Corporate Accounting Report: Treasury Wine Estates Financial Analysis

VerifiedAdded on 2020/05/16

|11

|2056

|76

Report

AI Summary

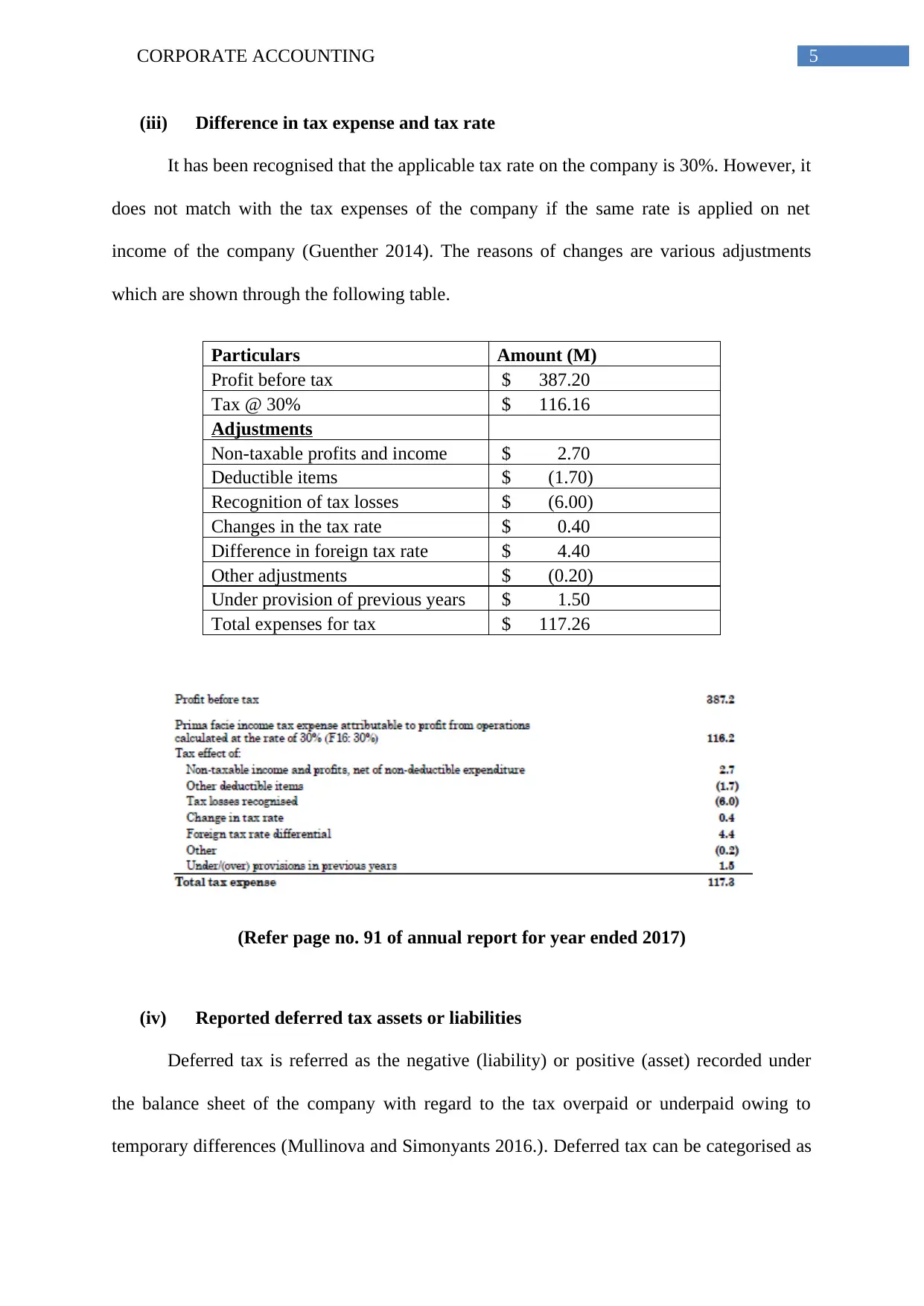

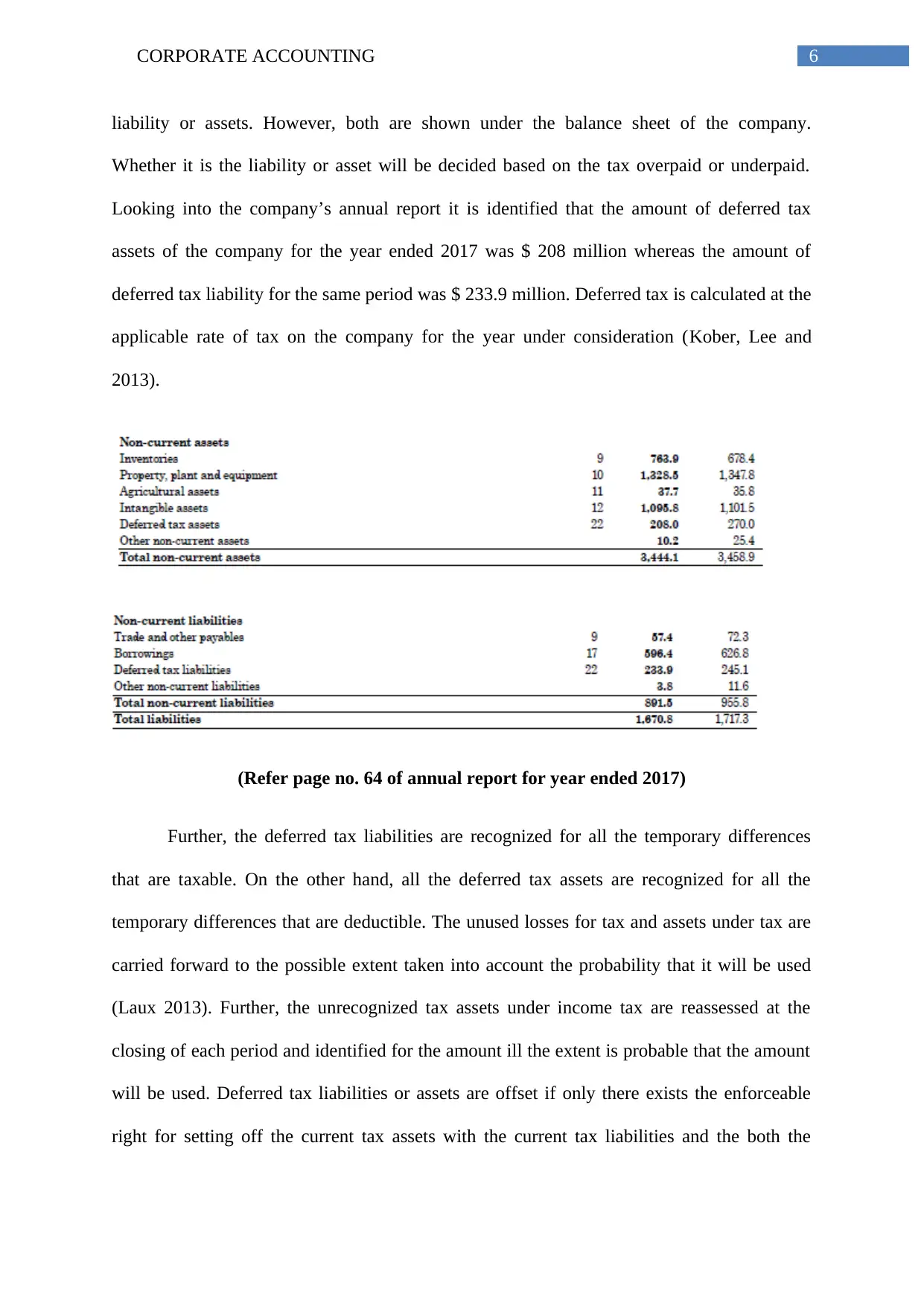

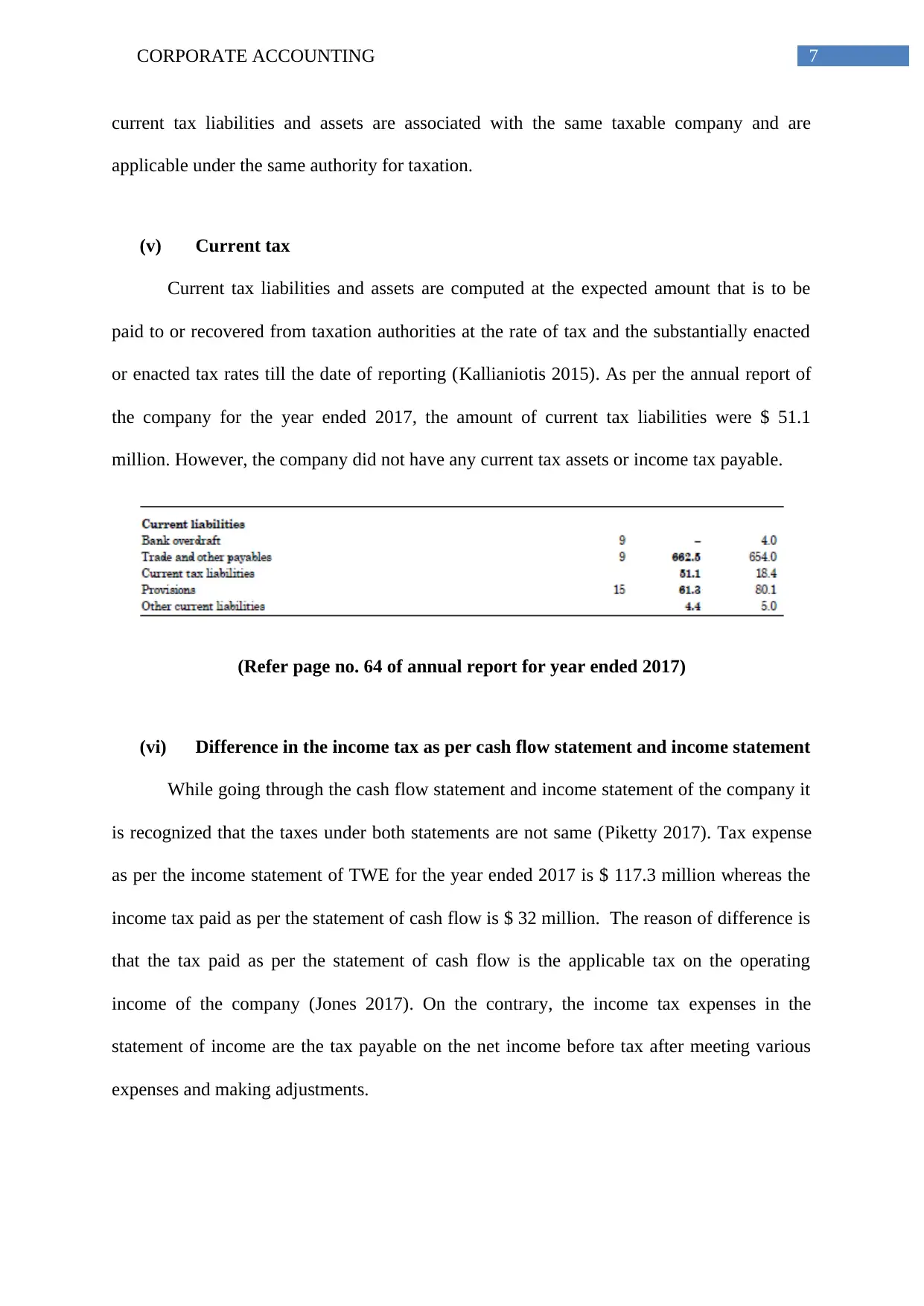

This report provides a comprehensive analysis of the corporate accounting practices of Treasury Wine Estates (TWE). It examines key equity items such as contributed equity, reserves, and retained earnings, detailing the reasons for changes in these items. The report further explores tax expenses, comparing the tax expense to the applicable tax rate and identifying the adjustments causing the difference. It delves into the treatment of deferred tax assets and liabilities, current tax liabilities, and the differences between income tax reported in the cash flow statement and the income statement. The analysis highlights the complexities of deferred tax recognition and the uncertainties in determining the final tax liability. The report concludes with new insights gained from analyzing TWE's financial statements, emphasizing the impact of calculations, adjustments, and transactions on tax provisions.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.