ACC200: Evaluating Traditional Costing vs. Activity Based Costing

VerifiedAdded on 2021/06/17

|11

|2387

|23

Report

AI Summary

This report analyzes two primary costing methods: traditional costing and activity-based costing (ABC). It begins with an executive summary highlighting the core differences in overhead cost allocation, followed by an introduction that explains the context of the analysis using a case study of Sewing Easy Limited. The report then delves into the calculation of cost per unit using both traditional and ABC methods, including detailed workings and calculations of predetermined overhead rates and overhead allocation. The report also presents profit and loss statements for a specific product model under both costing systems, followed by an analysis of why overseas buyers are interested in a particular model based on pricing differences. It concludes with a discussion on actual versus applied overheads and a review of the benefits and limitations of the ABC system, offering a comprehensive understanding of the two costing methods and their implications.

1

ACC200: ASSIGNMENT TERM 1 2018

ACC200: ASSIGNMENT TERM 1 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

There are mainly two methods of costing that are used to allocate the direct as well as

indirect cost to the cost system. The two main costing methods are traditional costing and

activity based costing. The main difference in traditional costing method and activity based

costing method is that way of allocating the overhead costs to different products. In this report a

given case problem has been solved using both traditional costing method and activity based

costing model. In this assignment advantages and limitations of the activity based costing has

been discussed in detail to have an overview on how activity based costing helps cost manager to

allocate various types of cost to the cost system. The give case problem is solved to find out the

cost per unit under traditional costing system and activity based costing system. It has been

found that Activity base costing model has used more sensible approach to allocate all the

indirect to given products: Basic Model and Advance Model. Activity based costing has applied

cost driver for each cost and on the basis of that overhead rate for each activity is determined to

allocate these overhead costs to each of product line. In this way overhead cost has been

proportioned to products on the basis of resources used by each product in each activity.

Executive Summary

There are mainly two methods of costing that are used to allocate the direct as well as

indirect cost to the cost system. The two main costing methods are traditional costing and

activity based costing. The main difference in traditional costing method and activity based

costing method is that way of allocating the overhead costs to different products. In this report a

given case problem has been solved using both traditional costing method and activity based

costing model. In this assignment advantages and limitations of the activity based costing has

been discussed in detail to have an overview on how activity based costing helps cost manager to

allocate various types of cost to the cost system. The give case problem is solved to find out the

cost per unit under traditional costing system and activity based costing system. It has been

found that Activity base costing model has used more sensible approach to allocate all the

indirect to given products: Basic Model and Advance Model. Activity based costing has applied

cost driver for each cost and on the basis of that overhead rate for each activity is determined to

allocate these overhead costs to each of product line. In this way overhead cost has been

proportioned to products on the basis of resources used by each product in each activity.

3

Introduction

In the field of management accounting the two main costing methods used to allocate the

indirect (Overhead) costs are activity based costing and traditional method. In both these

methods cost overhead rate of the production are calculated are assign to the total cost of product

using the cost driver rate. Traditional costing system uses only one cost driver rate while activity

based costing uses many cost driver rate to allocate the overhead cost to the total production cost.

In this report a typical case scenario has been given to calculate the cost per unit of

products using both traditional costing and activity based costing system. The given case

scenario is of Sewing Easy Limited that manufactures two models of sewing machines and these

models are basic model and advance model. In the given case problem management at Sewing

Easy Limited is concerned why oversea buyers are interested only in advance model not in the

basic model. Company currently is using the traditional method for allocating the cost and wants

to move to activity based costing system. In order to find out the reason why oversea buyer are

interested in advance model not in basic model, calculation has been made to find out cost per

unit using both traditional costing method and activity based budgeting method.

Solution-1: Calculation of cost per unit under the traditional costing system

The traditional method of cost accounting is used for allocation of manufacturing

overhead costs as per the manufactured products. The method is used for allocation of indirect

costs as per the volume of products manufactured. The method is highly useful for the business

managers to gain an overview of the overall indirect costs involved in the manufacturing process

of the company. The indirect costs are allocated on the basis of number of units produced or on

the basis of direct labor or the machine hours. The method involves identifying the indirect cost

related to the manufacturing process of the company on a regular basis (Tulsian, 2006).

The most significant advantage of the method is that it is relatively simple to be applied

as it is easy for the business managers to identify the indirect costs as per the products produced

or labor and machine hours consumed. The method also has a significant drawback that the

method is less reliable to be sued in the firms involved in manufacturing of large volume of few

products. This is because the increase in the amount of overhead expenses can increase the

chances of error occurrence in allocating the overhead costs to different products (Drury, 2008).

Introduction

In the field of management accounting the two main costing methods used to allocate the

indirect (Overhead) costs are activity based costing and traditional method. In both these

methods cost overhead rate of the production are calculated are assign to the total cost of product

using the cost driver rate. Traditional costing system uses only one cost driver rate while activity

based costing uses many cost driver rate to allocate the overhead cost to the total production cost.

In this report a typical case scenario has been given to calculate the cost per unit of

products using both traditional costing and activity based costing system. The given case

scenario is of Sewing Easy Limited that manufactures two models of sewing machines and these

models are basic model and advance model. In the given case problem management at Sewing

Easy Limited is concerned why oversea buyers are interested only in advance model not in the

basic model. Company currently is using the traditional method for allocating the cost and wants

to move to activity based costing system. In order to find out the reason why oversea buyer are

interested in advance model not in basic model, calculation has been made to find out cost per

unit using both traditional costing method and activity based budgeting method.

Solution-1: Calculation of cost per unit under the traditional costing system

The traditional method of cost accounting is used for allocation of manufacturing

overhead costs as per the manufactured products. The method is used for allocation of indirect

costs as per the volume of products manufactured. The method is highly useful for the business

managers to gain an overview of the overall indirect costs involved in the manufacturing process

of the company. The indirect costs are allocated on the basis of number of units produced or on

the basis of direct labor or the machine hours. The method involves identifying the indirect cost

related to the manufacturing process of the company on a regular basis (Tulsian, 2006).

The most significant advantage of the method is that it is relatively simple to be applied

as it is easy for the business managers to identify the indirect costs as per the products produced

or labor and machine hours consumed. The method also has a significant drawback that the

method is less reliable to be sued in the firms involved in manufacturing of large volume of few

products. This is because the increase in the amount of overhead expenses can increase the

chances of error occurrence in allocating the overhead costs to different products (Drury, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

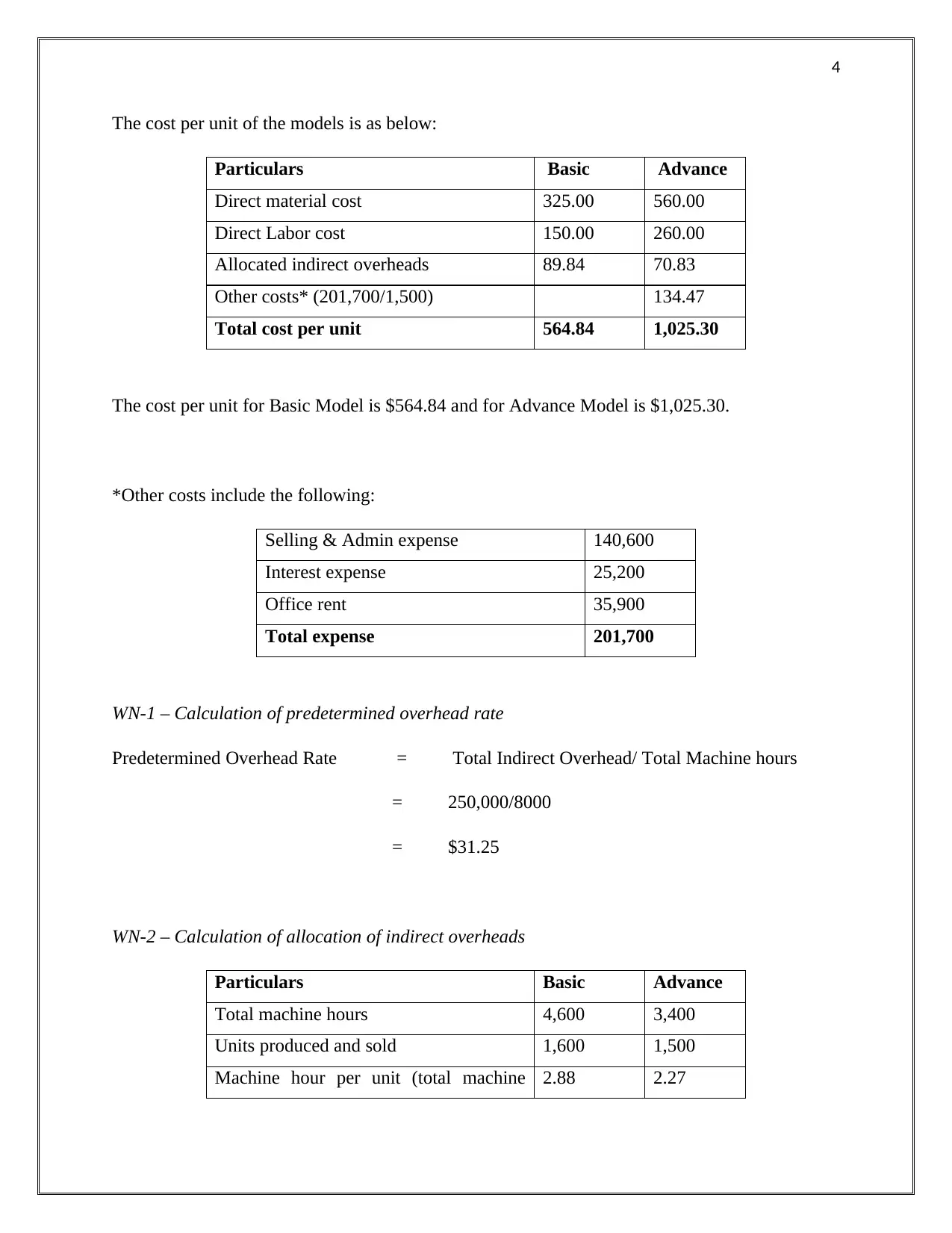

The cost per unit of the models is as below:

Particulars Basic Advance

Direct material cost 325.00 560.00

Direct Labor cost 150.00 260.00

Allocated indirect overheads 89.84 70.83

Other costs* (201,700/1,500) 134.47

Total cost per unit 564.84 1,025.30

The cost per unit for Basic Model is $564.84 and for Advance Model is $1,025.30.

*Other costs include the following:

Selling & Admin expense 140,600

Interest expense 25,200

Office rent 35,900

Total expense 201,700

WN-1 – Calculation of predetermined overhead rate

Predetermined Overhead Rate = Total Indirect Overhead/ Total Machine hours

= 250,000/8000

= $31.25

WN-2 – Calculation of allocation of indirect overheads

Particulars Basic Advance

Total machine hours 4,600 3,400

Units produced and sold 1,600 1,500

Machine hour per unit (total machine 2.88 2.27

The cost per unit of the models is as below:

Particulars Basic Advance

Direct material cost 325.00 560.00

Direct Labor cost 150.00 260.00

Allocated indirect overheads 89.84 70.83

Other costs* (201,700/1,500) 134.47

Total cost per unit 564.84 1,025.30

The cost per unit for Basic Model is $564.84 and for Advance Model is $1,025.30.

*Other costs include the following:

Selling & Admin expense 140,600

Interest expense 25,200

Office rent 35,900

Total expense 201,700

WN-1 – Calculation of predetermined overhead rate

Predetermined Overhead Rate = Total Indirect Overhead/ Total Machine hours

= 250,000/8000

= $31.25

WN-2 – Calculation of allocation of indirect overheads

Particulars Basic Advance

Total machine hours 4,600 3,400

Units produced and sold 1,600 1,500

Machine hour per unit (total machine 2.88 2.27

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

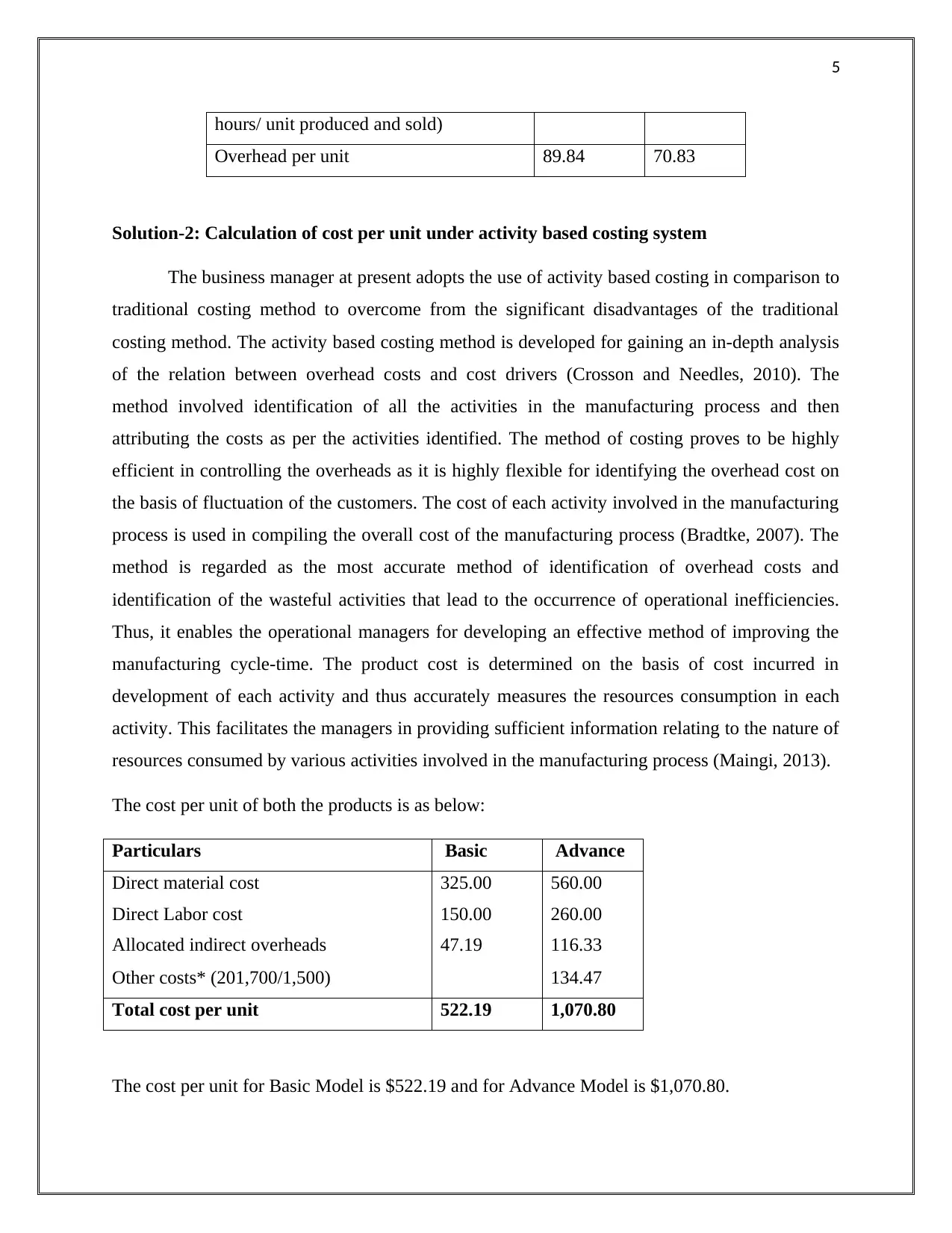

hours/ unit produced and sold)

Overhead per unit 89.84 70.83

Solution-2: Calculation of cost per unit under activity based costing system

The business manager at present adopts the use of activity based costing in comparison to

traditional costing method to overcome from the significant disadvantages of the traditional

costing method. The activity based costing method is developed for gaining an in-depth analysis

of the relation between overhead costs and cost drivers (Crosson and Needles, 2010). The

method involved identification of all the activities in the manufacturing process and then

attributing the costs as per the activities identified. The method of costing proves to be highly

efficient in controlling the overheads as it is highly flexible for identifying the overhead cost on

the basis of fluctuation of the customers. The cost of each activity involved in the manufacturing

process is used in compiling the overall cost of the manufacturing process (Bradtke, 2007). The

method is regarded as the most accurate method of identification of overhead costs and

identification of the wasteful activities that lead to the occurrence of operational inefficiencies.

Thus, it enables the operational managers for developing an effective method of improving the

manufacturing cycle-time. The product cost is determined on the basis of cost incurred in

development of each activity and thus accurately measures the resources consumption in each

activity. This facilitates the managers in providing sufficient information relating to the nature of

resources consumed by various activities involved in the manufacturing process (Maingi, 2013).

The cost per unit of both the products is as below:

Particulars Basic Advance

Direct material cost 325.00 560.00

Direct Labor cost 150.00 260.00

Allocated indirect overheads 47.19 116.33

Other costs* (201,700/1,500) 134.47

Total cost per unit 522.19 1,070.80

The cost per unit for Basic Model is $522.19 and for Advance Model is $1,070.80.

hours/ unit produced and sold)

Overhead per unit 89.84 70.83

Solution-2: Calculation of cost per unit under activity based costing system

The business manager at present adopts the use of activity based costing in comparison to

traditional costing method to overcome from the significant disadvantages of the traditional

costing method. The activity based costing method is developed for gaining an in-depth analysis

of the relation between overhead costs and cost drivers (Crosson and Needles, 2010). The

method involved identification of all the activities in the manufacturing process and then

attributing the costs as per the activities identified. The method of costing proves to be highly

efficient in controlling the overheads as it is highly flexible for identifying the overhead cost on

the basis of fluctuation of the customers. The cost of each activity involved in the manufacturing

process is used in compiling the overall cost of the manufacturing process (Bradtke, 2007). The

method is regarded as the most accurate method of identification of overhead costs and

identification of the wasteful activities that lead to the occurrence of operational inefficiencies.

Thus, it enables the operational managers for developing an effective method of improving the

manufacturing cycle-time. The product cost is determined on the basis of cost incurred in

development of each activity and thus accurately measures the resources consumption in each

activity. This facilitates the managers in providing sufficient information relating to the nature of

resources consumed by various activities involved in the manufacturing process (Maingi, 2013).

The cost per unit of both the products is as below:

Particulars Basic Advance

Direct material cost 325.00 560.00

Direct Labor cost 150.00 260.00

Allocated indirect overheads 47.19 116.33

Other costs* (201,700/1,500) 134.47

Total cost per unit 522.19 1,070.80

The cost per unit for Basic Model is $522.19 and for Advance Model is $1,070.80.

6

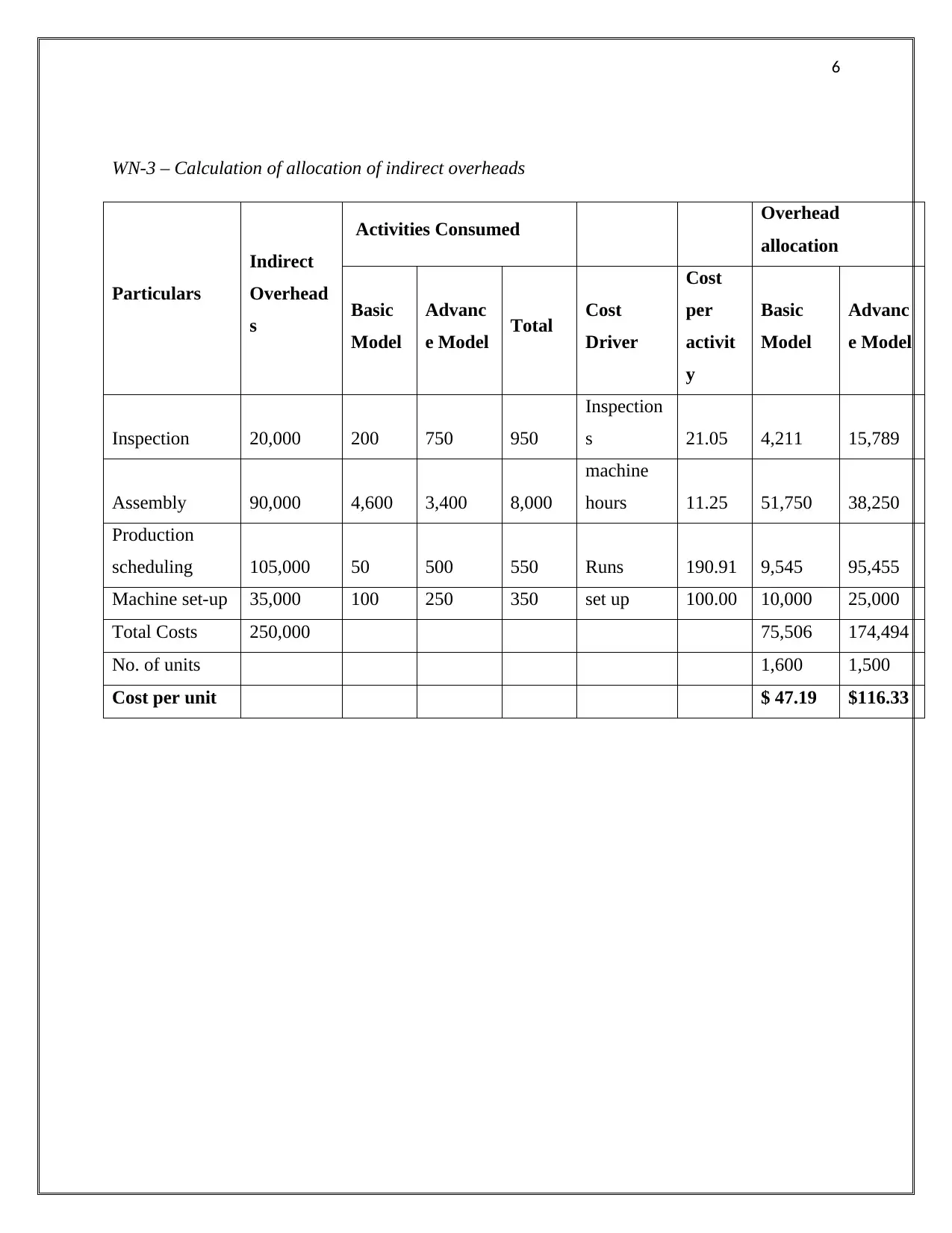

WN-3 – Calculation of allocation of indirect overheads

Particulars

Indirect

Overhead

s

Activities Consumed Overhead

allocation

Basic

Model

Advanc

e Model Total Cost

Driver

Cost

per

activit

y

Basic

Model

Advanc

e Model

Inspection 20,000 200 750 950

Inspection

s 21.05 4,211 15,789

Assembly 90,000 4,600 3,400 8,000

machine

hours 11.25 51,750 38,250

Production

scheduling 105,000 50 500 550 Runs 190.91 9,545 95,455

Machine set-up 35,000 100 250 350 set up 100.00 10,000 25,000

Total Costs 250,000 75,506 174,494

No. of units 1,600 1,500

Cost per unit $ 47.19 $116.33

WN-3 – Calculation of allocation of indirect overheads

Particulars

Indirect

Overhead

s

Activities Consumed Overhead

allocation

Basic

Model

Advanc

e Model Total Cost

Driver

Cost

per

activit

y

Basic

Model

Advanc

e Model

Inspection 20,000 200 750 950

Inspection

s 21.05 4,211 15,789

Assembly 90,000 4,600 3,400 8,000

machine

hours 11.25 51,750 38,250

Production

scheduling 105,000 50 500 550 Runs 190.91 9,545 95,455

Machine set-up 35,000 100 250 350 set up 100.00 10,000 25,000

Total Costs 250,000 75,506 174,494

No. of units 1,600 1,500

Cost per unit $ 47.19 $116.33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

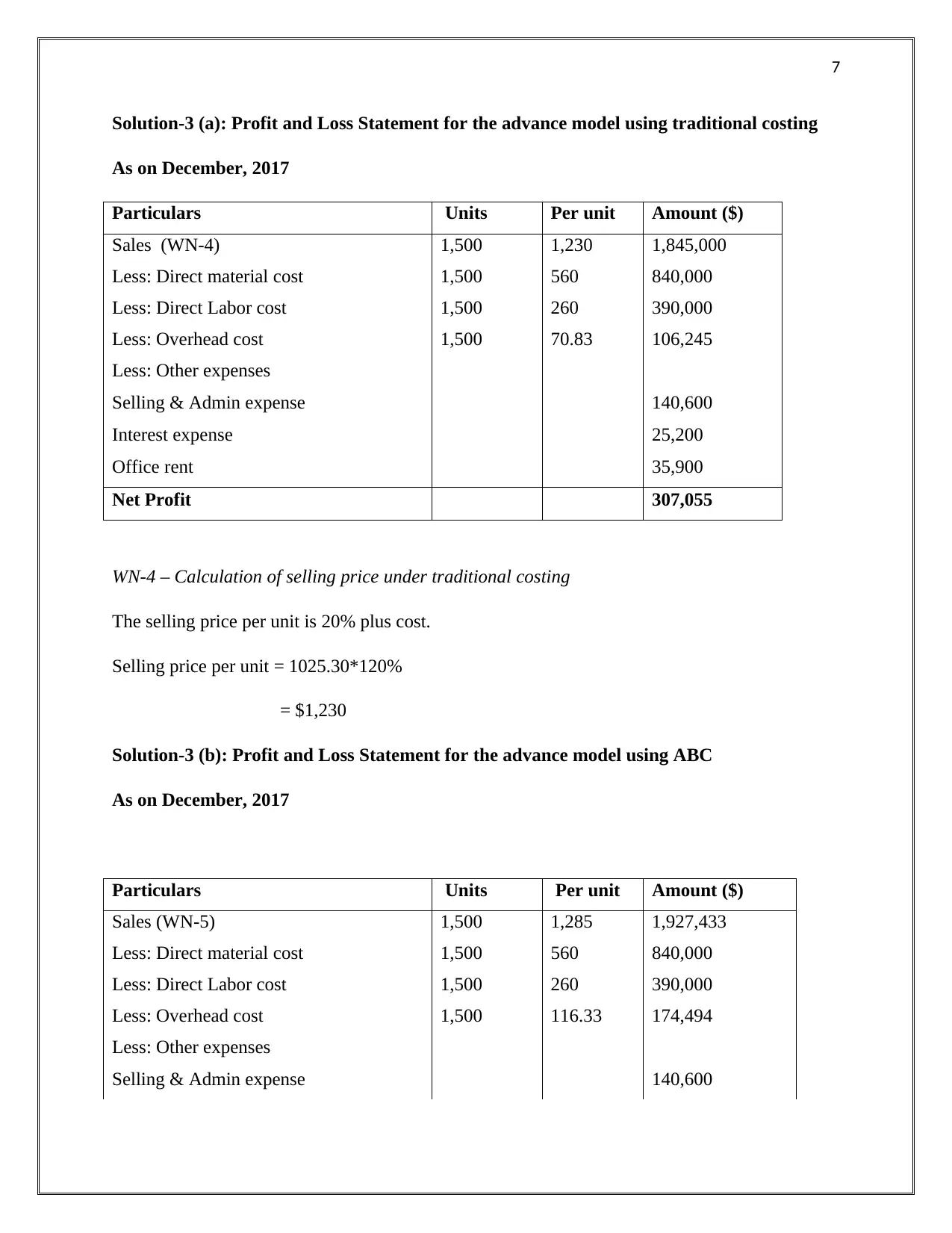

Solution-3 (a): Profit and Loss Statement for the advance model using traditional costing

As on December, 2017

Particulars Units Per unit Amount ($)

Sales (WN-4) 1,500 1,230 1,845,000

Less: Direct material cost 1,500 560 840,000

Less: Direct Labor cost 1,500 260 390,000

Less: Overhead cost 1,500 70.83 106,245

Less: Other expenses

Selling & Admin expense 140,600

Interest expense 25,200

Office rent 35,900

Net Profit 307,055

WN-4 – Calculation of selling price under traditional costing

The selling price per unit is 20% plus cost.

Selling price per unit = 1025.30*120%

= $1,230

Solution-3 (b): Profit and Loss Statement for the advance model using ABC

As on December, 2017

Particulars Units Per unit Amount ($)

Sales (WN-5) 1,500 1,285 1,927,433

Less: Direct material cost 1,500 560 840,000

Less: Direct Labor cost 1,500 260 390,000

Less: Overhead cost 1,500 116.33 174,494

Less: Other expenses

Selling & Admin expense 140,600

Solution-3 (a): Profit and Loss Statement for the advance model using traditional costing

As on December, 2017

Particulars Units Per unit Amount ($)

Sales (WN-4) 1,500 1,230 1,845,000

Less: Direct material cost 1,500 560 840,000

Less: Direct Labor cost 1,500 260 390,000

Less: Overhead cost 1,500 70.83 106,245

Less: Other expenses

Selling & Admin expense 140,600

Interest expense 25,200

Office rent 35,900

Net Profit 307,055

WN-4 – Calculation of selling price under traditional costing

The selling price per unit is 20% plus cost.

Selling price per unit = 1025.30*120%

= $1,230

Solution-3 (b): Profit and Loss Statement for the advance model using ABC

As on December, 2017

Particulars Units Per unit Amount ($)

Sales (WN-5) 1,500 1,285 1,927,433

Less: Direct material cost 1,500 560 840,000

Less: Direct Labor cost 1,500 260 390,000

Less: Overhead cost 1,500 116.33 174,494

Less: Other expenses

Selling & Admin expense 140,600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

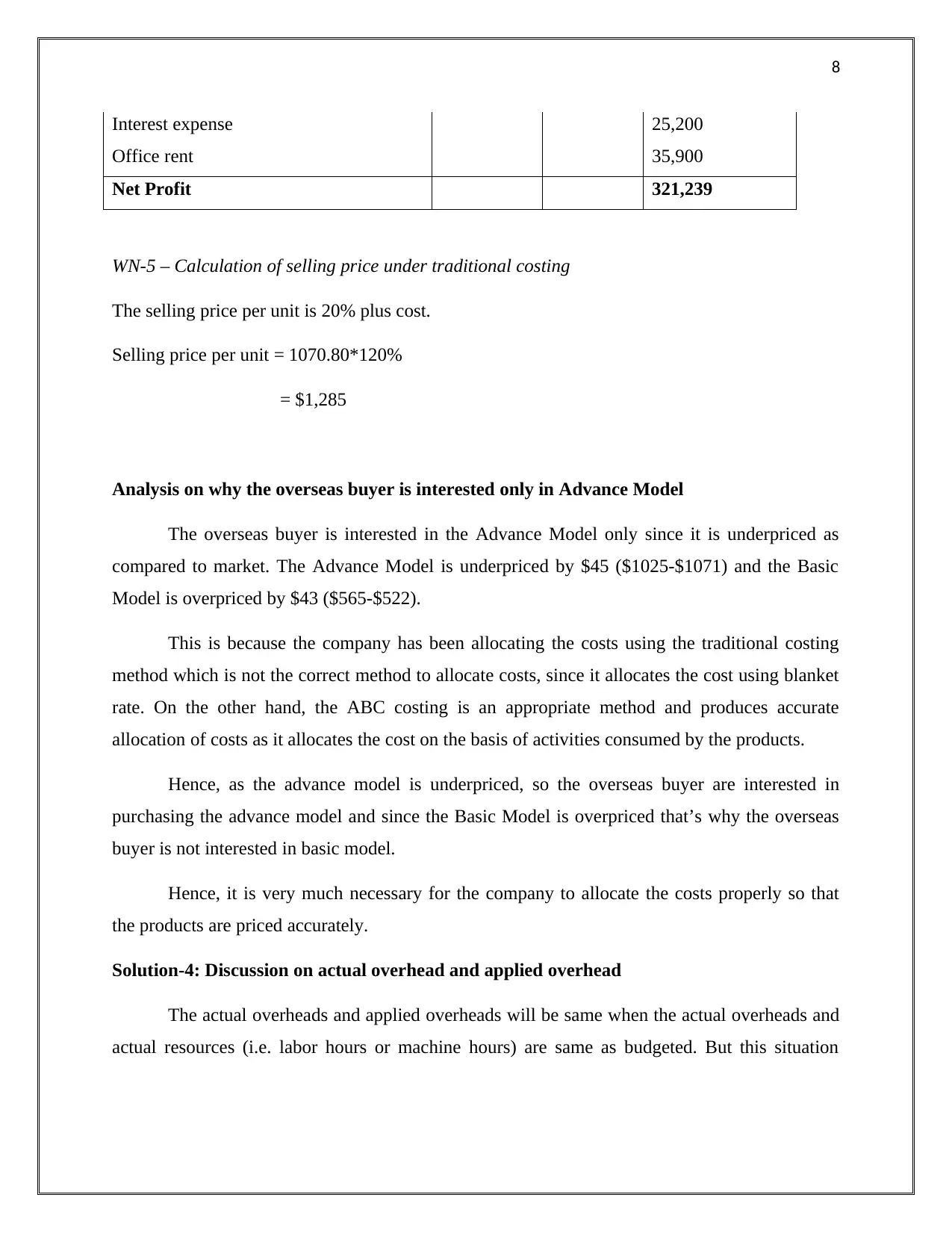

Interest expense 25,200

Office rent 35,900

Net Profit 321,239

WN-5 – Calculation of selling price under traditional costing

The selling price per unit is 20% plus cost.

Selling price per unit = 1070.80*120%

= $1,285

Analysis on why the overseas buyer is interested only in Advance Model

The overseas buyer is interested in the Advance Model only since it is underpriced as

compared to market. The Advance Model is underpriced by $45 ($1025-$1071) and the Basic

Model is overpriced by $43 ($565-$522).

This is because the company has been allocating the costs using the traditional costing

method which is not the correct method to allocate costs, since it allocates the cost using blanket

rate. On the other hand, the ABC costing is an appropriate method and produces accurate

allocation of costs as it allocates the cost on the basis of activities consumed by the products.

Hence, as the advance model is underpriced, so the overseas buyer are interested in

purchasing the advance model and since the Basic Model is overpriced that’s why the overseas

buyer is not interested in basic model.

Hence, it is very much necessary for the company to allocate the costs properly so that

the products are priced accurately.

Solution-4: Discussion on actual overhead and applied overhead

The actual overheads and applied overheads will be same when the actual overheads and

actual resources (i.e. labor hours or machine hours) are same as budgeted. But this situation

Interest expense 25,200

Office rent 35,900

Net Profit 321,239

WN-5 – Calculation of selling price under traditional costing

The selling price per unit is 20% plus cost.

Selling price per unit = 1070.80*120%

= $1,285

Analysis on why the overseas buyer is interested only in Advance Model

The overseas buyer is interested in the Advance Model only since it is underpriced as

compared to market. The Advance Model is underpriced by $45 ($1025-$1071) and the Basic

Model is overpriced by $43 ($565-$522).

This is because the company has been allocating the costs using the traditional costing

method which is not the correct method to allocate costs, since it allocates the cost using blanket

rate. On the other hand, the ABC costing is an appropriate method and produces accurate

allocation of costs as it allocates the cost on the basis of activities consumed by the products.

Hence, as the advance model is underpriced, so the overseas buyer are interested in

purchasing the advance model and since the Basic Model is overpriced that’s why the overseas

buyer is not interested in basic model.

Hence, it is very much necessary for the company to allocate the costs properly so that

the products are priced accurately.

Solution-4: Discussion on actual overhead and applied overhead

The actual overheads and applied overheads will be same when the actual overheads and

actual resources (i.e. labor hours or machine hours) are same as budgeted. But this situation

9

happens very rarely as there is always difference between the budgeted and actual overheads and

budgeted and actual resources consumed.

The three ways to deal with over or under applied overheads are:

One way is to calculate a supplementary rate of the difference between actual and applied

overheads. Then this difference is charged to the products.

Second way is to write off the difference of applied and actual overheads in the profit and

loss account.

The last way is to carry forward the difference of actual and applied overheads in the next

year.

Solution-5: Benefits and Limitations of Activity based costing system

Activity based costing method is a popular and most used methods for the cost allocation.

It has the following advantages (Your Article Library, 2018):

(a) The ABC method allocates the costs on a systematic basis and hence the product costs

are generally accurate and error free.

(b) Since, the allocation of costs is correct and error free, the product cost or selling price

assigned to the products is also correct.

(c) ABC is best for the organizations having multiple products and various indirect

overheads. As it involves systematicallocation of overheads by allocating the costs to the

activities and mapping those activities with the cost drivers.

(d) It helps the management in managing the costs. As it gives the clear picture of costs and

there related activities, the management can easily identify the performing activities or

divisions and non-performing activities and division. On the basis of this information, the

management can take various decisions.

The disadvantages of ABC are as below (Money Matters | All Management Articles, 2018):

(a) The ABC method is very costly system for its implementation as it involves through

understanding of the process and identifying the related costs and cost drivers.

(b) Since, it is a costly system, it is not advisable for smaller firms.

happens very rarely as there is always difference between the budgeted and actual overheads and

budgeted and actual resources consumed.

The three ways to deal with over or under applied overheads are:

One way is to calculate a supplementary rate of the difference between actual and applied

overheads. Then this difference is charged to the products.

Second way is to write off the difference of applied and actual overheads in the profit and

loss account.

The last way is to carry forward the difference of actual and applied overheads in the next

year.

Solution-5: Benefits and Limitations of Activity based costing system

Activity based costing method is a popular and most used methods for the cost allocation.

It has the following advantages (Your Article Library, 2018):

(a) The ABC method allocates the costs on a systematic basis and hence the product costs

are generally accurate and error free.

(b) Since, the allocation of costs is correct and error free, the product cost or selling price

assigned to the products is also correct.

(c) ABC is best for the organizations having multiple products and various indirect

overheads. As it involves systematicallocation of overheads by allocating the costs to the

activities and mapping those activities with the cost drivers.

(d) It helps the management in managing the costs. As it gives the clear picture of costs and

there related activities, the management can easily identify the performing activities or

divisions and non-performing activities and division. On the basis of this information, the

management can take various decisions.

The disadvantages of ABC are as below (Money Matters | All Management Articles, 2018):

(a) The ABC method is very costly system for its implementation as it involves through

understanding of the process and identifying the related costs and cost drivers.

(b) Since, it is a costly system, it is not advisable for smaller firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

(c) It is a complicated system to understand, and only the professionals or high level people

can understand this. Hence, specialized knowledge or professionals are required for

implementation and use of ABC.

Conclusion

It has been found on the basis of overall analysis that traditional costing system does not

accurate cost allocation and also leads to wrong decision making. Under traditional costing

system one can face issue of over pricing or under pricing of products as overheads is divided

using single recovery rate without giving effect of actual resources (activity consumption) by

each product. This create many issues while making the decision of profitability provided by

each product as traditional costing does not give any actual profit provided by each product. On

the contrast activity based costing method uses actual consumption of resources used by each

product to allocate the overhead costs. Activity based costing helps to ascertain overhead rate of

each activity in order to allocate each overhead cost to each product on the basis of actual

consumption of activity in production of each product.

(c) It is a complicated system to understand, and only the professionals or high level people

can understand this. Hence, specialized knowledge or professionals are required for

implementation and use of ABC.

Conclusion

It has been found on the basis of overall analysis that traditional costing system does not

accurate cost allocation and also leads to wrong decision making. Under traditional costing

system one can face issue of over pricing or under pricing of products as overheads is divided

using single recovery rate without giving effect of actual resources (activity consumption) by

each product. This create many issues while making the decision of profitability provided by

each product as traditional costing does not give any actual profit provided by each product. On

the contrast activity based costing method uses actual consumption of resources used by each

product to allocate the overhead costs. Activity based costing helps to ascertain overhead rate of

each activity in order to allocate each overhead cost to each product on the basis of actual

consumption of activity in production of each product.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Bradtke, D. 2007. Activity-Based-Costing. GRIN Verlag.

Crosson, S. and Needles, B. 2010. Managerial Accounting. Cengage Learning.

Drury, C. 2008. Management and Cost Accounting. Cengage Learning EMEA.

Maingi, J. 2013. Advantages & Disadvantages of activity based costing with reference to

economic value addition. GRIN Verlag.

Money Matters: All Management Articles. 2018. Advantages and Disadvantages of Activity

Based Costing. [Online] Available at: https://accountlearning.com/advantages-and-

disadvantages-of-activity-based-costing/ [Accessed on: 9 May 2018].

Referenceforbusiness.com. 2018. Activity-Based Costing - type, benefits, How activity-based

costing works. [Online] Available at: http://www.referenceforbusiness.com/small/A-Bo/Activity-

Based-Costing.html [Accessed on: 11 May 2018].

Tulsian. 2006. Cost Accounting. Tata McGraw-Hill Education.

Your Article Library. 2018. Advantages and Demerits of Activity Based Costing (ABC).

[Online] Available at: http://www.yourarticlelibrary.com/accounting/costing/advantages-and-

demerits-of-activity-based-costing-abc/52617 [Accessed on: 9 May 2018].

References

Bradtke, D. 2007. Activity-Based-Costing. GRIN Verlag.

Crosson, S. and Needles, B. 2010. Managerial Accounting. Cengage Learning.

Drury, C. 2008. Management and Cost Accounting. Cengage Learning EMEA.

Maingi, J. 2013. Advantages & Disadvantages of activity based costing with reference to

economic value addition. GRIN Verlag.

Money Matters: All Management Articles. 2018. Advantages and Disadvantages of Activity

Based Costing. [Online] Available at: https://accountlearning.com/advantages-and-

disadvantages-of-activity-based-costing/ [Accessed on: 9 May 2018].

Referenceforbusiness.com. 2018. Activity-Based Costing - type, benefits, How activity-based

costing works. [Online] Available at: http://www.referenceforbusiness.com/small/A-Bo/Activity-

Based-Costing.html [Accessed on: 11 May 2018].

Tulsian. 2006. Cost Accounting. Tata McGraw-Hill Education.

Your Article Library. 2018. Advantages and Demerits of Activity Based Costing (ABC).

[Online] Available at: http://www.yourarticlelibrary.com/accounting/costing/advantages-and-

demerits-of-activity-based-costing-abc/52617 [Accessed on: 9 May 2018].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.