Transfer Pricing for Vans: Cost, Market, and External Offers

VerifiedAdded on 2022/10/14

|4

|570

|14

Homework Assignment

AI Summary

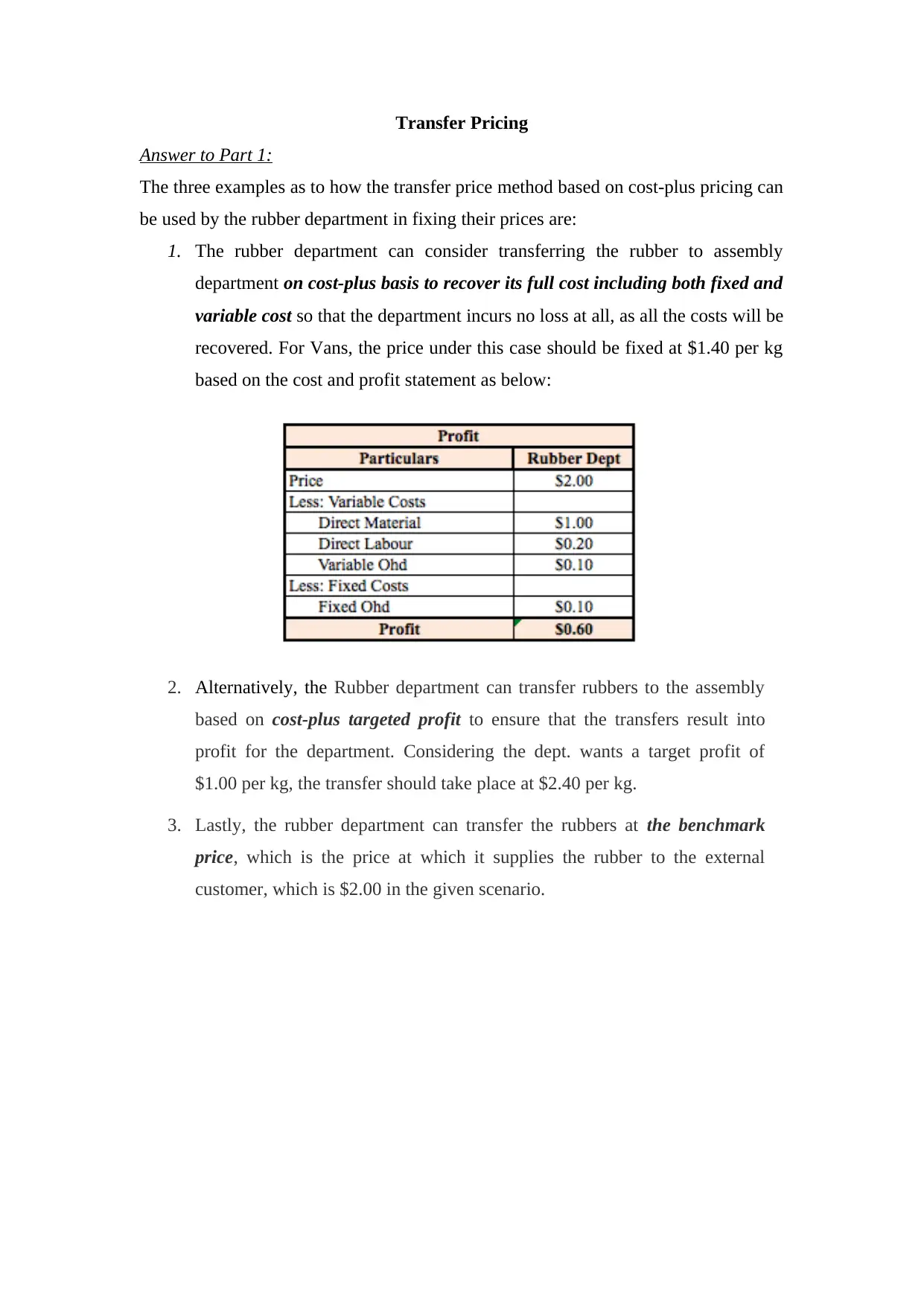

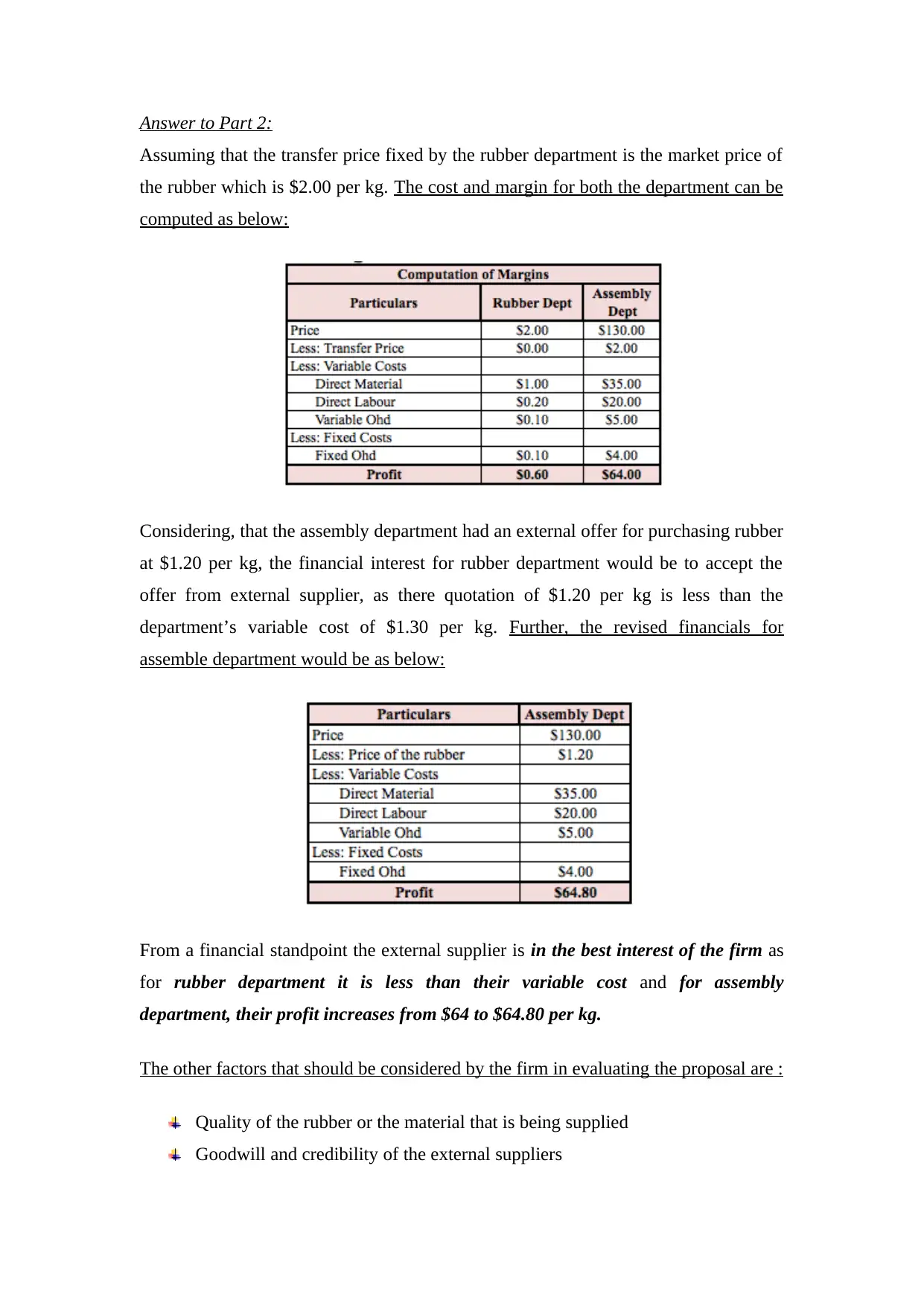

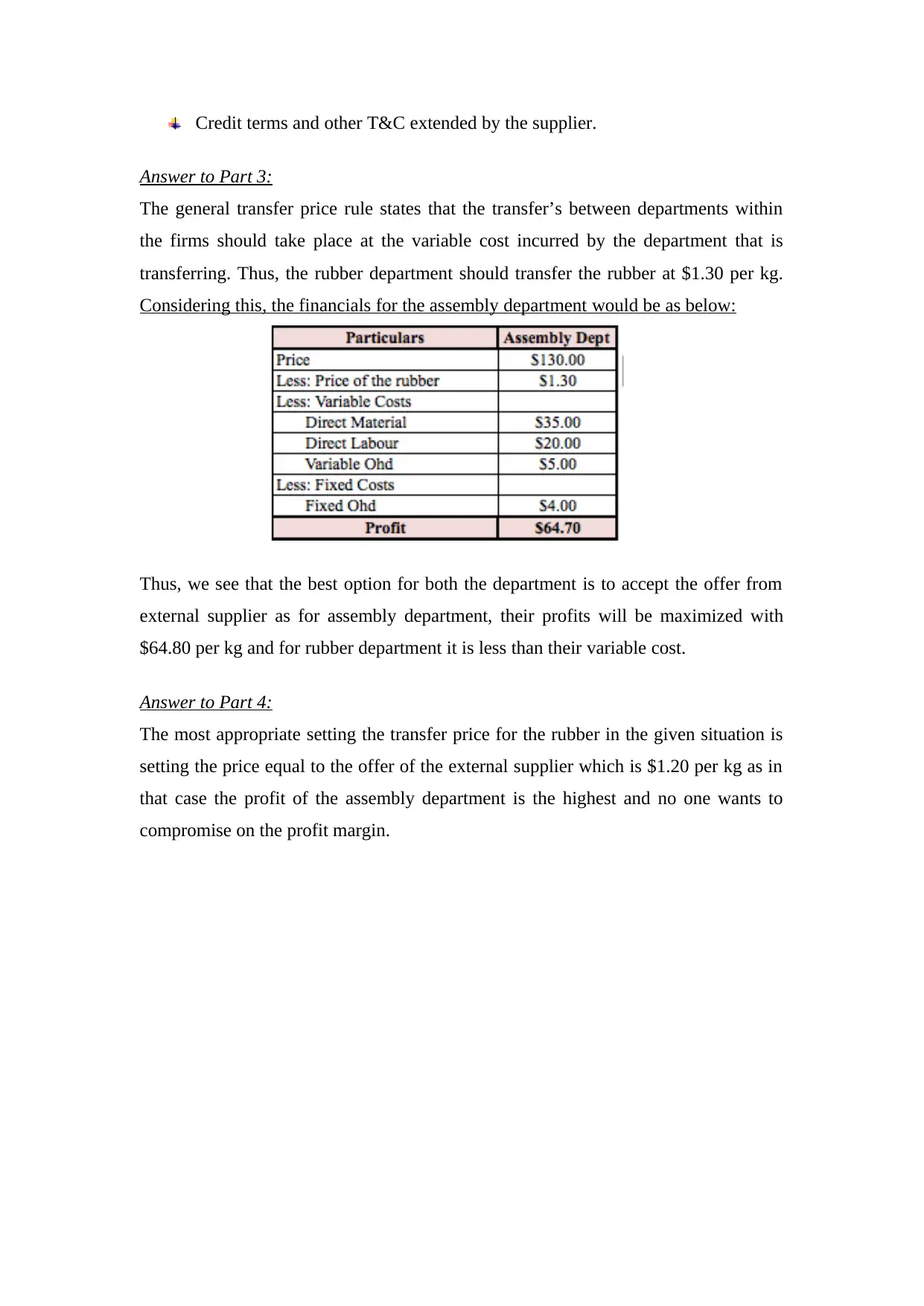

This assignment solution addresses a transfer pricing problem for Vans, a footwear company. The solution examines how the Rubber Department can use cost-plus pricing to determine transfer prices for rubber transferred to the Assembly Department, providing three examples with different cost bases and markups. It then analyzes the financial implications of using the market price for transfer pricing and compares it to an external supplier's offer. The analysis considers the best financial interests of both departments and the firm as a whole. Finally, it explores the general transfer pricing rule based on variable costs and its impact on the departments' financials, ultimately concluding which scenario maximizes the firm's profit and addresses other non-financial factors such as quality and credibility.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.