FINM008 - Corporate Reporting Analysis: Travis Perkins Annual Report

VerifiedAdded on 2022/08/27

|13

|2817

|31

Report

AI Summary

This report provides a detailed analysis of Travis Perkins' 2018 annual report, focusing on several key areas. It begins by examining the company's compliance with International Financial Reporting Standards (IFRS), specifically IFRS 9, IFRS 15, and IFRS 16, detailing their impact on the financial statements. The report then assesses Travis Perkins' financial performance and health, utilizing ratio analysis to evaluate liquidity, leverage, and profitability, comparing figures from 2017 and 2018 to identify trends and draw conclusions. A critical discussion of accounting standards, including Generally Accepted Accounting Principles (GAAP) and IFRS, is presented, emphasizing their roles in financial reporting. Finally, the report explores the significance of segmental analysis in providing insights into the financial results of Travis Perkins' operating units, highlighting its importance for stakeholders. The report concludes with an overall assessment of the company's financial position and performance based on the analysis conducted.

Running head: CORPORATE REPORTING 1

Corporate reporting 1

Name of the student

Name of the university

Student ID

Author note

Corporate reporting 1

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE REPORTING 1

Table of Contents

Introduction......................................................................................................................................2

1. Compliance with IFRS.............................................................................................................2

2. Comment on financial performance and financial health........................................................5

3. Accounting standards for financial reporting...........................................................................8

4. Significance of segmental analysis...........................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

1. Compliance with IFRS.............................................................................................................2

2. Comment on financial performance and financial health........................................................5

3. Accounting standards for financial reporting...........................................................................8

4. Significance of segmental analysis...........................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

2CORPORATE REPORTING 1

Introduction

Travis Perkins is largest distributor in UK for building materials for construction of

building as well as home improvement market. It operates through various segments namely

plumbing and heating, general merchanting, consumers and contracts. Various items the entity

deals with are timber, doors, joinery and windows, building materials, plumbing, gardens and

landscaping, heating, tool hire, clearance, electrical and lighting and trade offers. Purpose of the

task is conducting detailed analysis that focuses on how financial statement of the entity

demonstrates the compliance with IFRSs (Travis Perkins | Builders Merchants, Building

Supplies & Material 2020). The report will further use the analytical techniques and tools for

providing comments on the financial health as well as financial performance of the entity as

against the previous year. In addition, it will critically discuss the requirement and role for

national as well as IAS while preparing the corporate financial reporting. Finally, the report will

discuss significance of data delivered under segmental analysis of financial report and the reason

why the same disclosure is required for the entity.

1. Compliance with IFRS

IFRS 9 – Financial instruments

Reclassifications as well as adjustments on account of new impairment rules are not

reported under restated balance sheet as at 31st December 2017. However, the same has been

reported under closing balance sheet dated 31st December 2018 for the alterations in the financial

assets of the group for impairment required by IFRS 9 have been reported under opening balance

sheet as at 1st January 2018. IFRS 9 substituted provision of IAS 39 that is associated with

measurement, classification and recognition of financial asset as well as financial liabilities,

Introduction

Travis Perkins is largest distributor in UK for building materials for construction of

building as well as home improvement market. It operates through various segments namely

plumbing and heating, general merchanting, consumers and contracts. Various items the entity

deals with are timber, doors, joinery and windows, building materials, plumbing, gardens and

landscaping, heating, tool hire, clearance, electrical and lighting and trade offers. Purpose of the

task is conducting detailed analysis that focuses on how financial statement of the entity

demonstrates the compliance with IFRSs (Travis Perkins | Builders Merchants, Building

Supplies & Material 2020). The report will further use the analytical techniques and tools for

providing comments on the financial health as well as financial performance of the entity as

against the previous year. In addition, it will critically discuss the requirement and role for

national as well as IAS while preparing the corporate financial reporting. Finally, the report will

discuss significance of data delivered under segmental analysis of financial report and the reason

why the same disclosure is required for the entity.

1. Compliance with IFRS

IFRS 9 – Financial instruments

Reclassifications as well as adjustments on account of new impairment rules are not

reported under restated balance sheet as at 31st December 2017. However, the same has been

reported under closing balance sheet dated 31st December 2018 for the alterations in the financial

assets of the group for impairment required by IFRS 9 have been reported under opening balance

sheet as at 1st January 2018. IFRS 9 substituted provision of IAS 39 that is associated with

measurement, classification and recognition of financial asset as well as financial liabilities,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE REPORTING 1

impairment of the financial assets, de-recognition of the financial assets as well as hedge

accounting. Adoption of the IFRS 9 since 1st January 2018 led to changes in the accounting

policies as well as adjustments for the amounts reported under financial statements. However, for

the transitional provision of IFRS 9 the entity did no restate the comparative figures (Travis

Perkins | Builders Merchants, Building Supplies & Material 2020).

IFRS 15 – Revenue from the contracts with customers

The entity adopted IFRS 15 since 1st January 2018that resulted in alterations in the

accounting policies as well as reclassification of the recognised amounts under financial

statements. However, none of the adjustments had its effect on retained earnings of the group

and this standard does not have notable impact on the entity. Further, previously the provisions

for the customers returns were used to be presented on the net basis as the part of deferred and

accrual income. Since the adoption of IFRS 15 the same are presented on gross basis whereas the

liabilities for entire amount likely to be repaid are added under trade and other receivables

(Travis Perkins | Builders Merchants, Building Supplies & Material 2020).

IFRS 16 – Leases

IFRS 16 was released by IASB in January and the same was endorsed by EU in 2017

October. It has material impact on the entity as value for operating lease entered by the entity

will be reported in the balance sheet in future period. The entity has one project team that works

for implementing procedures as well as systems required for complying with the requirements.

Effect of adopting standard on 1st January 2019 may alter the present estimates as the lease

portfolio of the entity is changing frequently and new accounting policies are tend to alter until

the entity presents the 1st financial statement that involve date for initial application. Exemption

impairment of the financial assets, de-recognition of the financial assets as well as hedge

accounting. Adoption of the IFRS 9 since 1st January 2018 led to changes in the accounting

policies as well as adjustments for the amounts reported under financial statements. However, for

the transitional provision of IFRS 9 the entity did no restate the comparative figures (Travis

Perkins | Builders Merchants, Building Supplies & Material 2020).

IFRS 15 – Revenue from the contracts with customers

The entity adopted IFRS 15 since 1st January 2018that resulted in alterations in the

accounting policies as well as reclassification of the recognised amounts under financial

statements. However, none of the adjustments had its effect on retained earnings of the group

and this standard does not have notable impact on the entity. Further, previously the provisions

for the customers returns were used to be presented on the net basis as the part of deferred and

accrual income. Since the adoption of IFRS 15 the same are presented on gross basis whereas the

liabilities for entire amount likely to be repaid are added under trade and other receivables

(Travis Perkins | Builders Merchants, Building Supplies & Material 2020).

IFRS 16 – Leases

IFRS 16 was released by IASB in January and the same was endorsed by EU in 2017

October. It has material impact on the entity as value for operating lease entered by the entity

will be reported in the balance sheet in future period. The entity has one project team that works

for implementing procedures as well as systems required for complying with the requirements.

Effect of adopting standard on 1st January 2019 may alter the present estimates as the lease

portfolio of the entity is changing frequently and new accounting policies are tend to alter until

the entity presents the 1st financial statement that involve date for initial application. Exemption

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE REPORTING 1

for elective recognition is there for the short term leases and for the leases with low value items.

However, the accounting for lessor remains same with the current standards. Lessor will classify

the leases as operating lease or finance lease (Travis Perkins | Builders Merchants, Building

Supplies & Material 2020).

for elective recognition is there for the short term leases and for the leases with low value items.

However, the accounting for lessor remains same with the current standards. Lessor will classify

the leases as operating lease or finance lease (Travis Perkins | Builders Merchants, Building

Supplies & Material 2020).

5CORPORATE REPORTING 1

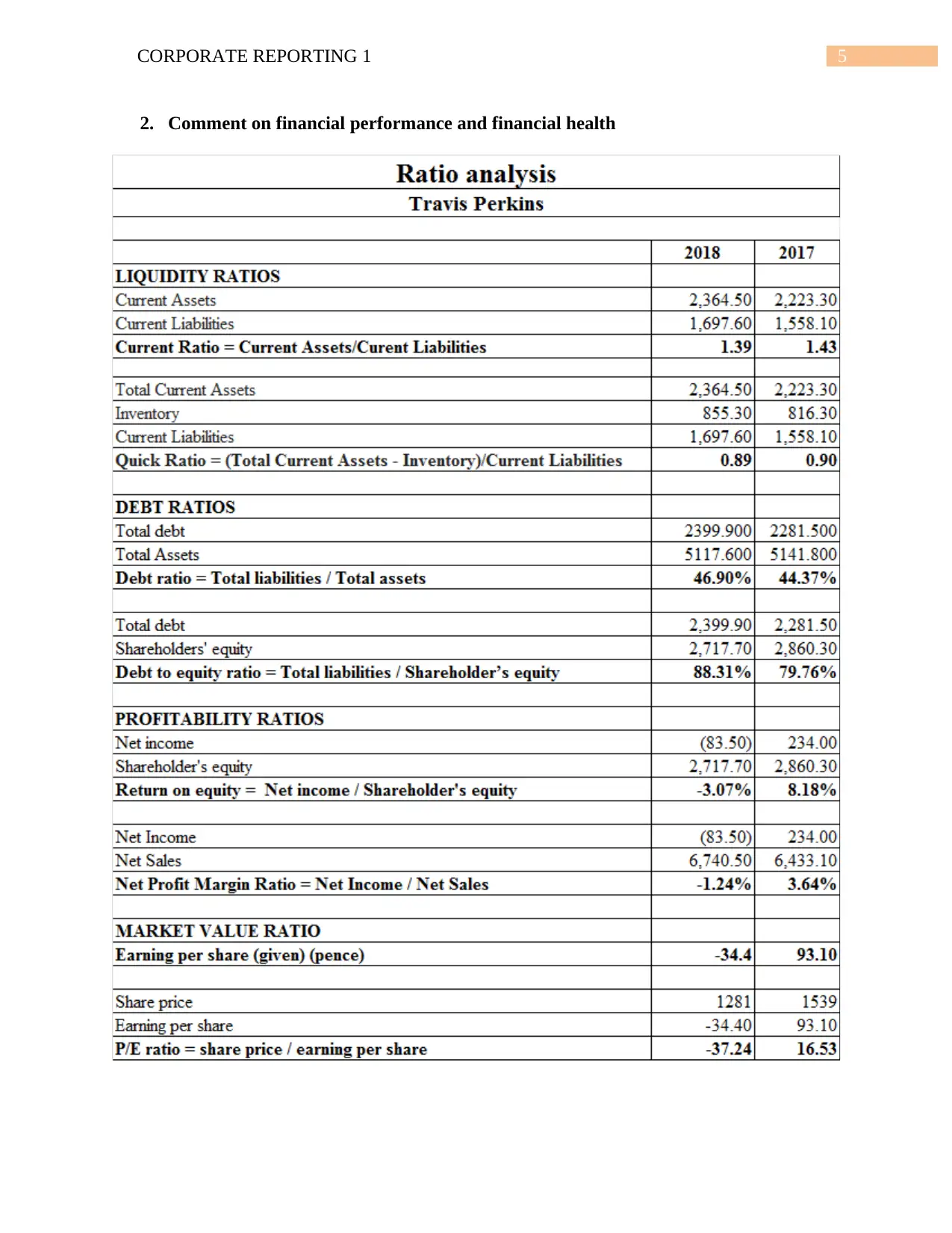

2. Comment on financial performance and financial health

2. Comment on financial performance and financial health

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE REPORTING 1

Financial statements offer information those are significantly useful in context of the

financial performance based on the structure of liabilities, assets, equities, income and expenses.

Hence, financial statement offers summarized view in context of the entity’s financial position.

Ratio analysis is used on wide basis for analysing the financial performance and can be applied

for comparing the risks as well as returns association for the entities of different sizes (Faello

2015).

Liquidity ratio – it is notably important as sufficient liquidity is crucial for any firm to meet the

short term obligation while they become due for the purpose of payment. In other sense, liquidity

is pre-requisite for any firm’s survival. Liquidity status implies from viewpoint of using the

firm’s fund. Major liquidity ratios considered for measuring the liquidity are current ratio and

quick ratio. The current ratio measures total current assets against the total current liabilities and

is computed through dividing the current assets by the current liabilities. If the current ratio of

the entity is more than 2 it is considered to be adequately liquid (Arkan 2016). On the other hand,

quick ratio measures the quick assets against the current liabilities. Here, only the liquid asset

that is assets those are readily convertible into cash are considered. If the quick ratio of the entity

is more than 1 it is considered to be adequately liquid. It can be identified from the data provided

in the balance sheet of the entity that current ratio for both the years are less than 2 and quick

ratio for both the years are less than 1. Further, both the ratios in 2018 have been reduced as

compared to the preceding year. Hence, it can be stated that the liquidity status of the entity has

been deteriorated (Boyas and Teeter 2017)

Leverage ratios – long term creditors as well as lenders judge the firm’s soundness on the basis

of long term financial strength that is measured through the proportion of debt raised by the

entity as against proportion of equity. Debt ratio is the solvency ratio used for measuring total

Financial statements offer information those are significantly useful in context of the

financial performance based on the structure of liabilities, assets, equities, income and expenses.

Hence, financial statement offers summarized view in context of the entity’s financial position.

Ratio analysis is used on wide basis for analysing the financial performance and can be applied

for comparing the risks as well as returns association for the entities of different sizes (Faello

2015).

Liquidity ratio – it is notably important as sufficient liquidity is crucial for any firm to meet the

short term obligation while they become due for the purpose of payment. In other sense, liquidity

is pre-requisite for any firm’s survival. Liquidity status implies from viewpoint of using the

firm’s fund. Major liquidity ratios considered for measuring the liquidity are current ratio and

quick ratio. The current ratio measures total current assets against the total current liabilities and

is computed through dividing the current assets by the current liabilities. If the current ratio of

the entity is more than 2 it is considered to be adequately liquid (Arkan 2016). On the other hand,

quick ratio measures the quick assets against the current liabilities. Here, only the liquid asset

that is assets those are readily convertible into cash are considered. If the quick ratio of the entity

is more than 1 it is considered to be adequately liquid. It can be identified from the data provided

in the balance sheet of the entity that current ratio for both the years are less than 2 and quick

ratio for both the years are less than 1. Further, both the ratios in 2018 have been reduced as

compared to the preceding year. Hence, it can be stated that the liquidity status of the entity has

been deteriorated (Boyas and Teeter 2017)

Leverage ratios – long term creditors as well as lenders judge the firm’s soundness on the basis

of long term financial strength that is measured through the proportion of debt raised by the

entity as against proportion of equity. Debt ratio is the solvency ratio used for measuring total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE REPORTING 1

liabilities of the entity as a percentage of total assets. It represents the ability of the entity in

paying off the liabilities with the help of assets. It assists the creditors as well as investors to

analyse overall debt burden on entity along with the ability of the firm to make the payment of

debt in the future period or during economic downtimes (Williams and Dobelman 2017). Lower

debt ratio is preferable as the lower ratio signifies that the entity is solvent. On the other hand,

debt to equity ratio compares the total debt of the entity against total equity. It further reveals the

proportion of financing for the entity that has been received from investors and creditors. Higher

debt to equity ratio signifies that the company is highly leveraged. Debt ratio of the entity though

is increased from 44.37% to 46.90% and debt to equity ratio has been increased from 79.76% to

88.31% over the years from 2017 to 2018 both these ratios are representing that the entity is

lower leveraged and major portion of the capital is raised through equity (Travis Perkins |

Builders Merchants, Building Supplies & Material 2020).

Profitability ratio – it measures profitability which in turn helps in measuring the entity’s

performance. It is simply the ability of the entity to earn profit that is the amount left over from

the earnings made by the entity after making all the deduction for the business expenses. ROE

offers the investors with the insight regarding the efficiency with which the entity managing

money contributed by the shareholders. It is generally used for comparing the entity with the

competitors and with overall market (Oshoke and Sumaina 2015). As the net earnings of the

entity for 2018 was in negative, ROE for the same year was also negative 3.07% as against

8.18% in 2017. On the other hand, net profit margin is the revenue proportion remaining after

payment of all the expenses made. It reveals profit amount that can be extracted by a business

from total revenue. As the net earnings for the year 2018 is in negative, net profit margin for the

liabilities of the entity as a percentage of total assets. It represents the ability of the entity in

paying off the liabilities with the help of assets. It assists the creditors as well as investors to

analyse overall debt burden on entity along with the ability of the firm to make the payment of

debt in the future period or during economic downtimes (Williams and Dobelman 2017). Lower

debt ratio is preferable as the lower ratio signifies that the entity is solvent. On the other hand,

debt to equity ratio compares the total debt of the entity against total equity. It further reveals the

proportion of financing for the entity that has been received from investors and creditors. Higher

debt to equity ratio signifies that the company is highly leveraged. Debt ratio of the entity though

is increased from 44.37% to 46.90% and debt to equity ratio has been increased from 79.76% to

88.31% over the years from 2017 to 2018 both these ratios are representing that the entity is

lower leveraged and major portion of the capital is raised through equity (Travis Perkins |

Builders Merchants, Building Supplies & Material 2020).

Profitability ratio – it measures profitability which in turn helps in measuring the entity’s

performance. It is simply the ability of the entity to earn profit that is the amount left over from

the earnings made by the entity after making all the deduction for the business expenses. ROE

offers the investors with the insight regarding the efficiency with which the entity managing

money contributed by the shareholders. It is generally used for comparing the entity with the

competitors and with overall market (Oshoke and Sumaina 2015). As the net earnings of the

entity for 2018 was in negative, ROE for the same year was also negative 3.07% as against

8.18% in 2017. On the other hand, net profit margin is the revenue proportion remaining after

payment of all the expenses made. It reveals profit amount that can be extracted by a business

from total revenue. As the net earnings for the year 2018 is in negative, net profit margin for the

8CORPORATE REPORTING 1

same year was also negative 1.24% as against 3,64% in 2017 (Travis Perkins | Builders

Merchants, Building Supplies & Material 2020).

Market value ratio – these ratios are applied for evaluation current share price of any publicly

held entity. These ratios are utilised by the existing as well as potential investors for defining

whether the share price of the entity is under-priced or over-priced. Most widely used market

value ratios are price earnings ratios and earning per share. EPS is the profit available with the

entity for its shareholders divide by the number of shares outstanding. On account of negative

bottom line profit the EPS for the year 2018 is negative 34.4 pence against 93.10 pence for 2017

(Kanapickienė and Grundienė 2015). On the other hand, PE ratio is used to compare market

price of the entity’s stock against the EPS. High PE ratio indicates that the investors will be in

view that the share price of the entity will go up whereas low PE ratios designates that the share

price will come down. Negative PE ratio of 37.24 in 2018 against 16.53 in 2017 is signifying that

the investors will think that the entity’s share price will come down in future (Ping-fu and Kwai-

yee 2016).

3. Accounting standards for financial reporting

Accounting standard developed as well as established by standard setting bodies to

determine the manner in which the financial statements are prepared as well as presented.

Collectively these standards are known as GAAP (generally accepted accounting standards). It

is based on the established objectives, concepts, convention sand standards those are evolved

over the time for guiding how the financial statements are prepared as well as presented. GAAP

is set with the purpose of delivering useful information to users including lenders, investors or

those who offer resources to profit seeking concern or the non-profit entities (Bentley et al.

2016). Lenders, investors and other users are dependent on the GAAP based financial reporting

same year was also negative 1.24% as against 3,64% in 2017 (Travis Perkins | Builders

Merchants, Building Supplies & Material 2020).

Market value ratio – these ratios are applied for evaluation current share price of any publicly

held entity. These ratios are utilised by the existing as well as potential investors for defining

whether the share price of the entity is under-priced or over-priced. Most widely used market

value ratios are price earnings ratios and earning per share. EPS is the profit available with the

entity for its shareholders divide by the number of shares outstanding. On account of negative

bottom line profit the EPS for the year 2018 is negative 34.4 pence against 93.10 pence for 2017

(Kanapickienė and Grundienė 2015). On the other hand, PE ratio is used to compare market

price of the entity’s stock against the EPS. High PE ratio indicates that the investors will be in

view that the share price of the entity will go up whereas low PE ratios designates that the share

price will come down. Negative PE ratio of 37.24 in 2018 against 16.53 in 2017 is signifying that

the investors will think that the entity’s share price will come down in future (Ping-fu and Kwai-

yee 2016).

3. Accounting standards for financial reporting

Accounting standard developed as well as established by standard setting bodies to

determine the manner in which the financial statements are prepared as well as presented.

Collectively these standards are known as GAAP (generally accepted accounting standards). It

is based on the established objectives, concepts, convention sand standards those are evolved

over the time for guiding how the financial statements are prepared as well as presented. GAAP

is set with the purpose of delivering useful information to users including lenders, investors or

those who offer resources to profit seeking concern or the non-profit entities (Bentley et al.

2016). Lenders, investors and other users are dependent on the GAAP based financial reporting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE REPORTING 1

for taking decisions regarding how to assign the capital and assisting financial markets in

efficient operating. At the time of establishing GAAP standard setters were majorly concerned

regarding the users of financial statements including lenders, potential as well as existing

investors those analyze the financial statements for taking investment related decisions.

Standards setters prefer making consistent standards for assisting end users in understanding as

well as using the financial data of the entity. Primary intention of GAAP is not assisting the

businesses but to assist the users (Isidro and Marques 2015).

IFRS set common rules for the financial statements for making the same transparent,

comparable and consistent all over the world. It was issued by IASB and it specifies the manner

in which the entities shall maintain as well as report the accounts, provides explanation regarding

various types of transactions along with various other events with the financial impact. It was

established for creating common accounting language that will in turn allow the businesses as

well as financial statements to be consistent as well as reliable from entity to entity and from

country to country (Cascino and Gassen 2015)

4. Significance of segmental analysis

Main purpose of segment reporting is delivering information to the creditors as well as

investors in context of financial results as well as position of most crucial operating units of the

entity. Segment reporting can be used as basis for making decisions associated with the entity.

Major advantage of the segment reporting is it provides transparency. Investors, analysts as well

as other stakeholders require information for analysing growth and sustainability of the entity

and monitoring performance of the management (Bugeja, Czernkowski and Moran 2015). From

the annual report of Travis Perkins it can be found out that the entity operates through different

segments including Merchanting, Retail, Plumbing & heating and Toolstation. Hence, segment

for taking decisions regarding how to assign the capital and assisting financial markets in

efficient operating. At the time of establishing GAAP standard setters were majorly concerned

regarding the users of financial statements including lenders, potential as well as existing

investors those analyze the financial statements for taking investment related decisions.

Standards setters prefer making consistent standards for assisting end users in understanding as

well as using the financial data of the entity. Primary intention of GAAP is not assisting the

businesses but to assist the users (Isidro and Marques 2015).

IFRS set common rules for the financial statements for making the same transparent,

comparable and consistent all over the world. It was issued by IASB and it specifies the manner

in which the entities shall maintain as well as report the accounts, provides explanation regarding

various types of transactions along with various other events with the financial impact. It was

established for creating common accounting language that will in turn allow the businesses as

well as financial statements to be consistent as well as reliable from entity to entity and from

country to country (Cascino and Gassen 2015)

4. Significance of segmental analysis

Main purpose of segment reporting is delivering information to the creditors as well as

investors in context of financial results as well as position of most crucial operating units of the

entity. Segment reporting can be used as basis for making decisions associated with the entity.

Major advantage of the segment reporting is it provides transparency. Investors, analysts as well

as other stakeholders require information for analysing growth and sustainability of the entity

and monitoring performance of the management (Bugeja, Czernkowski and Moran 2015). From

the annual report of Travis Perkins it can be found out that the entity operates through different

segments including Merchanting, Retail, Plumbing & heating and Toolstation. Hence, segment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE REPORTING 1

reporting will assist the entity breaking the financial data of the entity by segments. It will further

deliver accurate picture of the entity’s performance to the shareholders. Further, it will help the

management in evaluating the assets, liabilities, incomes and expenses segment wise (Zimnicki

2016).

Conclusion

From above it is established that the financial performance of the entity has been

deteriorated in 2018 as compared to the preceding year 2017. It can be determined through the

fact that liquidity ratios, profitability ratios, leverage ratios and market value ratios have been

dropped in 2018 as against 2017. National as well as international accounting standards deliver

useful information to users including lenders, investors or those who offer resources to profit

seeking concern or the non-profit entities. Segment reporting will assist Travis Perkins in

breaking the financial data of the entity by segments.

reporting will assist the entity breaking the financial data of the entity by segments. It will further

deliver accurate picture of the entity’s performance to the shareholders. Further, it will help the

management in evaluating the assets, liabilities, incomes and expenses segment wise (Zimnicki

2016).

Conclusion

From above it is established that the financial performance of the entity has been

deteriorated in 2018 as compared to the preceding year 2017. It can be determined through the

fact that liquidity ratios, profitability ratios, leverage ratios and market value ratios have been

dropped in 2018 as against 2017. National as well as international accounting standards deliver

useful information to users including lenders, investors or those who offer resources to profit

seeking concern or the non-profit entities. Segment reporting will assist Travis Perkins in

breaking the financial data of the entity by segments.

11CORPORATE REPORTING 1

Reference

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), pp.13-26.

Bentley, J.W., Christensen, T.E., Gee, K.H. and Whipple, B.C., 2018. Disentangling managers’

and analysts’ non‐GAAP reporting. Journal of Accounting Research, 56(4), pp.1039-1081.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

Bugeja, M., Czernkowski, R. and Moran, D., 2015. The impact of the management approach on

segment reporting. Journal of Business Finance & Accounting, 42(3-4), pp.310-366.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Faello, J., 2015. Understanding the limitations of financial ratios. Academy of Accounting and

Financial Studies Journal, 19(3), p.75.

Isidro, H. and Marques, A., 2015. The role of institutional and economic factors in the strategic

use of non-GAAP disclosures to beat earnings benchmarks. European Accounting Review, 24(1),

pp.95-128.

Kanapickienė, R. and Grundienė, Ž., 2015. The model of fraud detection in financial statements

by means of financial ratios. Procedia-Social and Behavioral Sciences, 213, pp.321-327.

Reference

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), pp.13-26.

Bentley, J.W., Christensen, T.E., Gee, K.H. and Whipple, B.C., 2018. Disentangling managers’

and analysts’ non‐GAAP reporting. Journal of Accounting Research, 56(4), pp.1039-1081.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

Bugeja, M., Czernkowski, R. and Moran, D., 2015. The impact of the management approach on

segment reporting. Journal of Business Finance & Accounting, 42(3-4), pp.310-366.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Faello, J., 2015. Understanding the limitations of financial ratios. Academy of Accounting and

Financial Studies Journal, 19(3), p.75.

Isidro, H. and Marques, A., 2015. The role of institutional and economic factors in the strategic

use of non-GAAP disclosures to beat earnings benchmarks. European Accounting Review, 24(1),

pp.95-128.

Kanapickienė, R. and Grundienė, Ž., 2015. The model of fraud detection in financial statements

by means of financial ratios. Procedia-Social and Behavioral Sciences, 213, pp.321-327.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.