Evaluating the Impact of Traditional Budgeting on XYZ Ltd

VerifiedAdded on 2023/06/12

|44

|5575

|458

Report

AI Summary

This report investigates the impact of traditional budgetary control on the profitability of XYZ Ltd, employing a qualitative research methodology with an inductive approach. Data was collected through questionnaires distributed to key personnel, including the CFO, production and sales managers, and the CEO, using simple random sampling. The conceptual framework identifies factors like lack of planning, coordination, and monitoring as key influences on budgetary control and organizational effectiveness. Thematic analysis was used to analyze the data, revealing that while there is awareness of budgeting concepts, traditional budgeting methods are perceived to have limitations affecting profitability. The report also addresses ethical considerations, reliability, validity, and research limitations, ultimately providing insights into the challenges and benefits of traditional budgeting within the context of XYZ Ltd.

The Impact of Traditional Budgetary

Control On the Profitability of XYZ Ltd

Control On the Profitability of XYZ Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

CHAPTER 3- RESEARCH METHODOLOGY.............................................................................3

Introduction.................................................................................................................................3

Research Strategy........................................................................................................................3

Research approach & philosophy................................................................................................3

Sampling Procedure....................................................................................................................4

Conceptual Framework...............................................................................................................4

Qualitative Research – Factor Definition....................................................................................5

Data and Data collection.............................................................................................................5

CHAPTER 4: DATA ANALYSIS..................................................................................................6

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS...................................................23

REFERENCES..............................................................................................................................28

APPENDIX....................................................................................................................................29

CHAPTER 3- RESEARCH METHODOLOGY.............................................................................3

Introduction.................................................................................................................................3

Research Strategy........................................................................................................................3

Research approach & philosophy................................................................................................3

Sampling Procedure....................................................................................................................4

Conceptual Framework...............................................................................................................4

Qualitative Research – Factor Definition....................................................................................5

Data and Data collection.............................................................................................................5

CHAPTER 4: DATA ANALYSIS..................................................................................................6

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS...................................................23

REFERENCES..............................................................................................................................28

APPENDIX....................................................................................................................................29

CHAPTER 3- RESEARCH METHODOLOGY

Introduction

Research methodology is related with having the specific procedure that is taken into consideration for identifying, selecting.

Processing and evaluating information about a particular subject matter. The current study will involve research strategy, sampling

procedure, conceptual framework, data collection, evaluation technique, etc. so that significant understanding can be derived.

Research Strategy

There are basically two types of the research which can be taken into considerations by the organization in respect to gain the

proper understanding for accomplishing the objectives which involves qualitative and quantitative. The qualitative type of study is

widely taken into process for collecting the theoretical study. Quantitative type of research is used to get the numerical & fact based

data. For the current study regarding impact of traditional control on profitability is theoretical concept so that significant ability gain

relevant & reliable information can be derived. This has permitted the scholar to get the understanding about theories and framework

in turn depth knowledge to meet highlighted objectives can become possible. Qualitative research type is highly taken into procedure

by the businesses for gaining the proper understanding for ensuring that reliable report can be formulated. Ascertaining impact of

budgetary control over the revenue system and mitigation strategy to overcome the challenge of significant negative of variation

between actual performance & budgetary planning can be exerted in effective manner. Collection of non-numerical data for this

purpose can allow to get the accurate and fair understanding about the research in assessing accurate impact on profitability due to

traditional budgetary control can be derived.

Research approach & philosophy

Inductive and deductive are the two research approaches which can be taken into process for understanding the process taken

into consideration for carrying out the research. For recent study the focus has been provided on having utilization of inductive

approach so that appropriate conducting of research can be exerted. There are two form of philosophies such as Interpretivism and

Introduction

Research methodology is related with having the specific procedure that is taken into consideration for identifying, selecting.

Processing and evaluating information about a particular subject matter. The current study will involve research strategy, sampling

procedure, conceptual framework, data collection, evaluation technique, etc. so that significant understanding can be derived.

Research Strategy

There are basically two types of the research which can be taken into considerations by the organization in respect to gain the

proper understanding for accomplishing the objectives which involves qualitative and quantitative. The qualitative type of study is

widely taken into process for collecting the theoretical study. Quantitative type of research is used to get the numerical & fact based

data. For the current study regarding impact of traditional control on profitability is theoretical concept so that significant ability gain

relevant & reliable information can be derived. This has permitted the scholar to get the understanding about theories and framework

in turn depth knowledge to meet highlighted objectives can become possible. Qualitative research type is highly taken into procedure

by the businesses for gaining the proper understanding for ensuring that reliable report can be formulated. Ascertaining impact of

budgetary control over the revenue system and mitigation strategy to overcome the challenge of significant negative of variation

between actual performance & budgetary planning can be exerted in effective manner. Collection of non-numerical data for this

purpose can allow to get the accurate and fair understanding about the research in assessing accurate impact on profitability due to

traditional budgetary control can be derived.

Research approach & philosophy

Inductive and deductive are the two research approaches which can be taken into process for understanding the process taken

into consideration for carrying out the research. For recent study the focus has been provided on having utilization of inductive

approach so that appropriate conducting of research can be exerted. There are two form of philosophies such as Interpretivism and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

positivism which aids in meeting objectives in accurate manner. Interpretivism is suitable in order to asses the impact of traditional

budgetary control on profitability of specified organization.

Sampling Procedure

Sampling is basically selection of group from the total population in order to collect the accurate and reliable data from

suitable people. There are different kinds of the technique which can be taken into procedure for collecting data from the sampling

size that involve probability and non probabilistic. In order to collect the data from the selected groups such as CFO, production, sales,

procedure manager and CEO. These have been selected by simple random sampling technique which is part of probability precise

views and opinion regarding the impact of traditional budgeting on profitability can be ascertained. This is helpful in gaining the non

bias information in respect to get the significant ability to evaluate impact of traditional budgetary control on profitability of

mentioned enterprise. In order to conduct the research in highly effective manner utilization of simple random sampling aids scholar to

ensure that bias based behavior can be avoided. The main reason behind such benefit is that there is involvement of selecting

participants on random basis via eliminating aspect of giving preference to anyone. This contributes in achieving relevant information

about the prevailing circumstance so that meeting objectives and assessing answer to research questions can be done.

Conceptual Framework

Has impact on

organizational

efficiency &

effectiveness

Traditional budgetary control

Have

influence on

profitability Change

Factors

Lack of Planning

Lack of co–

ordination and

management

Monitoring the

Financial

condition

budgetary control on profitability of specified organization.

Sampling Procedure

Sampling is basically selection of group from the total population in order to collect the accurate and reliable data from

suitable people. There are different kinds of the technique which can be taken into procedure for collecting data from the sampling

size that involve probability and non probabilistic. In order to collect the data from the selected groups such as CFO, production, sales,

procedure manager and CEO. These have been selected by simple random sampling technique which is part of probability precise

views and opinion regarding the impact of traditional budgeting on profitability can be ascertained. This is helpful in gaining the non

bias information in respect to get the significant ability to evaluate impact of traditional budgetary control on profitability of

mentioned enterprise. In order to conduct the research in highly effective manner utilization of simple random sampling aids scholar to

ensure that bias based behavior can be avoided. The main reason behind such benefit is that there is involvement of selecting

participants on random basis via eliminating aspect of giving preference to anyone. This contributes in achieving relevant information

about the prevailing circumstance so that meeting objectives and assessing answer to research questions can be done.

Conceptual Framework

Has impact on

organizational

efficiency &

effectiveness

Traditional budgetary control

Have

influence on

profitability Change

Factors

Lack of Planning

Lack of co–

ordination and

management

Monitoring the

Financial

condition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgetary control (dependent variable)

On the basis of the above prepared conceptual framework it can be identified that these are the main causes which is leading

to impact the budgetary control. This is affecting the profitability of XYZ in adverse manner. It is important in gaining significant

knowledge about the aspects regarding which are the root causes that is impacting traditional budgetary control and affecting the

profitability of enterprise . In order to get accurate ability to influence profitability in positive pattern it is important to give focus on

these aspects so that higher ability to get positive outcomes can become possible. The reason behind considering these as lacking

aspect as ineffective planning coordination & management and irrelevant level of monitoring hampers functioning of enterprise.

Qualitative Research – Factor Definition

Factors Phenomenon

Lack of Planning This can be measured by ability of firm to

conduct operational practices

Lack of co–ordination and management level of outcome derived on profitability

Impacts

On the basis of the above prepared conceptual framework it can be identified that these are the main causes which is leading

to impact the budgetary control. This is affecting the profitability of XYZ in adverse manner. It is important in gaining significant

knowledge about the aspects regarding which are the root causes that is impacting traditional budgetary control and affecting the

profitability of enterprise . In order to get accurate ability to influence profitability in positive pattern it is important to give focus on

these aspects so that higher ability to get positive outcomes can become possible. The reason behind considering these as lacking

aspect as ineffective planning coordination & management and irrelevant level of monitoring hampers functioning of enterprise.

Qualitative Research – Factor Definition

Factors Phenomenon

Lack of Planning This can be measured by ability of firm to

conduct operational practices

Lack of co–ordination and management level of outcome derived on profitability

Impacts

Monitoring the budget Improvement actions conducted.

Data and Data collection

Data collection is gathering the information for attaining the research questions in effective manner in turn reliable

formulation of study can become possible. There are two ways in which data is collected such as primary and secondary that permit

receiving significant level of data in turn attaining objectives can become possible. The primary method is related with gathering

information particular for the specific topic which has not been utilized before. This can be done via using methods such as

questionnaire, interview, observation n and focus group. For the present research report, researcher has paid attention on spreading

questionnaire to the selected sampling size in respect to gain insights about their views, opinion and experience regarding impact of

traditional budgetary control on profitability of firm. Secondary research is associated with using articles, journals and books in turn

ability to support the collected data can become possible. These both specified method has been helpful in meeting the objectives of

achieving relevant and reliable information to conduct study.

Data analysing methods and techniques

For the purpose of analyzing the data, there are two ways of the techniques which is widely taken into procedure by the

scholar that comprises thematic sampling technique and SPSS. For the qualitative study the thematic perception test technique is

suitable which is related with referring to the response gathered through survey, graphical presentation so that findings can be

supported to LR. On the other side, SPSS is used for having descriptive statistics, regression, correlation, etc. in addition to this, it

can be interpreted that current study has taken thematic analysis into consideration for achieving appropriate information in tun better

reliable formulation of report has become possible.

Ethical consideration

Data and Data collection

Data collection is gathering the information for attaining the research questions in effective manner in turn reliable

formulation of study can become possible. There are two ways in which data is collected such as primary and secondary that permit

receiving significant level of data in turn attaining objectives can become possible. The primary method is related with gathering

information particular for the specific topic which has not been utilized before. This can be done via using methods such as

questionnaire, interview, observation n and focus group. For the present research report, researcher has paid attention on spreading

questionnaire to the selected sampling size in respect to gain insights about their views, opinion and experience regarding impact of

traditional budgetary control on profitability of firm. Secondary research is associated with using articles, journals and books in turn

ability to support the collected data can become possible. These both specified method has been helpful in meeting the objectives of

achieving relevant and reliable information to conduct study.

Data analysing methods and techniques

For the purpose of analyzing the data, there are two ways of the techniques which is widely taken into procedure by the

scholar that comprises thematic sampling technique and SPSS. For the qualitative study the thematic perception test technique is

suitable which is related with referring to the response gathered through survey, graphical presentation so that findings can be

supported to LR. On the other side, SPSS is used for having descriptive statistics, regression, correlation, etc. in addition to this, it

can be interpreted that current study has taken thematic analysis into consideration for achieving appropriate information in tun better

reliable formulation of report has become possible.

Ethical consideration

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are various ethical requirements which are required to be taken into consideration by the researcher in respect to give

emphasis on developing fair research. For this purpose the consent form has been signed by the targeted audience. Data has not been

copied and maintained privacy details of targeted audience. This has lead to conduct fair & reliable study to meet objectives.

Reliability and validity

For maintaining the reliability & validity of the research scholar has given emphasis on using the latest sources, no alteration in

data gathered, and copy right sources utilization. This is helpful in making the significant report in turn achieving appropriate

knowledge to meet aim of study has become possible

Research limitation

The research limitations comprise time, access to resources and availability of limited monetary source. This has been highly

considered by scholar for meeting accurate knowledge via ensuring optimum utilization of resources o that better outcomes can be

offered.

emphasis on developing fair research. For this purpose the consent form has been signed by the targeted audience. Data has not been

copied and maintained privacy details of targeted audience. This has lead to conduct fair & reliable study to meet objectives.

Reliability and validity

For maintaining the reliability & validity of the research scholar has given emphasis on using the latest sources, no alteration in

data gathered, and copy right sources utilization. This is helpful in making the significant report in turn achieving appropriate

knowledge to meet aim of study has become possible

Research limitation

The research limitations comprise time, access to resources and availability of limited monetary source. This has been highly

considered by scholar for meeting accurate knowledge via ensuring optimum utilization of resources o that better outcomes can be

offered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

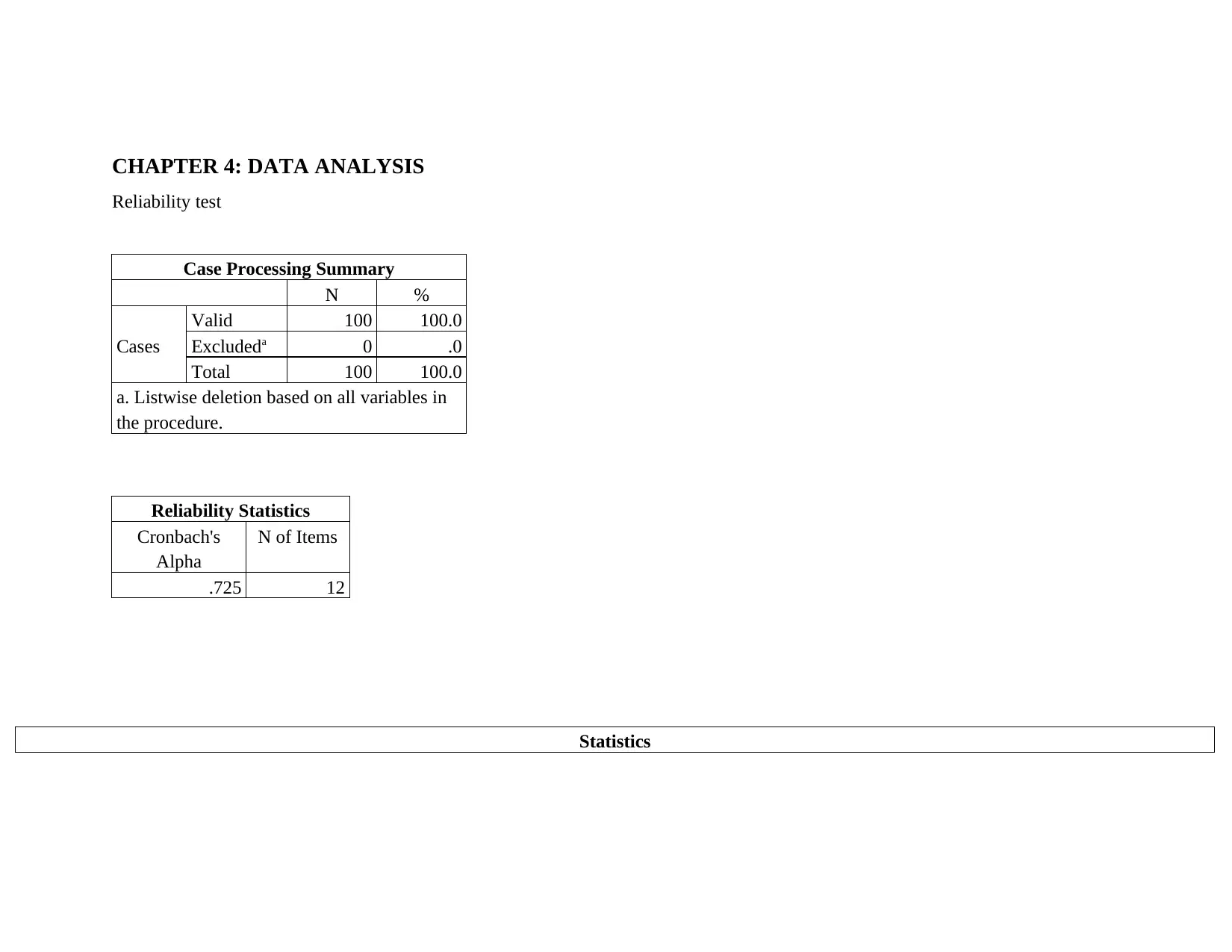

CHAPTER 4: DATA ANALYSIS

Reliability test

Case Processing Summary

N %

Cases

Valid 100 100.0

Excludeda 0 .0

Total 100 100.0

a. Listwise deletion based on all variables in

the procedure.

Reliability Statistics

Cronbach's

Alpha

N of Items

.725 12

Statistics

Reliability test

Case Processing Summary

N %

Cases

Valid 100 100.0

Excludeda 0 .0

Total 100 100.0

a. Listwise deletion based on all variables in

the procedure.

Reliability Statistics

Cronbach's

Alpha

N of Items

.725 12

Statistics

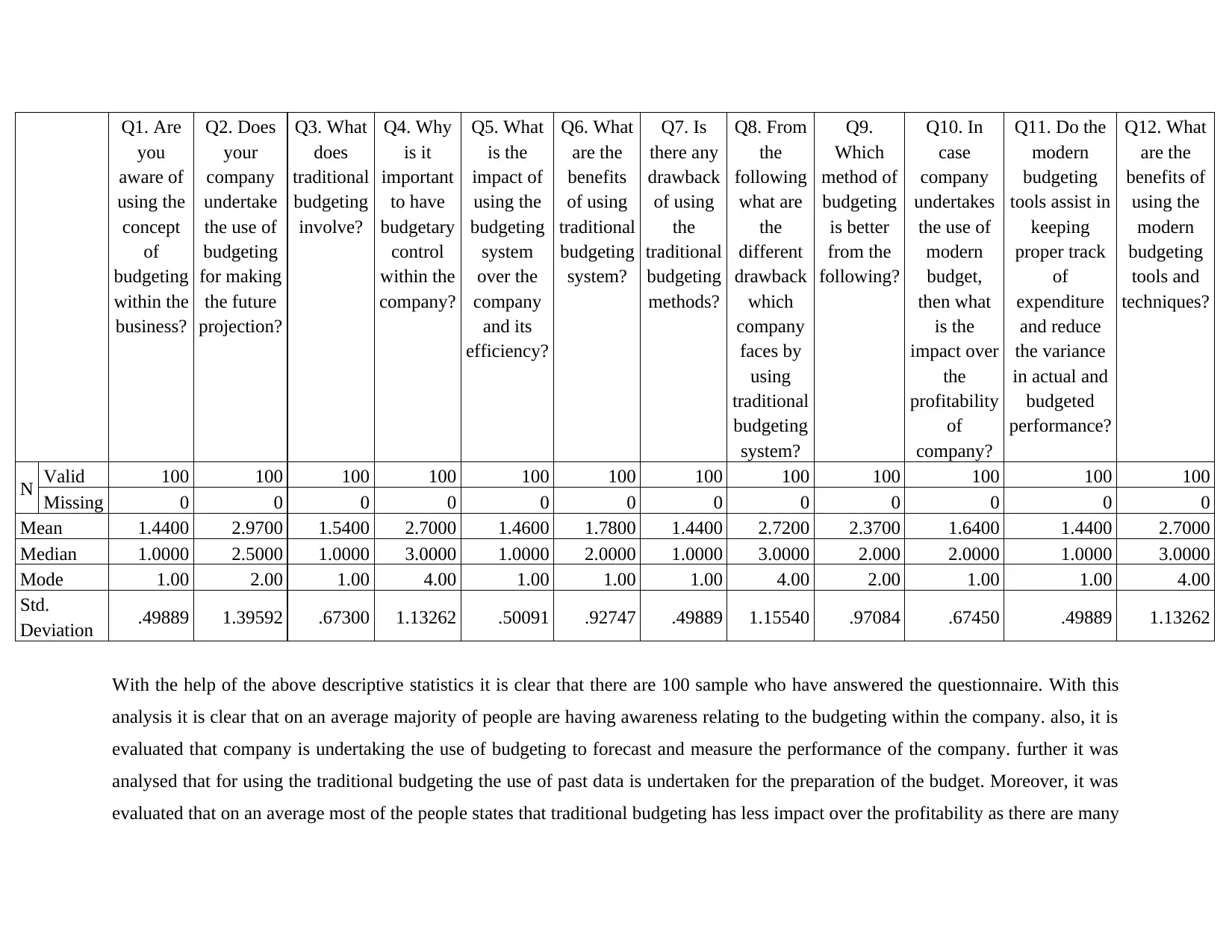

Q1. Are

you

aware of

using the

concept

of

budgeting

within the

business?

Q2. Does

your

company

undertake

the use of

budgeting

for making

the future

projection?

Q3. What

does

traditional

budgeting

involve?

Q4. Why

is it

important

to have

budgetary

control

within the

company?

Q5. What

is the

impact of

using the

budgeting

system

over the

company

and its

efficiency?

Q6. What

are the

benefits

of using

traditional

budgeting

system?

Q7. Is

there any

drawback

of using

the

traditional

budgeting

methods?

Q8. From

the

following

what are

the

different

drawback

which

company

faces by

using

traditional

budgeting

system?

Q9.

Which

method of

budgeting

is better

from the

following?

Q10. In

case

company

undertakes

the use of

modern

budget,

then what

is the

impact over

the

profitability

of

company?

Q11. Do the

modern

budgeting

tools assist in

keeping

proper track

of

expenditure

and reduce

the variance

in actual and

budgeted

performance?

Q12. What

are the

benefits of

using the

modern

budgeting

tools and

techniques?

N Valid 100 100 100 100 100 100 100 100 100 100 100 100

Missing 0 0 0 0 0 0 0 0 0 0 0 0

Mean 1.4400 2.9700 1.5400 2.7000 1.4600 1.7800 1.4400 2.7200 2.3700 1.6400 1.4400 2.7000

Median 1.0000 2.5000 1.0000 3.0000 1.0000 2.0000 1.0000 3.0000 2.000 2.0000 1.0000 3.0000

Mode 1.00 2.00 1.00 4.00 1.00 1.00 1.00 4.00 2.00 1.00 1.00 4.00

Std.

Deviation .49889 1.39592 .67300 1.13262 .50091 .92747 .49889 1.15540 .97084 .67450 .49889 1.13262

With the help of the above descriptive statistics it is clear that there are 100 sample who have answered the questionnaire. With this

analysis it is clear that on an average majority of people are having awareness relating to the budgeting within the company. also, it is

evaluated that company is undertaking the use of budgeting to forecast and measure the performance of the company. further it was

analysed that for using the traditional budgeting the use of past data is undertaken for the preparation of the budget. Moreover, it was

evaluated that on an average most of the people states that traditional budgeting has less impact over the profitability as there are many

you

aware of

using the

concept

of

budgeting

within the

business?

Q2. Does

your

company

undertake

the use of

budgeting

for making

the future

projection?

Q3. What

does

traditional

budgeting

involve?

Q4. Why

is it

important

to have

budgetary

control

within the

company?

Q5. What

is the

impact of

using the

budgeting

system

over the

company

and its

efficiency?

Q6. What

are the

benefits

of using

traditional

budgeting

system?

Q7. Is

there any

drawback

of using

the

traditional

budgeting

methods?

Q8. From

the

following

what are

the

different

drawback

which

company

faces by

using

traditional

budgeting

system?

Q9.

Which

method of

budgeting

is better

from the

following?

Q10. In

case

company

undertakes

the use of

modern

budget,

then what

is the

impact over

the

profitability

of

company?

Q11. Do the

modern

budgeting

tools assist in

keeping

proper track

of

expenditure

and reduce

the variance

in actual and

budgeted

performance?

Q12. What

are the

benefits of

using the

modern

budgeting

tools and

techniques?

N Valid 100 100 100 100 100 100 100 100 100 100 100 100

Missing 0 0 0 0 0 0 0 0 0 0 0 0

Mean 1.4400 2.9700 1.5400 2.7000 1.4600 1.7800 1.4400 2.7200 2.3700 1.6400 1.4400 2.7000

Median 1.0000 2.5000 1.0000 3.0000 1.0000 2.0000 1.0000 3.0000 2.000 2.0000 1.0000 3.0000

Mode 1.00 2.00 1.00 4.00 1.00 1.00 1.00 4.00 2.00 1.00 1.00 4.00

Std.

Deviation .49889 1.39592 .67300 1.13262 .50091 .92747 .49889 1.15540 .97084 .67450 .49889 1.13262

With the help of the above descriptive statistics it is clear that there are 100 sample who have answered the questionnaire. With this

analysis it is clear that on an average majority of people are having awareness relating to the budgeting within the company. also, it is

evaluated that company is undertaking the use of budgeting to forecast and measure the performance of the company. further it was

analysed that for using the traditional budgeting the use of past data is undertaken for the preparation of the budget. Moreover, it was

evaluated that on an average most of the people states that traditional budgeting has less impact over the profitability as there are many

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

drawbacks of using the traditional budgeting. Moreover, descriptive statistics stated that the most frequently used budgeting tool is

the zero based budgeting.

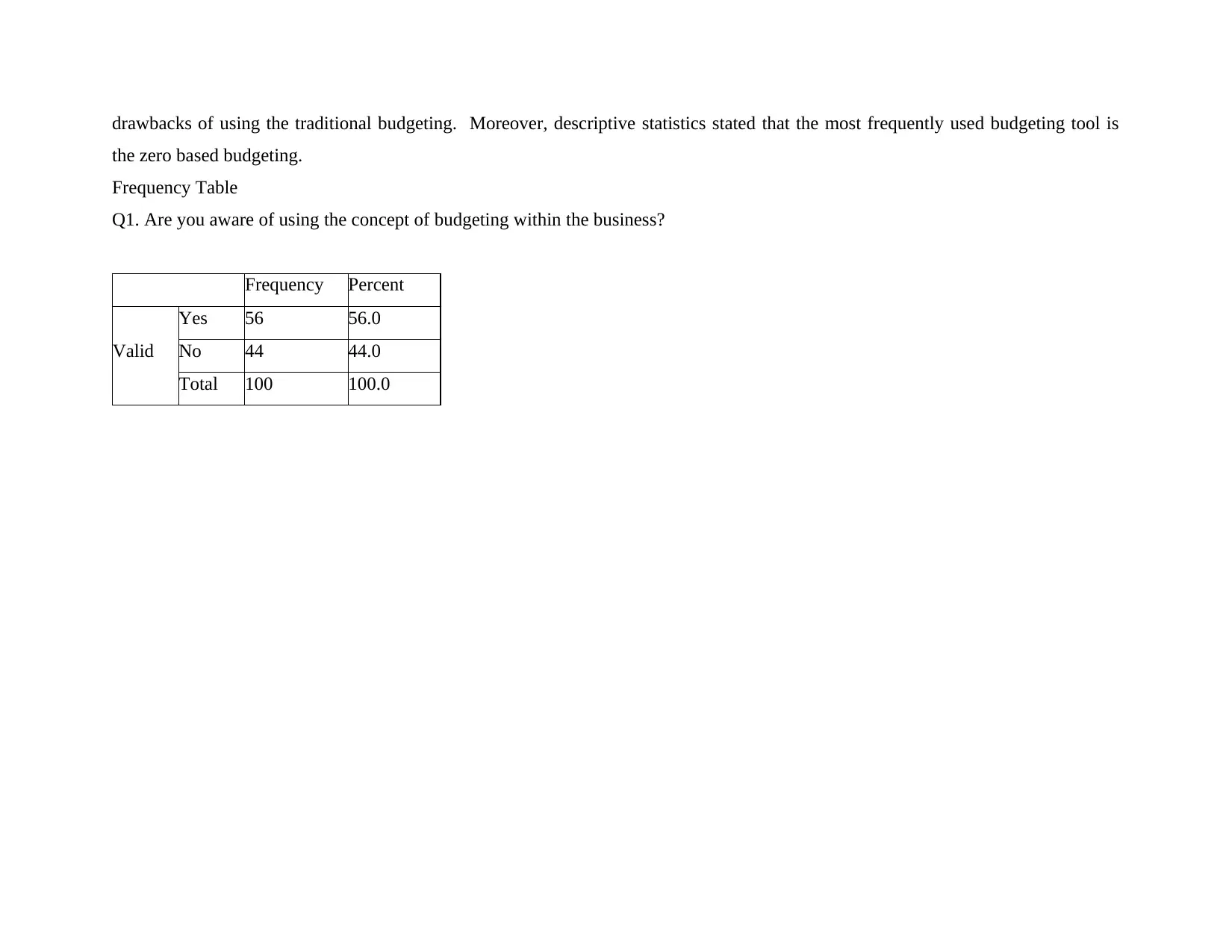

Frequency Table

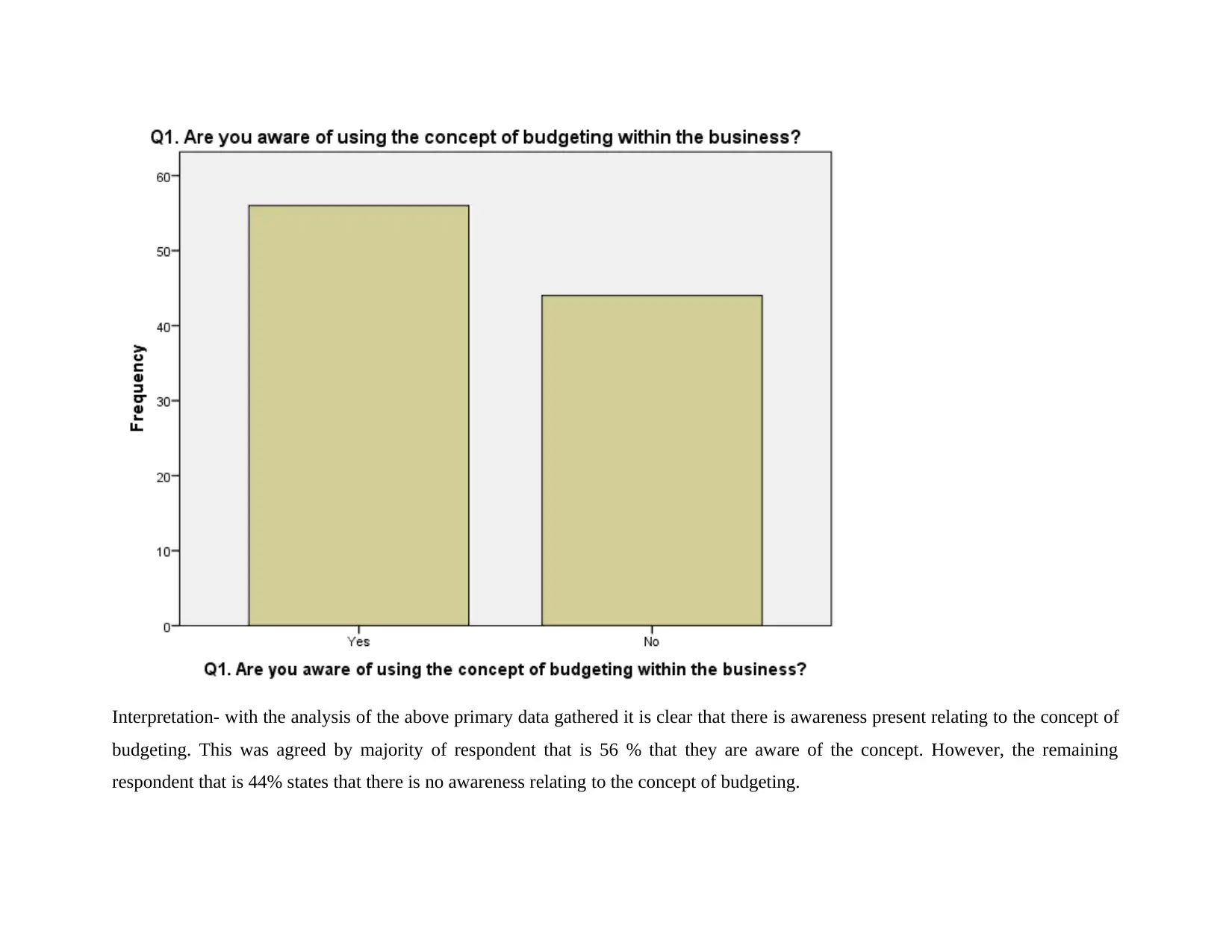

Q1. Are you aware of using the concept of budgeting within the business?

Frequency Percent

Valid

Yes 56 56.0

No 44 44.0

Total 100 100.0

the zero based budgeting.

Frequency Table

Q1. Are you aware of using the concept of budgeting within the business?

Frequency Percent

Valid

Yes 56 56.0

No 44 44.0

Total 100 100.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- with the analysis of the above primary data gathered it is clear that there is awareness present relating to the concept of

budgeting. This was agreed by majority of respondent that is 56 % that they are aware of the concept. However, the remaining

respondent that is 44% states that there is no awareness relating to the concept of budgeting.

budgeting. This was agreed by majority of respondent that is 56 % that they are aware of the concept. However, the remaining

respondent that is 44% states that there is no awareness relating to the concept of budgeting.

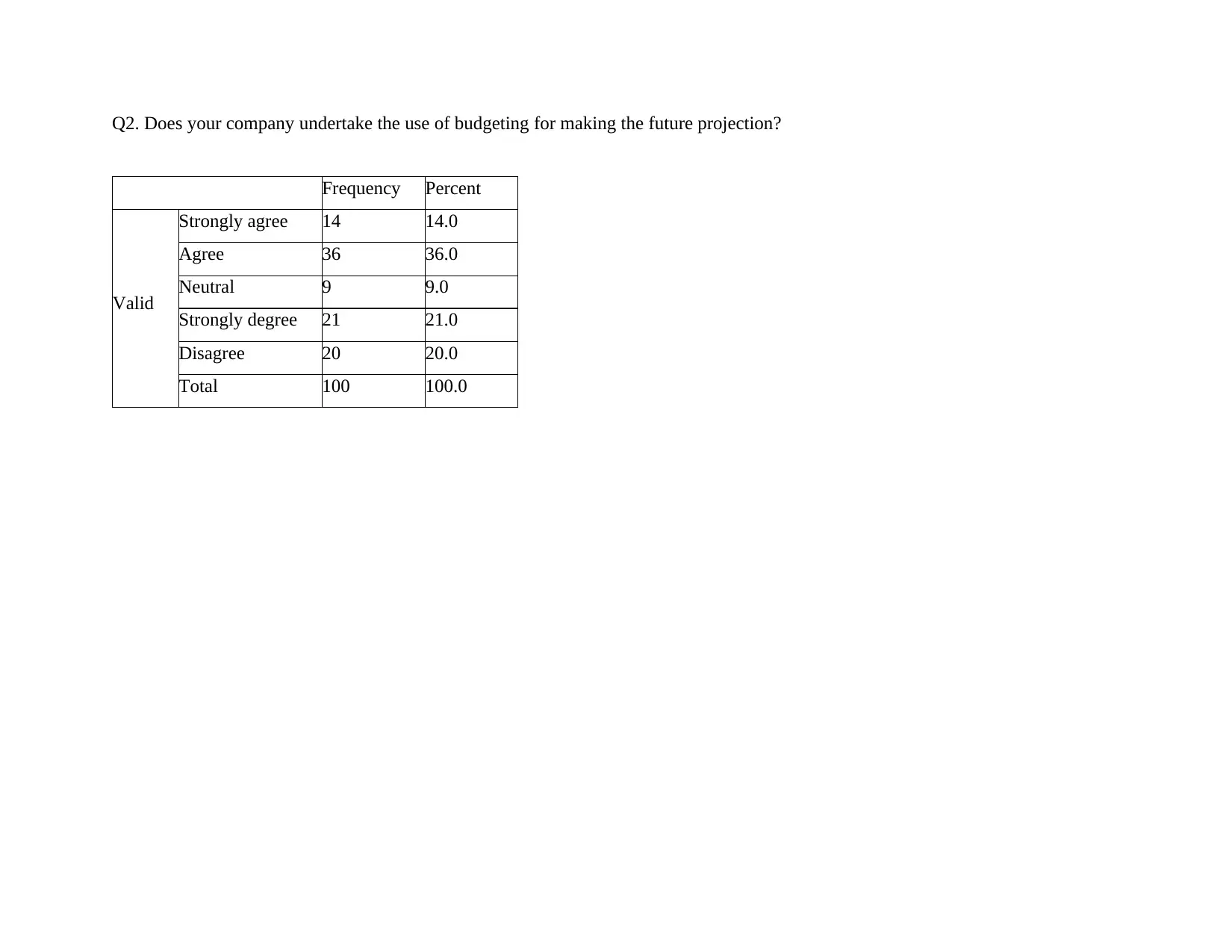

Q2. Does your company undertake the use of budgeting for making the future projection?

Frequency Percent

Valid

Strongly agree 14 14.0

Agree 36 36.0

Neutral 9 9.0

Strongly degree 21 21.0

Disagree 20 20.0

Total 100 100.0

Frequency Percent

Valid

Strongly agree 14 14.0

Agree 36 36.0

Neutral 9 9.0

Strongly degree 21 21.0

Disagree 20 20.0

Total 100 100.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.