Detailed Financial Analysis and Projections for Trainline (2013-2019)

VerifiedAdded on 2020/01/28

|13

|4126

|69

Report

AI Summary

This report provides a comprehensive financial analysis of Trainline, a UK-based SME, focusing on its performance from 2013 to 2016 and projecting cash flow through 2019. The analysis includes a critical evaluation of Trainline's performance using ratio analysis, highlighting profitability, liquidity, and efficiency trends. A projected cash budget for the years 2017-2019 is presented, along with an evaluation of financing sources within the Statement of Financial Position (SOFP) and investment appraisal techniques. Furthermore, the report discusses the entrepreneurial ecosystem's role in Trainline's development and explores ethical considerations crucial for an IPO issuance. The report uses financial statements and various financial tools to assess the financial health of the company and provide insights into its financial strategies and future prospects. The report includes key financial ratios, cash flow projections, and discussions on investment and financing strategies, offering valuable insights into Trainline's financial operations and potential future growth.

Finance in an SME context

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis..............3

Q2. Projected Cash Budget For the year 2017, 2018, 2019.........................................................5

Q3. Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal........................................................................................................................................6

Q.4. Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline.............................................................................................................8

Q.5. Critical discussion of ethical consideration that must be taken into account for IPO

issuance........................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis..............3

Q2. Projected Cash Budget For the year 2017, 2018, 2019.........................................................5

Q3. Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal........................................................................................................................................6

Q.4. Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline.............................................................................................................8

Q.5. Critical discussion of ethical consideration that must be taken into account for IPO

issuance........................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Since this present scenario has been seen as a domination of small medium sized firms

who are growing at a rapid pace equally contributing in the growth of the economy as well

through continuously contributing towards the GDP and different factors which generate

employment and satisfy customer needs up to an extent. When we talk about startups or small

business who marks their presence in industry with innovative and creative set of services these

days, they execute their routine functions by acquiring funds and utilizing them in an efficient

and effective manner. As per this report it is emphasized on one of the small and medium sized

firms of UK which is Trainline. Trainline delivers quality services , in its portfolio of services it

includes railway ticket, distribution and other ancillary facilities to the consumers. The report

here is undertaken in order to put emphasis on performance evaluation and financial status of

Trainline. Further it will also look upon the variety of financial sources and ethical

considerations that firms need to take into consideration at the time of IPO issue.

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis

For the purpose of calculating the Ratio's comparative balance sheet of Trainline is

mentioned above:

2012 2013 2014 2015 2016

Intangible assets 4035 4418 6206 7913 19931

Tangible assets 20784 20149 15537 9859 2035

Non-current(Fixed)

assets 24819 24567 21743 17772 21966

Inventories 61 63 56 34 31

Accounts

receivables 148873 189072 91043 124455 153121

Cash at bank and in

hand 42280 50747 43949 77886 44408

Current assets 191214 239882 135048 202375 197560

Total Assets 216033 264449 156791 220147 219526

Equity and liabilities

Accounts payable 120227 128772 114502 143067 162990

Provision for

liabilities 91 142 222 259 378

Current Liabilities 120318 128914 114824 143326 163368

Since this present scenario has been seen as a domination of small medium sized firms

who are growing at a rapid pace equally contributing in the growth of the economy as well

through continuously contributing towards the GDP and different factors which generate

employment and satisfy customer needs up to an extent. When we talk about startups or small

business who marks their presence in industry with innovative and creative set of services these

days, they execute their routine functions by acquiring funds and utilizing them in an efficient

and effective manner. As per this report it is emphasized on one of the small and medium sized

firms of UK which is Trainline. Trainline delivers quality services , in its portfolio of services it

includes railway ticket, distribution and other ancillary facilities to the consumers. The report

here is undertaken in order to put emphasis on performance evaluation and financial status of

Trainline. Further it will also look upon the variety of financial sources and ethical

considerations that firms need to take into consideration at the time of IPO issue.

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis

For the purpose of calculating the Ratio's comparative balance sheet of Trainline is

mentioned above:

2012 2013 2014 2015 2016

Intangible assets 4035 4418 6206 7913 19931

Tangible assets 20784 20149 15537 9859 2035

Non-current(Fixed)

assets 24819 24567 21743 17772 21966

Inventories 61 63 56 34 31

Accounts

receivables 148873 189072 91043 124455 153121

Cash at bank and in

hand 42280 50747 43949 77886 44408

Current assets 191214 239882 135048 202375 197560

Total Assets 216033 264449 156791 220147 219526

Equity and liabilities

Accounts payable 120227 128772 114502 143067 162990

Provision for

liabilities 91 142 222 259 378

Current Liabilities 120318 128914 114824 143326 163368

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

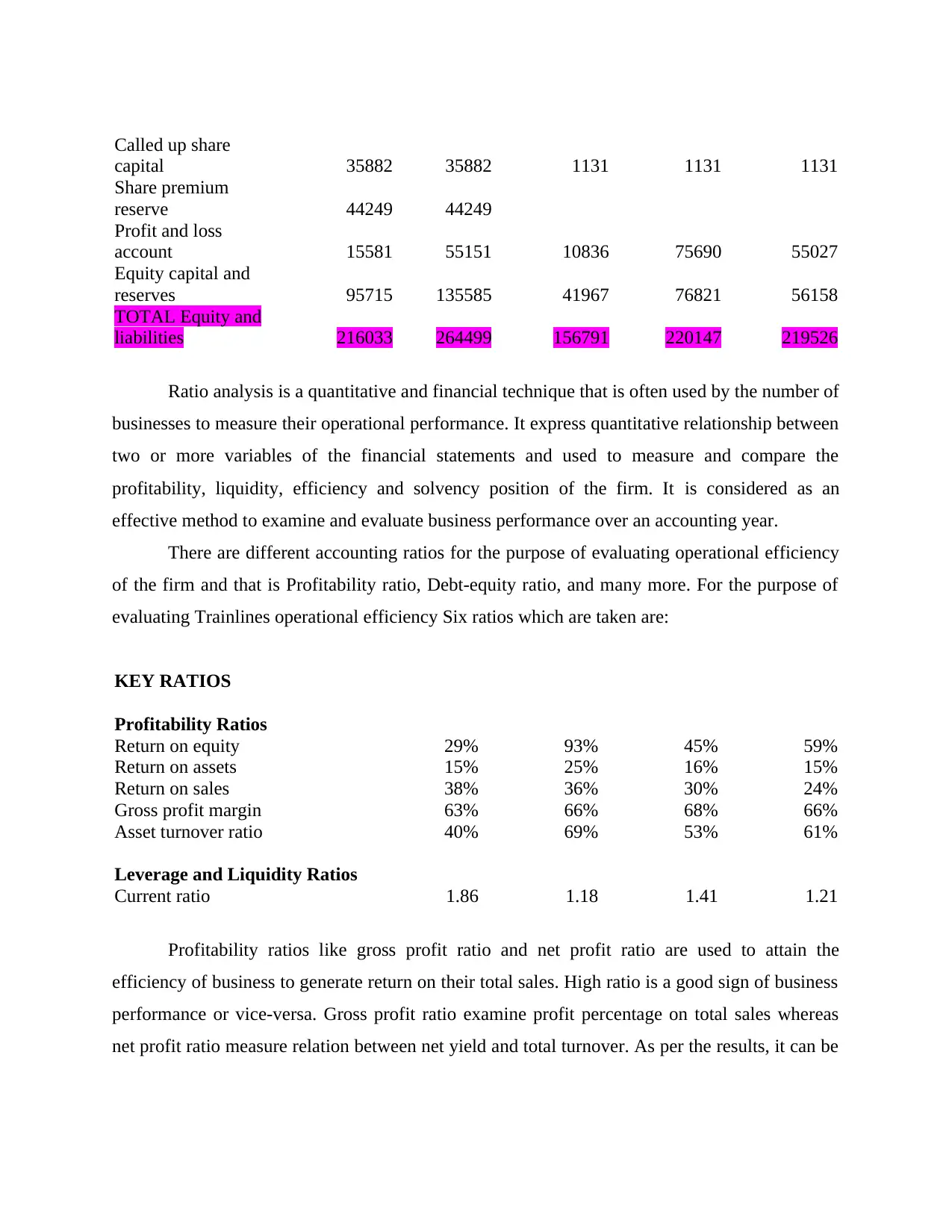

Called up share

capital 35882 35882 1131 1131 1131

Share premium

reserve 44249 44249

Profit and loss

account 15581 55151 10836 75690 55027

Equity capital and

reserves 95715 135585 41967 76821 56158

TOTAL Equity and

liabilities 216033 264499 156791 220147 219526

Ratio analysis is a quantitative and financial technique that is often used by the number of

businesses to measure their operational performance. It express quantitative relationship between

two or more variables of the financial statements and used to measure and compare the

profitability, liquidity, efficiency and solvency position of the firm. It is considered as an

effective method to examine and evaluate business performance over an accounting year.

There are different accounting ratios for the purpose of evaluating operational efficiency

of the firm and that is Profitability ratio, Debt-equity ratio, and many more. For the purpose of

evaluating Trainlines operational efficiency Six ratios which are taken are:

KEY RATIOS

Profitability Ratios

Return on equity 29% 93% 45% 59%

Return on assets 15% 25% 16% 15%

Return on sales 38% 36% 30% 24%

Gross profit margin 63% 66% 68% 66%

Asset turnover ratio 40% 69% 53% 61%

Leverage and Liquidity Ratios

Current ratio 1.86 1.18 1.41 1.21

Profitability ratios like gross profit ratio and net profit ratio are used to attain the

efficiency of business to generate return on their total sales. High ratio is a good sign of business

performance or vice-versa. Gross profit ratio examine profit percentage on total sales whereas

net profit ratio measure relation between net yield and total turnover. As per the results, it can be

capital 35882 35882 1131 1131 1131

Share premium

reserve 44249 44249

Profit and loss

account 15581 55151 10836 75690 55027

Equity capital and

reserves 95715 135585 41967 76821 56158

TOTAL Equity and

liabilities 216033 264499 156791 220147 219526

Ratio analysis is a quantitative and financial technique that is often used by the number of

businesses to measure their operational performance. It express quantitative relationship between

two or more variables of the financial statements and used to measure and compare the

profitability, liquidity, efficiency and solvency position of the firm. It is considered as an

effective method to examine and evaluate business performance over an accounting year.

There are different accounting ratios for the purpose of evaluating operational efficiency

of the firm and that is Profitability ratio, Debt-equity ratio, and many more. For the purpose of

evaluating Trainlines operational efficiency Six ratios which are taken are:

KEY RATIOS

Profitability Ratios

Return on equity 29% 93% 45% 59%

Return on assets 15% 25% 16% 15%

Return on sales 38% 36% 30% 24%

Gross profit margin 63% 66% 68% 66%

Asset turnover ratio 40% 69% 53% 61%

Leverage and Liquidity Ratios

Current ratio 1.86 1.18 1.41 1.21

Profitability ratios like gross profit ratio and net profit ratio are used to attain the

efficiency of business to generate return on their total sales. High ratio is a good sign of business

performance or vice-versa. Gross profit ratio examine profit percentage on total sales whereas

net profit ratio measure relation between net yield and total turnover. As per the results, it can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

seen that trainline's net profit is continuously declining which is it came down from 38% to 24%

in 4 years. Trainline needs to think on this issue immediately. Trainline's turnover has been

increased but still due to high proportionate increase in cost of sales. Effective managerial

control over indirect spending and overheads like rent, salaries, general, office and

administration and marketing expenditures may be the reason behind increase net profit

indicating that in 2015, TUI performed comparatively well than earlier year.

On the other hand, liquidity ratios measure relationship between short-term (current

assets) and short-term obligations (current liabilities). It is used to examine that whether trainline

has improved its capability or not to repay their short-term debts on decided time. Current ratio

and quick ratio are the best way of examining liquidity performance of the firm. Current Ratio

measure relationship CA and CL, whereas QR examine liquidity position without taking into

account closing inventory balance. Trainline's liquidity ratio does not show an increasing trend as

well as decreasing trend. In 2013 it is 1.86 and further it decreases and then increases but in 2016

it again decreases. Rising trend reflects that Trainline improved its current assets like debtors,

receivables and cash to repay short-term obligations on correct time. Besides this, efficiency

ratios are used to measure that managers have effectively utilized business assets or not to gather

maximum revenues through operational activities. On the contrary to this, solvency ratios helps

to measure firm’s capability to repay their long-term debt like loans as per repayment schedule.

But in the case of Trainline since debt is not there no solvency ratios can be calculated for

measuring the payable capacity of the firm.

Q2. Projected Cash Budget For the year 2017, 2018, 2019

Since trainline needs to have an IPO in future and for the growth of the business they

need to think on the financial matters of the company. So in order they need to set up its

projected cash budget to be used in future. They need to forecast their cash needs as per the

current operations of the businesses. Through projected cash needs they want in future they will

be draw conclusions on their operation and try to make use of the resources in an efficient and

effective manner so that in future they meet the required amount of cash needed to pay the

people from cash has been taken or the funds have been acquired.

in 4 years. Trainline needs to think on this issue immediately. Trainline's turnover has been

increased but still due to high proportionate increase in cost of sales. Effective managerial

control over indirect spending and overheads like rent, salaries, general, office and

administration and marketing expenditures may be the reason behind increase net profit

indicating that in 2015, TUI performed comparatively well than earlier year.

On the other hand, liquidity ratios measure relationship between short-term (current

assets) and short-term obligations (current liabilities). It is used to examine that whether trainline

has improved its capability or not to repay their short-term debts on decided time. Current ratio

and quick ratio are the best way of examining liquidity performance of the firm. Current Ratio

measure relationship CA and CL, whereas QR examine liquidity position without taking into

account closing inventory balance. Trainline's liquidity ratio does not show an increasing trend as

well as decreasing trend. In 2013 it is 1.86 and further it decreases and then increases but in 2016

it again decreases. Rising trend reflects that Trainline improved its current assets like debtors,

receivables and cash to repay short-term obligations on correct time. Besides this, efficiency

ratios are used to measure that managers have effectively utilized business assets or not to gather

maximum revenues through operational activities. On the contrary to this, solvency ratios helps

to measure firm’s capability to repay their long-term debt like loans as per repayment schedule.

But in the case of Trainline since debt is not there no solvency ratios can be calculated for

measuring the payable capacity of the firm.

Q2. Projected Cash Budget For the year 2017, 2018, 2019

Since trainline needs to have an IPO in future and for the growth of the business they

need to think on the financial matters of the company. So in order they need to set up its

projected cash budget to be used in future. They need to forecast their cash needs as per the

current operations of the businesses. Through projected cash needs they want in future they will

be draw conclusions on their operation and try to make use of the resources in an efficient and

effective manner so that in future they meet the required amount of cash needed to pay the

people from cash has been taken or the funds have been acquired.

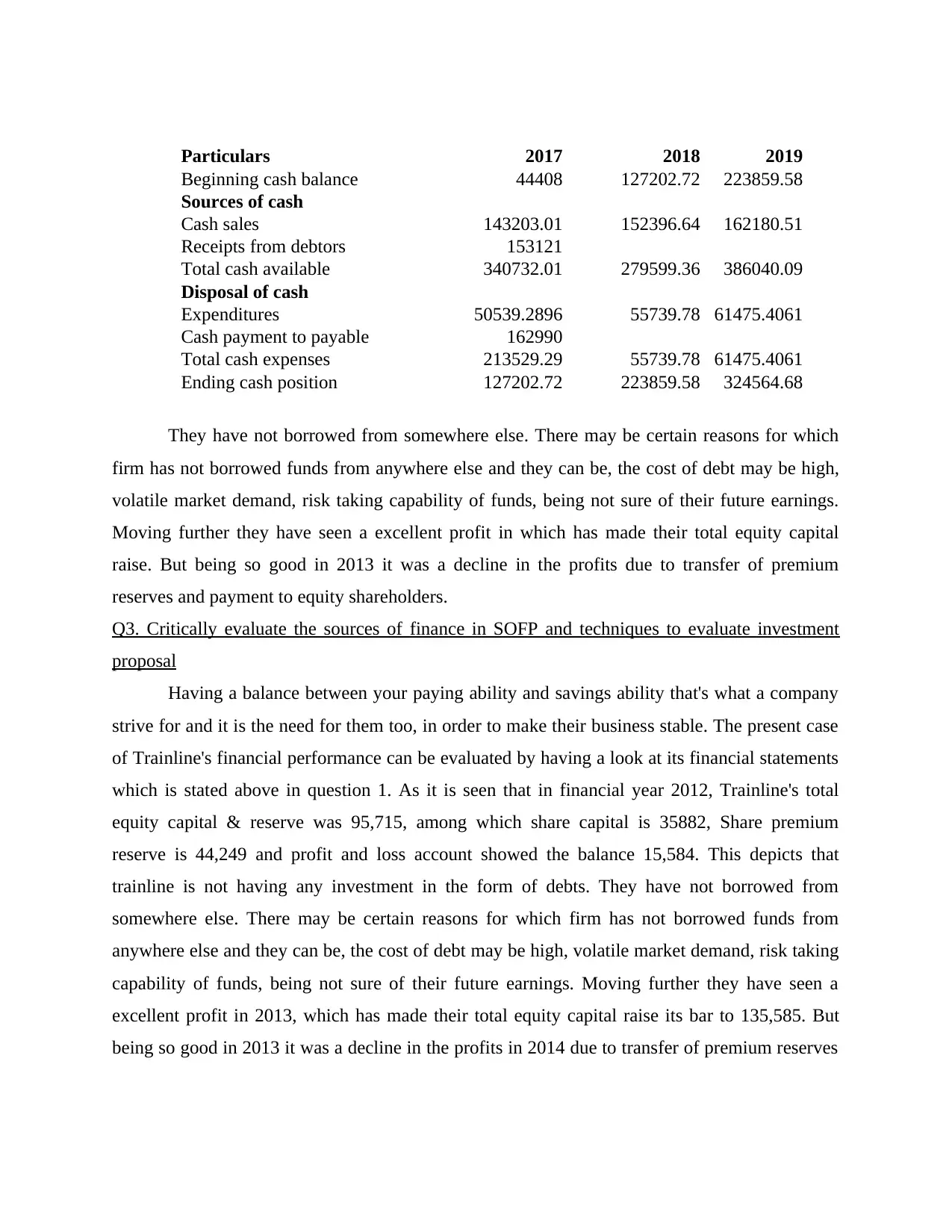

Particulars 2017 2018 2019

Beginning cash balance 44408 127202.72 223859.58

Sources of cash

Cash sales 143203.01 152396.64 162180.51

Receipts from debtors 153121

Total cash available 340732.01 279599.36 386040.09

Disposal of cash

Expenditures 50539.2896 55739.78 61475.4061

Cash payment to payable 162990

Total cash expenses 213529.29 55739.78 61475.4061

Ending cash position 127202.72 223859.58 324564.68

They have not borrowed from somewhere else. There may be certain reasons for which

firm has not borrowed funds from anywhere else and they can be, the cost of debt may be high,

volatile market demand, risk taking capability of funds, being not sure of their future earnings.

Moving further they have seen a excellent profit in which has made their total equity capital

raise. But being so good in 2013 it was a decline in the profits due to transfer of premium

reserves and payment to equity shareholders.

Q3. Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal

Having a balance between your paying ability and savings ability that's what a company

strive for and it is the need for them too, in order to make their business stable. The present case

of Trainline's financial performance can be evaluated by having a look at its financial statements

which is stated above in question 1. As it is seen that in financial year 2012, Trainline's total

equity capital & reserve was 95,715, among which share capital is 35882, Share premium

reserve is 44,249 and profit and loss account showed the balance 15,584. This depicts that

trainline is not having any investment in the form of debts. They have not borrowed from

somewhere else. There may be certain reasons for which firm has not borrowed funds from

anywhere else and they can be, the cost of debt may be high, volatile market demand, risk taking

capability of funds, being not sure of their future earnings. Moving further they have seen a

excellent profit in 2013, which has made their total equity capital raise its bar to 135,585. But

being so good in 2013 it was a decline in the profits in 2014 due to transfer of premium reserves

Beginning cash balance 44408 127202.72 223859.58

Sources of cash

Cash sales 143203.01 152396.64 162180.51

Receipts from debtors 153121

Total cash available 340732.01 279599.36 386040.09

Disposal of cash

Expenditures 50539.2896 55739.78 61475.4061

Cash payment to payable 162990

Total cash expenses 213529.29 55739.78 61475.4061

Ending cash position 127202.72 223859.58 324564.68

They have not borrowed from somewhere else. There may be certain reasons for which

firm has not borrowed funds from anywhere else and they can be, the cost of debt may be high,

volatile market demand, risk taking capability of funds, being not sure of their future earnings.

Moving further they have seen a excellent profit in which has made their total equity capital

raise. But being so good in 2013 it was a decline in the profits due to transfer of premium

reserves and payment to equity shareholders.

Q3. Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal

Having a balance between your paying ability and savings ability that's what a company

strive for and it is the need for them too, in order to make their business stable. The present case

of Trainline's financial performance can be evaluated by having a look at its financial statements

which is stated above in question 1. As it is seen that in financial year 2012, Trainline's total

equity capital & reserve was 95,715, among which share capital is 35882, Share premium

reserve is 44,249 and profit and loss account showed the balance 15,584. This depicts that

trainline is not having any investment in the form of debts. They have not borrowed from

somewhere else. There may be certain reasons for which firm has not borrowed funds from

anywhere else and they can be, the cost of debt may be high, volatile market demand, risk taking

capability of funds, being not sure of their future earnings. Moving further they have seen a

excellent profit in 2013, which has made their total equity capital raise its bar to 135,585. But

being so good in 2013 it was a decline in the profits in 2014 due to transfer of premium reserves

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and payment to equity shareholders. Further in 2015 and 2016 profits were noted as 76821 and

56158 respectively. Among the years of operations Trainline has never been into borrowing of

funds, their capital structure was consisting of only equity capitals may be due to high cost of

borrowings on debt capitals. Since they have not been familiar with debt capitals there capital

structure cannot be considered as efficient.

Further if Trainline have thought of investing in some projects in order to have a look

what they will be gaining in future for the funds invested today, they need to go through a deep

study of techniques which will be best for them in order to make decisions regarding the projects

that in which projects they should be investing. So, in order to make right decisions regarding the

best investment proposal to be chosen, here are the techniques which can be used by Trainline: Net Present Value: In Net present value investors discount their associated project’s cash

flows using an appropriate discounting rate based on cost of capital. The discounting

rates can be fixed and can be variable too, it depends on the projects nature too. It is

because; the amount that investors gain today will not be of the same value in future, So,

Trainline require to discount their successive cash inflows and determine current value.

After that, NPV is the difference between cash inflows and outflows of a company. If

NPV is positive and Zero then Trainline should adopt the investment proposal and if

NPV is negative then the proposal should not be accepted. Internal Rate of Return: Likewise NPV, IRR also is of the belief that worth of currency

that an investor have today is more than receiving a specified amount in forthcoming

period. IRR refers to the discounting rate which equates both the present value of future

cash flows and initial outlay. IRR is that rate at which present cash inflow is equal to

present cash outflow. Lower the rate much better it is. Pay-back Period: It is the simplest method of assessing and comparing various projects

by just identifying the length of time that the project will take to repay the initial

investment. It will enable Trainline to prefer such project that indicates quick payback. It

also avoids giving higher weight to risky project and long-term projection also.

Accounting rate of return: Accounting rate of return compares expected profit

percentage on the amount of initial investment that Trainline need to invest. In case of

single project, company can compare expected ARR with the desired or targeted return

56158 respectively. Among the years of operations Trainline has never been into borrowing of

funds, their capital structure was consisting of only equity capitals may be due to high cost of

borrowings on debt capitals. Since they have not been familiar with debt capitals there capital

structure cannot be considered as efficient.

Further if Trainline have thought of investing in some projects in order to have a look

what they will be gaining in future for the funds invested today, they need to go through a deep

study of techniques which will be best for them in order to make decisions regarding the projects

that in which projects they should be investing. So, in order to make right decisions regarding the

best investment proposal to be chosen, here are the techniques which can be used by Trainline: Net Present Value: In Net present value investors discount their associated project’s cash

flows using an appropriate discounting rate based on cost of capital. The discounting

rates can be fixed and can be variable too, it depends on the projects nature too. It is

because; the amount that investors gain today will not be of the same value in future, So,

Trainline require to discount their successive cash inflows and determine current value.

After that, NPV is the difference between cash inflows and outflows of a company. If

NPV is positive and Zero then Trainline should adopt the investment proposal and if

NPV is negative then the proposal should not be accepted. Internal Rate of Return: Likewise NPV, IRR also is of the belief that worth of currency

that an investor have today is more than receiving a specified amount in forthcoming

period. IRR refers to the discounting rate which equates both the present value of future

cash flows and initial outlay. IRR is that rate at which present cash inflow is equal to

present cash outflow. Lower the rate much better it is. Pay-back Period: It is the simplest method of assessing and comparing various projects

by just identifying the length of time that the project will take to repay the initial

investment. It will enable Trainline to prefer such project that indicates quick payback. It

also avoids giving higher weight to risky project and long-term projection also.

Accounting rate of return: Accounting rate of return compares expected profit

percentage on the amount of initial investment that Trainline need to invest. In case of

single project, company can compare expected ARR with the desired or targeted return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

whilst in case of having number of proposals, obviously, Trainline will prefer higher

ARR generating project.

Q.4. Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline

Trainline known as UK rail ticket retailers and variety of services in its pocket it is a

company which is founded and funded by Vrigin rail group, it sells its ticket through a call

center. When it comes to the role of entrepreneurs who were part of the firm and contributed

their services in developing the business. there are some entrepreneurs or rather chief executive

officers they have impacted the business of company in many ways, whether it is about

increasing customer base or hitting new segments or targets. In 2008 Murray Hennessy joined

trainline.com as chief executive officer and by joining it in a span of one year he increased

investment of organization in advertisements which eventually benefited them in hitting new

customers. The company with its first TV advertisements campaign launched the ability for

customers to print their own tickets containing a secure bar code. So what this did was customers

were attracted to this feature and the practice of booking tickets from trainline.com was

increased in a rapid manner. Further more in 2009, Trainline launched its first I Phone mobile

app and started to new era of development of smartphone applications. Many further

establishments and developments have been done in leadership of Murray Hennessy. This shows

that trainline without a CEO or the leader of Murray's kind was nothing, after the joining of

Murray only these amendments have taken place so this shows the entrepreneur thinking skills

and how can a entrepreneur can lift the entire business with its capabilities.

Further more in 2014 Clare Gilmartin was recruited as the chief executive officer of the

firm and in 2015 what he did was he rejuvenated the whole concept of company to Trainline

only which means he with his entrepreneurial thinking and capabilities not just changed the name

of the company he changed the color combination and logos and everything which was looking

old and set up a new trainline company which was new in every manner and matching with the

modern world. The presence of current trainline is bold, positive, friendly and is a mordern

brand, just as it was imagined by Gilmartin.

So, as per the history of trainline it is pretty clear that behind the developments in the

decade the two entrepreneurs have played their part in most of them. Thus the emphasis which

ARR generating project.

Q.4. Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline

Trainline known as UK rail ticket retailers and variety of services in its pocket it is a

company which is founded and funded by Vrigin rail group, it sells its ticket through a call

center. When it comes to the role of entrepreneurs who were part of the firm and contributed

their services in developing the business. there are some entrepreneurs or rather chief executive

officers they have impacted the business of company in many ways, whether it is about

increasing customer base or hitting new segments or targets. In 2008 Murray Hennessy joined

trainline.com as chief executive officer and by joining it in a span of one year he increased

investment of organization in advertisements which eventually benefited them in hitting new

customers. The company with its first TV advertisements campaign launched the ability for

customers to print their own tickets containing a secure bar code. So what this did was customers

were attracted to this feature and the practice of booking tickets from trainline.com was

increased in a rapid manner. Further more in 2009, Trainline launched its first I Phone mobile

app and started to new era of development of smartphone applications. Many further

establishments and developments have been done in leadership of Murray Hennessy. This shows

that trainline without a CEO or the leader of Murray's kind was nothing, after the joining of

Murray only these amendments have taken place so this shows the entrepreneur thinking skills

and how can a entrepreneur can lift the entire business with its capabilities.

Further more in 2014 Clare Gilmartin was recruited as the chief executive officer of the

firm and in 2015 what he did was he rejuvenated the whole concept of company to Trainline

only which means he with his entrepreneurial thinking and capabilities not just changed the name

of the company he changed the color combination and logos and everything which was looking

old and set up a new trainline company which was new in every manner and matching with the

modern world. The presence of current trainline is bold, positive, friendly and is a mordern

brand, just as it was imagined by Gilmartin.

So, as per the history of trainline it is pretty clear that behind the developments in the

decade the two entrepreneurs have played their part in most of them. Thus the emphasis which

was on entrepreneurship system as the factor of affecting trainline business have been clearly

understood with the introduction of certain important measures by the two CEO's.

Q.5. Critical discussion of ethical consideration that must be taken into account for IPO issuance

An IPO is a huge task which can make the companies future and can destroy it too, so in

order to make initial public offer a company should undertake a explicit examination of its

environment internal and external both. The factors that trainline managers or financial advisers

need to examine before IPO issuance are some of these:

1. Performance and Growth over the years: A finance manager should

consider its profitability levels over the years, Considering what has been the

performance of the company in terms of profitability as well as the 'year on

year' growth in the company should be undertaken by a manager in order to

know that IPO which needs to be undertaken will be fruitful or not. Revenue

growth is one of the most important factors to consider while determining

whether an IPO is worth investing in. Trainline should follow above

discussed things in order to be successful in its IPO.

2. Promoter's Standing: promoter plays important role in an IPO since he is

the person who manages all the work of an IPO on the behalf of company. So

his status and symbol is important for the trainline in order to make their IPO

successful i9n the markets.

3. Post IPO Promoter Share Holding: Financial analyst of the company should

consider the shareholding of promoter in the company post IPO. If the

promoter have high share holding in the companies shares they have great

confidence in the future growth and profitability of the company.

4. Objective of the Issue: Consider what are the objectives of the current issue

and how the proceeds from the issue is to be utilised by the company?

Whether the company will utilise the proceeds to fund an expansion plan or

merely repay existing debt, are issues to be considered in this regard.

5. P/E Ratio: P/E Ratio or the Price-Earning ratio is an effective tool to

determine how attractively the issue price is valued. P/E Ratio is simply the

understood with the introduction of certain important measures by the two CEO's.

Q.5. Critical discussion of ethical consideration that must be taken into account for IPO issuance

An IPO is a huge task which can make the companies future and can destroy it too, so in

order to make initial public offer a company should undertake a explicit examination of its

environment internal and external both. The factors that trainline managers or financial advisers

need to examine before IPO issuance are some of these:

1. Performance and Growth over the years: A finance manager should

consider its profitability levels over the years, Considering what has been the

performance of the company in terms of profitability as well as the 'year on

year' growth in the company should be undertaken by a manager in order to

know that IPO which needs to be undertaken will be fruitful or not. Revenue

growth is one of the most important factors to consider while determining

whether an IPO is worth investing in. Trainline should follow above

discussed things in order to be successful in its IPO.

2. Promoter's Standing: promoter plays important role in an IPO since he is

the person who manages all the work of an IPO on the behalf of company. So

his status and symbol is important for the trainline in order to make their IPO

successful i9n the markets.

3. Post IPO Promoter Share Holding: Financial analyst of the company should

consider the shareholding of promoter in the company post IPO. If the

promoter have high share holding in the companies shares they have great

confidence in the future growth and profitability of the company.

4. Objective of the Issue: Consider what are the objectives of the current issue

and how the proceeds from the issue is to be utilised by the company?

Whether the company will utilise the proceeds to fund an expansion plan or

merely repay existing debt, are issues to be considered in this regard.

5. P/E Ratio: P/E Ratio or the Price-Earning ratio is an effective tool to

determine how attractively the issue price is valued. P/E Ratio is simply the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio between the Market Price of a share and its Earnings per Share (EPS).

A higher P/E ratio could mean that the IPO is over-valued. Note that P/E ratio

should not be considered in isolation but combined with other meaningful

data to arrive at your conclusion.

6. Post IPO Debt-Equity Ratio: What would be the post listing Debt-Equity

Ratio of the company. The debt equity ratio refers to the ratio which shows

the proportion of equity and debt that a firm uses in its capital structure. Here

trainline does not have a debt so the future prospects should be kept in mind

by the firm in order to implement successful IPO.

7. Outlook of the company: What is the future outlook of the company? How

well are they placed in terms of competition? What opportunities lie before

the company and how well are they equipped to explore and take advantages

of such opportunities? What immediate threats the company faces?

8. Future Outlook of the Industry: Keeping up with the future operations that

firm is going to undertake should be known and considered because this will

effect the price of its shares. Future outlook of the industry in which the

company is operating is an important factor to consider while determining

whether to invest in an IPO. A country's demographic structure, its economic

and political environment as well as its laws and regulations have a

significant impact on the future outlook of any industry.

CONCLUSION

From this report it has been concluded that Trainline has developed at a very

rapid pace in the recent 10 years and continues to do so with its thinking of offering

IPO to public. Further Trainline has been into delivery of rail tickets then they have

been personalized their apps for I Phone and now they are offering IPO to public.

This all has been done by two of the entrepreneurs. So from this report it has been

concluded that for every small business who needs to be at the top have to have a

good leader so that he can take decisions towards the growth of the sector. From

this report it has been concluded that Trainline in order to make his impact on the

A higher P/E ratio could mean that the IPO is over-valued. Note that P/E ratio

should not be considered in isolation but combined with other meaningful

data to arrive at your conclusion.

6. Post IPO Debt-Equity Ratio: What would be the post listing Debt-Equity

Ratio of the company. The debt equity ratio refers to the ratio which shows

the proportion of equity and debt that a firm uses in its capital structure. Here

trainline does not have a debt so the future prospects should be kept in mind

by the firm in order to implement successful IPO.

7. Outlook of the company: What is the future outlook of the company? How

well are they placed in terms of competition? What opportunities lie before

the company and how well are they equipped to explore and take advantages

of such opportunities? What immediate threats the company faces?

8. Future Outlook of the Industry: Keeping up with the future operations that

firm is going to undertake should be known and considered because this will

effect the price of its shares. Future outlook of the industry in which the

company is operating is an important factor to consider while determining

whether to invest in an IPO. A country's demographic structure, its economic

and political environment as well as its laws and regulations have a

significant impact on the future outlook of any industry.

CONCLUSION

From this report it has been concluded that Trainline has developed at a very

rapid pace in the recent 10 years and continues to do so with its thinking of offering

IPO to public. Further Trainline has been into delivery of rail tickets then they have

been personalized their apps for I Phone and now they are offering IPO to public.

This all has been done by two of the entrepreneurs. So from this report it has been

concluded that for every small business who needs to be at the top have to have a

good leader so that he can take decisions towards the growth of the sector. From

this report it has been concluded that Trainline in order to make his impact on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

world in the coming years should acquire funds from financial institutions or

somewhere else so that they can grow with a steady rate.

somewhere else so that they can grow with a steady rate.

REFERENCES

Books and Journals

Page, J. & Tarp, F., (2017). The Practice of Industrial Policy: GovernmentDLBusiness

Coordination in Africa and East Asia. Oxford University Press.

Hilson, G. & McQuilken, J., (2014). Four decades of support for artisanal and small-scale mining

in sub-Saharan Africa: a critical review. The Extractive Industries and Society. 1(1). pp.104-118.

Marlow, S. & Swail, J., (2014). Gender, risk and finance: why can't a woman be more like a

man?. Entrepreneurship & Regional Development. 26(1-2). pp.80-96.

Abdulsaleh, A. M. & Worthington, A. C., (2013). Small and medium-sized enterprises financing:

A review of literature. International Journal of Business and Management. 8(14). pp.36.

Mahmood, R. & Mohd Rosli, M., (2013). Microcredit position in micro and small enterprise

performance: the Malaysian case. Management research review. 36(5). pp.436-453.

Hultman, M., Bonnedahl, K. J. & O'Neill, K. J., (2016). Unsustainable societies–sustainable

businesses? Introduction to special issue of small enterprise research on transitional

Ecopreneurs. Small Enterprise Research. 23(1). pp.1-9.

Herselman, S., 2014. creating meaning through microfinance: the case of the Small Enterprise

Foundation. South African Review of Sociology. 45(1). pp.45-65.

Abanis, T. & et.al., (2013). Financial Management Practices In Small And Medium Enterprises

in Selected Districts In Western Uganda. Financial Management. 4(2).

Bharati, P. & Chaudhury, A., (2015). SMEs and competitiveness: The role of information

systems.

Zuo, R. & Liu, Z., (2015). Based on the AHP Method to Build Small Medium Enterprise Credit

Rating Index System. Communication of Finance and Accounting. 11. pp.80-83.

Cole, R. A., (2013). What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance.Financial Management. 42(4). pp.777-813.

Chowdhury, M. S. A., Azam, M. K. G. & Islam, S., (2015). Problems and prospects of SME

financing in Bangladesh. Asian Business Review. 2(2). pp.51-58.

Amoako, G. K., (2013). Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). pp.73.

Kamau, L., (2017). WOMEN EMPOWERMENT THROUGH ENTERPRISE

Books and Journals

Page, J. & Tarp, F., (2017). The Practice of Industrial Policy: GovernmentDLBusiness

Coordination in Africa and East Asia. Oxford University Press.

Hilson, G. & McQuilken, J., (2014). Four decades of support for artisanal and small-scale mining

in sub-Saharan Africa: a critical review. The Extractive Industries and Society. 1(1). pp.104-118.

Marlow, S. & Swail, J., (2014). Gender, risk and finance: why can't a woman be more like a

man?. Entrepreneurship & Regional Development. 26(1-2). pp.80-96.

Abdulsaleh, A. M. & Worthington, A. C., (2013). Small and medium-sized enterprises financing:

A review of literature. International Journal of Business and Management. 8(14). pp.36.

Mahmood, R. & Mohd Rosli, M., (2013). Microcredit position in micro and small enterprise

performance: the Malaysian case. Management research review. 36(5). pp.436-453.

Hultman, M., Bonnedahl, K. J. & O'Neill, K. J., (2016). Unsustainable societies–sustainable

businesses? Introduction to special issue of small enterprise research on transitional

Ecopreneurs. Small Enterprise Research. 23(1). pp.1-9.

Herselman, S., 2014. creating meaning through microfinance: the case of the Small Enterprise

Foundation. South African Review of Sociology. 45(1). pp.45-65.

Abanis, T. & et.al., (2013). Financial Management Practices In Small And Medium Enterprises

in Selected Districts In Western Uganda. Financial Management. 4(2).

Bharati, P. & Chaudhury, A., (2015). SMEs and competitiveness: The role of information

systems.

Zuo, R. & Liu, Z., (2015). Based on the AHP Method to Build Small Medium Enterprise Credit

Rating Index System. Communication of Finance and Accounting. 11. pp.80-83.

Cole, R. A., (2013). What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance.Financial Management. 42(4). pp.777-813.

Chowdhury, M. S. A., Azam, M. K. G. & Islam, S., (2015). Problems and prospects of SME

financing in Bangladesh. Asian Business Review. 2(2). pp.51-58.

Amoako, G. K., (2013). Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). pp.73.

Kamau, L., (2017). WOMEN EMPOWERMENT THROUGH ENTERPRISE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.