Treasury and Risk Management: SNB De-pegging and Hedging Strategies

VerifiedAdded on 2021/04/24

|9

|1788

|60

Report

AI Summary

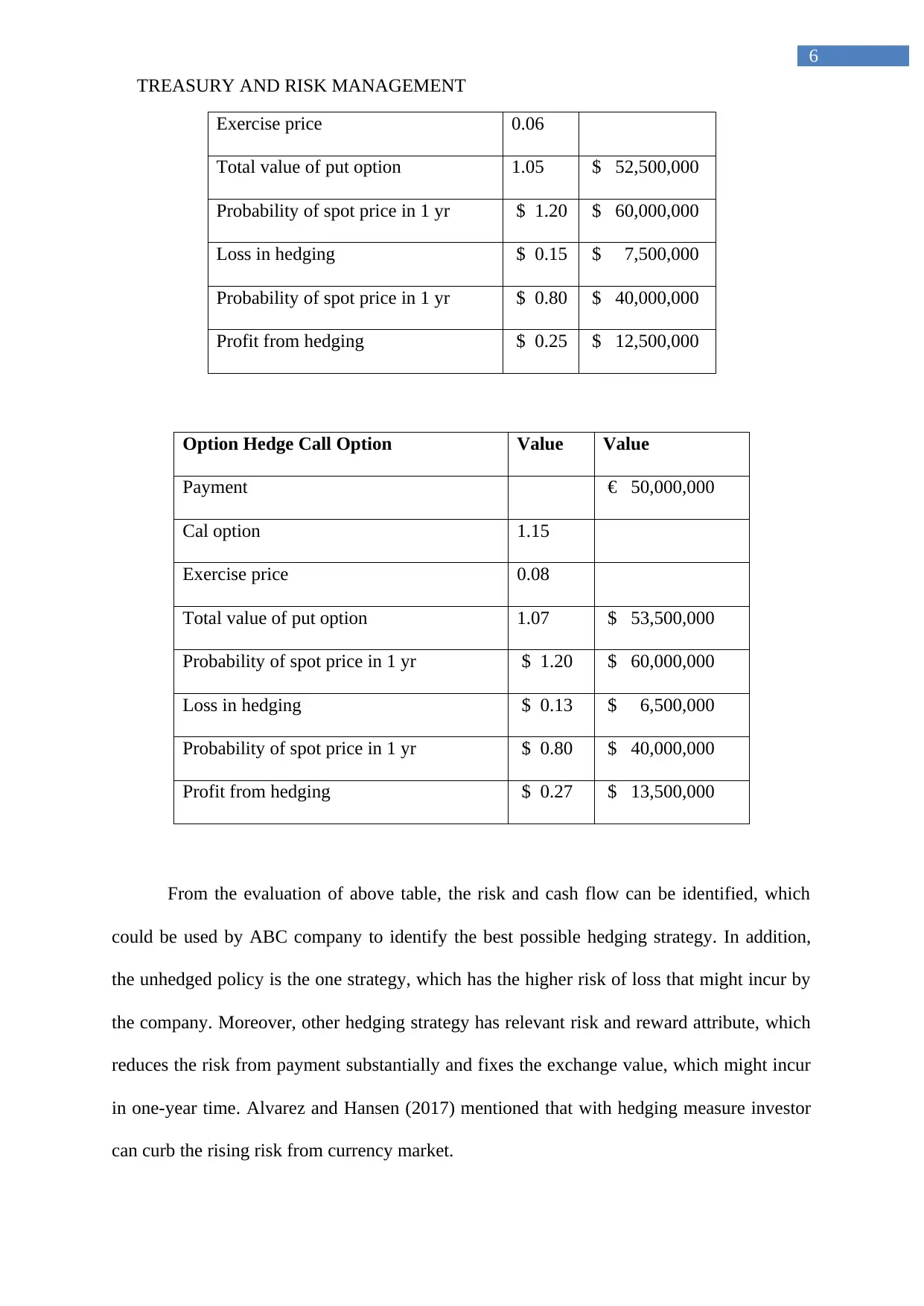

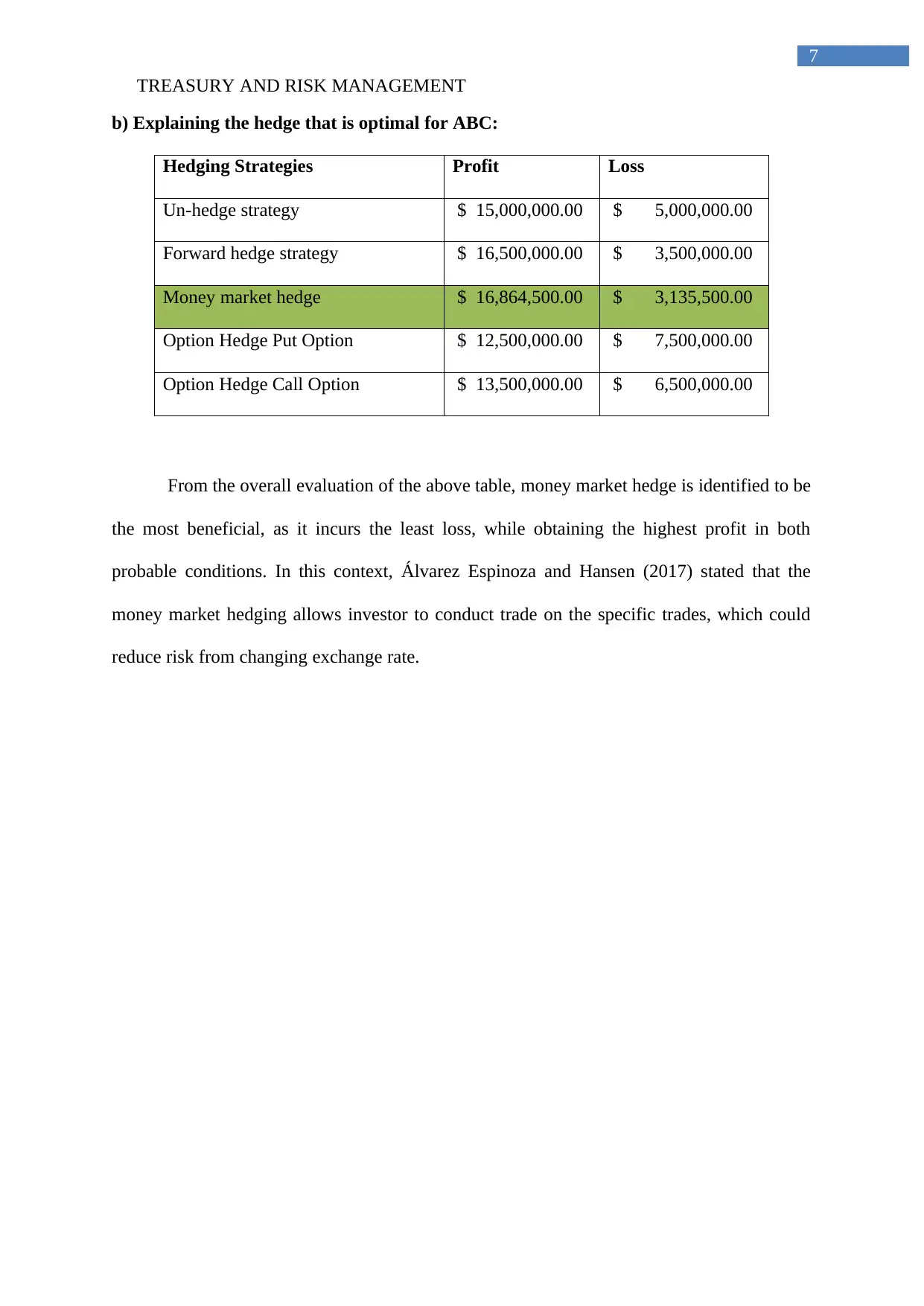

This report provides a comprehensive analysis of treasury and risk management, focusing on the Swiss National Bank's (SNB) decision to de-peg the Swiss Franc from the Euro in January 2011. The report delves into the reasons behind the SNB's action, including the accumulation of Euro and foreign currency reserves, and the devaluation of the Euro. It then evaluates various hedging strategies employed by Swiss exporters to mitigate currency risk, including unhedged strategies, forward hedges, money market hedges, and option hedges (both put and call options). The report calculates potential dollar cash flows for each strategy under different spot price scenarios, identifies the risks associated with each approach, and ultimately recommends the optimal hedging strategy for a hypothetical company, ABC. The analysis highlights the benefits and drawbacks of each method, with a money market hedge being identified as the most beneficial approach due to its potential for minimizing losses and maximizing profits under various market conditions. References and bibliography are included.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.