Transfer Pricing and Performance Measurement at Raven Industries

VerifiedAdded on 2022/11/27

|16

|3736

|192

Report

AI Summary

This report examines transfer pricing within Raven Industries, focusing on the determination of prices for goods and services transferred between divisions. It explores the significance of transfer pricing in decentralized organizations and its impact on divisional performance. The report analyzes various transfer pricing methods, including negotiated pricing, cost-based methods, market price, and the contribution margin approach, evaluating their suitability for Raven Industries. It highlights the importance of aligning transfer pricing with performance measurement to enhance overall company efficiency and productivity. The analysis includes calculations of contribution margins and revised profit statements to demonstrate the effects of different transfer pricing strategies. The report recommends the most effective transfer pricing and performance measurement approach for Raven Industries, aiming to optimize the company's financial outcomes. This study emphasizes the importance of transfer pricing in fostering departmental accountability and maximizing company profitability.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Generally,organizations apply the decentralization method for running the operations. With this

aspect, sometimes internal transfer takes place among the division due to which the role of

transfer price is very important. The present study revolves around the determination of transfer

price with the main objective of enhancement of the productivity and efficiency of the overall

company. It is the price at which one department transfers its goods and services to another

department. There are several approaches such as negotiated pricing method, cost method,

market price and others, by which transfer price can be determined by the company. The study

concludes that the performance basis approach is most suitable to evaluate the overall efficiency

of the business.

Generally,organizations apply the decentralization method for running the operations. With this

aspect, sometimes internal transfer takes place among the division due to which the role of

transfer price is very important. The present study revolves around the determination of transfer

price with the main objective of enhancement of the productivity and efficiency of the overall

company. It is the price at which one department transfers its goods and services to another

department. There are several approaches such as negotiated pricing method, cost method,

market price and others, by which transfer price can be determined by the company. The study

concludes that the performance basis approach is most suitable to evaluate the overall efficiency

of the business.

Table of Contents

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Task 2...........................................................................................................................................8

Task 3.........................................................................................................................................10

Conclusion.....................................................................................................................................12

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Task 2...........................................................................................................................................8

Task 3.........................................................................................................................................10

Conclusion.....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In large corporations, the company divides its operation into some departments. Sometimes, one

department of a company can sell its product outside the company or transfer its product to other

division as per the requirement. At the time of transfer of goods to another department, the

determination of the transfer price plays a significant role. Along with this, the manager of the

division is accountable for their performance of the division. Therefore they want to improve the

performance if division (Davies et al. 2018). The present report is related with the Raven

Industries, which has three distinct divisions. The report contains the issues related to the

determination of the transfer price and appropriate method which should be considered for

transfer price. Along with this, among the transfer pricing and the performance measurement

approach, the recommendation to the company also provided, which assist in the optimization of

performance and effectiveness.

TASK 1

Explanation related to the statement made by Cleveland for the determination of transfer price

The issue of transfer price arises at the time when the division of one company transfers its

goods or services to other division of the company. Generally, the departmental manager

isresponsible for the performance of their own division. Therefore they want to determine the

transfer price in such a way by which profit of the department can be maximized (Wu, and Lu,

2018). On the other hand, other division may not want to pay the higher price for purchasing of

the product. Therefore, sometime conflicts may take place in the department. Generally, it is

closely related with the market price of the product, so that there will be no significant difference

In large corporations, the company divides its operation into some departments. Sometimes, one

department of a company can sell its product outside the company or transfer its product to other

division as per the requirement. At the time of transfer of goods to another department, the

determination of the transfer price plays a significant role. Along with this, the manager of the

division is accountable for their performance of the division. Therefore they want to improve the

performance if division (Davies et al. 2018). The present report is related with the Raven

Industries, which has three distinct divisions. The report contains the issues related to the

determination of the transfer price and appropriate method which should be considered for

transfer price. Along with this, among the transfer pricing and the performance measurement

approach, the recommendation to the company also provided, which assist in the optimization of

performance and effectiveness.

TASK 1

Explanation related to the statement made by Cleveland for the determination of transfer price

The issue of transfer price arises at the time when the division of one company transfers its

goods or services to other division of the company. Generally, the departmental manager

isresponsible for the performance of their own division. Therefore they want to determine the

transfer price in such a way by which profit of the department can be maximized (Wu, and Lu,

2018). On the other hand, other division may not want to pay the higher price for purchasing of

the product. Therefore, sometime conflicts may take place in the department. Generally, it is

closely related with the market price of the product, so that there will be no significant difference

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in purchasing or selling in the external market or to another department (Tran, Croson, and

Seldon, 2016).

In the present case, Raven Industries has three divisions. The cushion division of the company

sells its product to the furniture division at the variable cost of the product. No profit is earned by

the cushion division from this transfer; therefore, it assists in the reduction of the performance of

the division. Since the product has the external market, and by this cushion division can generate

the profit and improve its performance. Therefore the manager of the cushion division was not

happy with the existing performance and wants to transfer the furniture division at the transfer

price, which is based on the contribution margin approach. It has seemed that manager of the

cushion division was right, as he is accountable for the performance of division; therefore,

maximization of the profit of division is the main objective. Moreover, due to the external

market of the product, he can sell the product and generate profits. On the basis of this, for

performance measurement, the determination of the transfer price should be based on market

price instead of the variable cost.

Description of the other approaches that could be used by the company to ascertain the transfer

price, except manufacturing cost or market price

The ascertainment of the transfer price plays a very important role related to the performance of

the company. There are several methods by which the transfer price can be determined, which

are as follows –

Negotiated transfer price method

This method is formed on the basis of negotiation among the buying division and selling a

division of a company. This method is suitable; it is probable that negotiation assists in the

Seldon, 2016).

In the present case, Raven Industries has three divisions. The cushion division of the company

sells its product to the furniture division at the variable cost of the product. No profit is earned by

the cushion division from this transfer; therefore, it assists in the reduction of the performance of

the division. Since the product has the external market, and by this cushion division can generate

the profit and improve its performance. Therefore the manager of the cushion division was not

happy with the existing performance and wants to transfer the furniture division at the transfer

price, which is based on the contribution margin approach. It has seemed that manager of the

cushion division was right, as he is accountable for the performance of division; therefore,

maximization of the profit of division is the main objective. Moreover, due to the external

market of the product, he can sell the product and generate profits. On the basis of this, for

performance measurement, the determination of the transfer price should be based on market

price instead of the variable cost.

Description of the other approaches that could be used by the company to ascertain the transfer

price, except manufacturing cost or market price

The ascertainment of the transfer price plays a very important role related to the performance of

the company. There are several methods by which the transfer price can be determined, which

are as follows –

Negotiated transfer price method

This method is formed on the basis of negotiation among the buying division and selling a

division of a company. This method is suitable; it is probable that negotiation assists in the

overall profitability of the company, which would be adopted by the related parties. For the

implementation of this method, the formal meeting can be called by the top executives of the

company (Hamamura, 2019). In this meeting, managers of the buying and selling department

make the discussion and decide the transfer price. Moreover, this method is workable only if it

impacts the profit centre of business. However, implementation of this method is not very easy,

as it is time-consuming. Further, conflict may arise among the buying division and selling

division (Johnson, Johnson, and Pfeiffer, 2016).

It has been observed that negotiated price is the results of the discussion among the two

divisions; there are so many advantages of this method, which are as follows –

This method is consistent with the main motive of the decentralization. Since, the main

objective of decentralization is to improve the performance and effectiveness of the

operations of the company by delegating the responsibility and authority to the other

divisions (Clempner, 2019).

Negotiated pricing method also safeguards the autonomy of the division.

Further, it is likely that managers of the department have full knowledge regarding the

cost and advantages of the transfer as compared with the other executives of the company

(Sengul, 2018). Therefore, they can decide the price in a proper manner, which leads to

the overall profitability of the company.

When this method is implemented in a company for the determination of the transfer price, then

the managers of the department who are involving in the transfer make the discussion and agreed

on the terms and condition. They may choose not to transfer if the terms and condition of transfer

price are not agreed upon by the managers. Further, the selling division of the company will

implementation of this method, the formal meeting can be called by the top executives of the

company (Hamamura, 2019). In this meeting, managers of the buying and selling department

make the discussion and decide the transfer price. Moreover, this method is workable only if it

impacts the profit centre of business. However, implementation of this method is not very easy,

as it is time-consuming. Further, conflict may arise among the buying division and selling

division (Johnson, Johnson, and Pfeiffer, 2016).

It has been observed that negotiated price is the results of the discussion among the two

divisions; there are so many advantages of this method, which are as follows –

This method is consistent with the main motive of the decentralization. Since, the main

objective of decentralization is to improve the performance and effectiveness of the

operations of the company by delegating the responsibility and authority to the other

divisions (Clempner, 2019).

Negotiated pricing method also safeguards the autonomy of the division.

Further, it is likely that managers of the department have full knowledge regarding the

cost and advantages of the transfer as compared with the other executives of the company

(Sengul, 2018). Therefore, they can decide the price in a proper manner, which leads to

the overall profitability of the company.

When this method is implemented in a company for the determination of the transfer price, then

the managers of the department who are involving in the transfer make the discussion and agreed

on the terms and condition. They may choose not to transfer if the terms and condition of transfer

price are not agreed upon by the managers. Further, the selling division of the company will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

agree on the terms and conditions of transfer price only if the profit on transfer is equivalent or

more than on profit on the sale of goods or services to the external market. Similarly, buying

division will agree to buy the product and services internally only if the transfer price less than or

equivalent to the market price of the cost of the product (Trang, 2016). Moreover, if the transfer

price is less than the cost of the product, then in such case, the loss will be incurred to the selling

division, and manager of selling division will not agree to make the transfer. Just like this, if the

transfer price is determined too high, then in such case buying division will not agree to buy the

product internally. Therefore, in this method,the transfer price is determined on the basis

acceptable range, within which the return of both the division involving in the transfer would

enhance (Martini, 2015).

By considering the perspective of the seller, transfer price must be set in such a way, by which

division can cover the variable cost along with the loss of contribution from the sale of goods to

the external market. On the other hand, on the basis of the viewpoint of the buyer, the transfer

price should be less than or equivalent to the cost of purchasing the product from the external

supplier. (Hofmann, and van Lent, 2017)

Dual Transfer Price Method

If the transfer price is determined differently for the buying division and selling division, then it

is referred to as a dual transfer pricing method. In this method, selling division charges the

transfer price, which may be based on cost plus some profit margin. On the other hand, buying

division will record the transaction at the cost of the product. The main motive of this method is

to encourage the buying division to purchase the product from the other department (Hamamura,

2018). Similarly, selling division also agree to transfer, as the profit of division will not be

more than on profit on the sale of goods or services to the external market. Similarly, buying

division will agree to buy the product and services internally only if the transfer price less than or

equivalent to the market price of the cost of the product (Trang, 2016). Moreover, if the transfer

price is less than the cost of the product, then in such case, the loss will be incurred to the selling

division, and manager of selling division will not agree to make the transfer. Just like this, if the

transfer price is determined too high, then in such case buying division will not agree to buy the

product internally. Therefore, in this method,the transfer price is determined on the basis

acceptable range, within which the return of both the division involving in the transfer would

enhance (Martini, 2015).

By considering the perspective of the seller, transfer price must be set in such a way, by which

division can cover the variable cost along with the loss of contribution from the sale of goods to

the external market. On the other hand, on the basis of the viewpoint of the buyer, the transfer

price should be less than or equivalent to the cost of purchasing the product from the external

supplier. (Hofmann, and van Lent, 2017)

Dual Transfer Price Method

If the transfer price is determined differently for the buying division and selling division, then it

is referred to as a dual transfer pricing method. In this method, selling division charges the

transfer price, which may be based on cost plus some profit margin. On the other hand, buying

division will record the transaction at the cost of the product. The main motive of this method is

to encourage the buying division to purchase the product from the other department (Hamamura,

2018). Similarly, selling division also agree to transfer, as the profit of division will not be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

compromised because of the transfer. If the company has adequate spare capacity, then this

method will assist in the overall profitability of the organization. However, at the time of

consolidation of the results of the department, then the head office of the company is required to

make the entry,which eliminates the unrealized profit. By considering the above analysis, the

following advantages can be achieved by the company, which are as follows –

Buying division of the company will purchase the product at the least cost; therefore,

they wish to buy the product internally instead of the external market (Bouwens,

Hofmann, and van Lent, 2017).

Similarly, selling division can generate the profit as the transfer price is normally based

on the market price. Therefore the manager wants to transfer the product to another

department.

Therefore, it can be said that Raven Industries can apply the negotiated pricing method or dual

pricing method for the determination of the transfer price while selling the product of the cushion

department to the furniture department. It satisfies the main objective of the decentralization and

could enhance the overall profitability of the company (Christensen, 2018).

TASK 2

The cushion division sales its product to furniture division at the variable cost. The given

solution is based on the determination of the transfer price based on the contribution margin

approach. As per this method, contribution earned by the cushion division is computed on the

basis of sales of its product to the external market, and this is applied on sales to furniture

division.

method will assist in the overall profitability of the organization. However, at the time of

consolidation of the results of the department, then the head office of the company is required to

make the entry,which eliminates the unrealized profit. By considering the above analysis, the

following advantages can be achieved by the company, which are as follows –

Buying division of the company will purchase the product at the least cost; therefore,

they wish to buy the product internally instead of the external market (Bouwens,

Hofmann, and van Lent, 2017).

Similarly, selling division can generate the profit as the transfer price is normally based

on the market price. Therefore the manager wants to transfer the product to another

department.

Therefore, it can be said that Raven Industries can apply the negotiated pricing method or dual

pricing method for the determination of the transfer price while selling the product of the cushion

department to the furniture department. It satisfies the main objective of the decentralization and

could enhance the overall profitability of the company (Christensen, 2018).

TASK 2

The cushion division sales its product to furniture division at the variable cost. The given

solution is based on the determination of the transfer price based on the contribution margin

approach. As per this method, contribution earned by the cushion division is computed on the

basis of sales of its product to the external market, and this is applied on sales to furniture

division.

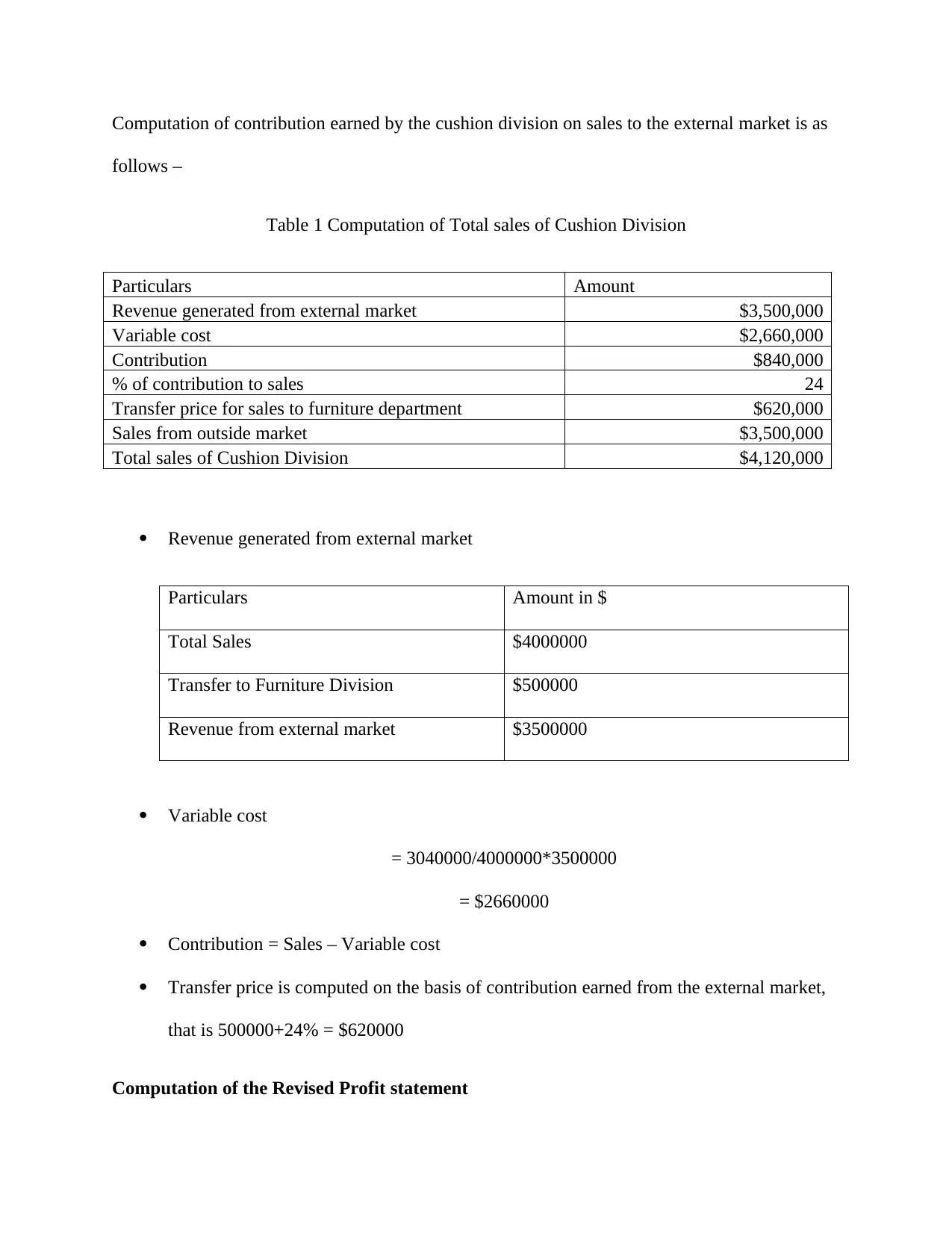

Computation of contribution earned by the cushion division on sales to the external market is as

follows –

Table 1 Computation of Total sales of Cushion Division

Particulars Amount

Revenue generated from external market $3,500,000

Variable cost $2,660,000

Contribution $840,000

% of contribution to sales 24

Transfer price for sales to furniture department $620,000

Sales from outside market $3,500,000

Total sales of Cushion Division $4,120,000

Revenue generated from external market

Particulars Amount in $

Total Sales $4000000

Transfer to Furniture Division $500000

Revenue from external market $3500000

Variable cost

= 3040000/4000000*3500000

= $2660000

Contribution = Sales – Variable cost

Transfer price is computed on the basis of contribution earned from the external market,

that is 500000+24% = $620000

Computation of the Revised Profit statement

follows –

Table 1 Computation of Total sales of Cushion Division

Particulars Amount

Revenue generated from external market $3,500,000

Variable cost $2,660,000

Contribution $840,000

% of contribution to sales 24

Transfer price for sales to furniture department $620,000

Sales from outside market $3,500,000

Total sales of Cushion Division $4,120,000

Revenue generated from external market

Particulars Amount in $

Total Sales $4000000

Transfer to Furniture Division $500000

Revenue from external market $3500000

Variable cost

= 3040000/4000000*3500000

= $2660000

Contribution = Sales – Variable cost

Transfer price is computed on the basis of contribution earned from the external market,

that is 500000+24% = $620000

Computation of the Revised Profit statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

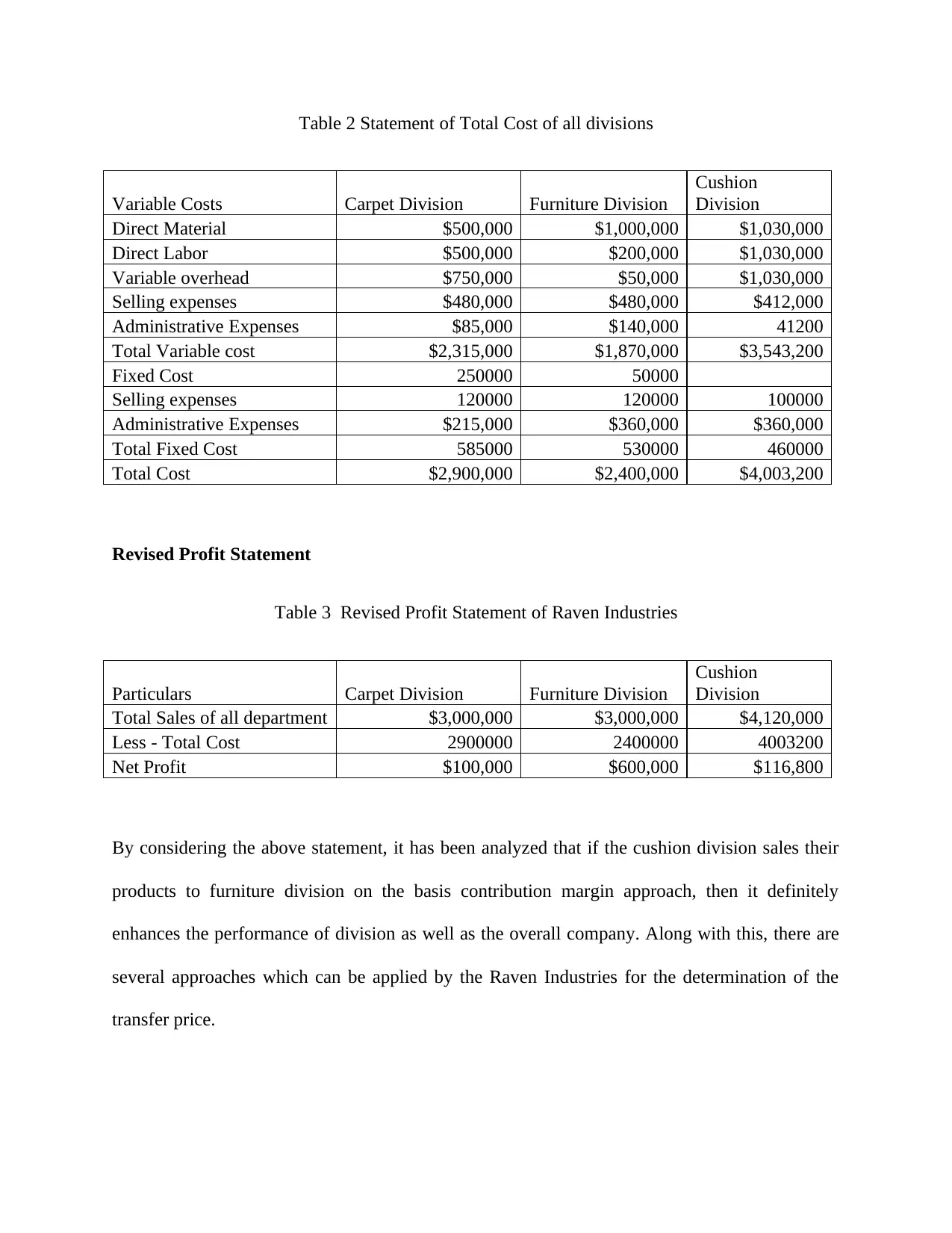

Table 2 Statement of Total Cost of all divisions

Variable Costs Carpet Division Furniture Division

Cushion

Division

Direct Material $500,000 $1,000,000 $1,030,000

Direct Labor $500,000 $200,000 $1,030,000

Variable overhead $750,000 $50,000 $1,030,000

Selling expenses $480,000 $480,000 $412,000

Administrative Expenses $85,000 $140,000 41200

Total Variable cost $2,315,000 $1,870,000 $3,543,200

Fixed Cost 250000 50000

Selling expenses 120000 120000 100000

Administrative Expenses $215,000 $360,000 $360,000

Total Fixed Cost 585000 530000 460000

Total Cost $2,900,000 $2,400,000 $4,003,200

Revised Profit Statement

Table 3 Revised Profit Statement of Raven Industries

Particulars Carpet Division Furniture Division

Cushion

Division

Total Sales of all department $3,000,000 $3,000,000 $4,120,000

Less - Total Cost 2900000 2400000 4003200

Net Profit $100,000 $600,000 $116,800

By considering the above statement, it has been analyzed that if the cushion division sales their

products to furniture division on the basis contribution margin approach, then it definitely

enhances the performance of division as well as the overall company. Along with this, there are

several approaches which can be applied by the Raven Industries for the determination of the

transfer price.

Variable Costs Carpet Division Furniture Division

Cushion

Division

Direct Material $500,000 $1,000,000 $1,030,000

Direct Labor $500,000 $200,000 $1,030,000

Variable overhead $750,000 $50,000 $1,030,000

Selling expenses $480,000 $480,000 $412,000

Administrative Expenses $85,000 $140,000 41200

Total Variable cost $2,315,000 $1,870,000 $3,543,200

Fixed Cost 250000 50000

Selling expenses 120000 120000 100000

Administrative Expenses $215,000 $360,000 $360,000

Total Fixed Cost 585000 530000 460000

Total Cost $2,900,000 $2,400,000 $4,003,200

Revised Profit Statement

Table 3 Revised Profit Statement of Raven Industries

Particulars Carpet Division Furniture Division

Cushion

Division

Total Sales of all department $3,000,000 $3,000,000 $4,120,000

Less - Total Cost 2900000 2400000 4003200

Net Profit $100,000 $600,000 $116,800

By considering the above statement, it has been analyzed that if the cushion division sales their

products to furniture division on the basis contribution margin approach, then it definitely

enhances the performance of division as well as the overall company. Along with this, there are

several approaches which can be applied by the Raven Industries for the determination of the

transfer price.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

To,

The CEO

Cushion Division.

Dear Sir,

Subject: Discussion relating to transfer pricing and performance measurement approach which

would assist in optimizing the performance and efficiency of company.

Transfer price is the price at which the company sells its goods, services, which consist of

labour, parts or any other products to its other division or it's subsidiary (Ansoff& et al. 2019).

On the other hand, performance measurement is the technique which is applied for measuring the

performance of the division. In the present case, it is given that Raven Industries has three

distinct divisions, in which Cushion division sales its products to furniture division. It is given

that; transfer price represents the variable cost. In other words, the cushion division transfers its

product to furniture division at cost price, which is the variable cost incurred by division for the

production of one unit its product. By this method, the manager of the cushion division was not

happy with the performance of the company. Therefore he wants to implement the contribution

margin method for determination of the transfer price. As per this method, the transfer price is

consisting of the contribution that can be generated by the external sale of the product. There are

three managerial accounting areas, which are affected by the transfer price, which are, transfer

price ascertain costs and revenue among the transacting division and impact on the performance

analysis (Whittington, 2016). If the company applies the cost method for the ascertainment of the

transfer price, then cushion division will not want to sell the product to furniture division, as

To,

The CEO

Cushion Division.

Dear Sir,

Subject: Discussion relating to transfer pricing and performance measurement approach which

would assist in optimizing the performance and efficiency of company.

Transfer price is the price at which the company sells its goods, services, which consist of

labour, parts or any other products to its other division or it's subsidiary (Ansoff& et al. 2019).

On the other hand, performance measurement is the technique which is applied for measuring the

performance of the division. In the present case, it is given that Raven Industries has three

distinct divisions, in which Cushion division sales its products to furniture division. It is given

that; transfer price represents the variable cost. In other words, the cushion division transfers its

product to furniture division at cost price, which is the variable cost incurred by division for the

production of one unit its product. By this method, the manager of the cushion division was not

happy with the performance of the company. Therefore he wants to implement the contribution

margin method for determination of the transfer price. As per this method, the transfer price is

consisting of the contribution that can be generated by the external sale of the product. There are

three managerial accounting areas, which are affected by the transfer price, which are, transfer

price ascertain costs and revenue among the transacting division and impact on the performance

analysis (Whittington, 2016). If the company applies the cost method for the ascertainment of the

transfer price, then cushion division will not want to sell the product to furniture division, as

there is no generation of profit by this transfer. On the other hand, cushion division has an

external market for the selling of the product, by which the department can generate the profit.

Thus the application of the cost method for the ascertainment of transfer price was not in order.

If the division does not have any external market for the selling of the product, then is such case

the department will agree to sell their product at the cost. In the given problem, it is stated that

cushion division has an external market for the product, by which it can generate profit by selling

their product. Further, for measuring the performance, determination of price through the

contribution based margin approach is the good technique (Baldenius, and Michaeli, 2017).

By considering the above analysis, it has been observed that optimization of the performance and

efficiency of the company is possible through by implementation of the performance

measurement approach (Meyer & et al. 2017). Therefore, the same is recommended to the Raven

Industries to implement the performance-based approach instead of transfer pricing approach. By

this approach, the divisional manager gets motivated to sell the product internally, which leads

towards improvement in the profitability. In addition, it also gives the opportunity to the manager

to review and assess the performance of each division, by which they can make the strategies and

plans and allocate the resources of the company accordingly (Hofmann, and Indjejikian, 2018).

Along with this, the performance of one department can influence or motivate the other

departmental manager for improvising the activities of the department. Further, the company can

identify the division whose performance is not as per the strategies, so take the proper actions by

which optimum utilization of the resources is possible (Reineke, and Weiskirchner-Merten,

2018). Moreover, it also gives the separate responsibility to each divisional manager, so that they

take all actions carefully and put the efforts for improvising the performance. However,

sometimes by this company may face challenges, because there is a possibility that divisional

external market for the selling of the product, by which the department can generate the profit.

Thus the application of the cost method for the ascertainment of transfer price was not in order.

If the division does not have any external market for the selling of the product, then is such case

the department will agree to sell their product at the cost. In the given problem, it is stated that

cushion division has an external market for the product, by which it can generate profit by selling

their product. Further, for measuring the performance, determination of price through the

contribution based margin approach is the good technique (Baldenius, and Michaeli, 2017).

By considering the above analysis, it has been observed that optimization of the performance and

efficiency of the company is possible through by implementation of the performance

measurement approach (Meyer & et al. 2017). Therefore, the same is recommended to the Raven

Industries to implement the performance-based approach instead of transfer pricing approach. By

this approach, the divisional manager gets motivated to sell the product internally, which leads

towards improvement in the profitability. In addition, it also gives the opportunity to the manager

to review and assess the performance of each division, by which they can make the strategies and

plans and allocate the resources of the company accordingly (Hofmann, and Indjejikian, 2018).

Along with this, the performance of one department can influence or motivate the other

departmental manager for improvising the activities of the department. Further, the company can

identify the division whose performance is not as per the strategies, so take the proper actions by

which optimum utilization of the resources is possible (Reineke, and Weiskirchner-Merten,

2018). Moreover, it also gives the separate responsibility to each divisional manager, so that they

take all actions carefully and put the efforts for improvising the performance. However,

sometimes by this company may face challenges, because there is a possibility that divisional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.