Evaluation of Transfer Pricing Strategies and Divisional Performance

VerifiedAdded on 2023/03/23

|16

|3663

|44

Report

AI Summary

This report provides an analysis of transfer pricing strategies within Raven Industries, focusing on the impact of different methods on divisional performance and overall company profitability. It addresses the concerns of the Cushion Division manager regarding the use of market price versus cost for internal transfers and explores approaches like dual pricing and negotiated transfer pricing. The report includes a revised profit statement based on contribution margin approach, evaluating the profitability of the Carpet, Furniture, and Cushion divisions. Ultimately, the study recommends strategies to motivate both selling and buying divisions, align with decentralization objectives, improve performance measurement, and enhance managerial autonomy, contributing to the company's overall effectiveness and productivity. Desklib provides a platform to access similar solved assignments and resources for students.

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Transfer price is used for the measurement of the value of goods or services, which are

transferred from one department to another department of the same company. The determination

of the transfer price should be in such a way which increases the overall profitability of the

company. Further, it assists in the achievement of the main objective of the decentralization,

which is the improvisation in the productivity and the effectiveness of the company by the

participation by every division.

Transfer price is used for the measurement of the value of goods or services, which are

transferred from one department to another department of the same company. The determination

of the transfer price should be in such a way which increases the overall profitability of the

company. Further, it assists in the achievement of the main objective of the decentralization,

which is the improvisation in the productivity and the effectiveness of the company by the

participation by every division.

Table of Contents

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Statement by the manager of Cushion Division..........................................................................4

Approaches Company can use to set transfer pricing:.................................................................5

Task 2...........................................................................................................................................9

Task 3.........................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Statement by the manager of Cushion Division..........................................................................4

Approaches Company can use to set transfer pricing:.................................................................5

Task 2...........................................................................................................................................9

Task 3.........................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Transfer price is refers as a selling price of goods or services from the one department of a

company to the other department or associated entity. Setting up of the transfer price is one of

the crucial aspects for the company (Sikka, 2017). Multinational Corporation generally divided

into some departments, and each department is considered as self-contained unit. Therefore, it is

essential for managers to maintain the performance of their division. With this aspect, the present

study is related with the transfer pricing issues. In this problem, Raven Industries has three

different departments, in which one department sales its goods to other department. The study

contains the several techniques for ascertainment of transfer price. Along with this, in this report

the recommendation also provided to the company, by which it could enhance the productivity

and effectiveness of the operations.

ASSESSMENT 3

Task 1

Statement by the manager of Cushion Division

By considering the case scenario, it can be stated that, company has two total divisions, furniture

division and cushion division. However, lately the division of cushion is facing under profits,

and is not profitable enough to meet its cost even. The statement of Cleveland of transfers from

the Cushion Division to the Furniture Division should be at market price rather than at cost, for

performance measurement is considered as correct, due to the fact that cushions are sold at the

outer market, and these commodities must be priced at a cost, that include some of the profit.

Conversely, seeing the unsatisfactory performance of the cushion division, the decision of the

Transfer price is refers as a selling price of goods or services from the one department of a

company to the other department or associated entity. Setting up of the transfer price is one of

the crucial aspects for the company (Sikka, 2017). Multinational Corporation generally divided

into some departments, and each department is considered as self-contained unit. Therefore, it is

essential for managers to maintain the performance of their division. With this aspect, the present

study is related with the transfer pricing issues. In this problem, Raven Industries has three

different departments, in which one department sales its goods to other department. The study

contains the several techniques for ascertainment of transfer price. Along with this, in this report

the recommendation also provided to the company, by which it could enhance the productivity

and effectiveness of the operations.

ASSESSMENT 3

Task 1

Statement by the manager of Cushion Division

By considering the case scenario, it can be stated that, company has two total divisions, furniture

division and cushion division. However, lately the division of cushion is facing under profits,

and is not profitable enough to meet its cost even. The statement of Cleveland of transfers from

the Cushion Division to the Furniture Division should be at market price rather than at cost, for

performance measurement is considered as correct, due to the fact that cushions are sold at the

outer market, and these commodities must be priced at a cost, that include some of the profit.

Conversely, seeing the unsatisfactory performance of the cushion division, the decision of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cleveland is effective, and can result successful, in terms of increasing the profits. Thus, it can

be reflected that for the measurement of performance, should transfer the furniture division at

market price than the cost.

A transfer price is considered as the money amount that a subunit such as department or division

etc of firm charges for product and services from other subunit of a firm. Further, the transfer

price forms optimal revenue for the sold subunit and cost of purchasing for the purchased

subunit, impacting operating income of every subunit (Monsenego, 2015). Transfer price is

engaged with selling goods and services in the organizational departments, it is conducted for the

management of profit and loss ratio of various departments in the organization. The price utilized

to do the valuation of the transfer of goods or service amongst divisions in the similar company

is known as transfer price. Yet, there are distinct approaches for developing a transfer price, the

common economic transfer pricing rules specify that the transfer price are required to be set at

differential cost to the selling division, usually variable cost, added with the opportunity cost of

creating the sale on an internal basis (Cooper and te.al, 2017). The objective is to develop a

transfer pricing that motivates managers to do the aspects that are in the best interest of the

company, at the same time the aspects which are in the best interest of the divisional manager.

Approaches Company can use to set transfer pricing:

Dual pricing:

The dual pricing method makes use of two prices. The division of supplying is credit with a total

cost based on price plus a mark-up as well as the deriving division with marginal cost. Similarly,

the selling division is entitled to gain profits and the receiving divisions is allowed with accurate

information for making appropriate selling decision for the maximization of the corporate or

be reflected that for the measurement of performance, should transfer the furniture division at

market price than the cost.

A transfer price is considered as the money amount that a subunit such as department or division

etc of firm charges for product and services from other subunit of a firm. Further, the transfer

price forms optimal revenue for the sold subunit and cost of purchasing for the purchased

subunit, impacting operating income of every subunit (Monsenego, 2015). Transfer price is

engaged with selling goods and services in the organizational departments, it is conducted for the

management of profit and loss ratio of various departments in the organization. The price utilized

to do the valuation of the transfer of goods or service amongst divisions in the similar company

is known as transfer price. Yet, there are distinct approaches for developing a transfer price, the

common economic transfer pricing rules specify that the transfer price are required to be set at

differential cost to the selling division, usually variable cost, added with the opportunity cost of

creating the sale on an internal basis (Cooper and te.al, 2017). The objective is to develop a

transfer pricing that motivates managers to do the aspects that are in the best interest of the

company, at the same time the aspects which are in the best interest of the divisional manager.

Approaches Company can use to set transfer pricing:

Dual pricing:

The dual pricing method makes use of two prices. The division of supplying is credit with a total

cost based on price plus a mark-up as well as the deriving division with marginal cost. Similarly,

the selling division is entitled to gain profits and the receiving divisions is allowed with accurate

information for making appropriate selling decision for the maximization of the corporate or

division’s profit (Rugman and Eden, 2017). Under the approach of dual pricing, the selling price

derived by the upstream division varies from the buying price payable by the downstream

division. By considering this approach, Division A transfers out at cost added up with a mark-up

and B division transfer the same at variable cost. Thus, the division A can make a profit based on

motivation, at the same time Division B is benefitted with optimal economic data regarding the

cumulative group variable costs. Indeed, the divisional current account does not agree with this,

and there would be requirement of certain period-end adjustments to reconcile those and to

reduce untrue interdivisional profits (Clempner and Poznyak, 2018).

Dual price provides motivation to selling divisions as well as buying division, goods are

transferrable to market price and eventually it offers the reduced cost to the respective buying

division (Jack and Mundy, 2013) . Henceforth, dual pricing approach has the characteristic of

motivating selling division as well as buying division that are reliable with the entire

decentralisation purposes, which are higher motivation provided to divisional managers, goal

congruence, proper performance measurement and autonomy.

The dual pricing can be used with the market price in the given case in place of the marginal cost

for the receiving division. Further, this can help the supplying division in a specified scenario.

For instance, when there is volatility in market process and the market price of the component

collapses in a sudden way, then it might be non-realistic to believe the supplying division to

overcome with the reduction (Ito and Komoriya, 2015). In this situation, the receiving division

would be willing to purchase elsewhere in case the transfer price set is higher as compared to the

market price. Thus, the supplying division can be credited with the total costs, and debiting the

receiving division with the decreased market price. The dual pricing is beneficial for the

derived by the upstream division varies from the buying price payable by the downstream

division. By considering this approach, Division A transfers out at cost added up with a mark-up

and B division transfer the same at variable cost. Thus, the division A can make a profit based on

motivation, at the same time Division B is benefitted with optimal economic data regarding the

cumulative group variable costs. Indeed, the divisional current account does not agree with this,

and there would be requirement of certain period-end adjustments to reconcile those and to

reduce untrue interdivisional profits (Clempner and Poznyak, 2018).

Dual price provides motivation to selling divisions as well as buying division, goods are

transferrable to market price and eventually it offers the reduced cost to the respective buying

division (Jack and Mundy, 2013) . Henceforth, dual pricing approach has the characteristic of

motivating selling division as well as buying division that are reliable with the entire

decentralisation purposes, which are higher motivation provided to divisional managers, goal

congruence, proper performance measurement and autonomy.

The dual pricing can be used with the market price in the given case in place of the marginal cost

for the receiving division. Further, this can help the supplying division in a specified scenario.

For instance, when there is volatility in market process and the market price of the component

collapses in a sudden way, then it might be non-realistic to believe the supplying division to

overcome with the reduction (Ito and Komoriya, 2015). In this situation, the receiving division

would be willing to purchase elsewhere in case the transfer price set is higher as compared to the

market price. Thus, the supplying division can be credited with the total costs, and debiting the

receiving division with the decreased market price. The dual pricing is beneficial for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company in terms of sound decisions, incentive to transferring divisions and no unjust

enrichment.

Negotiated transfer Price

It means the identification of transfer prices on the basis of active engagement, participation,

collaboration and consent of managers of the recipient division and transferring. Principally, in

case the division managers interpret their individual business and are collaborative, then the

negotiated transfer price would be more effective. It is easy in such a circumstance to search out

for a transfer price that would help in increasing each related divisions profit (Abdallah, 2016).

At the same time, negotiated transfer price can be effective under accurate conditions; in case the

managers are fiercely competitive and uncooperative then negotiations might not be lost. There

are benefits to the company, when using negotiated transfer prices, inclusive of better decision

making, as negotiated process result into business-oriented behaviour between the divisions of

company (Solilova and Nerudova, 2018). The buying division might but from external source, in

case the external prices are lesser as compared to the price of internal division. It also benefits

with optimal autonomy as well as motivation value; every sub-unit is stated as a free unit. In this

way, buyers, as well as sellers, are totally independent to assess external of the company. This

supports the autonomy of the subunit and increases motivation amongst managers. It is also

advantageous in terms of inclusive corporate profitability; it is because, with the help of proper

direct negotiations, division managers would be capable of identifying the most suitable transfer

prices that meet the requirements and criteria of the division and is incorporate the best interest

(Klassen, Lisowsky and Mescall, 2017). On the other hand, there is no rationale to estimate that

the result of such transfer pricing negotiations will deliver the corporate, divisional managers and

shareholder best interest. In addition, in case the divisional manager did not succeed to arrive at a

enrichment.

Negotiated transfer Price

It means the identification of transfer prices on the basis of active engagement, participation,

collaboration and consent of managers of the recipient division and transferring. Principally, in

case the division managers interpret their individual business and are collaborative, then the

negotiated transfer price would be more effective. It is easy in such a circumstance to search out

for a transfer price that would help in increasing each related divisions profit (Abdallah, 2016).

At the same time, negotiated transfer price can be effective under accurate conditions; in case the

managers are fiercely competitive and uncooperative then negotiations might not be lost. There

are benefits to the company, when using negotiated transfer prices, inclusive of better decision

making, as negotiated process result into business-oriented behaviour between the divisions of

company (Solilova and Nerudova, 2018). The buying division might but from external source, in

case the external prices are lesser as compared to the price of internal division. It also benefits

with optimal autonomy as well as motivation value; every sub-unit is stated as a free unit. In this

way, buyers, as well as sellers, are totally independent to assess external of the company. This

supports the autonomy of the subunit and increases motivation amongst managers. It is also

advantageous in terms of inclusive corporate profitability; it is because, with the help of proper

direct negotiations, division managers would be capable of identifying the most suitable transfer

prices that meet the requirements and criteria of the division and is incorporate the best interest

(Klassen, Lisowsky and Mescall, 2017). On the other hand, there is no rationale to estimate that

the result of such transfer pricing negotiations will deliver the corporate, divisional managers and

shareholder best interest. In addition, in case the divisional manager did not succeed to arrive at a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pricing agreement, even though the transfer is well-set and is in the best interest of the company,

top management may further make decisions to enforce a transfer price. On the other hand, the

imposition of top management of a transfer price overcomes the motivation for making use of

negotiated transfer price at the first instance. Division managers are generally likely to act free of

each other. To support the autonomy of every division managers, the company generally need

the buying and selling division for the negotiation of a transfer price. This seems to be viable in

concept, but in using this approach, weakness also exists, as using cost for setting transfer price

(Löffler, 2018). Further, the buying division might opt to buy the goods or services from an

external source if there is a breakdown in negotiation, which might eventually result to a

suboptimal decision for the company as a large. A further weakness is a time needed to do the

negotiation with the transfer pricing. However, managers spend a considerable amount of time

while negotiating when the time may be effectively spent in a productive way in the division

elsewhere.

It might be vital to negotiate a transfer price among subsidiaries, in the absence of employing

any market price as a base. Further, this scenario takes place where the discernible market price

is not present, as the market is comparatively very small or the products are heavily customized.

This leads to prices that are dependent on the comparative negotiating party skills (Epstein and

Malina , 2015) . Through the negotiated transfer pricing, specified corporate units do the

negotiation of price, irrespective of the market baseline price. As a matter of fact, it seems quite

different as compared to the existing market price. This approach is selected by companies when

the market price tends to be complex to compute, there is a restriction in the market for goods or

services, or the commodity is highly customized.

top management may further make decisions to enforce a transfer price. On the other hand, the

imposition of top management of a transfer price overcomes the motivation for making use of

negotiated transfer price at the first instance. Division managers are generally likely to act free of

each other. To support the autonomy of every division managers, the company generally need

the buying and selling division for the negotiation of a transfer price. This seems to be viable in

concept, but in using this approach, weakness also exists, as using cost for setting transfer price

(Löffler, 2018). Further, the buying division might opt to buy the goods or services from an

external source if there is a breakdown in negotiation, which might eventually result to a

suboptimal decision for the company as a large. A further weakness is a time needed to do the

negotiation with the transfer pricing. However, managers spend a considerable amount of time

while negotiating when the time may be effectively spent in a productive way in the division

elsewhere.

It might be vital to negotiate a transfer price among subsidiaries, in the absence of employing

any market price as a base. Further, this scenario takes place where the discernible market price

is not present, as the market is comparatively very small or the products are heavily customized.

This leads to prices that are dependent on the comparative negotiating party skills (Epstein and

Malina , 2015) . Through the negotiated transfer pricing, specified corporate units do the

negotiation of price, irrespective of the market baseline price. As a matter of fact, it seems quite

different as compared to the existing market price. This approach is selected by companies when

the market price tends to be complex to compute, there is a restriction in the market for goods or

services, or the commodity is highly customized.

Based on the above analysis, it can be stated that using the approaches of either the negotiated

pricing or dual pricing, there can be inducement and motivation in both selling and buying

divisions also, the division managers would be encouraged to make optimal decisions stabilized

with goal congruence, decentralization objectives, better performance measurement and

adequate motivation for the division managers.

Task 2

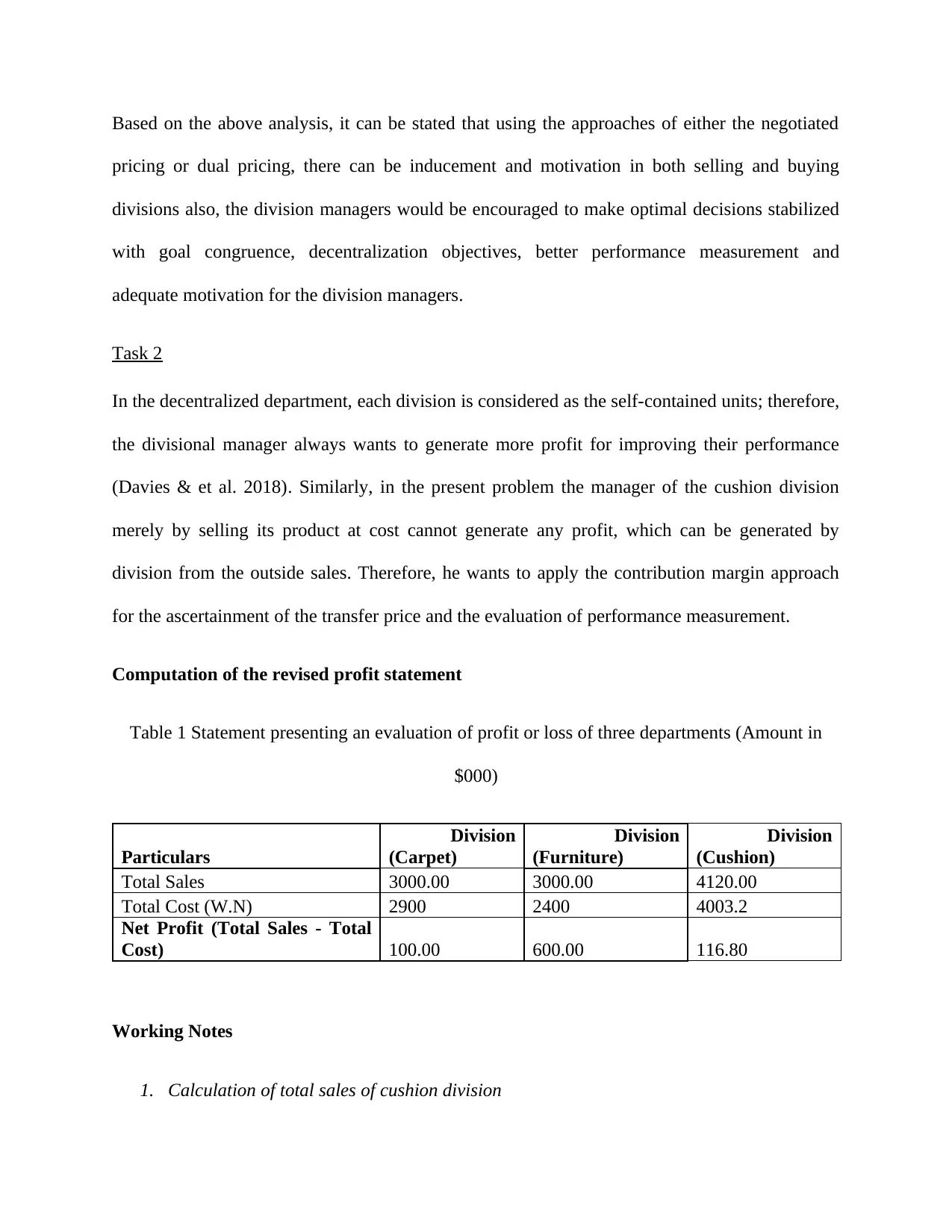

In the decentralized department, each division is considered as the self-contained units; therefore,

the divisional manager always wants to generate more profit for improving their performance

(Davies & et al. 2018). Similarly, in the present problem the manager of the cushion division

merely by selling its product at cost cannot generate any profit, which can be generated by

division from the outside sales. Therefore, he wants to apply the contribution margin approach

for the ascertainment of the transfer price and the evaluation of performance measurement.

Computation of the revised profit statement

Table 1 Statement presenting an evaluation of profit or loss of three departments (Amount in

$000)

Particulars

Division

(Carpet)

Division

(Furniture)

Division

(Cushion)

Total Sales 3000.00 3000.00 4120.00

Total Cost (W.N) 2900 2400 4003.2

Net Profit (Total Sales - Total

Cost) 100.00 600.00 116.80

Working Notes

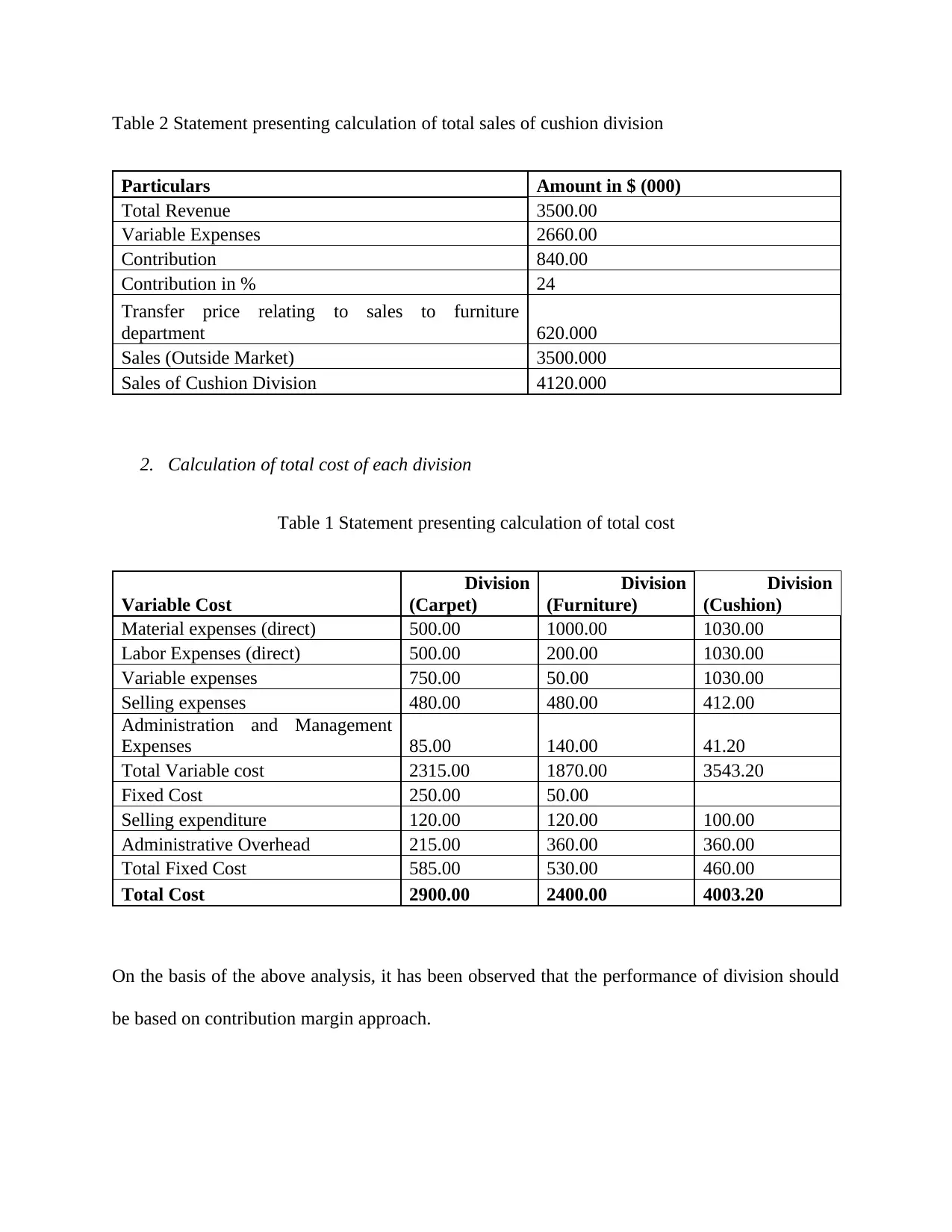

1. Calculation of total sales of cushion division

pricing or dual pricing, there can be inducement and motivation in both selling and buying

divisions also, the division managers would be encouraged to make optimal decisions stabilized

with goal congruence, decentralization objectives, better performance measurement and

adequate motivation for the division managers.

Task 2

In the decentralized department, each division is considered as the self-contained units; therefore,

the divisional manager always wants to generate more profit for improving their performance

(Davies & et al. 2018). Similarly, in the present problem the manager of the cushion division

merely by selling its product at cost cannot generate any profit, which can be generated by

division from the outside sales. Therefore, he wants to apply the contribution margin approach

for the ascertainment of the transfer price and the evaluation of performance measurement.

Computation of the revised profit statement

Table 1 Statement presenting an evaluation of profit or loss of three departments (Amount in

$000)

Particulars

Division

(Carpet)

Division

(Furniture)

Division

(Cushion)

Total Sales 3000.00 3000.00 4120.00

Total Cost (W.N) 2900 2400 4003.2

Net Profit (Total Sales - Total

Cost) 100.00 600.00 116.80

Working Notes

1. Calculation of total sales of cushion division

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table 2 Statement presenting calculation of total sales of cushion division

Particulars Amount in $ (000)

Total Revenue 3500.00

Variable Expenses 2660.00

Contribution 840.00

Contribution in % 24

Transfer price relating to sales to furniture

department 620.000

Sales (Outside Market) 3500.000

Sales of Cushion Division 4120.000

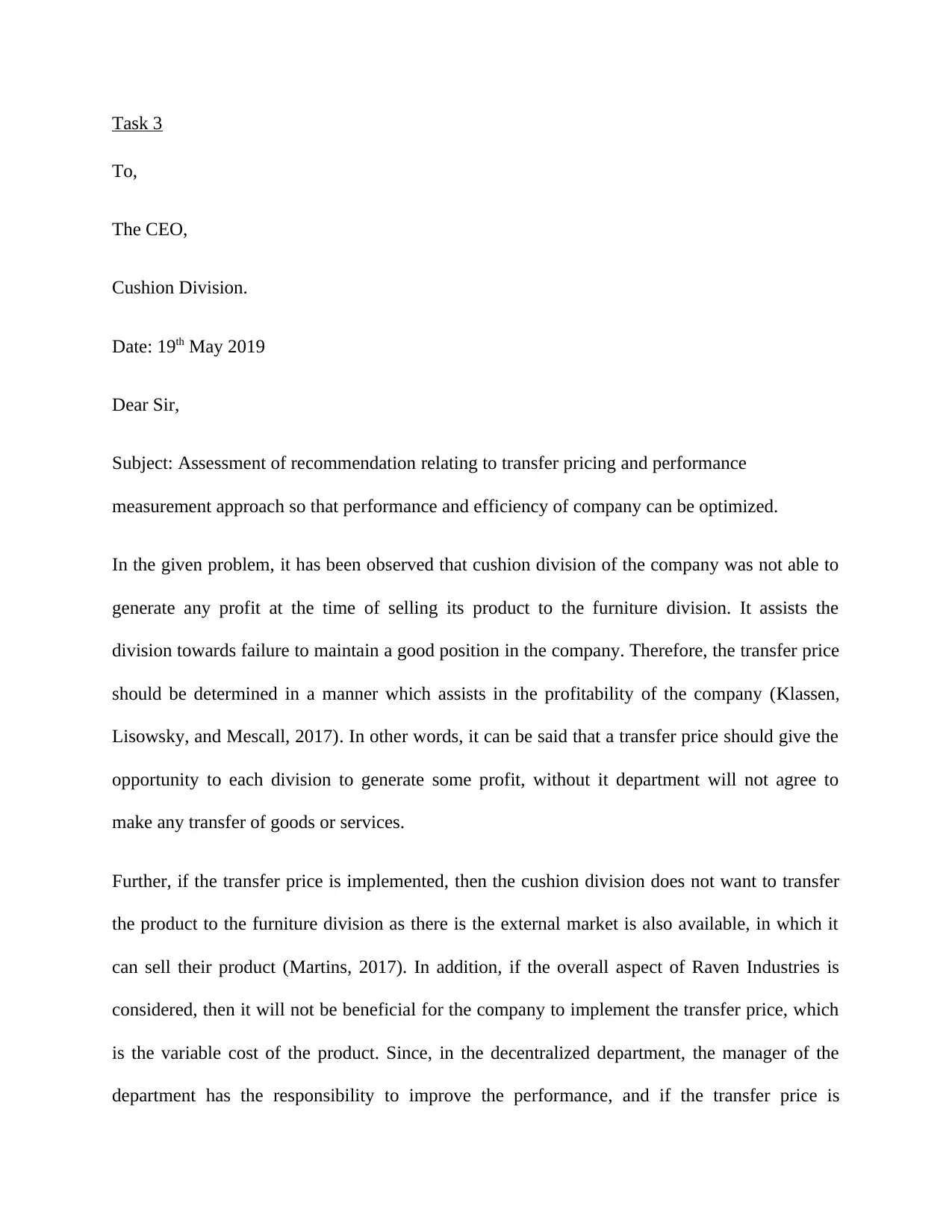

2. Calculation of total cost of each division

Table 1 Statement presenting calculation of total cost

Variable Cost

Division

(Carpet)

Division

(Furniture)

Division

(Cushion)

Material expenses (direct) 500.00 1000.00 1030.00

Labor Expenses (direct) 500.00 200.00 1030.00

Variable expenses 750.00 50.00 1030.00

Selling expenses 480.00 480.00 412.00

Administration and Management

Expenses 85.00 140.00 41.20

Total Variable cost 2315.00 1870.00 3543.20

Fixed Cost 250.00 50.00

Selling expenditure 120.00 120.00 100.00

Administrative Overhead 215.00 360.00 360.00

Total Fixed Cost 585.00 530.00 460.00

Total Cost 2900.00 2400.00 4003.20

On the basis of the above analysis, it has been observed that the performance of division should

be based on contribution margin approach.

Particulars Amount in $ (000)

Total Revenue 3500.00

Variable Expenses 2660.00

Contribution 840.00

Contribution in % 24

Transfer price relating to sales to furniture

department 620.000

Sales (Outside Market) 3500.000

Sales of Cushion Division 4120.000

2. Calculation of total cost of each division

Table 1 Statement presenting calculation of total cost

Variable Cost

Division

(Carpet)

Division

(Furniture)

Division

(Cushion)

Material expenses (direct) 500.00 1000.00 1030.00

Labor Expenses (direct) 500.00 200.00 1030.00

Variable expenses 750.00 50.00 1030.00

Selling expenses 480.00 480.00 412.00

Administration and Management

Expenses 85.00 140.00 41.20

Total Variable cost 2315.00 1870.00 3543.20

Fixed Cost 250.00 50.00

Selling expenditure 120.00 120.00 100.00

Administrative Overhead 215.00 360.00 360.00

Total Fixed Cost 585.00 530.00 460.00

Total Cost 2900.00 2400.00 4003.20

On the basis of the above analysis, it has been observed that the performance of division should

be based on contribution margin approach.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

To,

The CEO,

Cushion Division.

Date: 19th May 2019

Dear Sir,

Subject: Assessment of recommendation relating to transfer pricing and performance

measurement approach so that performance and efficiency of company can be optimized.

In the given problem, it has been observed that cushion division of the company was not able to

generate any profit at the time of selling its product to the furniture division. It assists the

division towards failure to maintain a good position in the company. Therefore, the transfer price

should be determined in a manner which assists in the profitability of the company (Klassen,

Lisowsky, and Mescall, 2017). In other words, it can be said that a transfer price should give the

opportunity to each division to generate some profit, without it department will not agree to

make any transfer of goods or services.

Further, if the transfer price is implemented, then the cushion division does not want to transfer

the product to the furniture division as there is the external market is also available, in which it

can sell their product (Martins, 2017). In addition, if the overall aspect of Raven Industries is

considered, then it will not be beneficial for the company to implement the transfer price, which

is the variable cost of the product. Since, in the decentralized department, the manager of the

department has the responsibility to improve the performance, and if the transfer price is

To,

The CEO,

Cushion Division.

Date: 19th May 2019

Dear Sir,

Subject: Assessment of recommendation relating to transfer pricing and performance

measurement approach so that performance and efficiency of company can be optimized.

In the given problem, it has been observed that cushion division of the company was not able to

generate any profit at the time of selling its product to the furniture division. It assists the

division towards failure to maintain a good position in the company. Therefore, the transfer price

should be determined in a manner which assists in the profitability of the company (Klassen,

Lisowsky, and Mescall, 2017). In other words, it can be said that a transfer price should give the

opportunity to each division to generate some profit, without it department will not agree to

make any transfer of goods or services.

Further, if the transfer price is implemented, then the cushion division does not want to transfer

the product to the furniture division as there is the external market is also available, in which it

can sell their product (Martins, 2017). In addition, if the overall aspect of Raven Industries is

considered, then it will not be beneficial for the company to implement the transfer price, which

is the variable cost of the product. Since, in the decentralized department, the manager of the

department has the responsibility to improve the performance, and if the transfer price is

ascertained at the cost, then the performance of the division cannot be measured in a proper

manner. Along with this, for the enhancement of performance with the effectiveness, it is

essential to motivate the departmental managers, which assist the overall growth of the company

(PAVONE, and DI NUNZIO, 2018). It is possible through only performance measurement.

Moreover, if the employees of the division found that, due to the transfer price division are not

able to generate any profit, then they got demotivated and by which their performance will be

influenced in the adverse manner (Gao, and Zhao, 2015). Further, if the company has a policy of

the performance-related pay, and then the salary or wages of the each employee is affected by

the change in profit. If they feel that, their salary is affected not in a fair manner, then the morals

of the employee reduced (Bhattacharjee, and Moreno, 2017). Apart from this, if the performance

of the division is measured by the Return on investment or residual income, and if the transfer

price is considered at cost, then management may wrongly evaluate the performance of the

division, then they may take wrong decision (Hong, and Li, 2017). Although, there are some

challenges, because if the division only wants to increase their growth only and do not consider

the overall growth of the company, then it may lead to the adverse impact, and the feeling of

competitiveness will take place internally. Therefore, the company should apply he balanced

aaprach which assist in the overall profitability.

By considering the above analysis, it has been recommended that Raven Industry should apply

the performance measurement, by which it could enhance the effectiveness and the productivity.

CONCLUSION

Determination of the transfer price is one of the major challenges for the organizations. By

considering the above analysis, it has been drawn that the ascertainment of the appropriate

manner. Along with this, for the enhancement of performance with the effectiveness, it is

essential to motivate the departmental managers, which assist the overall growth of the company

(PAVONE, and DI NUNZIO, 2018). It is possible through only performance measurement.

Moreover, if the employees of the division found that, due to the transfer price division are not

able to generate any profit, then they got demotivated and by which their performance will be

influenced in the adverse manner (Gao, and Zhao, 2015). Further, if the company has a policy of

the performance-related pay, and then the salary or wages of the each employee is affected by

the change in profit. If they feel that, their salary is affected not in a fair manner, then the morals

of the employee reduced (Bhattacharjee, and Moreno, 2017). Apart from this, if the performance

of the division is measured by the Return on investment or residual income, and if the transfer

price is considered at cost, then management may wrongly evaluate the performance of the

division, then they may take wrong decision (Hong, and Li, 2017). Although, there are some

challenges, because if the division only wants to increase their growth only and do not consider

the overall growth of the company, then it may lead to the adverse impact, and the feeling of

competitiveness will take place internally. Therefore, the company should apply he balanced

aaprach which assist in the overall profitability.

By considering the above analysis, it has been recommended that Raven Industry should apply

the performance measurement, by which it could enhance the effectiveness and the productivity.

CONCLUSION

Determination of the transfer price is one of the major challenges for the organizations. By

considering the above analysis, it has been drawn that the ascertainment of the appropriate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.