Financial Analysis and Investment Strategies for Trainline

VerifiedAdded on 2020/02/12

|15

|3988

|332

Report

AI Summary

This report provides a comprehensive financial analysis of Trainline, a small-sized business in the railway ticket and distribution sector. The analysis includes a critical evaluation of Trainline's financial performance over a five-year period using ratio analysis, covering profitability, liquidity, efficiency, and solvency ratios. The report also assesses various sources of finance, comparing the benefits of equity and long-term borrowing, and suggests techniques for evaluating investment proposals, such as the payback period and net present value (NPV) methods. Furthermore, the report examines the entrepreneurial ecosystem and business development aspects relevant to Trainline, along with ethical considerations for an Initial Public Offering (IPO). The findings offer insights into Trainline's financial health and potential strategies for future growth, providing valuable information for financial planning and management within the SME context.

FINANCE IN SME CONTEXT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question 1: Critical analysis of Trainline’s performance using ratio analysis for 5 years..........3

Question 2: Critical evaluation of sources of finance and techniques for investment proposal. .7

Question 3 Sources of finance and investment of project............................................................8

Question 4 Entrepreneurial ecosystem and business development............................................10

Question 5 Ethical consideration for IPO..................................................................................11

CONCLUSION..............................................................................................................................12

REFERNCES.................................................................................................................................13

APPENDIX....................................................................................................................................15

Ratio analysis.............................................................................................................................15

INTRODUCTION...........................................................................................................................3

Question 1: Critical analysis of Trainline’s performance using ratio analysis for 5 years..........3

Question 2: Critical evaluation of sources of finance and techniques for investment proposal. .7

Question 3 Sources of finance and investment of project............................................................8

Question 4 Entrepreneurial ecosystem and business development............................................10

Question 5 Ethical consideration for IPO..................................................................................11

CONCLUSION..............................................................................................................................12

REFERNCES.................................................................................................................................13

APPENDIX....................................................................................................................................15

Ratio analysis.............................................................................................................................15

INTRODUCTION

Finance is not only a crucial element required for the large business enterprises only, it is

equally important for the small and medium sized corporations as they need capital for the

continual of their regular operation, expansion and growth plans and taking the benefits of

market opportunities. Trainline is a small sized business that executes various operations such as

sale of railway tickets, distribution, information delivery and other ancillary services associated

with the railway journey. The present project will examine business performance and financial

status of the Trainline computing ratios for a period of 5 years. Moreover, budgeting is also an

essential element of financial planning for the purpose of forecasting, therefore, the report will

also prepare cash budgeting for the projection of future years cash position for 2017, 2018 &

2019. In addition to this, various financial sources will be critically evaluated and the techniques

for evaluation of investment proposal will be suggested to the Trainline. Lastly, ethical

consideration and ecosystem of the business will be analyzed for fulfilling environmental

responsibilities.

Question 1: Critical analysis of Trainline’s performance using ratio analysis for 5 years

Profitability performance:

2012 2013 2014 2015 2016

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

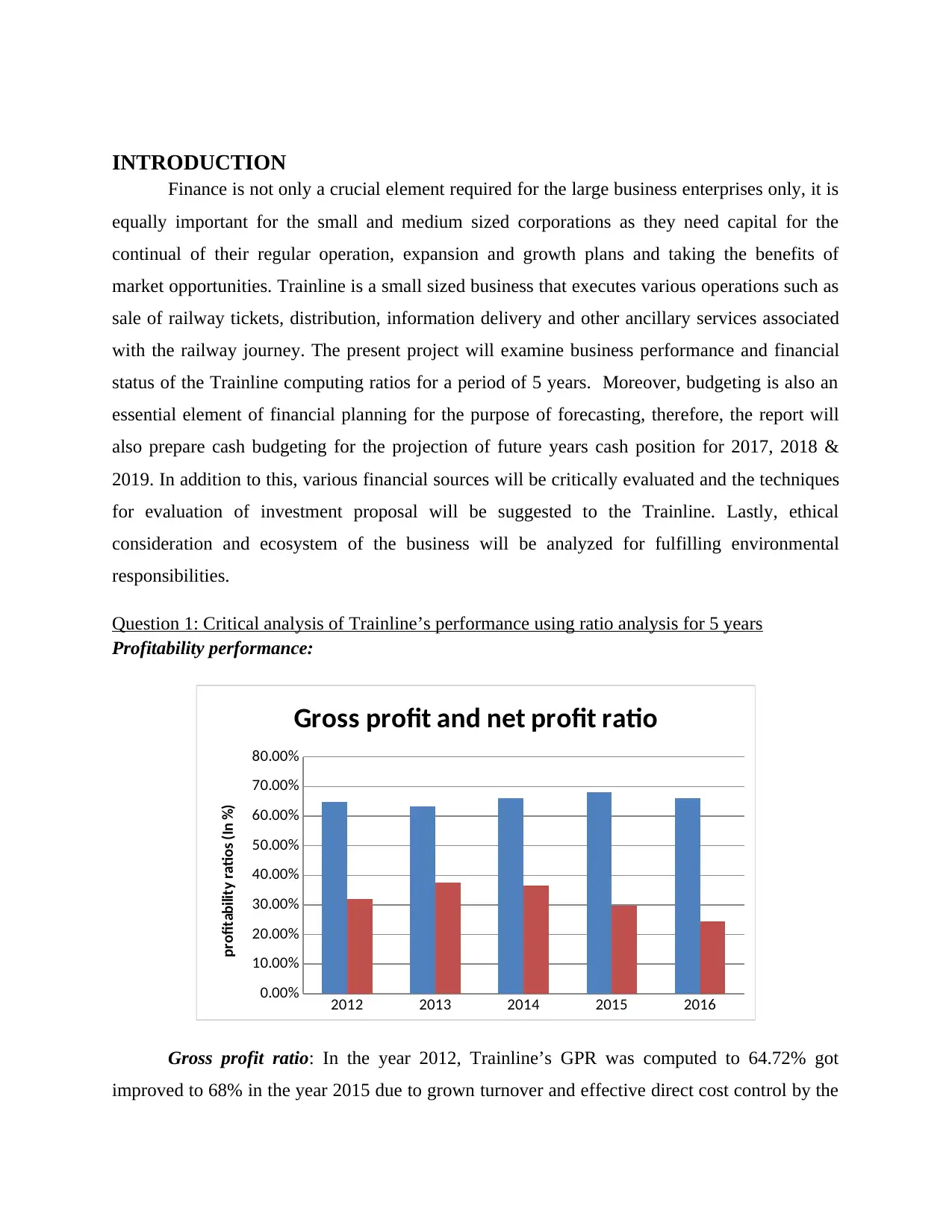

Gross profit and net profit ratio

profitability ratios (In %)

Gross profit ratio: In the year 2012, Trainline’s GPR was computed to 64.72% got

improved to 68% in the year 2015 due to grown turnover and effective direct cost control by the

Finance is not only a crucial element required for the large business enterprises only, it is

equally important for the small and medium sized corporations as they need capital for the

continual of their regular operation, expansion and growth plans and taking the benefits of

market opportunities. Trainline is a small sized business that executes various operations such as

sale of railway tickets, distribution, information delivery and other ancillary services associated

with the railway journey. The present project will examine business performance and financial

status of the Trainline computing ratios for a period of 5 years. Moreover, budgeting is also an

essential element of financial planning for the purpose of forecasting, therefore, the report will

also prepare cash budgeting for the projection of future years cash position for 2017, 2018 &

2019. In addition to this, various financial sources will be critically evaluated and the techniques

for evaluation of investment proposal will be suggested to the Trainline. Lastly, ethical

consideration and ecosystem of the business will be analyzed for fulfilling environmental

responsibilities.

Question 1: Critical analysis of Trainline’s performance using ratio analysis for 5 years

Profitability performance:

2012 2013 2014 2015 2016

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Gross profit and net profit ratio

profitability ratios (In %)

Gross profit ratio: In the year 2012, Trainline’s GPR was computed to 64.72% got

improved to 68% in the year 2015 due to grown turnover and effective direct cost control by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm. High GPR indicates that business performed excellent and generated greater return on their

total turnover (Islam, Alam and Hossain, 2014). In contrast, in the last year 2016, it turned down

to 65.95% due to higher increase in the cost of sale by 21.72% in comparison to the increase in

sales performance by 14.39% due to acquisition of Captain Train due a leading digital ticket

retailer. On the basis of it, it can be suggested to the Trainline to create optimum and excellent

pricing decisions for their tickets and create new revenue stream for achieving success.

Net profit ratio: This ratio measures net profitability performance of the Trainline

generated by exceeding the total sales over total payments made. In 2012, NPR was 32.12%

increased to 37.61% in the following year, and thereafter, it shows a consistent decline and in the

final year, it came down to 24.47%. YOY growth by administrative expenditures by 6.85%,

10.95% and 29.19% is the main reason behind lower net return to the firm (Goldmann, 2017). In

addition to this, in 2013, interest income gone up by 35.11% and thereafter it came down by

26.71%, 43.45% and in the last year, it shows a little bit improvement by 15.43%. Therefore, it

can be suggested to the Trainline to put excellent cost-controlling measures and better pricing

decisions for getting better yield.

Liquidity performance:

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

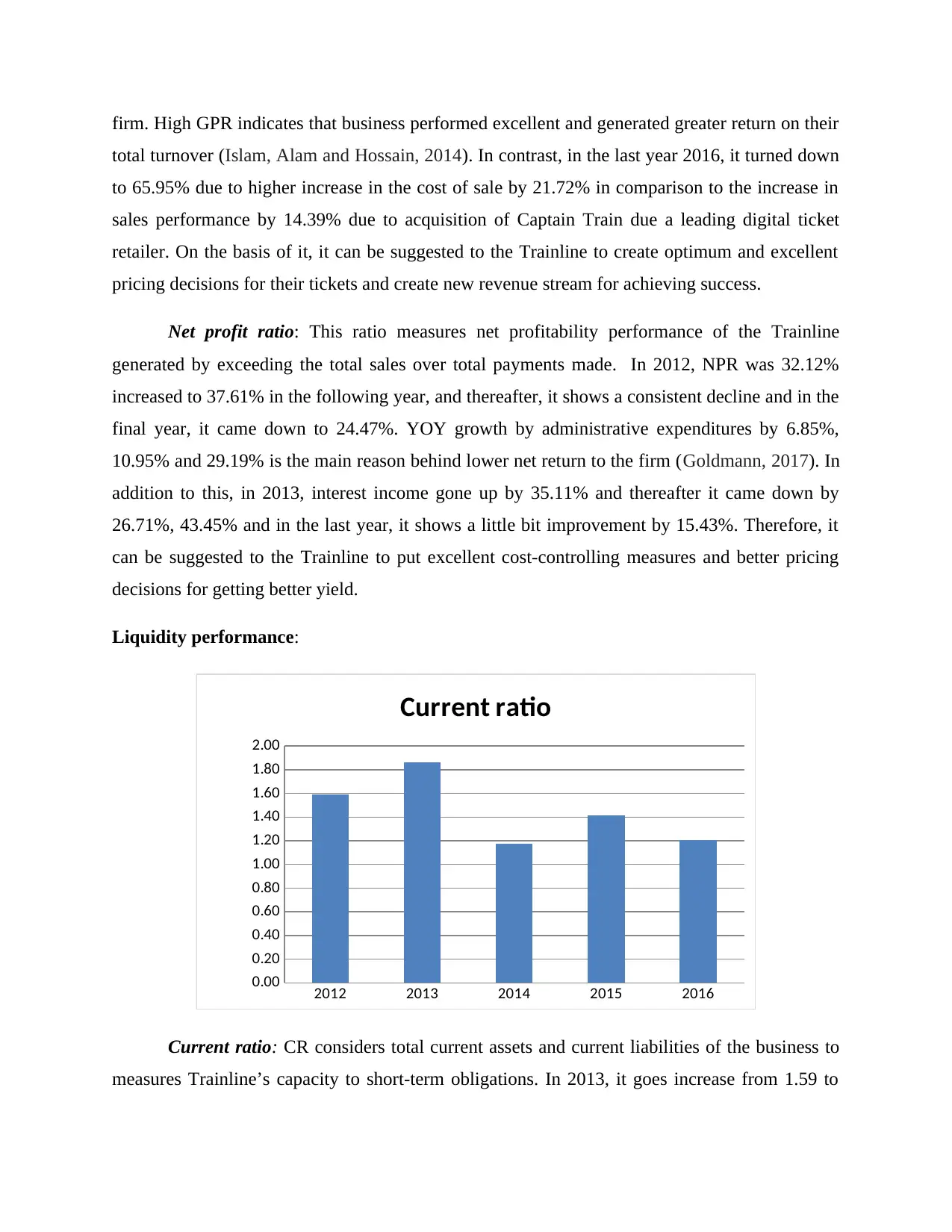

Current ratio

Current ratio: CR considers total current assets and current liabilities of the business to

measures Trainline’s capacity to short-term obligations. In 2013, it goes increase from 1.59 to

total turnover (Islam, Alam and Hossain, 2014). In contrast, in the last year 2016, it turned down

to 65.95% due to higher increase in the cost of sale by 21.72% in comparison to the increase in

sales performance by 14.39% due to acquisition of Captain Train due a leading digital ticket

retailer. On the basis of it, it can be suggested to the Trainline to create optimum and excellent

pricing decisions for their tickets and create new revenue stream for achieving success.

Net profit ratio: This ratio measures net profitability performance of the Trainline

generated by exceeding the total sales over total payments made. In 2012, NPR was 32.12%

increased to 37.61% in the following year, and thereafter, it shows a consistent decline and in the

final year, it came down to 24.47%. YOY growth by administrative expenditures by 6.85%,

10.95% and 29.19% is the main reason behind lower net return to the firm (Goldmann, 2017). In

addition to this, in 2013, interest income gone up by 35.11% and thereafter it came down by

26.71%, 43.45% and in the last year, it shows a little bit improvement by 15.43%. Therefore, it

can be suggested to the Trainline to put excellent cost-controlling measures and better pricing

decisions for getting better yield.

Liquidity performance:

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Current ratio

Current ratio: CR considers total current assets and current liabilities of the business to

measures Trainline’s capacity to short-term obligations. In 2013, it goes increase from 1.59 to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

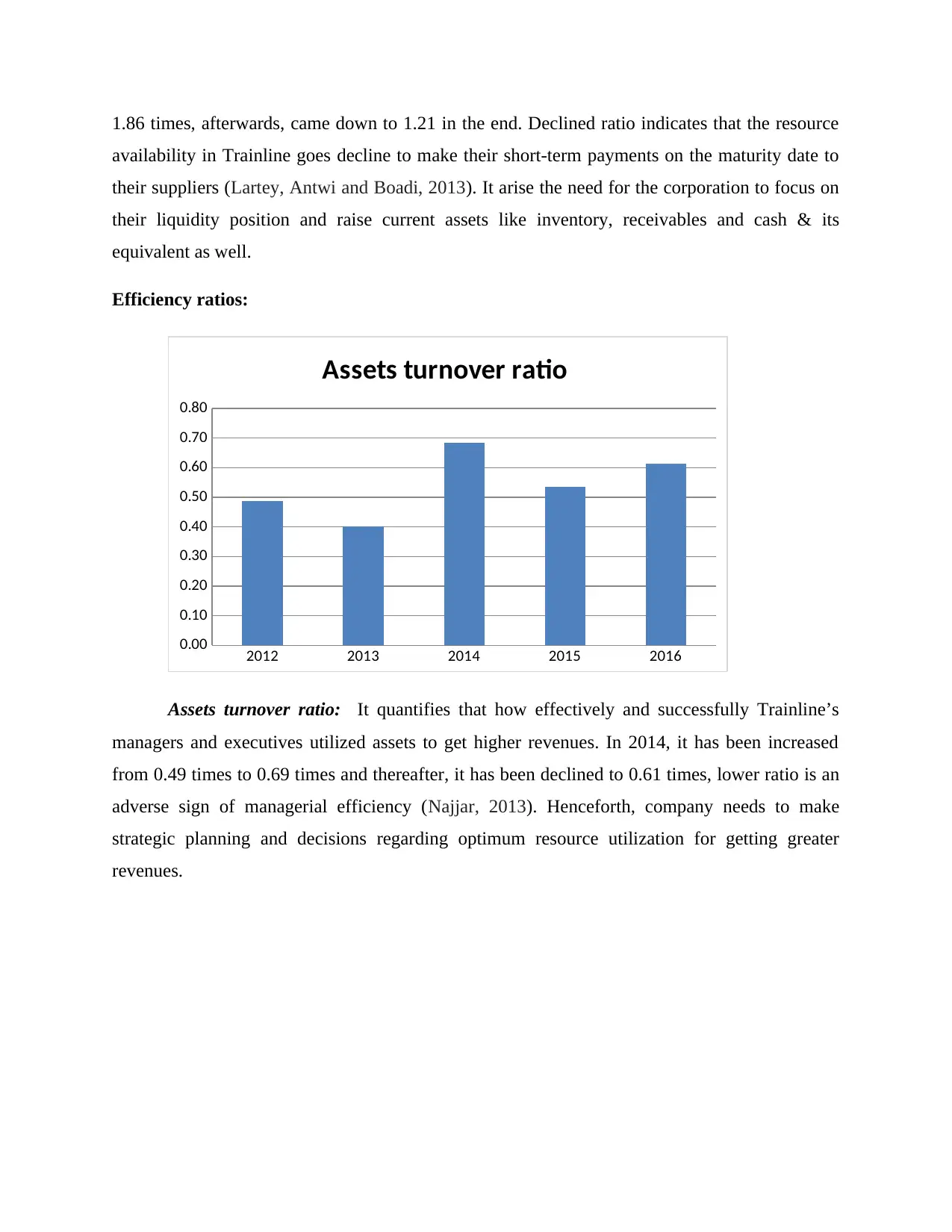

1.86 times, afterwards, came down to 1.21 in the end. Declined ratio indicates that the resource

availability in Trainline goes decline to make their short-term payments on the maturity date to

their suppliers (Lartey, Antwi and Boadi, 2013). It arise the need for the corporation to focus on

their liquidity position and raise current assets like inventory, receivables and cash & its

equivalent as well.

Efficiency ratios:

2012 2013 2014 2015 2016

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Assets turnover ratio

Assets turnover ratio: It quantifies that how effectively and successfully Trainline’s

managers and executives utilized assets to get higher revenues. In 2014, it has been increased

from 0.49 times to 0.69 times and thereafter, it has been declined to 0.61 times, lower ratio is an

adverse sign of managerial efficiency (Najjar, 2013). Henceforth, company needs to make

strategic planning and decisions regarding optimum resource utilization for getting greater

revenues.

availability in Trainline goes decline to make their short-term payments on the maturity date to

their suppliers (Lartey, Antwi and Boadi, 2013). It arise the need for the corporation to focus on

their liquidity position and raise current assets like inventory, receivables and cash & its

equivalent as well.

Efficiency ratios:

2012 2013 2014 2015 2016

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Assets turnover ratio

Assets turnover ratio: It quantifies that how effectively and successfully Trainline’s

managers and executives utilized assets to get higher revenues. In 2014, it has been increased

from 0.49 times to 0.69 times and thereafter, it has been declined to 0.61 times, lower ratio is an

adverse sign of managerial efficiency (Najjar, 2013). Henceforth, company needs to make

strategic planning and decisions regarding optimum resource utilization for getting greater

revenues.

2012 2013 2014 2015 2016

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

1600.00

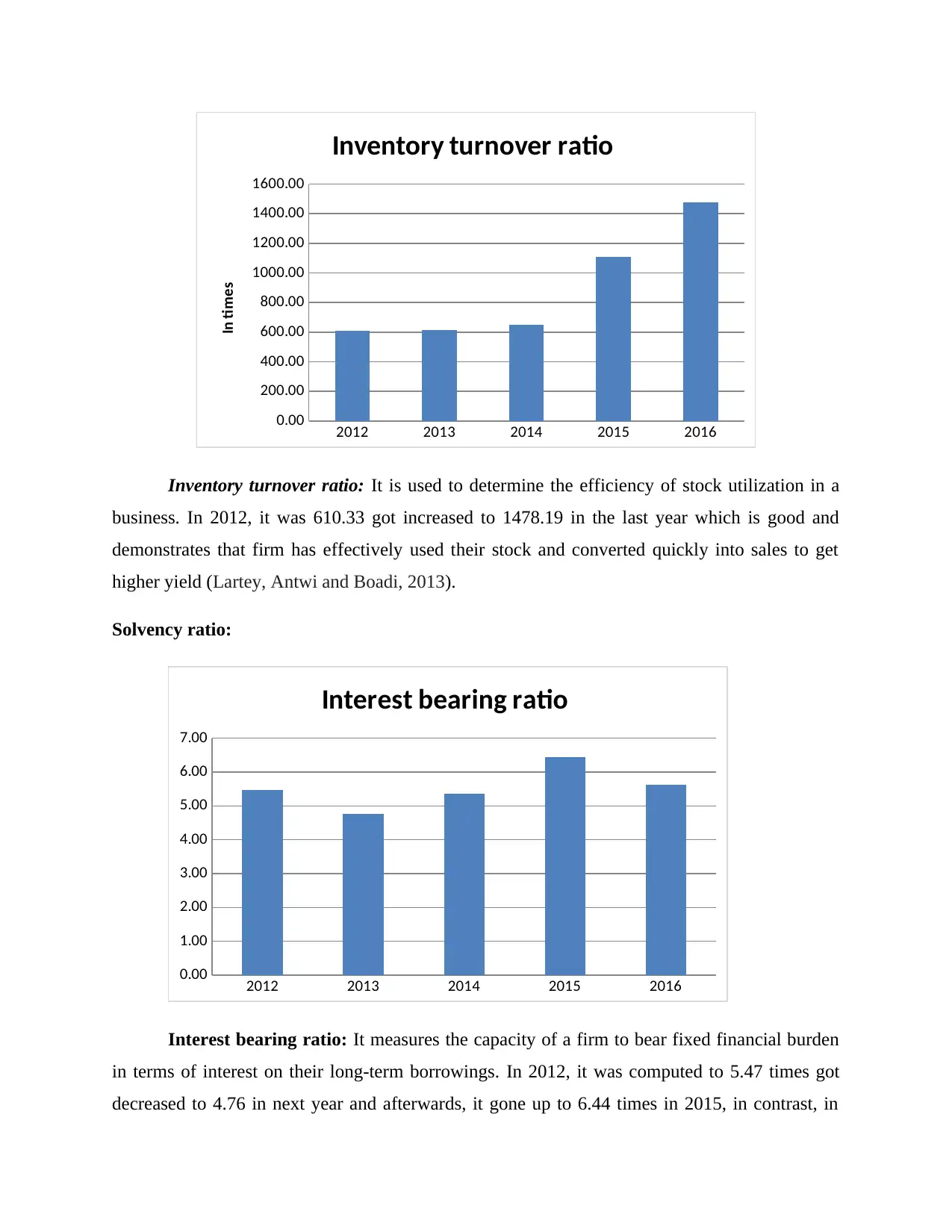

Inventory turnover ratio

In times

Inventory turnover ratio: It is used to determine the efficiency of stock utilization in a

business. In 2012, it was 610.33 got increased to 1478.19 in the last year which is good and

demonstrates that firm has effectively used their stock and converted quickly into sales to get

higher yield (Lartey, Antwi and Boadi, 2013).

Solvency ratio:

2012 2013 2014 2015 2016

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

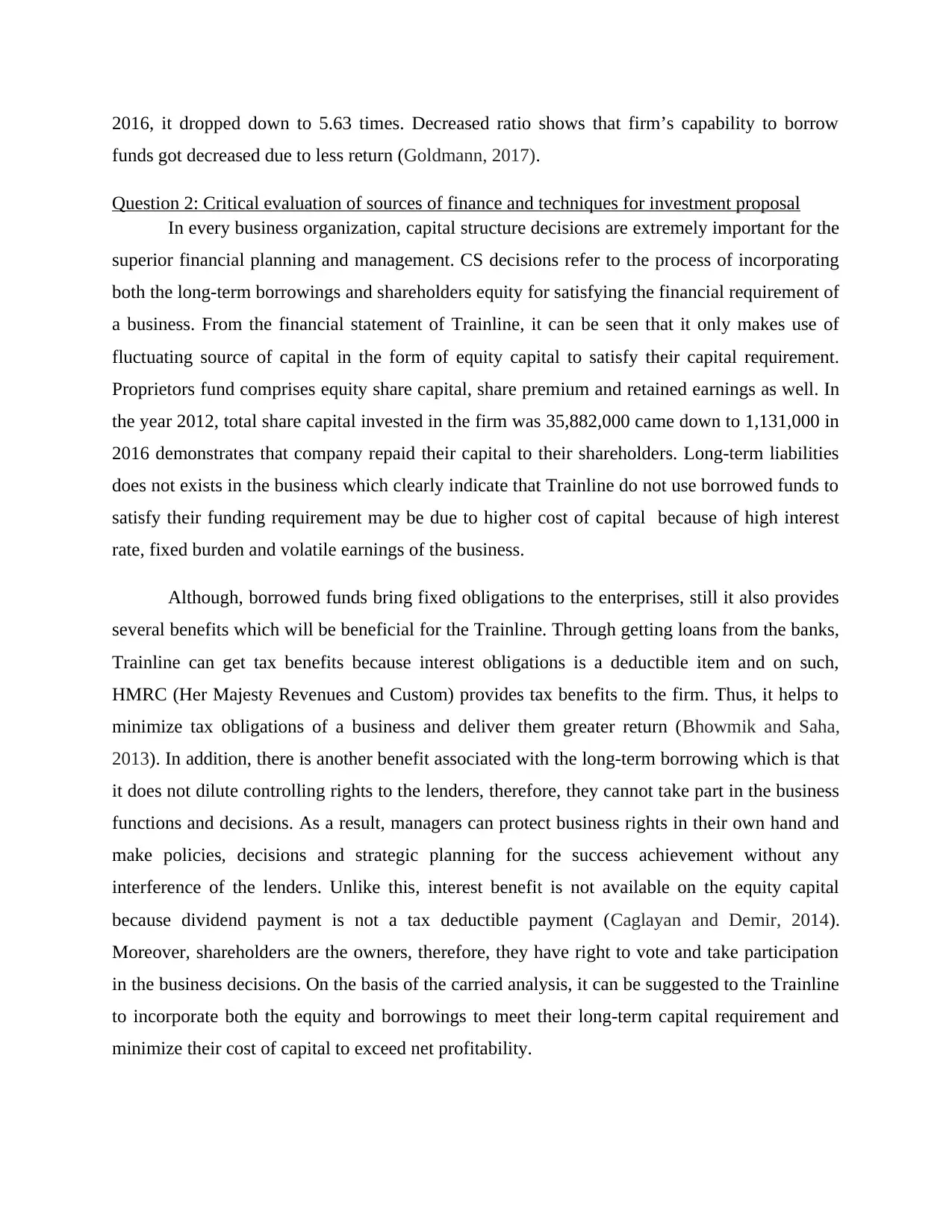

Interest bearing ratio

Interest bearing ratio: It measures the capacity of a firm to bear fixed financial burden

in terms of interest on their long-term borrowings. In 2012, it was computed to 5.47 times got

decreased to 4.76 in next year and afterwards, it gone up to 6.44 times in 2015, in contrast, in

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

1600.00

Inventory turnover ratio

In times

Inventory turnover ratio: It is used to determine the efficiency of stock utilization in a

business. In 2012, it was 610.33 got increased to 1478.19 in the last year which is good and

demonstrates that firm has effectively used their stock and converted quickly into sales to get

higher yield (Lartey, Antwi and Boadi, 2013).

Solvency ratio:

2012 2013 2014 2015 2016

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Interest bearing ratio

Interest bearing ratio: It measures the capacity of a firm to bear fixed financial burden

in terms of interest on their long-term borrowings. In 2012, it was computed to 5.47 times got

decreased to 4.76 in next year and afterwards, it gone up to 6.44 times in 2015, in contrast, in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016, it dropped down to 5.63 times. Decreased ratio shows that firm’s capability to borrow

funds got decreased due to less return (Goldmann, 2017).

Question 2: Critical evaluation of sources of finance and techniques for investment proposal

In every business organization, capital structure decisions are extremely important for the

superior financial planning and management. CS decisions refer to the process of incorporating

both the long-term borrowings and shareholders equity for satisfying the financial requirement of

a business. From the financial statement of Trainline, it can be seen that it only makes use of

fluctuating source of capital in the form of equity capital to satisfy their capital requirement.

Proprietors fund comprises equity share capital, share premium and retained earnings as well. In

the year 2012, total share capital invested in the firm was 35,882,000 came down to 1,131,000 in

2016 demonstrates that company repaid their capital to their shareholders. Long-term liabilities

does not exists in the business which clearly indicate that Trainline do not use borrowed funds to

satisfy their funding requirement may be due to higher cost of capital because of high interest

rate, fixed burden and volatile earnings of the business.

Although, borrowed funds bring fixed obligations to the enterprises, still it also provides

several benefits which will be beneficial for the Trainline. Through getting loans from the banks,

Trainline can get tax benefits because interest obligations is a deductible item and on such,

HMRC (Her Majesty Revenues and Custom) provides tax benefits to the firm. Thus, it helps to

minimize tax obligations of a business and deliver them greater return (Bhowmik and Saha,

2013). In addition, there is another benefit associated with the long-term borrowing which is that

it does not dilute controlling rights to the lenders, therefore, they cannot take part in the business

functions and decisions. As a result, managers can protect business rights in their own hand and

make policies, decisions and strategic planning for the success achievement without any

interference of the lenders. Unlike this, interest benefit is not available on the equity capital

because dividend payment is not a tax deductible payment (Caglayan and Demir, 2014).

Moreover, shareholders are the owners, therefore, they have right to vote and take participation

in the business decisions. On the basis of the carried analysis, it can be suggested to the Trainline

to incorporate both the equity and borrowings to meet their long-term capital requirement and

minimize their cost of capital to exceed net profitability.

funds got decreased due to less return (Goldmann, 2017).

Question 2: Critical evaluation of sources of finance and techniques for investment proposal

In every business organization, capital structure decisions are extremely important for the

superior financial planning and management. CS decisions refer to the process of incorporating

both the long-term borrowings and shareholders equity for satisfying the financial requirement of

a business. From the financial statement of Trainline, it can be seen that it only makes use of

fluctuating source of capital in the form of equity capital to satisfy their capital requirement.

Proprietors fund comprises equity share capital, share premium and retained earnings as well. In

the year 2012, total share capital invested in the firm was 35,882,000 came down to 1,131,000 in

2016 demonstrates that company repaid their capital to their shareholders. Long-term liabilities

does not exists in the business which clearly indicate that Trainline do not use borrowed funds to

satisfy their funding requirement may be due to higher cost of capital because of high interest

rate, fixed burden and volatile earnings of the business.

Although, borrowed funds bring fixed obligations to the enterprises, still it also provides

several benefits which will be beneficial for the Trainline. Through getting loans from the banks,

Trainline can get tax benefits because interest obligations is a deductible item and on such,

HMRC (Her Majesty Revenues and Custom) provides tax benefits to the firm. Thus, it helps to

minimize tax obligations of a business and deliver them greater return (Bhowmik and Saha,

2013). In addition, there is another benefit associated with the long-term borrowing which is that

it does not dilute controlling rights to the lenders, therefore, they cannot take part in the business

functions and decisions. As a result, managers can protect business rights in their own hand and

make policies, decisions and strategic planning for the success achievement without any

interference of the lenders. Unlike this, interest benefit is not available on the equity capital

because dividend payment is not a tax deductible payment (Caglayan and Demir, 2014).

Moreover, shareholders are the owners, therefore, they have right to vote and take participation

in the business decisions. On the basis of the carried analysis, it can be suggested to the Trainline

to incorporate both the equity and borrowings to meet their long-term capital requirement and

minimize their cost of capital to exceed net profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trainline is a distributor of railway tickets and other ancillary services to the public and

as per the scenario, Trainline managers are looking to invest in a new investment project for the

growth of the business. Before investing into a long-term investment project, company is

required to assess the viability of the project because incorrect decisions may lead to failure

while successful decisions may bring growth. There are various techniques that can be utilized

by the financial manager divided into two, traditional versus modern.

Under the traditional techniques, through using payback period method, Trainline’s

administrative committee can determine the time period which project will take to recover their

invested capital. Although the method is very simple but ignoring post-payback return and time

value of the money is the main drawbacks of it (Götze, Northcott and Schuster, 2015). In order to

overcome second limitation, discounted pay-back period method has been developed which

consider the monetary value. Another technique is accounting rate of return which computes the

profitability percentage on beginning outlay but as it considers accounting return instead of cash

flows and avoids time-value, therefore, it is not founded appropriate.

On the contrary side, Net present value is a discounted technique that use discounting to

determine the present value of cash flows via (1/1+r)^n. The total present value of cash inflows

exceeding the beginning cost of capital is called NPV (Baum and Crosby, 2014). The main

downfall side of this technique is that it cannot be assured by the Trainline’s managers that cost

of capital remain constnt over the project life and affects the results, still, it is the best way or

method of capital budgeting because it makes proper adjustments regarding uncertain cash flows

by the means of discounting and provides net results (Götze, Northcott and Schuster, 2015).

Question 3 Sources of finance and investment of project

There are multiple sources of finance that are in the firm financial statements. Some of

these sources of finance are explained below.

Equity: Equity is the one of the most important source that is widely used by the firms in

their business. Under this sources of finance any firm issue shares in the market. Under

this it bring IPO in the market up to specific value. For issuing shares in the market

business firm needs to take approval from the stock exchange. It is mandatory to sign a

documents with the stock exchange. On review of the firm financial statement it can be

as per the scenario, Trainline managers are looking to invest in a new investment project for the

growth of the business. Before investing into a long-term investment project, company is

required to assess the viability of the project because incorrect decisions may lead to failure

while successful decisions may bring growth. There are various techniques that can be utilized

by the financial manager divided into two, traditional versus modern.

Under the traditional techniques, through using payback period method, Trainline’s

administrative committee can determine the time period which project will take to recover their

invested capital. Although the method is very simple but ignoring post-payback return and time

value of the money is the main drawbacks of it (Götze, Northcott and Schuster, 2015). In order to

overcome second limitation, discounted pay-back period method has been developed which

consider the monetary value. Another technique is accounting rate of return which computes the

profitability percentage on beginning outlay but as it considers accounting return instead of cash

flows and avoids time-value, therefore, it is not founded appropriate.

On the contrary side, Net present value is a discounted technique that use discounting to

determine the present value of cash flows via (1/1+r)^n. The total present value of cash inflows

exceeding the beginning cost of capital is called NPV (Baum and Crosby, 2014). The main

downfall side of this technique is that it cannot be assured by the Trainline’s managers that cost

of capital remain constnt over the project life and affects the results, still, it is the best way or

method of capital budgeting because it makes proper adjustments regarding uncertain cash flows

by the means of discounting and provides net results (Götze, Northcott and Schuster, 2015).

Question 3 Sources of finance and investment of project

There are multiple sources of finance that are in the firm financial statements. Some of

these sources of finance are explained below.

Equity: Equity is the one of the most important source that is widely used by the firms in

their business. Under this sources of finance any firm issue shares in the market. Under

this it bring IPO in the market up to specific value. For issuing shares in the market

business firm needs to take approval from the stock exchange. It is mandatory to sign a

documents with the stock exchange. On review of the firm financial statement it can be

observed that equity capital and reserves amount get changed at rapid pace. In some years

its value is increasing but in some years its value is decreasing (Baum and Crosby, 2014).

It can be observed that equity capital remain constant but amount of reserves get

changed. On this basis it can be said that equity and reserves are the one of the most

important source of finance for the business firm.

Account receivables: It is the source of finance for the business firm. It can be observed

from the financial statement of the business firm that account receivables value is

increasing consistently. Thus, it can be estimated that every year amount financed from

the receivables increased in the business. Thus, it can be assumed that receivables are the

one of the important source of finance for the business firm.

Current assets: Current assets include marketable securities which are commonly used

by the firm to finance its business. In order to meet short term fund requirements business

firm sold its securities in the market and meet its working capital requirements. Current

assets value is increasing consistently in the business. Thus, it can be said that firm

liquidity position is very strong and may improve in the upcoming time period.

In order to evaluate the project some of the most important methods can be used by the firms

in their business. Some of them are explained below.

Payback period: It is the method that is used to evaluate the project in terms of the duration

up to which firm have to wait for start earning profit on the project. The higher the value of

the payback period more the project is assumed viable by the firm. There are some merits

and demerits of the payback period method. The main merit of the payback period is that by

using same estimation of the time period can be made up to which firm will need to wait to

cover investment amount (Götze, Northcott and Schuster, 2015). The main demerit of this

method is that present value concept is not used in same and due to this reason it does not

measure viability of the project for current time period.

NPV: Net present value or NPV is the one of the most widely used method by the project

managers. This is because by using same project is evaluated in proper manner by the

business firm. In the NPV method discount factor is used and by using same present value of

the cash flows is computed and summed amount is deducted from the initial investment

value. There are some merits and demerits of the net present value method. One of the most

its value is increasing but in some years its value is decreasing (Baum and Crosby, 2014).

It can be observed that equity capital remain constant but amount of reserves get

changed. On this basis it can be said that equity and reserves are the one of the most

important source of finance for the business firm.

Account receivables: It is the source of finance for the business firm. It can be observed

from the financial statement of the business firm that account receivables value is

increasing consistently. Thus, it can be estimated that every year amount financed from

the receivables increased in the business. Thus, it can be assumed that receivables are the

one of the important source of finance for the business firm.

Current assets: Current assets include marketable securities which are commonly used

by the firm to finance its business. In order to meet short term fund requirements business

firm sold its securities in the market and meet its working capital requirements. Current

assets value is increasing consistently in the business. Thus, it can be said that firm

liquidity position is very strong and may improve in the upcoming time period.

In order to evaluate the project some of the most important methods can be used by the firms

in their business. Some of them are explained below.

Payback period: It is the method that is used to evaluate the project in terms of the duration

up to which firm have to wait for start earning profit on the project. The higher the value of

the payback period more the project is assumed viable by the firm. There are some merits

and demerits of the payback period method. The main merit of the payback period is that by

using same estimation of the time period can be made up to which firm will need to wait to

cover investment amount (Götze, Northcott and Schuster, 2015). The main demerit of this

method is that present value concept is not used in same and due to this reason it does not

measure viability of the project for current time period.

NPV: Net present value or NPV is the one of the most widely used method by the project

managers. This is because by using same project is evaluated in proper manner by the

business firm. In the NPV method discount factor is used and by using same present value of

the cash flows is computed and summed amount is deducted from the initial investment

value. There are some merits and demerits of the net present value method. One of the most

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

important plus point of using this method is that present value concept is used and by using

same value of the project in today date is computed. The only demerit of this method is that

calculation process is very lengthily and tough. Due to this reason one that does not have any

knowledge and background in the finance cannot use this method in systematic way

(Brealey, and et.al., 2012). The other negative point associated with this method is that if

wrong estimation will be made about the discount rate then in that case in wrong manner

present value of the project can be calculated which may lead to selection of wrong project

by the business firm.

IRR: IRR is the method that reflect the real rate of return that can be earned on the project.

More is the value of IRR project is assumed profitable by the business firm. Like other above

discussed methods there are some positive and negative points that are associated with the

IRR method. One of the main positive point of IRR is that by using same real rate of return

that will be generated by the project is computed. Negative point is that calculation process is

highly complex and every individual cannot perform calculation efficiently.

On analysis of all these methods it can be said that business firm must use NPV and IRR

method to evaluate the project. This is because NPV reflect the real value of the project that

remain after subtracting initial investment value from the sum of present value of cash flows.

On other hand, IRR reflect the real rate of return that can be gained on the project. Thus, it

can be said that both method NPV and IRR are best for evaluating any project.

Question 4 Entrepreneurial ecosystem and business development

Entrepreneurial ecosystem play an important role in growth of the business firm. This is

because the nations where ecosystem is good there are lots of opportunities that are available to

the business firms. Entrepreneurs by taking steps capitalize available opportunity. In most of the

nations of the world government takes varied steps in order to promote entrepreneurs to open

their new business. Under this sufficient amount of finance is made available to entrepreneurs.

Moreover, in plenty amount resources are provided to them in order to support manufacturing

activities of the business firm (Gitman and Zutter, 2012). On this basis it can be said that

entrepreneurial ecosystem play a great role in business development. Entrepreneurial ecosystem

to large extent is responsible for the business development of the Trainline. This is because firm

is operating in the sector on which there is due focus of the government in terms of growing a

same value of the project in today date is computed. The only demerit of this method is that

calculation process is very lengthily and tough. Due to this reason one that does not have any

knowledge and background in the finance cannot use this method in systematic way

(Brealey, and et.al., 2012). The other negative point associated with this method is that if

wrong estimation will be made about the discount rate then in that case in wrong manner

present value of the project can be calculated which may lead to selection of wrong project

by the business firm.

IRR: IRR is the method that reflect the real rate of return that can be earned on the project.

More is the value of IRR project is assumed profitable by the business firm. Like other above

discussed methods there are some positive and negative points that are associated with the

IRR method. One of the main positive point of IRR is that by using same real rate of return

that will be generated by the project is computed. Negative point is that calculation process is

highly complex and every individual cannot perform calculation efficiently.

On analysis of all these methods it can be said that business firm must use NPV and IRR

method to evaluate the project. This is because NPV reflect the real value of the project that

remain after subtracting initial investment value from the sum of present value of cash flows.

On other hand, IRR reflect the real rate of return that can be gained on the project. Thus, it

can be said that both method NPV and IRR are best for evaluating any project.

Question 4 Entrepreneurial ecosystem and business development

Entrepreneurial ecosystem play an important role in growth of the business firm. This is

because the nations where ecosystem is good there are lots of opportunities that are available to

the business firms. Entrepreneurs by taking steps capitalize available opportunity. In most of the

nations of the world government takes varied steps in order to promote entrepreneurs to open

their new business. Under this sufficient amount of finance is made available to entrepreneurs.

Moreover, in plenty amount resources are provided to them in order to support manufacturing

activities of the business firm (Gitman and Zutter, 2012). On this basis it can be said that

entrepreneurial ecosystem play a great role in business development. Entrepreneurial ecosystem

to large extent is responsible for the business development of the Trainline. This is because firm

is operating in the sector on which there is due focus of the government in terms of growing a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. Government have taken many steps that make business environment congenial for the

business firms. Thus, it can be said that entrepreneurial ecosystem to large extent play an

important role in development of Trainline as business.

Question 5 Ethical consideration for IPO

Company needs to consider several ethical considerations when it decides to go for IPO.

Ethical aspects are the key elements which in turn helps company in building effective image at

marketplace. Thus, Trainline has ethical responsibility to provide highly suitable and reliable

information to the investors. Moreover, with the aim to entice the decision making of large

number of investors companies sometime provide investors with false information regarding the

future growth and development. This is highly unethical and places adverse impact on the image

of business organization (Embrechts, Klüppelberg and Mikosch, 2013). Hence, Trainline is

required to issue prospectus after evaluating the each and every aspect in the best possible way.

Further, business unit should also issue or trade shares at fair value. Moreover, issuance of shares

at higher prices may result into rise in speculative activities or practices. Thus, by offering shares

at suitable prices business unit can ensure highly secured financial market and position. Along

with this, Trainline should offer equal chance of investment to each individual or investor.

Moreover, there are several investors who prefer to invest money in the shares of growing

business organization. Hence, by offering opportunities and providing information regarding IPO

to the general public business unit can enhance its goodwill. Further, by coordinating with green

show Management Company Trainline can monitor the performance of securities in an effectual

way. Besides this, it can be inferred that such team also provides direction to the firm about the

manner in which they need to make changes in equity aspects. Thus, by following all the above

mentioned ways business unit can meet ethical aspects to the significant level. There are some

other ethical factors that firm must take in to consideration like it must not launch its IPO in the

market when stock market is not performing well (Finance and Network, 2013). This is because

investors make an investment in the business firm on hope that they will earn good return on the

invested amount. Due to consistent downturn in the stock market pessimistic behavior comes in

the investors and due to this reason they start selling shares in the market. Due to this reason

shares values start falling from starting day after launch of IPO and investors lose money on

business firms. Thus, it can be said that entrepreneurial ecosystem to large extent play an

important role in development of Trainline as business.

Question 5 Ethical consideration for IPO

Company needs to consider several ethical considerations when it decides to go for IPO.

Ethical aspects are the key elements which in turn helps company in building effective image at

marketplace. Thus, Trainline has ethical responsibility to provide highly suitable and reliable

information to the investors. Moreover, with the aim to entice the decision making of large

number of investors companies sometime provide investors with false information regarding the

future growth and development. This is highly unethical and places adverse impact on the image

of business organization (Embrechts, Klüppelberg and Mikosch, 2013). Hence, Trainline is

required to issue prospectus after evaluating the each and every aspect in the best possible way.

Further, business unit should also issue or trade shares at fair value. Moreover, issuance of shares

at higher prices may result into rise in speculative activities or practices. Thus, by offering shares

at suitable prices business unit can ensure highly secured financial market and position. Along

with this, Trainline should offer equal chance of investment to each individual or investor.

Moreover, there are several investors who prefer to invest money in the shares of growing

business organization. Hence, by offering opportunities and providing information regarding IPO

to the general public business unit can enhance its goodwill. Further, by coordinating with green

show Management Company Trainline can monitor the performance of securities in an effectual

way. Besides this, it can be inferred that such team also provides direction to the firm about the

manner in which they need to make changes in equity aspects. Thus, by following all the above

mentioned ways business unit can meet ethical aspects to the significant level. There are some

other ethical factors that firm must take in to consideration like it must not launch its IPO in the

market when stock market is not performing well (Finance and Network, 2013). This is because

investors make an investment in the business firm on hope that they will earn good return on the

invested amount. Due to consistent downturn in the stock market pessimistic behavior comes in

the investors and due to this reason they start selling shares in the market. Due to this reason

shares values start falling from starting day after launch of IPO and investors lose money on

investment. It can be said that it is the ethical responsibility of the business firm to launch IPO in

the market on when there is probability that investor shares value will increase consistently.

CONCLUSION

On the basis of the performance analysis, it can be suggested to the Trainline manager to

make best pricing decisions, cost-controlling strategies, maximize current assets and optimally

use the assets business to improve business performance and financial status. However, from the

evaluation of financial sources, it has been suggested to the firm to utilize borrowings also in the

capital structure to manage their cost of capital. Under the investment appraisal evaluation, Net

Present Value has been suggested as the best way for evaluation of long-term investment

proposal to examine the viability of the project.

the market on when there is probability that investor shares value will increase consistently.

CONCLUSION

On the basis of the performance analysis, it can be suggested to the Trainline manager to

make best pricing decisions, cost-controlling strategies, maximize current assets and optimally

use the assets business to improve business performance and financial status. However, from the

evaluation of financial sources, it has been suggested to the firm to utilize borrowings also in the

capital structure to manage their cost of capital. Under the investment appraisal evaluation, Net

Present Value has been suggested as the best way for evaluation of long-term investment

proposal to examine the viability of the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.