Transfer Pricing and its Impact on Company Performance

VerifiedAdded on 2023/04/20

|3

|376

|478

Report

AI Summary

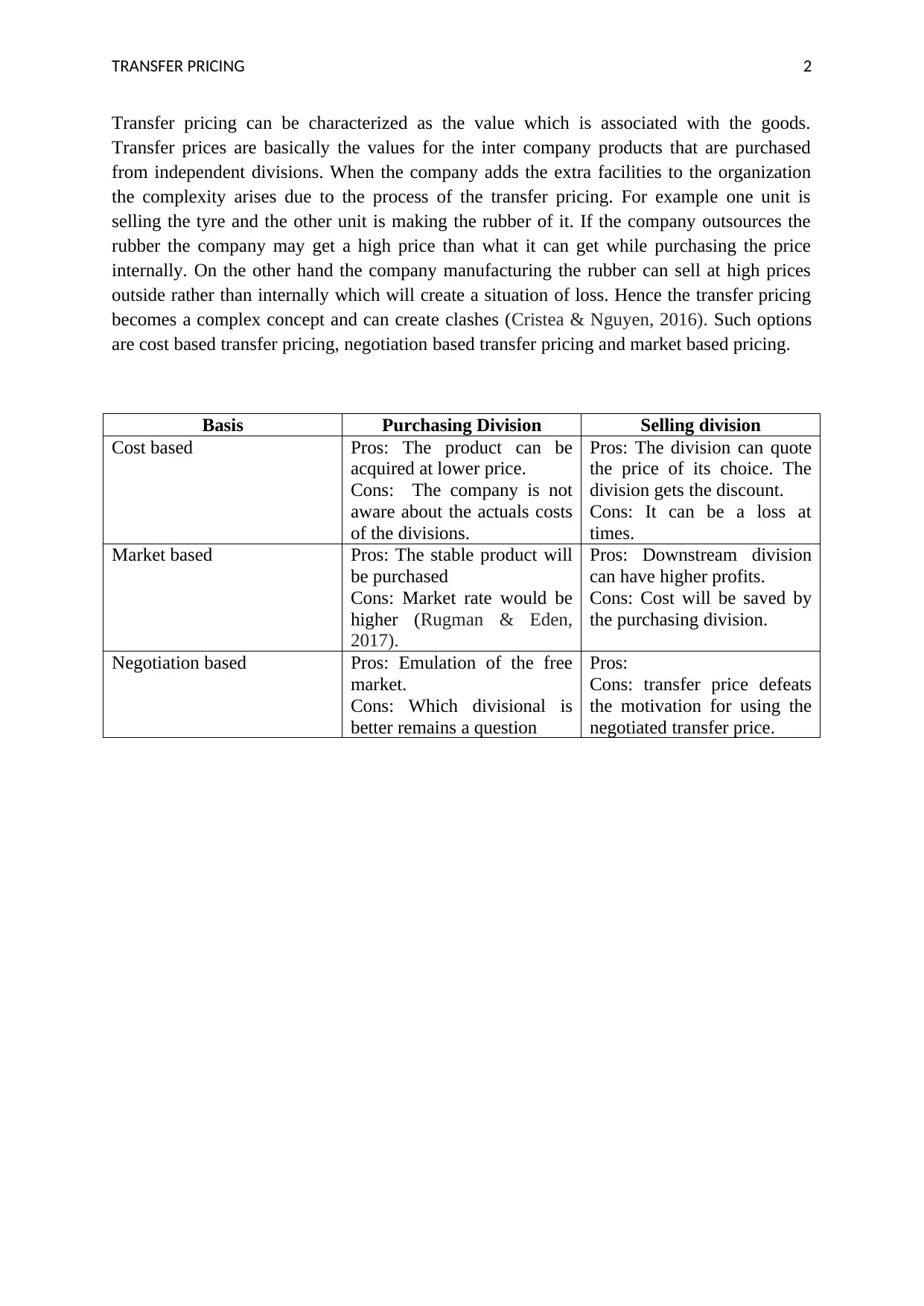

This report examines the concept of transfer pricing, focusing on its application within multinational firms. It highlights the complexities that arise when different divisions within a company engage in inter-company transactions, especially when one division supplies goods or services to another. The report explores three primary transfer pricing methods: cost-based, market-based, and negotiation-based. It analyzes the pros and cons of each method from the perspectives of both the purchasing and selling divisions, considering factors such as pricing, cost control, and potential for profit maximization. References include academic research on transfer pricing by Cristea & Nguyen (2016) and Rugman & Eden (2017), providing a comprehensive overview of the subject matter.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.