Analysis of Transfer Pricing in Management Accounting Report

VerifiedAdded on 2022/11/26

|19

|3315

|438

Report

AI Summary

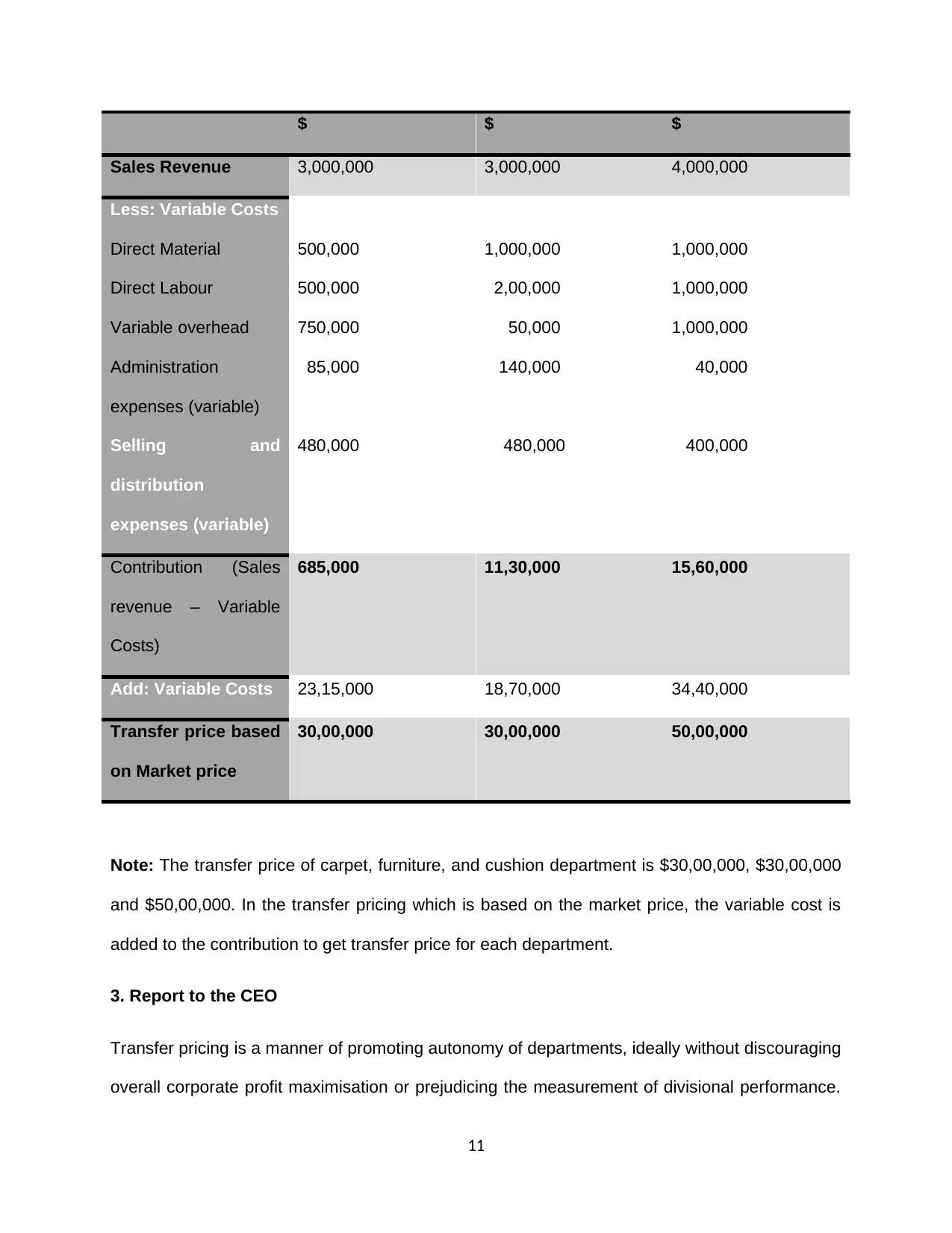

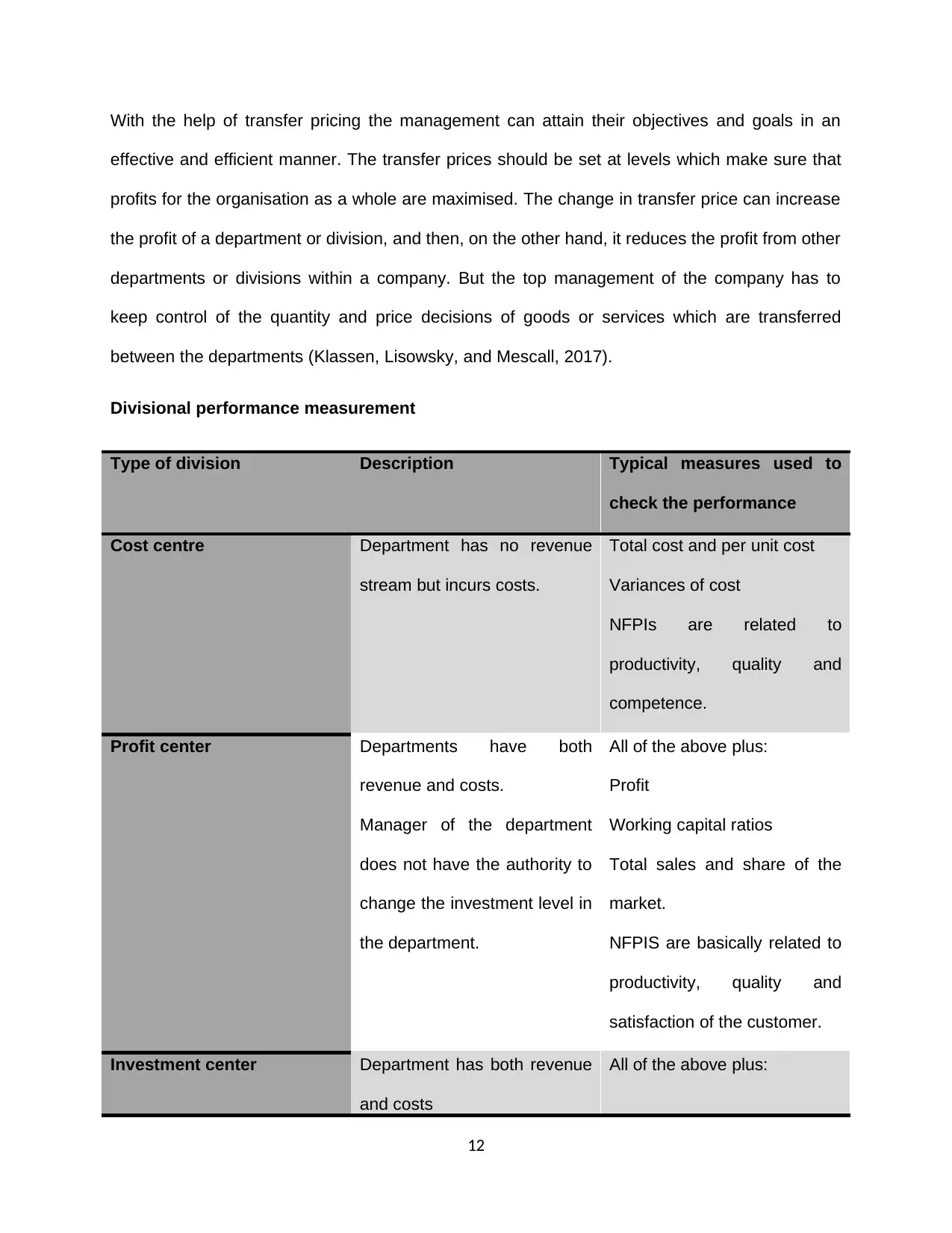

This report delves into the realm of management accounting, specifically focusing on the application of transfer pricing within organizations. The report examines the case of Raven Industries, a company with multiple departments, and analyzes various transfer pricing methods, including market price, negotiated, and dual pricing, to determine optimal solutions for interdepartmental transfers. The executive summary highlights the importance of management accounting in formulating organizational policies and procedures for growth and development. The main body of the report explores the objectives of transfer pricing, such as performance evaluation, autonomy, and goal congruency. The report concludes that the market-based transfer pricing method is the most appropriate approach for the transferor department. Additionally, the report presents financial data, including a profit and loss account, to illustrate the impact of transfer pricing on departmental performance, and it also includes a report to the CEO explaining the benefits of transfer pricing and its effect on divisional performance measurement. The report highlights the benefits of transfer pricing for both the organization and its departments.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.