Finance and Funding in Travel and Tourism: Investment & Ratio Analysis

VerifiedAdded on 2019/12/03

|18

|5519

|38

Report

AI Summary

This report delves into the critical aspects of finance and funding within the travel and tourism sector. It begins with an introduction to the significance of financial management, emphasizing cost, volume, and profit analysis in decision-making. The report then proceeds to Task 1, where it calculates unit costs, determines break-even points, and explores pricing strategies using methods like capital employed and mark-up. Task 2 focuses on investment appraisal techniques, evaluating the financial viability of potential projects. Task 3 involves a detailed ratio analysis of Magical Mystery Tours Ltd, assessing its financial position. Finally, Task 4 analyzes the sources and distribution of funding for capital projects. The report provides a comprehensive overview of financial management principles, cost analysis, investment appraisal, and ratio analysis within the context of the travel and tourism industry, offering insights into making informed financial decisions.

FINANCE AND FUNDING IN

TRAVEL AND TOURISM

1

TRAVEL AND TOURISM

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................................3

Task 1.........................................................................................................................................................3

A) Calculation of unit costs and making pricing decision................................................................3

B) Calculate price of New Romantic Movement tour......................................................................5

C) Analysis of factor influencing profit for travel and tourism businesses......................................6

Task 2.........................................................................................................................................................7

Investment Appraisal Techniques.....................................................................................................7

Task 3.......................................................................................................................................................11

Ratio Analysis.................................................................................................................................11

Task 4.......................................................................................................................................................13

Analyse sources and distribution of funding for development of capital project...........................13

Conclusion...............................................................................................................................................15

References................................................................................................................................................16

2

Introduction................................................................................................................................................3

Task 1.........................................................................................................................................................3

A) Calculation of unit costs and making pricing decision................................................................3

B) Calculate price of New Romantic Movement tour......................................................................5

C) Analysis of factor influencing profit for travel and tourism businesses......................................6

Task 2.........................................................................................................................................................7

Investment Appraisal Techniques.....................................................................................................7

Task 3.......................................................................................................................................................11

Ratio Analysis.................................................................................................................................11

Task 4.......................................................................................................................................................13

Analyse sources and distribution of funding for development of capital project...........................13

Conclusion...............................................................................................................................................15

References................................................................................................................................................16

2

INTRODUCTION

Finance and Funding can be defined as the crucial aspect for all the commercial companies who

are putting tons of efforts to sustain in business for long term periods. However, both these elements

have direct connections with growth and profitability. It is the duty of senior authorities of firm to

ensure that financial resources are managed and utilized in optimum manner so to attain desired outputs

(Cahill, 2010). Looking at the condition of corporate market it become more significant for the

companies to deliver best to its target audience otherwise it may have negative impact on overall future

contingency.

Financial resources are considered to be the most valuable assets that an organisation have

which requires intense care and appropriate management to carry out business activities effectively and

efficiently. Furthermore, finance manager has the responsibility of keeping proper balance between cots

and volume in order to manage and use financial resource adequately. In the present research project,

researcher is focusing on evaluating significance of finance and funding in travel and tourism sector. To

elaborate this in detail, report consist of importance of cost, volume and profit in making smart

decisions regarding future functioning. Researcher concentrates on evaluating three different methods

of determining the price of per unit and on that basis making the best possible decision for setting

pricing strategy. Other than this, report includes evaluation of different investment appraisal techniques

to determine the feasibility and reliability of future investment. Lastly, By the means of financial

information researcher will evaluate and analyse the financial position of Magical Mystery Tours Ltd

using ratio analysis.

TASK 1

A) Calculation of unit costs and making pricing decision

1) Analyse the figures to determine how many tourist booking require for break even point at price

of 30 per ticket

Break even point refers to the point of zero loss or zero profit. In other words, at break even

situation revenues of business enterprise are equal to the amount of its total costs and its contribution

margin is equals its total fixed costs (Irwin and Scott, 2010). In order to compute break-even point

manager have to use equation such as:

px = vx + FC + Profit

Where,

P is the price per unit

3

Finance and Funding can be defined as the crucial aspect for all the commercial companies who

are putting tons of efforts to sustain in business for long term periods. However, both these elements

have direct connections with growth and profitability. It is the duty of senior authorities of firm to

ensure that financial resources are managed and utilized in optimum manner so to attain desired outputs

(Cahill, 2010). Looking at the condition of corporate market it become more significant for the

companies to deliver best to its target audience otherwise it may have negative impact on overall future

contingency.

Financial resources are considered to be the most valuable assets that an organisation have

which requires intense care and appropriate management to carry out business activities effectively and

efficiently. Furthermore, finance manager has the responsibility of keeping proper balance between cots

and volume in order to manage and use financial resource adequately. In the present research project,

researcher is focusing on evaluating significance of finance and funding in travel and tourism sector. To

elaborate this in detail, report consist of importance of cost, volume and profit in making smart

decisions regarding future functioning. Researcher concentrates on evaluating three different methods

of determining the price of per unit and on that basis making the best possible decision for setting

pricing strategy. Other than this, report includes evaluation of different investment appraisal techniques

to determine the feasibility and reliability of future investment. Lastly, By the means of financial

information researcher will evaluate and analyse the financial position of Magical Mystery Tours Ltd

using ratio analysis.

TASK 1

A) Calculation of unit costs and making pricing decision

1) Analyse the figures to determine how many tourist booking require for break even point at price

of 30 per ticket

Break even point refers to the point of zero loss or zero profit. In other words, at break even

situation revenues of business enterprise are equal to the amount of its total costs and its contribution

margin is equals its total fixed costs (Irwin and Scott, 2010). In order to compute break-even point

manager have to use equation such as:

px = vx + FC + Profit

Where,

P is the price per unit

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

X is the number of Units

V is variable cost per unit and

FC is total fixed cost

Breakeven point in Sales units = x = FC/ p – v

Price per Unit = 30

Variable Cost per Unit = 2

Fixed Cost = 300

Breakeven point in Sales units = 300/ 30 – 2

Breakeven point in Sales units = 300/28

Breakeven point in Sales units = 10.71

Break-even point in Sales Pound = Price per Unit × Break-even Sales Units

Breakeven point in Sales Pound = 30 * 10.71

Breakeven point in Sales Pound = £321.42

2) How many tickets of sale require by Magical Mystery Tours Ltd to earn a profit on 30 per ticket

Profit = 500

Price per ticket = 30

Unit to be sold to earn 500= Fixed cost + desired profit / Contribution

800/28

= 29 bookings

3) Significance of cost and volume when determining how to make profit

In financial management cost and volume play a crucial role because both these elements have

direct impact on the overall functioning as they are highly correlated. When the volume is increases or

decreases it directly effects on the cost of production. However, it is the duty of finance manager to

manage and control financial resources in effective manner so that cost can be maintained (Narayanan

and Nanda, 2004). Mainly, there are three types of costs i.e. fixed, variable and semi variable cost.

According to the present given case, Travel and Tourism sector is becoming one of the most

competitive market to operate in. There are various companies making valiant efforts to execute

business activities by managing financial position systematically. In this regard, top level management

of Magical Mystery Tours Ltd should identify different types of costs for preparing variable cots

structure. By the means of this, management will be able to make feasible and effective utilisation of

available resources and make smart decision for increasing profitability.

4

V is variable cost per unit and

FC is total fixed cost

Breakeven point in Sales units = x = FC/ p – v

Price per Unit = 30

Variable Cost per Unit = 2

Fixed Cost = 300

Breakeven point in Sales units = 300/ 30 – 2

Breakeven point in Sales units = 300/28

Breakeven point in Sales units = 10.71

Break-even point in Sales Pound = Price per Unit × Break-even Sales Units

Breakeven point in Sales Pound = 30 * 10.71

Breakeven point in Sales Pound = £321.42

2) How many tickets of sale require by Magical Mystery Tours Ltd to earn a profit on 30 per ticket

Profit = 500

Price per ticket = 30

Unit to be sold to earn 500= Fixed cost + desired profit / Contribution

800/28

= 29 bookings

3) Significance of cost and volume when determining how to make profit

In financial management cost and volume play a crucial role because both these elements have

direct impact on the overall functioning as they are highly correlated. When the volume is increases or

decreases it directly effects on the cost of production. However, it is the duty of finance manager to

manage and control financial resources in effective manner so that cost can be maintained (Narayanan

and Nanda, 2004). Mainly, there are three types of costs i.e. fixed, variable and semi variable cost.

According to the present given case, Travel and Tourism sector is becoming one of the most

competitive market to operate in. There are various companies making valiant efforts to execute

business activities by managing financial position systematically. In this regard, top level management

of Magical Mystery Tours Ltd should identify different types of costs for preparing variable cots

structure. By the means of this, management will be able to make feasible and effective utilisation of

available resources and make smart decision for increasing profitability.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Cost: This is cost which is periodic in nature and does not affect the change in production

level. In the present case, fixed cost for Magical Mystery Tours Ltd is 300 pounds. This means

it will not change on the basis of tickets demand and sales. Fixed cost for Magical Mystery

Tours Ltd are maintenance cost, administration cost, depreciation of fixed assets and rental

charges.

Variable Cost: It is the amount of expenditure which changes as per the level of production. In

this case, variable cost per ticket is 2. However, the variable cost of Magical Mystery Tours Ltd

are fuel, food charges etc.

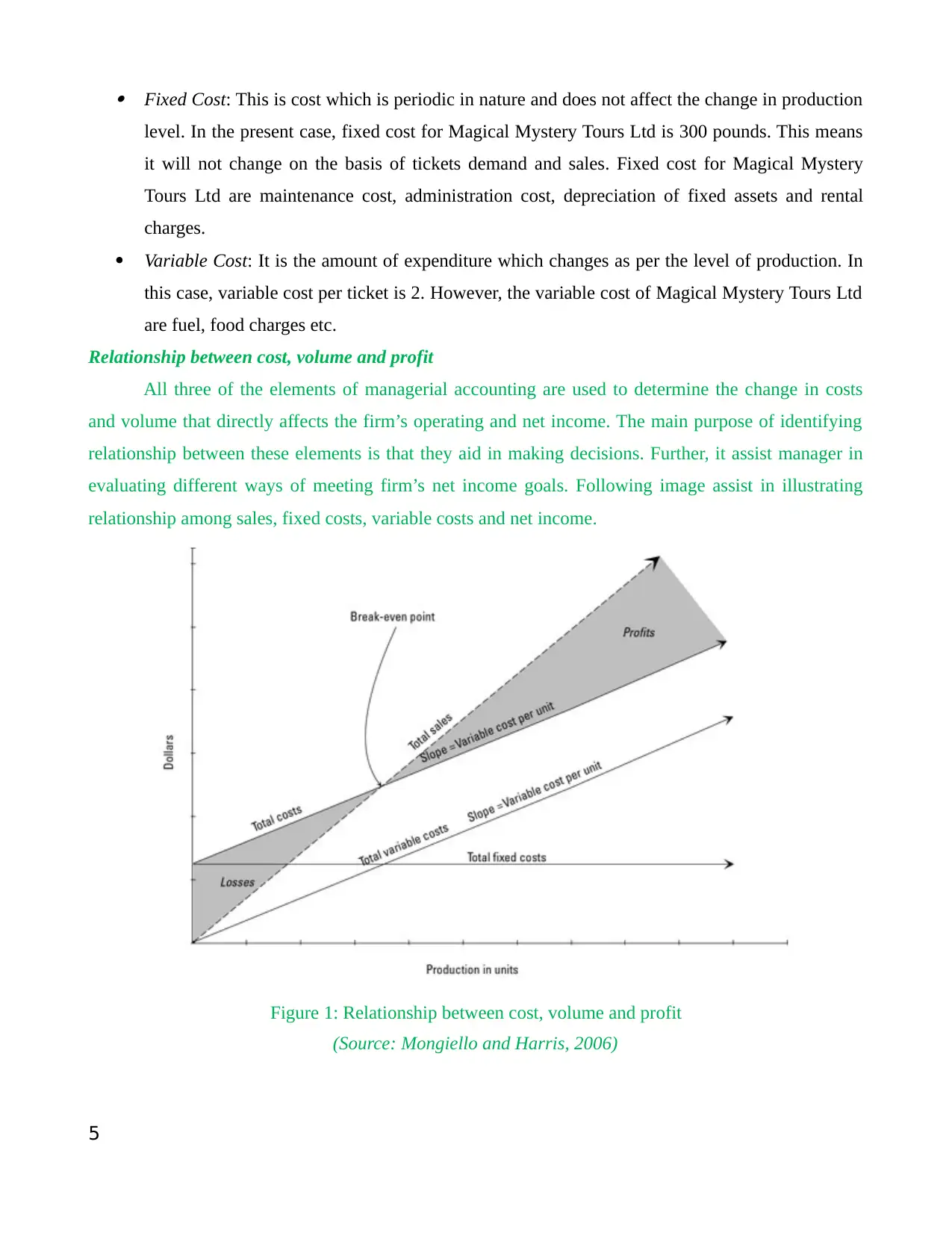

Relationship between cost, volume and profit

All three of the elements of managerial accounting are used to determine the change in costs

and volume that directly affects the firm’s operating and net income. The main purpose of identifying

relationship between these elements is that they aid in making decisions. Further, it assist manager in

evaluating different ways of meeting firm’s net income goals. Following image assist in illustrating

relationship among sales, fixed costs, variable costs and net income.

Figure 1: Relationship between cost, volume and profit

(Source: Mongiello and Harris, 2006)

5

level. In the present case, fixed cost for Magical Mystery Tours Ltd is 300 pounds. This means

it will not change on the basis of tickets demand and sales. Fixed cost for Magical Mystery

Tours Ltd are maintenance cost, administration cost, depreciation of fixed assets and rental

charges.

Variable Cost: It is the amount of expenditure which changes as per the level of production. In

this case, variable cost per ticket is 2. However, the variable cost of Magical Mystery Tours Ltd

are fuel, food charges etc.

Relationship between cost, volume and profit

All three of the elements of managerial accounting are used to determine the change in costs

and volume that directly affects the firm’s operating and net income. The main purpose of identifying

relationship between these elements is that they aid in making decisions. Further, it assist manager in

evaluating different ways of meeting firm’s net income goals. Following image assist in illustrating

relationship among sales, fixed costs, variable costs and net income.

Figure 1: Relationship between cost, volume and profit

(Source: Mongiello and Harris, 2006)

5

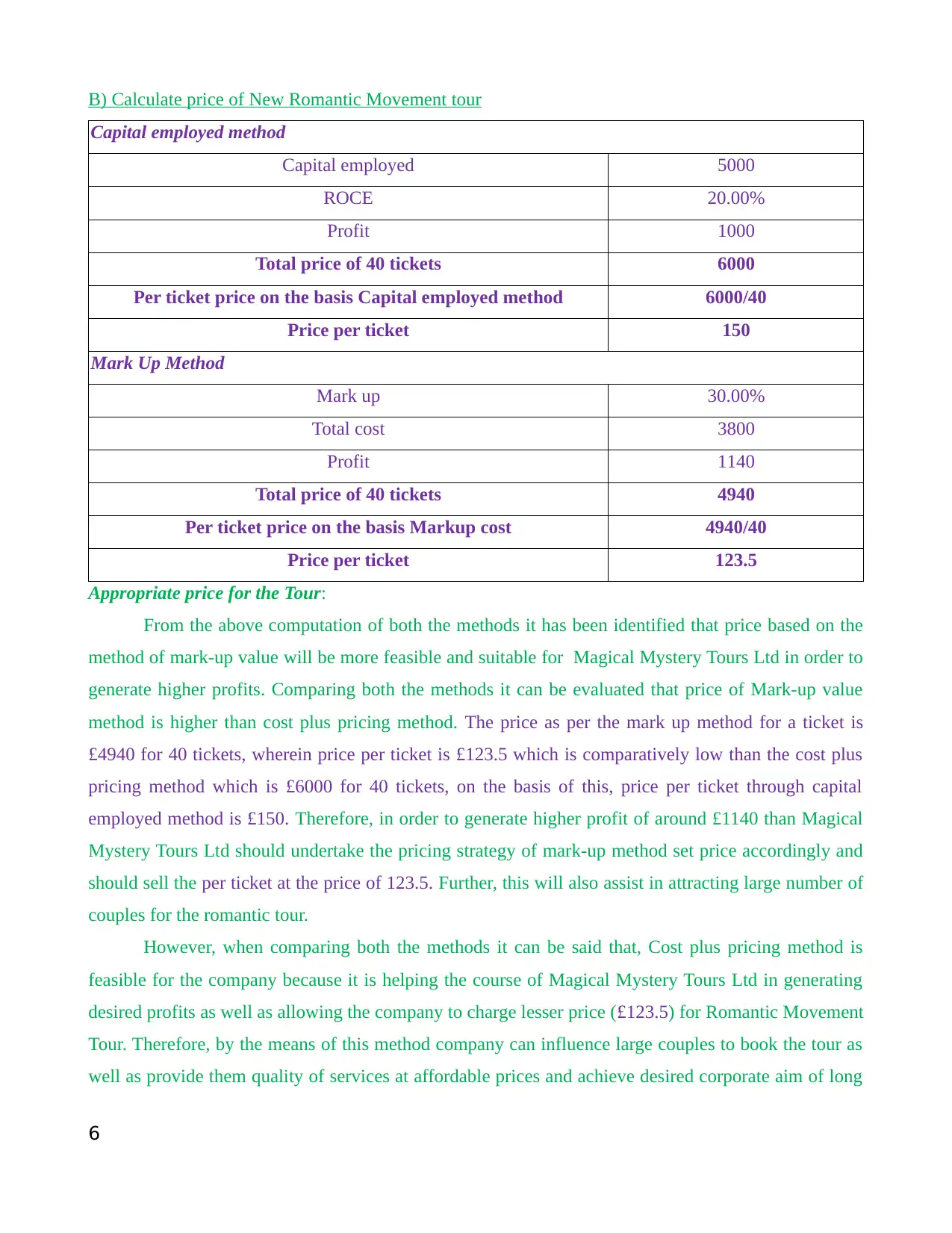

B) Calculate price of New Romantic Movement tour

Capital employed method

Capital employed 5000

ROCE 20.00%

Profit 1000

Total price of 40 tickets 6000

Per ticket price on the basis Capital employed method 6000/40

Price per ticket 150

Mark Up Method

Mark up 30.00%

Total cost 3800

Profit 1140

Total price of 40 tickets 4940

Per ticket price on the basis Markup cost 4940/40

Price per ticket 123.5

Appropriate price for the Tour:

From the above computation of both the methods it has been identified that price based on the

method of mark-up value will be more feasible and suitable for Magical Mystery Tours Ltd in order to

generate higher profits. Comparing both the methods it can be evaluated that price of Mark-up value

method is higher than cost plus pricing method. The price as per the mark up method for a ticket is

£4940 for 40 tickets, wherein price per ticket is £123.5 which is comparatively low than the cost plus

pricing method which is £6000 for 40 tickets, on the basis of this, price per ticket through capital

employed method is £150. Therefore, in order to generate higher profit of around £1140 than Magical

Mystery Tours Ltd should undertake the pricing strategy of mark-up method set price accordingly and

should sell the per ticket at the price of 123.5. Further, this will also assist in attracting large number of

couples for the romantic tour.

However, when comparing both the methods it can be said that, Cost plus pricing method is

feasible for the company because it is helping the course of Magical Mystery Tours Ltd in generating

desired profits as well as allowing the company to charge lesser price (£123.5) for Romantic Movement

Tour. Therefore, by the means of this method company can influence large couples to book the tour as

well as provide them quality of services at affordable prices and achieve desired corporate aim of long

6

Capital employed method

Capital employed 5000

ROCE 20.00%

Profit 1000

Total price of 40 tickets 6000

Per ticket price on the basis Capital employed method 6000/40

Price per ticket 150

Mark Up Method

Mark up 30.00%

Total cost 3800

Profit 1140

Total price of 40 tickets 4940

Per ticket price on the basis Markup cost 4940/40

Price per ticket 123.5

Appropriate price for the Tour:

From the above computation of both the methods it has been identified that price based on the

method of mark-up value will be more feasible and suitable for Magical Mystery Tours Ltd in order to

generate higher profits. Comparing both the methods it can be evaluated that price of Mark-up value

method is higher than cost plus pricing method. The price as per the mark up method for a ticket is

£4940 for 40 tickets, wherein price per ticket is £123.5 which is comparatively low than the cost plus

pricing method which is £6000 for 40 tickets, on the basis of this, price per ticket through capital

employed method is £150. Therefore, in order to generate higher profit of around £1140 than Magical

Mystery Tours Ltd should undertake the pricing strategy of mark-up method set price accordingly and

should sell the per ticket at the price of 123.5. Further, this will also assist in attracting large number of

couples for the romantic tour.

However, when comparing both the methods it can be said that, Cost plus pricing method is

feasible for the company because it is helping the course of Magical Mystery Tours Ltd in generating

desired profits as well as allowing the company to charge lesser price (£123.5) for Romantic Movement

Tour. Therefore, by the means of this method company can influence large couples to book the tour as

well as provide them quality of services at affordable prices and achieve desired corporate aim of long

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

term sustainability.

C) Analysis of factor influencing profit for travel and tourism businesses

Profitability of a business enterprise can be affected by several internal and external

environmental aspects. However, there are some of the factors which are not in the control of

businesses and raises the level of risks and uncertainties (Williams, 2012). Bellow discussed are some

of the factors which needs to be taken care of by the senior authority of Magical Mystery Tours Ltd to

attain growth and profitability. Seasonal Variations: In travel and tourism sector, seasons are of great importance. People likes

different season to travel in different destinations. However, for creating demand about the

services of tour packages it is important for top level management of Magical Mystery Tours

Ltd has to develop tour plan as per the seasonal variations so that best possible services can be

offered to clients (Helfrit, 2001). For example: there is high demand in June and July in travel

industry as the prices of tickets are relatively high as compared to other months. Economic environment: In economic environment factors like purchasing power, per capital

income and inflation rate in the economy are majorly concerned. Positive alteration in

economic condition encourages senior managers of Magical Mystery Tours Ltd top explore

new opportunities so that company can attain growth in near future. Tactics of competitive firms: Competition leads to affect the pricing structure of Magical

Mystery Tours Ltd. In case, if the price of competitor fluctuates than it is important for senior

managers of cited firm bring modifications within the pricing policy. However, customers will

face the obligations of fluctuations (Liu and et. al, 2007). Therefore, it can be stated that

Magical Mystery Tours Ltd has to make changes in its pricing strategy by considering the

strategies of competitors.

Political environment: There are several ways in which political environment can affect the

functioning of business enterprise. However, Tax is considered as one of the most significant

element which changes with the political environment. Magical Mystery Tours Ltd is working

in such a dynamic political environment of UK, that its managers are responsible to generate

desired results and outcomes easily. Decision regarding tax increase and decrease may affect

the overall profit margin of the cited firm.

7

C) Analysis of factor influencing profit for travel and tourism businesses

Profitability of a business enterprise can be affected by several internal and external

environmental aspects. However, there are some of the factors which are not in the control of

businesses and raises the level of risks and uncertainties (Williams, 2012). Bellow discussed are some

of the factors which needs to be taken care of by the senior authority of Magical Mystery Tours Ltd to

attain growth and profitability. Seasonal Variations: In travel and tourism sector, seasons are of great importance. People likes

different season to travel in different destinations. However, for creating demand about the

services of tour packages it is important for top level management of Magical Mystery Tours

Ltd has to develop tour plan as per the seasonal variations so that best possible services can be

offered to clients (Helfrit, 2001). For example: there is high demand in June and July in travel

industry as the prices of tickets are relatively high as compared to other months. Economic environment: In economic environment factors like purchasing power, per capital

income and inflation rate in the economy are majorly concerned. Positive alteration in

economic condition encourages senior managers of Magical Mystery Tours Ltd top explore

new opportunities so that company can attain growth in near future. Tactics of competitive firms: Competition leads to affect the pricing structure of Magical

Mystery Tours Ltd. In case, if the price of competitor fluctuates than it is important for senior

managers of cited firm bring modifications within the pricing policy. However, customers will

face the obligations of fluctuations (Liu and et. al, 2007). Therefore, it can be stated that

Magical Mystery Tours Ltd has to make changes in its pricing strategy by considering the

strategies of competitors.

Political environment: There are several ways in which political environment can affect the

functioning of business enterprise. However, Tax is considered as one of the most significant

element which changes with the political environment. Magical Mystery Tours Ltd is working

in such a dynamic political environment of UK, that its managers are responsible to generate

desired results and outcomes easily. Decision regarding tax increase and decrease may affect

the overall profit margin of the cited firm.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Investment Appraisal Techniques

Capital investment appraisal also known as capital budgeting. However, it is primarily a

planning process which facilitates the determination of concerned firm investments both short and long

term. The main aim of using these investment techniques is to evaluate and analyse the financial

viability and reliability of the investment. There are several appraisal techniques which are used by

managers to evaluate and analyse the reliability of project (Jin, Yu and Mi, 2011). All the techniques

have different implications on the outcomes and helps management in making smart and effective

judgement on the future contingency. Following are the three main investment appraisal techniques:

Payback Period: It is one of the easiest methods of computing feasibility and reliability of a

financial project. The main purpose behind calculating this techniques is that it assist managers in

identifying the time required by project to regain the invested amount, this process is termed as

payback period. In general less the time require by any project is considered to be more feasible as

compared to ones with longer payback periods (Hopwood and Mckeown, 2003). The formula to

compute payback period of a project highly depends upon the cash flow per period from the project is

even of uneven. In case of even the formula to calculate payback period is: initial investment / cash

inflow per period. While on the other hand, in case of uneven cash flows, manager have to calculate the

cumulative net cash flow of each period and then use in the following formula: A + B / C.

Where,

A is last period with the negative cumulative cash flow;

B is the absolute value of cumulative cash flow at the end of period A;

C is the total cash flow during the period after A.

In the present given scenario, cash flows of two projects has been shown which will help

researcher in evaluating and comparing the both the project easily (Beck, Levine and Loayza, 2000).

Looking at the uneven cash flows it is important for manager of Magical Mystery Tours Ltd to

calculate cumulative value and then evaluate the time required to regain the initial investment.

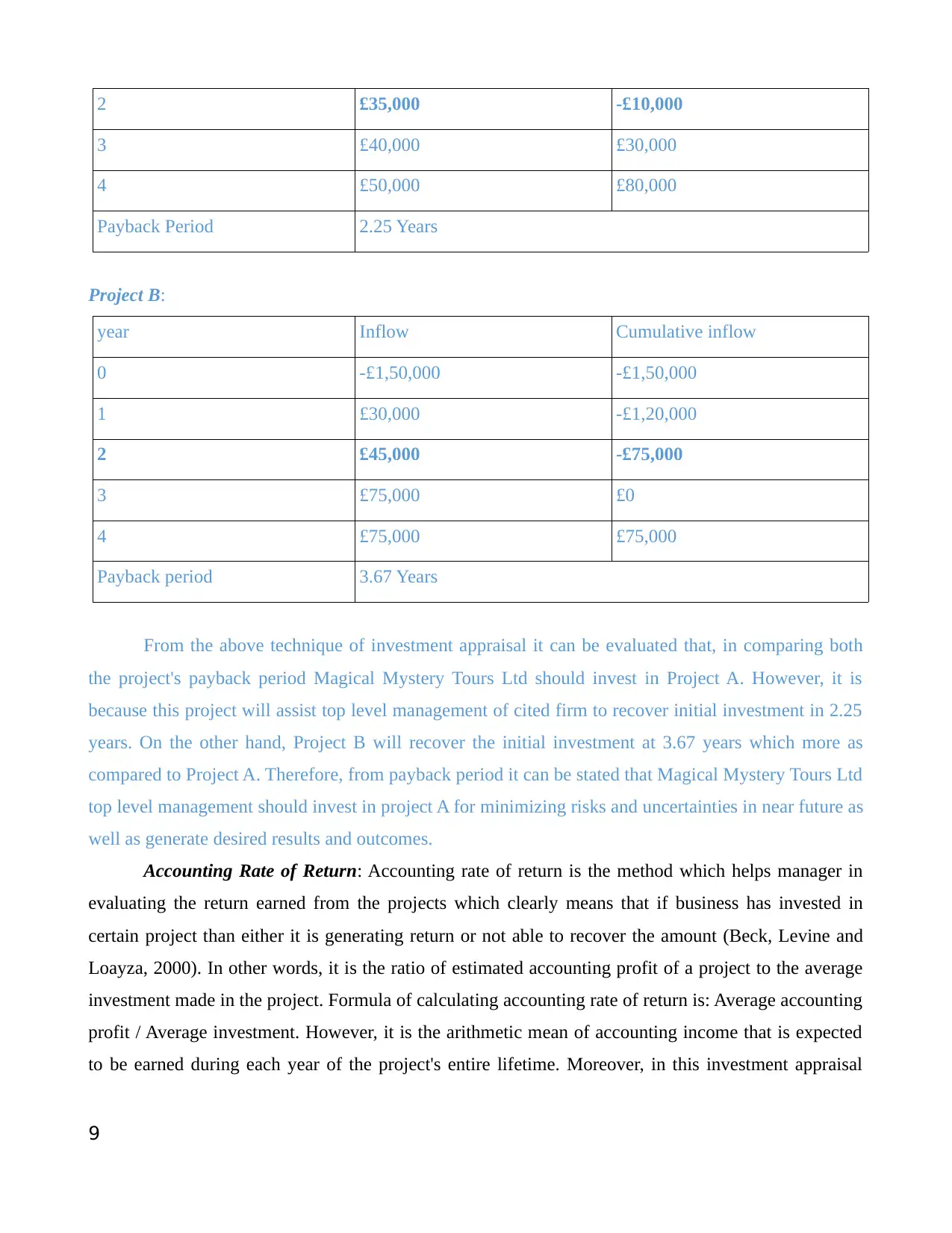

Project A:

year Inflow Cumulative inflow

0 -£80,000 -£80,000

1 £35,000 -£45,000

8

Investment Appraisal Techniques

Capital investment appraisal also known as capital budgeting. However, it is primarily a

planning process which facilitates the determination of concerned firm investments both short and long

term. The main aim of using these investment techniques is to evaluate and analyse the financial

viability and reliability of the investment. There are several appraisal techniques which are used by

managers to evaluate and analyse the reliability of project (Jin, Yu and Mi, 2011). All the techniques

have different implications on the outcomes and helps management in making smart and effective

judgement on the future contingency. Following are the three main investment appraisal techniques:

Payback Period: It is one of the easiest methods of computing feasibility and reliability of a

financial project. The main purpose behind calculating this techniques is that it assist managers in

identifying the time required by project to regain the invested amount, this process is termed as

payback period. In general less the time require by any project is considered to be more feasible as

compared to ones with longer payback periods (Hopwood and Mckeown, 2003). The formula to

compute payback period of a project highly depends upon the cash flow per period from the project is

even of uneven. In case of even the formula to calculate payback period is: initial investment / cash

inflow per period. While on the other hand, in case of uneven cash flows, manager have to calculate the

cumulative net cash flow of each period and then use in the following formula: A + B / C.

Where,

A is last period with the negative cumulative cash flow;

B is the absolute value of cumulative cash flow at the end of period A;

C is the total cash flow during the period after A.

In the present given scenario, cash flows of two projects has been shown which will help

researcher in evaluating and comparing the both the project easily (Beck, Levine and Loayza, 2000).

Looking at the uneven cash flows it is important for manager of Magical Mystery Tours Ltd to

calculate cumulative value and then evaluate the time required to regain the initial investment.

Project A:

year Inflow Cumulative inflow

0 -£80,000 -£80,000

1 £35,000 -£45,000

8

2 £35,000 -£10,000

3 £40,000 £30,000

4 £50,000 £80,000

Payback Period 2.25 Years

Project B:

year Inflow Cumulative inflow

0 -£1,50,000 -£1,50,000

1 £30,000 -£1,20,000

2 £45,000 -£75,000

3 £75,000 £0

4 £75,000 £75,000

Payback period 3.67 Years

From the above technique of investment appraisal it can be evaluated that, in comparing both

the project's payback period Magical Mystery Tours Ltd should invest in Project A. However, it is

because this project will assist top level management of cited firm to recover initial investment in 2.25

years. On the other hand, Project B will recover the initial investment at 3.67 years which more as

compared to Project A. Therefore, from payback period it can be stated that Magical Mystery Tours Ltd

top level management should invest in project A for minimizing risks and uncertainties in near future as

well as generate desired results and outcomes.

Accounting Rate of Return: Accounting rate of return is the method which helps manager in

evaluating the return earned from the projects which clearly means that if business has invested in

certain project than either it is generating return or not able to recover the amount (Beck, Levine and

Loayza, 2000). In other words, it is the ratio of estimated accounting profit of a project to the average

investment made in the project. Formula of calculating accounting rate of return is: Average accounting

profit / Average investment. However, it is the arithmetic mean of accounting income that is expected

to be earned during each year of the project's entire lifetime. Moreover, in this investment appraisal

9

3 £40,000 £30,000

4 £50,000 £80,000

Payback Period 2.25 Years

Project B:

year Inflow Cumulative inflow

0 -£1,50,000 -£1,50,000

1 £30,000 -£1,20,000

2 £45,000 -£75,000

3 £75,000 £0

4 £75,000 £75,000

Payback period 3.67 Years

From the above technique of investment appraisal it can be evaluated that, in comparing both

the project's payback period Magical Mystery Tours Ltd should invest in Project A. However, it is

because this project will assist top level management of cited firm to recover initial investment in 2.25

years. On the other hand, Project B will recover the initial investment at 3.67 years which more as

compared to Project A. Therefore, from payback period it can be stated that Magical Mystery Tours Ltd

top level management should invest in project A for minimizing risks and uncertainties in near future as

well as generate desired results and outcomes.

Accounting Rate of Return: Accounting rate of return is the method which helps manager in

evaluating the return earned from the projects which clearly means that if business has invested in

certain project than either it is generating return or not able to recover the amount (Beck, Levine and

Loayza, 2000). In other words, it is the ratio of estimated accounting profit of a project to the average

investment made in the project. Formula of calculating accounting rate of return is: Average accounting

profit / Average investment. However, it is the arithmetic mean of accounting income that is expected

to be earned during each year of the project's entire lifetime. Moreover, in this investment appraisal

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

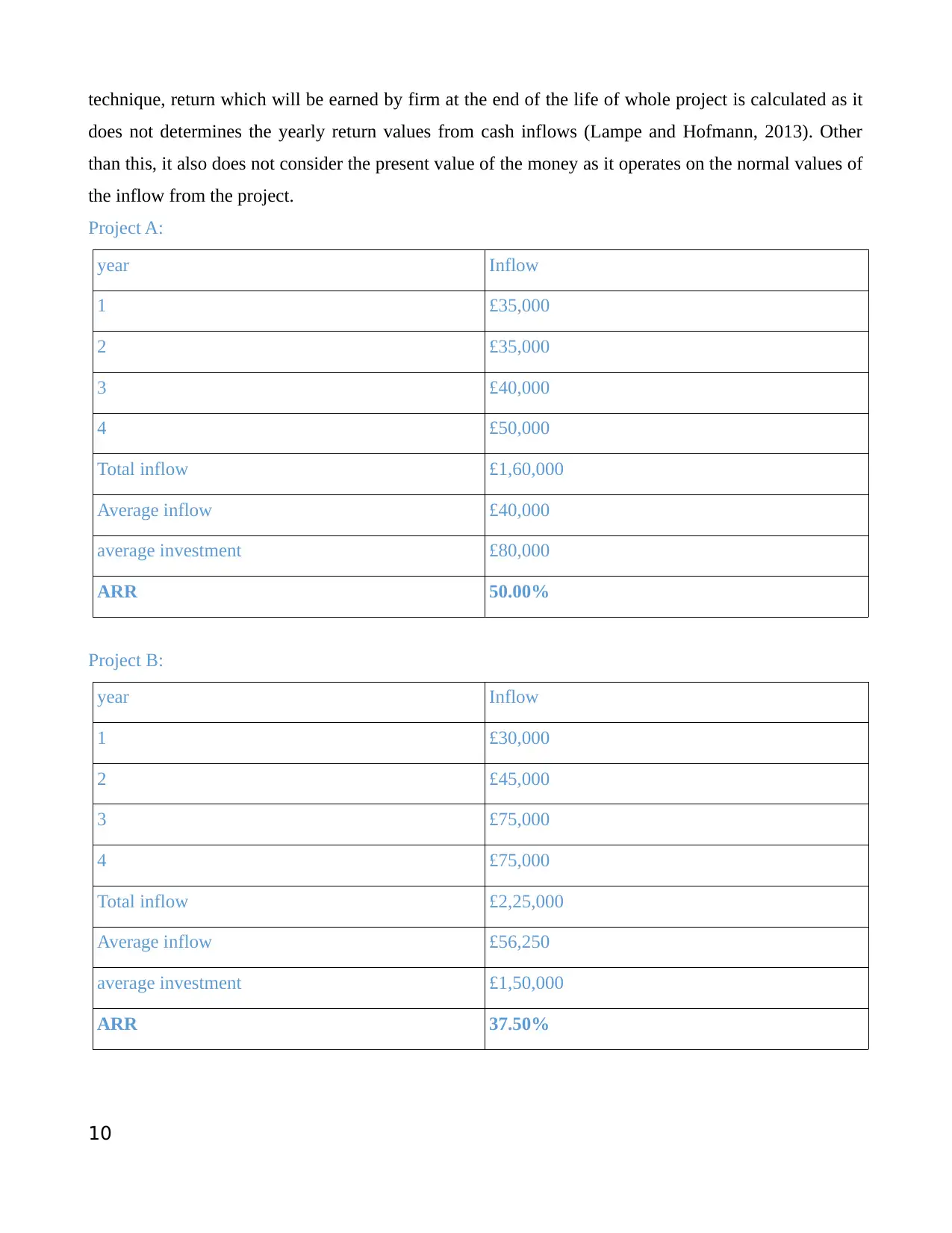

technique, return which will be earned by firm at the end of the life of whole project is calculated as it

does not determines the yearly return values from cash inflows (Lampe and Hofmann, 2013). Other

than this, it also does not consider the present value of the money as it operates on the normal values of

the inflow from the project.

Project A:

year Inflow

1 £35,000

2 £35,000

3 £40,000

4 £50,000

Total inflow £1,60,000

Average inflow £40,000

average investment £80,000

ARR 50.00%

Project B:

year Inflow

1 £30,000

2 £45,000

3 £75,000

4 £75,000

Total inflow £2,25,000

Average inflow £56,250

average investment £1,50,000

ARR 37.50%

10

does not determines the yearly return values from cash inflows (Lampe and Hofmann, 2013). Other

than this, it also does not consider the present value of the money as it operates on the normal values of

the inflow from the project.

Project A:

year Inflow

1 £35,000

2 £35,000

3 £40,000

4 £50,000

Total inflow £1,60,000

Average inflow £40,000

average investment £80,000

ARR 50.00%

Project B:

year Inflow

1 £30,000

2 £45,000

3 £75,000

4 £75,000

Total inflow £2,25,000

Average inflow £56,250

average investment £1,50,000

ARR 37.50%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above computation of accounting rate of return it can be evaluated that for Magical

Mystery Tours Ltd Project A will give the return of 50% which is highly beneficial in such competitive

market. On the other hand, Project B is generating the return at 37.50% which is comparatively low as

compared to Project A. Therefore, it can be recommended to senior authority of Magical Mystery Tours

Ltd that they should invest in Project A as it will help them in generating higher returns and increase

the chances of future growth and profitability.

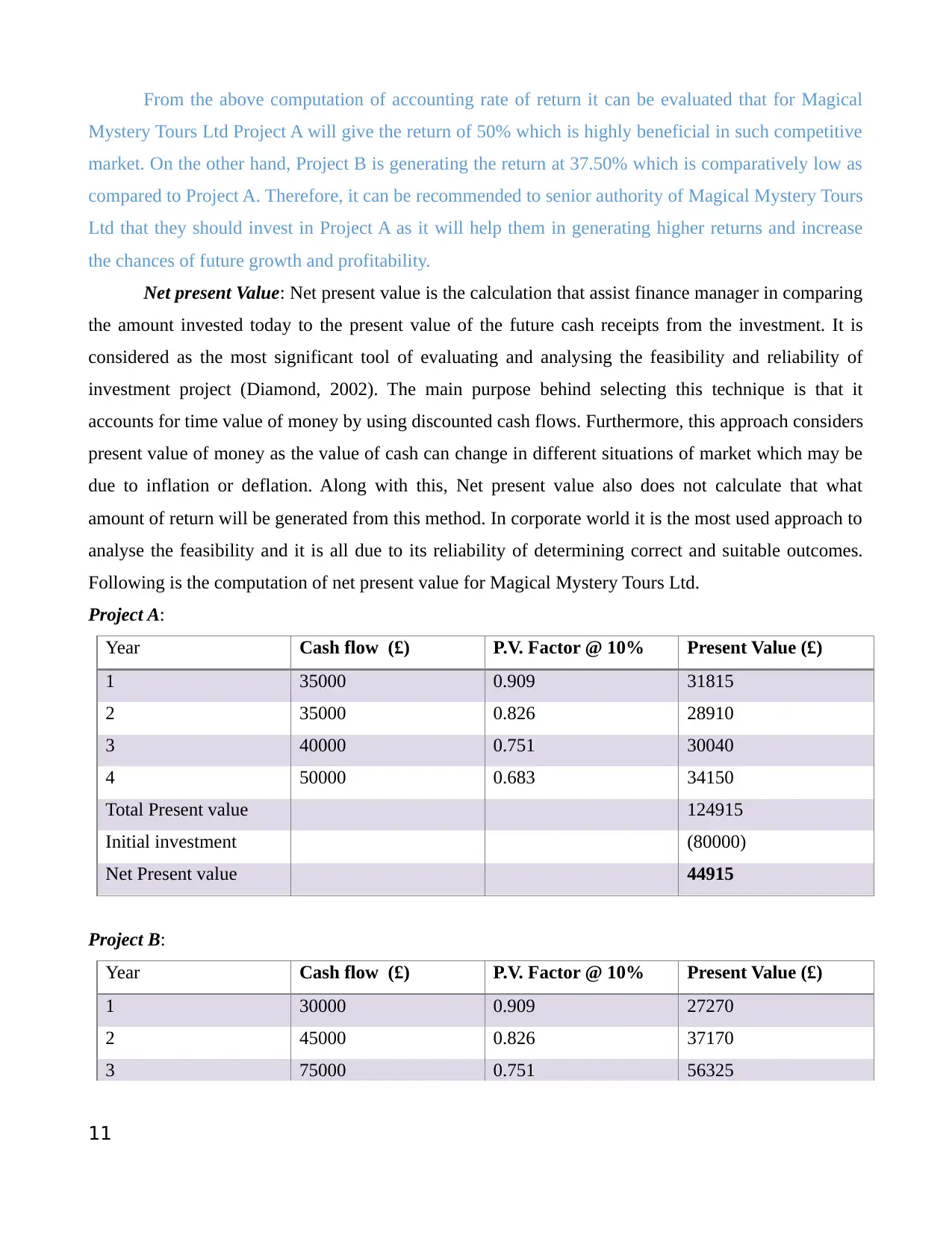

Net present Value: Net present value is the calculation that assist finance manager in comparing

the amount invested today to the present value of the future cash receipts from the investment. It is

considered as the most significant tool of evaluating and analysing the feasibility and reliability of

investment project (Diamond, 2002). The main purpose behind selecting this technique is that it

accounts for time value of money by using discounted cash flows. Furthermore, this approach considers

present value of money as the value of cash can change in different situations of market which may be

due to inflation or deflation. Along with this, Net present value also does not calculate that what

amount of return will be generated from this method. In corporate world it is the most used approach to

analyse the feasibility and it is all due to its reliability of determining correct and suitable outcomes.

Following is the computation of net present value for Magical Mystery Tours Ltd.

Project A:

Year Cash flow (£) P.V. Factor @ 10% Present Value (£)

1 35000 0.909 31815

2 35000 0.826 28910

3 40000 0.751 30040

4 50000 0.683 34150

Total Present value 124915

Initial investment (80000)

Net Present value 44915

Project B:

Year Cash flow (£) P.V. Factor @ 10% Present Value (£)

1 30000 0.909 27270

2 45000 0.826 37170

3 75000 0.751 56325

11

Mystery Tours Ltd Project A will give the return of 50% which is highly beneficial in such competitive

market. On the other hand, Project B is generating the return at 37.50% which is comparatively low as

compared to Project A. Therefore, it can be recommended to senior authority of Magical Mystery Tours

Ltd that they should invest in Project A as it will help them in generating higher returns and increase

the chances of future growth and profitability.

Net present Value: Net present value is the calculation that assist finance manager in comparing

the amount invested today to the present value of the future cash receipts from the investment. It is

considered as the most significant tool of evaluating and analysing the feasibility and reliability of

investment project (Diamond, 2002). The main purpose behind selecting this technique is that it

accounts for time value of money by using discounted cash flows. Furthermore, this approach considers

present value of money as the value of cash can change in different situations of market which may be

due to inflation or deflation. Along with this, Net present value also does not calculate that what

amount of return will be generated from this method. In corporate world it is the most used approach to

analyse the feasibility and it is all due to its reliability of determining correct and suitable outcomes.

Following is the computation of net present value for Magical Mystery Tours Ltd.

Project A:

Year Cash flow (£) P.V. Factor @ 10% Present Value (£)

1 35000 0.909 31815

2 35000 0.826 28910

3 40000 0.751 30040

4 50000 0.683 34150

Total Present value 124915

Initial investment (80000)

Net Present value 44915

Project B:

Year Cash flow (£) P.V. Factor @ 10% Present Value (£)

1 30000 0.909 27270

2 45000 0.826 37170

3 75000 0.751 56325

11

4 75000 0.683 51225

Total Present value 171990

Initial investment (150000)

Net Present value 21990

From the above calculation of net present value of both projects it can be stated that, top level

management of Magical Mystery Tours Ltd should consider Project A for the future investment because

it is showing higher results as compared to Project B. However, Net present value of project A is 44915

as compared to project B 21990. Therefore, calculation clearly illustrates that project A is more feasible

in terms of investment as by the means of this Magical Mystery Tours Ltd will generate higher returns

maintain its position in such competitive market.

Henceforth, from the above computation of all the investment appraisal techniques it can be

recommended that, project A is more feasible for Magical Mystery Tours Ltd to invest in as it is

showing higher return than project B when compared.

TASK 3

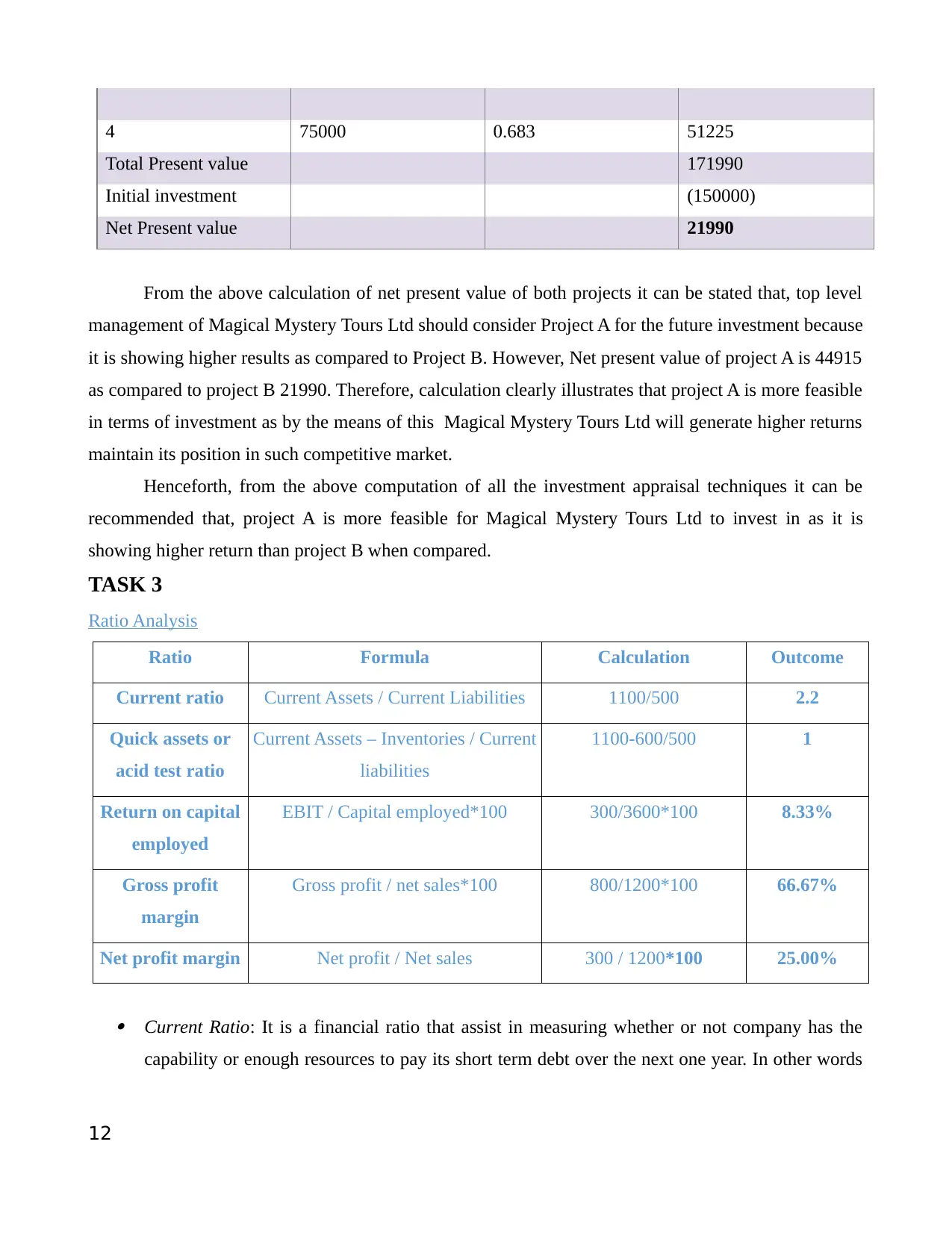

Ratio Analysis

Ratio Formula Calculation Outcome

Current ratio Current Assets / Current Liabilities 1100/500 2.2

Quick assets or

acid test ratio

Current Assets – Inventories / Current

liabilities

1100-600/500 1

Return on capital

employed

EBIT / Capital employed*100 300/3600*100 8.33%

Gross profit

margin

Gross profit / net sales*100 800/1200*100 66.67%

Net profit margin Net profit / Net sales 300 / 1200*100 25.00%

Current Ratio: It is a financial ratio that assist in measuring whether or not company has the

capability or enough resources to pay its short term debt over the next one year. In other words

12

Total Present value 171990

Initial investment (150000)

Net Present value 21990

From the above calculation of net present value of both projects it can be stated that, top level

management of Magical Mystery Tours Ltd should consider Project A for the future investment because

it is showing higher results as compared to Project B. However, Net present value of project A is 44915

as compared to project B 21990. Therefore, calculation clearly illustrates that project A is more feasible

in terms of investment as by the means of this Magical Mystery Tours Ltd will generate higher returns

maintain its position in such competitive market.

Henceforth, from the above computation of all the investment appraisal techniques it can be

recommended that, project A is more feasible for Magical Mystery Tours Ltd to invest in as it is

showing higher return than project B when compared.

TASK 3

Ratio Analysis

Ratio Formula Calculation Outcome

Current ratio Current Assets / Current Liabilities 1100/500 2.2

Quick assets or

acid test ratio

Current Assets – Inventories / Current

liabilities

1100-600/500 1

Return on capital

employed

EBIT / Capital employed*100 300/3600*100 8.33%

Gross profit

margin

Gross profit / net sales*100 800/1200*100 66.67%

Net profit margin Net profit / Net sales 300 / 1200*100 25.00%

Current Ratio: It is a financial ratio that assist in measuring whether or not company has the

capability or enough resources to pay its short term debt over the next one year. In other words

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.