Comparative Cost Accounting Analysis: Sewing Ltd. Case Study

VerifiedAdded on 2021/06/16

|15

|3180

|27

Report

AI Summary

This report provides a comprehensive analysis of cost accounting methods, specifically focusing on the comparison between traditional costing and activity-based costing (ABC). The analysis uses a case study of Sewing Ltd. to illustrate the practical implications of each method. The report begins by calculating the cost per unit for both basic and advance models under both costing approaches, highlighting the differences in overhead allocation and its impact on product costs. It then proceeds to calculate the selling prices and prepare profit and loss statements under both methods, demonstrating how different costing methods affect profitability and pricing decisions. The report further explores the implications of these cost allocation methods on buyer behavior, particularly in the context of an overseas buyer's purchasing decisions. Finally, it discusses various methods of cost allocation, the treatment of over and under-recovered overheads, and the advantages of ABC in providing a clearer view of production costs and aiding in better decision-making. The report emphasizes the importance of accurate cost allocation in product pricing and financial health.

Introduction to Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1:..................................................................................................................................3

Solution 2:..................................................................................................................................4

Solution 3:..................................................................................................................................6

Solution 4:..................................................................................................................................9

Solution 5:................................................................................................................................11

Bibliography.............................................................................................................................14

2

Solution 1:..................................................................................................................................3

Solution 2:..................................................................................................................................4

Solution 3:..................................................................................................................................6

Solution 4:..................................................................................................................................9

Solution 5:................................................................................................................................11

Bibliography.............................................................................................................................14

2

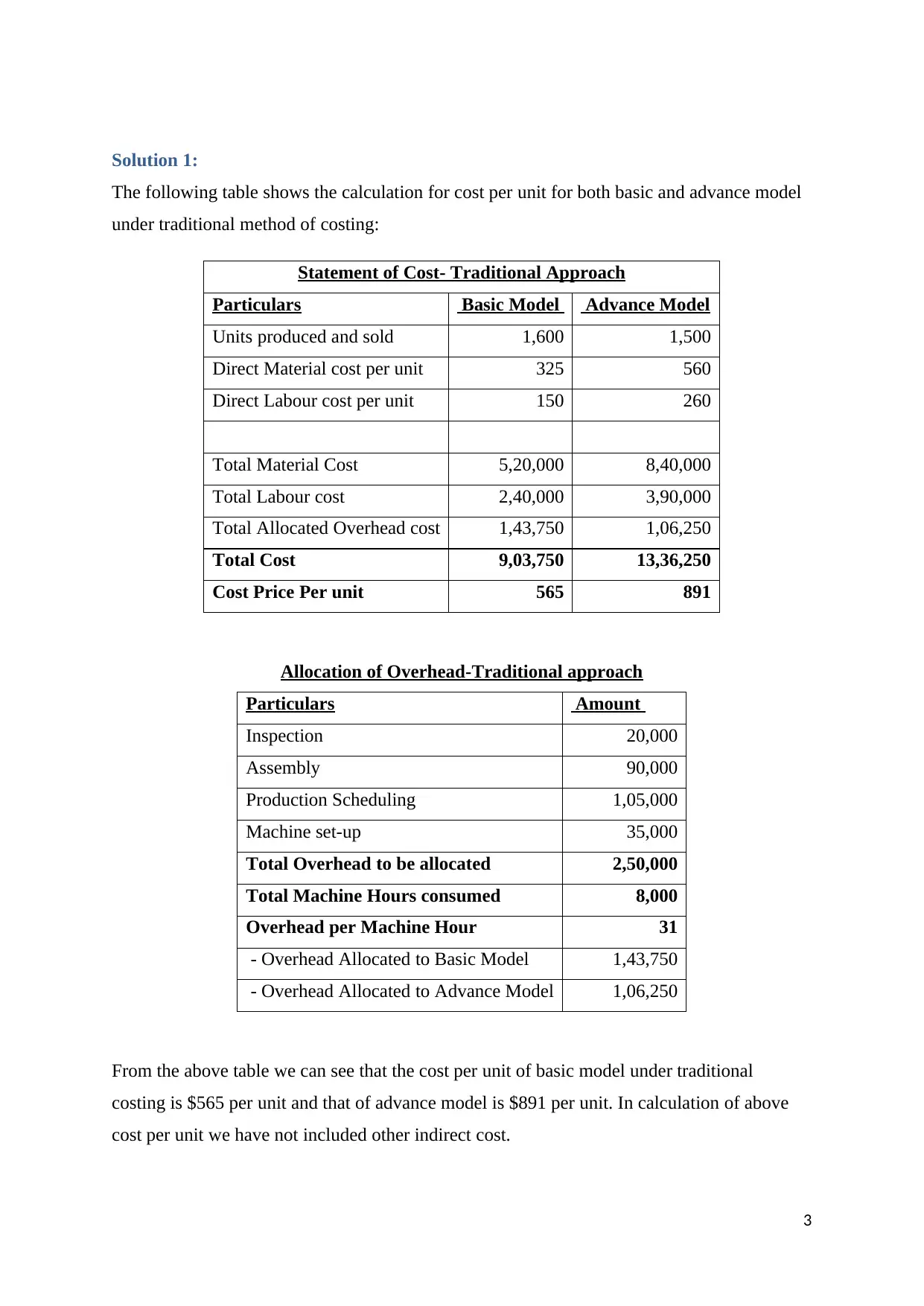

Solution 1:

The following table shows the calculation for cost per unit for both basic and advance model

under traditional method of costing:

Statement of Cost- Traditional Approach

Particulars Basic Model Advance Model

Units produced and sold 1,600 1,500

Direct Material cost per unit 325 560

Direct Labour cost per unit 150 260

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 1,43,750 1,06,250

Total Cost 9,03,750 13,36,250

Cost Price Per unit 565 891

Allocation of Overhead-Traditional approach

Particulars Amount

Inspection 20,000

Assembly 90,000

Production Scheduling 1,05,000

Machine set-up 35,000

Total Overhead to be allocated 2,50,000

Total Machine Hours consumed 8,000

Overhead per Machine Hour 31

- Overhead Allocated to Basic Model 1,43,750

- Overhead Allocated to Advance Model 1,06,250

From the above table we can see that the cost per unit of basic model under traditional

costing is $565 per unit and that of advance model is $891 per unit. In calculation of above

cost per unit we have not included other indirect cost.

3

The following table shows the calculation for cost per unit for both basic and advance model

under traditional method of costing:

Statement of Cost- Traditional Approach

Particulars Basic Model Advance Model

Units produced and sold 1,600 1,500

Direct Material cost per unit 325 560

Direct Labour cost per unit 150 260

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 1,43,750 1,06,250

Total Cost 9,03,750 13,36,250

Cost Price Per unit 565 891

Allocation of Overhead-Traditional approach

Particulars Amount

Inspection 20,000

Assembly 90,000

Production Scheduling 1,05,000

Machine set-up 35,000

Total Overhead to be allocated 2,50,000

Total Machine Hours consumed 8,000

Overhead per Machine Hour 31

- Overhead Allocated to Basic Model 1,43,750

- Overhead Allocated to Advance Model 1,06,250

From the above table we can see that the cost per unit of basic model under traditional

costing is $565 per unit and that of advance model is $891 per unit. In calculation of above

cost per unit we have not included other indirect cost.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

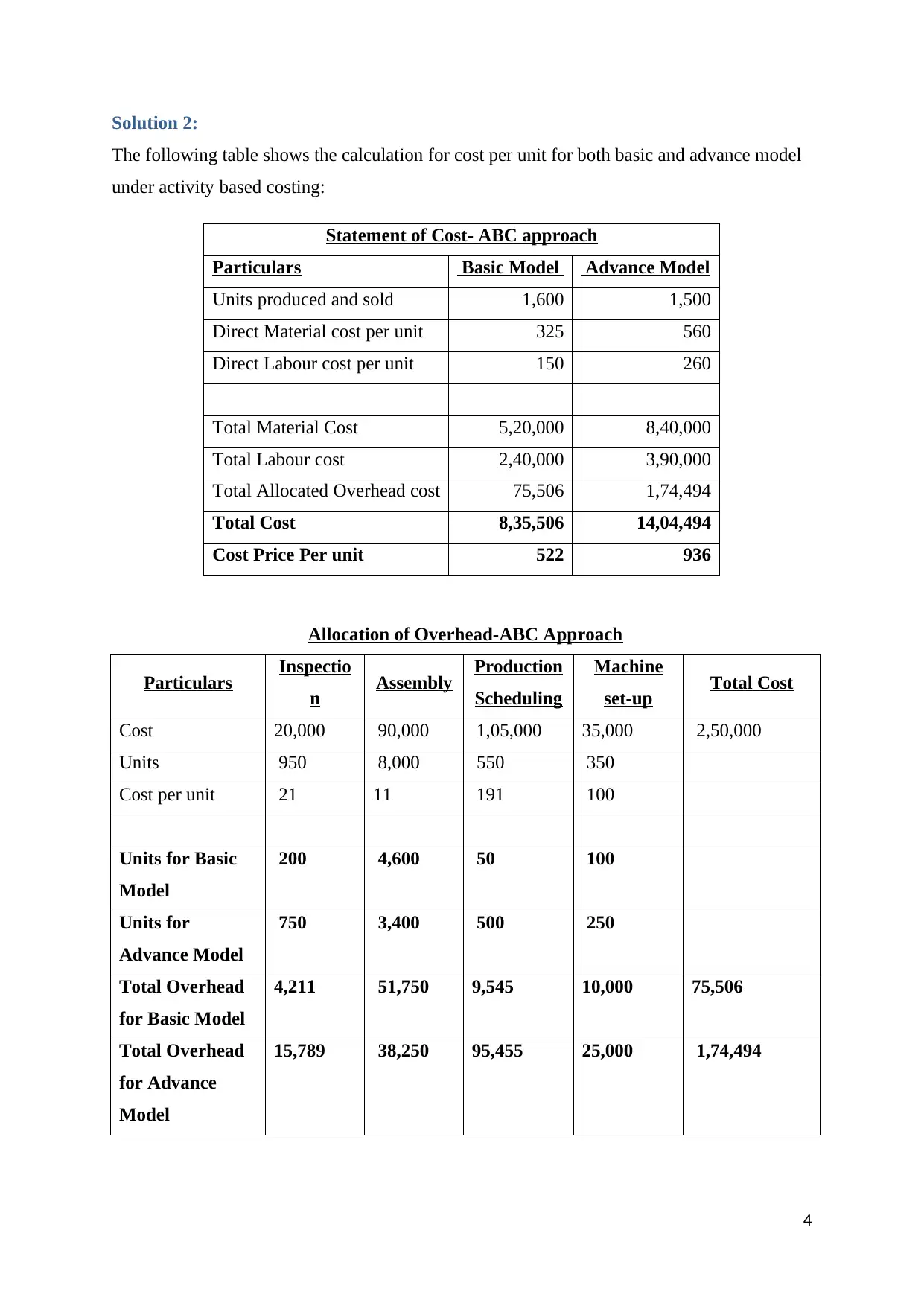

Solution 2:

The following table shows the calculation for cost per unit for both basic and advance model

under activity based costing:

Statement of Cost- ABC approach

Particulars Basic Model Advance Model

Units produced and sold 1,600 1,500

Direct Material cost per unit 325 560

Direct Labour cost per unit 150 260

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 75,506 1,74,494

Total Cost 8,35,506 14,04,494

Cost Price Per unit 522 936

Allocation of Overhead-ABC Approach

Particulars Inspectio

n Assembly Production

Scheduling

Machine

set-up Total Cost

Cost 20,000 90,000 1,05,000 35,000 2,50,000

Units 950 8,000 550 350

Cost per unit 21 11 191 100

Units for Basic

Model

200 4,600 50 100

Units for

Advance Model

750 3,400 500 250

Total Overhead

for Basic Model

4,211 51,750 9,545 10,000 75,506

Total Overhead

for Advance

Model

15,789 38,250 95,455 25,000 1,74,494

4

The following table shows the calculation for cost per unit for both basic and advance model

under activity based costing:

Statement of Cost- ABC approach

Particulars Basic Model Advance Model

Units produced and sold 1,600 1,500

Direct Material cost per unit 325 560

Direct Labour cost per unit 150 260

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 75,506 1,74,494

Total Cost 8,35,506 14,04,494

Cost Price Per unit 522 936

Allocation of Overhead-ABC Approach

Particulars Inspectio

n Assembly Production

Scheduling

Machine

set-up Total Cost

Cost 20,000 90,000 1,05,000 35,000 2,50,000

Units 950 8,000 550 350

Cost per unit 21 11 191 100

Units for Basic

Model

200 4,600 50 100

Units for

Advance Model

750 3,400 500 250

Total Overhead

for Basic Model

4,211 51,750 9,545 10,000 75,506

Total Overhead

for Advance

Model

15,789 38,250 95,455 25,000 1,74,494

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above table we can see that the cost per unit of the basic model under activity based

costing is $522 per unit and that of advance model is $936 per unit. In calculation of above

cost per unit we have not included other indirect cost.

5

costing is $522 per unit and that of advance model is $936 per unit. In calculation of above

cost per unit we have not included other indirect cost.

5

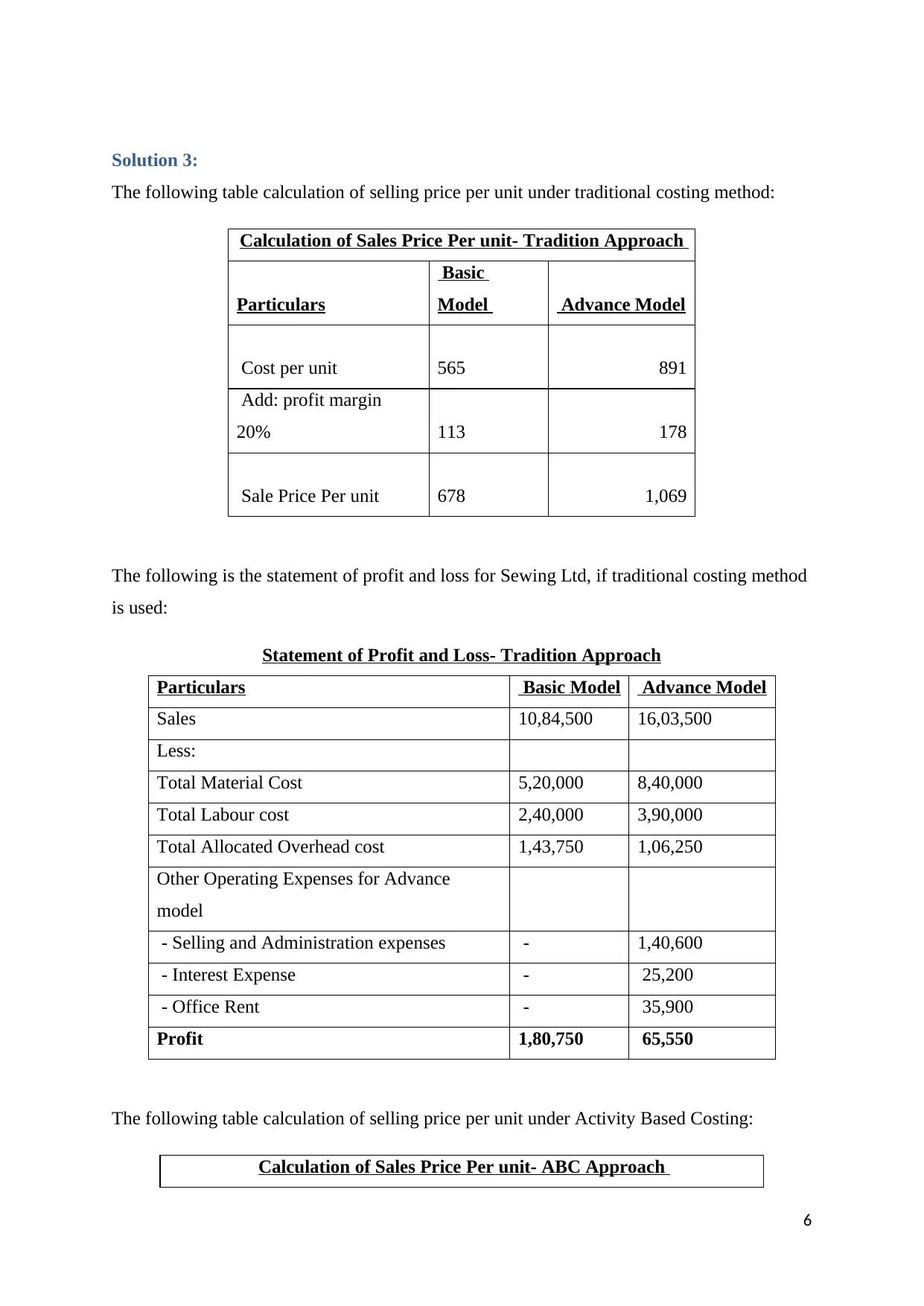

Solution 3:

The following table calculation of selling price per unit under traditional costing method:

Calculation of Sales Price Per unit- Tradition Approach

Particulars

Basic

Model Advance Model

Cost per unit 565 891

Add: profit margin

20% 113 178

Sale Price Per unit 678 1,069

The following is the statement of profit and loss for Sewing Ltd, if traditional costing method

is used:

Statement of Profit and Loss- Tradition Approach

Particulars Basic Model Advance Model

Sales 10,84,500 16,03,500

Less:

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 1,43,750 1,06,250

Other Operating Expenses for Advance

model

- Selling and Administration expenses - 1,40,600

- Interest Expense - 25,200

- Office Rent - 35,900

Profit 1,80,750 65,550

The following table calculation of selling price per unit under Activity Based Costing:

Calculation of Sales Price Per unit- ABC Approach

6

The following table calculation of selling price per unit under traditional costing method:

Calculation of Sales Price Per unit- Tradition Approach

Particulars

Basic

Model Advance Model

Cost per unit 565 891

Add: profit margin

20% 113 178

Sale Price Per unit 678 1,069

The following is the statement of profit and loss for Sewing Ltd, if traditional costing method

is used:

Statement of Profit and Loss- Tradition Approach

Particulars Basic Model Advance Model

Sales 10,84,500 16,03,500

Less:

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 1,43,750 1,06,250

Other Operating Expenses for Advance

model

- Selling and Administration expenses - 1,40,600

- Interest Expense - 25,200

- Office Rent - 35,900

Profit 1,80,750 65,550

The following table calculation of selling price per unit under Activity Based Costing:

Calculation of Sales Price Per unit- ABC Approach

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

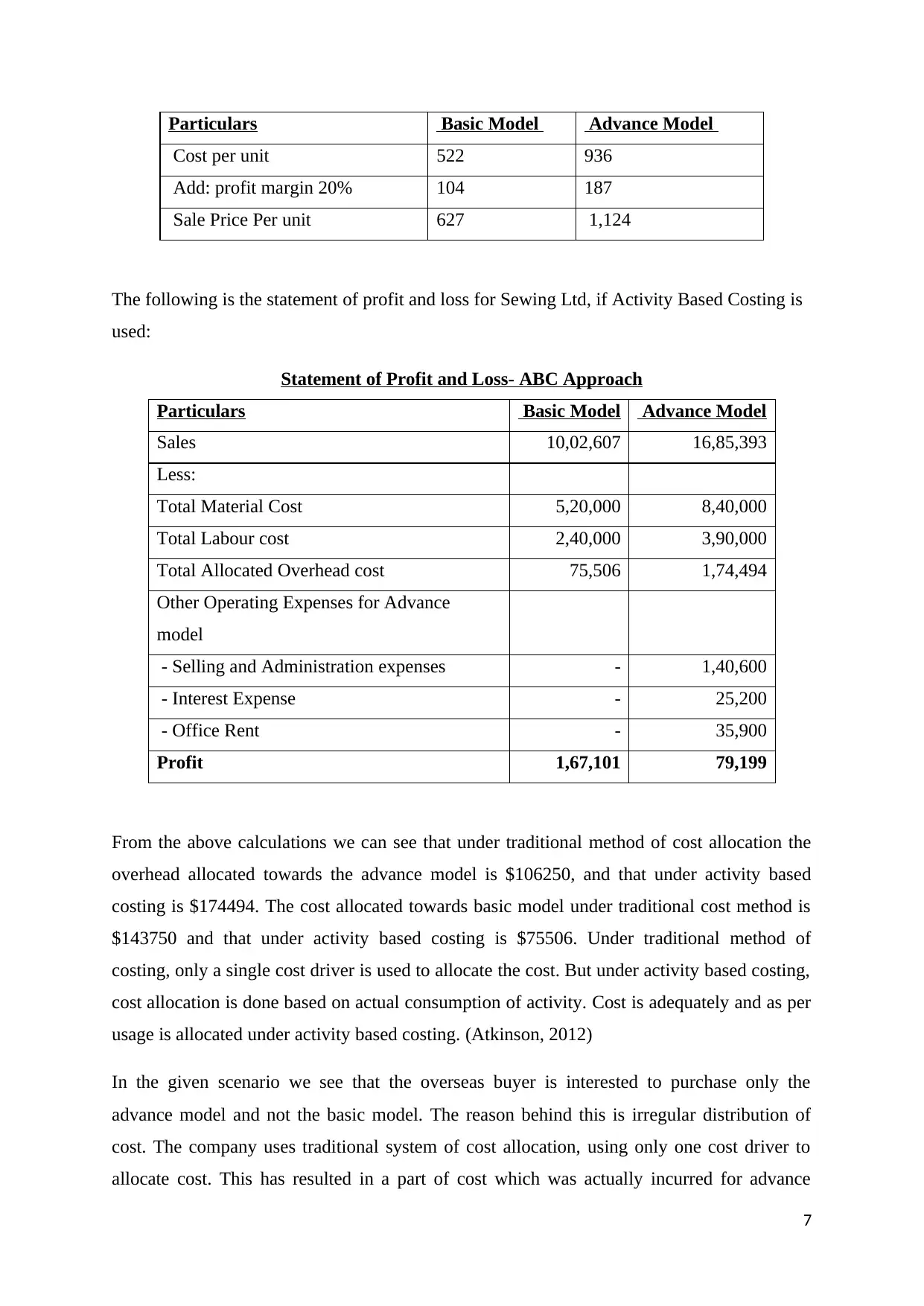

Particulars Basic Model Advance Model

Cost per unit 522 936

Add: profit margin 20% 104 187

Sale Price Per unit 627 1,124

The following is the statement of profit and loss for Sewing Ltd, if Activity Based Costing is

used:

Statement of Profit and Loss- ABC Approach

Particulars Basic Model Advance Model

Sales 10,02,607 16,85,393

Less:

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 75,506 1,74,494

Other Operating Expenses for Advance

model

- Selling and Administration expenses - 1,40,600

- Interest Expense - 25,200

- Office Rent - 35,900

Profit 1,67,101 79,199

From the above calculations we can see that under traditional method of cost allocation the

overhead allocated towards the advance model is $106250, and that under activity based

costing is $174494. The cost allocated towards basic model under traditional cost method is

$143750 and that under activity based costing is $75506. Under traditional method of

costing, only a single cost driver is used to allocate the cost. But under activity based costing,

cost allocation is done based on actual consumption of activity. Cost is adequately and as per

usage is allocated under activity based costing. (Atkinson, 2012)

In the given scenario we see that the overseas buyer is interested to purchase only the

advance model and not the basic model. The reason behind this is irregular distribution of

cost. The company uses traditional system of cost allocation, using only one cost driver to

allocate cost. This has resulted in a part of cost which was actually incurred for advance

7

Cost per unit 522 936

Add: profit margin 20% 104 187

Sale Price Per unit 627 1,124

The following is the statement of profit and loss for Sewing Ltd, if Activity Based Costing is

used:

Statement of Profit and Loss- ABC Approach

Particulars Basic Model Advance Model

Sales 10,02,607 16,85,393

Less:

Total Material Cost 5,20,000 8,40,000

Total Labour cost 2,40,000 3,90,000

Total Allocated Overhead cost 75,506 1,74,494

Other Operating Expenses for Advance

model

- Selling and Administration expenses - 1,40,600

- Interest Expense - 25,200

- Office Rent - 35,900

Profit 1,67,101 79,199

From the above calculations we can see that under traditional method of cost allocation the

overhead allocated towards the advance model is $106250, and that under activity based

costing is $174494. The cost allocated towards basic model under traditional cost method is

$143750 and that under activity based costing is $75506. Under traditional method of

costing, only a single cost driver is used to allocate the cost. But under activity based costing,

cost allocation is done based on actual consumption of activity. Cost is adequately and as per

usage is allocated under activity based costing. (Atkinson, 2012)

In the given scenario we see that the overseas buyer is interested to purchase only the

advance model and not the basic model. The reason behind this is irregular distribution of

cost. The company uses traditional system of cost allocation, using only one cost driver to

allocate cost. This has resulted in a part of cost which was actually incurred for advance

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

model to be shifted to basic model. Since, the cost allocated is less towards the advance

model; the selling price for the same is also reduced. The company is currently charging $

1069 per unit for advance model from the overseas buyer. If the company would have used

activity based costing the, price charged from the customer would have been $1124. The

overseas buyer has observed this difference in price for $55 per unit. Since sewing ltd is

charging $55 less per unit on the advance model, the overseas buyer is interested in buying

only the advance model.

For basic model, the company is charging $678 per unit under traditional costing method. If it

uses activity based costing then the company would charge $627 per unit for the basic model.

Since the company is using traditional costing method, it is charging $51 per unit more on the

basic model. The overseas buyer can purchase the basic model from market at $627 per unit.

This is why the overseas buyer is not interested in buying the basic model form Sewing Ltd.

Therefore, we see that method of cost allocation has a high effect on the product pricing.

Using the correct method of cost allocation is very important, as it affects the buyer’s

decision. (Berry, 2009) Wrong allocation of cost among products may lead to financial

troubles for the company.

8

model; the selling price for the same is also reduced. The company is currently charging $

1069 per unit for advance model from the overseas buyer. If the company would have used

activity based costing the, price charged from the customer would have been $1124. The

overseas buyer has observed this difference in price for $55 per unit. Since sewing ltd is

charging $55 less per unit on the advance model, the overseas buyer is interested in buying

only the advance model.

For basic model, the company is charging $678 per unit under traditional costing method. If it

uses activity based costing then the company would charge $627 per unit for the basic model.

Since the company is using traditional costing method, it is charging $51 per unit more on the

basic model. The overseas buyer can purchase the basic model from market at $627 per unit.

This is why the overseas buyer is not interested in buying the basic model form Sewing Ltd.

Therefore, we see that method of cost allocation has a high effect on the product pricing.

Using the correct method of cost allocation is very important, as it affects the buyer’s

decision. (Berry, 2009) Wrong allocation of cost among products may lead to financial

troubles for the company.

8

Solution 4:

There are various methods of cost allocation that can be used. When the absorption costing

method is used rate which is predetermined is taken into consideration in order to ascertain

the price of the products. It is obvious that company will not just ask for the expenses it will

also ask for a profit margin that will affect the change in cost and selling price of the product.

There seems to exists huge variations in the amount which is charged from the customers and

the actual amount that the firm incurs as expenses. (Bierman & Smidt, 2010)The differences

between the expenses and actual selling price of the product make differences in the books

and should be treated in the accounting system.

For example, if we take into consideration the concept of recovery of overheads, then you

will be able to understand the fact. If a company decides to produce 20000 units of a product

and it is also likely to incur $100000 as overhead expenses then it will be clear for the

company that it needs to charge $5 per unit as the overhead expenses. The selling price with

the customer is asked to pay contains the price of overhead expenses which in this case is $5.

The method which has been used in order to evaluate overhead expenses is on estimated

basis. The overhead expenses that were incurred by the company was $72000 and the units

produced by 18000 which resulted in the net per unit overhead expenses to value at $4. The

company was said to receive the dollar for $90000 of overhead expenses after selling the

18000 units which had produced. The over recovery amount in the given case around $18000

which is needed by the company to adjust in its book of accounts.

The only case when the actual overhead costs and the estimated overhead costs are same is

the case when the company charges the exact overhead charges that have actually been

incurred by the organization during the production of a certain product (Boyd, 2013). This is

the case where no under or over-recovery that may exist. There are several methods that can

be used by the organization in order to record the over and under expenses that have been

incurred during the time of production: (Datar M. S., 2015)

The amount which is the difference between the actual and applied overhead is settled with

the profit and loss statement. It is supposed to be one of the best and easiest methods in order

to treat this kind of transactions (Datar S. , 2016). This method consists of charging the

overhead expenses directly in the profit and loss account of the firm so that the expenses

incurred by the organization can be adjusted in the accounts of that particular financial year.

9

There are various methods of cost allocation that can be used. When the absorption costing

method is used rate which is predetermined is taken into consideration in order to ascertain

the price of the products. It is obvious that company will not just ask for the expenses it will

also ask for a profit margin that will affect the change in cost and selling price of the product.

There seems to exists huge variations in the amount which is charged from the customers and

the actual amount that the firm incurs as expenses. (Bierman & Smidt, 2010)The differences

between the expenses and actual selling price of the product make differences in the books

and should be treated in the accounting system.

For example, if we take into consideration the concept of recovery of overheads, then you

will be able to understand the fact. If a company decides to produce 20000 units of a product

and it is also likely to incur $100000 as overhead expenses then it will be clear for the

company that it needs to charge $5 per unit as the overhead expenses. The selling price with

the customer is asked to pay contains the price of overhead expenses which in this case is $5.

The method which has been used in order to evaluate overhead expenses is on estimated

basis. The overhead expenses that were incurred by the company was $72000 and the units

produced by 18000 which resulted in the net per unit overhead expenses to value at $4. The

company was said to receive the dollar for $90000 of overhead expenses after selling the

18000 units which had produced. The over recovery amount in the given case around $18000

which is needed by the company to adjust in its book of accounts.

The only case when the actual overhead costs and the estimated overhead costs are same is

the case when the company charges the exact overhead charges that have actually been

incurred by the organization during the production of a certain product (Boyd, 2013). This is

the case where no under or over-recovery that may exist. There are several methods that can

be used by the organization in order to record the over and under expenses that have been

incurred during the time of production: (Datar M. S., 2015)

The amount which is the difference between the actual and applied overhead is settled with

the profit and loss statement. It is supposed to be one of the best and easiest methods in order

to treat this kind of transactions (Datar S. , 2016). This method consists of charging the

overhead expenses directly in the profit and loss account of the firm so that the expenses

incurred by the organization can be adjusted in the accounts of that particular financial year.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The amount of the overhead expenses can also be transferred to the financial document of the

next year. This method is mostly used by the manufacturers in order keep the accounts of the

present financial year clean. (Holtzman, 2013)This method carries forwards the difference in

the overhead expenses to the next year and the treatment of the overhead expenses will take

place in the financial documents of the next year. In order to eliminate the difference of the

value of the overhead expenses, the manufacturer claims to adjust it in the statements.

Another method that can be used to evaluate the difference of the overhead expenses is to

charge them in the same financial year. This method is generally used when there have been

any mistakes in the calculation of the overhead expenses at the starting of year. This method

generally uses a predetermined overhead expense that is charged to the customers at the time

of selling process. (Horngren, 2012)

Therefore it is clear that there are cases arising in relation to the under and over expenses that

are charged to the customers and also there have been methods on how to treat these expenses

in the books of accounts so as to keep them clean.

10

next year. This method is mostly used by the manufacturers in order keep the accounts of the

present financial year clean. (Holtzman, 2013)This method carries forwards the difference in

the overhead expenses to the next year and the treatment of the overhead expenses will take

place in the financial documents of the next year. In order to eliminate the difference of the

value of the overhead expenses, the manufacturer claims to adjust it in the statements.

Another method that can be used to evaluate the difference of the overhead expenses is to

charge them in the same financial year. This method is generally used when there have been

any mistakes in the calculation of the overhead expenses at the starting of year. This method

generally uses a predetermined overhead expense that is charged to the customers at the time

of selling process. (Horngren, 2012)

Therefore it is clear that there are cases arising in relation to the under and over expenses that

are charged to the customers and also there have been methods on how to treat these expenses

in the books of accounts so as to keep them clean.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 5:

The activity-based costing system uses the technique of allocation of the cost and expenses of

the resources that have been incurred in the manufacturing of a certain product. This is a new

type of Costing method which is used by the firm in order to allocate all the cost and

expenses that have been incurred in the manufacturing of the product by the resources that

have been used as raw materials and does help the company in ascertainment of appropriate

decisions. (Menifield, 2014) It has been observed that these types of Costing methods are

very reliable when the organization needs to construct the relationship between the costs and

the actual price of the product. Also because of diverse nature of some of the expenses, it is

very hard for them to allocate in the type of cost on the manufacturing process. It has also

been clearly observed that this type of processes is mainly design for the use of

manufacturing industries and not for retail companies because of their diverse nature. The

main advantages of the use of the activity-based costing system are:

Analysis of the production cost - the main function which was observed about the activity-

based costing method was to assign groups for different cost so that there may be a clear

differentiation between the services actual and the real cost of the manufactured products and

thus Clear View of the cost required in order to manufacture the product is ascertained. They

are Organisation in which small overhead expenses group up in order to form a large expense

and does affecting the cost of the product sold, hence making it necessary for the firm to

allocate the cost in a specified manner so that the firm can be protected from the problems

that may prevail upon it in the future during the analysis of the course related to the

manufactured product. (Noreen, 2015)

Assistance in controlling costs - the activity-based costing system depends on the

functionality that is present between the activities that are required in order to manufacture

the product and the product itself thus making it easier for the managers to access the cost of

the overhead expenses that are incurred in order to perform the activities. There are also

many other available measures that can be used in order to control the costs. (Nwanji, 2016)

Discovering the activities - the ABC method of Costing includes the assessment of each

activity in order to make proper analysis on the costs related to a product so as to make

allocation of the activities that are related to the factory expenses thus ensuring that there are

11

The activity-based costing system uses the technique of allocation of the cost and expenses of

the resources that have been incurred in the manufacturing of a certain product. This is a new

type of Costing method which is used by the firm in order to allocate all the cost and

expenses that have been incurred in the manufacturing of the product by the resources that

have been used as raw materials and does help the company in ascertainment of appropriate

decisions. (Menifield, 2014) It has been observed that these types of Costing methods are

very reliable when the organization needs to construct the relationship between the costs and

the actual price of the product. Also because of diverse nature of some of the expenses, it is

very hard for them to allocate in the type of cost on the manufacturing process. It has also

been clearly observed that this type of processes is mainly design for the use of

manufacturing industries and not for retail companies because of their diverse nature. The

main advantages of the use of the activity-based costing system are:

Analysis of the production cost - the main function which was observed about the activity-

based costing method was to assign groups for different cost so that there may be a clear

differentiation between the services actual and the real cost of the manufactured products and

thus Clear View of the cost required in order to manufacture the product is ascertained. They

are Organisation in which small overhead expenses group up in order to form a large expense

and does affecting the cost of the product sold, hence making it necessary for the firm to

allocate the cost in a specified manner so that the firm can be protected from the problems

that may prevail upon it in the future during the analysis of the course related to the

manufactured product. (Noreen, 2015)

Assistance in controlling costs - the activity-based costing system depends on the

functionality that is present between the activities that are required in order to manufacture

the product and the product itself thus making it easier for the managers to access the cost of

the overhead expenses that are incurred in order to perform the activities. There are also

many other available measures that can be used in order to control the costs. (Nwanji, 2016)

Discovering the activities - the ABC method of Costing includes the assessment of each

activity in order to make proper analysis on the costs related to a product so as to make

allocation of the activities that are related to the factory expenses thus ensuring that there are

11

no expenses that have been left or excluded during the time of valuation of a specified

product. (Piper, 2015)

Enhancement of the decision-making process - the information that is collected using the

ABC method prove to be very helpful in ascertainment of decisions by the manager so that

the activities performed may be in the best concern for the organization. This also helps to

ascertain a realistic price of the product which is also affordable to the customer. (Seal, 2012)

Assistance in capacity realization - the main purpose of the ABC method is to allocate the

expenses in different groups show that the price of the product can be ascertained. The

process helps managers in order to ascertain the maximum utilization of expenses which can

be controlled and also help them to control the cost of the product by including the capacity.

(Seitz & Ellison, 2009)

The mentioned advantages of the ABC method one of the most important and reliable

objectives that are needed to be fulfilled by the firm. There is some limitation along with the

advantages they are as follows:

Expensive and torturing methods of application - all the data should be collected at a single

place which makes it easier for the appropriate allocation of the overheads. This process of

collecting data is very complex and hence is considered unsuitable for the application in the

process of Costing. (Siciliano, 2015)

Unsuitability regarding the small Enterprises - in order to perform the activity based costing

method it is important for the firm to collect all the data and work in a manual way so that

complete and useful information is achieved. Thus the application of this process makes it a

lot harder for the small firms because of the expenses required by the method in order to

function. (Taillard, 2013)

Difficulty in measurement - this method of cost allocation a certain lot of expenses but it still

lacks in a certain mint of the value of resources that are needed in order to manufacture the

product. Because of the complexity of this task, this requires a lot of attention and any

presence of incorrect data may lead to Bad effects on the form and also may lead to the

organization incurring losses in future. (What is Management Accounting?)

And suitability towards service industry - after the study of the given data it is your dad

appropriation of the expenses in order to manufacture the product is not an easy task and as

12

product. (Piper, 2015)

Enhancement of the decision-making process - the information that is collected using the

ABC method prove to be very helpful in ascertainment of decisions by the manager so that

the activities performed may be in the best concern for the organization. This also helps to

ascertain a realistic price of the product which is also affordable to the customer. (Seal, 2012)

Assistance in capacity realization - the main purpose of the ABC method is to allocate the

expenses in different groups show that the price of the product can be ascertained. The

process helps managers in order to ascertain the maximum utilization of expenses which can

be controlled and also help them to control the cost of the product by including the capacity.

(Seitz & Ellison, 2009)

The mentioned advantages of the ABC method one of the most important and reliable

objectives that are needed to be fulfilled by the firm. There is some limitation along with the

advantages they are as follows:

Expensive and torturing methods of application - all the data should be collected at a single

place which makes it easier for the appropriate allocation of the overheads. This process of

collecting data is very complex and hence is considered unsuitable for the application in the

process of Costing. (Siciliano, 2015)

Unsuitability regarding the small Enterprises - in order to perform the activity based costing

method it is important for the firm to collect all the data and work in a manual way so that

complete and useful information is achieved. Thus the application of this process makes it a

lot harder for the small firms because of the expenses required by the method in order to

function. (Taillard, 2013)

Difficulty in measurement - this method of cost allocation a certain lot of expenses but it still

lacks in a certain mint of the value of resources that are needed in order to manufacture the

product. Because of the complexity of this task, this requires a lot of attention and any

presence of incorrect data may lead to Bad effects on the form and also may lead to the

organization incurring losses in future. (What is Management Accounting?)

And suitability towards service industry - after the study of the given data it is your dad

appropriation of the expenses in order to manufacture the product is not an easy task and as

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.