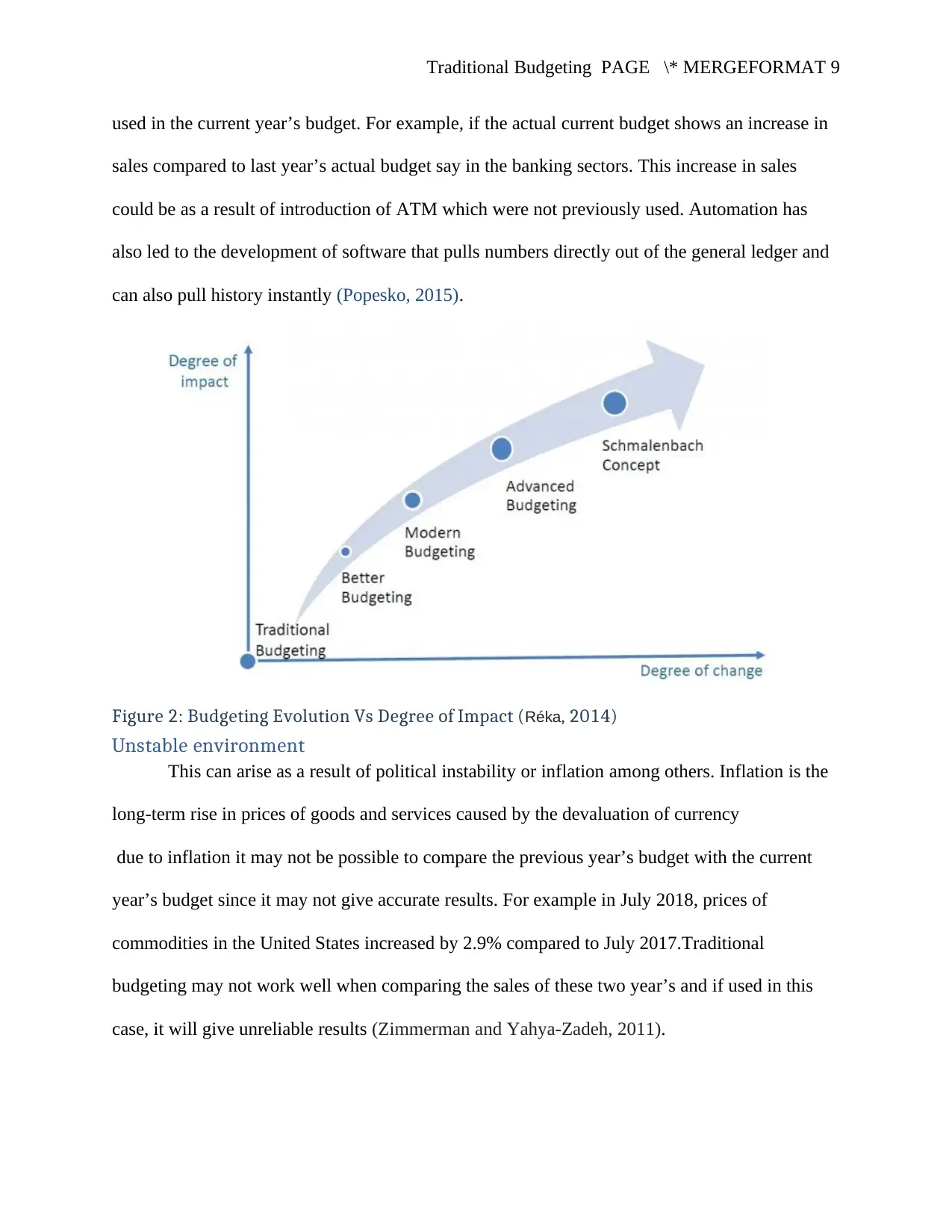

used in the current year’s budget. For example, if the actual current budget shows an increase in

sales compared to last year’s actual budget say in the banking sectors. This increase in sales

could be as a result of introduction of ATM which were not previously used. Automation has

also led to the development of software that pulls numbers directly out of the general ledger and

can also pull history instantly (Popesko, 2015).

Figure 2: Budgeting Evolution Vs Degree of Impact (Réka, 2014)

Unstable environment

This can arise as a result of political instability or inflation among others. Inflation is the

long-term rise in prices of goods and services caused by the devaluation of currency

due to inflation it may not be possible to compare the previous year’s budget with the current

year’s budget since it may not give accurate results. For example in July 2018, prices of

commodities in the United States increased by 2.9% compared to July 2017.Traditional

budgeting may not work well when comparing the sales of these two year’s and if used in this

case, it will give unreliable results (Zimmerman and Yahya-Zadeh, 2011).

used in the current year’s budget. For example, if the actual current budget shows an increase in

sales compared to last year’s actual budget say in the banking sectors. This increase in sales

could be as a result of introduction of ATM which were not previously used. Automation has

also led to the development of software that pulls numbers directly out of the general ledger and

can also pull history instantly (Popesko, 2015).

Figure 2: Budgeting Evolution Vs Degree of Impact (Réka, 2014)

Unstable environment

This can arise as a result of political instability or inflation among others. Inflation is the

long-term rise in prices of goods and services caused by the devaluation of currency

due to inflation it may not be possible to compare the previous year’s budget with the current

year’s budget since it may not give accurate results. For example in July 2018, prices of

commodities in the United States increased by 2.9% compared to July 2017.Traditional

budgeting may not work well when comparing the sales of these two year’s and if used in this

case, it will give unreliable results (Zimmerman and Yahya-Zadeh, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Traditional Budgeting PAGE \* MERGEFORMAT 9

Similarly, when a country is politically unstable, this might affects its economic

performance thus making comparison not practical. For instance, Kenya is known for political

violence especially during elections. During this time looting takes place and so forth as a result

this will impact the material budget. Kenya therefore does not realize the importance of the

budget put in place (Njogu, 2009).

Hierarchical structure of organization

Most companies today have a narrow chain of command hence faster decision making.

Such organizations are highly effective, can work as a team and pass information faster to the top

down mentalities and hence cannot adopt the traditional budgeting system (Popesko, 2015).

High competition

Companies are competing against one another in order to remain at the top. Traditional

budgeting being inflexible cannot cope up with this competition because for an idea (that

requires resources) to be implemented it has to take a long period of time before it is approved

just because it will interfere with the budget and as a result so many idea that would have

benefited the company are left unimplemented (Libby and Lindsay, 2010). As a result today’s

companies are doing away with the traditional budgeting and adopting other methods of

continuous planning. Due to competition, most companies are forced to migrate from the

traditional budgeting to other techniques such as Activity-Based budgeting system. For example,

most listed companies in the Netherland have adopted the Activity based costing technique as a

method of planning (Libby and Lindsay, 2010).

Similarly, when a country is politically unstable, this might affects its economic

performance thus making comparison not practical. For instance, Kenya is known for political

violence especially during elections. During this time looting takes place and so forth as a result

this will impact the material budget. Kenya therefore does not realize the importance of the

budget put in place (Njogu, 2009).

Hierarchical structure of organization

Most companies today have a narrow chain of command hence faster decision making.

Such organizations are highly effective, can work as a team and pass information faster to the top

down mentalities and hence cannot adopt the traditional budgeting system (Popesko, 2015).

High competition

Companies are competing against one another in order to remain at the top. Traditional

budgeting being inflexible cannot cope up with this competition because for an idea (that

requires resources) to be implemented it has to take a long period of time before it is approved

just because it will interfere with the budget and as a result so many idea that would have

benefited the company are left unimplemented (Libby and Lindsay, 2010). As a result today’s

companies are doing away with the traditional budgeting and adopting other methods of

continuous planning. Due to competition, most companies are forced to migrate from the

traditional budgeting to other techniques such as Activity-Based budgeting system. For example,

most listed companies in the Netherland have adopted the Activity based costing technique as a

method of planning (Libby and Lindsay, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional Budgeting PAGE \* MERGEFORMAT 9

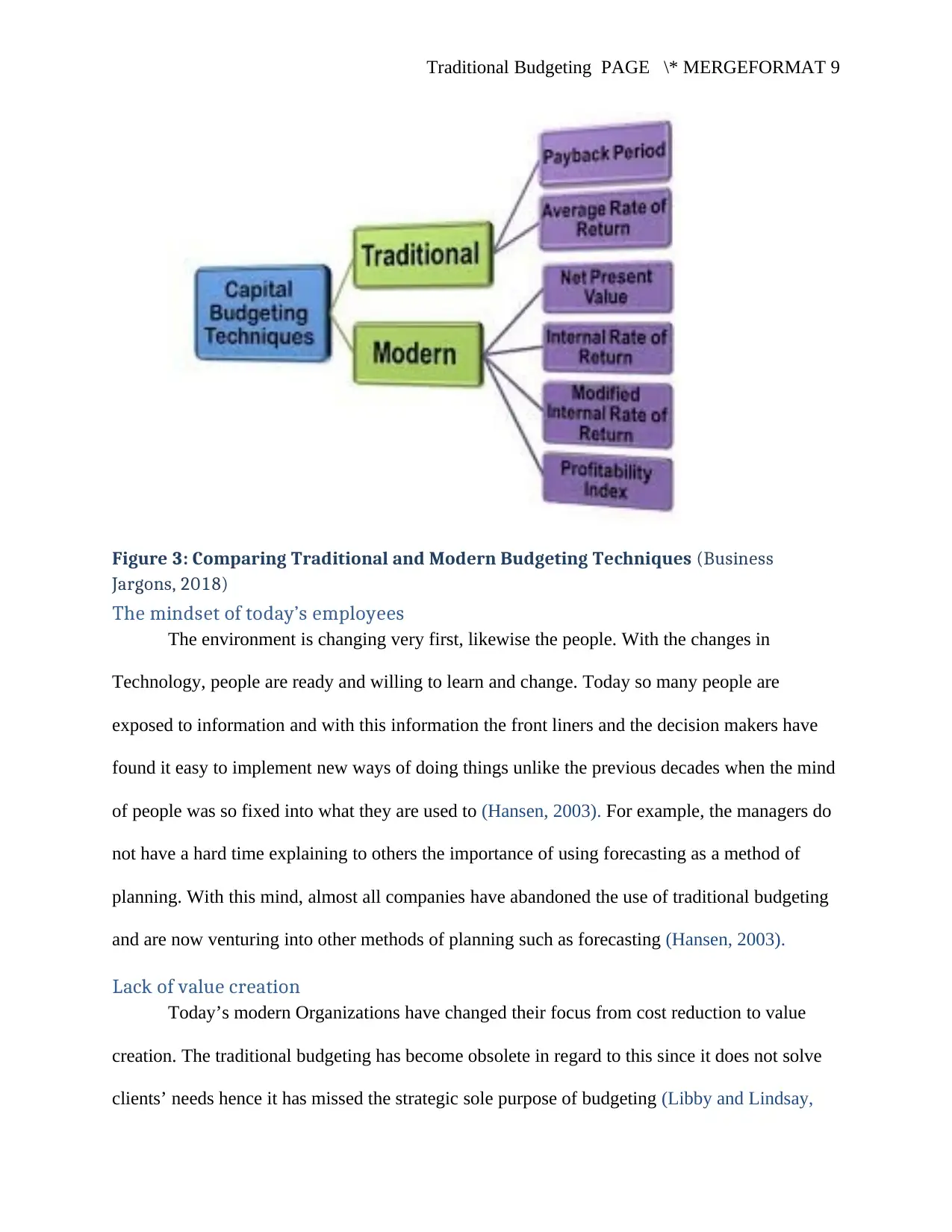

Figure 3: Comparing Traditional and Modern Budgeting Techniques (Business

Jargons, 2018)

The mindset of today’s employees

The environment is changing very first, likewise the people. With the changes in

Technology, people are ready and willing to learn and change. Today so many people are

exposed to information and with this information the front liners and the decision makers have

found it easy to implement new ways of doing things unlike the previous decades when the mind

of people was so fixed into what they are used to (Hansen, 2003). For example, the managers do

not have a hard time explaining to others the importance of using forecasting as a method of

planning. With this mind, almost all companies have abandoned the use of traditional budgeting

and are now venturing into other methods of planning such as forecasting (Hansen, 2003).

Lack of value creation

Today’s modern Organizations have changed their focus from cost reduction to value

creation. The traditional budgeting has become obsolete in regard to this since it does not solve

clients’ needs hence it has missed the strategic sole purpose of budgeting (Libby and Lindsay,

Figure 3: Comparing Traditional and Modern Budgeting Techniques (Business

Jargons, 2018)

The mindset of today’s employees

The environment is changing very first, likewise the people. With the changes in

Technology, people are ready and willing to learn and change. Today so many people are

exposed to information and with this information the front liners and the decision makers have

found it easy to implement new ways of doing things unlike the previous decades when the mind

of people was so fixed into what they are used to (Hansen, 2003). For example, the managers do

not have a hard time explaining to others the importance of using forecasting as a method of

planning. With this mind, almost all companies have abandoned the use of traditional budgeting

and are now venturing into other methods of planning such as forecasting (Hansen, 2003).

Lack of value creation

Today’s modern Organizations have changed their focus from cost reduction to value

creation. The traditional budgeting has become obsolete in regard to this since it does not solve

clients’ needs hence it has missed the strategic sole purpose of budgeting (Libby and Lindsay,

Traditional Budgeting PAGE \* MERGEFORMAT 9

2007) (Neely, 2003). For examples in the automobile industries, customers are looking for a car

that is efficient in terms of fuel saving and also convenient. On the other hand, managers will try

to cut down the budget so that they can satisfy their self-interest thus compromising on quality.

Managers can also manipulate the actual projection so that they look more appealing yet this

may not have a positive impact in the long-run (Libby and Lindsay, 2007).

Centralization of the traditional budgeting process

The today’s markets are so complex and so requires a budgeting technique that is

collaborative so as to meet the objectives of its customers in various markets and companies. The

traditional budget however does not provide opportunities for the different business functions to

work together in order to reflect the corporate overall strategy and position (Daum, 2002). Since

the task of centralizing the budgeting process is normally given to a person in charge of Finance

in the finance department, the person in charge may produce results that do not reflect the

companies’ true image. That is to say that the person may project that the company is

overspending when it is not and vice versa (De Waal, 2005).

Companies’ Strategy

Today most companies work on a set strategy in order to achieve their vision. According

to Nolan (2005), it is argued that the top management lay out the strategy which is translated into

numbers and carried out by different employees of the organization and hence the blame on the

budget that it is not in line with the company strategy.

CONCLUSION AND RECOMMENDATION

In as much as traditional budgeting is irrelevant but still it can be of use to most

organization if they feel the need to. This is because organizations have got their visions and

mission statements and if a company does not know its previous expenditures, then it means that

2007) (Neely, 2003). For examples in the automobile industries, customers are looking for a car

that is efficient in terms of fuel saving and also convenient. On the other hand, managers will try

to cut down the budget so that they can satisfy their self-interest thus compromising on quality.

Managers can also manipulate the actual projection so that they look more appealing yet this

may not have a positive impact in the long-run (Libby and Lindsay, 2007).

Centralization of the traditional budgeting process

The today’s markets are so complex and so requires a budgeting technique that is

collaborative so as to meet the objectives of its customers in various markets and companies. The

traditional budget however does not provide opportunities for the different business functions to

work together in order to reflect the corporate overall strategy and position (Daum, 2002). Since

the task of centralizing the budgeting process is normally given to a person in charge of Finance

in the finance department, the person in charge may produce results that do not reflect the

companies’ true image. That is to say that the person may project that the company is

overspending when it is not and vice versa (De Waal, 2005).

Companies’ Strategy

Today most companies work on a set strategy in order to achieve their vision. According

to Nolan (2005), it is argued that the top management lay out the strategy which is translated into

numbers and carried out by different employees of the organization and hence the blame on the

budget that it is not in line with the company strategy.

CONCLUSION AND RECOMMENDATION

In as much as traditional budgeting is irrelevant but still it can be of use to most

organization if they feel the need to. This is because organizations have got their visions and

mission statements and if a company does not know its previous expenditures, then it means that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Traditional Budgeting PAGE \* MERGEFORMAT 9

it would not be able to predict future expenditures. This may result in overspending or under-

spending hence interfering with the normal running of the organization’s activities.

Organizations need to work on the weaknesses of the traditional budgeting and come up

with more advanced techniques to help solve organization’s financial problems that arise from

inefficient budgeting practices. To achieve this organization need not to completely abandon the

traditional budgeting system because an organization is propelled forward when it can monitor

its past and present financial requirements. The bottom line is, companies should know their

environmental and technological needs, its culture and weaknesses before amending their

traditional budgeting practices.

it would not be able to predict future expenditures. This may result in overspending or under-

spending hence interfering with the normal running of the organization’s activities.

Organizations need to work on the weaknesses of the traditional budgeting and come up

with more advanced techniques to help solve organization’s financial problems that arise from

inefficient budgeting practices. To achieve this organization need not to completely abandon the

traditional budgeting system because an organization is propelled forward when it can monitor

its past and present financial requirements. The bottom line is, companies should know their

environmental and technological needs, its culture and weaknesses before amending their

traditional budgeting practices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional Budgeting PAGE \* MERGEFORMAT 9

References

Andrews, M. and Hill, H., 2003. The Impact of Traditional Budgeting Systems on the

Effectiveness of Performance‐Based Budgeting: A Different Viewpoint on Recent

Findings. International Journal of Public Administration, 26(2), pp.135-155.

Aviationweek.com. (2018). [online] Available at:

http://aviationweek.com/site-files/aviationweek.com/files/archive/cmsfiles/media/pdf/ad_pdf/

2011/11/11/avd_11_11_2011_cht1.pdf [Accessed 24 Aug. 2018].

Business Jargons. (2018). What are Capital Budgeting Techniques? definition and meaning -

Business Jargons. [online] Available at: https://businessjargons.com/capital-budgeting-

techniques.html [Accessed 25 Aug. 2018].

Daum, J.H., 2002. Beyond budgeting: a model for performance management and controlling in

the 21st century. Controlling & Finance, 5, pp.33-34.

De Waal, A.A., 2005. Is your organisation ready for beyond budgeting?. Measuring business

excellence, 9(2), pp.56-67.

Hansen, S.C., Otley, D.T. and Van der Stede, W.A., 2003. Practice developments in budgeting:

an overview and research perspective. Journal of management accounting research, 15(1),

pp.95-116.

Libby, T. and Lindsay, R.M., 2007. Beyond budgeting or better budgeting?. Strategic

Finance, 89(2), p.46.

Libby, T. and Lindsay, R.M., 2010. Beyond budgeting or budgeting reconsidered? A survey of

North-American budgeting practice. Management accounting research, 21(1), pp.56-75.

Neely, A., Bourne, M. and Adams, C., 2003. Better budgeting or beyond budgeting?. Measuring

business excellence, 7(3), pp.22-28.

References

Andrews, M. and Hill, H., 2003. The Impact of Traditional Budgeting Systems on the

Effectiveness of Performance‐Based Budgeting: A Different Viewpoint on Recent

Findings. International Journal of Public Administration, 26(2), pp.135-155.

Aviationweek.com. (2018). [online] Available at:

http://aviationweek.com/site-files/aviationweek.com/files/archive/cmsfiles/media/pdf/ad_pdf/

2011/11/11/avd_11_11_2011_cht1.pdf [Accessed 24 Aug. 2018].

Business Jargons. (2018). What are Capital Budgeting Techniques? definition and meaning -

Business Jargons. [online] Available at: https://businessjargons.com/capital-budgeting-

techniques.html [Accessed 25 Aug. 2018].

Daum, J.H., 2002. Beyond budgeting: a model for performance management and controlling in

the 21st century. Controlling & Finance, 5, pp.33-34.

De Waal, A.A., 2005. Is your organisation ready for beyond budgeting?. Measuring business

excellence, 9(2), pp.56-67.

Hansen, S.C., Otley, D.T. and Van der Stede, W.A., 2003. Practice developments in budgeting:

an overview and research perspective. Journal of management accounting research, 15(1),

pp.95-116.

Libby, T. and Lindsay, R.M., 2007. Beyond budgeting or better budgeting?. Strategic

Finance, 89(2), p.46.

Libby, T. and Lindsay, R.M., 2010. Beyond budgeting or budgeting reconsidered? A survey of

North-American budgeting practice. Management accounting research, 21(1), pp.56-75.

Neely, A., Bourne, M. and Adams, C., 2003. Better budgeting or beyond budgeting?. Measuring

business excellence, 7(3), pp.22-28.

Traditional Budgeting PAGE \* MERGEFORMAT 9

Njogu, K. ed., 2009. Healing the Wound. Personal Narratives about the 2007 Post-Election

Violence in Kenya: Personal Narratives about the 2007 Post-election Violence in Kenya. African

Books Collective.

Nolan, G.J., 2005. The end of traditional budgeting. Journal of Performance Management, 18(1),

p.27.

Ouda, H. and Makhlouf, S., 2014. Beyond Budgeting: is it a Substitute or Complimentary to

Traditional Budgeting? An Empirical Evidence from Telecommunications Companies in

Egypt. British Accounting & Finance Association (BAFA), 14(16), p.04.

Popesko, B. and Socova, V., 2016. Current trends in budgeting and planning: Czech survey

initial results. International Advances in Economic Research, 22(1), p.99.

Popesko, B., Novák, P., Papadaki, S. and Hrabec, D., 2015. ARE THE TRADITIONAL

BUDGETS STILL PREVALENT: THE SURVEY OF THE CZECH FIRMS BUDGETING

PRACTICES. Transformations in Business & Economics, 14.

Ramey, Karehka, 2013. "What Is Technology - Meaning of Technology and Its Use." Use of

Technology. Last modified December 12, 2013. https://www.useoftechnology.com/what-is-

technology/.

Réka, C.I., Ştefan, P. and Daniel, C.V., 2014. TRADITIONAL BUDGETING VERSUS

BEYOND BUDGETING: A LITERATURE REVIEW. Annals of the University of Oradea,

Economic Science Series, 23(1).

Zeller, T.L. and Metzger, L.M., 2013. Good Bye Traditional Budgeting, Hello Rolling Forecast:

Has the Time Come?. American Journal of Business Education, 6(3), pp.299-310.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

Njogu, K. ed., 2009. Healing the Wound. Personal Narratives about the 2007 Post-Election

Violence in Kenya: Personal Narratives about the 2007 Post-election Violence in Kenya. African

Books Collective.

Nolan, G.J., 2005. The end of traditional budgeting. Journal of Performance Management, 18(1),

p.27.

Ouda, H. and Makhlouf, S., 2014. Beyond Budgeting: is it a Substitute or Complimentary to

Traditional Budgeting? An Empirical Evidence from Telecommunications Companies in

Egypt. British Accounting & Finance Association (BAFA), 14(16), p.04.

Popesko, B. and Socova, V., 2016. Current trends in budgeting and planning: Czech survey

initial results. International Advances in Economic Research, 22(1), p.99.

Popesko, B., Novák, P., Papadaki, S. and Hrabec, D., 2015. ARE THE TRADITIONAL

BUDGETS STILL PREVALENT: THE SURVEY OF THE CZECH FIRMS BUDGETING

PRACTICES. Transformations in Business & Economics, 14.

Ramey, Karehka, 2013. "What Is Technology - Meaning of Technology and Its Use." Use of

Technology. Last modified December 12, 2013. https://www.useoftechnology.com/what-is-

technology/.

Réka, C.I., Ştefan, P. and Daniel, C.V., 2014. TRADITIONAL BUDGETING VERSUS

BEYOND BUDGETING: A LITERATURE REVIEW. Annals of the University of Oradea,

Economic Science Series, 23(1).

Zeller, T.L. and Metzger, L.M., 2013. Good Bye Traditional Budgeting, Hello Rolling Forecast:

Has the Time Come?. American Journal of Business Education, 6(3), pp.299-310.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.