Transfer Pricing Analysis and Airline Pricing Strategy Report

VerifiedAdded on 2021/06/14

|10

|1461

|46

Report

AI Summary

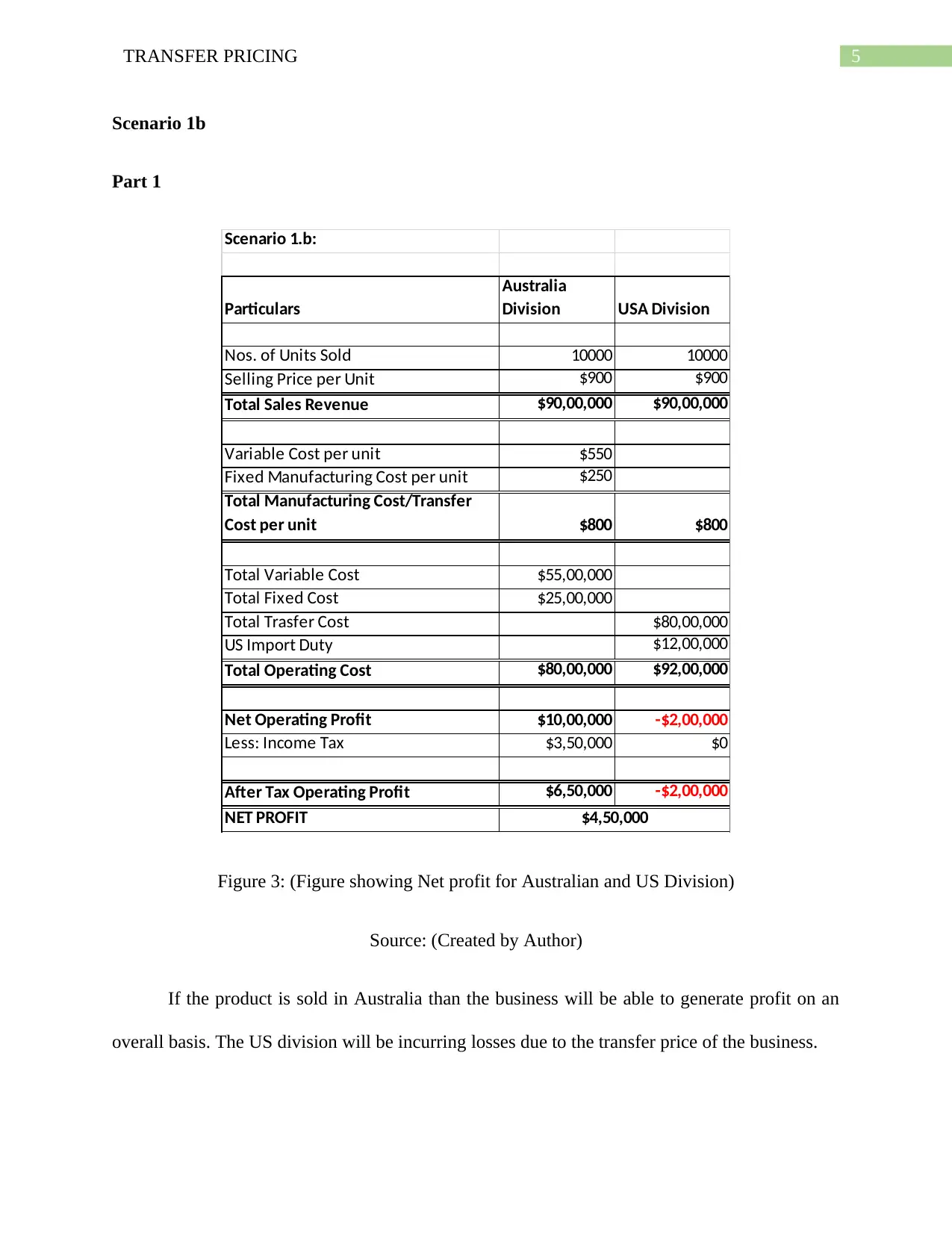

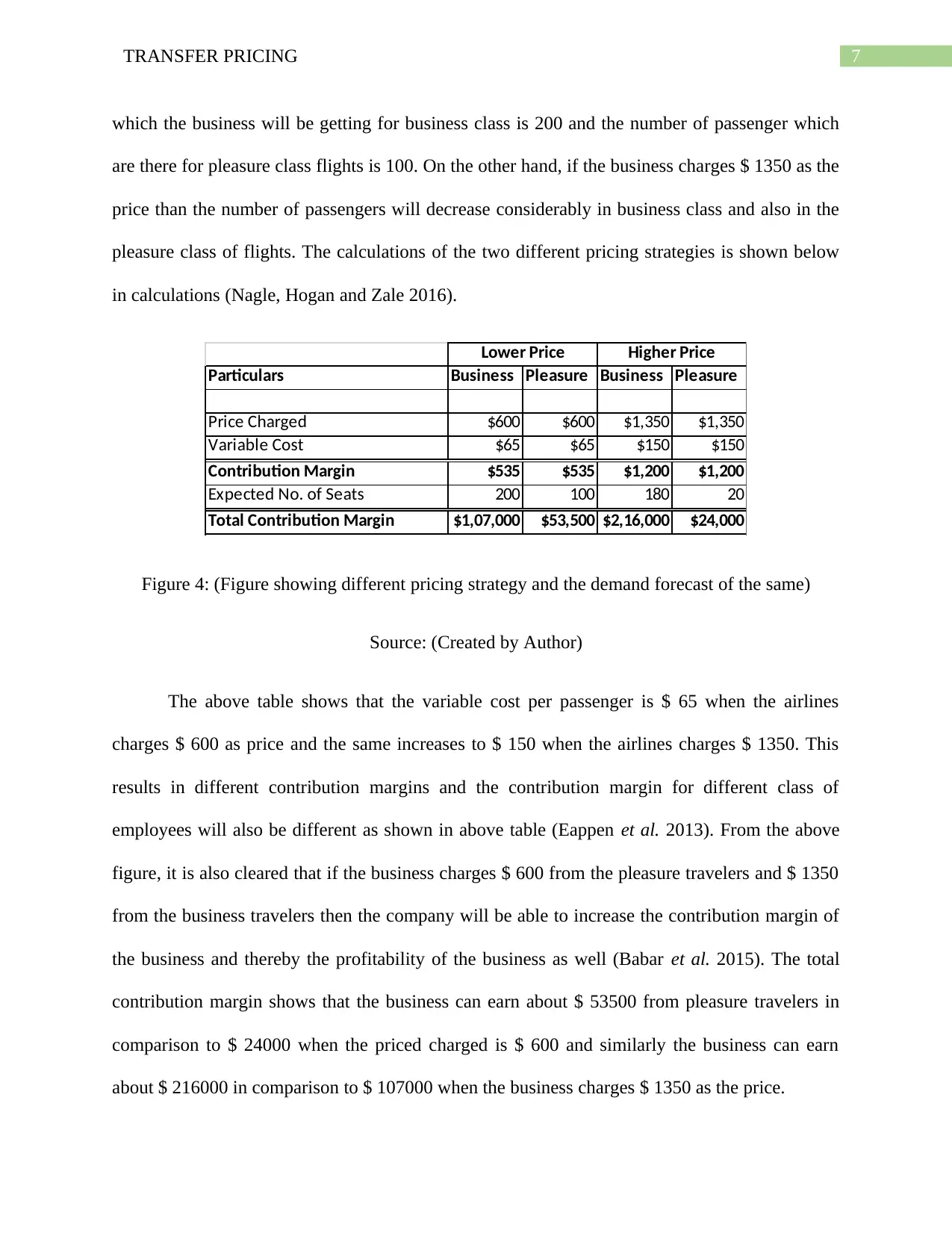

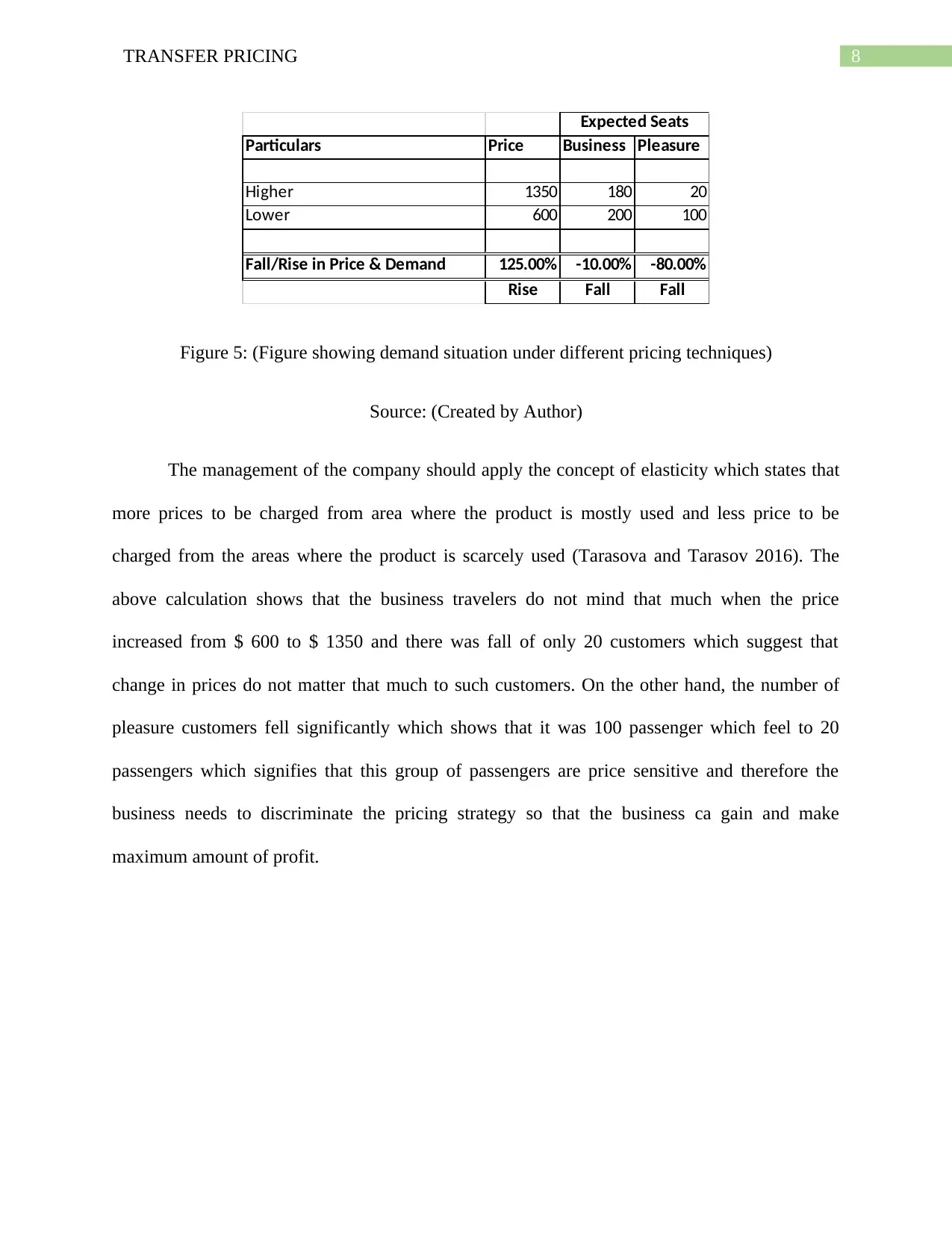

This report delves into transfer pricing and airline pricing strategies, analyzing financial data from Derwent Ltd and Eastcoast Airways. The analysis calculates after-tax operating profits under different transfer pricing scenarios, comparing market rates and their impact on profitability. It also examines how import duties and income taxes are affected by transfer pricing choices. For Eastcoast Airways, the report explores the impact of different pricing strategies on passenger demand, contribution margins, and overall profitability. The report applies elasticity concepts to optimize pricing for business and pleasure travelers, aiming to maximize revenue. Calculations and figures are provided to support the findings, offering insights into financial decision-making and strategic pricing approaches. The report provides a detailed analysis of how different pricing models can affect the profitability of a business. The report also provides various figures to make an effective decision.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.